Yellow Pea Protein Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

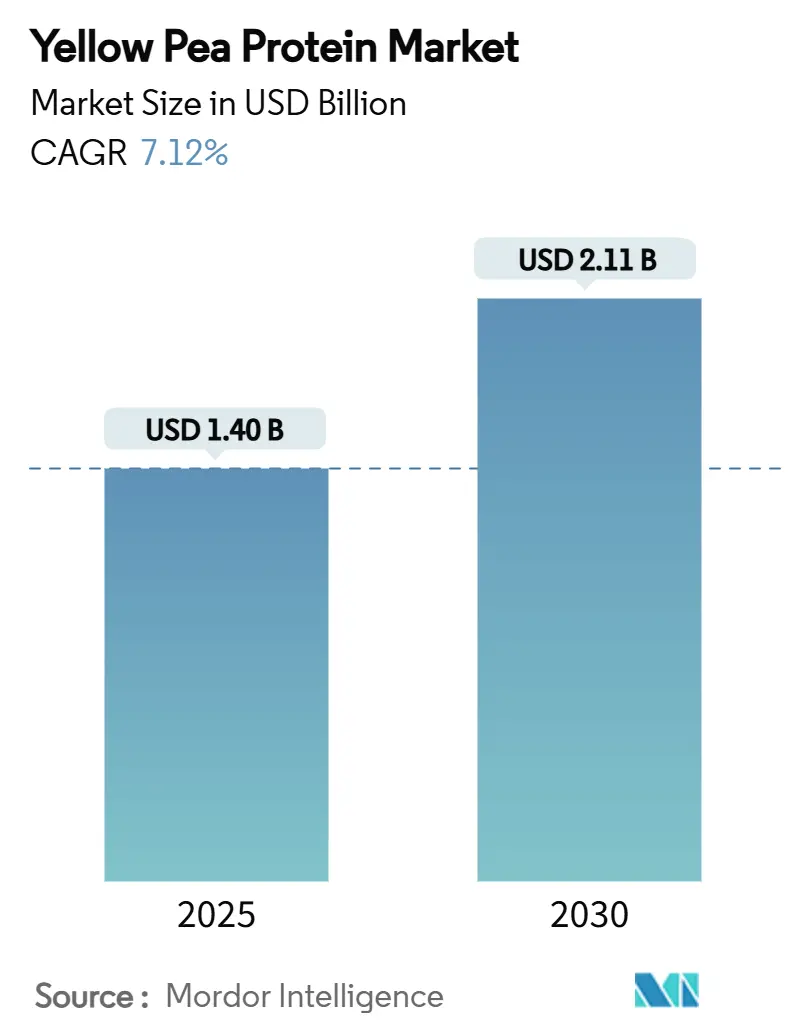

| Market Size (2025) | USD 1.40 Billion |

| Market Size (2030) | USD 2.11 Billion |

| Growth Rate (2025 - 2030) | 7.12% CAGR |

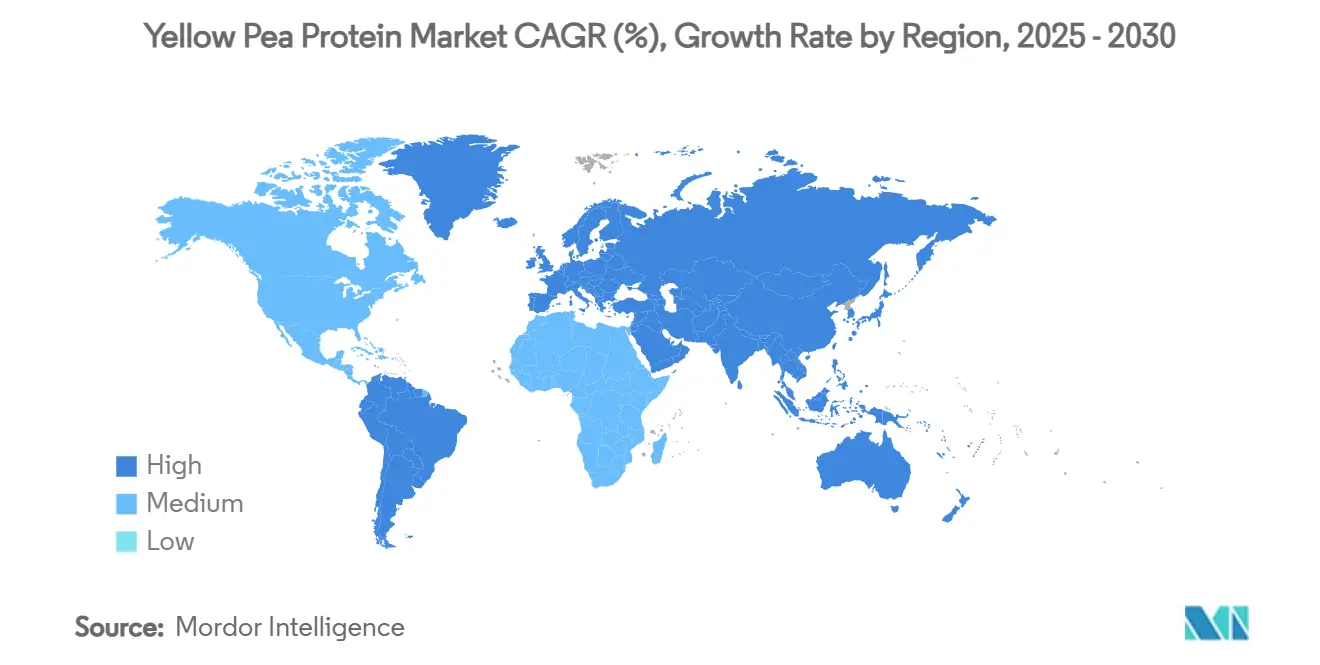

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

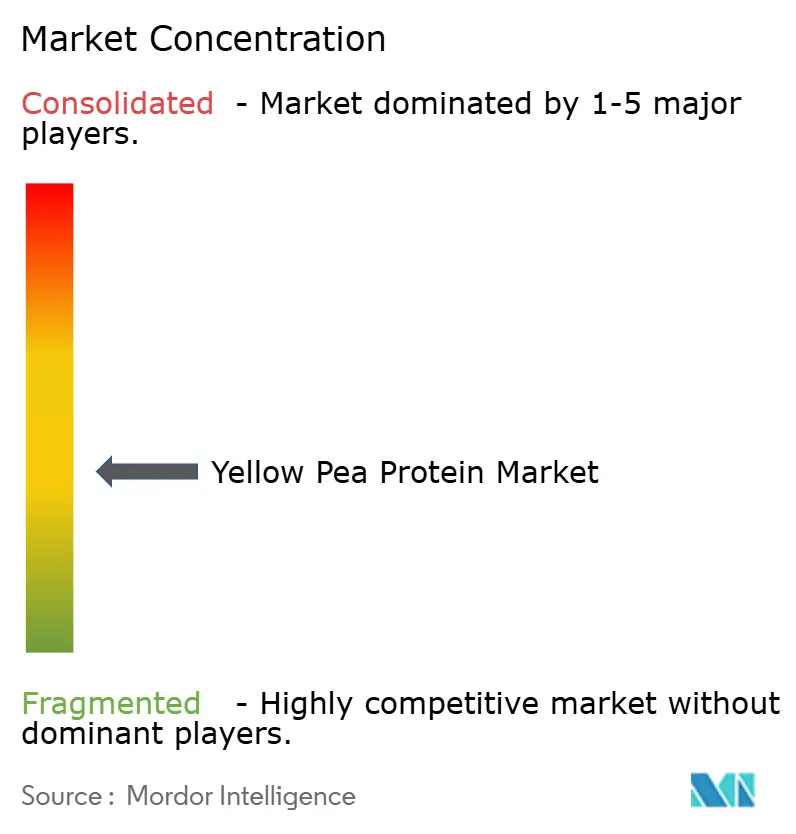

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Yellow Pea Protein Market Analysis by Mordor Intelligence

The yellow pea protein market size stands at USD 1.40 billion in 2025 and is projected to reach USD 2.11 billion by 2030, reflecting a 7.12% CAGR over the forecast period. Robust consumer interest in plant-based diets, regulatory clarity that now recognises plant proteins in “healthy” claims, and processing breakthroughs that neutralise beany off-flavours are together steering demand beyond niche vegan products into mainstream food manufacturing. Supply chain investments exceeding USD 1 billion in North America alone have reduced lead times and stabilised ingredient availability, allowing brand owners to focus on formulation efficiency rather than basic market education. Meanwhile, food-security programmes across Asia-Pacific have made domestic alternative proteins a strategic priority, accelerating technology transfers and public-private partnerships. Overall, the pea protein market is moving from an early adoption phase dominated by product launches to a scale-up phase defined by throughput optimisation, cost discipline and geographic diversification.

Key Report Takeaways

- By product type, isolates held the leading 45.01% of the yellow pea protein market share in 2024 and are forecast to grow at 6.50% CAGR to 2030, while textured pea protein is poised for the fastest 9.01% CAGR over the same horizon.

- By form, dry-processed ingredients accounted for 81.20% of the yellow pea protein market share in 2024 and are expanding at 6.70% CAGR, whereas wet-processed variants, though smaller, are projected to climb at an 8.34% CAGR.

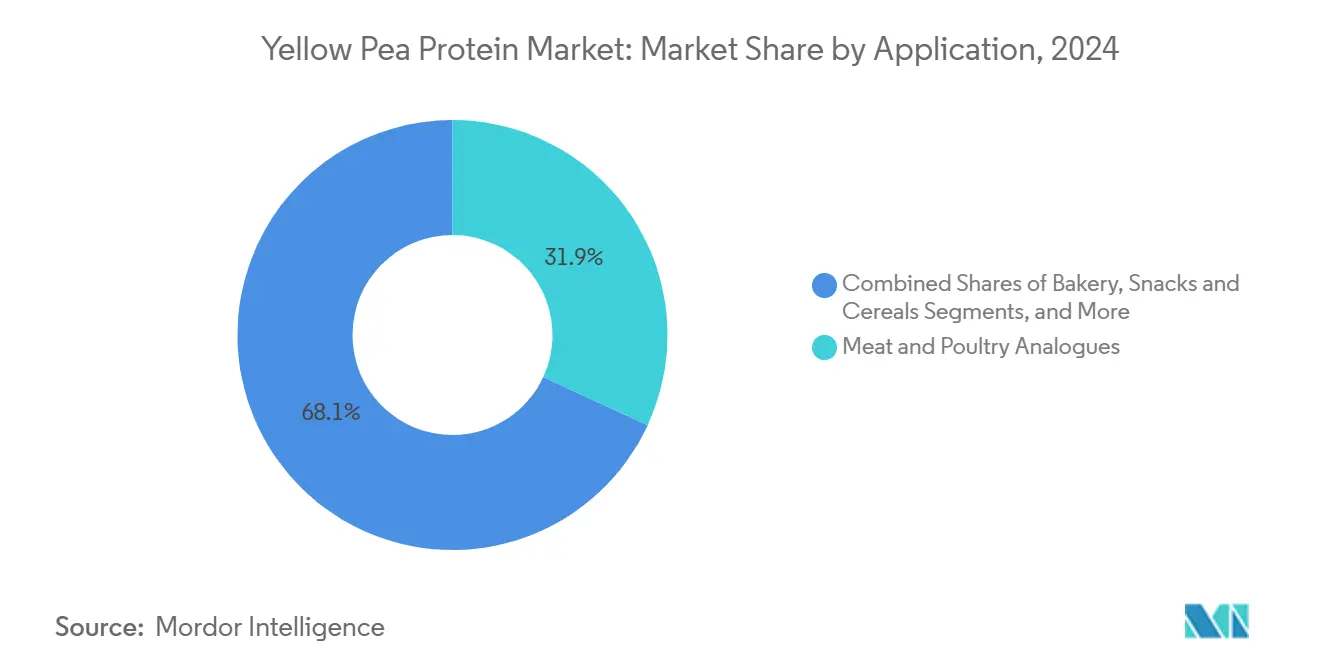

- By application, meat and poultry analogues captured 31.89% of total share in 2024, yet clinical and infant nutrition is positioned to advance at the highest 8.78% CAGR through 2030.

- By geography, North America dominated with 40.23% market share in 2024; Asia-Pacific represents the fastest-growing region, registering a 9.20% CAGR for 2025-2030.

Global Yellow Pea Protein Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for plant-based proteins in functional foods and beverages | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growth of vegan and flexitarian populations worldwide | +1.2% | Global, led by developed markets | Long term (≥ 4 years) |

| Processing advances improving taste, solubility and texture | +1.5% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Capacity expansions by North-American and Europe pulse processors | +1.1% | North America and Europe | Medium term (2-4 years) |

| Pet-food manufacturers adopting hypoallergenic pea proteins | +0.7% | Global, early adoption in North America | Medium term (2-4 years) |

| Government incentives for domestic pulse-processing clusters | +0.9% | North America, Europe, selective APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for plant-based proteins in functional foods and beverages

Manufacturers are increasingly adopting pea protein, not just for traditional meat alternatives, but also to enhance beverages, snacks, and bakery items. This shift marks a significant evolution in the market, moving from niche plant-based meat substitutes to a broader focus on protein fortification across various food categories. Recent product launches underscore this trend, such as Burcon NutraScience Corporation's Peazazz C™ ingredient, tailored for ready-to-drink beverages, boasting improved solubility and a grit-free texture. Additionally, the FDA's revised "healthy" food definition, set to take effect in February 2025, bolsters this movement by prioritizing plant-based protein content in food formulations. This regulatory shift not only boosts demand for pea protein across diverse food categories but also broadens its market appeal beyond just plant-based products. The functional foods sector is reaping the rewards of pea protein's neutral flavor and superior processing traits, allowing manufacturers to meet protein targets without sacrificing taste or texture in products aimed at mainstream consumers.

Growth of vegan and flexitarian populations worldwide

As demographic shifts lean towards plant-forward diets, demand for pea protein ingredients surges, driven predominantly by flexitarian consumers rather than staunch vegans. This shift underscores a growing health consciousness and environmental awareness, broadening the market's reach beyond conventional plant-based food categories. Institutional backing, highlighted by the 2025 Dietary Guidelines Advisory Committee's Scientific Report, underscores the benefits of plant-based diets, bolstering this demographic trend. In the Asia-Pacific, alternative protein adoption is witnessing robust growth, fueled by government-backed food security initiatives that bolster consumer acceptance of plant-based proteins. Flexitarian consumers, who seamlessly weave plant proteins into their diets, present a more lucrative avenue for market expansion than their vegan counterparts. This is because they don't necessitate a complete overhaul of their dietary choices. The integration of pea protein ingredients into familiar food experiences, rather than as replacements, accelerates market penetration, paving the way for broader acceptance in mainstream food manufacturing.

Processing advances improving taste, solubility and texture

Innovations in extracting and modifying pea protein have overcome past hurdles, notably the undesirable beany flavor and limited solubility that restricted its versatility. Research highlights that dry fractionation methods achieve a solubility rate of 44.64%, outpacing wet extraction's 12.09%, all while preserving native protein structures for better functionality Authorea. Techniques like electrospinning, tailored for meat analogs, and refined heat treatment protocols, empower manufacturers to craft products mimicking the texture and sensory profile of animal proteins Frontiers in Bioengineering and Biotechnology. A notable partnership between DSM-Firmenich and Meala FoodTech is pushing the envelope, creating thermostable textured pea proteins. These proteins not only retain their functionality during diverse cooking methods but are also marketed simply as "pea protein" on labels. Such advancements in processing are paving the way for pea proteins to infiltrate markets once dominated by animal counterparts, broadening opportunities beyond the conventional plant-based realm. For processors embracing these cutting-edge extraction and modification techniques, the benefits are clear: a distinct edge in a saturated market.

Capacity expansions by North-American and EU pulse processors

Global investments exceeding USD 1 billion in strategic capacity underscore the industry's confidence in the robust demand for pea protein. Major processors are proactively fortifying their supply chains in anticipation of market growth. Roquette has unveiled the world's largest pea protein processing plant in Manitoba, with a hefty USD 600 million investment, boasting an annual processing capacity of 125,000 metric tons. Meanwhile, Louis Dreyfus Company is set to bolster Canada's pulse-growing heartland with a new facility in Saskatchewan, slated to commence operations by late 2025. This strategic move capitalizes on the region's proximity to raw material sources, ensuring cost advantages. Cargill, through a USD 75 million stake in PURIS, has successfully doubled the production capacity at its Dawson, Minnesota facility, a move that directly benefits over 400 U.S. farmers in its pea supply network. These burgeoning capacity additions are not just numbers; they're pivotal in establishing regional processing hubs. Such hubs are instrumental in slashing transportation costs and bolstering supply chain resilience for food manufacturers. With a pronounced concentration of processing investments in North America, the region is poised to uphold its market leadership, catering to the surging global appetite for pea protein ingredients.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Off-flavour and mouthfeel limitations vs animal proteins | -1.4% | Global, particularly in premium applications | Short term (≤ 2 years) |

| Yellow-pea price volatility and crop-yield risk | -1.1% | North America and Europe production regions | Medium term (2-4 years) |

| US-China anti-dumping duties driving input cost spikes | -0.8% | Global, with concentration in North America | Short term (≤ 2 years) |

| Wet-fractionation bottlenecks lengthening lead times | -0.6% | Global processing capacity constraints | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Off-flavor and mouthfeel limitations vs animal proteins

Despite notable advancements in processing, sensory challenges still hinder the adoption of pea protein in premium applications, where taste and texture play pivotal roles in consumer acceptance. Research highlights that while various modification techniques can boost pea protein's functionality, the persistent beany aftertaste and subpar mouthfeel—especially when juxtaposed with animal proteins—pose formidable barriers to market growth. This limitation is evident in sports nutrition, where studies reveal that pea protein lacks the unique anabolic properties of whey protein, diminishing its allure for performance-driven consumers. The sensory disparity becomes even more evident in high-protein applications, where off-flavors are amplified, and processing tweaks fall short of matching animal protein standards. To meet acceptable sensory profiles, premium food manufacturers frequently resort to extensive flavor masking or blending pea protein with others, complicating formulations and driving up costs. This challenge is especially pronounced in categories like protein bars, ready-to-drink beverages, and dairy alternatives, where consumers have set taste expectations. As a result, pea protein struggles to secure premium pricing in these segments.

Yellow-pea price volatility and crop-yield risk

Fluctuations in agricultural commodity prices introduce uncertainties in the supply chain, hampering long-term planning and investments in pea protein processing. Canadian pea prices are set to drop to USD 400 per tonne in 2025, down from USD 455 in 2023-24, a shift influenced by global supply dynamics and trade policies. The European Union[1]European Commission, “EU Pea Supply Outlook 2025,” ec.europa.eu anticipates a 6% dip in pulse production for 2025, mainly due to a 19% cut in cultivated area, even with better yields. This tightens supply and could lead to price volatility. In the U.S., dry pea production fell by 6% to 16.7 million hundredweight in 2024, with yields down by 149 pounds per acre from the prior season, highlighting the crop's sensitivity to weather, according to the United States Department of Agriculture[2]United States Department of Agriculture, "Crop Production 2024 Summary", fas.usda.gov. Such weather-induced yield fluctuations pose significant challenges for processors with fixed-capacity investments; raw material shortages can lead to underutilized, costly equipment. These agricultural risks compel pea protein manufacturers to hold larger inventories and seek alternative sourcing, elevating working capital needs and complicating operations, which in turn limits market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Isolates Lead Despite Textured Growth

In 2024, isolates command a 45.01% market share, showcasing their adaptability in food applications and boasting a protein content of 80-90%. Meanwhile, textured pea protein stands out as the fastest-growing segment, charting a 9.01% CAGR through 2030. The established manufacturing processes and broad application compatibility make the isolate segment the go-to choice for protein fortification. It's favored in beverages, sports nutrition, and clinical applications, all of which prioritize a high protein concentration and a neutral flavor profile. Textured pea protein's rapid ascent is driven by its applications in meat analogs. Here, processing innovations have crafted fiber-like structures that closely resemble animal protein textures. Concentrate products, positioned in the middle, enjoy moderate growth. They present a cost-effective alternative to isolates, delivering adequate protein content for a variety of food applications.

Hydrolyzed pea protein carves out a niche, targeting clinical and infant nutrition. In these areas, pre-digested proteins shine due to their enhanced bioavailability and lower allergenic potential. Recent evaluations by the European Food Safety Authority on protein hydrolysates for infant formulas, though centered on dairy, set regulatory benchmarks. These could pave the way for pea protein hydrolysates in specialized nutrition sectors. Advances in processing technology, especially dry heat pretreatment for textured applications, have unlocked new potentials. They allow for optimal protein denaturation at 120°C, all while preserving functional properties, thus birthing opportunities for premium textured products. The segmentation by product type underscores a maturing market: isolates dominate established applications, while textured variants are seizing the momentum in the burgeoning plant-based meat sector.

By Form: Dry Processing Dominance with Wet Growth

In 2024, dry form pea protein commands an 81.20% market share, leveraging its cost advantages and shelf stability. Meanwhile, wet form processing is on an upward trajectory, boasting an 8.34% CAGR growth through 2030, thanks to technological advancements that rectify past challenges. Compared to wet extraction, dry fractionation methods not only achieve superior solubility rates but also preserve native protein structures, making them the preferred choice for high-functionality food applications, as highlighted by Legume Science. Beyond technical prowess, the economic edge of dry processing is evident: air classification methods demand a lower capital investment and consume less energy than their wet fractionation counterparts. The growth of wet processing is driven by technological strides that enhance protein yield and functionality, all while being environmentally conscious through water recycling and waste reduction.

Recent findings underscore the advantages of dry fractionated pea protein: it boasts enhanced mechanical strength and elasticity in gel applications. This makes it a prime candidate for meat analog formulations, where texture is paramount, as noted by Authorea. Yet, wet fractionation faces hurdles: its inherent processing complexities and extended lead times curtail capacity utilization, stunting growth in this arena. On the flip side, wet processing shines in achieving elevated protein purity and excising anti-nutritional factors. This positions it favorably in premium markets, where such attributes command a price premium. The segmentation of forms underscores a balancing act: weighing cost efficiency against functional performance. As the market matures, there's a discernible tilt towards technologies that harmonize both aspects.

By Application: Meat Analogues Lead Clinical Nutrition Growth

In 2024, meat and poultry analogues command a 31.89% market share, harnessing pea protein's prowess in crafting fibrous textures akin to animal proteins. Meanwhile, clinical and infant nutrition applications are on a rapid ascent, boasting an 8.78% CAGR projected through 2030. The meat analog segment thrives on the growing consumer acceptance of plant-based alternatives, bolstered by technological strides in texture creation. Notably, electrospinning techniques are at the forefront, crafting structures that closely resemble meat fibers. The surge in clinical nutrition can be attributed to pea protein's hypoallergenic nature and its comprehensive amino acid profile. These attributes render it ideal for specialized diets, especially where conventional protein sources might trigger adverse reactions. However, sports nutrition faces hurdles; research suggests that pea protein doesn't offer the distinct anabolic benefits of whey protein, curbing its growth in performance-centric markets.

In the realm of dairy and frozen dessert alternatives, pea protein's neutral flavor and superior processing traits shine. These attributes empower manufacturers to craft palatable products without heavy reliance on flavor masking. The bakery, snacks, and cereals sectors witness steady growth, with pea protein enhancing protein content without major alterations to product traits. Beverage innovations, spanning ready-to-drink items to concentrates, spotlight advancements in solubility and texture. A prime example is Burcon's Peazazz C™, tailored specifically for liquid applications. Meanwhile, the pet food sector is witnessing a budding expansion. Manufacturers are increasingly turning to hypoallergenic pea proteins, catering to specialized pet nutrition, especially for animals with food sensitivities, as highlighted by Pet Food Processing. This broad spectrum of applications underscores pea protein's adaptability, emphasizing the need for customized processing techniques to meet diverse end-use demands.

Geography Analysis

In 2024, North America commands a dominant 40.23% share of the market, leveraging its well-established pulse crop infrastructure, a favorable regulatory landscape, and strategic capacity investments. These factors collectively position the region as a pivotal global hub for pea protein. The region's supremacy is bolstered by integrated supply chains that seamlessly link prairie pulse farmers to processing facilities. This integration not only offers cost advantages but also ensures supply security for manufacturers. Recent trade policy shifts, notably the U.S. imposing anti-dumping duties on Chinese pea protein imports, fortify the competitive stance of North American producers, safeguarding their domestic market share, according to Federal Register[3]Federal Register, “Certain Pea Protein from China: Duty Orders,” federalregister.gov. With an eye on the future, Canada's Protein Industries Cluster initiative, buoyed by government backing and collaboration with Innovation, Science and Economic Development Canada, aims for a lofty target of USD 25 billion in annual plant-based food sales by 2035. Meanwhile, the U.S. reaps benefits from USDA-led research endeavors, such as the Pulse Crop Health Initiative, complemented by a substantial nearly USD 9 million research funding for FY 2024, all aimed at bolstering the long-term development of the supply chain.

Asia-Pacific stands out as the region with the most rapid growth, boasting a 9.20% CAGR projected through 2030. This surge is fueled by initiatives centered on food security, governmental backing for alternative proteins, and a growing consumer embrace of plant-based foods. India's alternative protein sector is on an impressive upward trajectory, with projections indicating a leap from USD 278 million to USD 864 million by 2030. Local innovators, such as Blue Tribe Foods and Seaspire, are at the forefront, creatively harnessing pea protein ingredients. Leading the charge in regional research on alternative proteins, China and Singapore are zeroing in on climate resilience and food security, underscoring the strategic importance of plant-based proteins. While the region grapples with challenges like elevated costs from ingredient imports and taxation policies, there's optimism. Developing local production could not only alleviate these challenges but also tap into the burgeoning domestic demand. The growth narrative in Asia-Pacific is further accentuated by demographic shifts favoring health-conscious consumption and proactive government policies championing food system sustainability, setting the stage for a robust expansion of the pea protein market.

Europe is witnessing steady growth, bolstered by regulatory measures that champion domestic protein production and aim to curtail reliance on imports. This is especially pertinent for soy-based ingredients, which carry notable environmental repercussions. However, the continent isn't without its hurdles. A 6% dip in pulse output in 2025, attributed to a shrinking cultivated area, has led to a tightening supply. This scenario could spur heightened investments in processing, as noted by the European Commission. In a bid to counteract import dependency, European firms like Wide Open Agriculture are ramping up their lupin protein production, showcasing a strategic pivot beyond the conventional pea protein. The European landscape is further enriched by well-established regulatory frameworks governing novel foods and a robust consumer inclination towards plant-based alternatives. This confluence of factors bodes well for sustained growth in pea protein applications across diverse food categories.

Competitive Landscape

The yellow pea protein market is moderately fragmented, posting a concentration score of 4 on a 10-point scale as no single player exceeds a 15% global revenue share. Roquette, Cosucra, Ingredion, and collectively account for significant shares, leaving ample headroom for mid-tier specialists and ingredient start-ups. Competitive dynamics revolve around vertical integration: majors secure everything from seed genetics to finished isolates, thereby lowering raw-material risk and enhancing traceability certifications sought by multinational food customers. Smaller firms carve out niches via patented extraction or texturisation techniques, creating high-margin grades for clinical nutrition or premium sports applications.

Strategic moves centre on capacity expansion, M&A, and technical partnerships. Louis Dreyfus Company’s Saskatchewan project marks its first foray into pulse protein, signalling traditional commodity houses’ intent to diversify beyond grains. Simply Good Foods’ USD 280 million takeover of OWYN underscores downstream consolidation into branded ready-to-drink categories, showing how control over finished-goods channels can lock in ingredient demand.

Innovation pipelines are notably aligned with ESG objectives. Proprietary dry-fractionation systems claim up to 40% lower water use than wet methods, while carbon-labelled SKUs command shelf-space in European retailers adhering to Scope 3 emissions reporting. Certification wars have emerged around non-GMO, organic and Upcycled Food labels. Players that bundle multiple claims within a single specification sheet enjoy a pricing premium, particularly in export-driven geographies where regulatory harmonisation is advancing.

Yellow Pea Protein Industry Leaders

-

Roquette Freres

-

The Scoular Company

-

Ingredion Incorporated

-

COSUCRA Groupe Warcoing S.A.

-

Puris

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: plant protein specialist Burcon made a significant advancement by successfully completing the first commercial production run of its Peazazz C pea protein ingredient at its newly commissioned facility in Galesburg, Illinois, USA.

- March 2025: PIP Lethbridge Inc., a yellow pea protein producer and researcher based in Lethbridge, received a USD 2.3 million grant from Results Driven Agriculture Research (RDAR). The funding was allocated to help the company enhance its innovation capabilities by scaling up its processes and implementing new technology that provides real-time processing data.

- December 2024: Ingredion Incorporated partnered with Lantmännen, Northern Europe’s leading agricultural cooperative, to expand their presence in the plant-based protein market. As part of the collaboration, Lantmännen committed to investing over USD 117.12 million in a state-of-the-art production facility in Sweden, scheduled to open in 2027, which will specialize in processing yellow peas into high-quality protein isolates.

Global Yellow Pea Protein Market Report Scope

| Isolate |

| Concentrate |

| Textured Pea Protein (TPP) |

| Hydrolyzed Pea Protein |

| Dry |

| Wet |

| Meat and Poultry Analogues |

| Dairy and Frozen Dessert Alternatives |

| Sports Nutrition Powders and Bars |

| Bakery, Snacks and Cereals |

| Beverages (RTD and Concentrates) |

| Clinical and Infant Nutrition |

| Pet Food |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Product Type | Isolate | |

| Concentrate | ||

| Textured Pea Protein (TPP) | ||

| Hydrolyzed Pea Protein | ||

| By Form | Dry | |

| Wet | ||

| By Application | Meat and Poultry Analogues | |

| Dairy and Frozen Dessert Alternatives | ||

| Sports Nutrition Powders and Bars | ||

| Bakery, Snacks and Cereals | ||

| Beverages (RTD and Concentrates) | ||

| Clinical and Infant Nutrition | ||

| Pet Food | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the yellow pea protein market, and how fast is it growing?

The yellow pea protein market size is USD 1.40 billion in 2025 and is projected to register a 7.12% CAGR to reach USD 2.11 billion by 2030.

Which region leads pea protein demand today?

North America holds the largest 40.23% revenue share thanks to integrated supply chains and recent processing capacity additions.

What application segment is expanding fastest?

Clinical and infant nutrition is forecast to grow at 8.78% CAGR through 2030 because pea protein’s hypoallergenic profile suits specialized dietary needs.

What technology has most improved pea protein’s sensory performance?

Dry fractionation paired with electrospinning and enzymatic de-amidation has significantly lifted solubility and texture, closing the gap with dairy and meat proteins.

Page last updated on: