North America Construction Equipment Rental Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

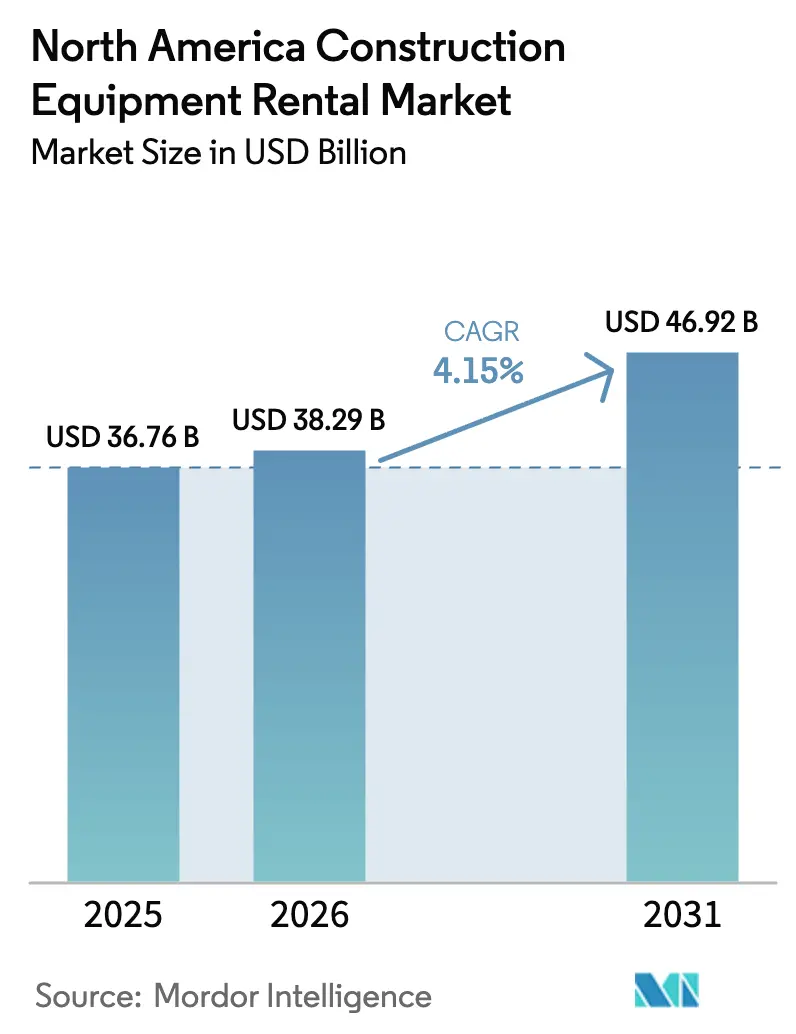

| Base Year Market Size (2025) | USD 36.76 Billion |

| Market Size (2026) | USD 38.29 Billion |

| Market Size (2031) | USD 46.92 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

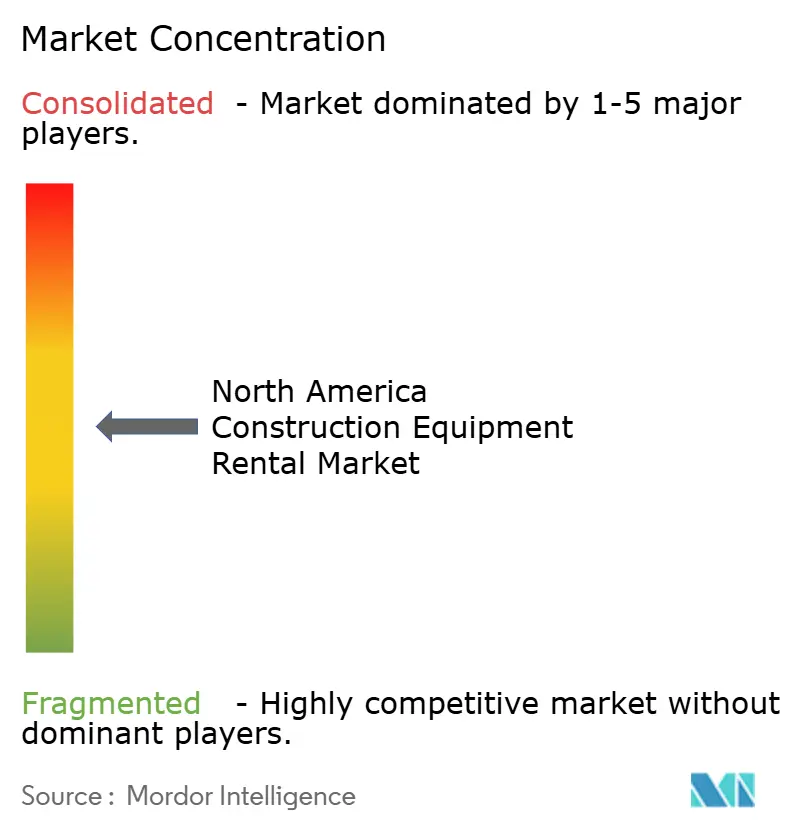

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Construction Equipment Rental Market Analysis by Mordor Intelligence

The North American construction equipment rental market size is expected to grow from USD 36.76 billion in 2025 to USD 38.29 billion in 2026 and is forecast to reach USD 46.92 billion by 2031 at 4.15% CAGR over 2026-2031. Infrastructure Investment and Jobs Act (IIJA) funding, contractor migration toward asset-light business models, and large data-center and renewable-energy projects collectively keep equipment utilization high across the region. Major federal allocations support more than 56,000 transportation schemes, and projects valued above USD 50 million have risen 42%, sustaining consistent excavator and road-equipment demand. Consolidation remains brisk, reinforcing an oligopolistic pricing environment. Labor shortages—estimated at 439,000 additional workers in 2024—are pushing contractors toward rental subscriptions and push-button technologies that offset skilled-operator gaps.

Key Report Takeaways

- By machinery type, excavators led with 36.28% revenue share of the North American construction equipment rental market in 2025, whereas compact track and skid-steer loaders are forecast to advance at a 10.09% CAGR through 2031.

- By drive type, hydraulic/internal-combustion equipment commanded 86.12% of the North American construction equipment rental market size in 2025.

- By application, infrastructure and civil engineering work held a 45.10% share of the North American construction equipment rental market size in 2025, while industrial and special projects are growing fastest at 8.05% CAGR.

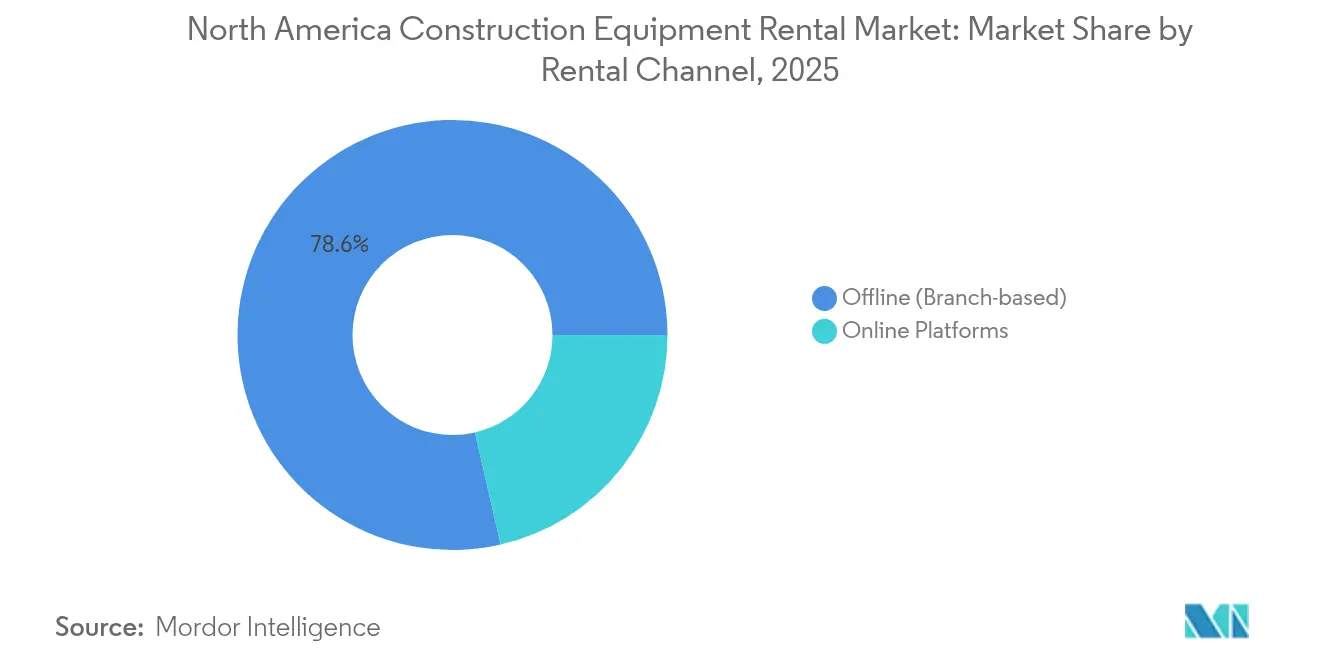

- By rental channel, offline branches retained 78.60% of the North American construction equipment rental market in 2025, yet online platforms are growing at 9.65% CAGR.

- By service type, medium-term contracts (1–12 months) captured 45.30% of the North American construction equipment rental market share in 2025, whereas short-term rentals are increasing at 8.55% CAGR.

- By country, the United States captured around 82.21% share of the North American construction equipment rental market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of North America Construction Equipment Rental Market*

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IIJA-Driven Infrastructure Surge | +1.8% | United States, with spillover to Canada | Long term (≥ 4 years) |

| Contractors Shift to Asset-Light Models | +1.2% | North America, concentrated in Texas, California, Florida | Medium term (2-4 years) |

| Boom in Data Center & Renewable Projects | +0.8% | United States, Canada, with focus on Virginia, Texas, Quebec | Medium term (2-4 years) |

| Fleet Optimization via Telematics | +0.6% | North America, early adoption in Ontario, California | Short term (≤ 2 years) |

| Rise of Equipment-as-a-Service Subscriptions | +0.4% | United States, pilot programs in Northeast, Southeast | Long term (≥ 4 years) |

| Growing Demand for Low-Emission & Hybrid Gear | +0.3% | California, New York, British Columbia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Investment & IIJA Funding Surge

Federal budgets allocate USD 550 billion of new spending, and state agencies downstream this capital into highway, bridge, and transit improvements that require emissions-compliant excavators, road pavers, and cranes. Specifications for resilience against extreme weather further promote premium units equipped with telematics to verify utilization and maintenance cycles. Rental companies can therefore forecast multi-year revenue streams tied to long construction timelines. Capacity constraints among fleet owners prompt additional spot-rental activity whenever project schedules accelerate.

Shift to Asset-Light Models among Contractors

Average equipment rental penetration climbed after contractors reallocated capital toward core project management. United Rentals alone posted USD 13.029 billion rental revenue in 2024, an 8% rise driven by mid-sized builders opting for OPEX rentals instead of CAPEX purchases. These firms value balance-sheet flexibility in an era of fluctuating interest rates and supply-chain volatility.

Rising Demand from Data-Center & Renewable Projects

Utility-scale solar farms, onshore wind farms, and hyperscale server campuses require synchronized lifts, groundworks, and material-handling sessions for short bursts, favoring rentals. Spending forecasts show multi-year growth in digital-infrastructure pipelines, positioning rental fleets with specialized cranes and telescopic handlers for premium margins.

Telematics-Driven Fleet Optimisation

Platforms such as Trackunit’s IrisX aggregate performance readings, location data, and predictive-maintenance alerts across mixed OEM fleets. Operators gain 3–5 percentage-point utilization improvements that directly increase revenue per unit. Early adopters leverage mobility dashboards to implement dynamic pricing, thereby accelerating share gains without fleet expansion.

Restraints Impact Analysis of North America Construction Equipment Rental Market*

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-Labour Shortage for Advanced Equipment | -1.1% | North America, acute in Alberta, North Dakota, Texas | Medium term (2-4 years) |

| High Interest-Rate Driven Fleet CAPEX Pressure | -0.9% | United States, Canada, affecting fleet financing | Short term (≤ 2 years) |

| Antitrust Scrutiny on Alleged Rental Price-Fixing | -0.5% | United States, focused on major metropolitan markets | Medium term (2-4 years) |

| Cross-Border Logistics & CBP Bottlenecks | -0.2% | US-Mexico border states, Texas, California, Arizona | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled-Labour Shortage for Advanced Equipment

A deficit of around 440,000 operators restricts deployment of cranes and aerial work platforms, particularly where regulation requires certified skills. Utilization thus lags equipment availability, and rental companies launch training academies but expect a multi-year payoff.

High Interest-Rate Driven Fleet CAPEX Pressure

Base-rate hikes raise borrowing costs, motivating fleet owners to defer replacement cycles. Smaller regionals face squeezed liquidity, catalyzing mergers as stronger firms cherry-pick distressed peers. The Equipment Leasing & Finance Foundation notes 4.7% investment growth in 2025, slower than prior years[1]“2025 Equipment Investment Outlook”, Equipment Leasing & Finance Foundation, elfaonline.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

North America Construction Equipment Rental Market Segment Analysis

By Machinery Type:

Excavators Lead Despite Compact Equipment SurgeExcavators accounted for 36.28% of the North American construction equipment rental market in 2025 because of their versatility across foundation digging, trenching, and demolition. Compact track and skid-steer loaders, rising at 10.09% CAGR, thrive in urban infill and interior demolition where maneuverability trumps raw capacity. Cranes retain consistent bookings on bridge upgrades, while telescopic handlers fulfill the lift-and-reach demands of warehouse construction. Aerial work platforms register double-digit growth serving high-bay data-center interiors. Operators note that compact loaders deliver 80% of a full-size unit’s output inside city footprint restrictions. Road equipment and motor graders benefit directly from the IIJA stimulus, whereas bulldozers align with earthmoving on renewable-energy projects. The machinery mix illustrates how fleet managers adjust inventories to mirror densifying job-site constraints.

Despite the push toward smaller machines, excavators remain indispensable for major civil works. Contractors prefer rental access to Tier 4-final compliant units rather than owning depreciating assets vulnerable to regulatory updates. Loaders and graders supply consistent volumes for pavement maintenance funded by state fuel-tax programs. Hybrid drive lines appear first in compact ranges because battery packs suit shorter duty cycles, signalling future evolution of larger classes. Telematics pickup reaches 90% penetration among high-value units, letting renters predict wear patterns and schedule mid-rental maintenance to protect uptime.

By Drive Type:

Hydraulic Dominance Faces Electric ChallengeHydraulic and diesel-based powertrains represented 86.12% of the North American construction equipment rental market size in 2025, thanks to proven torque delivery and readily available fuel. Battery-electric variants posted 17.82% CAGR, although from a modest installed base. Hybrid systems—pairing smaller diesel engines with electric assist—offer 20–30% fuel savings without charging downtime, a compelling bridge for contractors sceptical of full electrification. OEM roadmaps suggest compact electric excavators will capture 20% of municipal fleet rentals in California, New York, and British Columbia by 2027 due to incentive schemes.

Infrastructure limitations inhibit the rapid roll-out of fast-charging depots on dispersed sites. Consequently, hydraulic machines continue to dominate heavy categories, including 50-ton excavators, dozers, and graders. However, emissions-cap regulations in port cities spur pilot deployments of electric wheel loaders for material handling. Rental houses negotiate fleet-wide power-purchase agreements with utilities to guarantee on-site charging. Meanwhile, telematics data guides which models are ripe for electrification based on average duty cycles below six hours.

By Application:

Infrastructure Projects Drive Rental DemandInfrastructure and civil engineering claimed 45.10% of the North American construction equipment rental market size in 2025, a direct result of multi-year highway and bridge backlogs. Contractors rely on rentals to meet variable peak demands and to access specialized attachments. Industrial and special projects grow quickest at 8.05% CAGR, propelled by gigawatt-scale solar farms and multimillion-square-foot data centers requiring synchronized lift plans. Building construction maintains moderate momentum, though tighter lending standards impact speculative office starts. Road construction remains resilient owing to earmarked fuel-tax allocations and IIJA’s five-year disbursement guarantees.

Complex project choreography necessitates integrated rental solutions rather than ad-hoc machine drops. Larger rental firms bundle equipment, telematics, and operator onboarding to win turnkey contracts for data-center campuses. Renewable projects prefer low-emission equipment to meet power-purchase-agreement criteria, prompting hybrid crane demand. The shifting mix underscores how specialty projects generate higher daily rates than commodity residential builds, encouraging fleet diversification.

By Rental Channel:

Digital Transformation Accelerates Despite Branch DominanceBranch operations held 78.60% of the North American construction equipment rental market in 2025, supported by deep local relationships and on-site service trucks capable of a two-hour repair response. Online portals advance at 9.65% CAGR as contractors embrace self-service booking and transparent pricing. Platforms integrate with project-management tools to pre-populate rental schedules, reducing administrative overhead. BigRentz, for example, partners with lenders to bundle equipment and materials financing, expanding credit access to subcontractors.

Yet complex orders, such as 300-ton lattice-boom cranes, still require engineered lift plans and on-site surveys best delivered through branch specialists. Hybrid models emerge: national firms route standardized skid-steer orders through apps while routing high-touch inquiries to territory managers. Fleet analytics reveal online channels capture incremental customers rather than cannibalizing existing accounts, suggesting digital ecosystems extend the overall addressable market.

By Service Type:

Medium-Term Contracts Balance Flexibility and EconomicsMedium-term rentals (1–12 months) represented 45.30% of the North American construction equipment rental market share in 2025 because they align with typical project phases while securing volume discounts against daily rates. Infrastructure packages often specify rolling 90-day equipment windows subject to extension clauses. Long-term contracts exceed 12 months for mining and large infrastructure, but risk obsolescence given fast-changing emissions regulations.

Short-term rentals under 30 days expand at 8.55% CAGR, enabled by telematics that expedite asset tracking and billing accuracy. Urban contractors deploy compact loaders for weekend demolition, returning units Monday to avoid idle charges. Digital apps automate delivery scheduling and remote off-hire confirmation, compressing administrative cycles. Subscription models blur traditional tenure categories, offering usage-based billing that flexes with project progress.

Geography Analysis

United States Construction Equipment Rental Market

The United States contributed 82.21% of the North American construction equipment rental market in 2025 on the back of broad IIJA disbursements. Illinois alone earmarked USD 21.3 billion for highway and bridge upgrades that rely heavily on excavators, pavers, and aerial platforms. Consolidation remains a defining feature: Herc Holdings’ USD 5.3 billion purchase of H&E Equipment Services creates a challenger with USD 5.2 billion revenue across 600 depots, elevating competition in top metropolitan areas. Persistent labour shortfalls constrain utilization; rental firms respond by bundling operator certification programs to unlock latent equipment hours.

Canada Construction Equipment Rental Market

Canada sustained modest expansion, buoyed by resource-sector capital expenditure and provincial infrastructure maintenance. Alberta’s oil-sands projects favor heavy dozers and loaders resilient to sub-zero environments, while British Columbia’s hydroelectric upgrades drive crane rentals. Cross-border deployments allow US fleets to supplement Canadian peak seasons, though currency fluctuations affect rate structures. Provincial grants for low-emission equipment accelerate the adoption of hybrid compact loaders in Vancouver and Toronto municipalities.

Mexico Construction Equipment Rental Market

Mexico is forecast to grow 7.95% CAGR to 2031, outpacing its neighbours. Nearshoring initiatives under USMCA stimulate manufacturing-plant construction in states such as Nuevo León and Coahuila. Doosan Bobcat’s USD 300 million compact-loader facility in Salinas Victoria illustrates OEM commitment to regional capacity and shorter supply chains. Logistics bottlenecks at border crossings encourage rental companies to establish permanent Mexican fleets instead of repositioning US assets. Regulatory complexity and fragmented local competition present entry barriers, yet demand for Tier 4-final compliant machinery creates niches for international players offering emission-compliant units.

Competitive Landscape

The North American construction equipment rental market exhibits moderate concentration with oligopolistic characteristics, where the top 5 players control approximately 40% of rental revenues while hundreds of smaller operators serve local and specialized niches. Competitive strategy centres on telematics deployment, predictive maintenance, and customer-experience enhancements rather than price undercutting. United Rentals’ 10-K outlines objectives to raise fleet productivity per branch by leveraging advanced analytics and cross-selling specialized solutions[2]“United Rentals Form 10-K 2024”, EDGAR Online, sec.gov.

Technology partnerships proliferate: Trackunit supplies IoT modules across mixed fleets, and OEM APIs permit deeper health diagnostics. Companies differentiate through guaranteed uptime programmes that reimburse downtime above defined thresholds, incentivising internal service excellence. Consolidation momentum is expected to continue as interest-rate headwinds squeeze smaller operators’ refinancing options, making them attractive tuck-in targets for nationals seeking geographic fill-in.

Emerging disruptors experiment with equipment-as-a-service, offering flat-rate packages with embedded telematics and digital workflows. However, capital-intensive fleet requirements and relationship-driven procurement temper their scale. Large contractors still value branch proximity and the ability to escalate service requests via local managers. Consequently, traditional rental leaders integrate digital capabilities but maintain regional service footprints to protect share.

North America Construction Equipment Rental Industry Leaders

Deere & Company

United Rentals, Inc.

Herc Rentals Inc.

Caterpillar Inc.

Sunbelt Rentals

- *Disclaimer: Major Players sorted in no particular order

North America Construction Equipment Rental Market Companies Covered in this Report

- United Rentals, Inc.

- Sunbelt Rentals (Ashtead Group plc)

- Herc Rentals Inc.

- Caterpillar Inc.

- Deere & Company

- Volvo Construction Equipment AB

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

- CNH Industrial N.V. (Case Construction)

- Cooper Equipment Rentals Ltd.

- H&E Equipment Services Inc.

- Maxim Crane Works L.P.

- BigRentz Inc.

- DOZR Inc.

- Terex Corporation

- Doosan Bobcat North America

- Kubota North America

- XCMG Group

- Wacker Neuson SE

- Aggreko plc

Recent Industry Developments in North America Construction Equipment Rental Market

- February 2025: Herc Holdings completed the acquisition of H&E Equipment Services for USD 5.3 billion, including USD 1.5 billion debt, creating the third-largest renter with anticipated USD 300 million annual EBITDA synergies by year three.

- September 2024: Trackunit launched the IrisX data platform, integrating AI and telemetry across 1,200 systems to lift fleet productivity.

- June 2024: Doosan Bobcat announced USD 300 million investment for a compact-loader plant in Salinas Victoria, Mexico, opening 2026 and boosting global capacity 20%.

- May 2024: Herc Rentals acquired Rental Works of Maryland, adding three depots across Maryland, Washington D.C., and Northern Virginia.

North America Construction Equipment Rental Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the North American construction equipment rental market as the yearly gross revenue earned by general and specialty rental firms from leasing earth-moving, material-handling, road-building, aerial work, and related heavy machinery to contractors and industrial users across the United States, Canada, and Mexico. Revenues from tool-only hire centers, outright equipment sales, re-rentals, and pure financing leases are outside this calculation.

Scope exclusion: Portable hand tools, temporary site infrastructure such as mobile generators or scaffolding, and service-only contracts are not covered.

Segments Covered in This Report

- By Machinery Type

- Cranes

- Telescopic Handlers

- Excavators

- Loaders

- Motor Graders

- Road Construction Equipment

- Aerial Work Platforms

- Compact Track & Skid-Steer Loaders

- Bulldozers

- Others

- By Drive Type

- Hydraulic / IC Engine

- Hybrid

- Electric

- By Application

- Building Construction

- Infrastructure & Civil Engineering

- Road Construction

- Industrial & Special Projects

- Others

- By Rental Channel

- Offline (Branch-based)

- Online Platforms

- By Service Type

- Short-Term Rental (Less than 1 Month)

- Medium-Term Rental (1 - 12 Months)

- Long-Term Rental (Over 1 Year)

- By Country

- United States

- Canada

- Rest of North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts complemented the desk work with interviews and structured questionnaires directed at fleet managers, OEM channel partners, and contractor associations across key US states and Canadian provinces. Discussions clarified live daily-rate movements, anticipated electric compact-loader penetration, and average fleet churn cycles; these insights tuned assumptions and stress tests.

Desk Research

We began with structured desk work that pulled tariff-coded import data from the US International Trade Commission and fleet-utilization updates from the American Rental Association, followed by highway spending tables from the Federal Highway Administration and monthly housing-start statistics from the US Census. Annual reports, 10-Ks, and investor decks from listed rental operators revealed price curves and utilization ratios, while project pipelines from Infrastructure Canada and Mexico's Secretariat of Communications and Transport calibrated regional demand. Subscription sources, including D&B Hoovers and Dow Jones Factiva, added company-level revenue splits and news sentiment. This list is illustrative; many other public and paid sources supported data collection, validation, and clarification.

Market-Sizing & Forecasting

A single top-down build starts from 2024 public rental-revenue filings and American Rental Association regional ratios, which are then allocated by equipment class using trade and production splits. Selective bottom-up cross-checks, such as sampled average daily rate multiplied by active units, validate totals and adjust variance. Core drivers modeled include fleet-utilization percentage, average daily rental rate, infrastructure capital outlay, housing starts, equipment replacement age, and the federal funds rate. Multivariate regression projects each driver through 2030, while scenario analysis cushions regulatory or macro shocks. Any subclass gaps are bridged with proxy ratios drawn from interviewed fleets.

Data Validation & Update Cycle

Outputs pass a two-step peer review. Anomalies above three percent trigger model reruns and fresh source checks. We refresh every twelve months and issue an interim pulse when stimulus packages, emission rules, or major mergers materially shift the baseline.

How Mordor Intelligence's North America Construction Equipment Rental Market Size Compares to Other Published Estimates

Published estimates often diverge because firms choose different revenue lenses, geographic splits, and refresh cadences.

Key gap drivers include the inclusion of short-term tool hire, contrasting residual-value pass-through assumptions, and uneven inflation adjustments.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 36.8 Bn (2025) | Mordor Intelligence | |

| USD 62.2 Bn (2024) | Regional Consultancy A | Counts tool hire and oil-field support fleets, inflating scope |

| USD 58.5 Bn (2024) | Global Consultancy B | Values fleet at acquisition cost rather than net rental revenue |

| USD 42.6 Bn (2022) | Trade Journal C | Applies straight-line inflation to an outdated base year |

These contrasts show that Mordor's disciplined scope selection, driver-level modeling, and annual refresh deliver a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the North American construction equipment rental market?

The market stands at USD 38.29 billion in 2026 and is projected to reach USD 46.92 billion by 2031.

Which machinery type holds the largest rental share?

Excavators dominate with 36.28% revenue share in 2025, reflecting their versatility across infrastructure and commercial works.

How fast are electric construction machines growing in rentals?

Electric drive systems post an 17.82% CAGR through 2031, supported by emissions regulations in California, New York, and British Columbia.

Why are rental companies investing in telematics platforms?

Telematics lift equipment utilization by 3–5 percentage points, enable predictive maintenance, and support dynamic pricing strategies.

Which country is the fastest-growing market in North America?

Mexico expands at 7.95% CAGR to 2031 due to nearshoring-driven factory construction and infrastructure upgrades.

Page last updated on: