ユーティリティトラクター市場規模

| 調査期間 | 2019 - 2029 |

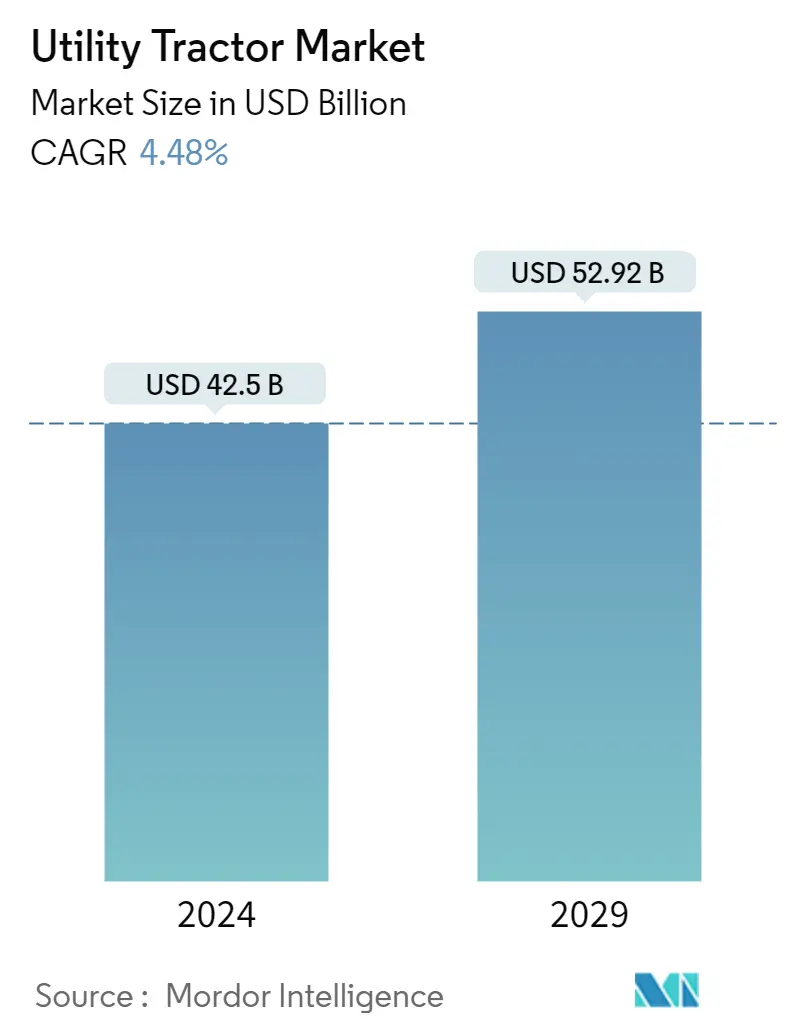

| 市場規模 (2024) | USD 425億ドル |

| 市場規模 (2029) | USD 529.2億ドル |

| CAGR(2024 - 2029) | 4.48 % |

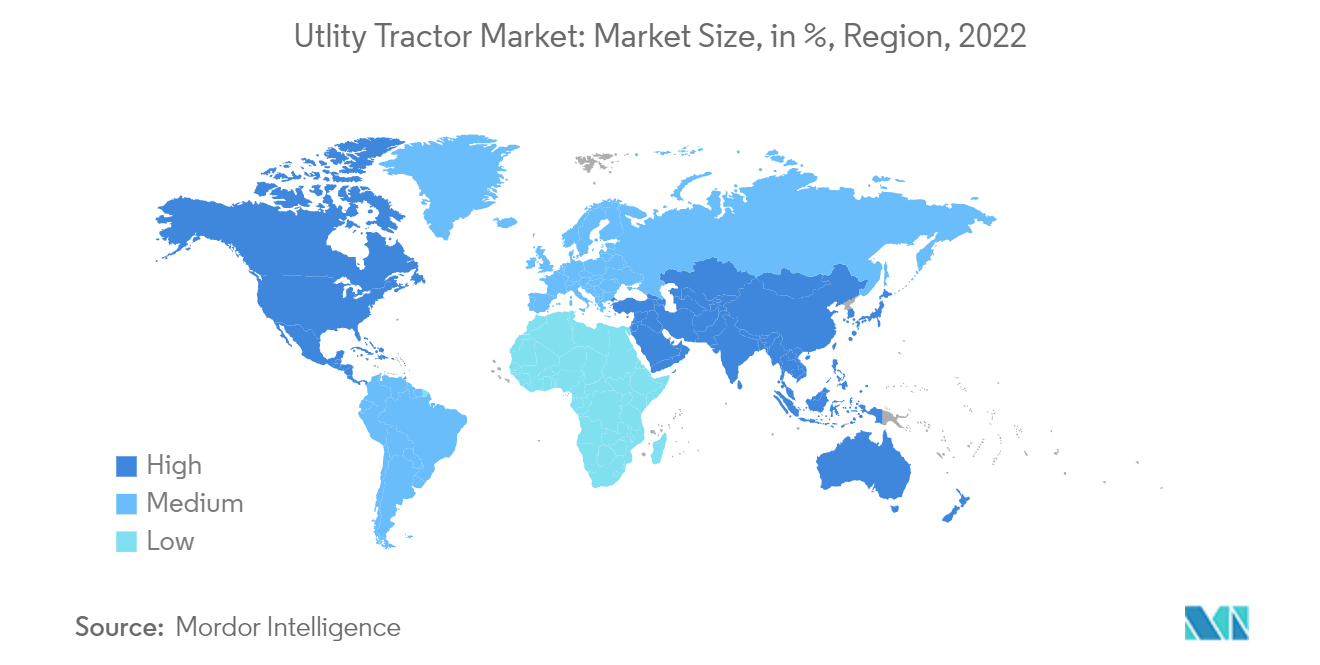

| 最も成長が速い市場 | 北米 |

| 最大の市場 | アジア太平洋地域 |

主なプレーヤー

*免責事項:主要選手の並び順不同 |

何かお手伝いできることはありますか?

ユーティリティトラクター市場分析

ユーティリティトラクター市場規模は、2024年に425億米ドルと推定され、2029年までに529億2000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.48%のCAGRで成長します。

- ユーティリティトラクターは、フロントローダー作業、土づくり、運搬などさまざまな作業に使用できるように設計されています。このタイプのトラクターは、耕耘や重量物を牽引するなどの農業作業に使用されます。食糧需要の増加と農業機械化の普及により、世界的に農業における機械の使用が増加しています。ユーティリティトラクターは、農家が農業プロセスを簡単に実行できるように支援します。

- ユーティリティ トラクターは、35 馬力から 100 馬力の範囲のセグメントで構成されており、小規模から中規模の農業作業向けの多くのコンパクトなユーティリティ タイプのトラクターが含まれます。小規模農家は、平均的な農業用トラクターよりもはるかに小さく、価格がはるかに安いため、コンパクトユーティリティトラクター (40HP ~ 70HP) を採用することが増えています。低コストにもかかわらず、コンパクトなトラクターは、農家がバックホーやフロントエンドローダーなどの農機具を使って多くの作業を実行し、人件費を節約するのに役立ちます。大型 (41 ~ 50 馬力) トラクターの需要増加の主な理由は硬い土壌条件ですが、インフラストラクチャーや建設分野などの非農業分野での使用の増加もこのカテゴリーの需要の増加に貢献しています。これにより、ユーティリティトラクター業界は今後数年間で成長するでしょう。

- ユーティリティトラクターは、フロントエンドローダーやバックホーなどの重要な前部または後部のアタッチメントを使用して、積み込みや掘削を行うことができます。それでも、造園、種まき、干し草の栽培、除雪にも使用できるため、この分野の市場を世界的に牽引しています。インドの農業機械化レベルは、2019年に4.48%~45.0%と記録されました。国内の零細農家のほぼ80.0%が所有する土地が5ヘクタール未満であるため、農機具の普及は遅れています。インドの農業部門では、動物の力や人間の力の使用が大幅に減少しています。これらの多くは、トラクターやディーゼル エンジンなどの化石燃料を燃料とする車両によって駆動されます。これにより、伝統的な農業プロセスからより機械化された農業プロセスに移行しました。

- インドの機械化のレベルは、中国やブラジルなどの他の発展途上国に比べて低いものの、確実に成長段階にあります。機械化レベルを高めるために、インド政府は「バランスの取れた農業機械化を推進しています。さまざまな機器に補助金を提供し、フロントエンド代理店を通じて大量購入をサポートすることで、予測期間中にユーティリティトラクター市場が強化されると予想されます。

ユーティリティ・トラクターの市場動向

高まる農業機械化志向

- 精密農業と、生産量増加のための農業技術導入の増加は、世界中の最小限の耕作地におけるユーティリティ・トラクターの需要を押し上げている。農業機械の使用を広く推進する農業研修プログラムの増加も、トラクター業界を牽引している。さらに、いくつかの発展途上国では、政府が主要な農業プロセスの自動化を支援するために補助金や財政援助を行っている。

- さらに、さまざまな技術的躍進により、GPSやテレマティクス・システムがプリインストールされた最新のトラクターも登場している。世界の農業用トラクター市場は、自動化されたトラクターの人気の高まりと、遠隔監視のためのワイヤレス接続の普及によって牽引される可能性が高い。

- 農業の機械化は、現代農業において農家の収入を増やすために不可欠である。しかし、中国における作物生産への機械の使用は非効率的である。北京の中国農業大学(CAU)が実施した調査によると、2020年、全国の作物の植え付けと収穫の機械化率は71%に達した。

- 作付けと収穫の機械化率の合計は、小麦、コメ、トウモロコシでそれぞれ95%、85%、90%を超えた。農業の機械化を加速させるため、中国政府は農民の機械利用を奨励する一連の政策を打ち出し、機械購入や機械操作に対する財政補助、個人農家に機械を提供する協同組合への支援などを行った。

- また、アジア太平洋地域の農家は、効率的な農業を実現するために、ニーズに合わせた機能を備えたユーティリティ・トラクターを求めている。そのため、消費者の需要に応えるため、国内外の多くの農業機械メーカーが、様々な農業用途に対応できる技術的に先進的な新型実用トラクターを開発し、今後の市場の成長を後押ししている。

- 2022年、ジョンディアUSは農家向けユーティリティ・トラクターGtaorを発売した。オートトラックアシストステアリングシステムは、車両が圃場を移動する際に一貫した再現可能な精度と効率を維持することで、オペレーターの生産性を向上させる。オートトラックが作動することで、農家は注意力を維持したまま、機械の設定や変化する圃場条件の制御に集中することができる。農家はユーティリティ・トラクターを、正確なグリッド・サンプリング、散布、圃場境界の作成に使用しています。

アジア太平洋地域が市場を支配

- インドでは豊富で安価な労働力があるにもかかわらず、食糧需要が伸びており、トラクターを中心とした農業機械化の導入が進んでいる。これは中国でも同様で、農業の機械化が進んでいる。インドや中国の農家が機械化を進めるようになったのには、いくつかの理由がある。ひとつは、人口増加と都市化による食糧需要の増大で、農業の生産性向上が求められていること。もうひとつの理由は、人件費の高騰で、機械に投資したほうが費用対効果が高くなっていることだ。

- 国内における実用トラクターの普及率は、北インド、特にパンジャブ州、ウッタル・プラデシュ州、ハリヤナ州で高い。インドでは、インド政府による農業マクロ管理スキームの機械化部門において、農業機械化を促進するための補助金制度があり、最大35馬力(PTO)のトラクターを購入する場合、3万インドルピーを上限として費用の25%が補助される。インドでは、カスタム・ハイヤー・サービスが小規模農家に恩恵をもたらし、小規模土地所有者の利益のためにユーティリティ・トラクターを運営する新しいタイプの起業家が出現している。これらの要因によって、予測期間中、同地域の市場は成長すると思われる。

- 中国における農業機械化の増加の背景には、農業投資の増加と政府による農業機械化への後押しがある。農業機械化への投資は、アジア太平洋地域におけるユーティリティ・トラクターの需要を生み出している。中国国家統計局のデータによると、中国は2019年に617,700台のトラクターを生産した。大型・中型トラクターが徐々に小型トラクターに取って代わった。

- 2019年末までに、中国は444万台の大型・中型トラクターを含む2224万台の農業用トラクターを誇った。中国はまた、「メイド・イン・チャイナ2025計画を導入しており、2020年までに農業用トラクターのようなハイエンド機械がそのセグメントの3分の1のシェアを占めるように、農業機械の90%を生産することに焦点を当てている。これにより、自国生産トラクターが後押しされ、同国の農業用トラクター市場が活性化する。

- ユーティリティ・トラクターは農業プロセスに使用されており、マヒンドラ&マヒンドラ社やジョンディア社など、同国の主要プレーヤーはその製品の助けを借りて、今後数年間の市場成長を増加させるためにこの地域で実施される農業慣行に大きく貢献している。発展途上国では、農家の可処分所得が低く人件費が高いため、35HP~100HPのトラクターの需要が高い。農家は農地が狭いため、農業用に小型でカスタマイズされたコンパクト/ユーティリティトラクターを好む。さらに、小型トラクターによる燃料消費量の少なさは、小規模農家や限界農家を力づけるのに役立っている。

ユーティリティ・トラクター産業の概要

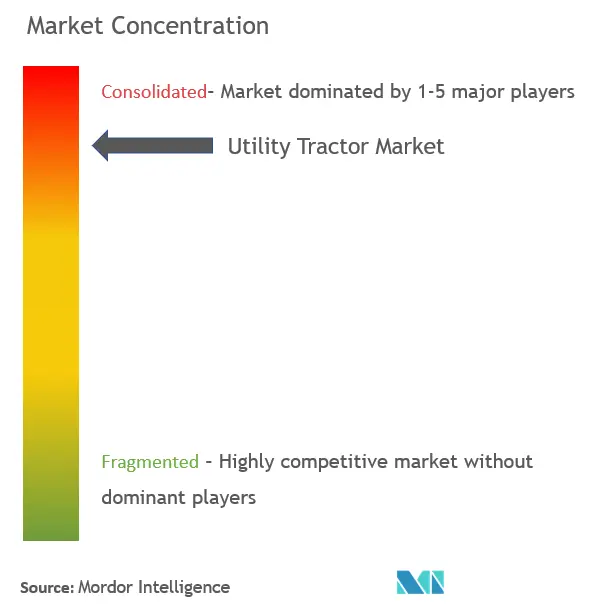

ユーティリティ・トラクター市場は高度に統合されており、少数のプレーヤーが市場シェアの大半を占めている。Deere Company、CNH Industrial、AGCO Corporation、CLAAS KGaA mbH、Mahindra Mahindra Corporationがこの市場の主要プレーヤーである。新製品の発売、パートナーシップ、買収は、世界の主要企業が採用する主要戦略である。技術革新や事業拡大とともに、研究開発への投資や斬新な製品ポートフォリオの開発も、今後数年間は重要な戦略となりそうだ。

ユーティリティ・トラクター市場のリーダー

-

Deere and Company

-

CLAAS KGaA mbH

-

Mahindra and Mahindra Corporation

-

AGCO Corporation

-

CNH Global NV

*免責事項:主要選手の並び順不同

ユーティリティ・トラクター市場ニュース

- 2022年4月:クボタは、北米の顧客のトラクターニーズに対応するため、ジョージア州の280エーカーの新しい土地に研究開発部門を拡張した。クボタは、新施設のオンラインプラットフォーム化に8,500万米ドル以上を投資。

- 2021年12月ジョンディアは、電気自動車ユーティリティトラクターのラインナップを拡充し、市場における製品ポートフォリオを拡大するため、クライゼルエレクトリック社を買収。

ユーティリティ・トラクター市場レポート-目次

1. 導入

1.1 研究の前提条件と市場定義

1.2 研究の範囲

2. 研究方法

3. エグゼクティブサマリー

4. 市場ダイナミクス

4.1 市場概況

4.2 市場の推進力

4.3 市場の制約

4.4 ポーターのファイブフォース分析

4.4.1 新規参入の脅威

4.4.2 買い手/消費者の交渉力

4.4.3 サプライヤーの交渉力

4.4.4 代替品の脅威

4.4.5 競争の激しさ

5. 市場セグメンテーション

5.1 地理

5.1.1 北米

5.1.1.1 アメリカ

5.1.1.2 カナダ

5.1.1.3 北米のその他の地域

5.1.2 ヨーロッパ

5.1.2.1 ドイツ

5.1.2.2 イギリス

5.1.2.3 フランス

5.1.2.4 スペイン

5.1.2.5 イタリア

5.1.2.6 ヨーロッパの残りの部分

5.1.3 アジア太平洋地域

5.1.3.1 中国

5.1.3.2 日本

5.1.3.3 インド

5.1.3.4 残りのアジア太平洋地域

5.1.4 世界のその他の地域

5.1.4.1 ブラジル

5.1.4.2 南アフリカ

5.1.4.3 他の国々

6. 競争環境

6.1 最も採用されている戦略

6.2 市場シェア分析

6.3 会社概要

6.3.1 Deere and Company

6.3.2 CNH Global NV

6.3.3 AGCO Corporation

6.3.4 CLAAS KGaA mbH

6.3.5 Mahindra and Mahindra Corporation

6.3.6 Kubota Corporation

6.3.7 Escorts Group

6.3.8 Tractors and Farm Equipment Limited (TAFE)

6.3.9 Kuhn Group

6.3.10 Yanmar Company Limited

7. 市場機会と将来のトレンド

ユーティリティ・トラクター産業のセグメント化

ユーティリティトラクターは、主に補助装置を牽引するために使用される低~中馬力のトラクターですが、溝掘り、溝掘り、破砕などのアタッチメントを装着して建設現場でも使用されます。50から100馬力のユーティリティ・トラクターのほとんどは、農場周辺でできるほとんどすべてのことに対応できる。

ユーティリティトラクター市場は地域別に北米、ヨーロッパ、アジア太平洋、南米、アフリカに区分され、15カ国以上をカバーしている。

本レポートでは、上記のすべてのセグメントについて、台数(単位)と金額(単位:百万米ドル)の市場規模と予測を提供しています。

| 地理 | ||||||||||||||

| ||||||||||||||

| ||||||||||||||

| ||||||||||||||

|

ユーティリティ・トラクター市場調査FAQ

ユーティリティトラクター市場の規模はどれくらいですか?

ユーティリティトラクター市場規模は、2024年に425億米ドルに達し、4.48%のCAGRで成長し、2029年までに529億2000万米ドルに達すると予想されています。

現在のユーティリティトラクターの市場規模はどれくらいですか?

2024 年のユーティリティトラクター市場規模は 425 億米ドルに達すると予想されます。

ユーティリティトラクター市場の主要プレーヤーは誰ですか?

Deere and Company、CLAAS KGaA mbH、Mahindra and Mahindra Corporation、AGCO Corporation、CNH Global NVは、ユーティリティトラクター市場で活動している主要企業です。

ユーティリティトラクター市場で最も急速に成長している地域はどこですか?

北米は、予測期間 (2024 ~ 2029 年) にわたって最も高い CAGR で成長すると推定されています。

ユーティリティトラクター市場で最大のシェアを持っている地域はどこですか?

2024年には、アジア太平洋地域がユーティリティトラクター市場で最大の市場シェアを占めます。

このユーティリティトラクター市場は何年をカバーしており、2023年の市場規模はどれくらいですか?

2023年のユーティリティトラクター市場規模は406億8,000万米ドルと推定されています。このレポートは、2019年、2020年、2021年、2022年、2023年のユーティリティトラクター市場の過去の市場規模をカバーしています。また、レポートは、2024年、2025年、2026年、2027年、2028年、2029年のユーティリティトラクター市場の規模も予測します。

ユーティリティ・トラクター産業レポート

Mordor Intelligence™ Industry Reports によって作成された、2024 年のユーティリティ トラクター市場シェア、規模、収益成長率の統計。ユーティリティトラクターの分析には、2029年までの市場予測見通しと過去の概要が含まれます。この業界分析のサンプルを無料のレポート PDF ダウンロードとして入手してください。

ユーティリティトラクター レポートスナップショット