In Vitro Toxicology Testing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

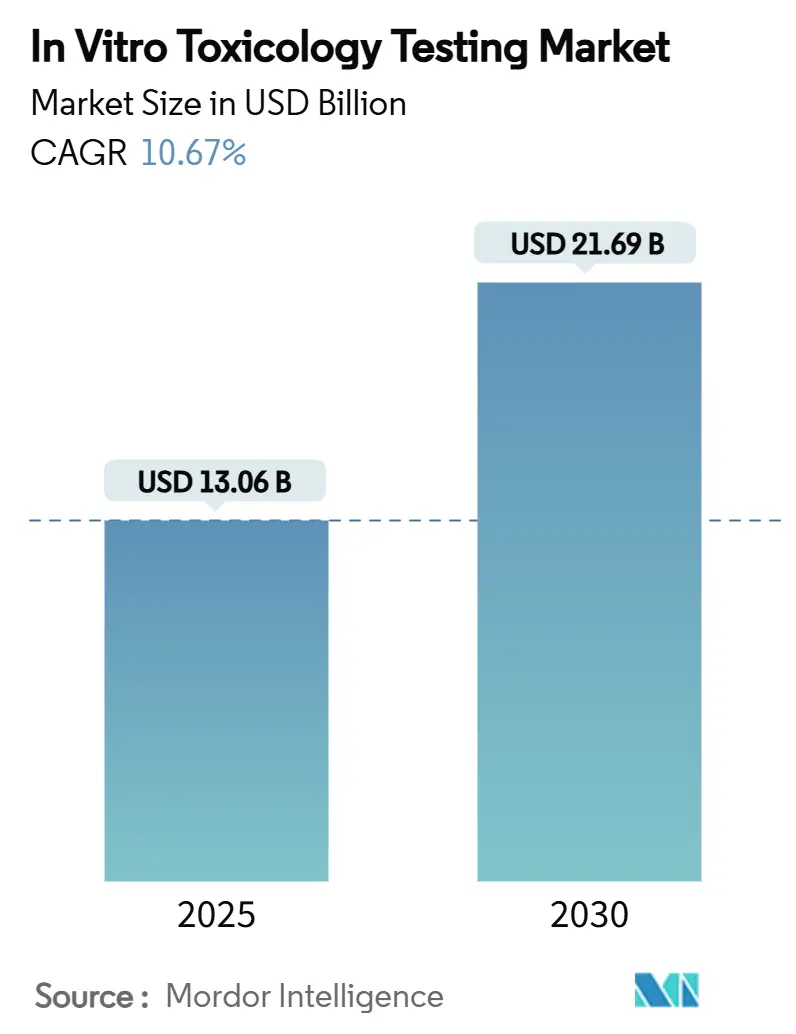

| Market Size (2025) | USD 13.06 Billion |

| Market Size (2030) | USD 21.69 Billion |

| Growth Rate (2025 - 2030) | 10.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

In Vitro Toxicology Testing Market Analysis by Mordor Intelligence

The In Vitro Toxicology Testing Market size is estimated at USD 13.06 billion in 2025, and is expected to reach USD 21.69 billion by 2030, at a CAGR of 10.67% during the forecast period (2025-2030).

This pace underscores the sector’s central role in safeguarding human health across pharmaceuticals, cosmetics, and chemicals while meeting global regulations that discourage animal testing. Tighter safety mandates, the FDA’s New Alternative Methods program, and Europe’s roadmap to phase out animal models are spurring demand. Parallel advances in 3D cell culture, organ-on-chip systems, and AI-enabled analytics are raising predictive accuracy, trimming R&D costs, and opening new revenue streams for contract research organizations. Investor interest remains strong as the technology shift promises earlier toxicity detection, fewer late-stage failures, and faster time-to-market for innovative therapeutics.

Key Report Takeaways

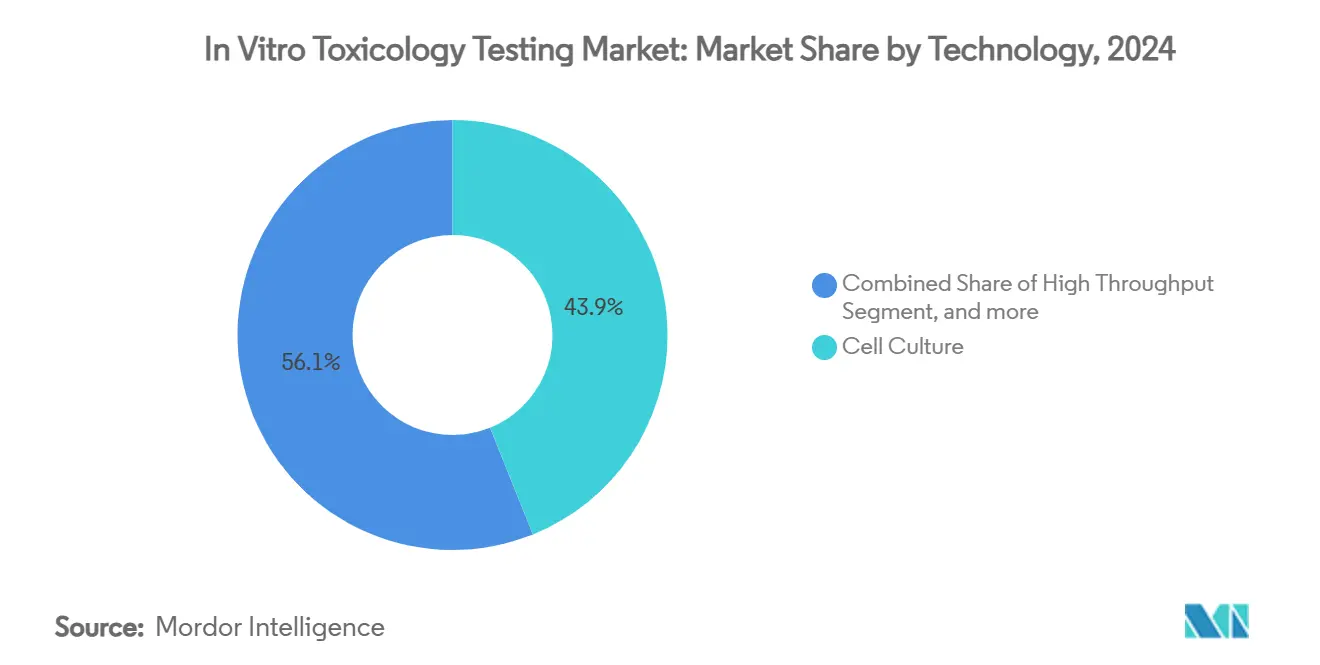

- By technology, cell culture led with 43.91% of the in vitro toxicology testing market share in 2024, while OMICS methods are forecast to grow at 13.88% CAGR through 2030.

- By method, cellular assays accounted for 36.28% share of the in vitro toxicology testing market size in 2024; in-silico techniques are projected to expand at 14.24% CAGR to 2030.

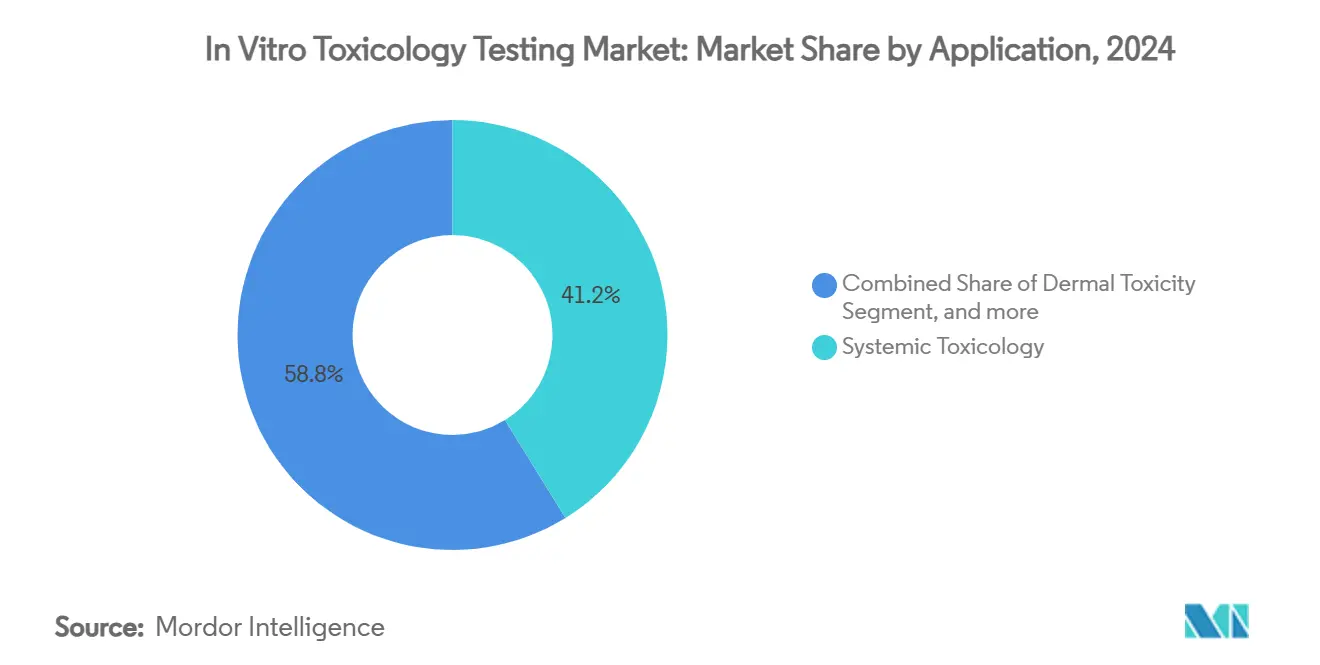

- By application, systemic toxicology commanded 41.24% of the in vitro toxicology testing market size in 2024, whereas endocrine disruption testing is advancing at a 12.56% CAGR through 2030.

- By end user, the pharmaceutical industry held 48.43% of the in vitro toxicology testing market share in 2024, while diagnostics is the fastest-growing segment at 13.21% CAGR.

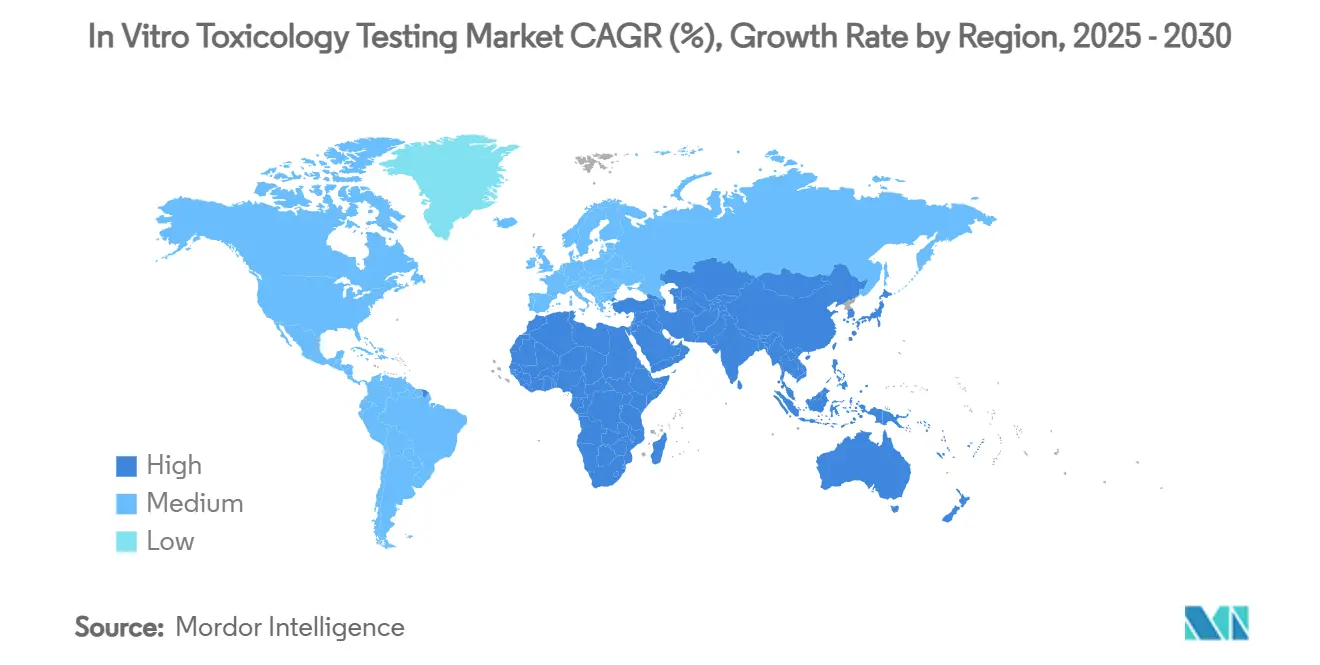

- By geography, North America contributed 47.75% revenue in 2024; Asia-Pacific is set to register a 12.58% CAGR from 2025 to 2030.

Global In Vitro Toxicology Testing Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reduced animal use in pre-clinical research | +3.2% | Europe, North America | Medium term (2-4 years) |

| Advanced in-vitro assay development | +2.8% | North America, Europe | Long term (≥4 years) |

| Greater awareness of drug safety | +2.1% | Developed markets worldwide | Medium term (2-4 years) |

| Personalized medicine uptake | +1.9% | Global | Long term (≥4 years) |

| Expansion of high-throughput screening | +1.6% | Global | Medium term (2-4 years) |

| Regulatory push for animal-free testing | +1.4% | Europe, North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Opposition to the Usage of Animals in Pre-clinical Research

Ethical pressure and regulatory bans continue to displace animal studies. The Society of Toxicology notes that Europe’s strict cosmetics directive and the FDA Modernization Act 2.0 have legitimized non-animal approaches.[1]Society of Toxicology, “Alternatives to Animal Testing,” toxicology.org As companies align with these rules, demand for validated in vitro assays accelerates. Multinational firms now embed alternative methods into global submission dossiers, creating unified workflows across regions. The trend also catalyzes public-private partnerships that share reference data to speed assay validation. Rising social awareness further encourages investors to favor firms offering cruelty-free testing services.

Significant Advancements In-vitro Toxicology Assays

Breakthroughs in 3D organoids, microfluidics, and single-cell analytics deliver richer human-relevant data. Microfluidic lung-on-chip models now evaluate particulate toxicity with higher throughput than classical air–liquid interface tests.[2]Environmental Toxicology, “Microfluidic Approaches for Particulate Matter Toxicity,” environmentaltox.com Combined with real-time imaging and AI, scientists can capture subtle phenotypic changes hours after exposure. These tools support regulatory decision-making for complex endpoints such as developmental neurotoxicity, where rodent models often fall short. As protocols mature, CROs integrate assay bundles to provide full mechanistic insights, boosting their revenue per project.

Increasing Awareness Regarding Drug Product Safety

Late-stage toxicity failures cost the pharmaceutical sector billions. Roughly 30% of phase II/III attrition stems from unforeseen safety issues.[3]ScienceDirect, “Drug Attrition and Safety Assessment,” sciencedirect.com In response, companies invest in predictive multi-omics screens that flag liabilities earlier. Regulators encourage real-world-data integration, and precision-medicine initiatives rely on genomic-to-clinical correlation. Together, these factors push sponsors to adopt higher-content in vitro tests that reduce uncertainty, satisfy health-technology-assessment criteria, and protect brand reputation.

Rising Demand for Personalized Medicine

Tailoring therapy requires understanding individual toxicity risk. Single-cell omics and patient-derived organoids reveal genotype-specific responses, enabling bespoke dosing strategies. Hospitals adopt point-of-care cytotoxicity panels to monitor adverse events in real time, creating spill-over demand for commercial kits. Industry players respond by co-developing companion diagnostic-to-therapy bundles that combine efficacy and safety readouts.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited autoimmunity & immunostimulation modeling | −1.8% | Advanced research hubs | Short term (≤2 years) |

| Complex regulatory pathways for novel assays | −1.4% | North America, Europe | Medium term (2-4 years) |

| Incomplete predictive accuracy for systemic toxicities | −1.2% | Global | Long term (≥4 years) |

| Data management and integration hurdles | −1.0% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Incapability of In-vitro Models to Determine Autoimmunity and Immunostimulation

Even sophisticated 3D tissues lack full immune complexity. AZoLifeSciences underscores that organoids without vascular and lymphoid components struggle to predict cytokine storms. Biologics developers therefore still complement assays with in vivo studies. Emerging multi-organ-on-chip systems show promise, but reproducibility and regulatory validation remain ongoing challenges, delaying widespread adoption.

Stringent Regulatory Framework for the In-vitro Tests

The FDA’s 2024 rule classifying laboratory-developed tests as medical devices imposes design-control, quality, and post-market surveillance duties. Smaller innovators face resource constraints when compiling performance evidence. Lack of harmonized global standards further complicates multi-region approvals, slowing ROI for new platforms. Regulators, however, signal willingness to fast-track well-designed, context-of-use-specific assays.

Segment Analysis

By Technology: Molecular-Level Insight Drives Adoption

Cell culture retained the largest share at 43.91% of in vitro toxicology testing market in 2024, benefiting from mature protocols and broad user familiarity. The segment’s strength lies in its versatility across exploratory screens, potency assays, and regulatory submissions. The in vitro toxicology testing market size for Cell Culture applications is projected to remain above USD 8 billion by 2030 as enhancements such as CRISPR-edited lines and AI-assisted imaging unlock new mechanistic insights. Emerging 3D constructs further emulate human organs, reducing false negatives often seen with two-dimensional monolayers.

OMICS approaches, spanning transcriptomics, proteomics, and metabolomics, recorded the fastest CAGR at 13.88% to 2030. Rapid declines in sequencing costs and advances in single-cell analytics broaden adoption among pharma, biotech, and academia. The integration of multi-omics layers offers systems-level toxicological signatures that complement phenotypic screens, positioning OMICS as a cornerstone of next-generation safety pipelines. As datasets grow, machine-learning models trained on OMICS fingerprints refine structure–activity relationships and predict idiosyncratic toxicities earlier in drug discovery.

Note: Segment shares of all individual segments available upon report purchase

By Method: Digital Models Rise, Classical Assays Persist

Cellular assays commanded 36.28% of the in vitro toxicology testing market share in 2024. Fluorescent reporter systems and automated microscopy supply quantitative data on apoptosis, oxidative stress, and DNA damage, underpinning regulatory-grade submissions. Concurrently, in-silico techniques are projected to generate the highest revenue increment, propelled by cloud-based machine-learning platforms that screen virtual libraries at minimal incremental cost.

The in vitro toxicology testing market size for in-silico tools is growing with CAGR 13.88% between 2025 and 2030, driven by pharmaceutical portfolio rationalization and regulatory acceptance of data-rich computational evidence. Biochemical assays and ex-vivo preparations continue to address pathway-specific questions and serve as bridging tools for complex endpoints where predictive models lack validation.

By Application: Hormone Safety in the Spotlight

Systemic toxicology remained the largest use case, contributing 41.24% of total revenue in 2024. Integrated liver, kidney, and cardiac models allow simultaneous multi-organ readouts, streamlining regulatory packages for new chemical entities.

In contrast, endocrine disruption testing posted the fastest CAGR at 12.56% amid mounting concern over hormone-active pollutants. European authorities fund projects such as ENDpoiNTs to refine predictive assays that incorporate species and sex differences. Heightened scrutiny of endocrine-active ingredients in plastics, pesticides, and cosmetics drives industry to adopt sensitive receptor-binding and gene-expression panels that detect subtle hormonal perturbations well before overt phenotypic changes arise.

Note: Segment shares of all individual segments available upon report purchase

By End User: Diagnostics Accelerates, Pharma Dominates

Pharmaceutical companies retained 48.43% share as they anchor toxicology budgets from discovery through clinical phases. Heightened pipeline complexity and the shift toward biologics stretch traditional models, fueling demand for advanced in vitro platforms.

Meanwhile, Diagnostics shows the swiftest momentum at 13.21% CAGR as hospitals implement lab-developed cytotoxicity tests to safeguard personalized regimens. CROs leverage this opportunity by bundling toxicology with genomics and bioinformatics to offer turnkey services, while academic institutions remain pivotal in method invention and early validation stages.

Geography Analysis

North America led the in vitro toxicology testing market with 47.75% revenue in 2024, supported by FDA funding for alternative methods and high R&D spend per capita. The in vitro toxicology testing market size in the United States is driven by rapid adoption of AI-guided high-throughput platforms and a favorable reimbursement environment for advanced diagnostics. Regulatory clarity around laboratory-developed tests, although stringent, signals official endorsement of validated in vitro technologies.

Asia-Pacific is the fastest-growing region, forecast at 12.58% CAGR from 2025 to 2030. Multinational firms establish regional innovation hubs to tap the vast patient base and cost-effective talent pool. These factors collectively elevate local demand for predictive safety solutions that meet global regulatory criteria.

Europe holds a firm second place, bolstered by stringent animal-test bans and progressive chemical-safety directives. The European Commission’s November 2024 roadmap to eliminate animal studies propels early adoption of organ-on-chip and multi-omics assays. Regional consortia standardize validation pathways, offering companies smoother submission routes. Meanwhile, emerging markets in South America and the Middle East & Africa witness steady uptake as healthcare infrastructure and pharmacovigilance frameworks mature, presenting long-term growth prospects for test kit suppliers and service providers.

Competitive Landscape

The market shows moderate concentration, with a mix of diversified life-science conglomerates, midsize CROs, and agile start-ups. Incumbents expand service breadth through acquisition: Eurofins Scientific’s April 2025 purchase of an endocrine-testing lab widens its niche capabilities. Thermo Fisher’s January 2025 launch of an automated screening system strengthens its hardware–service bundle, enticing clients seeking unified platforms. Such moves signal a shift toward vertically integrated offerings that span data generation, analytics, and regulatory reporting.

Strategic partnerships between AI specialists and assay developers redefine competitive dynamics. The merger of Recursion and Exscientia aims to create a large-scale AI drug-discovery engine that incorporates toxicity prediction from day one. Smaller firms counter by focusing on white-space areas, including developmental neurotoxicity and immunotoxicity, offering high-fidelity models that incumbents lack. Pricing pressure intensifies as automation reduces per-sample costs, but providers differentiate on data quality, turnaround time, and consultative expertise.

Intellectual-property portfolios centered on microfluidic design, imaging algorithms, and multi-omics analytics become critical assets. Companies leverage these patents to negotiate exclusive agreements with big pharma, securing recurring revenue through multi-year master-service contracts. Overall, competition now hinges less on capacity and more on the scientific validity and regulatory acceptance of advanced human-relevant models.

In Vitro Toxicology Testing Industry Leaders

-

Charles River Laboratories International Inc.

-

Thermo Fisher Scientific Inc.

-

Eurofins Scientific SE

-

Merck KGaA

-

Agilent Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Cocrystal Pharma reported significant advancements in its antiviral drug development, with its oral pan-viral protease inhibitor CDI-988 demonstrating superior in vitro activity against norovirus strains, highlighting the critical role of in vitro testing in therapeutic development.

- April 2025: Eurofins Scientific expanded its in vitro toxicology testing capabilities through the acquisition of a specialized laboratory focusing on endocrine disruption testing, strengthening its position in this rapidly growing application segment.

- February 2025: Charles River Laboratories unveiled an advanced 3D cell culture platform for hepatotoxicity assessment, incorporating AI-driven image analysis to enhance the detection of subtle cellular changes indicative of liver toxicity.

- January 2025: Thermo Fisher Scientific launched a new high-throughput screening system specifically designed for in vitro toxicology applications, enabling the simultaneous evaluation of multiple toxicity endpoints across thousands of compounds.

Global In Vitro Toxicology Testing Market Report Scope

In-vitro toxicity testing is referred to the method of scientifically analyzing the effects of lethal or toxic chemical materials either on mammalian cells or on cultured bacteria. In-vitro testing methods are performed mainly for the purpose of identifying potentially harmful chemicals and/or for confirming the deficiency of certain toxic properties in the initial stages of the development of possibly useful novel substances, including therapeutic drugs, agricultural chemicals, and even food additives.

| Cell Culture |

| High Throughput |

| Molecular Imaging |

| OMICS |

| 3D Cell Culture & Organoids |

| Cellular Assay |

| Biochemical Assay |

| In-Silico |

| Ex-Vivo |

| Systemic Toxicology |

| Dermal Toxicity |

| Endocrine Disruption |

| Ocular Toxicity |

| Other Applications |

| Pharmaceutical Industry |

| Biotechnology & CROs |

| Diagnostics |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Cell Culture | |

| High Throughput | ||

| Molecular Imaging | ||

| OMICS | ||

| 3D Cell Culture & Organoids | ||

| By Method | Cellular Assay | |

| Biochemical Assay | ||

| In-Silico | ||

| Ex-Vivo | ||

| By Application | Systemic Toxicology | |

| Dermal Toxicity | ||

| Endocrine Disruption | ||

| Ocular Toxicity | ||

| Other Applications | ||

| By End User | Pharmaceutical Industry | |

| Biotechnology & CROs | ||

| Diagnostics | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the in vitro toxicology testing market?

The in vitro toxicology testing market size stands at USD 13.06 billion in 2025 and is forecast to reach USD 21.69 billion by 2030.

Which technology segment is growing fastest?

OMICS-based platforms lead growth with a projected 13.88% CAGR through 2030 as they deliver comprehensive molecular insights and earlier toxicity detection.

Why is North America dominant in this market?

Strict FDA regulations supporting alternative methods, high R&D spending, and rapid adoption of AI-driven high-throughput systems give North America 47.75% revenue share.

What restrains complete replacement of animal testing?

Current in vitro models struggle to replicate autoimmunity and systemic immunostimulation, necessitating some complementary in vivo studies for complex biologics.

How does AI enhance toxicology testing?

AI algorithms analyze multi-omics and imaging data, predict toxic liabilities sooner, and optimize compound selection, cutting development timelines and costs.

Which end-user segment is expanding most rapidly?

Diagnostics is advancing at a 13.21% CAGR as hospitals integrate toxicity assays into personalized treatment monitoring.

Page last updated on: