Paracetamol Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.05 Billion |

| Market Size (2031) | USD 14.93 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

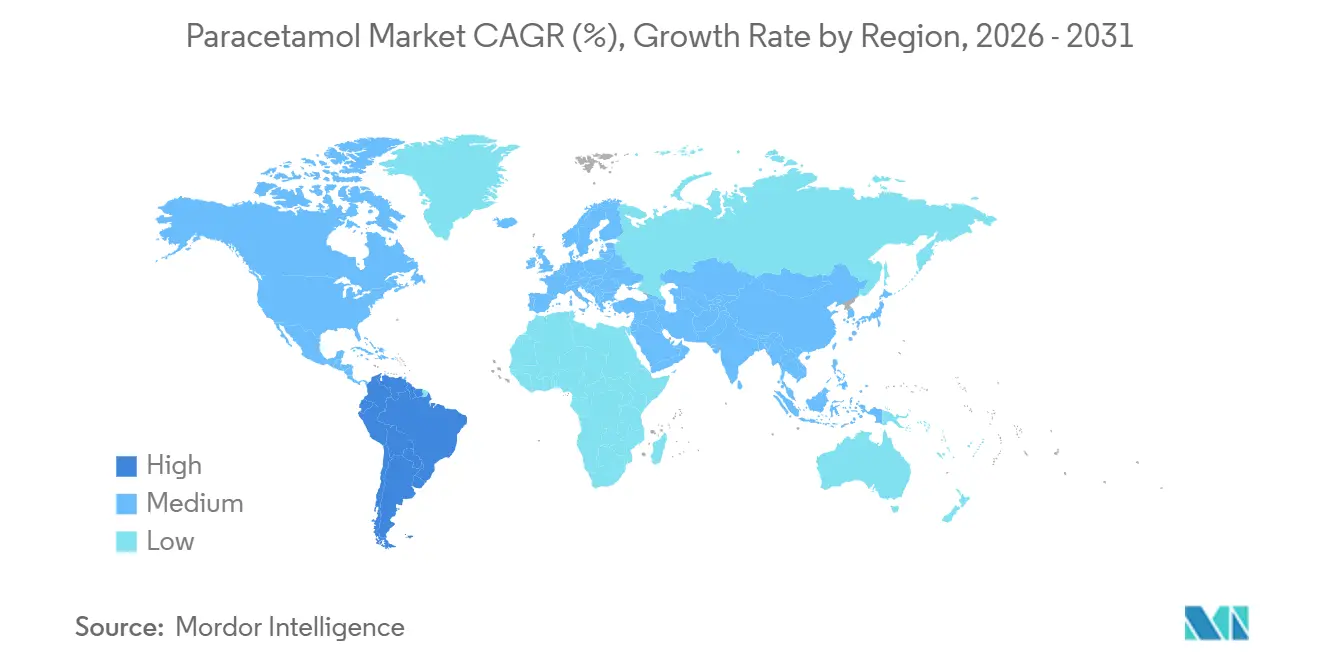

| Fastest Growing Market | Asia Pacific |

| Largest Market | South America |

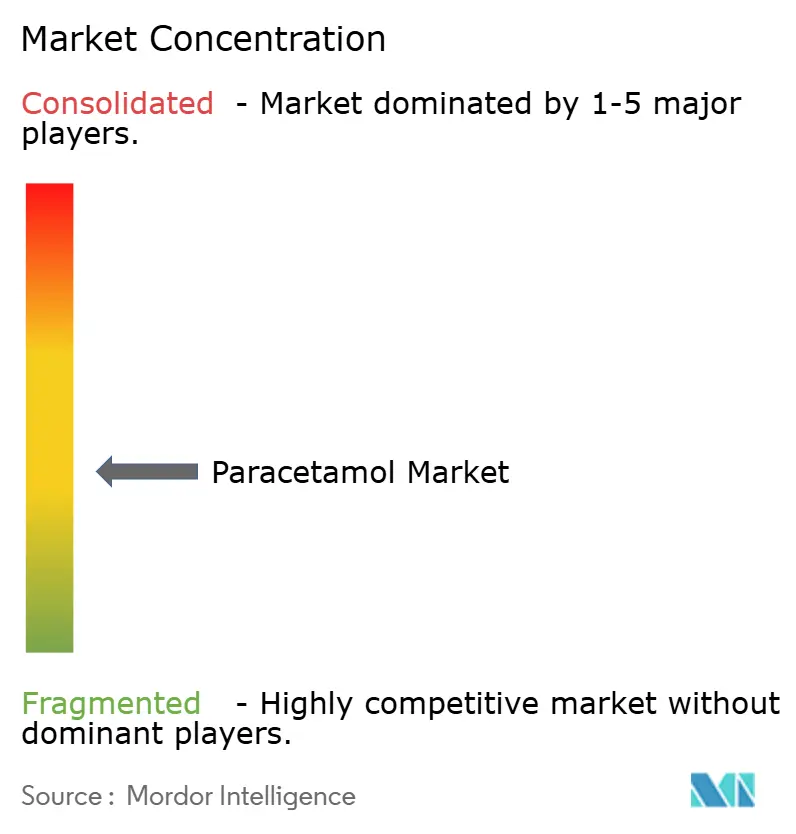

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paracetamol Market Analysis by Mordor Intelligence

The Paracetamol Market size was valued at USD 11.59 billion in 2025 and is estimated to grow from USD 12.05 billion in 2026 to reach USD 14.93 billion by 2031, at a CAGR of 4.38% during the forecast period (2026-2031).

Long-term demand is underpinned by chronic pain prevalence, guideline endorsements that position acetaminophen as the first-line non-opioid therapy, and hospital adoption of intravenous formulations to curb opioid exposure. At the same time, ample generic capacity from Asian API hubs and new European reshoring projects have pushed average bulk-drug prices down more than 70% since the COVID-19 peak, compressing manufacturer margins. Safety regulators are tightening dosing, labeling, and pack-size rules in response to concerns about hepatotoxicity, raising compliance costs but also creating product-differentiation headroom for extended-release and taste-masked innovations. Digital dispensing, particularly e-prescription-enabled pharmacy platforms, continues to redirect volumes away from brick-and-mortar stores, accelerating the paracetamol market’s channel recalibration. Taken together, these countervailing forces produce moderate headline growth yet intense competition for value capture along the supply chain.

Key Report Takeaways

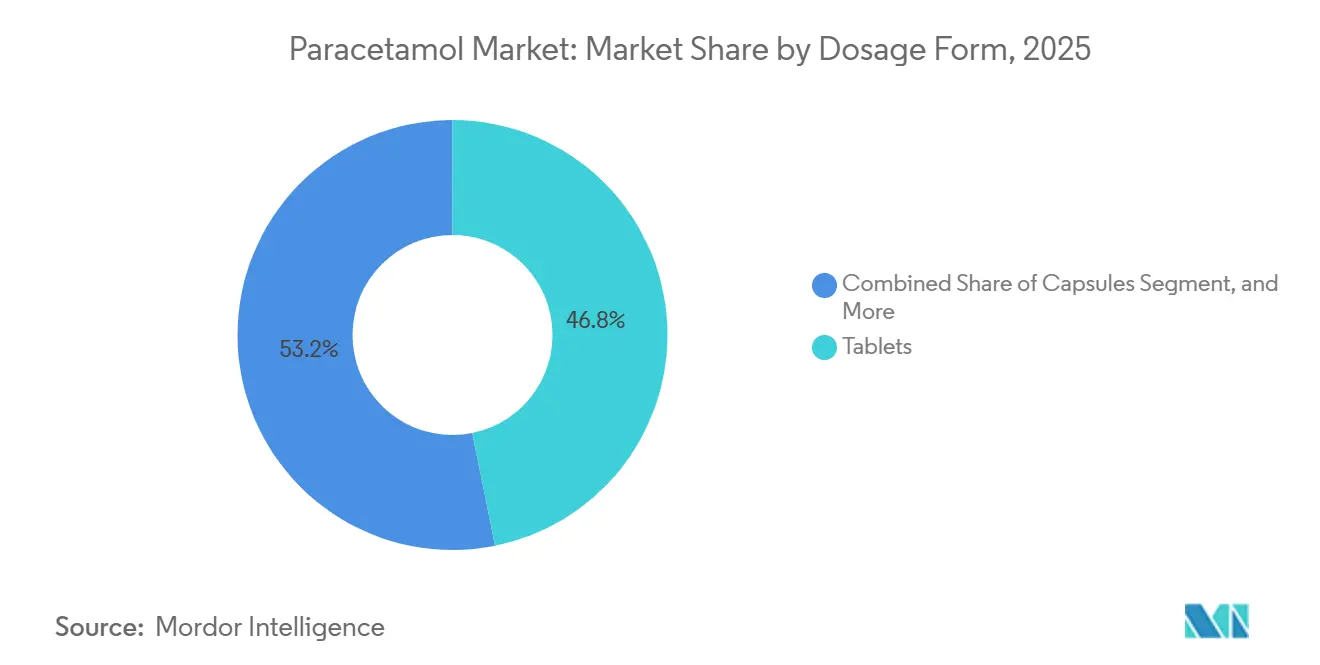

- By dosage form, tablets led with 46.83% of the paracetamol market share in 2025; liquid suspensions are the fastest-growing format, with a 4.86% CAGR through 2031.

- By application, pain management accounted for 39.27% of the paracetamol market in 2025, while fever reduction is advancing at a 6.63% CAGR through 2031.

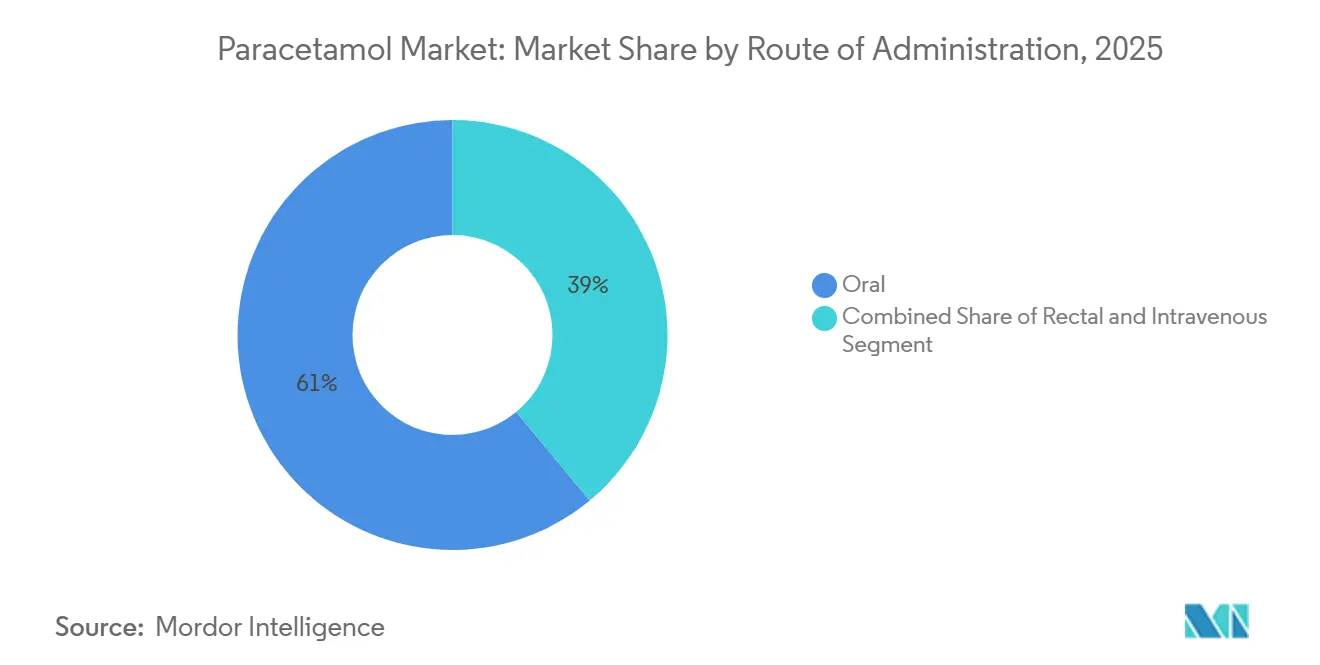

- By route of administration, oral products dominated with 61.02% revenue share in 2025; intravenous paracetamol is recording the highest growth at 5.63% CAGR over the forecast period.

- By distribution channel, retail pharmacies held 28.78% of 2025 revenues, but online pharmacies are set to expand at a 5.79% CAGR on the back of mandatory e-prescription rollouts across major European markets.

- By geography, North America commanded 34.12% 2025 sales, whereas Asia-Pacific is projected to post the strongest regional CAGR of 7.76% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Paracetamol Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Pain- & Fever-Related Disorders | +0.7% | Global, most acute in aging North America and urbanizing Asia-Pacific | Medium term (2-4 years) |

| OTC Self-Medication Boom & Retail Channel Expansion | +0.8% | Global, led by e-prescription rollouts in Europe and direct-to-consumer services in North America | Short term (≤ 2 years) |

| Capacity Expansion of API & Finished-Dose Plants | +0.5% | Europe (France), India (production-linked incentives) | Long term (≥ 4 years) |

| Extended/Rapid-Release Formulation Innovation | +0.4% | North America and Europe premium OTC segments | Medium term (2-4 years) |

| Opioid-Sparing Surgical Protocols Driving IV Uptake | +0.6% | North America and Europe hospital formularies, emerging in GCC hospitals | Medium term (2-4 years) |

| Green-Chemistry Incentives & API Re-Shoring | +0.3% | Europe (ECHA mandates), United States onshoring subsidies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Pain- & Fever-Related Disorders

The updated CDC guideline explicitly lists acetaminophen before NSAIDs or opioids, reinforcing the paracetamol market’s clinical relevance. Pediatric vaccination programs add episodic demand because acetaminophen remains the recommended antipyretic for post-injection symptoms.[1]Centers for Disease Control and Prevention, “CDC Clinical Practice Guideline for Prescribing Opioids,” cdc.gov As global life expectancy rises, osteoarthritis, cancer pain, and post-operative recovery drive sustained baseline volumes. Although unit sales grow, profit capture depends on navigating private-label competition and insurer step-therapy policies that favor low-cost generics.

OTC Self-Medication Boom & Retail Channel Expansion

Regulatory moves that enable pharmacists to initiate therapy, such as England’s Pharmacy First program launched in 2024, have generated millions of reimbursed consultations, often resulting in over-the-counter analgesic recommendations.[2]National Institute for Health and Care Excellence, “Intravenous Paracetamol for Acute Pain,” nice.org.uk Simultaneously, Germany’s nationwide e-prescription system, fully enforced in 2024, has expanded the addressable online pharmacy audience, boosting basket sizes for household OTC staples. U.S. retailers capitalize on loyalty data to place targeted digital offers, steering shoppers toward exclusive-label acetaminophen ranges. These dynamics expand the paracetamol market’s non-prescription footprint, even as traditional drugstores confront foot traffic leakage.

Capacity Expansion of API & Finished-Dose Plants

Seqens broke ground on a 10,000-ton-per-year acetaminophen facility in France in December 2025, the largest Western investment in the molecule for more than two decades. India’s production-linked incentive (PLI) program, meanwhile, subsidizes backward integration, funding zero-liquid-discharge plants that meet European import standards. These projects diversify supply away from China, which currently delivers about 70% of global volume, and help governments secure critical medicine stockpiles. Accelerated approval pathways such as the U.S. FDA’s PreCheck, unveiled in 2025, further shorten construction-to-qualification timelines.

Extended/Rapid-Release Formulation Innovation

Hydroxypropyl methylcellulose matrices and Eudragit coatings maintain therapeutic plasma levels for up to 12 hours, enabling twice-daily dosing in chronic indications. Taste-masking breakthroughs such as chitosan-coated alginate beads achieving 99% encapsulation efficiency have reinvigorated pediatric suspensions, a sub-segment growing faster than the overall paracetamol market. Brands price these technologies at a 40-60% premium over immediate-release generics, cushioning margin declines from commodity tablets. Patent estates around bilayer architecture and gastro-retentive systems also extend exclusivity windows in otherwise crowded OTC aisles.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hepatotoxicity/Over-Dose Safety Tightening | -0.5% | Australia, United Kingdom, United States | Short term (≤ 2 years) |

| Intense Generic Price Competition | -0.7% | North America and Europe retail segments | Short term (≤ 2 years) |

| API Supply-Chain Concentration & Tariff Risk | -0.4% | Global importers dependent on China | Medium term (2-4 years) |

| Pack-Size Restrictions Curbing Consumption | -0.3% | Australia (in force), potential EU adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hepatotoxicity/Over-Dose Safety Tightening

Australia limited non-prescription pack sizes in February 2025 after averaging 225 hospitalizations and 50 overdose deaths per year, mirroring earlier U.K. curbs.[3]Therapeutic Goods Administration, “Final Decisions on Paracetamol Scheduling Amendment,” tga.gov.au The U.S. FDA’s June 2024 proposed order for OTC analgesics addresses pediatric dosing and life-threatening skin reactions, with a final rule expected by late 2025. Implementation will force relabeling and could discourage high-strength formats. Litigation over potential neuro-developmental effects during pregnancy is adding further reputational risk for leading brands.

Intense Generic Price Competition

Spot API quotes in India fell from INR 900 per kg during the pandemic to INR 250 in 2024, a 72% drop that filtered through to finished-dose bids in the United States’ federal supply schedules. Mallinckrodt’s Q3 2024 acetaminophen revenue shrank 30.3% year-on-year to USD 40 million, underscoring the down-cycle. Private-label substitution by large retail chains piles additional pressure on branded OTC players, accelerating consolidation among smaller formulators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Form: Tablets Continue to Lead While Liquids Accelerate

Tablets held 46.83% of the paracetamol market share in 2025, reflecting consumer familiarity, a mechanically stable shelf life, and low unit costs. Liquids, however, registered the highest forecast CAGR at 4.86% through 2031, propelled by pediatric dosing needs and advanced taste-masking science that now achieves 99% encapsulation efficiency. Extended-release bilayer tablets priced at a median 45% premium over immediate-release lines defend retailer margins in mature Western markets, though cost sensitivity in emerging economies still favors plain generics.

Green-chemistry manufacturing routes such as solvent-free ball-mill acetylation yield up to 96% conversion while trimming Scope 3 emissions, a feature increasingly cited in European tenders. As retailers expand their private-label offerings, formulators that can supply both commodity tablets and value-added liquids are best positioned to balance volume with profitability. Premium chewable and fast-dissolving variants also attract adult consumers seeking convenience, further widening the paracetamol market.

By Application: Pain Management Dominates; Fever Reduction Rises Fast

Pain management contributed 39.27% of the 2025 value, anchored by 50 million U.S. chronic-pain sufferers and similar prevalence patterns across Europe and Japan. Fever-reduction therapies, though smaller, are slated to grow 6.63% annually, buoyed by vaccine-related prophylaxis and rising pharmacy-administered immunizations. Cold-and-flu combination SKUs bundle acetaminophen with decongestants or antihistamines, capturing incremental share in winter seasons and driving basket upselling.

Higher frequency of point-of-care testing at community pharmacies channels symptomatic patients directly into OTC purchase pathways. Yet, possible pack-size caps and safety labeling expansions could blunt fever-related volume upside, a factor the paracetamol industry must monitor when planning capacity.

By Route of Administration: Oral Rules; IV Gains in Hospitals

Oral formats accounted for 61.02% of 2025 sales, thanks to their ease of self-administration and broad OTC availability. Intravenous paracetamol, currently small in absolute dollars, is projected to advance 5.63% annually on hospital adoption of opioid-sparing protocols. Rectal suppositories retain niche roles where oral intake is contraindicated.

Expanded generic competition has already reduced the average U.S. wholesale-acquisition cost of IV acetaminophen by roughly 25% since 2024. Nevertheless, formulary committees still value its distinct pharmacokinetic profile for immediate postoperative pain. These opposing price-volume dynamics imply steady, rather than explosive, revenue growth for IV suppliers.

By Distribution Channel: Physical Pharmacies Hold Lead but Online Surges

Retail pharmacies captured 28.78% of 2025 global value, leveraging front-of-store promotions and pharmacist counseling. Online pharmacies, boosted by nationwide e-prescription mandates in Germany and ongoing telehealth adoption in the United States, are on a 5.79% growth trajectory. Hospital pharmacies remain essential for IV-dose throughput, while emerging automated-dispensing kiosks may capture incremental convenience-driven transactions in urban Asia.

For branded OTC players, shifting promotional spend toward digital retail media and search optimization becomes critical for maintaining visibility as storefront traffic fragments. The paracetamol market is thus migrating toward a hybrid omnichannel equilibrium.

Geography Analysis

North America accounted for 34.12% of 2025 revenue, underpinned by entrenched OTC infrastructures and extensive hospital formularies that include intravenous acetaminophen. FDA’s forthcoming monograph amendments will likely raise labeling costs but are not expected to materially impede volume. Consolidation is underway as Kimberly-Clark moves to acquire Kenvue for USD 48.7 billion, signaling the strategic value of heritage brands despite litigation noise. API self-sufficiency remains low, making the region sensitive to tariff turbulence and Chinese output fluctuations.

Europe features robust regulatory oversight and rapidly expanding online dispensing channels. Germany’s full e-prescription rollout in 2024 immediately lifted electronic pharmacy turnover, illustrating latent demand for digital convenience. France’s 10,000-ton Seqens plant, scheduled to be fully online by end-2025, exemplifies the bloc’s bid to cut API import exposure. Environmental standards are tightening, with ECHA’s 2025 priority list foreshadowing possible discharge-limit legislation for paracetamol waste streams.

Asia-Pacific is the fastest-growing region, with a 7.76% CAGR, driven by large populations, improving insurance coverage, and government generic-medicine schemes. India alone operates 8,787 Janaushadhi stores that retail low-cost paracetamol nationwide. The India-U.K. Free Trade Agreement, which entered into force in July 2025, eliminated tariffs on 99% of pharma exports, opening a premium European market for Indian producers. China remains the dominant API exporter, while its domestic consumption benefits from Healthy China 2030's preventive-care priorities.

The Middle East & Africa show divergent patterns: GCC states localize drug manufacturing under mandatory insurance expansion, while Sub-Saharan countries rely on donor-funded procurement. South America grapples with currency volatility, yet Brazil’s public-sector programs secure a baseline for essential analgesics. Overall, emerging markets collectively provide the paracetamol market with double-digit growth headroom despite pricing constraints.

Competitive Landscape

The paracetamol market remains fragmented, with more than 40 meaningful API makers and hundreds of finished-dose licensees worldwide. Chinese suppliers deliver roughly 70% of bulk output, leveraging coal-based phenol-acetone routes to retain scale cost advantages. India, boosted by PLI incentives, is rising as an alternative source, although raw-material imports still link its cost base to China.

Seqens’ French project exemplifies Western governments’ drive for strategic autonomy even at higher ex-works prices. Mallinckrodt’s U.S. facility, the only domestic API plant, continues to face under-utilization, and 2024 sales fell 30.3% year-on-year. Downstream, Kimberly-Clark’s pending purchase of Kenvue consolidates trademark heft and OTC shelf space, potentially boosting its bargaining power with retailers. Innovators focus on extended-release technology and sugar-free pediatric lines to command price premiums, while private labels push unit economies of scale. Sustainability credentials, such as low solvent use, zero-liquid discharge, and renewable energy, are emerging as a new yardstick in European tenders, favoring early adopters of green chemistry.

Paracetamol Industry Leaders

GlaxoSmithKline plc

Mallinckrodt Pharmaceuticals

Sun Pharmaceutical Industries Ltd.

Teva Pharmaceuticals, Inc.

Sanofi SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The Federal Register listed withdrawal of approval for 39 NDAs including Ofirmev (acetaminophen) 1000 mg/100 mL, underscoring regulatory compliance imperatives

- February 2025: Australia enacted new paracetamol pack-size limits, restricting non-pharmacy retail to 16 tablets and pharmacy sales to 50 tablets without pharmacist oversight.

Global Paracetamol Market Report Scope

As per the scope of the report, paracetamol is the most widely used analgesic and antipyretic that relieves pain and reduces fever.

The Paracetamol Market Report is Segmented by Dosage Form (Tablets, Capsules, Liquid Suspensions, Powders & Granules), Application (Pain Management, Fever Reduction, Cold & Flu, Others), Route of Administration (Oral, Rectal, Intravenous), Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Tablets |

| Capsules |

| Liquid Suspensions |

| Powders & Granules |

| Pain Management |

| Fever Reduction |

| Cold & Flu |

| Others (Dental, Post-operative, etc.) |

| Oral |

| Rectal |

| Intravenous |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Dosage Form | Tablets | |

| Capsules | ||

| Liquid Suspensions | ||

| Powders & Granules | ||

| By Application | Pain Management | |

| Fever Reduction | ||

| Cold & Flu | ||

| Others (Dental, Post-operative, etc.) | ||

| By Route of Administration | Oral | |

| Rectal | ||

| Intravenous | ||

| By Distribution Channel | Retail Pharmacies | |

| Hospital Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the paracetamol market be by 2031?

It is forecast to reach USD 14.93 billion by 2031, growing at a 4.38% CAGR from 2026.

Which dosage form is growing fastest?

Liquid suspensions are expected to expand at a 4.86% CAGR through 2031, driven by pediatric demand and advanced taste-masking.

Why is intravenous paracetamol gaining usage?

Multimodal surgical guidelines show it can cut opioid consumption by about 30% in the first four hours post-procedure.

What impact do pack-size limits have on sales?

Australia’s 2025 restriction is expected to trim unit volumes, and similar rules under review in Europe could modestly dampen per-capita consumption.

How are environmental rules shaping production?

ECHA’s 2025 assessment of paracetamol metabolites encourages solvent-free and zero-liquid-discharge technologies, influencing API plant design in Europe.

Page last updated on: