Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

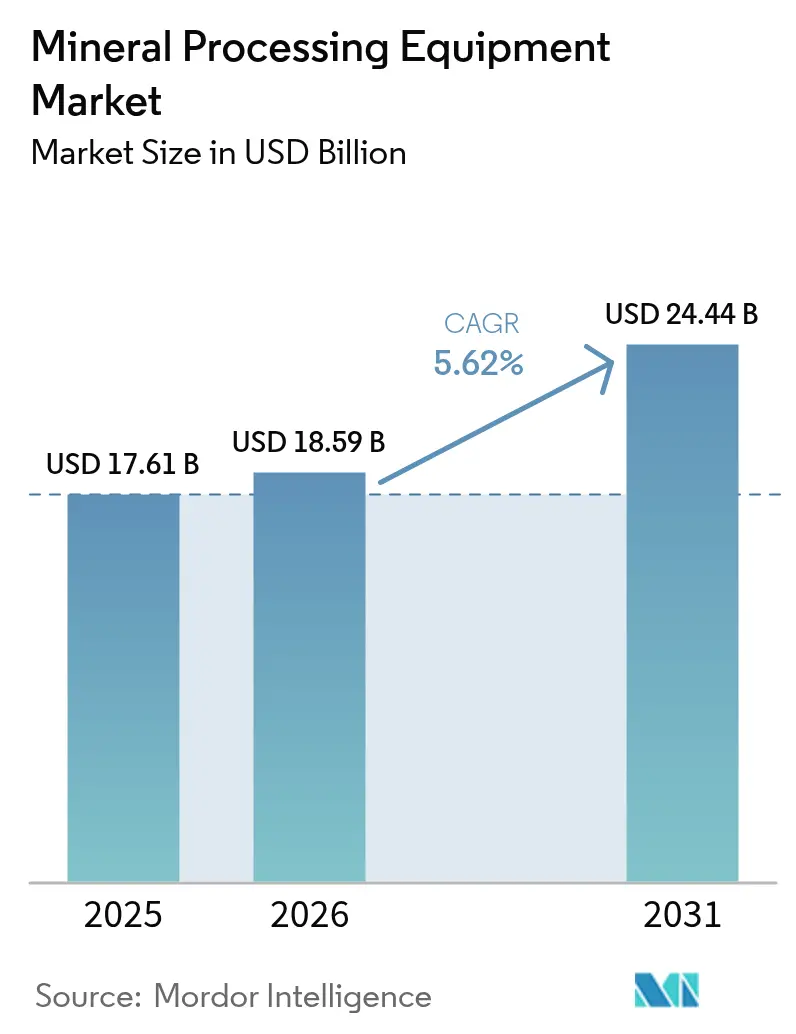

| Market Size (2026) | USD 18.59 Billion |

| Market Size (2031) | USD 24.44 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mineral Processing Equipment Market Analysis by Mordor Intelligence

The Mineral Processing Equipment market size was valued at USD 17.61 billion in 2025 and estimated to grow from USD 18.59 billion in 2026 to reach USD 24.44 billion by 2031, at a CAGR of 5.62% during the forecast period (2026-2031). Continuous ore-grade decline, the energy-transition metals boom, and tightening environmental standards reinforce multi-year investment cycles favoring higher-capacity, digitally enabled plants. Growing demand for lithium, nickel, and rare earth elements pushes equipment orders toward finer-grinding, precision-separation, and advanced dust-control systems. Producers prioritize energy efficiency to reduce cost per tonne and Scope 1 emissions, elevating technologies such as high-pressure grinding rolls (HPGRs) and column flotation. Aftermarket services gain strategic importance as remote mine operators seek guaranteed uptime and predictive maintenance. Supply-chain nationalism adds urgency to domestic processing capacity in North America, Europe, and Asia, further broadening the mineral processing equipment market opportunity.

Key Report Takeaways

- By mineral mining sector, the “Others” category commanded 89.55% share of the mineral processing equipment market size in 2025, whereas lithium processing equipment is expected to expand at a robust 13.58% CAGR to 2031.

- By equipment, crushers and mills held 32.72% of the mineral processing equipment market share in 2025, while flotation cells are projected to record the fastest 5.88% CAGR through 2031.

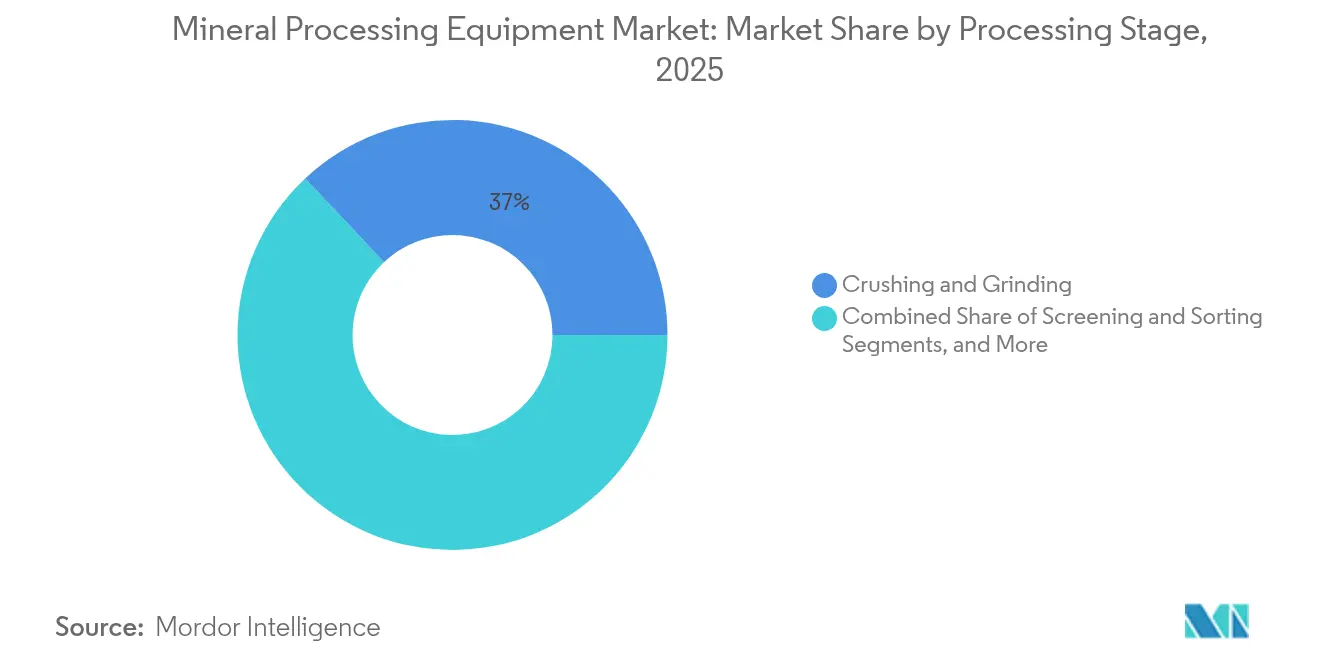

- By processing stage, crushing and grinding accounted for 37.02% of the mineral processing equipment market share in 2025, yet concentration processes are slated to grow at a 5.67% CAGR over the forecast period.

- By end-user industry, mineral and ore mining companies controlled 57.95% of the mineral processing equipment market share in 2025, while recycling and secondary metals processors are set to advance at a 6.05% CAGR through 2031.

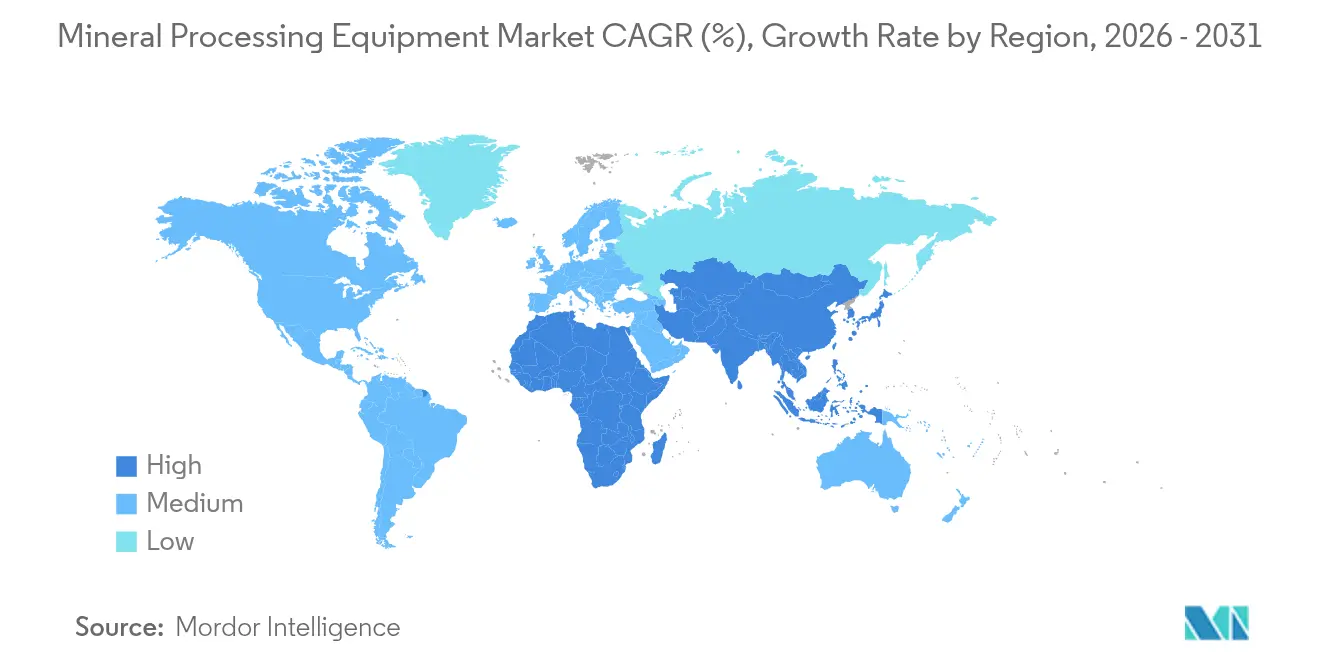

- By geography, Asia-Pacific dominated the mineral processing equipment market with a 67.92% revenue share in 2025, while the Middle East and Africa region is forecast to register the highest 9.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-Battery Metal Boom (Lithium, Nickel) | +2.1% | Global, concentrated in Asia-Pacific and South America | Medium term (2-4 years) |

| Shift to Finer-Grade Ores Driving High-Capacity Crushers | +1.8% | Australia, Chile, South Africa | Long term (≥ 4 years) |

| CAPEX Surge in African Critical-Mineral Projects | +1.2% | Sub-Saharan Africa | Medium term (2-4 years) |

| Digital-Twin Adoption for Plant-Wide Optimization | +0.9% | North America, Europe, advanced Asia-Pacific | Short term (≤ 2 years) |

| Green-Steel Initiatives Increasing Pelletizing Demand | +0.7% | Europe, North America, select Asia-Pacific | Long term (≥ 4 years) |

| AI-Based Ore-Sorting Reducing Downstream Energy Use | +0.6% | Early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV-Battery Metal Boom (Lithium, Nickel)

Soaring demand for battery-grade inputs drives a pronounced shift in the Mineral Processing Equipment market. Lithium projects require specialized roasting, leaching, and crystallization circuits able to deliver 99.5%+ purity levels, prompting new orders for Metso’s pCAM and calciner packages[1]“Advanced Lithium Processing Solutions,”, Metso Corporation, metso.com. Nickel laterite processing equally benefits larger autoclaves, sulfuric-acid leach reactors, and downstream solvent-extraction units. OEMs with high-temperature, high-pressure design credentials command premium margins as investors fast-track integrated battery-metal hubs in Australia, Indonesia, and Chile. The resulting capacity build-out sustains double-digit equipment demand even when bulk-commodity spending moderates. Suppliers also integrate ESG reporting modules that trace cradle-to-gate emissions for each tonne of battery metal.

Shift to Finer-Grade Ores Driving High-Capacity Crushers

Copper, gold, and iron ore head grades continue to fall, obliging plants to process larger tonnages to maintain metal output. HPGR circuits yield 20-40% energy savings and finer product size distributions that elevate downstream flotation recovery, as demonstrated by Weir Group’s ENDURON installs [2].“ENDURON HPGR Energy Savings,”, Weir Group, global.weir Mines in Australia and Chile retrofit primary crushers with 20,000 t/h nameplate capacities, complemented by real-time particle-size analyzers that close the control loop. This cascading effect lifts demand for screens, cyclones, and dewatering equipment sized for higher slurry volumes. Suppliers that provide integrated comminution-to-classification packages capture added service revenue, reinforcing the Mineral Processing Equipment market’s focus on high-throughput, low-specific-energy solutions.

CAPEX Surge in African Critical-Mineral Projects

Record capital expenditure in cobalt, graphite, and rare-earth projects positions Sub-Saharan Africa as the fastest-growing export base for advanced concentrators. Kumba Iron Ore’s UHDMS plant shows how local miners adopt density-based separation to upgrade low-grade feeds [3]“Kumba’s UHDMS Plant Commissioning,”, Anglo American, angloamerican.com. Angola’s Longonjo rare-earth venture requires multi-stage magnetic and gravity modules to meet 99%+ NdPr specifications, opening scope for specialized European OEMs. Infrastructure build-outs—rail spurs, bulk-handling ports, and grid upgrades—enable mega-projects that justify full-line plant purchases. Political-risk premiums remain, yet OEMs mitigate exposure through local service partnerships and flexible vendor-financing terms, ensuring sustained Mineral Processing Equipment market momentum.

Digital-Twin Adoption for Plant-Wide Optimization

ABB and other control-system vendors increasingly embed high-resolution digital twins that mirror every valve, pump, and sensor in real time. Remote-operation centers in Perth and Santiago supervise multiple mines simultaneously, reducing fly-in-fly-out labor spend and safety incidents. Digital twins also support autonomous reagent dosing in flotation, enabling precise pH and frother control for complex polymetallic ores. Cybersecurity architecture remains a barrier; nevertheless, standardized OPC-UA and IEC 62443 frameworks accelerate broader rollouts. Consequently, software revenue becomes a sticky annuity stream inside the Mineral Processing Equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ESG-Driven Capital Rationing for Green-Field Mines | -1.4% | Europe and North America | Short term (≤ 2 years) |

| Tightening Particulate-Matter Emission Norms | -1.1% | Global, intensity varies | Medium term (2-4 years) |

| Skilled-Workforce Shortages in Remote Regions | -0.8% | Australia, Canada, parts of Africa | Long term (≥ 4 years) |

| Geopolitical Supply-Chain Nationalism on Key Spares | -0.6% | United States–China corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

ESG-Driven Capital Rationing for Green-Field Mines

Institutional investors apply stringent ESG filters, slowing approvals for new mines and delaying linked plant orders. Greenfield iron ore and copper projects in Canada now require upfront carbon-neutral processing designs, adding up to 20% to installed costs. Extended permitting cycles compress near-term demand for crushers and mills, even as retrofit orders for dust-suppression and water-recycling systems rise. OEMs respond with modular, relocatable plants that minimize land disturbance and shorten environmental reviews, preserving a pipeline of smaller, faster-moving purchase orders within the Mineral Processing Equipment market.

Tightening Particulate-Matter Emission Norms

The U.S. Environmental Protection Agency’s New Source Performance Standards mandate <0.05 kg/t PM10 thresholds on screening and conveying circuits, driving investment in high-efficiency baghouses and enclosure systems [4]“PM10 Emission Limits for Crushers,”, U.S. Environmental Protection Agency, epa.gov. Similar rules in Canada and the EU further pressure operators to retrofit. Compliance accelerates demand for smart fan-control and filter-condition monitoring, though capital diversion from expansion projects can temper broader market growth. Suppliers that bundle emission-control guarantees with uptime contracts achieve differentiation, sustaining premium pricing within the Mineral Processing Equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Lithium Drives Transformation

Lithium’s meteoric 13.58% CAGR through 2031 underscores structural change inside the mineral processing equipment market. Although bulk commodities under the “Others” banner still generated 89.55% of the mineral processing equipment market size in 2025, battery-metal plants are specifying calcination kilns, solvent-extraction mixers, and crystallizers built for ultra-low impurity thresholds. The Mineral Processing Equipment market captures investor enthusiasm as automakers seek secure, traceable supply chains. Traditional iron-ore and copper flows maintain large volumes; however, their single-digit growth contrasts sharply with double-digit expansion in critical mineral circuits.

Continued head-grade decline in copper and gold extends capex cycles for HPGR, fine-grinding, and flash-flotation gear. Though small in tonnage, rare-earth element circuits demand complex multi-stage separation that commands high unit pricing, lifting margin contribution. Suppliers thus allocate R&D toward hydrometallurgy and selective leaching, balancing legacy bulk-commodity exposure with high-growth specialty segments.

By Equipment: Flotation Innovation Accelerates

Crushers and mills represented the largest 32.72% slice of the mineral processing equipment market size in 2025, yet advanced flotation cells booked the quickest 5.88% CAGR through 2031. Plants processing complex lead-zinc or nickel ores adopt automated air-flow and froth-camera systems to sustain grade. Integrated skid-mounted flotation modules shorten delivery to six months, suiting fast-track lithium projects.

Downstream, high-rate thickeners and paste-fill plants address tailings dam risk, while smart slurry pumps with wear-performance sensors extend the mean time between overhauls. Therefore, the Mineral Processing Equipment market share mix tilts gradually toward separation and tailings handling, reflecting heightened water stewardship and value-recovery priorities.

By Processing Stage: Concentration Gains Momentum

Crushing and grinding held 37.02% of the mineral processing equipment market size in 2025, underlining their indispensable role in mineral liberation. Nevertheless, concentration stages comprising flotation, magnetic, and gravity separation are forecast to log a 5.67% CAGR through 2031, outpacing comminution growth through 2030. AI-enabled sensor-based ore sorting removes 10-15% waste before energy-intensive milling, improving site emissions metrics and plant throughput.

Enhanced dewatering and filtration complete the flowsheet revamp, delivering stackable dry tails that meet tougher global safety codes. Coupled with digital twin orchestration, these advances elevate circuit-wide net recovery, justifying premium capex even amid volatile commodity pricing. Integrated suppliers can furnish “mine-to-mill-to-market” optimisation and secure durable customer lock-in across processing stages.

By End-User Industry: Recycling Emerges

Mineral/Ore Mining Companies still generated 57.95% of the mineral processing equipment market size in 2025. Yet secondary-metal processors show the sharpest 6.05% CAGR through 2031, as governments legislate circular economy mandates. Urban ore plants for spent EV batteries need shredders, hydromet reactors, and cobalt-nickel precipitators engineered for high-impurity feeds. Contract processors handle multi-client concentrates, driving demand for rapid-switch hoppers and flexible control logic.

As steelmakers trial low-carbon direct-reduced iron modules, scrap-based feed blends open new channels for compact pelletizing lines and hot-briquetted iron equipment. End-user boundaries blur: miners invest in recycling to secure ESG credits, while recyclers explore upstream sourcing. Such cross-pollination diversifies revenue sources and underpins steady Mineral Processing Equipment market expansion.

Geography Analysis

Asia-Pacific, with 67.92% of 2025 turnover, remains the nucleus of the mineral processing equipment market. China’s vast smelting and refining backbone absorbs crushers, mills, and filtration packages on an unparalleled scale. Australian iron-ore majors commit to 700+ Mt/y capacity, sustaining HPGR and screening upgrades, while Indonesian nickel laterite projects specify autoclaves and acid-plant tie-ins. India’s Production-Linked Incentive scheme for critical minerals and mining code reforms stimulates greenfield lithium and graphite developments that underpin incremental equipment demand in 2025-2030.

The Middle East and Africa deliver the fastest 9.82% CAGR through 2031, as Saudi Arabia, Namibia, and Angola deploy sovereign capital to monetize phosphate, copper, and rare-earth resources. Solar-powered desalination plants feed water-intensive concentrators, cutting unit opex. Ma’aden’s mega-phosphate complex exemplifies integrated mine-to-fertilizer flows, capturing service contracts for pumps, thickeners, and rotary dryers. Localized maintenance hubs in Durban, Muscat, and Tema mitigate logistics delays, favoring OEMs that invest in on-ground technicians. North America and Europe record mid-single-digit growth rates anchored by supply-chain security agendas. United States federal grants fast-track domestic lithium-hydroxide refineries, benefitting calciner and crystallizer specialists. The EU’s Critical Raw Materials Act subsidizes rare-earth separation and battery recycling, boosting column-flotation and hydromet plant orders. South America’s lithium triangle retains momentum, although water-use restrictions in the high Andes propel the adoption of direct-lithium-extraction (DLE) modules that consume less brine. Geopolitics, ESG imperatives, and resource nationalism jointly reshape regional equipment procurement patterns, sustaining broad-based Mineral Processing Equipment market growth.

Mordor Intelligence provides coverage of the mineral processing equipment market across other key regional markets. Detailed country-level analysis extends to Japan, Mexico, Oman, Egypt, Morocco, South Africa, Italy, Brazil, Saudi Arabia, and Australia incorporating local coverage and market participation, as required.

Competitive Landscape

The Mineral Processing Equipment market features a moderate concentration with major players like FLSmidth expanding its digital suite by integrating advanced process control into its Knelson Gravity concentrators, allowing mine-wide reconciliation dashboards. Metso continues to deploy modular hydrogen-fuel-ready roasting systems, capturing early-mover advantage in low-carbon battery-metal flowsheets. Sandvik’s Rock Processing division benefits from a growing installed base of hybrid surface drills equipped with in-pit ore-grading sensors.

Weir Group leverages its Motion Metrics payload-optimization platform to upsell spare-part kits, lifting lifecycle margin per machine. Epiroc’s May 2024 acquisition spree adds underground automation capabilities, positioning the firm for fleet-agnostic digital contracts. Emerging competitors such as TOMRA, Eriez, and Glencore Technology focus on niche separation and ore-sorting niches, using performance guarantees to displace incumbents in brownfield expansions.

Strategic collaborations intensify: OEMs partner with cloud providers for secure telemetry infrastructure, and with chemical suppliers to co-develop reagent-plus-equipment packages for complex ores. Sustainability credentials act as new battlegrounds; vendors publish cradle-to-gate carbon footprints and offer refurbishment programs that extend equipment life cycles. While price competition persists in mature crusher lines, differentiation pivots toward throughput guarantees, remote-support SLAs, and comprehensive training for local technicians—further consolidating customer relationships inside the mineral processing equipment market.

Mineral Processing Equipment Industry Leaders

FLSmidth A/S

Komatsu Ltd

Sandvik AB

Weir Group

Metso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Rio Tinto plans to invest CAD 7.6 million in an industrial demonstration project at its Lac Tio mine in Havre-Saint-Pierre to evaluate ore sorting technology integration. The Quebec Government will provide CAD 2.5 million for this project through its Support Program for the Scale-up of Mineral Processing or Primary Transformation for Critical and Strategic Minerals.

- February 2025: Sandvik showcased its latest developments in infrastructure, mining, tunneling, and quarrying at Bauma 2025 in Munich. The company presented its advancements in ground support, surface drilling, stationary crushing and screening, rock tools, and parts and services, emphasizing sustainability and digitalization.

Global Mineral Processing Equipment Market Report Scope

Mineral processing equipment is designed to separate ores and mineral products from rock and gangue. It is used in a process wherein ores undergo processing to yield a more concentrated material.

The mineral processing equipment market is segmented into the mineral mining sector, equipment, and geography. Based on the mineral mining sector, the market is segmented into bauxite, iron, lithium, and others. By equipment, the market is segmented into crushers, feeders, conveyors, drills and breakers, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

For each segment, the market sizing and forecast have been done on the basis of value (USD).

| Bauxite |

| Copper |

| Iron |

| Lithium |

| Nickel |

| Rare-earth Elements |

| Gold and Precious Metals |

| Others |

| Crushers and Mills |

| Screens and Separators |

| Feeders and Conveyors |

| Drills and Breakers |

| Thickening and Clarification |

| Flotation Cells |

| Magnetic and Gravity Separators |

| Pumps and Valves |

| Filtration and Dewatering |

| Crushing and Grinding |

| Screening and Sorting |

| Concentration (Flotation/Separation) |

| Dewatering |

| Material Handling |

| Mineral/Ore Mining Companies |

| Contract Processing Plants |

| Recycling and Secondary Metals |

| Aggregates and Construction |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Australia | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Mineral Mining Sector | Bauxite | |

| Copper | ||

| Iron | ||

| Lithium | ||

| Nickel | ||

| Rare-earth Elements | ||

| Gold and Precious Metals | ||

| Others | ||

| By Equipment | Crushers and Mills | |

| Screens and Separators | ||

| Feeders and Conveyors | ||

| Drills and Breakers | ||

| Thickening and Clarification | ||

| Flotation Cells | ||

| Magnetic and Gravity Separators | ||

| Pumps and Valves | ||

| Filtration and Dewatering | ||

| By Processing Stage | Crushing and Grinding | |

| Screening and Sorting | ||

| Concentration (Flotation/Separation) | ||

| Dewatering | ||

| Material Handling | ||

| By End-User Industry | Mineral/Ore Mining Companies | |

| Contract Processing Plants | ||

| Recycling and Secondary Metals | ||

| Aggregates and Construction | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Australia | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Mineral Processing Equipment market in 2026?

The Mineral Processing Equipment market size stands at USD 18.59 billion in 2026 and is forecast to reach USD 24.44 billion by 2031.

Which region dominates demand for mineral processing equipment?

Asia-Pacific leads with 67.92% revenue share, driven by China’s large-scale processing capacity and Australia’s high-throughput iron-ore operations.

What equipment category is growing the fastest?

Flotation cells post the quickest 5.88% CAGR because falling ore grades require more efficient separation to maintain metal recovery.

Why is lithium processing equipment in high demand?

Battery-metal supply chains need ultra-pure feedstock, prompting lithium projects to invest in specialized roasting, leaching, and crystallization circuits.

How are ESG regulations affecting equipment purchases?

Stricter particulate-matter and carbon-emission rules drive investment in dust-control, energy-efficient grinding, and water-recycling systems, influencing overall capex decisions.

Page last updated on: