Generative AI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

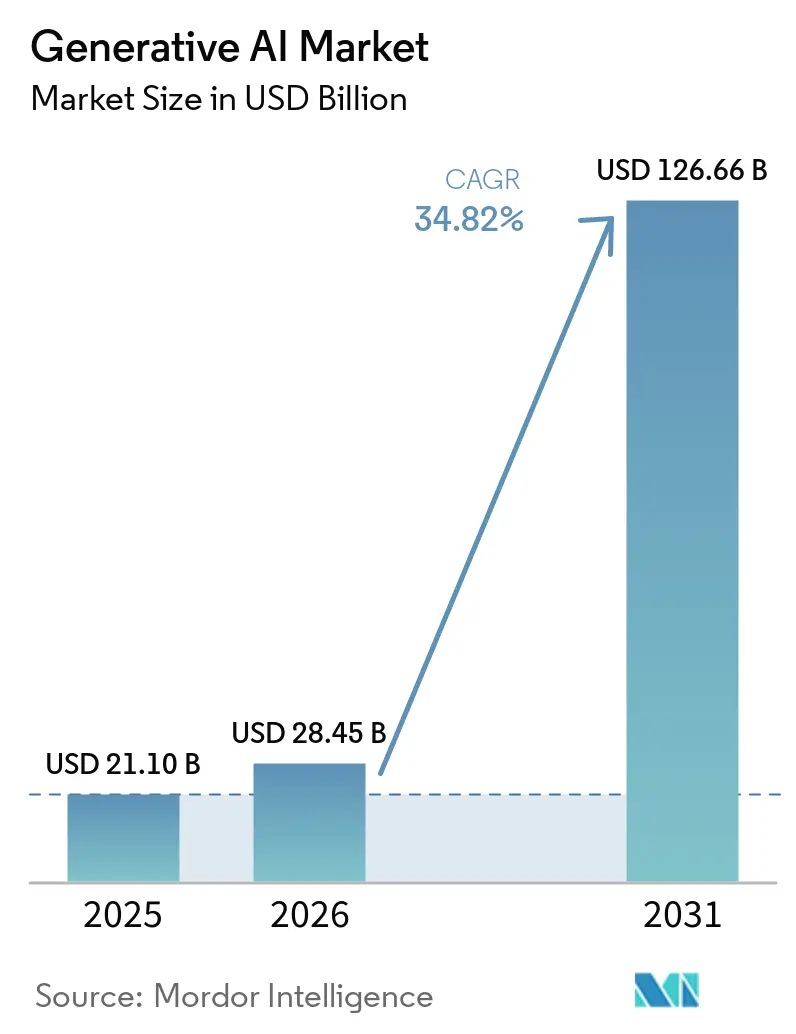

| Market Size (2026) | USD 28.45 Billion |

| Market Size (2031) | USD 126.66 Billion |

| Growth Rate (2026 - 2031) | 34.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Generative AI Market Analysis by Mordor Intelligence

The generative AI market size is expected to grow from USD 21.1 billion in 2025 to USD 28.45 billion in 2026 and is forecast to reach USD 126.66 billion by 2031 at 34.82% CAGR over 2026-2031. Rapid enterprise migration from instruction-driven software to intention-driven systems is reshaping productivity expectations across functions, and 20%–40% of workers are already using AI tools in their daily workflows. North America continues to lead adoption thanks to capital availability and mature cloud infrastructure, while large public-sector initiatives such as India’s USD 1.25 billion IndiaAI Mission position Asia for outsized long-term growth. Falling model-training costs, wider access to foundation-model APIs, and sustained venture funding further reinforce a flywheel that lowers barriers to entry and accelerates use-case experimentation. At the same time, the EU AI Act introduces stringent governance obligations that drive up compliance budgets but also create new service opportunities in risk management and audit readiness. Rising power demand from large-scale inference clusters is a mounting concern, and energy-efficiency breakthroughs have become a decisive differentiator for chipmakers such as NVIDIA, which already covers 76% of its electricity use with renewables.

Key Report Takeaways

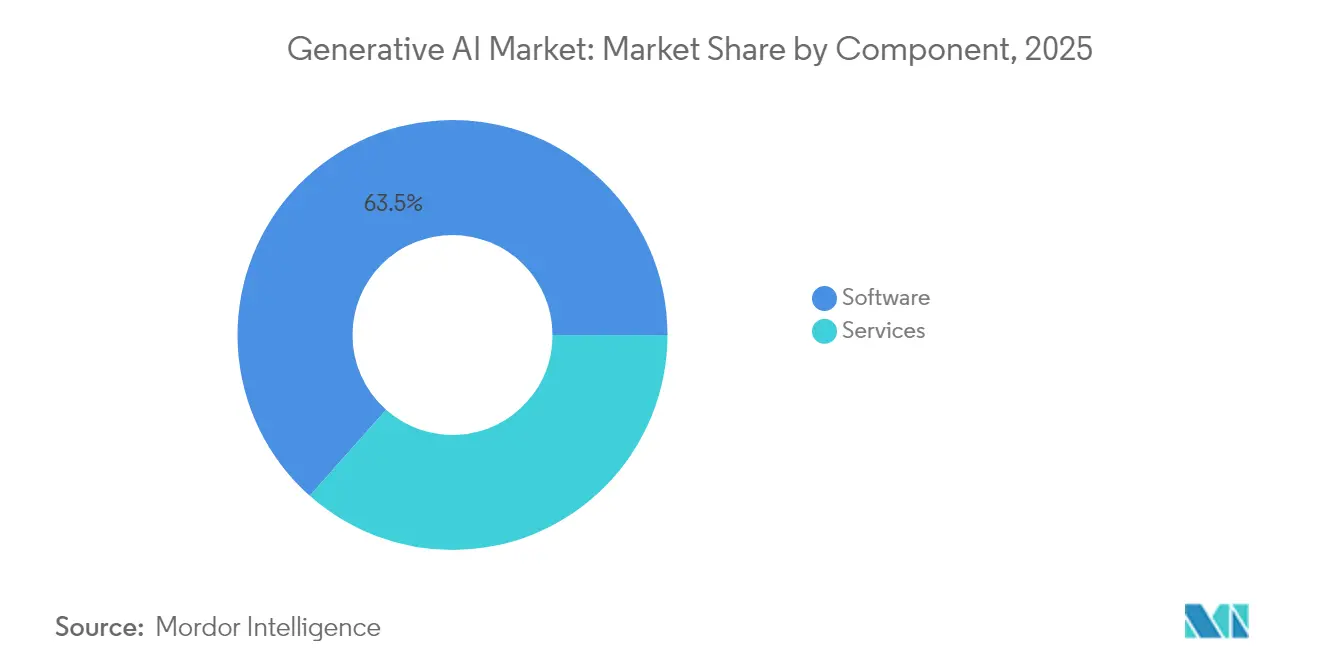

- By component, software held 63.45% of the generative AI market share in 2025, while services are projected to expand at a 43.36% CAGR to 2031.

- By deployment mode, cloud infrastructure accounted for 71.80% of the generative AI market size in 2025, whereas edge and on-device solutions are advancing at a 49.88% CAGR through 2031.

- By application, content creation led with 35.10% revenue share in 2025; code generation is forecast to grow at a 49.4% CAGR to 2031.

- By end-user industry, BFSI captured 22.15% of the generative AI market size in 2025, while healthcare is set to rise at a 36.36% CAGR between 2026 and 2031.

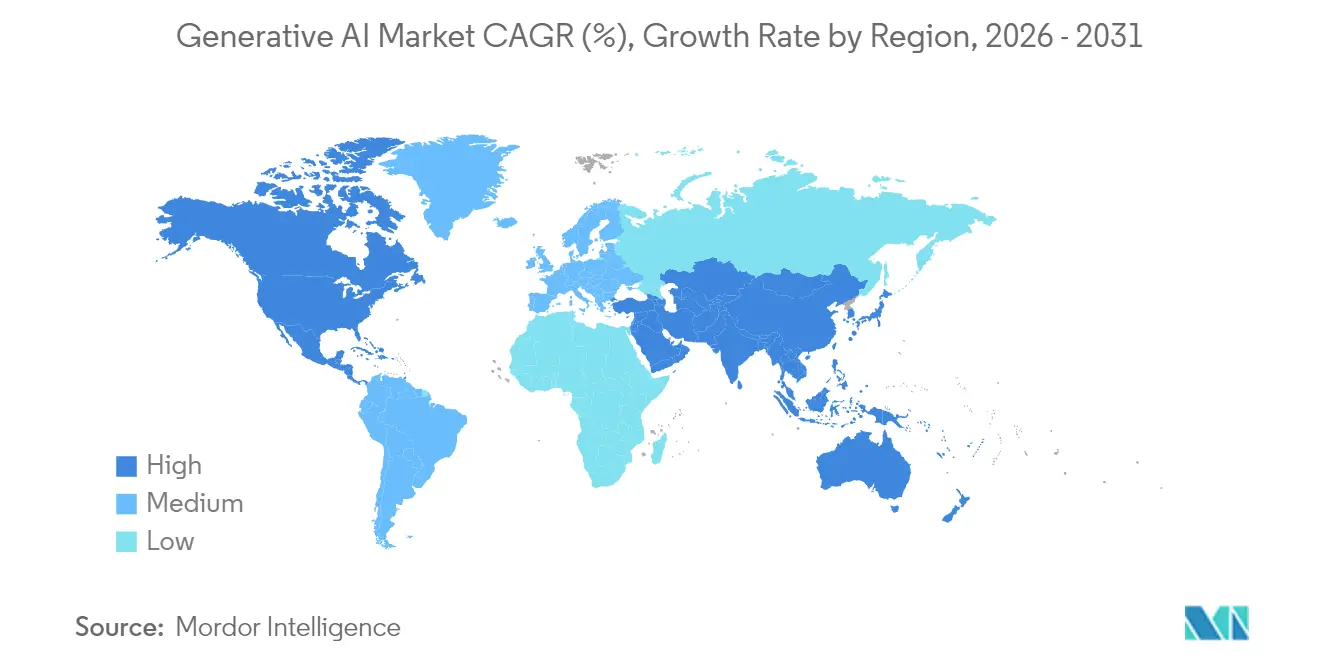

- By geography, North America commanded 40.60% of the generative AI market share in 2025, but the Asia-Pacific region is poised for the fastest expansion with a 36.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Generative AI Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise-wide productivity push | +8.5% | Global with concentration in North America and EU | Medium term (2–4 years) |

| VC and corporate mega-funding rounds | +7.8% | North America and China, spillover to Asia-Pacific | Medium term (2–4 years) |

| Falling model-training costs via foundation models | +6.2% | Global, strongest effect in emerging markets | Short term (≤ 2 years) |

| On-device generative-AI enablement in consumer hardware | +5.3% | Asia-Pacific manufacturing hubs, global rollout | Medium term (2–4 years) |

| AI-assisted code-generation demand spike | +4.6% | Global, tech-centric regions | Short term (≤ 2 years) |

| Synthetic-data marketplaces take-off | +4.1% | Global, early use in regulated industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise-wide Productivity Push

Widespread deployment of AI copilots and chat-based work assistants is beginning to translate into measurable operational gains, particularly among early adopters in North America and Europe. Fortune-class enterprises integrating AI into document creation, meeting summarization, and customer-service workflows report noticeable reductions in cycle time and error rates. UK Finance forecasts that financial services firms will raise the share of technology budgets dedicated to generative AI from 12% in 2024 to 16% in 2025. Despite clear upside, only one-quarter of projects currently meet return-on-investment targets, underscoring the importance of change-management expertise and robust governance frameworks. This capability gap sustains strong demand for implementation services and creates durable competitive advantages for firms that combine domain knowledge with AI fluency.

Falling Model-Training Costs via Foundation Models

Foundation-model providers have slashed the compute requirements for advanced capabilities by allowing enterprises to fine-tune rather than build from scratch, which compresses time-to-value and lowers cash burn. NVIDIA’s Blackwell architecture, designed for energy-efficient training and inference, illustrates this trajectory while also pushing the company toward its goal of 100% renewable electricity by fiscal 2025. The rise of GPU marketplaces has created transparent spot pricing that helps smaller firms match resource needs to project scale. Lower thresholds for experimentation accelerate global diffusion, with particular benefits for innovators in emerging markets who previously lacked access to large-scale compute.

VC and Corporate Mega-Funding Rounds

Generative-AI startups attract multibillion-dollar rounds from venture funds as well as strategic investors that seek to embed proprietary models deep inside existing cloud ecosystems. Several single-company raises already exceed the combined AI funding of entire industry cycles a decade ago. Large capital infusions allow rapid scaling of talent and infrastructure, but they also reinforce winner-take-most dynamics by raising the minimum efficient scale for credible new entrants. Consolidation at the model layer is therefore likely to continue, making downstream specialization and service differentiation critical for challengers.

Synthetic-Data Marketplaces Take-Off

High-quality synthetic datasets help organizations comply with privacy and copyright rules while still training models on representative examples. The United States Copyright Office underscores that purely AI-generated material lacks copyright protection, prompting enterprises to seek transparent data provenance solutions. Regulators such as the European Patent Office now require fuller disclosure of training-data characteristics, which is pushing the market toward standardized synthetic-data validation frameworks. Initial traction is strongest in pharmaceutical R&D and financial-risk modeling, where privacy constraints and data scarcity have long hindered AI experiments.

Restraints Impact Analysis of Generative AI Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and ethical-AI compliance risk | -4.8% | EU and California lead, global spillover | Medium term (2–4 years) |

| Escalating GPU and energy costs plus carbon footprint | -3.2% | Global, acute in energy-constrained regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Ethical-AI Compliance Risk

The EU AI Act introduces fines reaching EUR 35 million (USD 40.44 million) or 7% of global turnover for non-compliance, compelling providers to produce detailed technical documentation and copyright-law checks before model release. Japan’s new AI Business Guidelines extend governance standards to foreign suppliers that process domestic user data. In the United States, the Federal Trade Commission is examining exclusivity clauses in cloud-AI alliances, pointing to heightened antitrust scrutiny. Multinational vendors now juggle overlapping rules that mandate local data processing, algorithmic transparency, and human oversight, raising the cost of market entry and favoring incumbents with robust legal resources.

Escalating GPU and Energy Costs plus Carbon Footprint

The International Monetary Fund projects that AI workloads could consume 1,500 TWh annually by 2030, roughly equal to India’s current electricity use. United States data centers already draw 4.4% of national power, and policy forecasts see the figure rising to 12% by 2028. Capital-spending models compiled by CSIS indicate that physical infrastructure additions could add 83.7 GW to the US grid within this decade. While chipmakers focus on energy-efficient designs, the lag between renewable deployment and compute demand may trigger carbon taxes that eat into profit margins for compute-intensive training runs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Generative AI Market Segment Analysis

By Component:

Services Acceleration Outpaces Software DominanceSoftware continued to capture 63.45% of the generative AI market in 2025, reflecting its role as the core enabler of model development, orchestration, and application delivery. The services segment is scaling faster at a 43.36% CAGR because many organizations lack in-house data-science skills and must rely on consultancies for integration, customization, and governance. Adoption of turnkey AI platforms lowers entry hurdles, yet enterprises still grapple with change management that requires bespoke training and process redesign. The generative AI market size for services is projected to grow steadily as compliance mandates create additional advisory demand.

The services surge also mirrors the strategic importance of domain expertise when tailoring models to regulated sectors such as healthcare and banking. Advisory firms bundle risk assessments and ethics audits with deployment work, creating multi-year revenue streams aligned to ongoing model monitoring. As software vendors open their ecosystems to third-party plug-ins, integrators gain new cross-selling avenues. Over time, subscription-based support packages may blur the line between software and services offerings, but the current revenue breakout suggests enough differentiation to sustain separate growth narratives.

By Deployment Mode:

Edge Computing Disrupts Cloud HegemonyCloud vendors accounted for 71.80% of the generative AI market in 2025, leveraging global data-center footprints and managed-service models that eliminate upfront hardware spend. Consumption-based pricing aligns costs with usage peaks, a feature that remains attractive for experimental workloads. However, latency-sensitive tasks in manufacturing, mobility, and public safety highlight the limits of remote inference. The generative AI market size allocated to edge solutions is forecast to expand at a 49.88% CAGR as organizations embed accelerators into gateways, appliances, and handheld devices.

Edge deployment appeals to firms seeking resilience when connectivity is unreliable or data sovereignty rules forbid external transmission. Advances chronicled in the 2025 Edge AI Technology Report demonstrate that quantization, pruning, and on-chip caching can crush model footprints without compromising accuracy. Hybrid architectures that decide dynamically where computation runs will likely dominate as customers weigh latency, cost, and regulatory constraints. Over the forecast period, cloud providers are expected to launch managed edge stacks that bring their developer toolchains closer to local silicon.

By End-User Industry:

Healthcare Transformation Accelerates Beyond BFSI LeadershipBanking, financial services, and insurance contributed 22.15% of generative AI market revenue in 2025, leveraging conversational bots for customer engagement and advanced analytics for fraud detection. Strong regulatory oversight in finance drives high demand for audit-ready models, which in turn fuels specialized software and compliance-service opportunities. Healthcare, however, is forecast to grow at a 36.36% CAGR as hospitals deploy AI for imaging analysis, clinical-trial design, and administrative automation. The surge follows regulatory openness exemplified by the US Food and Drug Administration’s expanding list of AI-enabled medical devices.

Clinical-decision support tools promise tangible patient-outcome improvements, which justifies investment despite strict privacy rules. Pharmaceutical firms use generative models to explore chemical space and simulate trial cohorts, shortening discovery cycles. In parallel, public-sector payers expect AI to mitigate personnel shortages and budget pressures. As reimbursement frameworks evolve, reference deployments will spread across tier-two providers, reinforcing healthcare’s long-run status as the fastest-moving vertical in the generative AI market.

By Application:

Code Generation Surge Challenges Content Creation DominanceContent creation held 35.10% of application revenue in 2025, with marketing, media, and education sectors quickly adopting text, image, and video generation. Yet code generation is projected to climb at a 49.4% CAGR, propelled by productivity gains that compound across iterative software-development lifecycles. The generative AI market size attached to developer tooling is therefore expected to rival creative-content spending by the end of the forecast period. Early adopters report steep drops in boilerplate coding time, freeing engineers to focus on architecture and security reviews.

As large enterprises standardize on private models trained on proprietary repositories, demand for secure supply-chain integrations grows. Automated documentation, test-case synthesis, and refactoring capabilities extend AI’s footprint beyond initial code suggestion. Intellectual-property teams also exploit generative assistance for patent claim drafting, a trend validated by the American Bar Association’s recent guidance. Over the next five years, packaged AI agents may evolve into full life-cycle orchestration engines that incorporate planning, design, and deployment.

By Model Architecture:

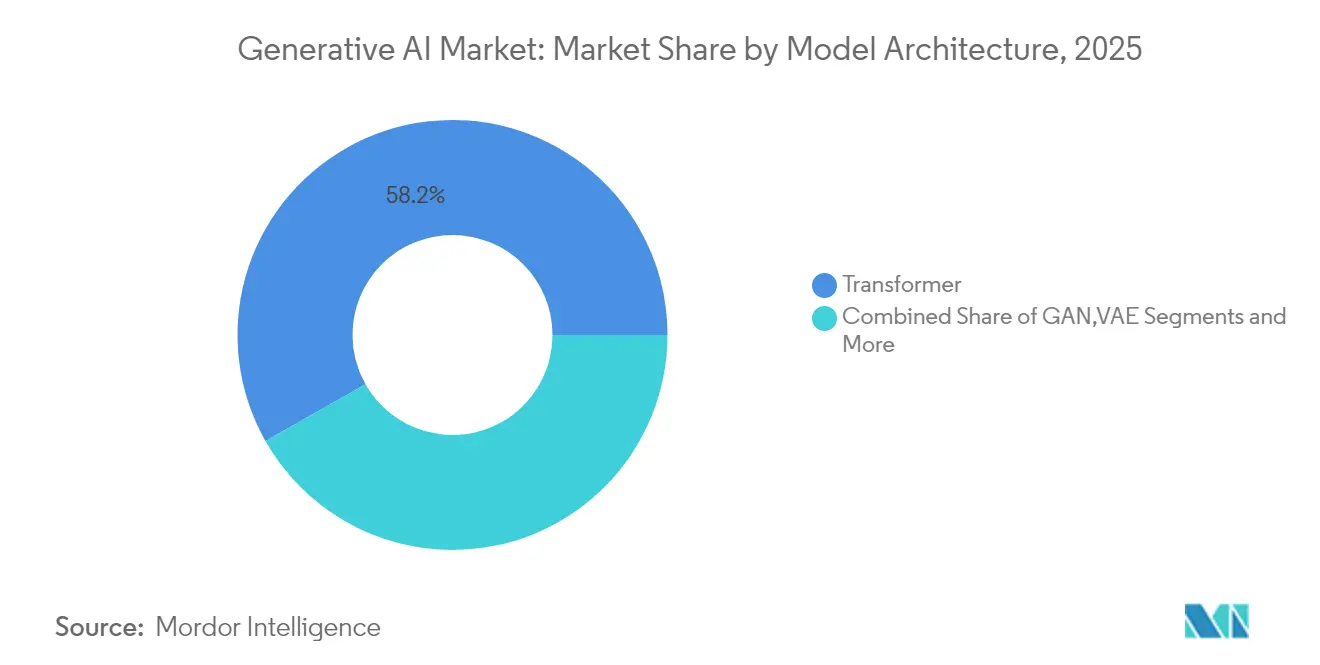

Diffusion Models Challenge Transformer SupremacyTransformers retained a 58.20% share of the architecture landscape in 2025 thanks to their versatility across language, audio, and multimodal tasks. Generative Adversarial Networks and Variational Autoencoders serve niche requirements, but diffusion models are rising fastest at a 45.12% CAGR because of their superior sample quality in image and video synthesis. Patent-filing trends tracked by IFI CLAIMS confirm a surge in diffusion-related inventions, particularly from major cloud and semiconductor firms. Continuous improvements in denoising algorithms and scheduler efficiency have cut inference latency, opening the door to real-time applications.

Enterprises drawn to visual-content generation now evaluate whether to combine text-based transformers with diffusion back-ends to achieve unified multimodal workflows within the evolving Multimodal AI ecosystem. Tool-chain flexibility will likely dictate architecture choices as teams seek to balance performance, licensing terms, and hardware compatibility. Over time, new hybrid approaches may blend the interpretability of autoregressive models with the richness of diffusion outputs, further fragmenting the landscape.

By Organization Size:

SME Adoption Accelerates Despite Enterprise DominanceLarge enterprises absorbed 66.10% of generative-AI spending in 2025, reflecting bigger budgets and higher risk tolerance for production rollouts. Many Fortune 500 companies have embedded AI assistants into knowledge-management systems, bolstered by dedicated governance boards that oversee model usage. Small and medium enterprises, however, are predicted to expand their spend at a 37.04% CAGR as pay-as-you-go APIs remove hefty capital requirements. India’s national GPU-sharing initiative, which provisions 18,693 chips for public access, illustrates how policy can democratize high-performance compute.

SMEs typically focus on narrow, high-impact tasks such as chatbot-enabled sales support or automated invoice processing, yielding quick wins that free up resources for further AI pilots. Vendor ecosystems now market domain-specific templates that cut configuration time, allowing smaller teams to skip lengthy data-science cycles. As a result, competitive pressure on incumbents intensifies, since nimble SMEs can offer AI-augmented services without matching the headcount or infrastructure scale of larger rivals.

Geography Analysis

North America Generative AI Market

North America generated 40.60% of 2025 revenue for the generative AI market, buoyed by abundant venture capital, deep pools of technical talent, and a robust cloud-provider landscape. Ongoing public-sector programs that promote trustworthy AI research complement private initiatives, maintaining the region’s innovation momentum. Tight coupling between model developers and infrastructure vendors further accelerates commercialization, though antitrust probes signal growing regulatory interest in platform power dynamics.

APAC Generative AI Market

The Asia-Pacific region is on track for a 36.88% CAGR through 2031, propelled by government stimulus, a thriving electronics supply chain, and rapid digital-workforce expansion. India’s aggressive investment in public compute illustrates the region’s determination to close capability gaps and localize key AI assets. Australia, Singapore, and South Korea add momentum by turning national-security and healthcare challenges into AI innovation sandboxes, while cross-border venture funds channel capital toward high-growth startups.

EMEA and South America Generative AI Market

Europe pursues balanced progress by pairing industrial-policy incentives with the continent’s most comprehensive AI governance regime. The EU AI Act’s transparency rules are expected to raise compliance spending but also create a market for audit tooling and certified datasets. Northern European utilities accelerate renewable-energy capacity to meet data-center demand, positioning the bloc as a potential leader in low-carbon AI hosting. Emerging regions in South America, the Middle East, and Africa explore sector-specific deployments in natural resources and financial inclusion, adding diversity to the global adoption map.

Competitive Landscape

The competitive arena is consolidating as capital requirements and data-network effects push scale advantages to the forefront. Patent analytics show that four companies—Google, Microsoft, IBM, and NVIDIA—filed a significant share of new generative-AI inventions during 2024. Cloud providers deepen vertical integration by bundling proprietary silicon, foundation models, and managed-service layers, creating sticky ecosystems that lower customer churn yet raise switching costs.

Regulators respond by scrutinizing exclusivity clauses and preferential access to compute. The US Federal Trade Commission’s inquiry into cloud-AI partnerships underscores concerns that infrastructure gatekeepers could foreclose competition. In parallel, hardware challengers develop specialized accelerators to bypass GPU bottlenecks, while open-source model communities attempt to chip away at proprietary leads. Service providers carve niches in compliance, localization, and sector-specific fine-tuning, areas less exposed to scale economics.

Mature vendors pursue global expansion through joint ventures and sovereign-cloud offerings that satisfy data-residency rules. Strategic focus is shifting from landmark model releases to operational hardening, where reliability, fault tolerance, and energy efficiency become procurement criteria. The medium-term outlook therefore favors players capable of balanced investment across research, infrastructure, and regulatory engagement, reinforcing the importance of deep, diversified capital pools.

Generative AI Industry Leaders

Google LLC

IBM Corporation

Microsoft Corporation

Adobe Inc

Amazon Web Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Generative AI Market Companies Covered in this Report

- Google LLC

- Microsoft Corporation

- OpenAI LP

- IBM Corporation

- Amazon Web Services Inc.

- Nvidia Corporation

- Adobe Inc.

- SAP SE

- Cohere Inc.

- Anthropic PBC

- Stability AI

- Midjourney Inc.

- Hugging Face Inc.

- Salesforce Inc.

- Databricks – MosaicML

- Oracle Corporation

- ServiceNow Inc.

- Arm Holdings plc

- Jasper AI

- Synthesia Ltd.

- Rephrase AI

- Konverge AI

Recent Industry Developments in Generative AI Market

- June 2025: OpenAI reported USD 10 billion in annual recurring revenue and closed a USD 40 billion funding round led by SoftBank.

- June 2025: The US Food and Drug Administration introduced “Elsa,” a generative-AI system that streamlines clinical-protocol and safety-report reviews.

- May 2025: Google Cloud unveiled the Agentspace platform, positioning agentic AI as a core differentiator for enterprise solutions.

- April 2025: Japan released its AI Strategy 2025 mid-term update, outlining plans for sector-specific legislation that balances innovation and risk.

Generative AI Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the generative artificial intelligence market as global revenue earned from proprietary GenAI software licenses, foundation-model API subscriptions, and paid integration or enablement services that let algorithms create new text, code, images, audio, or video from learned patterns.

Scope exclusion: Hardware sales, generic analytics suites, and downstream royalties that only embed GenAI output remain outside this valuation.

Segments Covered in This Report

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-Premise

- Hybrid

- Edge / On-Device

- By End-User Industry

- BFSI

- Healthcare

- IT and Telecommunication

- Government

- Retail and Consumer Goods

- Manufacturing

- Media and Entertainment

- Others

- By Application

- Content Creation

- Code Generation

- Data Augmentation

- Design and Prototyping

- Security and Risk Analytics

- Others

- By Model Architecture

- GAN

- Transformer

- VAE

- Diffusion

- Autoregressive / Flow-based

- By Organisation Size

- Large Enterprises

- Small and Medium Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts spoke with cloud architects, GenAI product leads, risk advisers, and enterprise buyers across North America, Europe, and Asia-Pacific. The conversations confirmed spending intentions, contract sizes, and GPU capacity constraints, letting us tighten critical assumptions.

Desk Research

We began by mapping demand through open sources such as the US Bureau of Economic Analysis ICT tables, Eurostat digital-economy surveys, the OECD AI compute index, NIST risk-management guidance, Questel patent records, and Volza shipment traces. Company 10-Ks, investor decks, and leading trade-association papers refined price bands and adoption curves. These references are illustrative; numerous additional materials supported data collection, confirmation, and clarifications.

Market-Sizing & Forecasting

We first convert sector software outlays into an addressable pool, then filter it through GenAI penetration, usage intensity, and average subscription pricing. Selective supplier roll-ups and channel checks give a bottom-up cross-look that validates totals. Core variables include cloud AI billings, monthly active foundation-model users, data-center GPU hours, regulatory surcharge factors, and regional AI talent supply. A multivariate regression blended with scenario analysis projects values to 2030 and flags variance triggers.

Data Validation & Update Cycle

Outputs face variance checks against independent metrics; anomalies prompt senior analyst review and fresh respondent call-backs before sign-off. Reports refresh every year, with interim updates after landmark regulations or major model launches.

How Mordor Intelligence's Generative AI Market Size Compares to Other Published Estimates

Published estimates often diverge because other firms choose different revenue layers, geographies, and update rhythms.

Some enlarge totals by bundling infrastructure, while others stop at pilot spending.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 21.10 B (2025) | Mordor Intelligence | - |

| USD 22.20 B (2025) | Regional Consultancy A | Narrow regional sampling and no usage intensity adjustment |

| USD 71.36 B (2025) | Global Consultancy B | Includes hardware revenue and relies on vendor bookings without penetration checks |

The comparison shows how Mordor's clear scope, disciplined variables, and repeatable steps give decision-makers a balanced, traceable baseline they can trust.

Key Questions Answered in the Report

What is the current value of the generative AI market?

The generative AI market size stands at USD 28.45 billion in 2026 and is projected to reach USD 126.66 billion by 2031.

Which region leads generative AI adoption?

North America holds the largest regional position with 40.60% of 2025 revenue, supported by deep venture-capital pools and mature cloud infrastructure.

Why are services growing faster than software in this space?

Enterprises need external expertise for integration and governance, causing the services segment to grow at a 43.36% CAGR even though software retains most revenue.

What role will edge deployment play over the next five years?

Edge and on-device solutions are forecast to expand at a 49.88% CAGR as organizations seek lower latency.

Page last updated on: