Asphalt Pavers Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 3.23 Billion |

| Market Size (2031) | USD 4.15 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

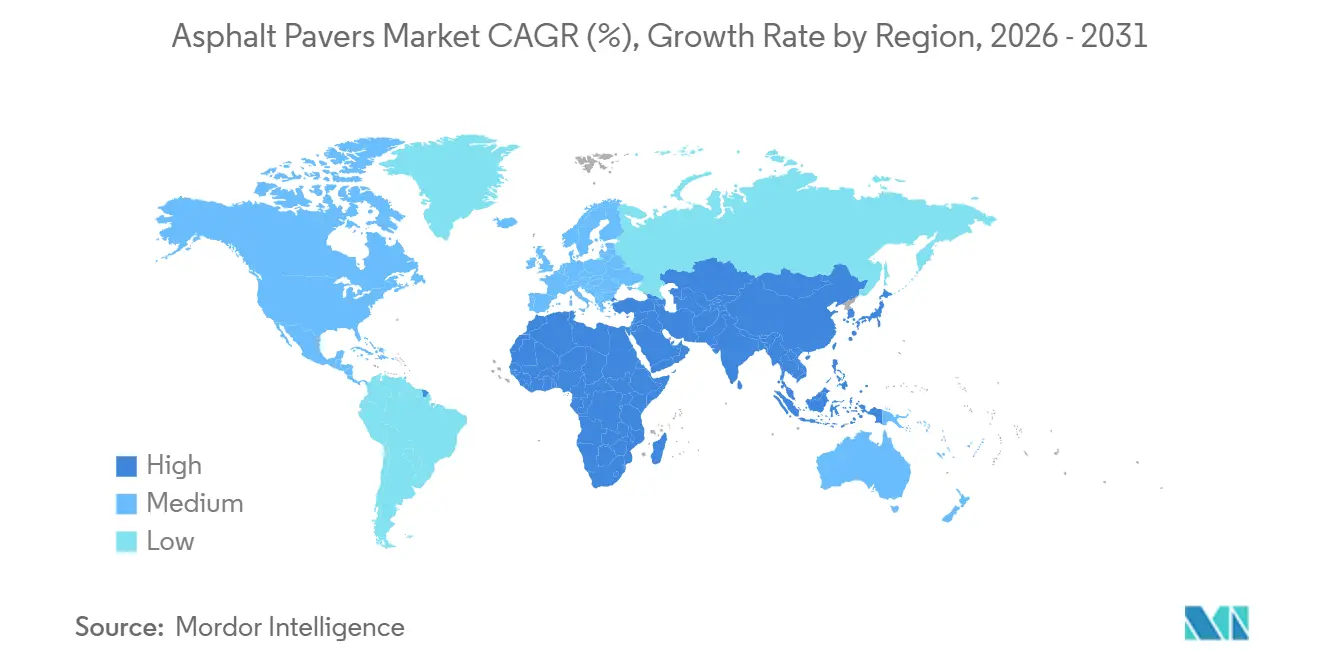

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

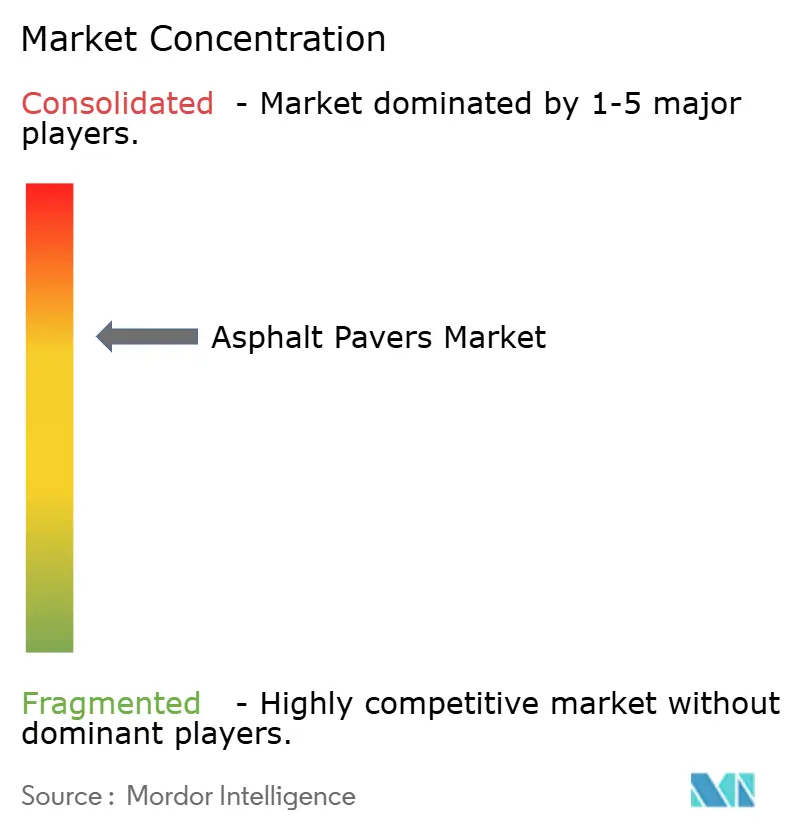

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asphalt Pavers Market Analysis by Mordor Intelligence

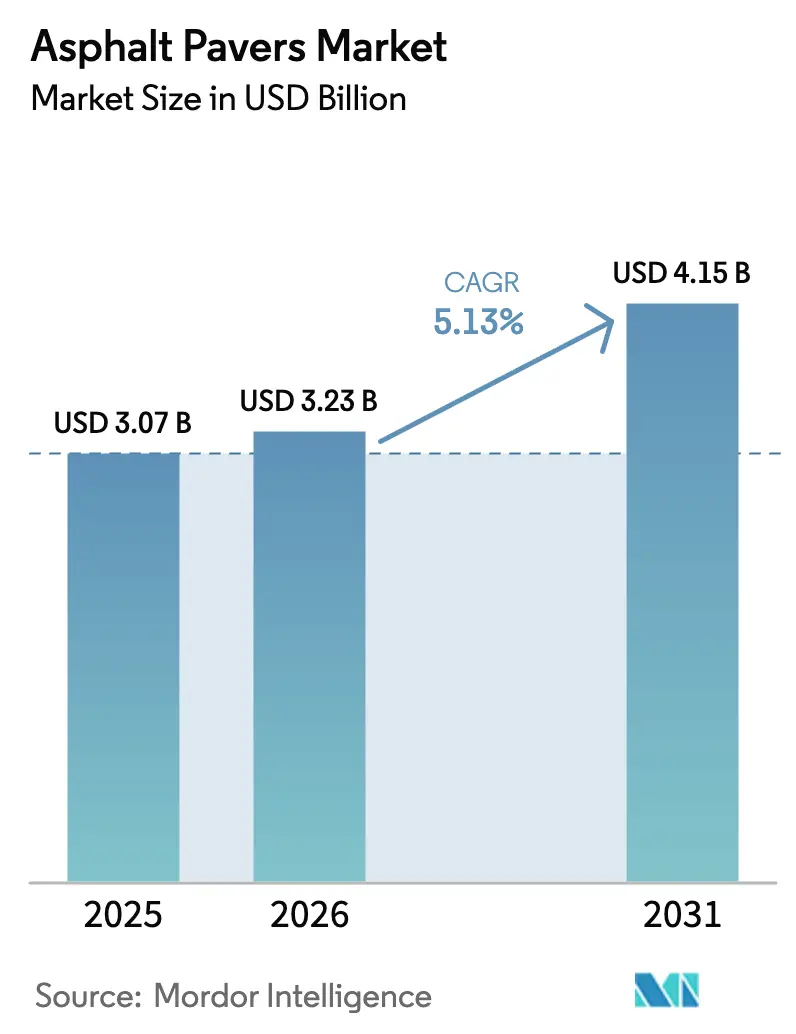

The asphalt paver market size is expected to grow from USD 3.07 billion in 2025 to USD 3.23 billion in 2026 and is forecast to reach USD 4.15 billion by 2031 at a 5.13% CAGR over 2026–2031. This steady climb reflects large-scale public-works allocations, a building frenzy in emerging megacities, and precision-technology packages that trim material waste and labor hours. Accelerated U.S. federal road funding, China’s expressway additions, and India’s Bharatmala highway program are keeping bid pipelines full, while warm-mix asphalt formulations are lengthening construction seasons in temperate climates. Contractors are gravitating toward machines that pair grade control with telematics because the data stream supports predictive maintenance and compliance documentation. Simultaneously, price-sensitive buyers in Africa and Southeast Asia are welcoming cost-competitive Chinese brands, even as emission rules in North America and Europe tilt demand toward Stage V-compliant engines and electric-drive options. The asphalt paver market stands at the intersection of productivity, sustainability, and data monetization, creating fresh opportunities for OEMs that can bundle hardware with software and training.

Key Report Takeaways

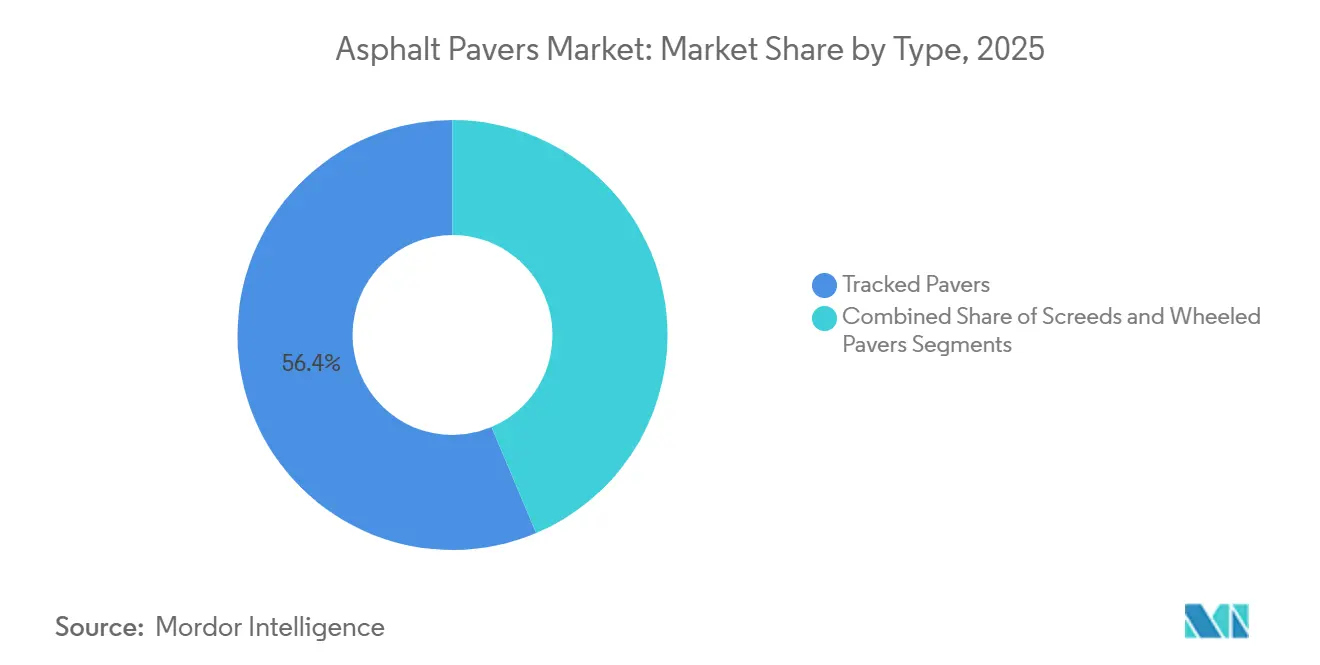

- By type, tracked pavers led with 56.36% asphalt paver market share in 2025, whereas screeds are advancing at a 6.88% CAGR through 2031, the fastest pace among all segments.

- By paving range, the standard 2.4-2.55 m width category accounted for 35.87% revenue share; units above 2.55 m are projected to post a 7.58% CAGR to 2031.

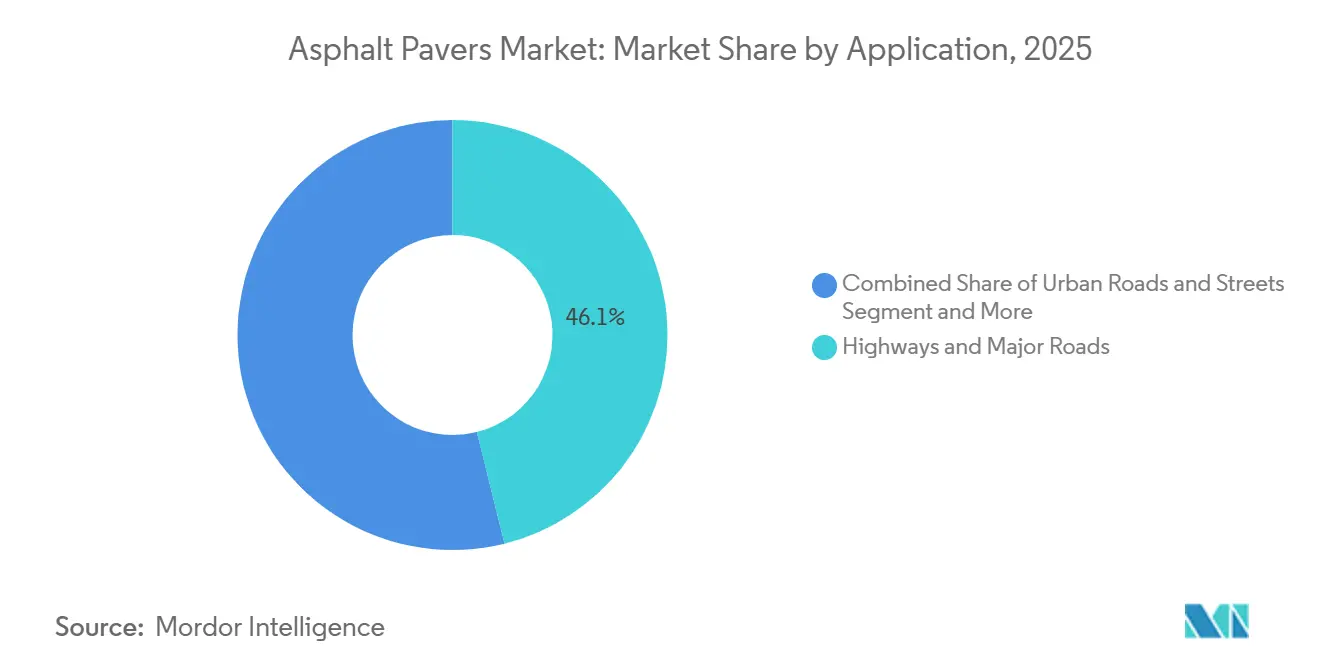

- By application, highways and major roads accounted for 46.12% of the 2025 demand, while airport runway projects are poised to grow at a 7.99% CAGR through 2031.

- By end-user, government and public agencies commanded 51.24% of 2025 spend, yet rental companies are expanding at a 6.17% CAGR as contractors pursue fleet flexibility.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Asphalt Pavers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Road-building and Urbanization | +1.8% | Asia-Pacific core, spill-over to Middle East | Long term (≥ 4 years) |

| Accelerated Infrastructure Funding | +1.5% | North America, selective EU programs | Medium term (2-4 years) |

| Integration of Telematics and Grade-Control | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Warm-Mix Asphalt Adoption | +0.7% | North America, Northern Europe | Short term (≤ 2 years) |

| Demand for Compact Pavers in Dense Cities | +0.5% | APAC urban centers, European metros | Long term (≥ 4 years) |

| Spray-Paver Bonded-Overlay Technology | +0.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Road-Building and Urbanization Across APAC

Rapid urbanization is spurring a wave of highway and municipal road projects in the Asia-Pacific. China's Guangdong had plans to complete 12,000 km of new expressways in 2025, and India aims for 17,000 km of upgrades by 2027, guaranteeing multi-year order books for tracked machines[1]GD Today, "Achieve 12,000 km of expressway to traffic in Guangdong by 2025 to accelerate connectivity in GBA", Foreign Affairs Office of Guangzhou Municipal Government, eguangzhou.gov.cn. Belt and Road financing is underwriting arterial-road tenders in Indonesia and Vietnam, each exceeding USD 5 billion in 2025, while tier-2 Indian cities are adding compact pavers for neighborhood streets. The Asian Development Bank estimates that developing Asia needs USD 1.7 trillion in annual infrastructure investment through 2030, assuring that the asphalt paver market will outpace Western regions in absolute unit growth[2]"Meeting Asia's Infrastructure Needs", Asian Development Bank, adb.org.

Accelerated Infrastructure Funding in North America

The U.S. Infrastructure Investment and Jobs Act earmarked USD 110 billion for roads and bridges, with around 76% of the funds already obligated by mid-2025. State transportation departments are emphasizing preventive maintenance, raising demand for thin-overlay screeds and spray-bonded pavers. Canada’s Investing in Canada program is injecting CAD 33.5 billion into public transit, green infrastructure, and social infrastructure, guiding specifications toward tracked pavers with cold-weather packages. Warm-mix asphalt mandates enable paving in temperatures as low as 10 °C, adding four to six extra working weeks and lifting annual machine utilization.

Integration of Telematics and Grade-Control Boosting ROI

Telematics and automated grade control are significantly reducing asphalt overages, according to a 2025 civil engineering field study. Contractors now track screed temperature, fuel burn, and idle hours remotely, scheduling service before breakdowns occur. Rental firms are pivoting to usage-based pricing, billing per cubic meter of asphalt placed, which further accelerates technology uptake among smaller contractors. European traceability rules require digital placement logs, a compliance edge that Tier 1 OEMs leverage to protect premium pricing.

Warm-Mix Asphalt Adoption Extending Paving Seasons

Warm-mix asphalt accounted for approximately 40% of the United States' tonnage as of the latest reports, witnessing a significant increase in the last 2-3 years. Lower mix temperatures shrink fuel use and GHG emissions, aligning with state climate targets. Longer paving seasons improve fleet utilization and hasten payback on new units, justifying the price premium of warm-mix-ready screeds. OEMs are fielding heated screed plates that maintain compaction temperature even at low ambient readings, reducing callbacks.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Maintenance Costs | -0.6% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Expansion of Rental Business Model | -0.5% | North America, Western Europe | Medium term (2-4 years) |

| Bitumen-Price Volatility | -0.4% | Global, linked to crude-oil markets | Short term (≤ 2 years) |

| Skilled-Operator Shortages | -0.3% | North America, Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs of Advanced Pavers

Telematics-equipped tracked pavers can list between USD 450,000 and USD 650,000, pricing many smaller contractors out of the ownership model. Maintenance needs grow more complex as sensor suites, hydraulics, and embedded software demand OEM-certified service providers, seldom found in rural regions. Import tariffs and limited access to credit further raise the total cost of ownership in emerging economies, pushing buyers toward basic models that skip premium electronics. Chinese brands offer stripped-down machines at a robust discount, but the technology gap narrows their appeal in regulated markets.

Expansion of Equipment Rental Business Model

Rental penetration reached over 50% of construction-equipment spending in North America in 2025, as contractors sought flexibility and balance-sheet relief. Utilization rates above 70% encourage rental houses to refurbish fleets rather than buy new, extending replacement cycles and compressing OEM volumes. Volume discounts of up to 25% erode manufacturer margins, though service-parts sales and telematics subscriptions partly offset the shortfall. Rental’s arrival in India and Southeast Asia signals a global diffusion that will reshape sales strategies over the decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type – Tracked Pavers Dominate as Screeds Surge

Tracked pavers captured 56.36% of 2025 revenue, illustrating contractor trust in their traction on soft base layers and steep grades. Wheeled variants remain favored for urban resurfacing because quicker relocation lowers idle time, yet their market share is eroding as tracked models add higher travel-speed modes. The screed segment stands out with a 6.88% CAGR to 2031, propelled by pavement-preservation budgets that emphasize thin overlays and bonded-wearing courses. State maintenance outlays in the United States channeled the majority of 2025 highway funds into preventive treatments, boosting orders for extendable screeds. This demand reinforced the appeal of intelligent screeds that auto-correct tamper frequency for temperature swings.

Electrified tracked machines debuted in 2025, promising quieter night paving and compliance with zero-emission mandates in dense cities. Wheeled pavers have responded with tighter turning radii and semi-autonomous steering to remain relevant. Screed suppliers now integrate sensors that capture mat density and temperature, feeding project owners with audit-ready reports and elevating after-sales software revenue. The convergence of type categories foreshadows multi-role platforms able to toggle between highway, street, and overlay duties through bolt-on modules.

By Paving Range – Wide Pavers Accelerate on Mega-Projects

Standard 2.4-2.55 m widths yielded 35.87% of 2025 revenue, matching single-lane highway specifications in most regions. Yet machines above 2.55 m are growing at 7.58% CAGR as airport runways and multi-lane expressways demand faster passes and fewer cold joints. China’s 3.75 m lane requirements for future autonomous trucking push even wider screeds, inspiring models that place two lanes in one go. Compact ranges under 1.5 m cover bike paths and pedestrian precincts, benefiting from European city plans that expand car-free zones.

Airport tenders routinely cite airline delay costs of USD 50,000-100,000 per hour, justifying investment in wide pavers capable of relentless throughput. European OEMs have capitalized, with flagship units securing high-profile runway jobs at Frankfurt and Amsterdam during 2025. Narrow urban alleys in Jakarta and Ho Chi Minh City are fueling uptake of sub-1.5 m pavers, a sweet spot that Asian manufacturers are exploiting with lightweight, rubber-track designs. Buyers now evaluate range categories through total project economics rather than sticker price, further segmenting demand by application urgency.

By Application – Airports Outpace Highways

Highways and major roads absorbed 46.12% of paving-equipment demand in 2025, reflecting government dominance in surface-transport spending. Airports, however, will expand at a 7.99% CAGR to 2031, driven by passenger recovery and runway capacity upgrades. The International Air Transport Association expects 5.2 billion passengers in 2026, propelling a rush for polymer-modified asphalt mixes that endure high jet-blast heat. The asphalt paver market size for airport jobs is set to rise as reconstruction cycles tighten. Urban streets and collector roads underpin steady volumes for compact machines, while parking-lot paving tracks commercial real-estate trends.

Runway closures carry stiff penalties, so project owners mandate 24/7 operations and telemetry to document mat density. Rental providers stock wide pavers with laser-guided screeds specifically for these compressed timelines. Highway paving is shifting toward intelligent compaction, where on-board sensors guide roller sequences, minimizing premature cracking. Municipal night work is spurring demand for battery-electric pavers that trim noise and emissions, opening a green premium niche yet to be fully captured.

By End-User – Rental Companies Reshape Procurement

Government and public agencies retained a 51.24% 2025 share, driven by sovereign infrastructure mandates. Private contractors, although the second-largest segment, are pivoting to leasing, offloading depreciation and maintenance to rental specialists. The resulting 6.17% CAGR for rental companies will reshape OEM revenue models around fleet packages, extended warranties, and predictive-maintenance dashboards. The asphalt paver market share of rental fleets could be among the highest by 2031 if current utilization holds.

OEMs have started offering rental-optimized SKUs with quick-swap screeds and ruggedized telematics, cutting downtime between hires. Public-sector owners in emerging regions still prefer outright purchase for asset-control reasons, but multilateral lenders that fund PPP roads often require lifecycle cost analysis, indirectly favoring rental. Subscription models that bundle equipment, operator training, and consumables on a monthly fee are spreading from Germany to the wider EU, signaling another layer of service-based disruption.

Geography Analysis

Asia-Pacific contributed 37.92% of 2025 revenue and is advancing at a 5.09% CAGR, anchored by India’s Bharatmala highway program and provincial expressways in China. Middle East and Africa, though smaller in absolute terms, will accelerate at 6.57% CAGR through 2031 as oil-funded sovereign plans finance multilane corridors and airport expansions. Saudi Arabia earmarked USD 40 billion for transport under Vision 2030, and the UAE is modernizing 2,500 km of federal highways to support autonomous-vehicle pilots. Sub-Saharan African projects financed under Belt and Road terms favor lower-cost Chinese pavers, yet technology gaps in telematics and emission compliance limit penetration in North American and EU tenders.

North America is growing at a 3.15% CAGR thanks to ongoing federal appropriations and state-level climate-resilience programs that call for warm-mix asphalt and spray-overlay gear. Europe registers a modest 2.88% CAGR as fiscal constraints weigh on new build, though the European Green Deal pushes municipalities toward electric pavers for night work. South America’s 2.01% rate reflects currency volatility and public-debt overhang, yet Brazil’s Rota 2030 road upgrades linked to EV charging corridors provide a mid-term tailwind. Oceania sits at 2.89% CAGR, driven by seismic-resilience retrofits in New Zealand and Australia’s rolling infrastructure plan.

Divergent regulation shapes product specifications. The EU’s Stage V engine rules raise unit cost but create a compliance moat protecting premium OEMs. Middle Eastern buyers demand high-temperature and dust-filtration features to withstand desert climates. India’s IS 16246 standard, introduced in 2024, enforces screed-heating uniformity and compaction thresholds, pruning the influx of low-end imports. Such fragmentation compels global manufacturers to run region-specific certification portfolios, inflating R&D and inventory carrying costs.

Competitive Landscape

Competition is moderately concentrated, led by Caterpillar, Wirtgen Group, Volvo Construction Equipment, Fayat Group, and Ammann together. Caterpillar’s success hinges on its dealer network and proprietary telematics, which lock customers into service contracts. Wirtgen leverages German engineering to rule wide pavers and premium screeds, banking on patented automated-leveling software. Volvo’s minority stake in telematics supplier Trackunit enables it to embed predictive-maintenance analytics at the controller level, opening up subscription revenue streams.

Chinese brands XCMG, SANY, and Zoomlion together are advancing in Africa and Southeast Asia by pairing cost advantages with Belt and Road project financing. Emission-compliant powertrains and advanced telematics remain their weak points in regulated markets, but joint ventures with European sensor firms aim to close the gap. Fayat Group is integrating Dynapac and BOMAG parts supply to reduce inventory duplication and cross-sell compaction rollers, a move that raises customer switching costs.

White-space opportunities abound in electric-drive pavers for night-time urban contracts and in modular screeds that let fleet owners match width to job requirements without purchasing multiple machines. Scandinavian startups are piloting zero-emission prototypes, yet small production runs keep prices high. ISO 9001 quality management and regional engine certifications such as EPA Tier 4 Final in North America have become cost-of-entry thresholds, elevating barriers for newcomers and supporting incumbent margins.

Asphalt Pavers Industry Leaders

-

Caterpillar Inc.

-

Fayat Group

-

Ammann Group

-

Wirtgen Group

-

Volvo Construction Equipment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Vögele placed the first Dash 5 mini paver into global distribution, adding a redesigned hopper, ergonomic operator deck, and upgraded LED lighting.

- August 2025: Ammann India shipped its inaugural tracked asphalt paver from the new Gujarat assembly line, delivering a Tier III-compliant model aimed at efficiency-minded contractors.

- April 2025: Dynapac and Leica Geosystems released an integrated interface that automates steering and screed-edge control on the Dynapac SD25 and XD25 series.

- March 2025: BOMAG Americas unveiled the CR 820 T-2 rubber-track paver with a 10-ton hopper and 173-hp diesel engine, targeting steep-grade commercial jobs.

Global Asphalt Pavers Market Report Scope

An asphalt paver is a machinery utilized for road pavements. These machines have unique roles to play and mark their existence in the construction of large areas of pavement. An asphalt paver is a self-propelled laydown machine that has two main assemblies, i.e., a tractor and screed, used to spread hot mix asphalt.

The asphalt pavers market is segmented by type, paving range, application, end-user, and geography. By type, the market is segmented into tracked pavers, wheeled pavers, and screeds. By paving range, the market is segmented as less than 1.5 m, 1.5 m to 2.3 m, 2.4 m to 2.55 m, and above 2.55 m. By application, the market is segmented as highways and major roads, urban roads and streets, parking lots and driveways, and airport runways and taxiways. By end-user, the market is segmented as government and public agencies, private construction contractors, and rental equipment companies. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. The market forecasts are provided in terms of value (USD) and volume (units).

The report offers market size and forecasts in value (USD) and volume (units) for all the above segments.

| Tracked Pavers |

| Wheeled Pavers |

| Screeds |

| Less than 1.5 m |

| 1.5 to 2.3 m |

| 2.4 to 2.55 m |

| Above 2.55 m |

| Highways and Major Roads |

| Urban Roads and Streets |

| Parking Lots and Driveways |

| Airport Runways and Taxiways |

| Government and Public Agencies |

| Private Construction Contractors |

| Rental Equipment Companies |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Tracked Pavers | |

| Wheeled Pavers | ||

| Screeds | ||

| By Paving Range | Less than 1.5 m | |

| 1.5 to 2.3 m | ||

| 2.4 to 2.55 m | ||

| Above 2.55 m | ||

| By Application | Highways and Major Roads | |

| Urban Roads and Streets | ||

| Parking Lots and Driveways | ||

| Airport Runways and Taxiways | ||

| By End-User | Government and Public Agencies | |

| Private Construction Contractors | ||

| Rental Equipment Companies | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the asphalt paver market?

The asphalt paver market size was USD 3.23 billion in 2026 and is forecast to reach USD 4.15 billion by 2031.

Which type of paver generates the most revenue?

Tracked pavers led with 56.36% revenue share in 2025 due to superior traction on uneven surfaces.

Which application will grow fastest through 2031?

Airport runway and taxiway paving is projected to post a 7.99% CAGR, the highest among all applications.

How will rental fleets affect equipment sales?

Rental companies are growing at 6.17% CAGR, extending replacement cycles yet boosting demand for service contracts and telematics subscriptions.

Which region is poised for the highest growth?

Middle East and Africa will expand at 6.57% CAGR, propelled by oil-funded megaprojects and airport expansions.

Page last updated on: