Track Laying Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

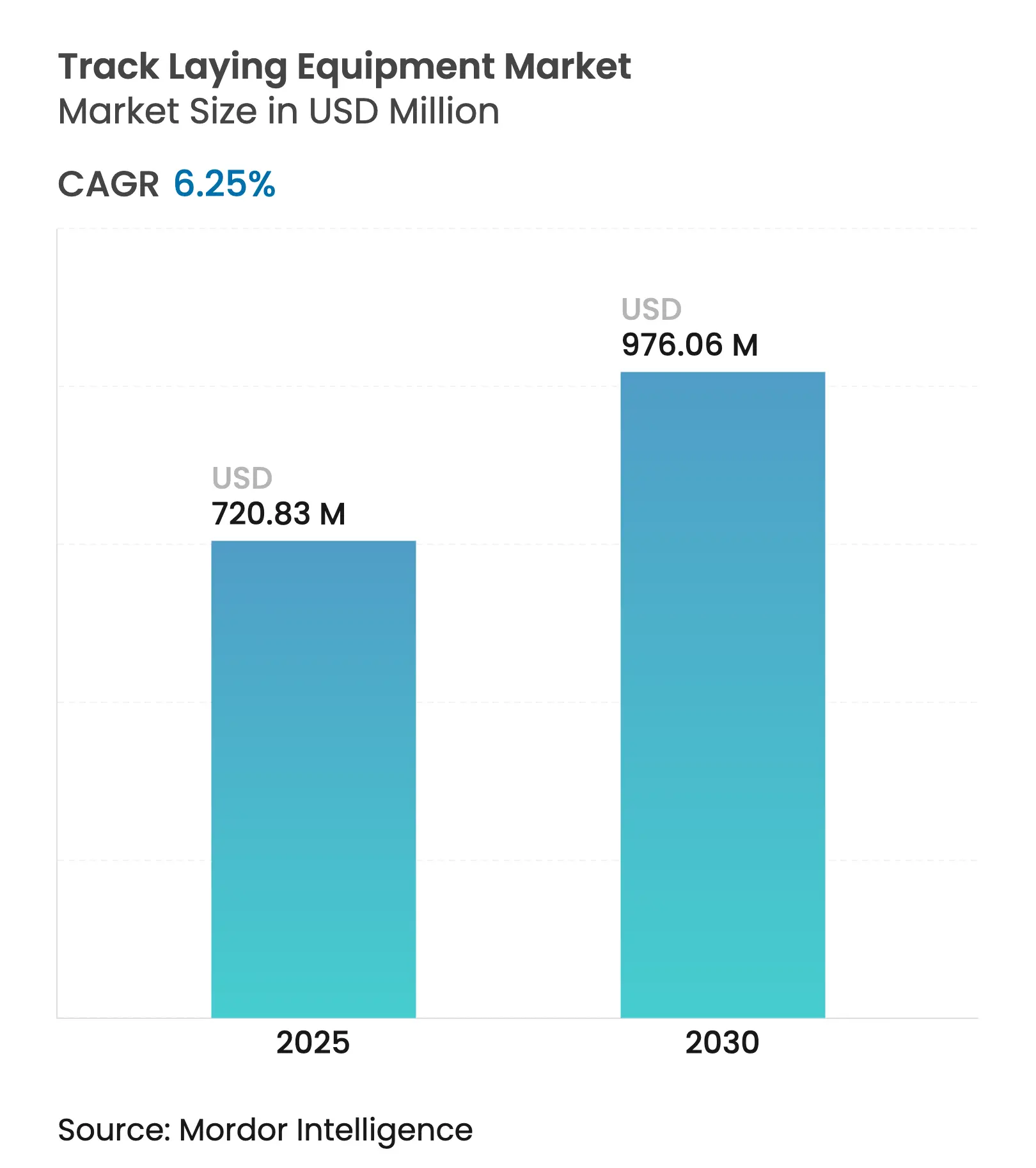

| Market Size (2025) | USD 720.83 Million |

| Market Size (2030) | USD 976.06 Million |

| Growth Rate (2025 - 2030) | 6.25 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Track Laying Equipment Market Analysis by Mordor Intelligence

The Track Laying Equipment market is valued at USD 720.83 million in 2025 and is forecast to reach USD 970.06 million by 2030, registering a 6.25% CAGR over the period. Rapid public-sector capital programs, climate-linked freight shift strategies, and the steady roll-out of automated site technologies are steering this expansion. Major project pipelines—from Germany’s EUR 40 billion rail upgrade to Mexico’s USD 58 billion network expansion—anchor long-term demand for sophisticated machinery. Continuous digitalisation of job-site workflows, growing preference for service-based procurement, and tightening safety regulations further reinforce the growth outlook. Competitive intensity is increasing as OEMs retrofit fleets with IoT sensors, alternative fuels, and AI-enabled diagnostics to offset margin pressure from volatile steel and ballast prices while enabling contractors to deliver on compressed project schedules.

Key Report Takeaways

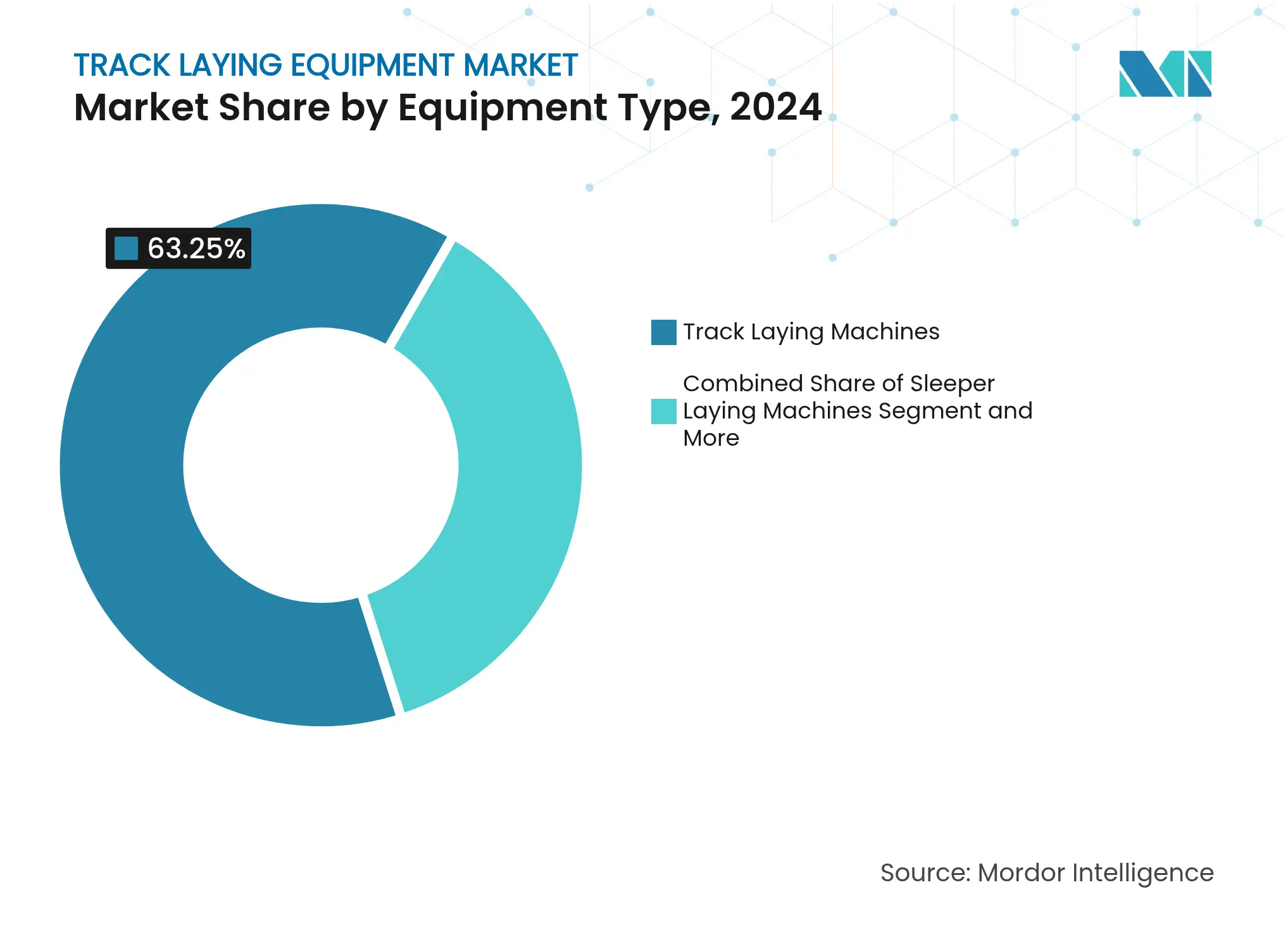

- By equipment type, Track Laying Machines held 63.25% of the track laying equipment market share in 2024; Sleeper Laying Machines are projected to post the fastest 7.27% CAGR to 2030.

- By application, Heavy Freight Rail led with 57.25% revenue share in 2024, whereas High-Speed Passenger Rail is expected to advance at 7.84% CAGR through 2030.

- By technology, Manual systems retained 45.36% share in 2024; Fully Automated solutions will expand at an 8.24% CAGR into 2030.

- By lifting capacity, equipment rated above 12 tonnes accounted for 45.26% of the Track Laying Equipment market size in 2024 and will grow 7.86% annually to 2030.

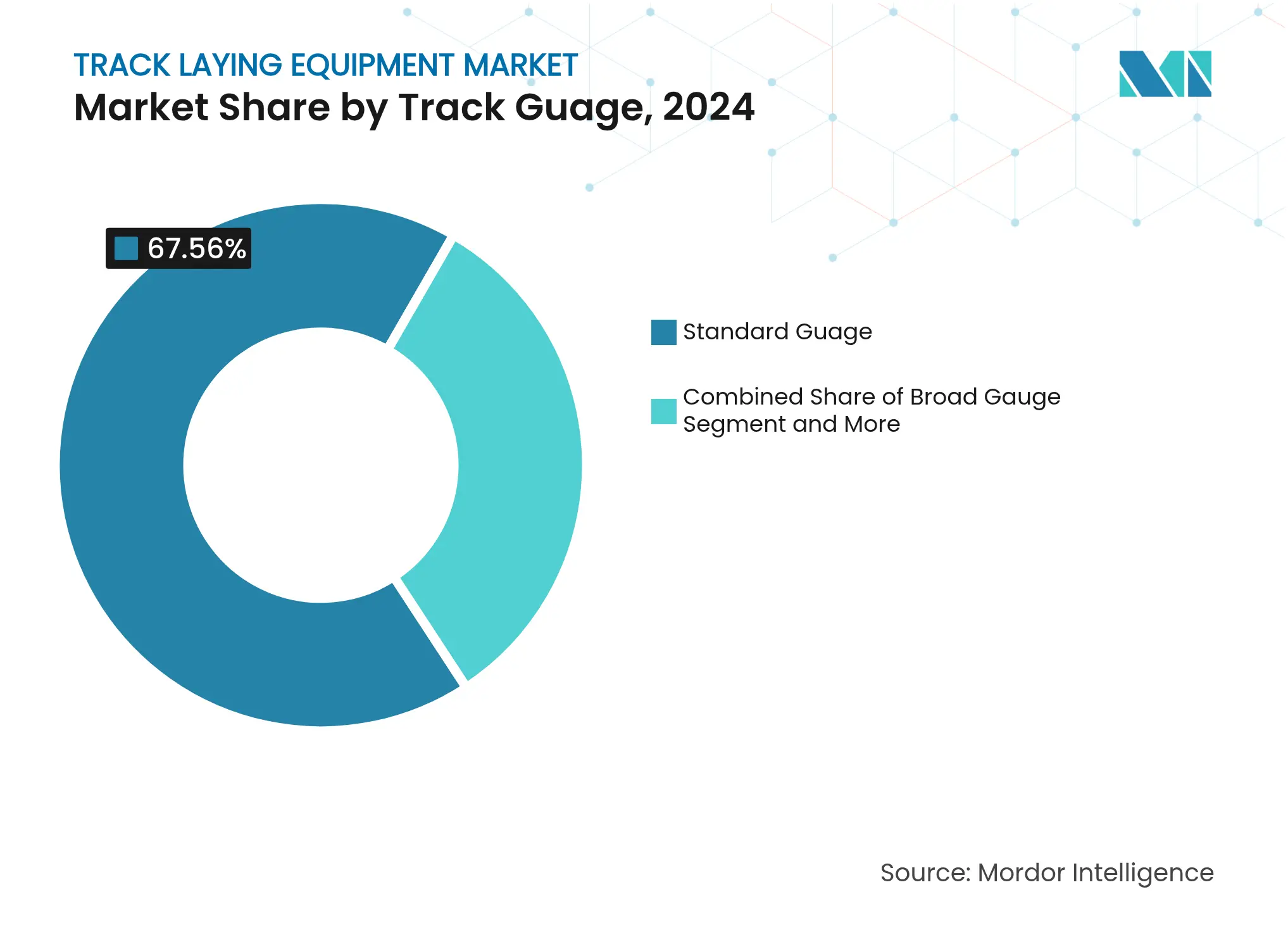

- By track gauge, Standard Gauge systems controlled 67.56% of the Track Laying Equipment market size in 2024 and should grow 7.45% a year through 2030.

- By laying method, Continuous-action machines accounts for 58.34% share of the track laying equipment market in 2024, whereas cyclic methods are growing at 7.20% CAGR by 2030.

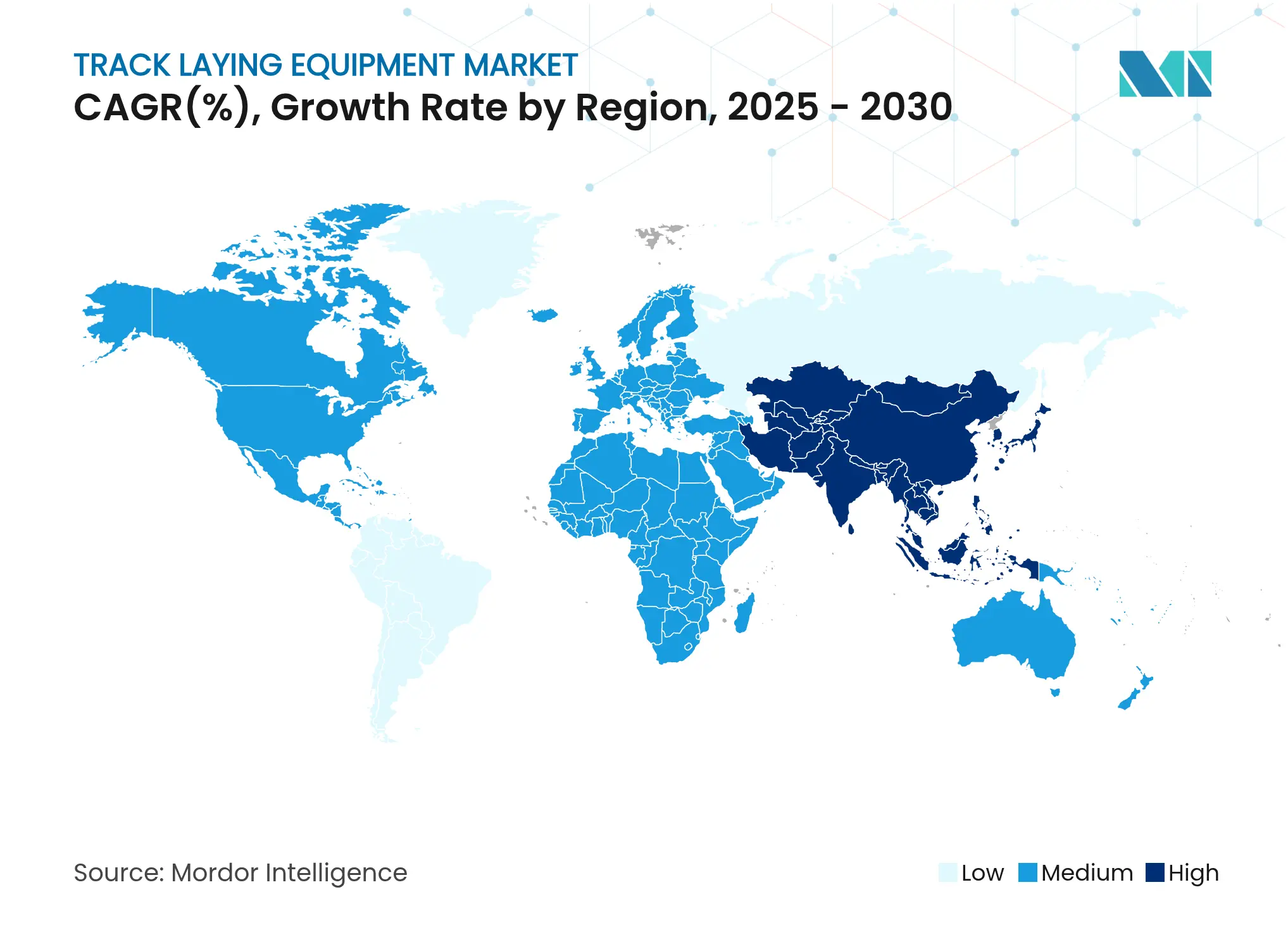

- By geography, Asia-Pacific commanded 41.21% share in 2024 and is set to register the highest 7.80% CAGR over the forecast window.

Global Track Laying Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Government Megaproject Pipelines Expanding Rail Track Government Megaproject Pipelines Expanding Rail Track | +1.8% | Global, concentrated in APAC, Europe, NA | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Global, concentrated in APAC, Europe, NA | Impact Timeline:Medium term (2-4 years) |

Climate-Linked Modal-Shift Policies Favouring Rail Freight Climate-Linked Modal-Shift Policies Favouring Rail Freight | +1.2% | Global; strongest in EU and North America | Long term (≥ 4 years) | |||

Precision Continuous-Action Laying Systems Cut Labour and Time Precision Continuous-Action Laying Systems Cut Labour and Time | +0.9% | Global; early adoption in developed markets | Short term (≤ 2 years) | |||

OEM Equipment-as-a-Service Models Lower CAPEX Barriers OEM Equipment-as-a-Service Models Lower CAPEX Barriers | +0.7% | North America & EU; expanding into APAC | Medium term (2-4 years) | |||

Uptake of Low-Carbon Premium Rails Accelerates Renewal Cycles Uptake of Low-Carbon Premium Rails Accelerates Renewal Cycles | +0.5% | EU and North America | Long term (≥ 4 years) | |||

Predictive Analytics and Digital-Twin Scheduling Boost Demand Predictive Analytics and Digital-Twin Scheduling Boost Demand | +0.6% | Global, tech-advanced markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Government Megaproject Pipelines Expanding Rail Track Km (2025-2030)

Unprecedented public-sector funding sustains a high volume of tenders for heavy-duty machines. Germany is renovating 4,000 km of track with a plan to surpass 9,000 km, while Morocco approved a USD 10.3 billion program that connects 87% of its population[1]“Morocco approves USD 10.3 billion rail plan,” France 24, france24.com. Vietnam fast-tracked a USD 8 billion cross-border line scheduled to break ground before 2026[2]“Vietnam fast-tracks cross-border rail,” Caixin Global, caixinglobal.com. These overlapping schedules shorten equipment availability windows, advantaging OEMs with global service fleets and ready inventory.

Climate-Linked Modal-Shift Policies Favouring Rail Freight

Carbon-pricing regimes and decarbonisation targets push freight volumes onto steel rails. The EU seeks a rail freight share of 36% by 2050, and the U.S. Department of Energy has set a net-zero goal for rail by 2050[3]“Rail Energy and Emissions Action Plan,” U.S. Department of Energy, energy.gov. The Association of American Railroads estimates a 25% truck-to-rail shift would save 1.2 billion gallons of fuel annually. These long-term policies give investors confidence to fund corridor expansions that require modern track-laying fleets.

Precision Continuous-Action Laying Systems Cut Labour and Time

Automation addresses shortages of certified operators and intensifying safety regulations. Herzog’s Rail Unloading Machine enables hands-free rail placement, reducing crew counts and manual handling risk. Simulation training further compresses learning curves, as shown by reductions from six months to seven weeks in crane operations. The payback on productivity offsets premium equipment pricing, accelerating adoption.

Predictive Analytics and Digital-Twin Scheduling Boost Demand

Project owners now mandate integrating sensor data, BIM, and real-time track geometry feeds into central control rooms. Digital twins cut re-work by flagging alignment deviations early, and predictive models schedule tamping or sleeper changeouts before faults escalate as specifications migrate into bid documents, OEMs that supply analytics-ready hardware secure preferred vendor status.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Ballooning Ballast and Steel Prices Squeeze Project Budgets Ballooning Ballast and Steel Prices Squeeze Project Budgets | -1.4% | Global, acute in commodity-dependent regions | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:Global, acute in commodity-dependent regions | Impact Timeline:Short term (≤ 2 years) |

Shortage Of Certified Rail-Equipment Operators Shortage Of Certified Rail-Equipment Operators | -0.8% | North America & EU primarily, spreading globally | Medium term (2-4 years) | |||

Cyber-Risk Exposure Of Sensor-Rich Automated Trains Cyber-Risk Exposure Of Sensor-Rich Automated Trains | -0.6% | Global, concentrated in developed markets with advanced systems | Medium term (2-4 years) | |||

Lengthy Regulatory Approvals For Next-Gen Automated Fleets Lengthy Regulatory Approvals For Next-Gen Automated Fleets | -0.4% | EU, North America, APAC developed markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Ballooning Ballast and Steel Prices Squeeze Project Budgets

Construction input prices climbed 40.5% between 2020 and January 2025, and agencies such as the Illinois DOT have inserted price-escalation clauses to keep tenders viable. Steel volatility inflates the cost of continuous-welded rail, sometimes delaying procurement cycles. Contractors respond by prioritising high-efficiency machines that reduce crew hours, but stretched budgets can still slow near-term orders.

Shortage of Certified Rail-Equipment Operators

An ageing workforce and stricter qualification rules strain project delivery timelines. The FRA’s Track Safety Standards require certified personnel for inspections, yet the talent pipeline remains shallow[4]“Track Safety Standards,” FRA, railroads.dot.gov. Automation eases head-count requirements but increases demand for technicians capable of maintaining sensor-rich fleets, shifting the skill mix rather than eliminating it.

Segment Analysis

By Equipment Type: Dominance of Track Layers amid Sleeper Innovation

Track Laying Machines accounted for 63.25% of the Track Laying Equipment market in 2024, a position unlikely to erode quickly thanks to versatility across freight and high-speed lines. The Track Laying Equipment market size for this category is supported by recurring renewal programs as well as greenfield lines. Sleeper Laying Machines, aided by continuous-action technology, are forecast to grow 7.27% annually as contractors prioritise speed and labour savings. Digitised tampers and rail welders benefit from the same automation wave, bringing end-to-end data continuity to the job-site.

Innovation centres on electrified powertrains, remote diagnostics, and hybrid drives that limit emissions inside tunnels and dense urban pockets. OEMs now bundle sensor kits across machine families so managers can compare utilisation rates and plan preventive maintenance through a single dashboard. This integrated approach strengthens the Track Laying Equipment market by turning machinery into a data-generating asset class.

Note: Segment shares of all individual segments available upon report purchase

By Application: Freight Infrastructure Leads High-Speed Growth

Heavy Freight Rail represented 57.25% of the Track Laying Equipment market in 2024, underpinned by commodity-driven corridors such as Australia’s Inland Rail. Project owners favour high-capacity machines able to place continuous-welded rail strings and concrete sleepers quickly to minimise line closures. In parallel, High-Speed Passenger Rail will log the fastest 7.84% CAGR as governments treat 250 km/h-plus lines as a decarbonised alternative to short-haul flights.

Urban metro, light-rail, and mixed-traffic upgrades support long-duration demand because they require work windows that change daily around passenger schedules. The Track Laying Equipment market size for these sub-applications rises in tandem with smart-city budgets and last-mile freight initiatives. Suppliers that offer modular attachments suited to both ballast-bed and slab-track designs capture the widest customer base.

By Technology: Manual Systems Yield to Automation

Manual machines retained 45.36% share in 2024, a reminder of the sizeable retrofit pool and conservative procurement cultures in many public agencies. Semi-automated models bridge familiarity with incremental gains, but Fully Automated systems will secure the fastest 8.24% CAGR. Their edge comes from closed-loop geometry control, AI-driven fault prediction, and compliance with emerging inspection mandates.

The FRA’s proposed TGMS rule effectively embeds automation into regulatory frameworks, compelling Class I and II railroads to capture geometry data at set intervals. Once adopted, such mandates normalise higher-spec bids, reinforcing the Track Laying Equipment market’s shift toward data-centric fleets.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Lifting Capacity: Heavy-Duty Dominance Reflects Infrastructure Scale

Equipment rated above 12 tonnes controlled 45.26% of the Track Laying Equipment market in 2024 and is forecast to expand 7.86% annually. Long rail strings exceeding 100 m and prestressed concrete sleepers demand high lifting torque, especially on high-speed alignments. Mid-range 9-12 tonne machines serve metro extensions, while below 9 tonne units address narrow-gauge or maintenance niches where manoeuvrability prevails.

Heavy-duty demand correlates with a preference for low-maintenance slab track and premium head-hardened rails, which shift weight upstream to construction equipment. Suppliers capable of delivering heavy-lift rigs with low ground pressure avoid speed limits on temporary work tracks, shortening closure windows and improving contractor economics across the Track Laying Equipment market.

By Track Gauge: Standard Gauge Universality Drives Market Leadership

Standard Gauge commanded 67.56% share in 2024 and is projected to grow 7.45% annually. Its dominance rests on interoperability across transcontinental networks and most high-speed systems. Broad Gauge maintains relevance in India and the CIS region, requiring OEM catalogues to cover multiple variants. Meter and Narrow Gauge applications retain niche demand in mining and tourism.

Global megaproject consortia increasingly specify standard gauge to streamline rolling-stock procurement and border-nation connectivity. Consequently, standardisation enables OEMs to attain economies of scale, reinforcing price competitiveness and service coverage across the Track Laying Equipment market.

Note: Segment shares of all individual segments available upon report purchase

By Laying Method: Continuous-Action Efficiency Meets Cyclic Precision

Continuous-action machines held 58.34% share in 2024 thanks to productivity on greenfield lines. Their uninterrupted workflow can exceed 1,500 m per shift, a pace attractive to contractors chasing cost-plus incentives. Cyclic methods, growing 7.20% annually, shine in confined urban sites where millimetric precision outranks speed.

Manufacturers now market convertible platforms that can switch between modes, widening the addressable demand pool. Equipment telemetry captures cycle counts, alignment drift, and component wear, allowing site managers to choose the optimal laying method for each segment, thereby enlarging the Track-Laying Equipment market footprint.

Geography Analysis

Asia-Pacific led with 41.21% of the Track Laying Equipment market in 2024 and will record the fastest 7.80% CAGR to 2030. China raised railway capital spending by 10.8% in the first five months of 2024, while Vietnam accelerated a USD 8 billion cross-border corridor. The Asian Development Bank projects USD 43 trillion in transport outlays through 2035, of which rail captures 17%. Local OEMs benefit from high-volume domestic orders that justify factory expansions and rapid product iteration, reinforcing regional dominance.

Europe follows as a mature yet dynamic arena. Germany’s EUR 40 billion overhaul spans 4,000 km of track, backed by Siemens Mobility’s EUR 2.8 billion signalling deal that locks in modern control architectures. The EU’s modal shift and circular-economy directives reward suppliers for delivering low-carbon equipment and recyclable components. Multilateral funding streams, such as the Connecting Europe Facility, buffer member-state fiscal constraints and sustain order pipelines for the Track-Laying Equipment market.

North America registers steady replacement-driven growth amid ageing infrastructure. The USD 16 billion Hudson Tunnel and California’s USD 135 billion high-speed line headline a list of megaprojects requiring specialised equipment fleets. Federal grants under the Infrastructure Investment and Jobs Act inject cash into state corridors, yet skills gaps and permitting hurdles temper rollout speed. Elsewhere, Morocco’s USD 10.3 billion high-speed plan and the UAE-Oman rail link illustrate rising momentum across the Middle East and Africa, opening new export theatres for established OEMs.

Competitive Landscape

Market Concentration

The Track-Laying Equipment market remains moderately fragmented. Players like Plasser & Theurer leverage a 17,700-unit global fleet and more than 10,000 patents to protect their lead. At the same time, CRRC Corporation supports expansion via CNY 15 billion annual R&D budgets and worldwide manufacturing hubs. Wabtec’s USD 960 million acquisition of Dellner Couplers signals an appetite for portfolio breadth in passenger systems.

Strategic priorities coalesce around digital integration, alternative fuels, and service-based contracts. Plasser’s HVO-ready drives cut CO₂ on work trains, whereas Colas Rail’s new tampers in the UK meet updated emissions rules. OEMs increasingly bundle analytics platforms that predict component wear, aligning with customers’ availability-based KPIs. Partnerships—such as Progress Rail’s memorandum with Borusan Cat in 2024—extend reach into growth geographies without heavy overhead.

Material price inflation and cybersecurity exposure raise entry barriers, favouring incumbents with scale, supply-chain control, and in-house software talent. Concurrently, niche entrants exploit equipment-as-a-service white spaces to win small-contractor business, intensifying price competition on standard gauge machines but expanding total addressable demand across the Track Laying Equipment market.

Track Laying Equipment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Morocco approved a USD 10.3 billion rail expansion, including a Marrakesh high-speed line.

- February 2025: Vietnam’s parliament cleared an USD 8 billion railway to China’s Yunnan province, bringing start-of-work forward to late 2025.

- September 2024: Progress Rail and Borusan Cat signed an MoU to pursue rail projects in Türkiye and neighboring markets.

Table of Contents for Track Laying Equipment Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Government Megaproject Pipelines Expanding Rail Track Km (2025-2030)

- 4.2.2Climate-Linked Modal-Shift Policies Favouring Rail Freight

- 4.2.3Precision Continuous-Action Laying Systems Cut Labour and Time

- 4.2.4OEM "Equipment-As-A-Service" Models Lower CAPEX Barriers

- 4.2.5Uptake of Low-Carbon Premium Rails Accelerates Renewal Cycles

- 4.2.6Predictive Analytics and Digital-Twin Scheduling Boosts Demand

- 4.3Market Restraints

- 4.3.1Ballooning Ballast and Steel Prices Squeeze Project Budgets

- 4.3.2Shortage of Certified Rail-Equipment Operators

- 4.3.3Cyber-Risk Exposure of Sensor-Rich Automated Trains

- 4.3.4Lengthy Regulatory Approvals for Next-Gen Automated Fleets

- 4.4Value/Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size and Growth Forecasts (Value (USD))

- 5.1By Equipment Type

- 5.1.1Track Laying Machines

- 5.1.2Sleeper Laying Machines

- 5.1.3Ballast Regulators

- 5.1.4Tamping Machines

- 5.1.5Track Maintenance Equipment

- 5.1.6Rail Welding Machines

- 5.1.7Others

- 5.2By Application

- 5.2.1Heavy Freight Rail

- 5.2.2High-Speed Passenger Rail

- 5.2.3Urban Metro / Subway

- 5.2.4Light Rail and Tram

- 5.2.5Mixed-Traffic Mainlines

- 5.2.6Industrial and Mining Rail

- 5.3By Technology

- 5.3.1Manual

- 5.3.2Semi-automated

- 5.3.3Fully Automated

- 5.4By Lifting Capacity

- 5.4.1Below 9 tonnes

- 5.4.29 - 12 tonnes

- 5.4.3Above 12 tonnes

- 5.5By Track Gauge

- 5.5.1Standard Gauge

- 5.5.2Broad Gauge

- 5.5.3Meter and Narrow Gauge

- 5.6By Laying Method

- 5.6.1Continuous-Action Method

- 5.6.2Cyclic / Intermittent Method

- 5.7By Geography

- 5.7.1North America

- 5.7.1.1United States

- 5.7.1.2Canada

- 5.7.1.3Mexico

- 5.7.1.4Rest of North America

- 5.7.2South America

- 5.7.2.1Brazil

- 5.7.2.2Argentina

- 5.7.2.3Rest of South America

- 5.7.3Europe

- 5.7.3.1Germany

- 5.7.3.2United Kingdom

- 5.7.3.3France

- 5.7.3.4Italy

- 5.7.3.5Spain

- 5.7.3.6Russia

- 5.7.3.7Rest of Europe

- 5.7.4Asia-Pacific

- 5.7.4.1China

- 5.7.4.2India

- 5.7.4.3Japan

- 5.7.4.4South Korea

- 5.7.4.5ASEAN-5

- 5.7.4.6Australia & New Zealand

- 5.7.4.7Rest of Asia-Pacific

- 5.7.5Middle East and Africa

- 5.7.5.1United Arab Emirates

- 5.7.5.2Saudi Arabia

- 5.7.5.3Turkey

- 5.7.5.4South Africa

- 5.7.5.5Egypt

- 5.7.5.6Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1Plasser & Theurer

- 6.4.2CRRC Corporation Ltd.

- 6.4.3Techne Kirow GmbH

- 6.4.4Matisa Materiel Industriel SA

- 6.4.5Geismar

- 6.4.6Harsco Rail (Enviri)

- 6.4.7Salcef Group SpA

- 6.4.8Vossloh AG

- 6.4.9BEML Ltd.

- 6.4.10Weihua Group

- 6.4.11Effiage Infra-Rail

- 6.4.12Simplex Engineering & Foundry Works

- 6.4.13Herzog Rail Services

- 6.4.14RailWorks Corp.

- 6.4.15Loram Maintenance of Way

- 6.4.16Swietelsky AG

- 6.4.17Strukton Rail

- 6.4.18Pandrol Ltd.

7. Market Opportunities & Future Outlook

Global Track Laying Equipment Market Report Scope

Track-laying equipment refers to heavy machinery deployed to install new railroad tracks or replace and maintain existing railway tracks. The track-laying equipment market consists of a wide range of companies involved in designing, manufacturing, and selling track-laying machines to end users.

The track-laying equipment market is segmented by type, application, lifting capacity, and geography. By type, the market is segmented into new construction equipment and renewal equipment. By application, the market is segmented into heavy rail and urban rail. By lifting capacity, the market is segmented into up to 9 tonnes, 9-12 tonnes, and more than 12 tonnes. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

The report offers market size and forecasts for track laying equipment in value (USD) for all the above segments.