Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

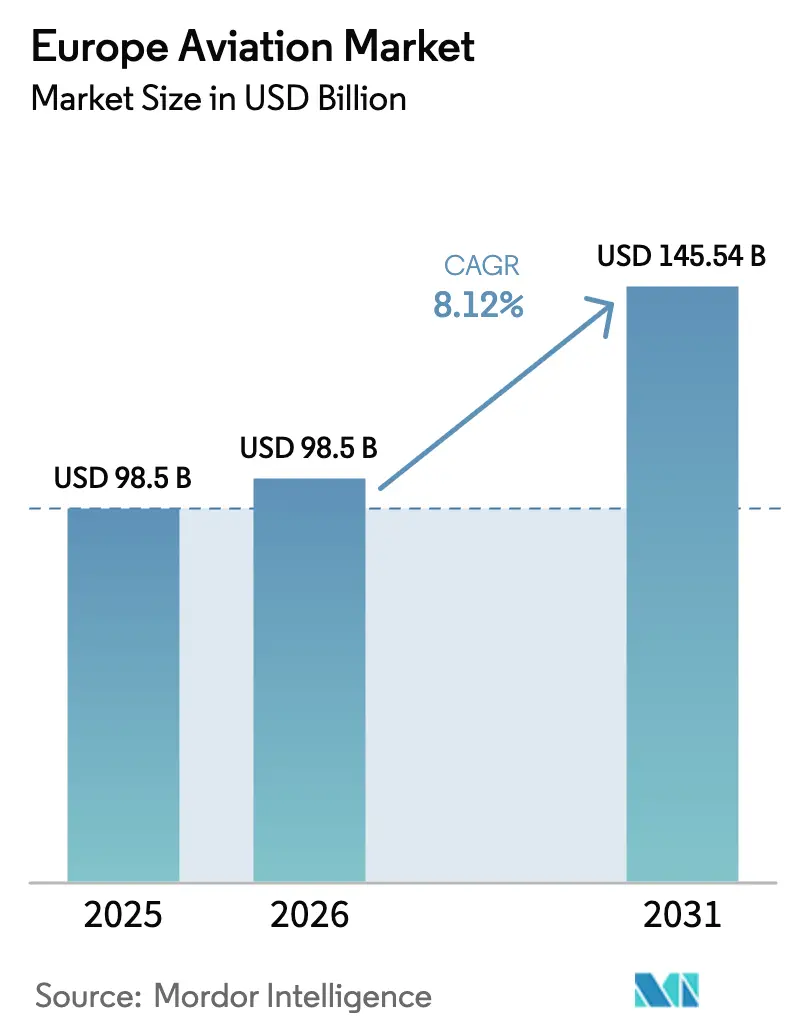

| Base Year Market Size (2025) | USD 98.5 Billion |

| Market Size (2026) | USD 98.5 Billion |

| Market Size (2031) | USD 145.54 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

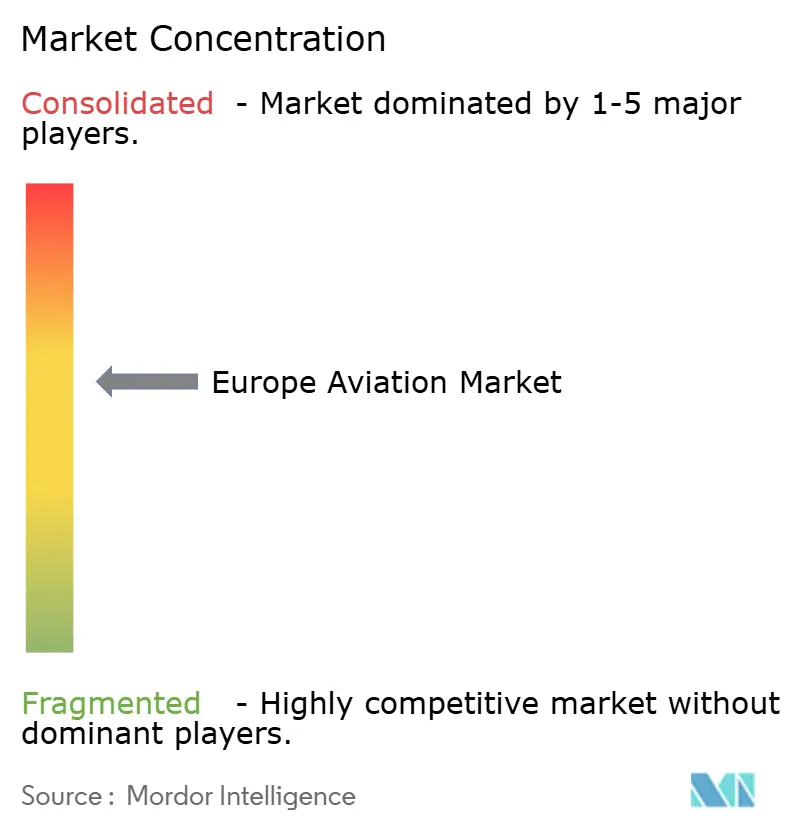

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Aviation Market Analysis by Mordor Intelligence

The Europe aviation market size is expected to grow from USD 98.5 billion in 2025 to USD 106.52 billion in 2026 and is forecasted to reach USD 157.38 billion by 2031 at 8.12% CAGR over 2026-2031. This acceleration signals that the rebound is not merely cyclical, but rooted in defense rearmament, green tax incentives, sustainable aviation fuel (SAF) mandates, and concerted bets on hydrogen propulsion. Budget reallocations prompted by the Ukraine conflict are widening the military order pipeline, while France, Germany, and the Netherlands are increasing carbon levies, thereby shortening the payback periods for new-generation aircraft. Private-public consortia, backed by the Clean Aviation Joint Undertaking and the UK Aerospace Technology Institute, are fast-tracking the certification of hydrogen-ready systems even as regulators finalize safety standards. Airlines, meanwhile, are extending the life of in-service narrowbodies through retrofit programs that offer rapid fuel-burn savings without significant capital outlays. The combined effect is that the Europe aviation market is entering a structurally expansionary phase, with venture capital and strategic investors directing record funds toward electric vertical takeoff and landing (eVTOL) programs.

Key Report Takeaways

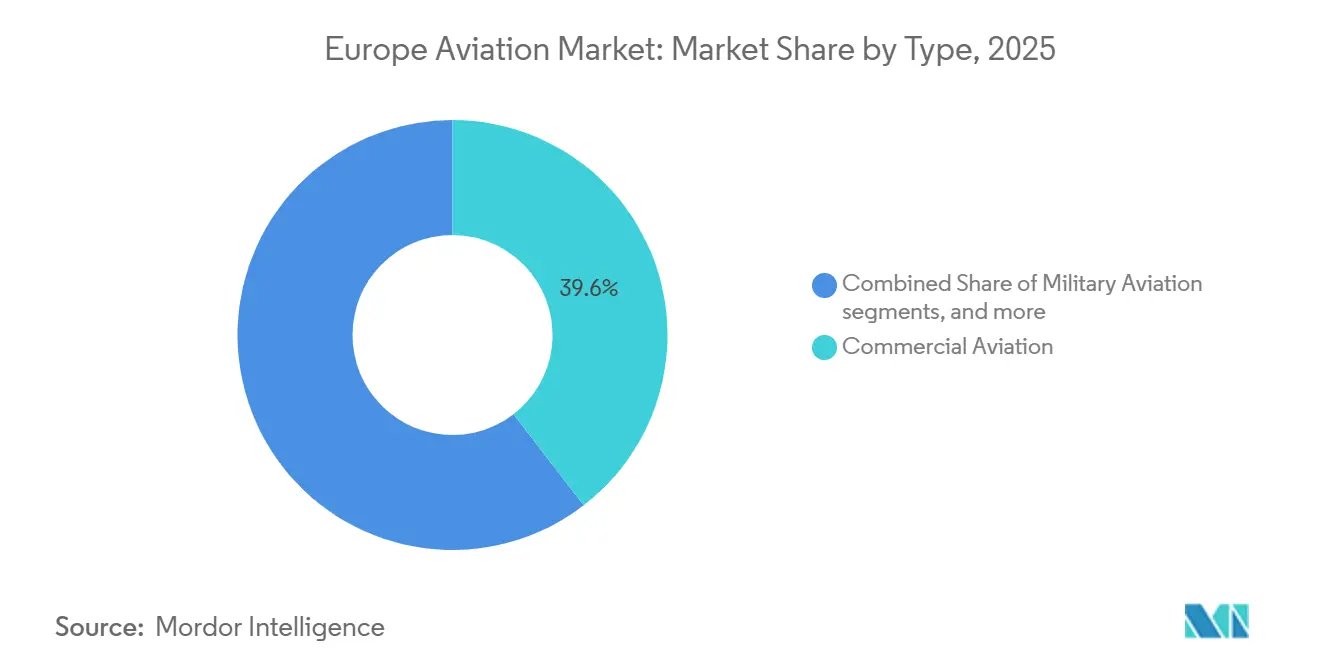

- By type, commercial aviation held 39.55% of the Europe aviation market share in 2025, while advanced air mobility (AAM) is projected to post the quickest expansion at a 9.45% CAGR through 2031.

- By propulsion technology, turbofan engines dominated with a 26.76% share in 2025, whereas electric propulsion is expected to advance at a 10.38% CAGR over the same horizon.

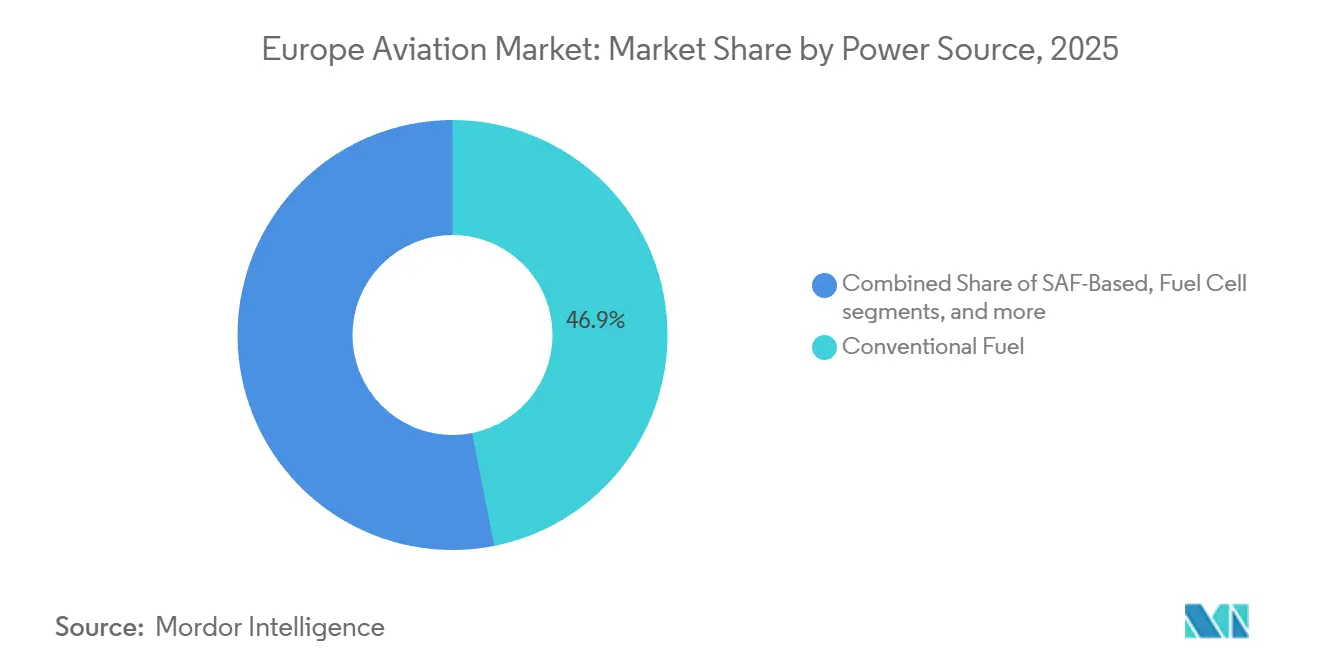

- By power source, conventional fuel continued to account for 46.88% of spending in 2025; however, solar-powered platforms are forecast to grow at an 11.26% CAGR as long-endurance missions increase.

- By fit, linefit installations accounted for 53.26% of deliveries in 2025; however, retrofit solutions are expected to expand faster, with a 9.21% CAGR through 2031.

- By geography, France retained the largest footprint, accounting for 36.71% of the Europe aviation market size in 2025, while the United Kingdom is expected to be the fastest climber, with an 8.88% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Aviation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-tax incentives for fleet renewal | +1.20% | France, Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Air-traffic recovery post-COVID | +1.50% | Europe-wide, strongest on Mediterranean routes | Short term (≤2 years) |

| Surge in e-commerce-driven freighter conversions | +0.80% | Germany, UK, Benelux hubs | Medium term (2-4 years) |

| Military re-armament budgets (Ukraine war spill-over) | +1.30% | Poland, Germany, UK, Finland, Sweden | Long term (≥4 years) |

| Hydrogen-ready propulsion R&D consortia (Clean Aviation JU) | +0.90% | France, Germany, UK, Spain | Long term (≥4 years) |

| SESAR-led U-space integration accelerating eVTOL deployment across Europe | +0.70% | France, Germany, UK, Italy urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Green-Tax Incentives Reshape Fleet Economics

European governments have increased carbon levies on short-haul flights, prompting airlines to adopt fuel-efficient aircraft and higher SAF blends. France lifted its domestic flight surcharge to EUR 30 (USD 35.06) per passenger in 2024, while Germany’s revised ticket tax rewards operators that meet ICAO CO2 performance standards.[1]Financial Times, “Europe Raises Aviation Carbon Levies,” ft.com The Netherlands introduced a new per-flight charge at Amsterdam Schiphol, linked to aircraft noise and emissions, prompting KLM to accelerate deliveries of the A320neo. Airlines operating legacy B737-800 and A320ceo fleets now face direct operating-cost penalties that compress the payback periods of new aircraft by up to 3 years. Low-cost carriers, whose unit economics hinge on fuel efficiency, are first movers in this transition. Nordic policymakers plan to implement a carbon border adjustment for aviation by 2027, further shifting the cost equation in favor of next-generation aircraft.

Air-Traffic Recovery Exceeds Pre-Pandemic Baseline

Eurocontrol data show that European flight volumes reached 102% of 2019 levels by August 2024, led by leisure demand on Mediterranean routes. Low-cost carriers (LCCs) increased capacity by 18% in 2024, adding service to secondary airports in Spain, Portugal, and Greece. Legacy airlines realigned their networks toward premium leisure travel, offsetting a 15% shortfall in corporate travel. Cargo tonnage increased by 6% year over year, driven by e-commerce and pharmaceutical shipments. Yet congestion persists at high-density airports, and Eurocontrol projects that 20 hubs will run out of peak-hour slots by 2027, leading to a shift in growth toward off-peak operations or regional fields.

Surge in E-Commerce-Driven Freighter Conversions

Express parcels expanded 22% in 2024, spurring integrators to convert mid-life narrowbodies into freighters.[2]IATA, “Air Cargo and Pilot Outlook 2024,” iata.org DHL ordered 12 A321 passenger-to-freighter conversions, while Amazon Air added eight B737-800Fs to its European fleet. Conversion lead times have lengthened from 12 to 18 months as MRO shops prioritize higher-margin widebody work. Narrowbody freighters deliver the right balance of payload and frequency for sub-2,000-kilometer routes that define Europe’s overnight parcel network, and residual values on 15-year-old B737-800s have risen 20% as a result.

Military Re-Armament Budgets Sustain Long-Run Demand

Germany’s EUR 100 billion (USD 111.36 billion) defense fund allocates approximately 35% to aviation programs, including Eurofighter upgrades and F-35A procurement. Poland exercised options for 32 more F-35As in 2024, while Finland and Sweden aligned force structures with NATO interoperability standards. The UK, France, and Italy advance the Global Combat Air Programme (GCAP) toward a sixth-generation fighter entry by 2035. Helicopters also benefit; Leonardo delivered 18 AW149s to Poland in 2024. Although supply chains for avionics and composites remain tight, multiyear funding commitments provide sustained visibility for OEMs and tier-one suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long certification cycle for novel propulsion | -0.60% | Europe-wide | Long term (≥4 years) |

| Persistent pilot/engineer labour shortages | -0.50% | UK, Germany, Scandinavia, Southern Europe | Medium term (2-4 years) |

| Volatile SAF pricing | -0.40% | Markets with SAF mandates; France, Netherlands, Nordics | Short term (≤2 years) |

| ATC capacity bottlenecks at core hubs | -0.30% | Amsterdam, Frankfurt, London, Paris, Munich | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Long Certification Cycle Delays Novel Propulsion Deployment

EASA issued only draft rules for electric and hydrogen propulsion in 2024, leaving OEMs unable to file final type-certificate applications until at least 2026.[3]EASA, “Draft Certification Specifications for Electric Propulsion,” easa.europa.eu Heart Aerospace has postponed the ES-30's entry into service by two years due to evolving battery safety standards. ZeroAvia must run separate campaigns for 19- and 80-seat hydrogen retrofits, each spanning four years. Regulatory caution, shaped by lessons from the B737 MAX crisis, doubles the engineering workload for projects seeking dual FAA-EASA approval. Start-ups, therefore, face prolonged cash burn and dilution risk while awaiting certification milestones.

Labor Shortages Constrain Operational Expansion

IATA forecasts a deficit of 90,000 pilots and 120,000 technicians in Europe by 2030, and carriers already feel the pinch. Ryanair deferred 20 B737 MAX deliveries in 2024 because it could not staff additional crews despite offering higher starting salaries. Airbus cites MRO labor gaps as a reason for delayed A320neo shop visits. The UK-EU regulatory split compounds the problem by limiting license portability, and military forces lure experienced aviators back with cash bonuses. OEMs are experimenting with single-pilot cockpit concepts, but unions resist on safety grounds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Defense Pivot Lifts Military Aviation

Advanced Air Mobility (AAM) is forecasted to grow at a 9.45% CAGR as conditional eVTOL orders are converted into deliveries once EASA certification is achieved in 2026-2027. Commercial aviation accounted for 39.55% of the Europe aviation market in 2025, driven by 735 Airbus and 528 Boeing deliveries. However, widebody demand lags behind narrowbody growth as Asia-Pacific routes recover slowly.

Military aviation is experiencing a structural uptick due to higher NATO spending, with Germany and Poland expanding their F-35 orders, and Airbus delivering six A400M transports in 2024.[4]Airbus, “Global Orders and Deliveries 2024,” airbus.com Special mission aircraft, including ATR 72MP patrol variants, answer renewed surveillance needs on Europe’s eastern flank. General aviation is stabilizing after a pandemic-era boom, with Dassault’s Falcon line delivering 33 jets in 2024.

The AAM opportunity expands regional aviation capacity without requiring additional runway slots, though the lack of certified products hinders future revenue recognition. Commercial airlines are pursuing scope-clause relief to deploy 100-seat Embraer E2 jets on thin routes, as evidenced by 24 E2 deliveries in Europe in 2024. Helicopter demand splits between defense and civil rescue roles; Airbus supplied 25 H145Ms to Germany for special operations, while emergency medical services (EMS) operators extend contracts for fleet renewals. The Europe aviation market, therefore, balances mature commercial aircraft demand with burgeoning defense orders and an emerging eVTOL segment poised for exponential growth once certification hurdles are cleared.

By Propulsion Technology: Electric Gains Certification Momentum

Electric propulsion is expected to post the fastest gain, at a 10.38% CAGR, driven by improvements in battery density that make sub-500-kilometer routes commercially viable. Turbofan products maintained a 26.76% share in 2025, driven by 1,200 LEAP-powered deliveries worldwide, of which 35% served European operators. Pratt & Whitney’s GTF durability issues grounded about 60 aircraft in Europe, nudging airlines toward CFM alternatives. Turboprops benefited from regional route growth; ATR delivered 41 aircraft in 2024, of which 28 went to European carriers. Hybrid-electric demonstrations by Rolls-Royce and Airbus promise 30% fuel savings, with megawatt-scale ground tests underway.[5]Rolls-Royce, “Hybrid-Electric Demonstrator Updates,” rolls-royce.com

Battery-only eVTOL concepts dominate urban mobility prototypes, for instance, Vertical Aerospace’s eight-rotor VX4 emphasizes low noise to clear EASA limits. Turboshaft engines, primarily used in helicopters, remain steady, with Safran shipping 450 units in 2024. Turbojet use is confined to niche military trainers. Electric advances hinge on solid-state batteries that may lift energy density to 400 Wh/kg by 2028, unlocking regional ranges of up to 1,000 kilometers. Until then, hybrid architectures bridge fuel-burn cuts and range constraints.

By Power Source: SAF Mandates Drive Blend Adoption

Conventional fuel still dominates the market with a 46.88% market share, yet the European ReFuelEU regulation requires a 6% SAF blend by 2030. Solar-powered aircraft, though niche, are projected to grow at a 11.26% CAGR because defense customers value multi-month endurance. Hydrogen fuel-cell programs gained momentum when Germany’s H2FLY flew a 124-kilometer mission in 2024, demonstrating the technology's viability for commuter operations. Fuel-cell propulsion for the 40-seat D328eco is scheduled to enter service in 2028. Battery-powered designs are suitable for eVTOL missions of 20-50 kilometers. Vertical Aerospace is optimizing its architecture around EASA’s stricter 10-decibel noise standard. However, SAF supply lags demand, and Neste’s 2024 output covered less than 3% of jet-fuel consumption. Airlines hedge exposure through five-year offtake deals, but price caps are absent, keeping cost volatility high.

By Fit: Retrofit Wave Extends Asset Life

Linefit installations accounted for 53.26% of the market in 2025, as Airbus and Boeing shipped 1,263 aircraft globally. Retrofit is forecasted to grow at a 9.21% CAGR as operators defer capital expenditures. Lufthansa Technik’s A320 cabin upgrade package costs USD 2.5 million, a small fraction of the cost of a new A320neo, and delivers seat-density gains and enhanced connectivity. Winglet retrofits reduce fuel burn by 2%, with 120 European B737NGs expected to receive Split Scimitar kits in 2024. ADS-B Out mandates due in 2025 are pushing avionics modernization across legacy fleets, while passenger-to-freighter conversions are turning mid-life A321s into revenue-generating assets. MRO capacity is tightening, pushing heavy-check slots to 90 days and increasing shop-visit pricing, which further incentivizes airlines to plan refurbishments well in advance.

Geography Analysis

France anchored 36.71% of the Europe aviation market in 2025, leveraging Airbus’s Toulouse final assembly lines and Dassault’s Falcon jet production. The United Kingdom leads growth with an 8.88% CAGR forecast to 2031, underpinned by a GBP 975 million (USD 1.22 billion) Aerospace Technology Institute program that funds research into hydrogen, electric propulsion, and SAF. Rolls-Royce completed full-throttle hydrogen combustion tests on its Pearl 15 in November 2024, a prelude to flight trials in 2025.

Germany benefits from a EUR 100 billion (USD 111.36 billion) defense modernization plan that includes Eurofighter upgrades and the procurement of F-35A aircraft. Airbus’s Hamburg plant delivered 180 A320neos in 2024 to European and Middle Eastern carriers. Italy’s Leonardo assembled 15 F-35As at Cameri in 2024, positioning the site as Europe’s F-35 hub. Spain specializes in aerostructures, notably A350 fuselage sections at Getafe and turbofan components at ITP Aero. Poland, Sweden, and Finland fill the “Rest of Europe” growth bracket; Poland’s 32 additional F-35A orders and Sweden’s Gripen E upgrades sustain defense demand.

France maintains its lead through integrated civil-military production, while UK policy agility and Germany’s defense stimulus are reshaping the competitive landscape. Post-Brexit regulatory divergence imposes dual certification layers for UK-built aircraft, adding cost, though it also enables a more flexible domestic path that eVTOL developers find attractive. Airbus’s footprint spans France, Germany, and Spain, providing geographic risk diversification, whereas Boeing relies on US production and must navigate European regulatory requirements for each of its models.

Competitive Landscape

In the Europe aviation market, key suppliers such as Airbus SE, Dassault Aviation, Leonardo S.p.A., BAE Systems plc, and Thales Group hold substantial market share by leveraging integrated capabilities across aircraft platforms, avionics systems, and defense electronics. The Europe aviation market features a moderate level of concentration, with Airbus accounting for about 60% of regional commercial deliveries in 2024 and Boeing regaining share after the B737 MAX recertification. Airbus aims to raise A320neo rates to 75 per month by 2026 and maintains first-mover status in hydrogen through its ZEROe program. Boeing confronts supply-chain quality issues that led Ryanair to defer 20 MAX units in 2024. Leonardo, BAE Systems, and Dassault capitalize on expanded defense budgets, while Rolls-Royce differentiates with its IntelligentEngine digital twin initiative, adopted by 12 European airlines in 2024.

Start-ups Volocopter, Lilium, and Vertical Aerospace collectively raised more than USD 500 million in 2024 despite lacking certified products, underscoring investor confidence in the emerging urban air mobility segment. Skyports and other infrastructure developers are racing to build vertiports ahead of the 2026 entry of eVTOL services. Quantum-Systems and Parrot disrupt the defense UAS space with cost-effective reconnaissance drones; Germany ordered 100 Vector units in 2024 at a fraction of the price of legacy platforms.

Digitalization is a competitive lever. Airbus’s Skywise analytics suite cut unscheduled ground time by 15% for subscribed carriers in 2024. For instance, Safran leverages predictive maintenance across its turboshaft engines to support helicopter availability contracts. EASA’s stringent noise and emissions thresholds raise entry barriers, yet conditional approvals for eVTOL prototypes lower hurdles for agile start-ups. The result is a bifurcated landscape in which incumbents dominate high-capital commercial aircraft programs while new entrants carve niches in electric propulsion and urban mobility.

Europe Aviation Industry Leaders

Dassault Aviation

Airbus SE

Leonardo S.p.A.

BAE Systems plc

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Leonardo secured a EUR 1.2 billion (USD 1.39 billion) contract for 28 AW249 attack helicopters from the Italian MoD.

- October 2025: Germany announced a potential enhancement of its defense capabilities through the acquisition of 20 new Eurofighters. As part of the contract, Airbus will manufacture the multi-role combat aircraft at its final assembly facility in Manching, near Munich, Germany. The first aircraft is expected to be delivered to the German Air Force in 2031, with the final delivery planned for 2034.

- September 2025: The French Defence Procurement Agency (DGA) contracted Dassault Aviation to supply five Falcon 2000 LXS Albatros aircraft in September 2025. This procurement is part of the Avsimar program, which aims to deliver a total of twelve maritime patrol and intervention aircraft.

Europe Aviation Market Report Scope

The Europe aviation market encompasses the sales of fixed-wing and rotary-wing aircraft within the region's commercial, military, and general aviation sectors. It provides an analysis of air passenger traffic, aircraft orders and deliveries, defense expenditures, the introduction of new routes, and country-specific investments in the aviation industry.

The Europe aviation market is segmented by type, propulsion technology, power source, fit, and geography. By type, the market is segmented into commercial aviation, military aviation, general aviation, unmanned aerial systems, and advanced air mobility (AAM). By propulsion technology, the market is segmented into turboprop, turbofan, piston engine, turboshaft, turbojet, hybrid-electric, and electric. By power source, the market is segmented into conventional fuel, SAF-based, fuel cell, battery powered, and solar powered. By fit, the market is segmented into linefit and retrofit. The report also offers the market size and forecasts for five countries across the region. For each segment, the market sizing and projections were made based on value (USD).

By Type

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Missions | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters | |

| Unmanned Aerial Systems | Civil and Commercial |

| Defense and Government | |

| Advanced Air Mobility (AAM) | eVTOL |

| Urban Air Mobility (UAM) |

By Propulsion Technology

| Turboprop |

| Turbofan |

| Piston Engine |

| Turboshaft |

| Turbojet |

| Hybrid-Electric |

| Electric |

By Power Source

| Conventional Fuel |

| SAF-Based |

| Fuel Cell |

| Battery Powered |

| Solar Powered |

By Fit

| Linefit |

| Retrofit |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Type | Commercial Aviation | Narrowbody |

| Widebody | ||

| Regional Jets | ||

| Military Aviation | Combat | |

| Transport | ||

| Special Missions | ||

| Helicopters | ||

| General Aviation | Business Jets | |

| Commercial Helicopters | ||

| Unmanned Aerial Systems | Civil and Commercial | |

| Defense and Government | ||

| Advanced Air Mobility (AAM) | eVTOL | |

| Urban Air Mobility (UAM) | ||

| By Propulsion Technology | Turboprop | |

| Turbofan | ||

| Piston Engine | ||

| Turboshaft | ||

| Turbojet | ||

| Hybrid-Electric | ||

| Electric | ||

| By Power Source | Conventional Fuel | |

| SAF-Based | ||

| Fuel Cell | ||

| Battery Powered | ||

| Solar Powered | ||

| By Fit | Linefit | |

| Retrofit | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe aviation market in 2026?

The Europe aviation market size is USD 98.50 billion in 2026 and is set to reach USD 145.54 billion by 2031 at an 8.12% CAGR.

Which segment is growing fastest?

Advanced air mobility leads with a 9.45% CAGR as eVTOL developers move toward EASA certification in 2026-2027.

Why is defense spending important for European aviation?

NATO realignment after the Ukraine conflict triggered sizable fighter and helicopter orders, ensuring long-term demand visibility for manufacturers.

How do carbon taxes influence fleet renewal?

Higher levies in France, Germany, and the Netherlands raise operating costs on older aircraft, shortening payback periods for fuel-efficient models and accelerating retirements.

What challenges slow hydrogen and electric aircraft?

EASA’s protracted certification timeline and limited refueling infrastructure delay commercial deployment, forcing OEMs to absorb R&D costs longer.

Where is SAF supply relative to demand?

Total European SAF output covered less than 3% of jet-fuel needs in 2024, keeping prices 150%-250% above conventional fuel and pressuring airline margins.

Page last updated on: