Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

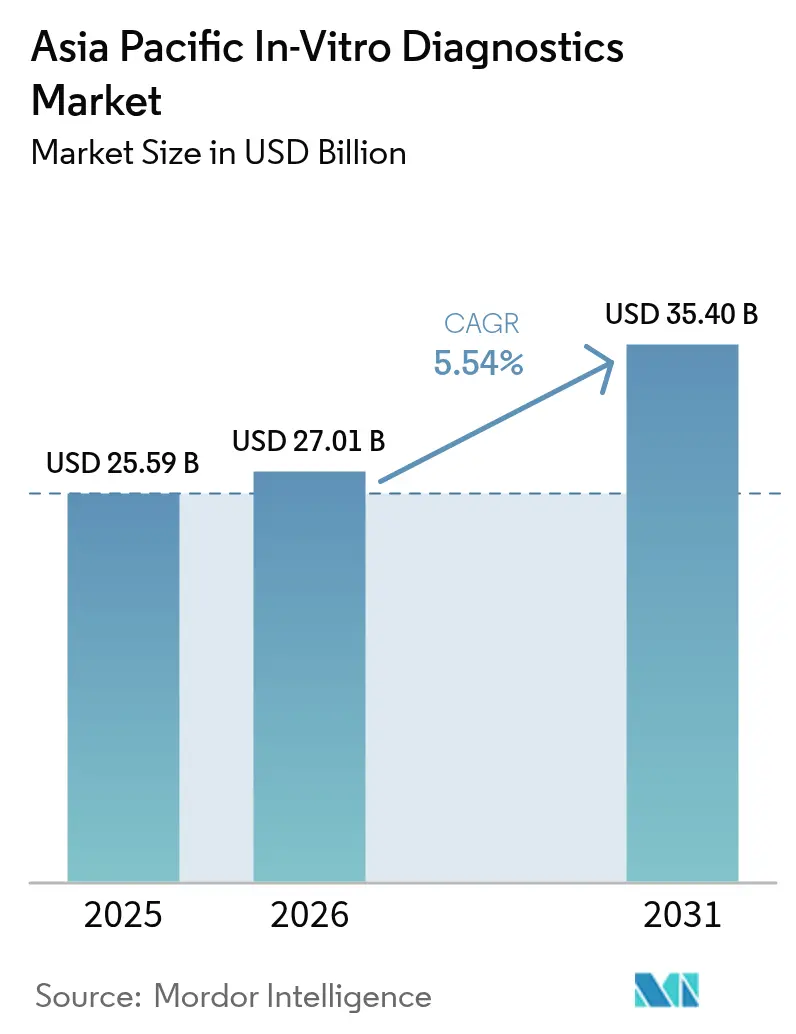

| Base Year Market Size (2025) | USD 25.59 Billion |

| Market Size (2026) | USD 27.01 Billion |

| Market Size (2031) | USD 35.4 Billion |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

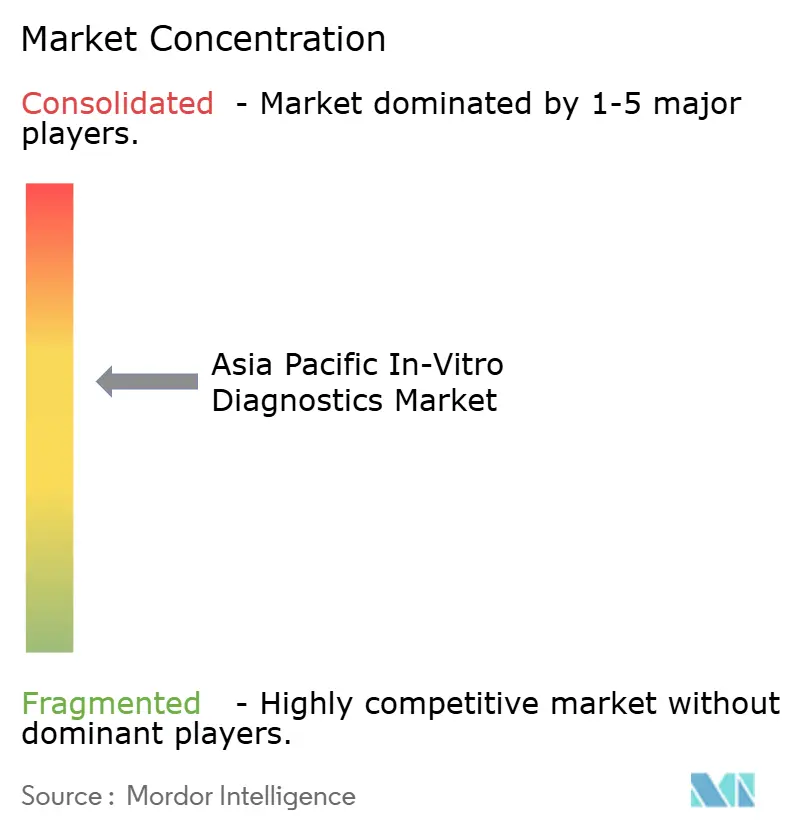

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific In-Vitro Diagnostics Market Analysis by Mordor Intelligence

Asia-Pacific in-vitro diagnostics market size in 2026 is estimated at USD 27.01 billion, growing from 2025 value of USD 25.59 billion with 2031 projections showing USD 35.4 billion, growing at 5.54% CAGR over 2026-2031. Robust healthcare spending, wider diagnostic reach, and a mounting chronic-disease burden underpin this steady trajectory. Rising government screening mandates, ageing populations, and industry-friendly localization incentives are opening profitable niches, while precision-medicine technologies—especially molecular assays—are changing competitive rules. Multinational and regional manufacturers are accelerating factory builds and digital upgrades to secure regulatory clearance faster, capture growth in Tier-2/3 cities, and serve the increasing preference for self-testing. Competitive intensity remains moderate, yet price pressure and quality concerns around ultra-low-cost reagents continue to shape procurement choices.

Key Report Takeaways

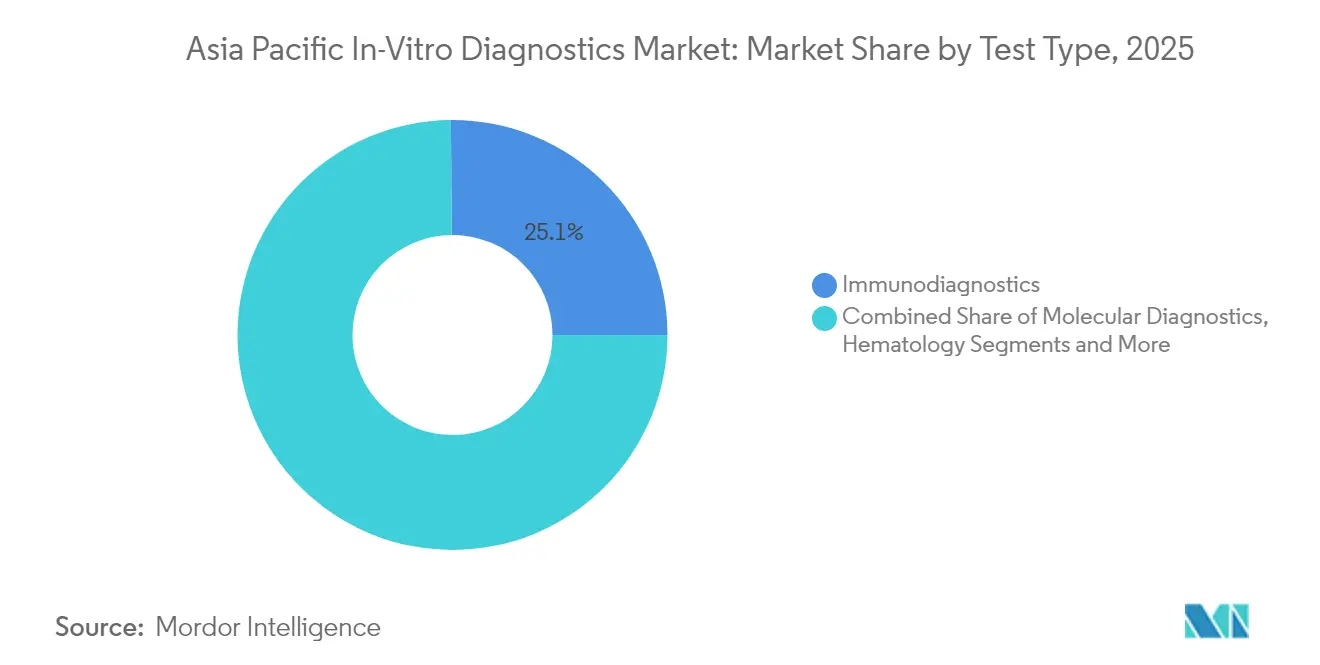

- By test type, immunodiagnostics led with 25.12% of Asia-Pacific in-vitro diagnostics market share in 2025; molecular diagnostics is projected to post the fastest 9.71% CAGR through 2031.

- By product, reagents and kits captured 59.65% of the Asia-Pacific in-vitro diagnostics market size in 2025, while software and services are advancing at an 11.07% CAGR between 2026 and 2031.

- By usability, reusable devices held 69.92% revenue share in 2025; disposable devices are forecast to expand at a 9.84% CAGR by 2031.

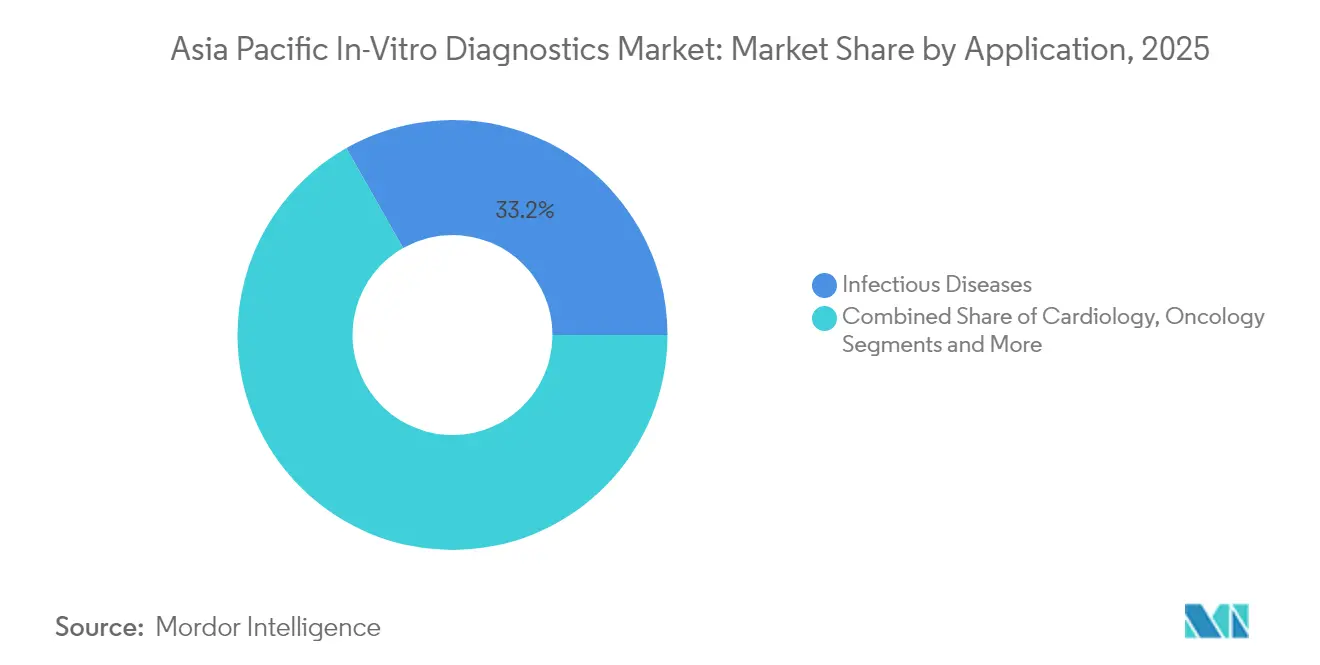

- By application, infectious-disease testing accounted for a 33.22% share of the Asia-Pacific in-vitro diagnostics market size in 2025, whereas oncology is growing at an 10.98% CAGR through 2031.

- By end user, diagnostic laboratories commanded 54.67% share in 2025 and home-care self-testing is expected to deliver a 12.06% CAGR over 2026-2031.

- By country, China dominated with 45.05% of regional revenue in 2025; India is on track for the strongest 11.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demographic ageing | +1.5% | Japan, China, South Korea, Southeast Asia | Long term (≥ 4 years) |

| Government cancer & infectious-disease screening | +1.2% | China, India, Australia, Thailand | Medium term (2-4 years) |

| Automated lab hubs in Tier-2/3 cities | +0.9% | India, China, Indonesia | Medium term (2-4 years) |

| Localization incentives for IVD manufacturing | +0.7% | India, China, Vietnam | Short term (≤ 2 years) |

| Rising diabetes & metabolic-syndrome burden | +0.5% | China, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demographic ageing escalating demand for high-value diagnostics

Japan’s 65+ cohort reached 29.1% in 2024 and China’s elderly population is expanding 3.2% yearly, translating into higher volumes for oncology and cardiovascular assays. Health ministries are backing proactive detection to trim downstream treatment spending, with every USD 1 spent on early testing saving USD 3.4 in future care. Biomarkers such as pTau181 are entering routine workflows following the 2025 launch of Roche’s Elecsys pTau181 assay. Specialized geriatric diagnostics—Alzheimer’s, frailty panels, and cardio-renal markers—are beginning to form micro-segments that command premium pricing.

Government-mandated cancer & infectious-disease screening programs

China’s Healthy China 2030 initiative directed USD 8.7 billion to cancer-screening infrastructure in 2024, while India lifted diagnostic allocations by 43% for 2024-2025. Standardized nationwide protocols favor automated, high-throughput platforms and incentivize firms aligned with priority diseases. bioMérieux now channels 75% of its global R&D budget to antimicrobial-resistance assays to meet these public-health agendas[1]bioMérieux, “Universal Registration Document 2024,” biomerieux.com. Economic planners link screening coverage to labor-productivity gains, further embedding diagnostics in macro-development strategy.

Expansion of automated laboratory hubs into Tier-2/3 cities improving test accessibility

More than 450 automated labs opened across India’s smaller cities in 2024, slashing result turn-around by 62% and trimming per-test operating cost by 28%. China’s rural-health program ties subsidies to hub-and-spoke laboratory networks. These facilities centralize high-complexity testing, permit night-shift processing, and integrate cloud-based reporting dashboards for remote clinicians. Suppliers able to configure scalable, modular systems that fit mid-volume settings are winning sizeable framework bids.

Localization incentives drawing IVD manufacturing CAPEX

India’s Production Linked Incentive scheme earmarked USD 400 million for medical devices, triggering 17 IVD-plant announcements in 2024. Local manufacturing entitles suppliers to tender preferences and condenses import-license timelines. Sysmex began reagent and instrument production at its first India plant in April 2025 to reinforce hematology leadership. Comparable benefits exist in Vietnam’s high-tech parks, where land-use holidays and R&D tax credits attract mid-tier manufacturers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy multi-agency regulatory approvals | −0.8% | Japan, China, South Korea | Medium term (2-4 years) |

| Skills shortage in molecular & bio-informatics | −0.6% | India, Indonesia, Vietnam, Philippines | Short term (≤ 2 years) |

| Quality variability of ultra-low-cost reagents | −0.4% | India, China, Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthy multi-agency regulatory approvals delaying product launches

Average clearance spans 18-24 months in Japan and 14-20 months in China, against 9-12 months for Western dossiers. Compliance outlays run 37% higher regionally, pushing smaller innovators to partner or concede share to multinationals that can field dedicated regulatory teams[2]Asia Pacific Medical Technology Association, “Regulatory Landscape of LDT in APAC,” apacmed.org. ASEAN’s harmonization roadmap shows progress, yet uneven national transposition slows benefits. Rapid-cycle technologies risk obsolescence before approval, compelling firms to sequence launches or adopt modular filings that can accommodate iterative upgrades.

Skills shortage in molecular and bio-informatics outside metropolitan laboratories

Regional labs lack roughly 45,000 qualified molecular technologists, constraining adoption of high-complexity assays. Talent premiums inflate wage bills 15-25%, nudging labs toward automation and AI-supported interpretation. Remote e-learning modules and cloud-based annotation services offer interim relief, while universities expand genomics curriculums. Roche’s cobas platforms illustrate simplified workflows that lower staffing thresholds and speed onboarding.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Redefining Clinical Practice

Immunodiagnostics held 25.12% Asia-Pacific in-vitro diagnostics market share in 2025, reflecting entrenched use across infection control and chronic-disease monitoring. Molecular diagnostics is forecast for a 9.71% CAGR, dwarfing the broader 5.54% trend, and its Asia-Pacific in-vitro diagnostics market size contribution will climb steadily through 2031. Investment funnels into precision oncology and real-time pathogen surveillance, with PCR remaining the workhorse while next-generation sequencing moves downstream.

Point-of-care molecular platforms now deliver results in under an hour, vital for sepsis and respiratory triage. AI-augmented algorithms raise diagnostic accuracy by 28% when paired with molecular outputs. The COVID-19 infrastructure boom left a durable installed base, lowering entry barriers for broader assays. Suppliers that integrate multiplex capability, sample-to-answer simplicity, and cloud analytics are best placed to win micro-lab and emergency-department budgets.

By Product: Software Integration Driving Value Creation

Reagents and kits provided 59.65% of revenue in 2025 thanks to repeat-purchase economics inherent in testing workflows. Instruments remain critical, yet software and services will compound at 11.07% annually and account for a rising slice of Asia-Pacific in-vitro diagnostics market size. Laboratories demand cloud laboratory-information systems, middleware analytics, and AI-driven decision support to convert raw data into actionable care insights.

Roche’s 2025 cobas roadmap embeds machine-learning modules that flag utilization gaps and recommend test panels, helping facilities balance cost and clinical yield. Subscription models tied to uptime guarantees and continuous algorithm upgrades broaden recurring revenue streams. Interoperability with electronic medical records and payer portals has become a key tender criterion, advantaging vendors that champion open-API strategies.

By Usability: Disposable Devices Expanding Access Points

Reusable analyzers dominated with 69.92% share in 2025, but disposable devices will outrun aggregate growth at a 9.84% CAGR. Microfluidic cartridges now host multiplex molecular and immunoassay chemistries, bringing lab-grade accuracy to physician offices, retail clinics, and homes. Reduced maintenance, no calibration flows, and biosafety convenience underpin clinical uptake.

Infectious-disease screening benefits strongly; single-use molecular panels for influenza and RSV entered mainstream pediatric practice after pandemic-era evaluation. BioMérieux’s 2024 acquisition of SpinChip provides edge-printed microfluidic disposables capable of running enzyme assays in <15 minutes. Sustainable materials and smart-chip recycling solutions are emerging to counter environmental cost criticisms.

By Application: Oncology Driving Precision Medicine Adoption

Infectious-disease testing held 33.22% of 2025 revenue, yet oncology diagnostics will post an 10.98% CAGR to 2031, almost double the Asia-Pacific in-vitro diagnostics market growth pace. Liquid biopsy advances allow early relapse detection and therapy monitoring without invasive tissue sampling. Comprehensive genomic panels and companion diagnostics underpin personalized treatment, with breast, lung, and colorectal cancers the early beneficiaries.

AI-assisted pattern recognition across imaging and molecular datasets yields 31% higher early-stage discovery rates. Payers gradually reimburse high-value genomics after cost-effectiveness evidence accumulates. Vendors offering end-to-end oncology solutions—from screening through minimal residual disease monitoring—will consolidate loyalty among leading cancer centers.

By End User: Self-Testing Revolution Transforming Care Models

Diagnostic laboratories processed 54.67% of volumes in 2025, leveraging bulk purchasing and sophisticated robotics. Home-care and self-testing, however, will accelerate at 12.06% CAGR, unlocking new Asia-Pacific in-vitro diagnostics market potential. Smartphone-linked lateral-flow cassettes and Bluetooth glucose readers demonstrate how consumer electronics ecosystems absorb health functions.

The FDA’s 2025 Home as a Health Care Hub guidance catalyzes device designs prioritizing intuitive app interfaces and remote physician oversight. Roche’s Accu-Chek SmartGuide pairs continuous glucose reading with AI-generated coaching, highlighting how hardware, software, and behavioral nudges interlock. National insurers explore reimbursements for validated self-tests that lower emergency visits and enable population-level surveillance.

Geography Analysis

China captured 45.05% of the Asia-Pacific in-vitro diagnostics market in 2025, anchored by vast population, hospital digitization, and strategic policy such as tender bundling for high-throughput systems. Despite near-term price caps that squeezed margins for multinationals, ongoing NMPA reforms promise streamlined pathways for localized production and innovative assays. Rural diagnostics networks supported by 5G cloud links extend testing far beyond megacities.

India is the growth pacesetter at a 11.68% CAGR. Government PLI incentives, rising insurance coverage, and public-private lab chains fuel double-digit revenue expansion. Immunology demand is set to double from INR 160 billion to INR 320 billion within the decade, signaling lucrative viral-hepatitis and auto-immune test segments. Urban dominance persists, but hub-and-spoke rollouts plus mobile vans gradually shrink rural diagnostic gaps. Japan and South Korea remain high-value markets thanks to affluent ageing demographics, automated mega-labs, and a culture of preventive screening. Australia’s strong evidence-based procurement sustains premium pricing for precision assays, while Indonesia, Thailand, and Vietnam climb from low bases with infrastructure upgrades and donor-backed disease programs. Hong Kong’s InnoLife Healthtech Hub positions the city as an R&D and finance gateway for regional genomics start-ups.

Competitive Landscape

Roughly 200 manufacturers vie for a share; the top 10 control a significant share, indicating moderate concentration. Abbott, Roche, and Siemens Healthineers leverage wide portfolios and service networks to lock multi-year reagent contracts. Mindray and Seegene exploit cost agility and local insight to penetrate mid-tier hospitals. Localization of manufacturing—e.g., Sysmex’s 2025 India plant—reduces tariffs and wins public tenders stipulating domestic value addition.

Molecular and point-of-care segments see brisk product launches and smaller players introducing niche platforms, spurring faster turnover of technology cycles. Integration of software analytics into instruments adds new barriers to entry; vendors capable of combining assay chemistry with AI dashboards achieve sticky customer relationships. Partnerships between diagnostics firms and tele-health platforms signal future ecosystem plays where test results trigger automated care pathways.

Regulatory navigation remains a differentiator. Advantaged firms pre-engage with agencies, leverage real-world evidence for conditional filings, and adopt modular submissions to shorten time-to-market. Pricing reform pressures compel innovation in value-based contracting, bundling reagents, service, and data analytics for outcome-linked payments, particularly in oncology and diabetes management.

Asia Pacific In-Vitro Diagnostics Industry Leaders

Siemens Healthineers AG

bioMérieux SA

Thermo Fisher Scientific

F Hoffmann-La Roche Ltd

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Sysmex began full-scale operations at its new Indian plant and commenced manufacturing the XQ-Series automated hematology analyzer.

- February 2025: Roche secured Japanese and Australian approval for its SBX sequencing technology, widening access to high-throughput genomic oncology testing.

Asia Pacific In-Vitro Diagnostics Market Report Scope

As per the scope of the report, in vitro diagnostics involve medical devices and consumables that are utilized to perform in-vitro tests on various biological samples. They diagnose various medical conditions, such as diabetes and cancer. The Asia Pacific In-vitro Diagnostics Market is segmented by test type (clinical chemistry, molecular diagnostics, immunodiagnostics, hematology, and other test types), product (instruments, reagents, and other products), usability (disposable IVD devices and reusable IVD devices), application (infectious disease, diabetes, cancer/oncology, cardiology, autoimmune disease, nephrology, and other applications), end user (diagnostic laboratories, hospitals and clinics, and other end users), and Geography (China, Japan, India, Australia, South Korea, and rest of Asia-Pacific). The report offers values (in USD) for the above segments.

By Test Type

| Clinical Chemistry |

| Molecular Diagnostics |

| Immunodiagnostics |

| Hematology |

| Coagulation |

| Microbiology |

| Urinalysis |

By Product

| Instruments |

| Reagents & Kits |

| Software & Services |

By Usability

| Disposable IVD Devices |

| Reusable IVD Devices |

By Application

| Infectious Diseases |

| Diabetes |

| Oncology |

| Cardiology |

| Autoimmune Diseases |

| Nephrology |

| Respiratory Diseases |

| Other Applications |

By End User

| Diagnostic Laboratories |

| Hospitals & Clinics |

| Academic & Research Institutes |

| Home Care & Self-testing |

By Country

| China |

| Japan |

| India |

| Australia |

| South Korea |

| Rest of Asia-Pacific |

| By Test Type | Clinical Chemistry |

| Molecular Diagnostics | |

| Immunodiagnostics | |

| Hematology | |

| Coagulation | |

| Microbiology | |

| Urinalysis | |

| By Product | Instruments |

| Reagents & Kits | |

| Software & Services | |

| By Usability | Disposable IVD Devices |

| Reusable IVD Devices | |

| By Application | Infectious Diseases |

| Diabetes | |

| Oncology | |

| Cardiology | |

| Autoimmune Diseases | |

| Nephrology | |

| Respiratory Diseases | |

| Other Applications | |

| By End User | Diagnostic Laboratories |

| Hospitals & Clinics | |

| Academic & Research Institutes | |

| Home Care & Self-testing | |

| By Country | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific in-vitro diagnostics market in 2026?

The market is valued at USD 27.01 billion in 2026 and is forecast to reach USD 35.4 billion by 2031.

Which test type is expanding the fastest across Asia-Pacific?

Molecular diagnostics is growing at a 9.71% CAGR due to wider precision-oncology and infectious-disease use cases.

Why is India considered the most dynamic market within Asia-Pacific?

India's 11.68% CAGR stems from large infrastructure investments, supportive manufacturing incentives, and rising disease awareness.

How are regulations affecting product launch timelines?

Multi-agency approvals in Japan and China extend launch timelines to 14-24 months, increasing compliance costs and favoring firms with dedicated regulatory teams.

Which companies recently expanded manufacturing in the region?

Sysmex opened a new Indian plant in April 2025, and Roche gained approvals for its SBX sequencing system in Japan and Australia in February 2025.

Page last updated on: