Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

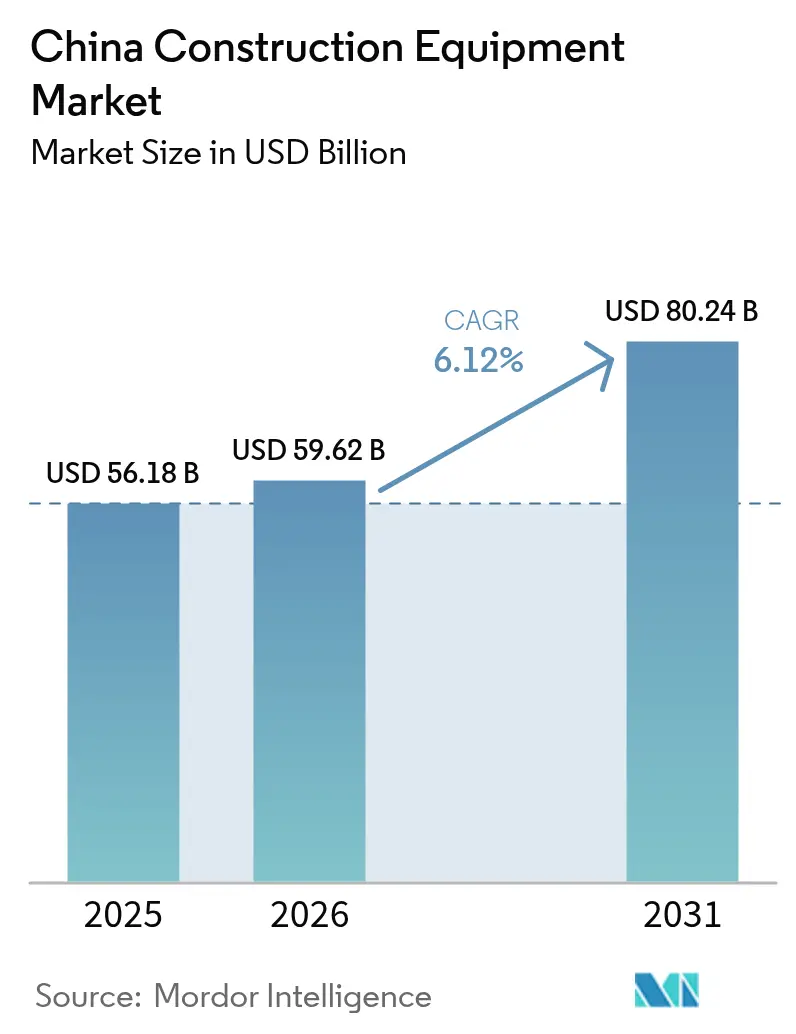

| Base Year Market Size (2025) | USD 56.18 Billion |

| Market Size (2026) | USD 59.62 Billion |

| Market Size (2031) | USD 80.24 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

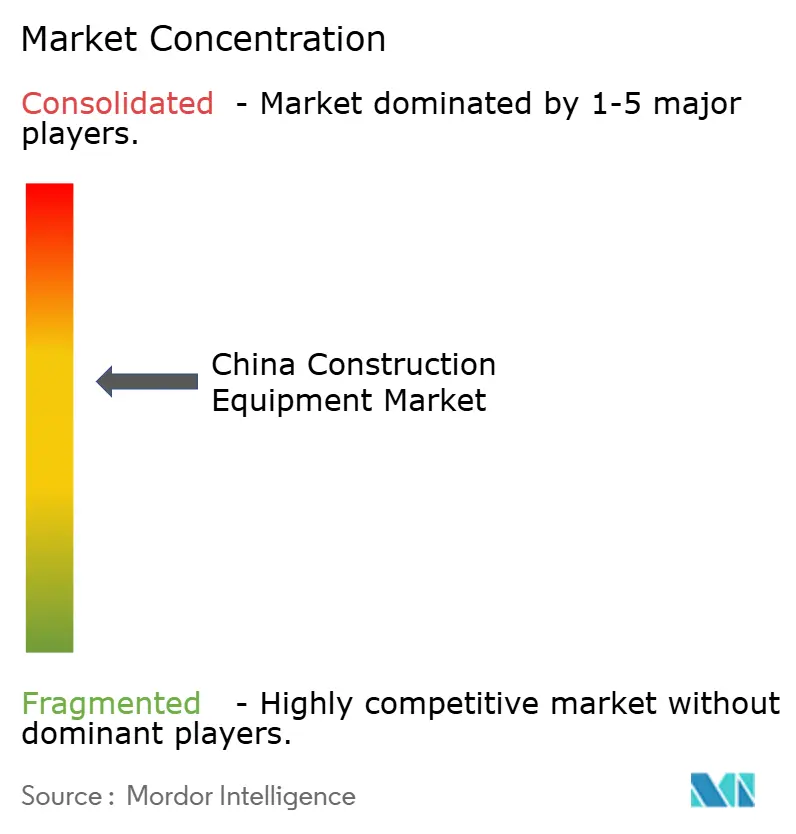

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Construction Equipment Market Analysis by Mordor Intelligence

The China construction equipment market size is expected to increase from USD 56.18 billion in 2025 to USD 59.62 billion in 2026 and reach USD 80.24 billion by 2031, growing at a CAGR of 6.12% over 2026-2031. The expansion reflects Beijing’s shift from residential property toward policy-led infrastructure and export-oriented production[1]“NDRC Announces Early-Batch Major Projects for 2026,” National Development and Reform Commission, ndrc.gov.cn. Carbon-neutrality rules, rising export penetration, and digital rental models are realigning competitive priorities. Electric drive systems, although still a niche, are scaling quickly as compliance costs climb. Meanwhile, an extended housing slump and semiconductor shortages dampen headline growth, creating a measured but durable trajectory for the Chinese construction equipment market.

Key Report Takeaways

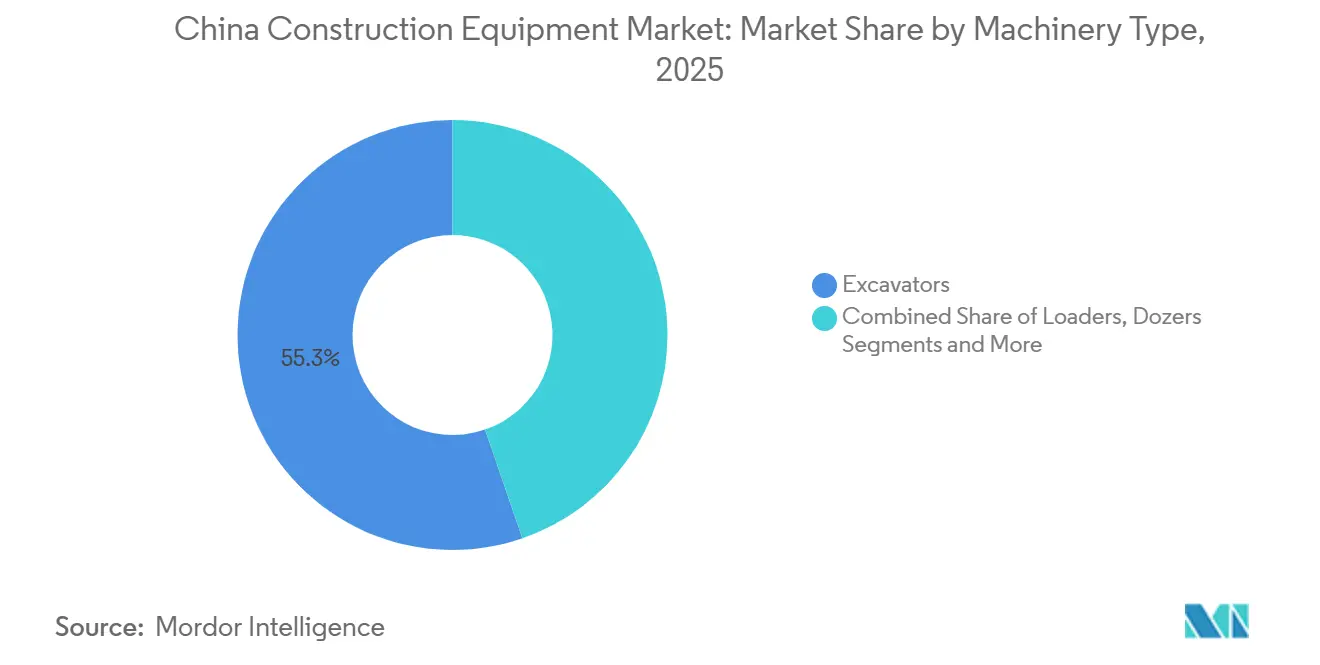

- By machinery type, excavators led with 55.28% of the China construction equipment market share in 2025, while full-electric excavators are expected to post the fastest 12.15% CAGR through 2031.

- By drive type, diesel equipment held 92.64% of the Chinese construction equipment market in 2025; full-electric systems are projected to expand at a 37.85% CAGR through 2031.

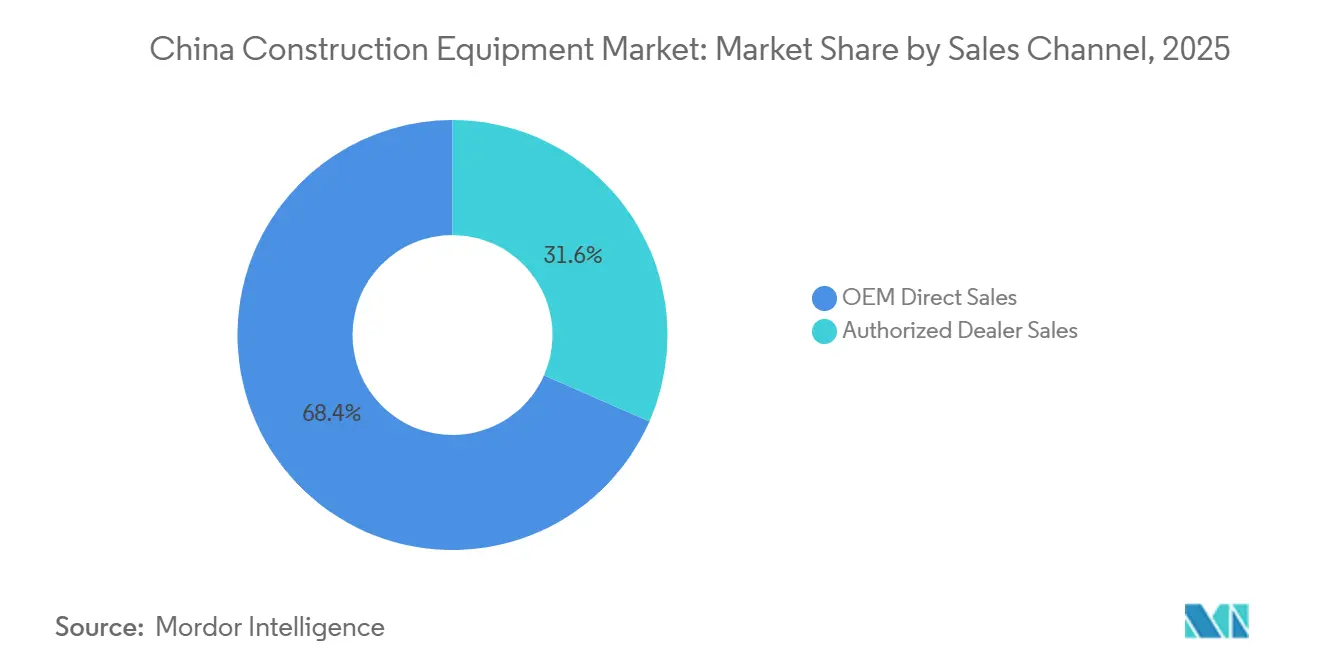

- By sales channel, OEM direct sales commanded 68.42% of 2025 revenue, whereas authorized dealers are expected to record the highest 11.51% CAGR during 2026-2031.

- By application, infrastructure construction accounted for a 45.87% share in 2025, and renewable-energy projects are expected to advance at a 14.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| New Infrastructure Pipeline | +1.8% | Nationwide, with concentration in Xinjiang, Tibet, Guangdong, Jiangsu, Shandong | Long term (≥ 4 years) |

| Carbon-Neutral Mandate | +1.5% | Guangdong, Zhejiang, Jiangsu, Shanghai, Beijing | Medium term (2-4 years) |

| OEM Export Push | +1.2% | Manufacturing hubs in Hunan, Jiangsu, Shandong, Guangxi | Medium term (2-4 years) |

| Digital Equipment-Rental Platforms | +0.9% | Tier-2 and Tier-3 cities across Henan, Sichuan, Anhui, Hubei | Short term (≤ 2 years) |

| Belt and Road Back-Orders | +0.6% | Coastal provinces: Guangdong, Zhejiang, Jiangsu, Shanghai | Medium term (2-4 years) |

| Provincial Carbon-Credit Markets | +0.4% | Guangdong, Shenzhen, Shanghai, Beijing pilot zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government ‘New Infrastructure 2025-30’ Pipeline

Central planners have placed transport links, water projects, and power-grid corridors at the heart of the next 5-year build-out. The early-batch project list has already accelerated tender activity for excavators, cranes, and road equipment. Contractors active in remote western provinces prefer domestic brands that can respond quickly to terrain and climate challenges. Equipment-rental demand is also rising as firms opt for asset-light participation in multi-year construction packages. Together, these shifts anchor a dependable stream of orders even as residential construction lags.

Carbon-Neutral Mandate Spurring Electric Machinery

China’s emissions-trading scheme now prices carbon for heavy industry, forcing site managers to weigh lifetime fuel and compliance costs more carefully. Zero-emission models are therefore moving from demonstration fleets into regular procurement lists, especially for urban projects that face strict air-quality targets. Local governments in coastal provinces offer expedited permits and publicity benefits to contractors using electric fleets. Manufacturers respond by expanding battery and drivetrain capacity while refining after-sales support to reduce buyers’ perceived risk. These non-price incentives accelerate adoption beyond what pure economics would dictate.

OEM Export Push Enables Domestic Economies of Scale

Facing margin pressure at home, leading Chinese brands have elevated overseas growth to a board-level priority. Belt and Road contracts create high-volume backlogs, enabling longer production runs and lower unit costs. Larger batch sizes also fund R&D for electrification and autonomy, reinforcing the cycle. As global customers grow familiar with Chinese machines, brand acceptance improves, further widening export lanes. The virtuous loop strengthens domestic suppliers while heightening competitive stakes for smaller peers.

Digital Equipment-Rental Platforms Unlocking SME Demand

Online marketplaces now match idle fleets with contractors that once lacked capital or credit. Automatic scheduling tools, verified maintenance records, and standardized contracts have significantly reduced transaction friction. Rural and lower-tier-city builders, in particular, favor mobile apps that bundle machine hire, parts, and micro-financing. Rising platform liquidity makes utilization more predictable for fleet owners, encouraging further listings. Over time, this ecosystem may change the ownership model from buy-and-hold to pay-per-use, expanding addressable demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-Estate Downturn | -1.8% | Tier-1 and Tier-2 cities: Beijing, Shanghai, Guangzhou, Shenzhen, Hangzhou, Chengdu | Medium term (2-4 years) |

| Domestic Price Wars | -1.2% | Manufacturing clusters in Hunan, Jiangsu, Shandong, Guangxi | Short term (≤ 2 years) |

| Tight Credit to SME Contractors | -0.8% | Tier-3 and Tier-4 cities across Henan, Anhui, Hubei, Sichuan, Shaanxi | Medium term (2-4 years) |

| Inverter and BMS Chip Shortages | -0.5% | Electric equipment production bases in Hunan, Jiangsu, Zhejiang | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Prolonged Real-Estate Downturn

Weak apartment presales continue to undermine private developers' cash flow, curbing demand for concrete pumps, tower cranes, and other building-centric gear. Even state rescue measures have merely slowed, not reversed, the slide. Large rental companies are redeploying fleets from housing to infrastructure, but utilization gaps remain. Manufacturers with heavy exposure to concrete machinery now lean harder on parts and service revenue. Until household sentiment turns, equipment tied to vertical construction is likely to lag broader market growth.

Domestic Price Wars from Over-Capacity

Factories expanded over the years, but now have more production lines than current orders demand. To keep assembly lines running, some brands slash list prices, triggering a chain reaction across the market. Margins thin, threatening investment in advanced components or automation upgrades. Smaller makers risk insolvency, which may eventually tighten supply, but the adjustment period is painful. Buyers reap short-term bargains, yet long-term innovation could suffer if profitability remains depressed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Excavators Anchor Revenue, Electric Variants Lead Innovation

Excavators captured 55.28% of the Chinese construction equipment market share in 2025, giving them a commanding influence over model development and supplier priorities. Their versatility in earthworks, mining, and demolition keeps demand resilient across cycles. Contractors value the growing range of attachments that convert one base machine into multiple task solutions. Meanwhile, rising labor costs elevate interest in semi-autonomous dig modes that reduce operator fatigue. Although full-electric excavators are currently limited, they are expected to achieve the segment's fastest growth, with a 12.15% CAGR projected through 2031, reflecting a gradual transition toward zero-emission solutions.

The rest of the machinery spectrum is adapting to this two-speed reality. Loaders and graders refine drivetrains for fuel savings, while dozers see early trials of hydrogen engines. Material-handling cranes stretch lifting capacities to serve offshore wind and modular housing. Concrete equipment, hit hardest by housing weakness, experiments with digital batching and predictive maintenance to stay relevant.

By Drive Type: Diesel Dominance Persists, Electric Surge Reshapes Outlook

Diesel power retained 92.64% of the Chinese construction equipment market share in 2025, thanks to dense refueling infrastructure and proven uptime in remote areas. Fleet managers appreciate the familiar maintenance routines and broad availability of parts. However, tightening emissions caps and urban noise rules erode diesel’s long-term appeal. Policy incentives, paired with falling battery costs, make the switch increasingly rational for lighter classes.

Full-electric systems, although starting from a low base, are projected to deliver a sector-leading 37.85% CAGR through 2031, underscoring the speed of change once tipping points are reached. Hybrids sit between these poles, offering fuel savings without range anxiety. Some provinces reward them with carbon credits, nudging skeptics toward partial electrification. Hydrogen pilots probe viability for heavy, continuous-duty tasks. Together, these alternatives sketch a future in which drivetrain choice aligns with specific site constraints rather than a one-size-fits-all diesel.

By Sales Channel: OEM Direct Sales Dominate, Dealers Accelerate in Lower-Tier Cities

OEM direct contracting supplied 68.42% of the Chinese construction equipment market share in 2025, reflecting close ties between large state contractors and major manufacturers. Direct deals streamline customization, bulk discounts, and integrated service packages. Yet the addressable customer base is finite, pushing brands to nurture other routes. Authorized dealers, projecting an 11.51% CAGR through 2031, bring localized credit, trade-in services, and rapid parts delivery to smaller builders scattered across vast inland regions. Their grassroots relationships unlock pockets of demand that corporate sales teams find costly to reach.

Completing the landscape, digital rental platforms empower contractors to book equipment by the hour, sidestepping hefty capital expenditures. Early adopters are drawn to this model, allowing them to trial electric equipment without the commitment of full ownership. As data-driven pricing algorithms become more refined, platform operators enhance their fleet sourcing capabilities. In the long run, diversifying the channel mix could stabilize revenues and bolster after-sales support nationwide.

By Application: Infrastructure Leads, Renewable Energy Gains Pace

Infrastructure construction accounted for 45.87% of the Chinese construction equipment market share in 2025, underpinned by long-duration public works that buffer the industry from residential volatility. Projects ranging from rail corridors to water management require diverse fleets, keeping both heavy and compact equipment in steady rotation. Clear project pipelines let OEMs schedule production more efficiently and tailor service hubs along key routes. The work also favors domestic brands familiar with local regulations and terrain.

Renewable-energy builds, paced for a 14.48% CAGR through 2031, now inject fresh momentum by introducing specialized lifting and earthmoving needs unique to wind and solar farms. Building construction remains subdued as developers deleverage, but prefab and industrial parks offer niche opportunities. Mining and resource projects maintain dependable baseline orders, anchoring demand in commodity-rich provinces. Municipal upgrades, from smart lighting to flood defenses, provide steady, smaller-ticket orders that suit rental fleets. Collectively, these varied applications diversify risk and keep factories humming even when one segment cools.

Geography Analysis

Coastal provinces, Guangdong, Jiangsu, Zhejiang, and Shandong, house the bulk of production capacity, supplier clusters, and export logistics for the Chinese construction equipment market. Guangdong leads electrification, supported by an active regional carbon market that raises diesel operating costs. Jiangsu, anchored by XCMG’s Xuzhou base, benefits from mature component ecosystems and proximity to Shanghai’s ports, thereby accelerating export cycle times.

Shandong specializes in heavy earth-moving equipment serving nearby mining activity, providing counter-cyclical insulation when housing wavers. Western regions exhibit the steepest demand ramp courtesy of state-funded mega-projects. The Yarlung Tsangpo hydropower development and the Xinjiang-Tibet Railway require fleets of excavators, loaders, and concrete pumps over a multi-year horizon, shifting equipment flows inland.

Domestic diesel units currently perform well in high-altitude conditions, while pilot schemes are exploring the feasibility of hydrogen and hybrid systems. Central provinces such as Hunan host R&D and advanced manufacturing parks, with Sany and Zoomlion expanding digital factories to shorten prototype cycles and embed telematics in standard offerings. Tier-3 urban clusters in Henan, Sichuan, Anhui, and Hubei offer untapped rental demand, spurring dealer expansion and platform experimentation.

Regulatory Landscape

China is tightening environmental compliance for non-road mobile machinery under the supervision of the Ministry of Ecology and Environment (MEE). On June 18, 2026, MEE released a public consultation draft for China Phase V emission standards for non-road mobile machinery and engines, with the consultation window running to July 18, 2026, signaling a new round of aftertreatment and calibration upgrades for OEMs and importers as final parameters and enforcement timelines are clarified.

Parallel to emissions, safety and noise standardization is advancing through national standards bodies. GB 45943-2025 (common safety requirements for building construction machinery and equipment) was released on June 30, 2025 and implemented on July 1, 2026, while GB 48002-2026 (earth-moving machinery safety technical specification) was issued on January 28, 2026 with implementation set for February 1, 2027. Noise compliance also tightened as GB 16710-2025 replaced GB 16710-2010, adding another design and validation layer for earthmoving equipment placed on the market.

Value Chain Analysis

China construction equipment value creation is anchored in large OEM-led manufacturing clusters and their dense supplier ecosystems. The Changsha cluster (anchored by Sany and Zoomlion) and the Xuzhou cluster (anchored by XCMG) concentrate engineering, fabrication, and Tier-1/Tier-2 component supply spanning hydraulics, transmissions, castings, and structural steel, which supports rapid iteration in core earthmoving lines such as excavators that dominate domestic volumes.

Downstream, distribution is split between OEM direct sales to large contractors, expanding dealer coverage into lower-tier cities, and a growing layer of digital rental platforms that aggregate fleets and smooth utilization. The export-led portion of the chain is becoming more logistics-integrated and partnership-driven: XCMG signed a strategic agreement with COSCO SHIPPING Lines in January 2026 to integrate manufacturing with cross-border logistics and green, digital supply-chain capabilities. At the component and capability layer, OEMs are using partnerships to raise attachment and automation performance (for example, Sany and Epiroc signed a global partnership in May 2026 for hydraulic breakers and ground-engaging tools), while robotics and intelligent control collaborations (such as Shantui with Luoshi Robot Group in June 2026) point to a supply chain that increasingly includes software, sensors, and autonomous-control subsystems alongside traditional mechanical parts.

Competitive Landscape

The Chinese construction equipment market is characterized by moderate and intense rivalry. Domestic leaders, Sany, XCMG, Zoomlion, Shantui, and LiuGong, command scale advantages but face shrinking margins amid price competition. Each pursues overseas diversification: SANY opened an industrial park in South Africa, XCMG localized assembly in Brazil and Saudi Arabia, and Zoomlion leverages convertible bond financing to fund the build-out of its export channel.

Technology differentiation is widening. Sany filed 246 patent applications in H1 2025, targeting low-carbon components[2]"SANY Reports Strong First Half 2025 Results, Delivering Profitable Growth", SANY Group, sanyglobal.com. XCMG commercialized autonomous underground mining trucks, and Shantui introduced the world’s first AI-driven dozer. International incumbents, Caterpillar, Komatsu, Volvo CE, Liebherr, and Hitachi, retain brand cachet but ceded share as domestic OEMs closed feature gaps at lower price points. Consolidation is expected as cash-flow pressure forces weaker firms to merge or exit.

After-sales service is becoming increasingly crucial. Domestic OEMs are integrating telematics platforms, allowing them to monitor equipment uptime and predict maintenance needs, addressing past service quality issues. Furthermore, by acquiring European hydraulic suppliers and forging battery partnerships with local cell manufacturers, these firms are securing essential components for the future of electrification and autonomy, ensuring long-term competitiveness.

China Construction Equipment Industry Leaders

-

Sany heavy industry Co. Ltd.

-

Zoomlion Heavy Industry Science and Technology Co., Ltd.

-

Shantui Construction Machinery Co., Ltd.

-

Xuzhou Construction Machinery Group Co., Ltd. (XCMG)

-

Guangxi LiuGong Machinery Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy-led equipment renewal and decarbonization are creating whitespace beyond the traditional real-estate cycle, particularly for low-emissions fleets, retrofit-ready platforms, and higher-value services. The Work Plan for Stable Growth of the Machinery Industry (2025-2026) explicitly targets upgrades of high-energy-consumption and high-pollution equipment and identifies construction machinery as a core sector for demand expansion, aligning with the market shift toward electrification and compliance-driven replacement. Reinforcing this, the Ministry of Finance introduced fiscal and financial policies on January 20, 2026 that include equipment-upgrade loan interest subsidies of up to 50 million yuan per enterprise, which directly lowers the cost barrier for contractors and fleet operators considering replacement cycles.

An additional opportunity is the move from standalone machine sales toward intelligent, connected fleet solutions and export-capable configurations. The Chinese Academy of Engineering technology roadmap (2025) emphasizes high-end, intelligent, and green manufacturing, including AI, big data, and Industrial IoT integration, supporting OEM investments in telematics, remote operation, and smart construction workflows. Export channels also provide a tangible pull for higher-spec equipment and more standardized after-sales networks, illustrated by Zoomlion reporting international revenue approaching 60% of its total in its 2025 results disclosure and by OEM-logistics integration efforts such as XCMG and COSCO SHIPPING Lines. These signals support opportunities in electrified earthmoving lines, intelligent attachments and automation kits, and service models that bundle uptime guarantees, parts, and digital monitoring for domestic infrastructure contractors and overseas buyers.

Recent Industry Developments

- June 2026: Shantui Construction Machinery and Luoshi Robot Group signed a strategic cooperation agreement to develop intelligent excavator control systems, autonomous excavating robots, and intelligent manufacturing production lines. The move strengthens Shantui's pathway to AI-enabled earthmoving products while also targeting production efficiency improvements that support cost competitiveness during domestic price pressure.

- August 2025: Volvo Construction Equipment agreed to sell its stake in China's SDLG for USD 837 million. The divestment reshapes competitive positioning around SDLG's installed base and distribution footprint and creates room for Chinese players to strengthen channels and product portfolios in segments where SDLG has been a key competitor.

- November 2024: Sany presented new-energy and intelligent construction machinery at Bauma China 2024, highlighting a product direction centered on electrification and smarter machine capabilities. The launch activity underscored how leading domestic OEMs are using major trade platforms to accelerate customer adoption and reinforce export-ready product positioning.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues earned from construction equipment sold and used in China for executing, operating, and maintaining construction activity, including large machines used in earthmoving and site preparation work.

Scope exclusions: The sizing excludes parts and attachments sold as standalone items, routine service-only revenue, and general-purpose industrial handling equipment that is not primarily used on construction sites.

Segmentation Overview

-

By Machinery Type

-

Earth-moving Machinery

- Excavators

- Loaders

- Dozers

-

Material-Handling Machinery

- Cranes

- Fork-lifts

- Telescopic Handlers

-

Road-Construction Machinery

- Motor Graders

- Rollers/Compactors

- Pavers

-

Concrete Equipment

- Concrete Mixers

- Concrete Pumps

-

Earth-moving Machinery

-

By Drive Type

- Internal-Combustion Engine (Diesel)

- Hybrid

- Full-Electric

-

By Sales Channel

- Original Equipment Manufacturer (OEM) Direct Sales

- Authorized Dealer Sales

-

By Application

- Building Construction

- Infrastructure Construction

- Energy and Natural Resources

- Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with a structured pass through public statistics and policy signals that influence equipment demand in China. We relied on sources such as the National Bureau of Statistics of China (fixed asset investment and construction indicators), China Customs trade data (imports and exports by machinery codes), and ministry-level infrastructure and energy project releases to understand the demand backdrop.

To keep pricing and volume assumptions grounded, we also reviewed customs unit values, listed-company annual reports and investor presentations, and reputable industry association pages and press releases that discuss equipment output, sales trends, and product shifts (like electric and hybrid machines). For technology direction, we used patent databases and peer-reviewed engineering journals as supporting evidence on electrification and automation. These desk sources are illustrative only, and additional public references were used for collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary discussions were run with equipment makers, dealers, rental fleet operators, contractors, and large end users that purchase machines for infrastructure and building activity. We used these calls to validate the demand drivers behind excavators, loaders, cranes, and road machinery, and to stress-test our assumptions on pricing, replacement cycles, and channel margins across provinces.

Because China is a large single-country market with varied regional construction intensity, we checked views from coastal manufacturing hubs and inland demand centers, then reconciled differences before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | |

| Mid tier: 48% | Functional/Unit leaders: 31% | |

| Smaller Players: 18% | Managers: 56% |

Market-Sizing & Forecasting

Our sizing uses a top-down build that reconstructs China equipment demand from construction and infrastructure spending signals, followed by category-level penetration and replacement logic to translate activity into machine volumes. Once these demand pools are built, the value is calculated using average selling prices that are adjusted for mix changes across machinery types, drive types, and sales channels.

To keep the result practical, we corroborate the totals with selective bottom-up approximations, including sampled unit volumes by equipment type, dealer and rental channel checks, and sanity checks against trade flows for relevant machinery codes. When gaps exist in public volume reporting, the missing pieces are filled using conservative share-based splits that are then validated through interviews.

For forecasting, scenario analysis is used around a central case, because construction starts, infrastructure funding pace, and credit conditions can shift quickly. Key inputs we track include fixed asset investment trends, major project pipeline visibility, housing and infrastructure activity indicators, equipment replacement cycles, and the pace of electrification adoption that affects pricing and mix.

Data Validation & Update Cycle

Validation is done through multiple checks so the final number is not driven by any single data series. We compare the modeled value and implied unit volumes against independent signals like trade movements, listed-company commentary, and visible changes in rental utilization and dealer inventory, and then we investigate any material variance before sign-off.

A multi-step analyst review is followed, where assumptions, formulas, and year-over-year movements are rechecked for reasonableness. The report is refreshed annually, and interim updates are triggered when major policy moves, sharp demand shocks, or notable pricing changes are observed. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's China Construction Equipment Market Estimate Compared With Other Published Estimates

Published market sizes for China construction equipment can look far apart because firms do not always count the same product boundaries, years, and revenue points in the chain. Differences also come from how pricing is handled during mix shifts, and whether demand is tied back to construction activity or projected mainly from historical sales trends.

Export and import movements in construction machinery codes, combined with local construction activity indicators and channel checks on dealer inventory, are the evidence used to keep Mordor Intelligence aligned to the equipment demand pool in China and to avoid counting adjacent off-highway categories. The spread in published values is also affected by whether used equipment, mining-only machines, or broader off-highway equipment is included, and by the choice of base year currency timing and refresh cadence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 56.18 B (2025) | |

| Industry Publisher A | USD 26.17 B (2025) | This estimate appears to use a narrower value pool and a different 2024 to 2025 base sizing path, which can undercount higher-value machinery categories and channel markups when compared with a demand-linked model. |

| Global Consultancy B | USD 60.45 B (2024) | This figure is for a broader off-highway equipment scope that also covers non-construction categories and often includes mining and agriculture equipment, so the boundary is wider than construction equipment alone. |

The table shows that differences mainly come from scope control and the activity signals used to translate construction demand into equipment value. By keeping inclusions specific to construction equipment sold in China, and by checking implied volumes and pricing against observable market indicators, the final market size stays transparent and repeatable year to year.

Key Questions Answered in the Report

How large is the China construction equipment market in 2026?

The market stands at USD 59.62 billion in 2026 and is forecasted to reach USD 80.24 billion by 2031.

Which machinery type leads demand in China?

Excavators contribute the largest share, accounting for 55.28% of 2025 revenue.

What is the fastest-growing drive technology?

Full-electric drive systems expand at an expected 37.85% CAGR through 2031.

How important are exports for Chinese OEMs?

Leading brands already generate more than half of their revenue overseas, using Belt and Road projects to absorb capacity.

Why are digital rental platforms gaining traction?

They reduce capital barriers for SME contractors and lower idle time, especially in tier-2 and tier-3 cities.

Page last updated on: