Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

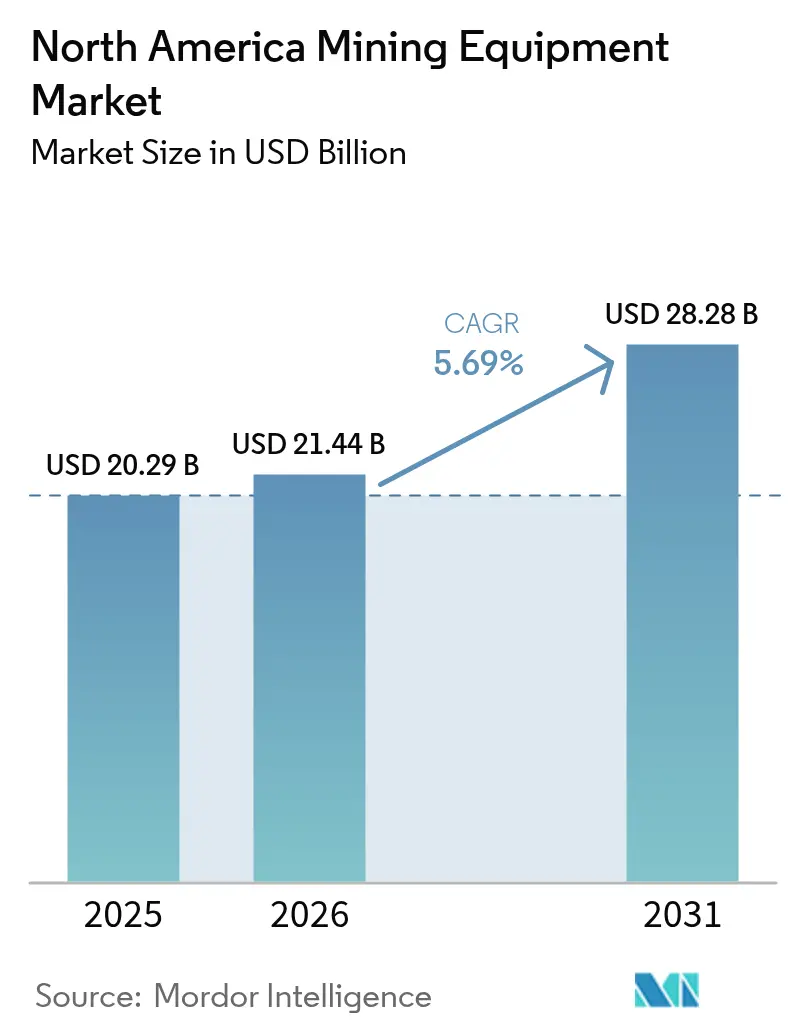

| Base Year Market Size (2025) | USD 20.29 Billion |

| Market Size (2026) | USD 21.44 Billion |

| Market Size (2031) | USD 28.28 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Mining Equipment Market Analysis by Mordor Intelligence

The North America mining equipment market size is projected to expand from USD 20.29 billion in 2025 and USD 21.44 billion in 2026 to USD 28.28 billion by 2031, registering a CAGR of 5.69% between 2026 and 2031. Several structural forces are driving this trend. Operators are focusing on battery-electric and hybrid fleets to meet Scope 3 emissions targets and reduce ventilation costs. Thanks to incentives from the Inflation Reduction Act, significant capital has been directed toward critical minerals exploration, boosting equipment demand even amid fluctuating commodity prices. At the same time, the global tally of autonomous haulage systems has increased, leading to notable improvements in fleet utilization and extended equipment lifespans. While spending still leans heavily on surface assets, there's a noteworthy shift: mineral-processing platforms, bolstered by AI-driven energy savings, are reaping a larger slice of the investment pie. Collectively, these trends ensure the North American mining equipment market continues its upward trajectory, undeterred by the ebb and flow of end-market metal prices.

Key Report Takeaways

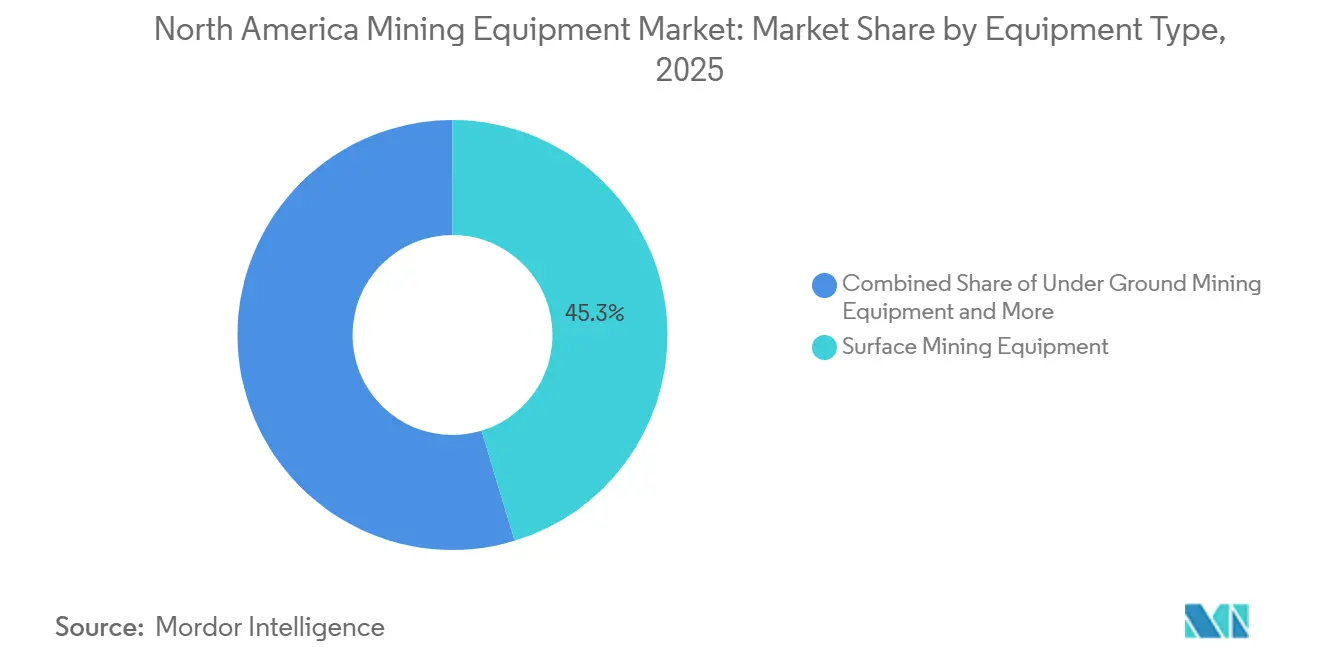

- By equipment type, surface mining assets led with 45.33% of the North America mining equipment market share in 2025, yet mineral-processing platforms are forecast to advance at a 6.18% CAGR through 2031.

- By power source, diesel held a 75.45% share of the North American mining equipment market in 2025, while battery-electric fleets are expanding at an 8.81% CAGR through 2031.

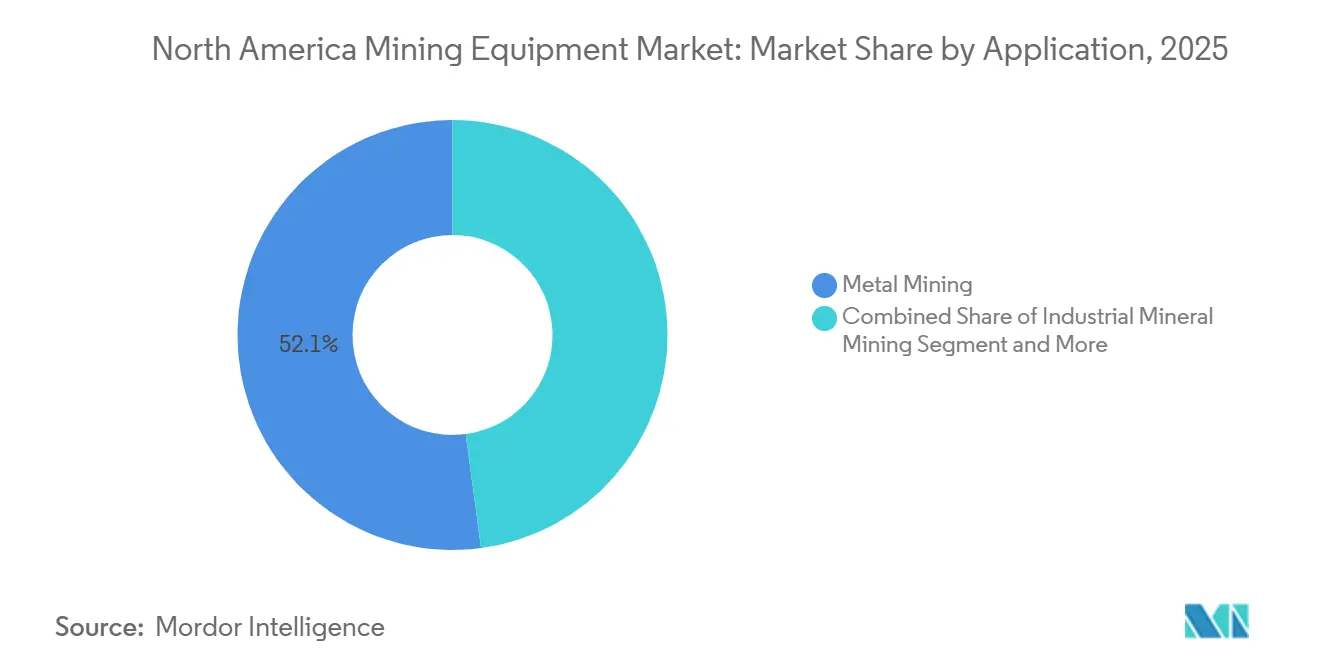

- By application, metal mining accounted for 52.12% revenue share in 2025, and industrial mineral operations accounted for 6.21% CAGR growth.

- By ownership model, new equipment sales accounted for 76.38% revenue share in 2025, and rental and leasing posted an 8.23% CAGR through 2031.

- By geography, the United States accounted for 80.82% revenue share in 2025, and Canada is forecast to grow at an 8.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Mining Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification of Mine Fleets | +1.2% | North America (early adoption in Canada) | Medium term (2-4 years) |

| Demand for Critical Minerals for Energy Transition | +1.1% | North America and EU | Long term (≥ 4 years) |

| Automation and Digital-Mine Transition | +0.9% | Global (U.S. and Canada lead) | Long term (≥ 4 years) |

| Replacement Cycle of Aging Machinery | +0.8% | Global (higher in mature regions) | Short term (≤ 2 years) |

| United States IRA-Linked Exploration Capex Surge | +0.7% | United States (spillover to Mexico) | Short term (≤ 2 years) |

| Ultra-Low-Ground-Pressure Equipment for Arctic Sites | +0.3% | Northern Canada and Alaska | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrification of Mine Fleets

Battery-electric underground loaders and trucks are revolutionizing cost structures by reducing ventilation power needs, which can consume a significant portion of an underground mine's energy budget. Epiroc's battery lineup, set to be deployed by Hudbay at the Lalor site, is projected to slash operating ventilation costs and enable deeper mining operations, previously limited by diesel exhaust constraints[1]“Battery-Electric Equipment Portfolio,”, Epiroc AB, epiroc.com. While surface adoption is slower—due to trolley-assist costs that limit commercial viability to ultra-high-throughput pits—regulatory momentum is gaining traction. British Columbia mandates battery-electric or hydrogen powertrains at new underground sites. This push has spurred OEMs to invest in one-megawatt mobile chargers, capable of recharging a substantial portion of a vehicle's capacity in a short time.

Automation and Digital-Mine Transition

Global deployments of autonomous haulage units by Caterpillar and Komatsu have grown significantly, and after fully adopting MineStar Command, Nevada Gold Mines reported higher truck utilization and reduced tire wear. Meanwhile, Sandvik's AutoMine stations enable a single operator to control multiple underground machines from surface control rooms, achieving a notable reduction in labor costs at KGHM's Morrison pilot. Predictive maintenance tools like Komtrax, which monitor thousands of machine parameters, have successfully reduced unplanned downtime across North American fleets, thereby avoiding substantial annual production losses at each mine. Digital twins synthesize data from drilling, haulage, and processing in real-time, enabling a reduction in unplanned downtime through predictive maintenance analytics.

Demand for Critical Minerals for Energy Transition

As decarbonization efforts ramp up, projects centered on lithium, copper, nickel, and rare-earth elements are leading the charge in new equipment orders. Lithium Americas is set to roll out rotary kilns and high-pressure grinding rolls at its Thacker Pass development, aiming to significantly increase lithium carbonate processing capacity. This move signals the onset of a substantial pipeline for processing equipment. Meanwhile, the Salton Sea's geothermal-lithium venture is turning to brine-handling and crystallization systems, which lie outside the traditional portfolios of OEMs, thereby expanding the overall demand. In Arizona, a looming copper shortfall has spurred brownfield expansions, leading to orders for ultra-class haul trucks. Additionally, Weir’s ESCO division reported a notable surge in bookings for wear parts for critical mineral plants.

United States IRA-Linked Exploration Capex Surge

Due to Section 45X (Advanced Manufacturing Production Credit) and Section 48C (Qualifying Advanced Energy Project Credit), the U.S. has seen a surge in critical-mineral projects, significantly increasing their market share [2]“45X and 48C Project Tracker,”, U.S. Department of Energy, energy.gov. This growth comes with a notable boost in exploration and processing spending, projected to grow at a substantial CAGR. In a noteworthy move, Albemarle has revived its Kings Mountain lithium mine, eyeing potential credits that could significantly impact its operations. This revival means the mine will now operate with multiple haul trucks, excavators, and a newly added concentrator line. Furthermore, recent Treasury guidance has opened doors for refurbished assets to qualify, leading to a spike in demand for certified rebuild programs from industry giants Caterpillar and Komatsu, which offer significant discounts on purchase prices.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Metals-Price Volatility Impacting Capex Plans | -0.6% | Global (higher in commodity-dependent areas) | Short term (≤ 2 years) |

| High Upfront Equipment Costs & Financing Gaps | -0.5% | North America (small operators) | Short term (≤ 2 years) |

| Stringent Emission and Safety Regulations | -0.4% | North America (varied by state/province) | Medium term (2-4 years) |

| Grid-Permitting Bottlenecks for Electrified Mines | -0.3% | United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Metals-Price Volatility Impacting Capex Plans

In recent times, lithium carbonate prices have significantly declined from their previous highs, settling at much lower levels. Concurrently, nickel, cobalt, and graphite prices have also declined sharply. These market fluctuations have led to a deferral of substantial expansion budgets for North American mines. Additionally, there has been a noticeable contraction in the demand for ultra-class trucks and large excavators. In response to the market's volatility, operators have begun segmenting their fleet orders into smaller tranches, often with short-term options. This strategy not only preserved their flexibility but also led to higher unit prices for OEMs. Furthermore, this trend has contributed to significant growth in the equipment rental and leasing sector, which is increasingly favored for its lower monthly operating costs compared to hefty upfront capital expenditures.

Grid-Permitting Bottlenecks for High-Power Electrified Mines

Battery-electric surface fleets are in dire need of significant interconnections. According to NERC’s FAQ, average queue times are significantly longer in both the WECC and ERCOT territories[3]Federal Energy Regulatory Commission, “Generator Interconnection Reform 2024,” ferc.gov. This effectively pushes the timeline for full-electric open-pit haulage further into the future. A case in point is Thacker Pass, which faced an extended wait to secure new capacity. The capital expenditure for a stand-alone substation, coupled with a line, can represent a substantial portion of a midsize mine’s budget. Although FERC’s reform aims to trim these queues, tangible relief is not anticipated in the near term. As a result, there's a pressing need for interim investments in diesel-hybrid trucks and on-site solar-plus-storage microgrids.

Segment Analysis

By Equipment Type: Processing Platforms Outpace Extraction Assets

In contrast, surface fleets—still 45.33% of 2025 revenue—advance at a slower 5.1% as autonomous retrofits defer replacement buys. Mineral-processing systems are forecast to grow 6.18% annually, outshining the broader North America mining equipment market by almost half a percentage point. AI-driven comminution, along with high-pressure grinding rolls and vertical roller mills, significantly slashes energy consumption. This efficiency not only promises robust returns but also shifts capital focus from the pit to the plant. FLSmidth secured substantial North American orders for its Planet Positive line, predominantly from copper and lithium clients.

Battery-electric technology is propelling underground machinery, leading to steady growth. Epiroc’s ST18 Battery loader, boasting extended runtimes and a high payload, is particularly favored by Canadian hard-rock mines grappling with depth-induced heat challenges. Meanwhile, drills and breakers experience growth, driven by demand for super-large blasthole rigs like Epiroc’s Pit Viper 275. Support equipment, encompassing graders and water carts, sees a rise. In contrast, specialized tools for Arctic conditions and narrow veins enjoy growth, fueled by a surge in northern exploration.

Note: Segment shares of all individual segments available upon report purchase

By Power Source: Electric Platforms Gain Despite Grid Constraints

Diesel retained 75.45% of the North America mining equipment market share in 2025, yet battery-electric units are on an 8.81% trajectory to 2031. Hudbay's Lalor order highlights the crucial role of ventilation in underground operations, emphasizing its economic significance in ensuring operational efficiency and worker safety.

Meanwhile, surface conversions face challenges due to the high costs of trolley infrastructure, which can hinder broader adoption despite their potential benefits. Komatsu's hybrid model, the PC7000-11, successfully balances significant fuel savings with stable grid demand, paving the way for the growth of hybrid models in the mining industry. The Tier 4 Final after-treatment, which comes at an added cost for larger trucks, now enjoys near-perfect uptime. This leap forward enables fleets to meet stringent air-quality standards, even as conventional electric vehicles continue to advance to enhance performance and adoption rates.

By Application: Industrial Minerals Outpace Metals

Metal mining still accounted for 52.12% of 2025 revenue, with copper hubs in Arizona and Nevada ordering ultra-class haul trucks to support incremental capacity debottlenecking. Industrial-mineral operations notch a 6.21% CAGR due to lithium-brine, potash, and phosphate projects that need novel pumps, crystallizers, and solution-mining equipment.

Thacker Pass secured a pivotal agreement with FLSmidth, centering on acid-leach and rotary-kiln technology. This partnership is expected to enhance operational efficiency and support the development of advanced processing solutions. As the Powder River Basin witnesses a yearly drop in coal equipment demand, machinery for aggregates is on the rise, buoyed by the Infrastructure Investment and Jobs Act, which aims to modernize infrastructure and stimulate economic growth.

Note: Segment shares of all individual segments available upon report purchase

By Ownership Model: Rental Model Advances

New equipment commanded 76.38% of 2025 spending but is pacing growth, while rental and leasing accounted for 8.23%. United Rentals and Herc Rentals increased mining fleets by more than a certain percentage to satisfy short-life project demand. Certified rebuild programs propel a rise in refurbished assets after Treasury confirmed credit eligibility under Section 48C. A rebuilt 400-tonne truck at a lower cost than a new one extends machine life significantly and keeps the North American mining equipment market expanding amid tighter capital budgets.

Geography Analysis

The United States held 80.82% of the North American mining equipment market in 2025, supported by USD 133 billion in announced Inflation Reduction Act (IRA)-linked manufacturing investments that drive upstream machinery demand. Nevertheless, Canada is set to outperform, with an 8.52% CAGR through 2031, as Ottawa earmarks CAD 195 million (USD 145 million) for critical-mineral infrastructure upgrades. British Columbia’s Golden Triangle saw CAD 265 million (USD 197 million) channeled into roads and power lines in 2025 alone, streamlining equipment logistics to remote sites.

Federal tax incentives and Indigenous partnership frameworks shorten project-approval timelines relative to the United States, creating earlier equipment deployment windows. OEMs have consequently expanded parts depots in Sudbury and Vancouver to cut lead times. Mexico remains a smaller slice of the North American mining equipment market, hampered by tariff uncertainty. Yet silver and copper operations maintain baseline demand for replacement parts and rental units.

In North America, Mexico faces equipment-supply headwinds tied to proposed 25% tariffs on United States imports. Mining companies invest in localized maintenance shops and training programs to mitigate cross-border disruptions. Silver miners in Zacatecas and copper producers in Sonora remain steady purchasers of high-capacity cone crushers and leach pad irrigation systems, albeit with longer replacement cycles. OEMs are hedging by stocking parts at Laredo and Manzanillo to ensure service continuity and maintain the region’s relevance to the broader North American mining equipment market.

Competitive Landscape

Caterpillar and Komatsu dominate the surface-fleet market, leveraging proprietary autonomy ecosystems that impose significant switching costs per site. Meanwhile, Liebherr, Epiroc, and Sandvik lead battery-electric underground fleets, securing exclusive long-term deals. A notable example is Epiroc's contract with Hudbay, which underscores this trend. SANY's recent launch undercut incumbents on price, prompting major companies to emphasize certified rebuilds. These rebuilds protect service margins but compress profitability on new machines. Deere's integration of Wirtgen has reduced customer-acquisition costs in aggregates, showcasing cross-sell leverage. Innovation remains a key driver: Caterpillar's patent for trolley-assist energy recovery aims to accelerate charging, while Weir's wear-parts division is scaling rapidly amid rising demand for critical minerals. The North American mining equipment market remains both competitive and dynamic. While there's a dominant presence in ultra-class haulage, the landscape is fragmented in areas like electrification and processing.

Today's competitive edge hinges on total cost of ownership packages. These packages seamlessly integrate autonomous haulage, predictive maintenance analytics, and lifecycle financing. Start-ups specializing in AI-driven ore sorting and swappable-battery platforms are forging partnerships with established players to leverage their manufacturing scale. A case in point is Caterpillar's alliance with IMA Engineering, in which it is embedding sensor-based material classification into Caterpillar's Precision Mining ecosystem. This move underscores a broader industry shift towards holistic integrated solutions, moving away from mere incremental hardware upgrades.

Regulatory mandates, especially those related to diesel emissions and battery safety, create hurdles. These hurdles tend to benefit established players, who boast robust engineering and certification capabilities. Concurrently, rental giants like Sunbelt Rentals and United Rentals are emerging as pivotal buyers. They're striking fleet-wide agreements, thereby influencing pricing dynamics. Suppliers who can pivot to these changing procurement trends and offer interoperable charging or autonomy standards stand to gain a larger foothold in the North American mining equipment landscape.

North America Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Epiroc AB

Sandvik AB

Liebherr Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Sandvik introduced its next-generation bolter miner, the Sandvik MB672, for longwall mining in Canada. This new model features advanced bolting technologies designed to improve productivity, enhance operator safety and ergonomics, and minimize total ownership costs.

- April 2025: Sandvik secured a SEK 750 million (USD 71 million) contract to deliver advanced battery-electric vehicles to South32 for its Hermosa project in Arizona. Deliveries are scheduled between 2026 and 2030, marking a significant step toward sustainable mining practices and transforming the mining landscape.

North America Mining Equipment Market Report Scope

The North American mining equipment market is segmented by equipment type (surface mining equipment, underground mining equipment, mineral processing equipment, and more), power source (diesel, electric, and hybrid), application (metal mining, industrial mineral mining, and more), ownership model (new equipment sales, rental/leasing, and more), and by country. The market forecasts are provided in terms of value (USD).

By Equipment Type

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills, Breakers & Crushing Tools |

| Support & Ancillary Equipment |

| Other Specialized Equipment |

By Power Source

| Diesel |

| Electric |

| Hybrid |

By Application

| Metal Mining |

| Industrial Mineral Mining |

| Coal Mining |

| Aggregates & Quarrying |

| Others |

By Ownership Model

| New Equipment Sales |

| Rental & Leasing |

| Refurbished/Rebuilt Equipment |

By Country

| United States |

| Canada |

| Rest of North America |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills, Breakers & Crushing Tools | |

| Support & Ancillary Equipment | |

| Other Specialized Equipment | |

| By Power Source | Diesel |

| Electric | |

| Hybrid | |

| By Application | Metal Mining |

| Industrial Mineral Mining | |

| Coal Mining | |

| Aggregates & Quarrying | |

| Others | |

| By Ownership Model | New Equipment Sales |

| Rental & Leasing | |

| Refurbished/Rebuilt Equipment | |

| By Country | United States |

| Canada | |

| Rest of North America |

Key Questions Answered in the Report

What is the projected size of the North America mining equipment sector by 2031?

The North America mining equipment market size is forecast to reach USD 28.28 billion by 2031.

How fast are battery-electric mining fleets growing in the region?

Battery-electric platforms are expanding at an 8.81% CAGR through 2031, triple the overall market pace.

Which country is expected to record the highest growth rate?

Canada is set to grow at an 8.52% CAGR thanks to electrification mandates and critical-mineral investments.

Which equipment categories are seeing the fastest adoption of AI solutions?

Mineral-processing units such as high-pressure grinding rolls and flotation cells are integrating AI to cut energy and reagent use by double-digit percentages.

What is the main obstacle to widespread surface-fleet electrification?

Lengthy grid-connection queues—often 10 years or more—delay the power infrastructure needed for high-load battery-electric haulage.

Page last updated on: