Size and Share of AI Software Market In Legal Industry

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

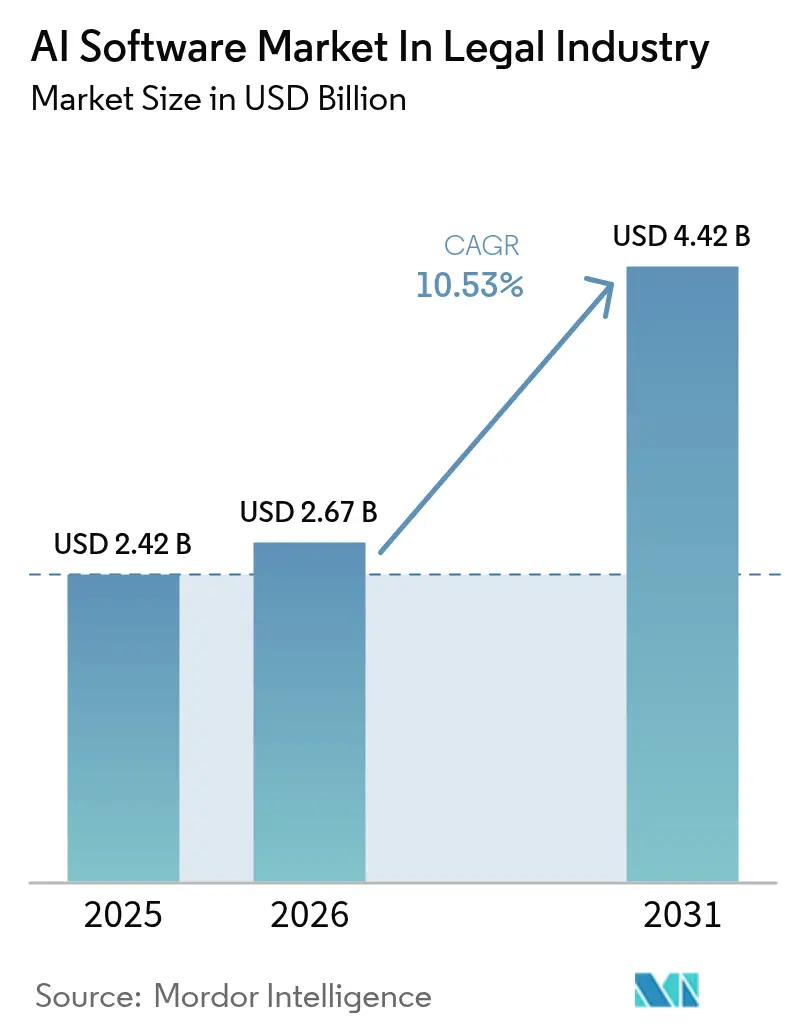

| Market Size (2026) | USD 2.67 Billion |

| Market Size (2031) | USD 4.42 Billion |

| Growth Rate (2026 - 2031) | 10.53% CAGR |

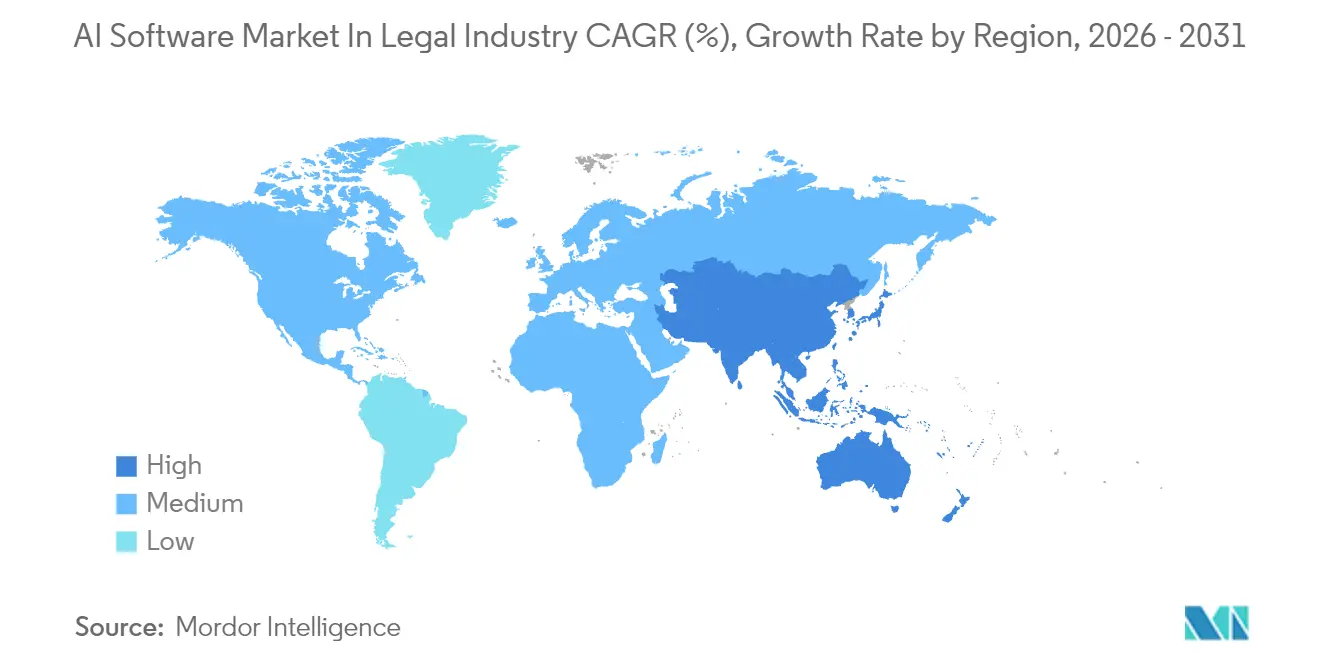

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of AI Software Market In Legal Industry by Mordor Intelligence

The AI software market size in legal industry market size in 2026 is estimated at USD 2.67 billion, growing from 2025 value of USD 2.42 billion with 2031 projections showing USD 4.42 billion, growing at 10.53% CAGR over 2026-2031. This growth profile underscores how automation, generative AI breakthroughs, and mounting fee-pressure are redefining legal workflows. Rapid adoption of cloud-hosted generative AI tools, rising litigation volumes, and talent scarcity are pushing firms to embed intelligent systems in research, e-discovery, and contract workflows. Meanwhile, heightened regulatory scrutiny around model transparency and client confidentiality is guiding purchasing criteria toward explainable, compliance-ready platforms. Venture investors continue to fuel innovation, yet competitive intensity is rising as long-established legal-information vendors race to integrate large language models and defend share against AI-native entrants. Finally, regional dynamics point to North American scale advantages and Asia Pacific’s policy-supported acceleration, setting a global agenda that favors providers able to balance speed with governance.

Key Report Takeaways

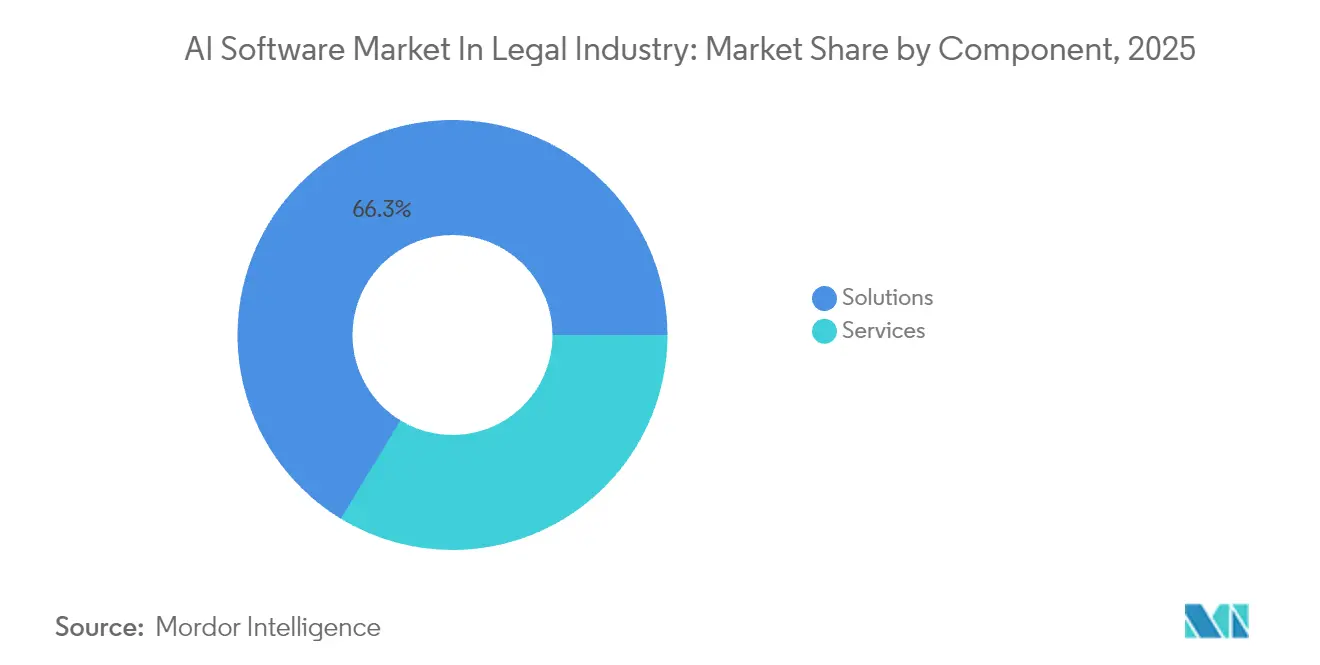

- By component, Solutions led with 66.30% of the AI software market share in 2025; Services are advancing at a 12.32% CAGR to 2031.

- By deployment, cloud platforms captured 73.20% of the AI software market size in 2025 and are growing at a 12.10% CAGR through 2031.

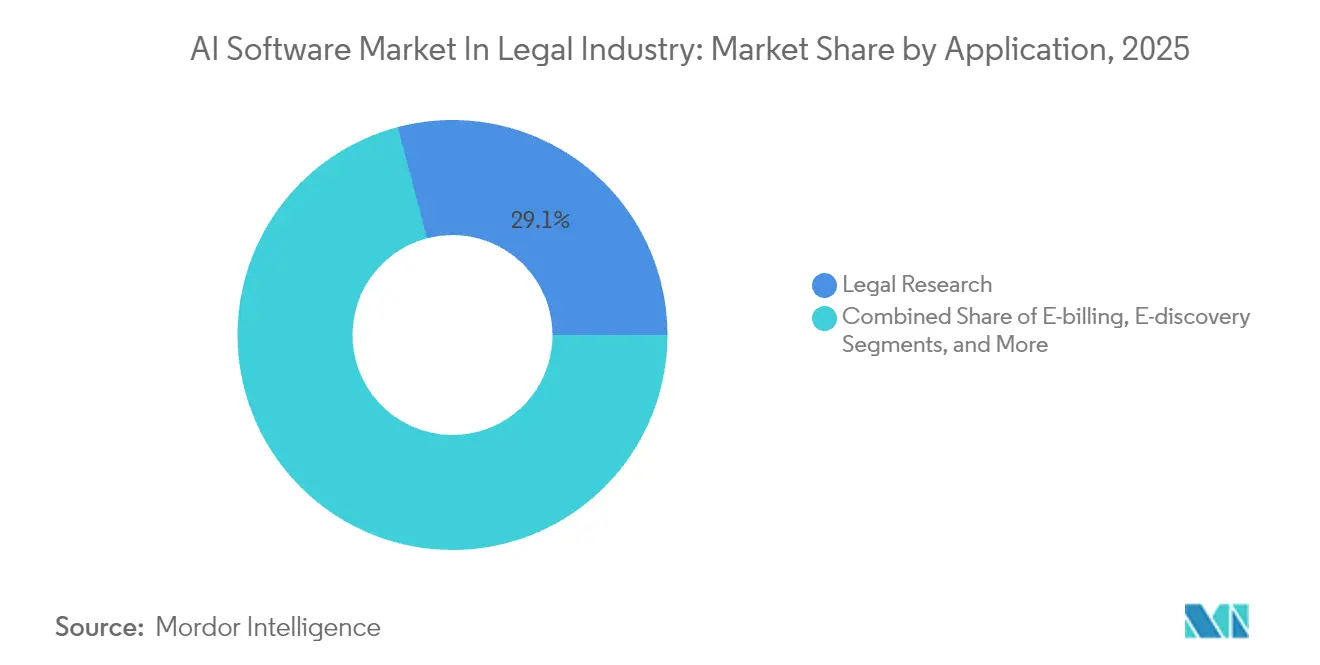

- By application, Legal Research accounted for 29.10% of the AI software market size in 2025; Case Prediction is expanding at an 11.07% CAGR to 2031.

- By end-user, law firms held 56.20% of the AI software market share in 2025, while corporate legal departments exhibited the highest 11.21% CAGR to 2031.

- By geography, North America commanded 36.40% of the AI software market in legal industry in 2025; Asia Pacific is set to lead growth at 11.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of AI Software Market In Legal Industry

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for automation amid rising litigation volume | +2.1% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Increasing adoption of AI-assisted legal-research tools | +1.8% | Global, led by APAC growth markets | Short term (≤ 2 years) |

| Rapid expansion of contract-lifecycle-management (CLM) platforms | +2.3% | North America and EU core, expanding to APAC | Medium term (2-4 years) |

| Cost-reduction pressure and legal-talent scarcity | +1.9% | Global, acute in developed markets | Long term (≥ 4 years) |

| Generative-AI breakthroughs for drafting and summarization | +1.5% | Global, early adoption in North America | Short term (≤ 2 years) |

| Open-justice data policies enabling AI training | +0.8% | North America and EU, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Automation Amid Rising Litigation Volume

Litigation teams now sift through unprecedented data, prompting e-discovery suites that remove up to 85% of documents from review and cut cycle times by half.[1]DISCO, “Improving E-Discovery with DISCO AI,” CSDISCO.COMAutomation also shortens drafting; systems condense hours of brief preparation into minutes, slicing costs by 80%.[2]IBM, “LegalMation,” IBM.COM Courts embracing AI-friendly rules, such as New South Wales’ procedural update, further legitimize these tools, pushing global legal departments to scale automation without proportional headcount increases.

Increasing Adoption of AI-Assisted Legal-Research Tools

Generative engines pull live case law across jurisdictions, returning vetted precedents in minutes.[3]vLex, “Vincent | AI for Lawyers,” VLEX.COM Law schools now embed AI coursework, exemplified by Singapore Management University’s blended curriculum, producing graduates fluent in AI-enhanced research. This generational shift accelerates firm-wide adoption and embeds research automation into everyday practice.

Rapid Expansion of Contract-Lifecycle-Management Platforms

Modern CLM suites feature agentic AI that scans clauses, scores risk, and suggests redlines while voice interfaces eliminate menu navigation.[4]Malbek, “The Top 10 Trends of Contract Lifecycle Management in 2025,” MALBEK.IO In-line analytics flag deviations during review, thanks to embedded clause-comparison and risk-scoring engines. These capabilities prove strategic as legal teams must show measurable business value while compressing turnaround times.

Cost-Reduction Pressure and Legal-Talent Scarcity

Firms face fee caps and burnout among junior staff, driving AI adoption to reallocate repetitive work and curb attrition. Alternative Legal Service Providers, already a USD 20.6 billion segment, undercut traditional rates by 30-40% through AI-augmented staffing models, forcing incumbent firms to adopt similar efficiencies

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and confidentiality concerns | -1.4% | Global, particularly EU under GDPR | Short term (≤ 2 years) |

| Limited AI explainability reducing lawyer trust | -0.9% | Global, acute in regulated jurisdictions | Medium term (2-4 years) |

| Proprietary-model vendor lock-in risk | -0.7% | Global, concentrated in North America and EU | Medium term (2-4 years) |

| AI-bias litigation and ethics compliance burden | -0.6% | Global, led by US regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Confidentiality Concerns

Formal Opinion 512 obliges U.S. attorneys to vet vendor safeguards before exposing privileged data. Parallel EU mandates restrict cross-border data flows, and recent litigation compels AI vendors to preserve user logs, raising conflicts with confidentiality rules. Firms respond with bespoke policies and localized deployments to balance AI benefit with privilege obligations.

Limited AI Explainability Reducing Lawyer Trust

Opaque reasoning clashes with lawyers’ duty to justify advice, fueling calls for open-source legal models and rigorous human oversight. Many firms now treat AI output like junior associate drafts, mandating partner review before client delivery to preserve reliability and mitigate risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Drive Market Leadership

Solutions represented 66.30% of AI software market share in 2025 as organizations favored unified suites bundling research, drafting, and analytics. The AI software market in legal industry relies on these broad platforms to satisfy confidentiality demands while simplifying vendor management. Strong traction from providers such as Harvey, which reached USD 100 million in recurring revenue within three years, validates this preference. Services, however, post the segment’s 12.32% CAGR because successful rollouts demand training, change management, and governance consulting. Constant model tuning and ethical audits reinforce the notion that technology adoption is a long-term transformation rather than a one-time license expenditure.

A growing share of budgets now funds integration specialists who embed AI outputs into matter-management, billing, and knowledge-management systems. The AI software market in legal industry therefore balances plug-and-play ambition with the reality of bespoke workflows and jurisdictional constraints. Over the forecast, vendors offering outcome-based services—such as performance guarantees tied to document-review speed—are expected to outpace pure license sellers, extending the service growth trajectory.

By Deployment: Cloud Platforms Accelerate Adoption

Cloud configurations captured 73.20% of the AI software market size in 2025, expanding at a 12.10% CAGR as firms prioritize collaboration and mobility. Bedrock partnerships between providers and hyperscale cloud vendors furnish encryption, regional data residency, and scalable GPUs, mitigating earlier security apprehensions. On-premise deployments persist where statutes or client contracts mandate local hosting, yet integration demands often render them costlier. Consequently, even highly regulated practices now pilot private-cloud variants that mirror on-prem controls while permitting distributed access.

The AI software market in legal industry benefits from cloud’s subscription economics, lowering entry barriers for midsize firms and accelerating time-to-value. In parallel, multi-cloud strategies gain favor to avoid proprietary-model lock-in and to balance sovereign data requirements with best-in-class functionality. Vendors offering containerized architectures capable of running behind firm firewalls are poised to capture risk-averse adopters seeking incremental transition paths.

By Application: Legal Research Leads While Case Prediction Emerges

Legal Research held 29.10% of the AI software market size in 2025, confirming that practitioners regard AI as a research enhancer rather than a replacement. Large language models surface nuanced precedent linkages, freeing lawyers to focus on analysis. The AI software market in legal industry is witnessing the ascent of Case Prediction, projected at 11.07% CAGR, where outcome forecasting informs settlement posture and resource allocation. Products like Theo AI deliver probability ranges and damages estimates, reshaping litigation strategy.

Contract Review stays robust as corporations streamline vendor and sales agreements, leveraging clause extraction to flag non-standard terms instantly. E-discovery, propelled by data growth, remains indispensable, especially for cross-border matters requiring multilingual review. Compliance monitoring tools increasingly parse regulatory updates, alerting counsel to emerging obligations—an area expected to converge with risk analytics, creating integrated governance dashboards.

By End-User: Law Firms Maintain Dominance While Corporate Departments Accelerate

Law firms retained 56.20% of AI software market share in 2025, acting as laboratories for innovation where billing leverage and client expectations align with efficiency gains. The AI software market in legal industry now sees corporate legal departments moving faster, with an 11.21% CAGR, as general counsel seek to deliver data-driven insights and operational savings. In-house teams harness AI to triage service requests, automate routine NDAs, and quantify legal spend, positioning themselves as strategic business partners.

Alternative Legal Service Providers amplify competitive pressure by deploying AI to deliver commoditized tasks at scale, capturing work traditionally handled by law firms. Government entities and legal aid groups are experimenting with AI chatbots to improve access to justice, backed by funding schemes such as Singapore’s Tech-celerate for Law, indicating broader societal uptake

Geography Analysis

North America’s USD-denominated opportunity remains the largest, propelled by capital inflows and a supportive professional framework. The region’s firms were first to embed large language models within legacy research platforms, and continued guidance from the American Bar Association facilitates experimentation while safeguarding privilege. Venture funding and blockbuster acquisitions confirm a maturing yet still growth-oriented ecosystem. As a result, the AI software market in legal industry will see new service tiers, including premium context-specific models targeting niche practice areas.

Asia Pacific’s growth narrative centers on policy incentives that lower technological barriers. Singapore’s regulatory sandbox encourages pilots without full-term licensing exposure, while Japanese corporates use AI to manage complex multilingual contracts, driving cross-border compliance demand. Rapid economic digitization in Southeast Asia further boosts software uptake as regional firms leapfrog legacy systems.

Europe’s methodical approach blends opportunity with oversight. The EU AI Act enforces risk categorization and documentation, nudging buyers toward vendors with embedded audit trails. Academic-industry collaboration, such as Oxford’s AI for English Law program accessing 400,000 cases, fuels algorithmic sophistication. Eastern European firms are emerging adopters, attracted by cross-European litigation funding that prioritizes analytics-backed case evaluation.

Competitive Landscape

The market remains fragmented yet dynamic. Legacy information providers partner with AI specialists to retain relevance; LexisNexis deepened its OpenAI collaboration, embedding large language models into its Protégé assistant. AI-native disruptors like Spellbook release autonomous agents capable of executing multi-step transactional tasks, leapfrogging incremental feature updates. Consolidation accelerates as incumbents acquire niche capabilities, illustrated by Aderant purchasing HerculesAI assets to strengthen billing compliance workflows.

Vendor strategies bifurcate: platform players chase breadth, integrating drafting, research, and workflow; specialists focus on depth, dominating a single function then extending horizontally via API ecosystems. Buyers increasingly demand outcome metrics, such as document-review savings or predictive-accuracy scores, pressuring vendors to validate claims with empirical studies. Sustainable differentiation now hinges on explainability features, multilingual training data, and configurable compliance layers that satisfy divergent jurisdictions.

Leaders of AI Software Market In Legal Industry

ROSS Intelligence Inc.

Luminance Technologies Ltd.

IBM Corporation

KIRA Inc.

RELX PLC (LexisNexis Legal and Professional)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Aderant agreed to acquire HerculesAI’s billing-compliance platform, enhancing machine-learning driven work-to-cash solutions.

- August 2025: AffiniPay partnered with Caseway to add AI-powered court-form automation to MyCase, launching with California coverage.

- June 2025: Harvey introduced Deep Research for Legal, broadening its AI platform beyond drafting into comprehensive research.

- June 2025: Clio finalized its USD 1 billion buyout of vLex, creating a unified practice-management and AI-research environment.

Scope of Report on AI Software Market In Legal Industry

Artificial intelligence (AI) is an incorporated result of machine learning, information science, computer vision, evolutionary computation, data mining, and multi-agent systems. AI is transforming the everyday practice of law, changing the skills and professionalism required from lawyers. Some of the applications of AI in the legal industry include contract review and management, legal research, e-billing, and e-discovery, among others.

AI Software Market in Legal Industry is Segmented by component (solution, services), deployment (on-premise, cloud), application (legal research, contract review and management, e-billing, e-discovery, compliance, case prediction), end-user industry (law firms, corporate legal departments), and geography (North America, Europe, Asia Pacific, Latin America, Middle East & Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions |

| Services |

| On-premises |

| Cloud |

| Legal Research |

| Contract Review and Management |

| E-billing |

| E-discovery |

| Compliance |

| Case Prediction |

| Other Applications |

| Law Firms |

| Corporate Legal Departments |

| Alternative Legal-Service Providers (ALSPs) |

| Other End-Users |

| North America |

| South America |

| Europe |

| Asia Pacific |

| Middle East and Africa |

| By Component | Solutions |

| Services | |

| By Deployment | On-premises |

| Cloud | |

| By Application | Legal Research |

| Contract Review and Management | |

| E-billing | |

| E-discovery | |

| Compliance | |

| Case Prediction | |

| Other Applications | |

| By End-User | Law Firms |

| Corporate Legal Departments | |

| Alternative Legal-Service Providers (ALSPs) | |

| Other End-Users | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

How large is the AI software market in legal industry today?

The AI software market in legal industry stands at USD 2.67 billion in 2026 and is projected to reach USD 4.42 billion by 2031.

Which application currently generates the highest revenue?

Legal Research contributes 29.10% of AI software market size, making it the highest-revenue application segment.

Which deployment model is growing fastest?

Cloud platforms lead adoption and are expanding at a 12.10% CAGR through 2031.

Which region offers the strongest growth outlook?

Asia Pacific shows the fastest 11.54% CAGR thanks to supportive government funding and corporate digital-transformation drives.

What is the biggest restraint facing adoption?

Data-privacy and confidentiality concerns impose the largest negative impact, reducing forecast CAGR by 1.4%.

Page last updated on: