Aminophylline Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 323.7 Million |

| Market Size (2031) | USD 363.03 Million |

| Growth Rate (2026 - 2031) | 2.32% CAGR |

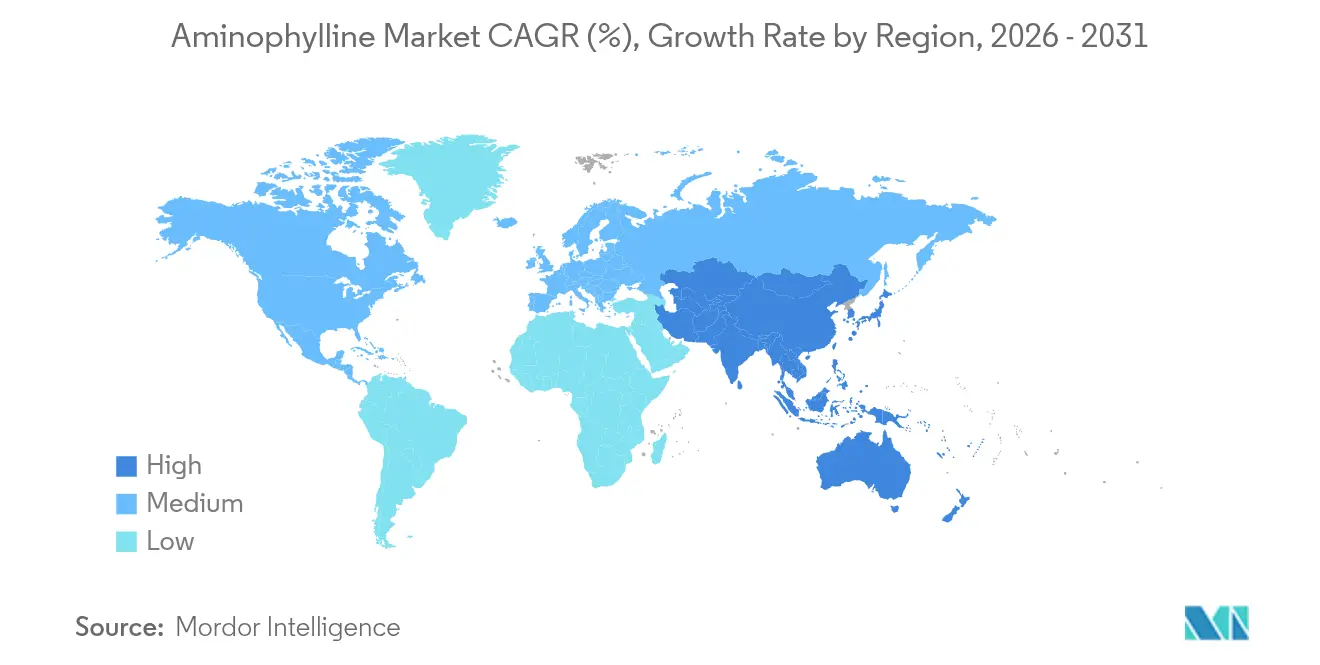

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

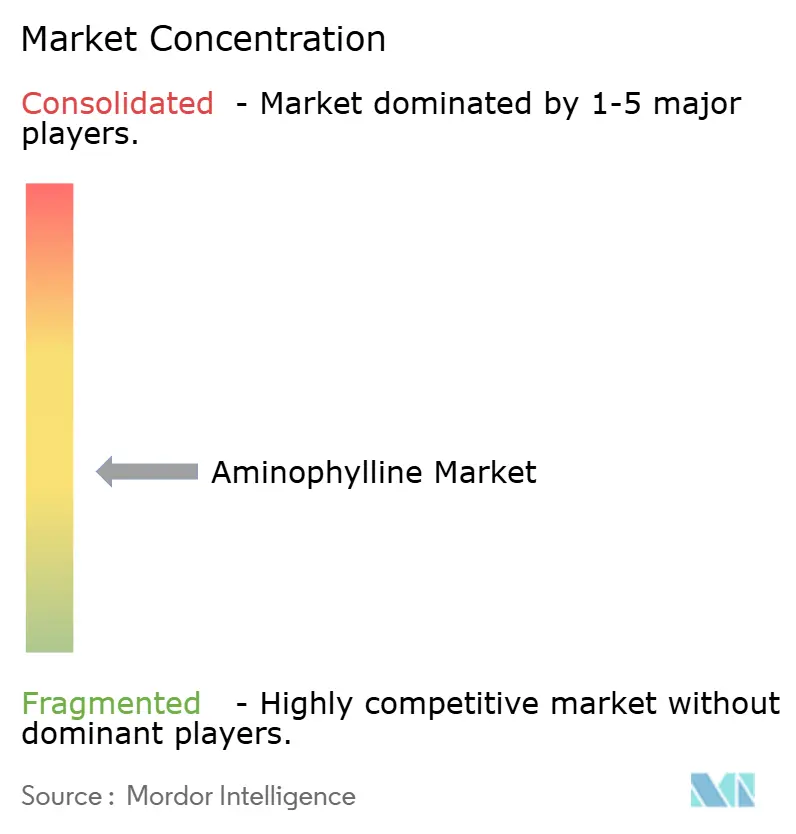

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aminophylline Market Analysis by Mordor Intelligence

The aminophylline market size was valued at USD 316.36 million in 2025 and estimated to grow from USD 323.7 million in 2026 to reach USD 363.03 million by 2031, at a CAGR of 2.32% during the forecast period (2026-2031). The growth profile reflects steady demand for this long-established bronchodilator, particularly in cost-sensitive health systems that prioritize proven respiratory therapies over premium novel drugs. North America dominates revenue because neonatal care and COPD management pathways still incorporate methylxanthines, while Asia-Pacific registers the strongest expansion as healthcare access widens and respiratory disease prevalence rises. Oral dosage forms underpin the bulk of prescriptions on the back of patient convenience, yet injectable products are scaling faster in hospitals where rapid bronchodilation is required. COPD remains the leading indication, but infant apnea contributes an outsized share of incremental volume owing to continuing NICU build-outs and supportive clinical data. Digital dispensing and tele-prescription momentum further expand access, positioning aminophylline as a practical option for long-term therapy continuity across geographies.

Key Report Takeaways

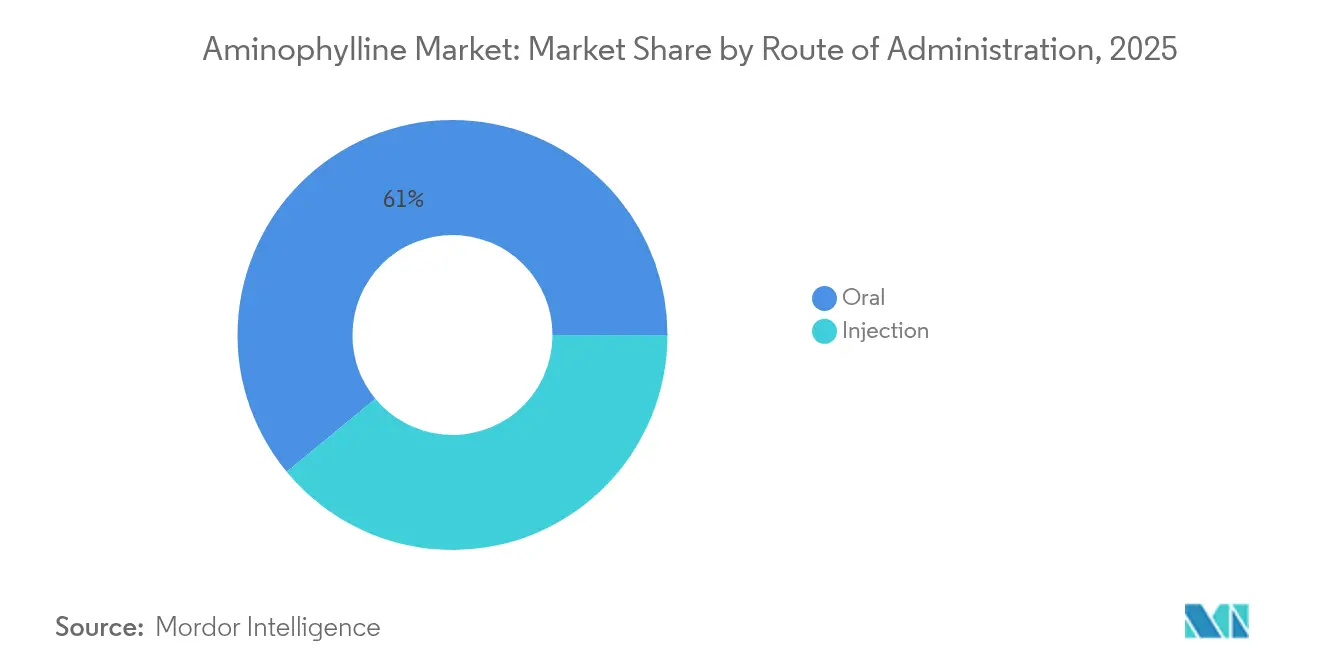

- By route of administration, oral products accounted for 60.98% of the aminophylline market share in 2025; injections are projected to expand at a 4.52% CAGR through 2031.

- By dosage form, tablets led with 54.03% revenue share in 2025, while solutions are forecast to grow at 5.67% CAGR between 2026-2031.

- By application, COPD captured 44.78% of the aminophylline market size in 2025 and infant apnea is advancing at a 6.55% CAGR to 2031.

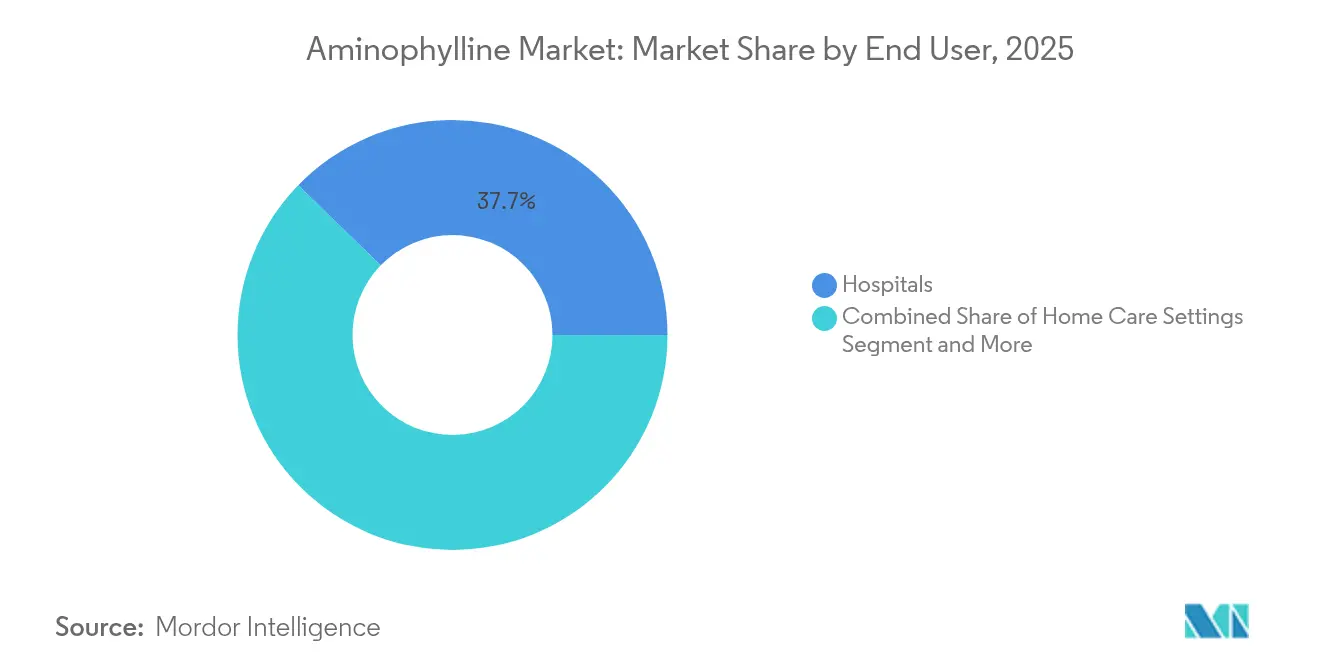

- By end user, hospitals represented 37.74% share of the aminophylline market in 2025; home-care settings exhibit the highest projected CAGR at 6.28% through 2031.

- By distribution channel, hospital pharmacies held 46.31% share in 2025, whereas online pharmacies are growing at 7.44% CAGR across the forecast horizon.

- By geography, North America contributed 37.29% of 2025 revenue; Asia-Pacific is expected to climb at an 6.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aminophylline Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in prevalence of chronic respiratory diseases | +0.8% | Global, strongest in Asia-Pacific and Middle East-Africa | Long term (≥ 4 years) |

| Price advantage over novel bronchodilators | +1.2% | India, China, Brazil | Medium term (2-4 years) |

| Growing adoption in neonatal respiratory stimulation | +0.9% | Developed economies with advanced NICUs | Medium term (2-4 years) |

| API supply diversification in emerging markets | +0.7% | Asia-Pacific core, spill-over to Latin America | Long term (≥ 4 years) |

| Integration into combination inhalers | +0.6% | North America and European Union | Long term (≥ 4 years) |

| Rising tele-prescription volumes | +0.4% | North America and European Union | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increase in prevalence of chronic respiratory diseases

Global COPD cases exceed 16 million adults in the United States alone, underpinning consistent demand for cost-effective bronchodilators such as aminophylline. Aging demographics in high-income countries heighten susceptibility to chronic airway obstruction, while pollution-driven morbidity in megacities escalates patient numbers across Asia-Pacific. The drug’s long clinical pedigree and multisource availability make it a viable alternative when patients cannot tolerate or afford newer dual- or triple-therapy inhalers. Health ministries in emerging economies often mandate formulary inclusion of essential generics to curb treatment costs, thereby reinforcing aminophylline uptake. These converging epidemiological and economic factors provide a durable volume base that steadies the overall aminophylline market.

Price advantage over novel bronchodilators

Benchmark procurement audits show that generic aminophylline can be priced more than 70% below patented respiratory agents, a differential that is decisive for payers managing tight budgets[1]U.S. Department of Health and Human Services, “Analysis of New Generic Markets,” hhs.gov. Recent withdrawals of high-priced inhalers have prompted insurers to steer prescribers toward lower-cost therapies to sustain access. Hospital pharmacy and group-purchasing contracts increasingly favour suppliers offering guaranteed volumes at predictable prices, positioning aminophylline manufacturers with diversified production networks to win tenders. The resulting savings free capacity for health systems to finance diagnostics and preventive programs, reinforcing the drug’s perceived value.

Growing adoption in neonatal respiratory stimulation

NICUs routinely administer aminophylline to preterm infants with central apnea, achieving 80-85% efficacy rates in reducing episodes and lowering ventilator dependence[2]Amir-Mohammad Armanian et al., “Prophylactic Aminophylline for Prevention of Apnea,” iranrccmj.org. Clinicians note ancillary renal-protective properties that extend utility beyond breathing support, broadening appeal among neonatologists. Capacity expansion of neonatal units across middle-income countries amplifies demand, especially where caffeine citrate is either unavailable or unaffordable. The drug’s established safety profile and decades of dosing know-how lessen adoption barriers, sustaining double-digit volume growth within this sub-segment.

API supply diversification in emerging markets

New multi-purpose reactors totalling 3,773 m³ commissioned by WuXi STA in 2024 enlarge global aminophylline API output and disperse sourcing risk[3]WuXi STA, “Launches New Small-Molecule API Facility,” wuxiapptec.com. Parallel capacity upgrades in India and Singapore provide additional buffers against single-site disruptions. Broader geographic spread supports competitive pricing and strengthens resilience, but trade-security regulations such as China’s anti-espionage law add layers of compliance and inspection complexity that manufacturers must navigate. Overall, supply diversification contributes positively to growth by stabilizing finished-product availability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Narrow therapeutic window & side-effect profile | -0.5% | Global, more restrictive in highly regulated markets | Medium term (2-4 years) |

| Decline in evidence-based COPD guidelines | -0.3% | North America and European Union | Long term (≥ 4 years) |

| Regulatory scrutiny on neonatal caffeine analogs | -0.4% | Global, highest in tier-one regulatory regions | Short term (≤ 2 years) |

| Periodic API shortages as CMOs exit | -0.2% | Global supply chain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Narrow therapeutic window & side-effect profile

Aminophylline requires serum monitoring because toxicity risk escalates above 20 mcg/mL, with documented arrhythmias and seizures at supratherapeutic exposures. Outpatient practices lacking point-of-care analyzers often prefer agents with wider margins such as long-acting beta-agonists, translating to slower uptake in primary-care settings. Elderly and multi-comorbidity cohorts present higher drug-interaction risk, prompting guideline committees to advocate caution. These safety demands elevate overall care costs, partly offsetting the product’s price advantage and thereby tempering growth.

Decline in evidence-based COPD guidelines

The 2024 GOLD and 2025 BTS/NICE/SIGN reviews relegate methylxanthines to adjunctive or second-line therapy, citing modest incremental benefit versus inhaled dual bronchodilators and inhaled corticosteroid combinations. Payer formularies in Europe and the United States align with these guidelines, tightening reimbursement pathways. Introduction of new classes like ensifentrine, approved in 2024 as a first-in-class PDE3/4 inhibitor, further narrows clinical mindshare. Reduced first-line positioning erodes potential prescription volume in mature markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Route of Administration: Oral Dominance Faces Injectable Growth

Oral products contributed 60.98% of global revenue in 2025, reflecting entrenched patient familiarity and streamlined manufacturing economics that favor tablets and extended-release capsules. The segment benefits from robust quality-assured supply networks and straightforward distribution, anchoring the aminophylline market despite periodic shortages in extended-release forms. Hospitals increasingly adopt injectable aminophylline for rapid symptom relief amid acute COPD exacerbations, fuelling a 4.52% CAGR that outpaces the broader aminophylline market. Uptake is most pronounced in emergency departments and NICUs where precise titration and immediate bioavailability are critical. Over the forecast period, technology-driven infusion pumps with integrated serum-level alarms could mitigate toxicity concerns and accelerate intravenous volumes.

Injectable adoption also aligns with the neonatal apnea segment, where prophylactic administration of aminophylline solutions significantly cuts apnea incidence in preterm infants. Broader critical-care infrastructure expansion, especially across Southeast Asia, supports sustained double-digit demand for parenteral formats. Nevertheless, the segment faces cost pressures as sterile-fill requirements raise capital outlays for prospective entrants. Overall, the coexistence of established oral regimens and fast-growing injectables reinforces diversified revenue streams for stakeholders.

By Dosage Form: Tablets Lead While Solutions Accelerate

Tablets generated 54.03% of sales in 2025 due to their portability, dosing familiarity, and low unit manufacturing cost, consolidating their role in chronic maintenance therapy within the aminophylline market. However, solutions are forecast to deliver the strongest growth at 5.67% CAGR to 2031 as nebulization and intravenous care protocols gain traction in pediatric and geriatric cohorts with swallowing difficulties. Pfizer’s long-standing injectable offerings remain widely available, highlighting supply continuity even when other respiratory drugs encounter shortages. The aminophylline market size for solution formats is expected to widen further once point-of-care mixing systems become mainstream in critical-care wards.

Solutions also facilitate outpatient nebulized therapy, allowing physicians to tailor regimens for patients intolerant to inhaled corticosteroids withdrawn from markets in 2024. Although manufacturing complexity remains higher versus solid dosage, premium pricing partly offsets additional overhead. The tablet segment will retain leadership given its cost advantage, yet its share may erode modestly as solution versatility attracts incremental prescribers and caregivers.

By Application: COPD Leadership Challenged by Neonatal Growth

COPD represented 44.78% of overall revenue in 2025, underscoring the prevalence of chronic airway obstruction and the role of methylxanthines as adjunct therapy in severe or refractory cases. The aminophylline market size for COPD is projected to expand steadily, albeit below the overall market CAGR, because guidelines increasingly prioritize long-acting bronchodilator combinations. By contrast, the infant apnea segment is set for 6.55% CAGR on the back of rising NICU coverage and favourable data showing up to 85% efficacy in managing central apnea events. As more tertiary centres upgrade neonatal services, demand for pediatric-grade injectable and oral solutions will climb, partially offsetting stagnation in mild-to-moderate COPD prescribing.

Off-label exploratory uses, including renal protection in birth asphyxia and potential anti-inflammatory effects, are under investigation and could unlock niche revenues. Nonetheless, any expansion beyond respiratory indications will hinge on additional evidence and regulatory review. Asthma remains a mature niche where inhaled alternatives are typically preferred in first-line care, thus contributing stable but limited incremental volume.

By End User: Hospitals Dominant Despite Home-Care Surge

Hospitals accounted for 37.74% of global sales in 2025, anchored by the need for therapeutic drug monitoring and rapid dose adjustment during acute episodes. Institutional buyers value suppliers that can guarantee on-time delivery and supply redundancy, which benefits vertically integrated manufacturers. Home-care demand is expected to rise at 6.28% CAGR as remote monitoring devices capable of fingertip theophylline testing reach commercial scale, easing safety management outside clinical settings. Clinics and ambulatory surgical centres maintain consistent uptake but are constrained by limited laboratory facilities for routine serum checks.

Telehealth integration facilitates virtual follow-up, enabling early dose optimisation that historically required hospital visits. However, reimbursement frameworks in emerging markets still favour inpatient management for high-risk cases, ensuring hospitals remain the prime revenue source. In the medium term, combined advances in diagnostic wearables and value-based care contracts could accelerate patient transition toward community and home settings.

By Distribution Channel: Hospital Pharmacies Lead Online Growth

Hospital pharmacies captured 46.31% of distribution in 2025, reflecting formulary alignment with institutional prescribing and centralised monitoring. Supply agreements emphasise volume discounts and vendor reliability, solidifying the channel’s primacy within the aminophylline market. Online pharmacies, though smaller, are forecast to post 7.44% CAGR as e-commerce penetration and prescription digitalisation broaden access, particularly in chronic disease management scenarios. Enhanced cold-chain and tamper-proof packaging technologies further support direct-to-patient shipments.

Retail pharmacies continue to serve walk-in refills but face competition from vertically integrated health plans that steer members to mail-order services. Persistent therapeutic-drug-monitoring prerequisites limit broad community-pharmacy dispensing, although collaborative practice agreements could gradually close this gap. Ultimately, omnichannel strategies blending hospital, online, and brick-and-mortar outlets will emerge to maximise patient reach while meeting regulatory safeguards.

Geography Analysis

North America retained 37.29% revenue share in 2025, powered by mature reimbursement systems, widespread NICU availability, and established COPD treatment algorithms. Market expansion is tempered by guideline shifts that prioritise inhaled dual therapy, yet domestic manufacturing investments such as AstraZeneca’s USD 50 billion programme through 2030 help safeguard supply continuity. The aminophylline market size for North America is anticipated to increase gradually, supported by tele-health adoption that simplifies drug-level surveillance.

Asia-Pacific is the fastest growing, projected at 6.33% CAGR through 2031, as rising air-pollution-linked morbidity and expanding insurance coverage elevate therapy adoption. Regional API capacity build-outs in China and India ensure competitive pricing, though regulatory headwinds such as data-security legislation may introduce periodic compliance costs. Still, governmental essential-medicine lists and public-sector purchasing underpin sustained volume growth.

Europe’s trajectory remains steady as pharmacoeconomic assessments continue to favour older generics in resource-constrained health systems. However, strict evidence-based formularies constrain first-line use outside severe COPD flares. Middle East & Africa and South America present incremental opportunities where public tenders favour low-cost therapeutics for expanding respiratory programmes. Inclusion of theophylline derivatives on the 2024 WHO Model List of Essential Medicines for Children supports global paediatric adoption. Across developing regions, the aminophylline market benefits from donor-funded capacity building in neonatal and emergency care.

Competitive Landscape

The aminophylline market exhibits moderate concentration, with established generics manufacturers such as Pfizer, Teva, and Hikma holding the largest combined share through integrated API-to-finished-dose operations. These firms leverage global supply redundancy to mitigate raw-material disruptions documented during the 277 active drug shortages reported in late 2024. Competition revolves around cost leadership, regulatory compliance, and delivery reliability rather than formulation innovation, given the molecule’s maturity and narrow therapeutic index.

Strategic moves include Pfizer’s SGD 1 billion API plant in Singapore that broadened regional sourcing resilience and Dr. Reddy’s USD 620 million investment in a Swiss unit to expand sterile injectable capacity. Teva reinforces distribution reach through strategic sNDAs that demonstrate regulatory agility across wider portfolios, indirectly supporting aminophylline brand reputation. On the M&A front, Merck’s USD 10 billion purchase of Verona Pharma underlines sustained big-pharma interest in respiratory therapeutics, potentially heightening competitive intensity over the long term.

Supply-chain digitisation remains a key differentiator. Leading players deploy AI-based predictive analytics to flag impending API shortages, enabling pre-emptive inventory allocation and reinforcing customer trust. Smaller regional firms exploit niche hospital relationships but face rising quality-compliance costs, nudging the market toward gradual consolidation without eliminating multisource competition.

Aminophylline Industry Leaders

Pfizer Inc.

Teva Pharmaceutical Industries Ltd

Hikma Pharmaceuticals PLC

Sandoz AG

Cipla Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: AstraZeneca confirmed plans to construct its largest US manufacturing campus in Virginia within a USD 50 billion expansion programme focused on respiratory medicines.

- July 2024: Pfizer invested SGD 1 billion to add 429,000 sq ft of small-molecule API capacity in Singapore, reinforcing supply for respiratory treatments.

Global Aminophylline Market Report Scope

Aminophylline is a drug combination that contains theophylline and ethylenediamine. It helps to prevent and treat wheezing, shortness of breath and lung diseases. The aminophylline market is segmented By Route of Administration, Applications, and Geography.

| Oral |

| Injection |

| Tablet |

| Solution |

| Extended-release Capsule |

| COPD |

| Asthma |

| Infant Apnea |

| Other Off-label Uses |

| Hospitals |

| Clinics |

| Ambulatory Surgical Centers |

| Home Care Settings |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Route of Administration | Oral | |

| Injection | ||

| By Dosage Form | Tablet | |

| Solution | ||

| Extended-release Capsule | ||

| By Application | COPD | |

| Asthma | ||

| Infant Apnea | ||

| Other Off-label Uses | ||

| By End User | Hospitals | |

| Clinics | ||

| Ambulatory Surgical Centers | ||

| Home Care Settings | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global value of the aminophylline market?

The sector is valued at USD 323.7 million in 2026 with a forecast to reach USD 363.03 million by 2031.

How fast is the aminophylline market expected to grow through 2031?

The market is projected to expand at a CAGR of 2.32% across the 2026-2031 period.

Which dosage form is growing quickest in aminophylline sales?

Solution formulations are expanding at 5.67% CAGR owing to increased hospital and pediatric use.

Why is the Asia-Pacific region important for aminophylline demand?

Asia-Pacific shows the highest CAGR at 6.33% driven by rising COPD prevalence, wider insurance cover, and expanding API production capacity.

What clinical area offers the fastest growth opportunity?

Infant apnea treatments are forecast to grow at 6.55% CAGR due to ongoing global NICU expansion and proven drug efficacy.

Page last updated on: