Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.95 Billion |

| Market Size (2026) | USD 4.23 Billion |

| Market Size (2031) | USD 5.95 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France In-Vitro Diagnostics Market Analysis by Mordor Intelligence

France in vitro diagnostics market size in 2026 is estimated at USD 4.23 billion, growing from 2025 value of USD 3.95 billion with 2031 projections showing USD 5.95 billion, growing at 7.08% CAGR over 2026-2031. Diagnostic testing underpins roughly 70% of clinical decisions and continues to gain relevance as chronic disease cases rise and preventive‐care models expand. Regulatory tightening under the European Union’s In Vitro Diagnostic Regulation (IVDR) is lengthening approval cycles yet driving demonstrable quality gains. Laboratory consolidation, especially among investor-backed chains, is steering volumes toward high-throughput hubs while home-based testing platforms widen patient access. Technology convergence—automation, artificial intelligence, and digital connectivity—remains the pivotal competitive lever as suppliers look to improve turnaround time, accuracy, and data integration[1]Organisation for Economic Co-operation and Development, “Health at a Glance: Europe 2024,” oecd.org.

Key Report Takeaways

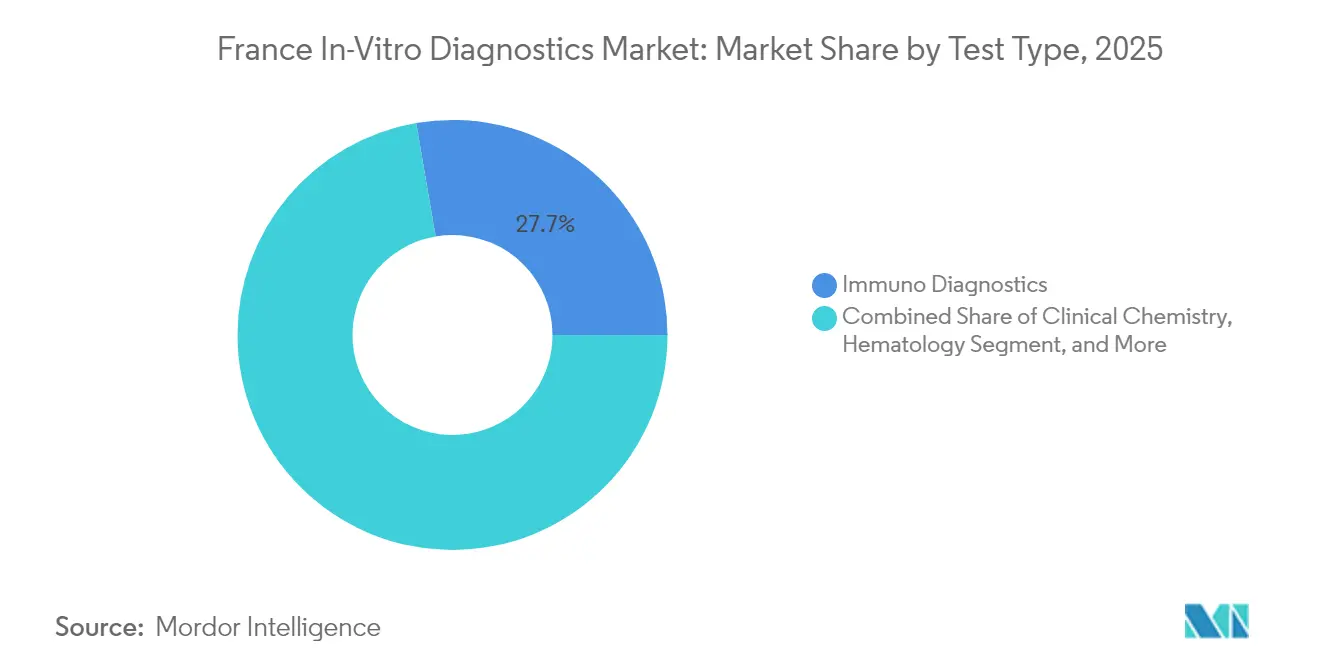

- By test type, Immuno Diagnostics led with 27.70% revenue share in 2025, whereas Molecular Diagnostics is forecast to advance at a 9.18% CAGR through 2031.

- By product & service, Reagents & Kits accounted for 64.80% of the France in vitro diagnostics market share in 2025; Software & Services are poised to grow at a 11.74% CAGR to 2031.

- By specimen, blood testing commanded 44.60% share of the France in vitro diagnostics market size in 2025, while salivary testing will expand at a 10.08% CAGR during 2026-2031.

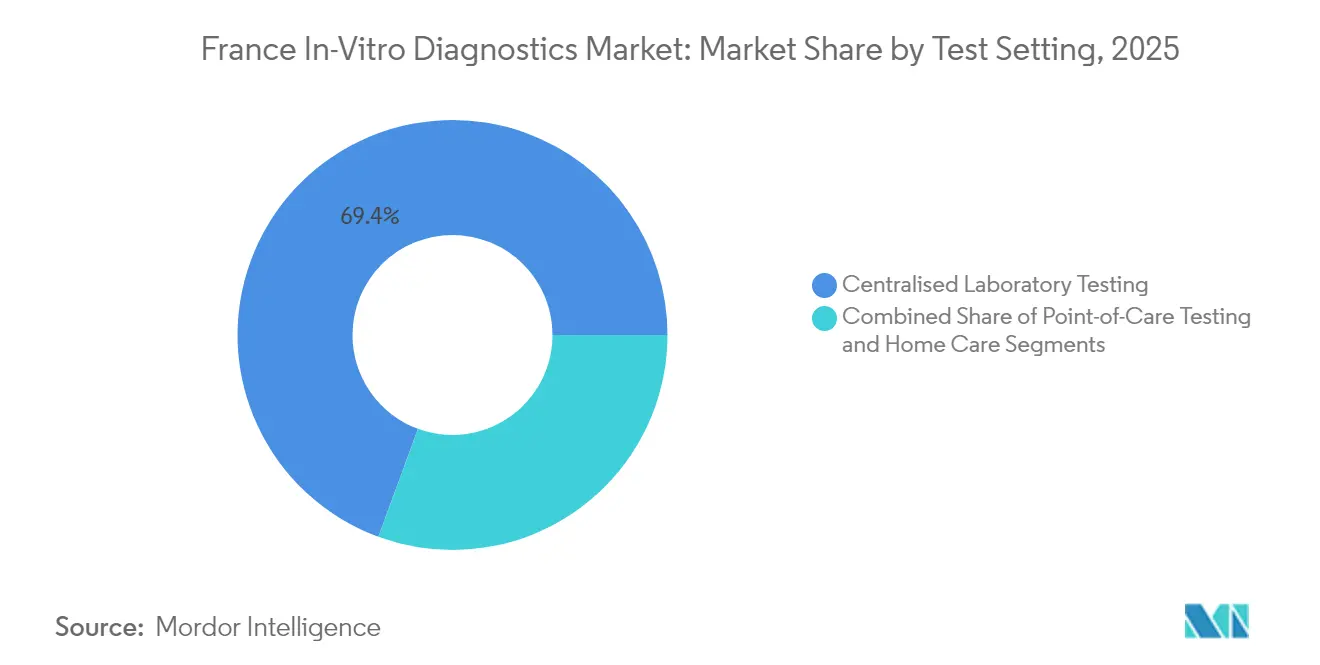

- By test setting, centralized laboratories captured 69.40% of the France in vitro diagnostics market in 2025; self-testing solutions are rising at an 10.92% CAGR to 2031.

- By application, infectious disease diagnostics held 29.90% share of the France in vitro diagnostics market size in 2025 and oncology diagnostics is progressing at a 9.62% CAGR through 2031.

- By end user, independent diagnostic laboratories represented 44.95% of the France in vitro diagnostics market share in 2025, while home-care users are on track for a 11.56% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic & infectious disease surge | +2.1% | National—highest in large metro areas | Long term (≥ 4 years) |

| Reimbursement expansion for high-value tests | +1.5% | National—roll-out starts in major cities | Medium term (2-4 years) |

| Laboratory automation & digital workflows | +1.3% | National—concentrated in chain laboratories | Medium term (2-4 years) |

| Private-lab consolidation | +0.7% | Urban & suburban clusters | Short term (≤ 2 years) |

| Consumer shift to near-patient testing | +0.6% | Early uptake in Paris, Lyon, Marseille | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating chronic and infectious disease burden expanding test volumes

France’s aging profile and rising multimorbidity are enlarging test menus across chemistry, immunoassay, and molecular panels. The share of citizens aged ≥65 is projected to reach 29% by 2050, sustaining high diagnostic demand. Infectious disease panels still represent 30.2% of application revenues, reflecting vigilance after the COVID-19 crisis. Antimicrobial-resistance surveillance is accelerating the uptake of rapid molecular assays that identify pathogens and resistance markers in hours rather than days. Preventive screening programs embed testing into routine care pathways, further lifting volumes across national laboratories and community settings.

National health insurance reimbursement expansion for high-value diagnostics

Policy makers are moving toward ‘coverage-with-evidence’ schemes that reward assays delivering clear clinical utility. Companion diagnostics benefit first, aligning with precision oncology regimens that require biomarker confirmation before targeted therapy initiation. Government reimbursement also extends to select digital diagnostics, incentivizing interoperability between test platforms and electronic health records. This environment encourages innovation while nudging suppliers to prove real-world outcome gains.

Rapid laboratory automation and digital workflow adoption enhancing throughput

Multi-site chains deploy total laboratory automation lines, robotics, and image-analysis algorithms to process >1,000 samples daily with minimal manual intervention. Integrating laboratory information systems with hospital records reduces transcription errors and supports fast clinical decision making. Flexible data architectures enable dynamic load balancing, reallocating instruments in real time to match fluctuating sample inflows.

Rising consumer preference for near-patient and home-based testing solutions

Self-sampling kits for diabetes, infectious disease screening, and fertility tracking gain traction as users seek privacy and convenience. Uptake accelerated during the pandemic, familiarizing consumers with nasal swabs and digital result portals. Mobile apps now interpret results, trend data, and transmit findings securely to physicians, bolstering chronic-disease monitoring programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent IVDR Compliance Increasing Time-to-Market | -0.8% | National, with greater impact on SMEs | Medium term (2-4 years) |

| Shortage of Qualified Medical Biologists & Technicians Limiting Capacity Expansion | -1.2% | National, with acute impact in rural areas | Long term (≥ 4 years) |

| Low-Cost Self-Testing Alternatives Cannibalising Central-Lab Revenues | -0.5% | National, with higher penetration in urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent IVDR compliance increasing time-to-market

The IVDR imposes a risk-based device classification and robust clinical-evidence dossier, stretching approval cycles for innovative assays[2]EUR-Lex, “Regulation (EU) 2024/1860,” eur-lex.europa.eu. July 2024 amendments added mandatory supply-shortage notifications and phased Eudamed registration, further intensifying administrative load. More than 70% of manufacturers have redirected resources to regulatory functions, delaying product launches and potentially limiting test availability during the transition period.

Shortage of qualified medical biologists and technicians limiting capacity expansion

France lists laboratory professions among its top workforce shortages, with retirements outpacing new entrants[3]World Health Organization, “Health Workforce Shortage in Europe,” who.int. Rural regions feel the pinch most acutely, experiencing longer turnaround times and service gaps. Automation mitigates repetitive workload but cannot replace specialist interpretation of complex results. Stakeholders pursue scholarship programs and cross-training initiatives, yet near-term relief remains constrained.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular diagnostics redefining clinical practice

Immuno Diagnostics secured 27.70% of the France in vitro diagnostics market share in 2025, supported by its role in routine hormone, autoimmune, and infectious-disease panels. Large installed analyzer bases and reagent tie-ins ensure stable demand. Molecular Diagnostics, projected to expand at a 9.18% CAGR between 2026 and 2031, increasingly permeates oncology, infectious disease, and hereditary-disease management. Platform trends favor multiplex PCR and next-generation sequencing, shrinking turnaround time from days to hours. Integrated devices such as BIOFIRE SPOTFIRE consolidate multiple respiratory targets into a single cartridge, underscoring the shift toward syndromic panels. Clinical Chemistry, Hematology, and Coagulation continue to provide core hospital metrics, though revenue growth trails molecular assays because of commoditized pricing. Point-of-care cartridges address decentralized needs, broadening access in emergency and outpatient contexts.

Growing emphasis on precision medicine propels companion diagnostics that identify actionable genomic alterations. Laboratories adopt automated extraction and library-prep stations to handle rising sample numbers without proportionate staff increases. This adoption cements molecular testing’s trajectory toward mainstream use, even for conditions historically monitored by immunoassay or microscopy. As a result, the France in vitro diagnostics market expects a rebalanced revenue mix, with molecular diagnostics capturing a progressively larger slice of overall spending.

By Product & Service: Software integration driving value creation

Reagents & Kits captured 64.80% of the France in vitro diagnostics market in 2025, reflecting the consumables-based economics of clinical testing. Proprietary chemistries with demonstrated sensitivity improvements preserve premium pricing, especially in viral-load and oncology panels. Instruments deliver lower share yet underpin long-term customer lock-in, as analyzer selection dictates future reagent pipelines. Software & Services, growing at 11.74% CAGR to 2031, provide laboratories with analytics, quality-control dashboards, and AI-driven decision support. Healthcare networks allocate capital toward interoperable middleware that bridges analyzer outputs and hospital information systems, reinforcing vendor relationships beyond physical hardware supply.

Service contracts now bundle remote monitoring, predictive maintenance, and workflow optimization consulting. This shift positions solution providers as partners in cost containment and regulatory compliance rather than mere equipment vendors. Consequently, software revenues buffer cyclical capital spending, smoothing supplier cash flows and elevating overall customer lifetime value within the France in vitro diagnostics market.

By Specimen: Saliva testing gaining clinical acceptance

Blood specimens remained dominant at 44.60% of the France in vitro diagnostics market size in 2025 because of their multiparametric biomarker richness and entrenched phlebotomy routines. Automated hematology and chemistry lines sustain high throughput and consistent quality metrics. Urine testing occupies the next tier, leveraging its non-invasive collection for metabolic and renal surveillance. Salivary diagnostics, forecast to rise at a 10.08% CAGR through 2031, benefit from painless collection suited for pediatric, geriatric, and remote contexts. Advanced spectrometry and sequencing now detect oncogenic mutations, cortisol rhythms, and viral RNA in micro-volume saliva, broadening clinical readiness.

Investments in stabilizing buffers extend sample viability during transport, enabling mail-in programs that connect rural patients to urban reference labs. Tissue biopsies and stool samples continue to anchor oncology and gastroenterology workflows, albeit with modest growth as liquid biopsy and non-invasive screening options gain traction.

By Test Setting: Self-testing revolution reshaping access

Centralized laboratories processed 69.40% of national test volumes in 2025, leveraging automated tracks and robotics for speed, standardization, and cost control. High fixed costs are offset by heavy throughput, with private-equity-backed chains optimizing logistics across hub-and-spoke networks. Point-of-care testing fills critical gaps in emergency wards and physician offices, providing decision-grade results within minutes. Self-testing platforms, posting an 10.92% CAGR to 2031, empower consumers through intuitive sample collection and smartphone-enabled result interpretation. Regulatory bodies issued new guidance on labeling, digital instructions, and post-market surveillance to safeguard test accuracy outside clinical environments.

Cloud-linked devices feed longitudinal datasets into telehealth consults, supporting medication titration and lifestyle counseling. This patient-centric evolution lifts overall France in vitro diagnostics market penetration, especially among populations that previously faced mobility, time, or stigma barriers to routine testing.

By Application: Oncology diagnostics driving precision medicine

Infectious disease panels retained 29.90% share of the France in vitro diagnostics market in 2025. Respiratory multiplex assays, sexually transmitted infection screens, and antimicrobial-resistance profiling form the backbone of public-health surveillance. Diabetes monitoring remains sizable thanks to steady prevalence and mandatory HbA1c tracking. Oncology diagnostics are projected to increase at a 9.62% CAGR during 2026-2031 as liquid biopsies and comprehensive genomic profiling transition from specialty centers to broader clinical use. Circulating tumor DNA tests complement tissue biopsy, guiding therapy selection and relapse monitoring without invasive procedures. Cardiovascular biomarker panels evolve toward multi-analyte risk scores, and prenatal testing shifts to non-invasive cell-free DNA approaches.

Growing payer acceptance of outcome-linked reimbursement accelerates advanced cancer diagnostics. Laboratories partner with oncology clinics to integrate genomic reports directly into tumor boards, streamlining precision-therapy decisions and elevating the strategic importance of oncology within the overall France in vitro diagnostics market.

By End User: Home-care users driving market expansion

Independent diagnostic laboratories held 44.95% France in vitro diagnostics market share in 2025, benefiting from economies of scale, specialized expertise, and robust purchasing power secured through consolidation. Hospital laboratories remain indispensable for acute care, offering round-the-clock testing and advanced esoteric panels critical to inpatient management. Physician-office laboratories cater to point-of-care needs but face reimbursement pressure and instrument-utilization challenges.

Home-care and self-testing users will grow at a 11.56% CAGR to 2031 as device miniaturization and digital literacy improve. Portable readers interpret lateral-flow cartridges for infections, metabolic markers, and reproductive health, feeding encrypted data to clinicians. This trend expands total diagnostic spend by engaging previously underserved users and shifting some burden away from overstretched hospital labs. Academic and research institutes continue to pilot emerging modalities such as spatial transcriptomics, ensuring France remains at the forefront of diagnostic innovation.

Geography Analysis

Regional dynamics shape access and innovation within the France in vitro diagnostics market. Paris-Île-de-France hosts the largest concentration of reference laboratories and med-tech headquarters, bolstered by proximity to major teaching hospitals and venture capital. Grand Est’s Alsace Biovalley cluster specializes in molecular diagnostics and imaging, nurturing start-ups via incubator programs and public-private grants. The Auvergne-Rhône-Alpes region, anchored by Lyon, benefits from hospital networks such as Hospices Civils de Lyon, which deploy high-throughput automation suites that process ≥1,200 microbiology samples per day.

Southern hubs around Marseille integrate port logistics with supply-chain efficiency, facilitating reagent imports and analyzer distribution. Government commitment, exemplified by a EUR 25 billion health-science investment fund, sustains R&D pipelines and helps SMEs navigate IVDR compliance hurdles. While urban centers enjoy dense laboratory coverage, rural départements experience technician shortages and longer sample transit times, prompting mobile collection programs and telepathology pilots. Initiatives such as tele-expertise platforms enable rural clinicians to obtain specialized second opinions, narrowing geographic disparities. Cross-border collaboration with Germany, Switzerland, and Italy strengthens market resilience and knowledge transfer. French laboratories participate in EU antimicrobial-resistance surveillance networks, sharing data and alerting authorities to emerging threats. The net result is a geographically balanced yet interconnected ecosystem that sustains demand and fosters innovation across the France in vitro diagnostics market.

Regulatory Landscape

France IVDs are governed primarily by the EU In Vitro Diagnostic Regulation (IVDR, Regulation (EU) 2017/746). ANSM is the competent authority for market surveillance, inspections, and vigilance oversight for medical devices and IVDs placed on the French market. In addition to CE marking requirements under IVDR, France also requires operator declarations and incident reporting to ANSM, supporting reactovigilance and traceability across centralized laboratories and self-testing channels.

In April 2026, Decree No. 2026-298 (IVDs) and Decree No. 2026-299 (medical devices) were published on 21 April 2026 and entered into force on 22 April 2026. The decrees codify the application of EU Regulations 2017/746 and 2017/745 into the French Public Health Code. They clarify administrative procedures and responsibilities for economic operators and reinforce documentation expectations, including French-language labeling and instructions for use for IVDs marketed in France, which adds compliance discipline as IVDR transition activities continue.

Competitive Landscape

Market concentration remains moderate. Roche, Abbott, bioMérieux, Siemens Healthineers, and Becton Dickinson collectively control an estimated 60-65% of national revenues through comprehensive reagent and analyzer portfolios. bioMérieux leverages domestic roots and a 10.3% organic sales jump in the first nine months of 2024 to fortify leadership in syndromic panels. Roche deepens digital connectivity, embedding algorithmic decision support within its cobas lines. Abbott expands point-of-care offerings while linking home glucose meters to cloud dashboards.

Specialized entrants target high-growth niches—liquid biopsy, non-invasive prenatal testing, and AI-assisted digital pathology—challenging incumbents on agility and depth. Becton Dickinson’s announced spin-off of its Biosciences and Diagnostic Solutions unit underscores portfolio optimization trends. Partnerships proliferate, pairing analyzer manufacturers with software firms to produce integrated end-to-end solutions. Procurement contracts increasingly stipulate performance-based metrics, compelling suppliers to prove throughput, uptime, and clinical impact.

Technology differentiation focuses on multiplexing capacity, automation compatibility, and cybersecurity safeguards. Suppliers offering seamless reagent-instrument-software stacks gain an edge, especially within consolidated laboratory chains negotiating at national scale. Meanwhile, government emphasis on domestic manufacturing resilience during supply disruptions encourages dual-sourcing strategies, granting smaller French innovators entry points into hospital formularies.

France In-Vitro Diagnostics Industry Leaders

Thermo Fischer Scientific Inc

QIAGEN N.V.

Siemens Healthcare GmbH

F. Hoffmann-La Roche AG

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

France offers multiple routes for novel diagnostics, including standard listing pathways (LPP/LPPR) and temporary mechanisms such as RIHN (for innovative tests outside the nomenclature) alongside the Forfait Innovation program, which supports conditional reimbursement while real-world evidence is collected. Suppliers that align clinical and economic evidence packages with HAS assessment requirements can reduce the gap between technical validation and scalable adoption across hospital and independent lab networks.

Digital and AI-enabled diagnostics are also a key opportunity area tied to national programs and assessment priorities. The French National Strategy for Artificial Intelligence and Health Data (2025) and the Health Data Hub roadmap support integration of algorithmic tools into clinical workflows, while the HAS 2025-2030 Strategic Project highlights the need to adapt evaluation methods for miniaturized devices, next-generation sequencing, and AI-driven diagnostics. For suppliers, this environment increases demand for interoperable software, connectivity, and governance-ready data pipelines that fit French care pathways, reinforcing the role of software and services alongside reagents and instruments in procurement decisions.

Recent Industry Developments

- July 2026: QIAGEN launched the QIAstat-Dx BCID GN Plus AMR panel in Europe, expanding its syndromic testing menu for high-acuity microbiology workflows. The launch supports faster pathogen identification and antimicrobial resistance marker detection within consolidated, high-throughput laboratory settings common in France.

- July 2025: Thermo Fisher Scientific announced availability of its EXENT Solution for monoclonal gammopathies and multiple myeloma diagnostics in France, expanding access to automated data-rich hematology workflows. The update enhances capacity and standardization in oncology and hematology testing across hospital networks.

- September 2024: QIAGEN received EU IVDR certification for QIAstat-Dx syndromic testing instruments and assays, including the Gastrointestinal Panel 2 and Respiratory Panel Plus. This certification strengthens continuity of supply and procurement confidence under tighter IVDR evidence requirements, helping laboratories maintain access to validated multiplex panels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers in vitro diagnostic tests and related products used in France to analyze human samples outside the body and support screening, diagnosis, and monitoring decisions.

Scope exclusions: This sizing does not include in vivo imaging diagnostics, therapeutic drugs, or general lab consumables that are not specifically used for IVD testing.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Molecular Diagnostics

- Immuno Diagnostics

- Hematology

- Coagulation

- Microbiology

- Point-of-Care Testing

- Other Test Types

- By Product & Service

- Instruments

- Reagents & Kits

- Software & Services

- By Specimen

- Blood

- Urine

- Saliva

- Tissue & Biopsy

- Stool

- Other Specimens

- By Test Setting

- Centralised Laboratory Testing

- Point-of-Care Testing

- Self-Testing / Home Care

- By Application

- Infectious Disease

- Diabetes

- Cancer / Oncology

- Cardiology

- Autoimmune Disorders

- Prenatal & Newborn Screening

- Other Applications

- By End User

- Independent Diagnostic Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Academic & Research Institutes

- Home Care & Self-Testing Users

- Other End Users

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by collecting stable France-level health and diagnostics signals, and then mapping them to IVD demand and spend. Public sources such as the World Health Organization, OECD health statistics, Eurostat, French public health publications, and medical device regulatory guidance were used to understand disease burden, testing pathways, and care delivery patterns. Where relevant, peer reviewed clinical literature was also checked to confirm how testing volumes change for key conditions.

To keep the model practical, the desk stage also used company annual reports, investor presentations, association webpages, and reputable press coverage to cross-check product availability and pricing direction. In addition, paid subscriptions covering company financials and patent activity were used selectively to validate business scale and technology activity without relying on a single data point. This list is illustrative only, and many other sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews were used to pressure test the desk assumptions, especially how testing shifts between centralized labs and point-of-care settings, and how price levels move for high volume assays. We spoke with manufacturers, distributors, lab operators, and clinical stakeholders across France so the final market build reflects purchasing behavior and tender dynamics.

Where inputs did not align, respondents were re-contacted and the assumptions were narrowed to what could be explained by clear demand drivers and common pricing practices.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 13% | |

| Mid tier: 47% | Functional/Unit leaders: 39% | |

| Smaller Players: 15% | Managers: 48% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where the main structure starts from France healthcare testing demand and then gets translated into IVD spending by test setting and product mix. In practice, this meant reconstructing the demand pool using indicators such as diagnosed and monitored patient counts for key conditions, routine screening rates, average test frequency per pathway, and the share of tests performed in centralized laboratories versus point-of-care and self-testing channels. Pricing was handled using representative selling price ranges that were checked by interview feedback, and then applied to volumes in a way that avoids double counting across instruments, reagents, and related services.

After the top-down build, the totals were cross-checked with selective bottom-up approximations, such as supplier revenue direction, channel checks with distributors, and sampled volume times price calculations for common assay groups. Where a specific category had limited visibility, the gap was handled through conservative share-based allocations anchored to known testing behavior, followed by a review with experts to confirm it still matches France care setting reality.

For forecasting, scenario analysis was used because year-to-year growth is strongly influenced by policy, reimbursement, and adoption pace for newer test formats. The forward view was anchored on how variables like the aging population, chronic disease monitoring intensity, infectious disease testing normalization, laboratory automation uptake, and price progression expectations are likely to evolve based on what primary respondents see in budgets and tenders.

Data Validation & Update Cycle

Validation was done in layers so the output does not depend on one dataset or one interview. Model results were compared with independent signals, including test setting shifts, mix changes between routine assays and advanced diagnostics, and plausible price bands, and then variances were reviewed before sign-off. If a number looked stretched, the assumptions behind volumes, price, or mix were revisited, and we followed up with sources to confirm what changed.

The report is refreshed annually, and interim checks are triggered when material events occur, such as reimbursement revisions or major regulatory changes affecting product availability. Before delivery, a final review pass is completed so clients receive an updated view aligned with the latest accessible information.

Mordor Intelligence's Vitro Diagnostics France Market Estimate Compared With Other Published Estimates

Published market sizes for France IVD can differ even when the topic label looks the same, because each estimate makes its own choices on what gets counted and how demand is reconstructed. The gaps usually come from differences in product boundary, the balance between volumes and pricing, and how quickly assumptions are refreshed when testing behavior changes.

By tracking test-setting mix, average selling price ranges, and annual refresh triggers, Mordor Intelligence keeps the France IVD total tied to observable demand signals (like routine monitoring cadence and point-of-care penetration) rather than broad device spending pools. In some estimates, adjacent lab supplies or wider medtech categories get blended in, while in others the model leans heavily on a single historical base year that does not fully capture post-period normalization in infectious testing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.95 B (2025) | |

| Global Consultancy A | USD 4.37 B (2025) | This estimate appears to use a broader inclusion set across products and services, which can pull in adjacent lab-related spend and lift the total versus a stricter IVD-only boundary. |

| Industry Publisher B | USD 3.11 B (2023) | The base year and growth window differ, and the model implies a much flatter expansion path, which can happen when post-2023 testing normalization, mix shifts, and price updates are not fully re-checked. |

Across the three values, the spread is mainly explained by boundary choices and the timing of the base year, followed by how volumes and pricing are blended across settings. Our approach is meant to stay repeatable, since each step is tied to clear demand drivers, practical price checks, and review loops that are easy to trace during validation.

Key Questions Answered in the Report

How large will diagnostic testing revenue be in France by 2031?

The France in vitro diagnostics market size is projected at USD 5.95 billion by 2031 under a 7.08% CAGR.

Which segment shows the fastest growth momentum?

Molecular diagnostics is forecast at 9.18% CAGR as precision oncology, infectious-disease surveillance, and genetic screening expand.

What drives the move toward at-home testing?

Higher consumer digital literacy, pandemic-era familiarity with self-sampling, and smartphone-linked result interpretation fuel an 10.92% CAGR in self-testing volumes.

How does IVDR affect French suppliers?

Stricter evidence requirements, phased Eudamed registration, and supply-notification rules extend approval timelines and raise compliance costs, particularly for SMEs.

What workforce challenges loom for laboratories?

France faces a 1.2% CAGR drag from shortages of medical biologists and technicians, especially outside major urban centers, prompting investment in automation and training.

Page last updated on: