Yellow Fever Treatment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

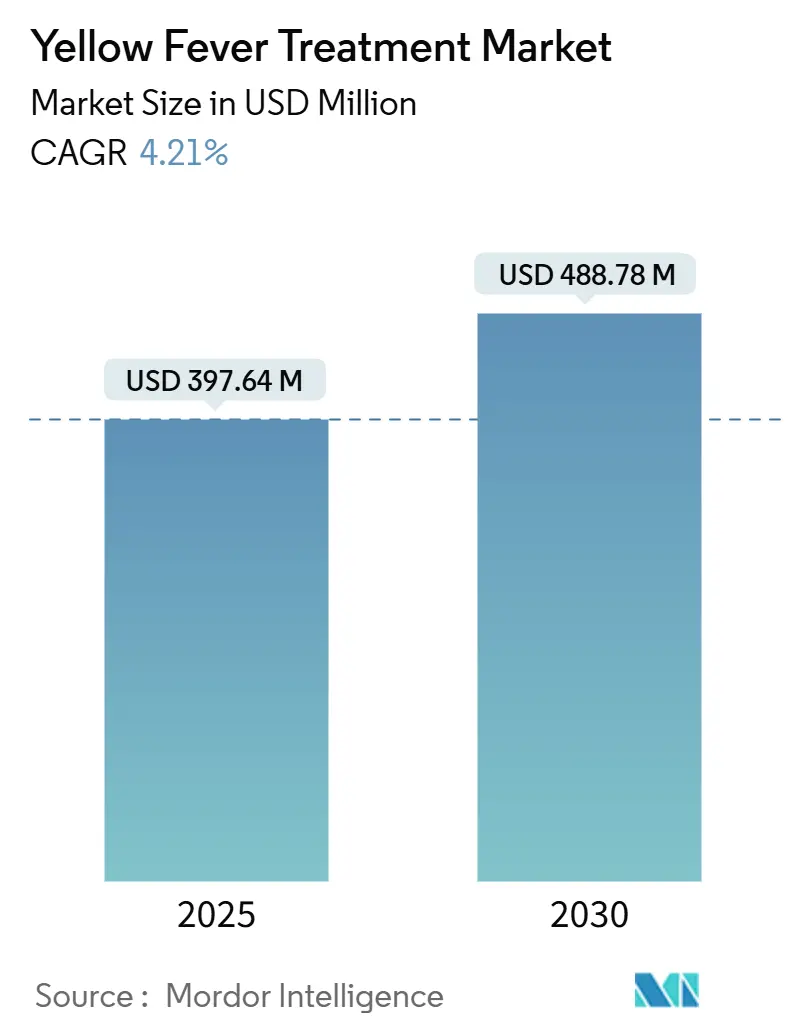

| Market Size (2025) | USD 397.64 Million |

| Market Size (2030) | USD 488.78 Million |

| Growth Rate (2025 - 2030) | 4.21% CAGR |

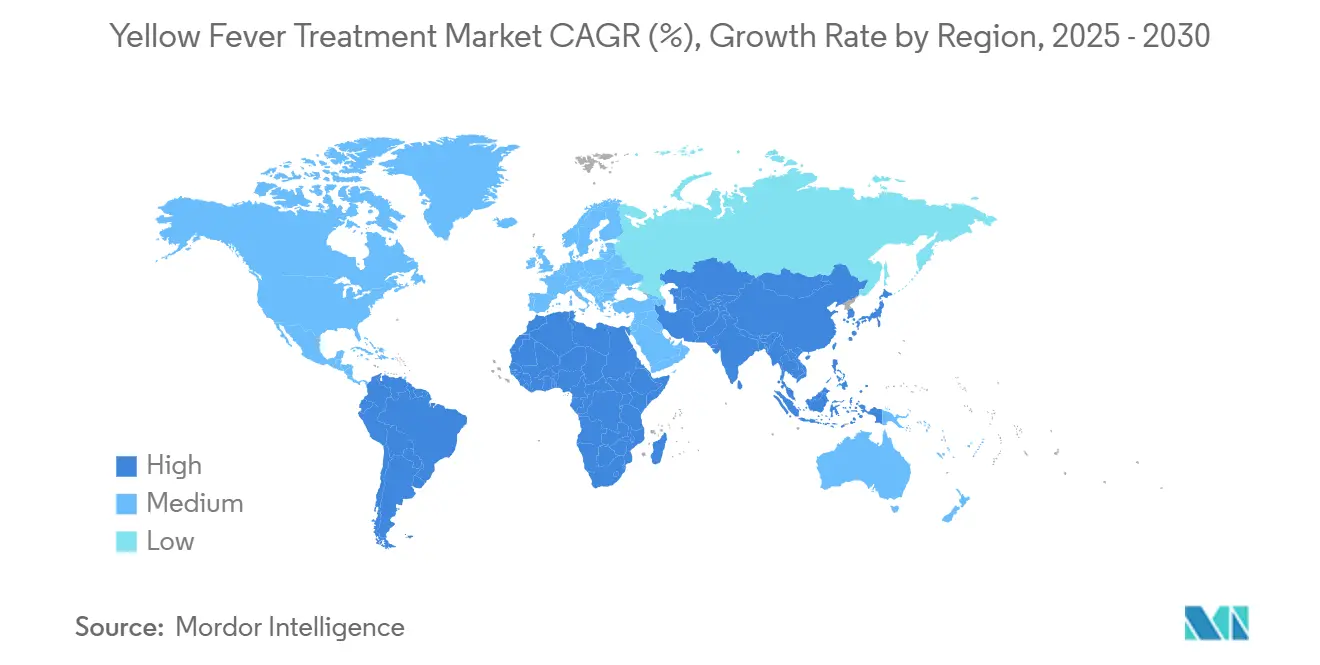

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

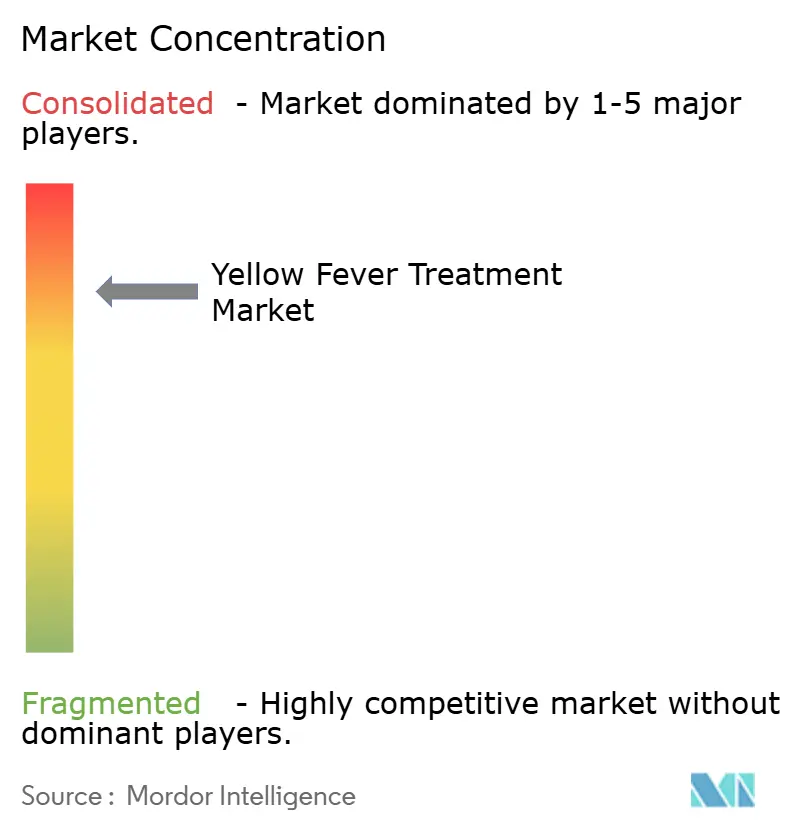

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Yellow Fever Treatment Market Analysis by Mordor Intelligence

The yellow fever treatment market size reached USD 397.64 million in 2025 and is projected to advance to USD 488.78 million by 2030, registering a 4.21% CAGR over the forecast period. This moderate pace conceals a pressing imbalance between rising vaccination demand in outbreak-prone regions and the limited global manufacturing base, which continues to strain health-security frameworks. The market benefits from the World Health Organization’s Eliminate Yellow Fever Epidemics (EYE) strategy, which has accelerated mass immunization funding commitments; however, production capacity remains concentrated in a handful of facilities.[1]World Health Organization, “Disease Outbreak News; Yellow fever in the Region of the Americas,” WHO.INT Persistent climate change, rapid urbanization, and a rebound in international travel have broadened the at-risk population and reshaped procurement priorities. Manufacturers are responding with thermostable formulations, mRNA-based candidates, and fractional-dose clinical protocols that promise greater agility during supply shocks. As these innovations mature, stakeholders anticipate a structural realignment that favors more regionally dispersed production hubs and diversified delivery channels, ultimately supporting a more resilient yellow fever treatment market.

Key Report Takeaways

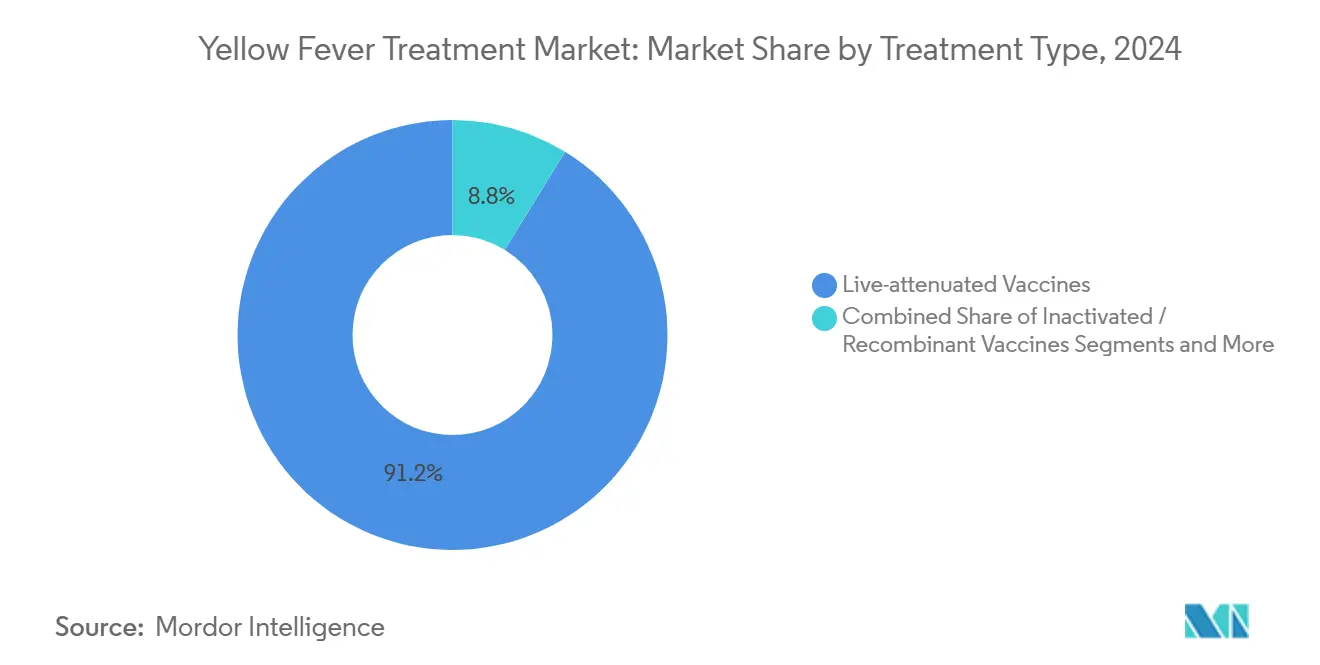

- By treatment type, live-attenuated vaccines accounted for 91.23% of the yellow fever treatment market share in 2024, while inactivated and recombinant alternatives are expected to expand at an 8.26% CAGR through 2030.

- By route of administration, subcutaneous injection held 90.57% share of the yellow fever treatment market size in 2024. In contrast, intradermal jet injection is projected to advance at a 7.35% CAGR during the same period.

- By distribution channel, government procurement agencies accounted for 68.92% of the yellow fever treatment market share in 2024; however, retail and online pharmacies are forecasted to grow at an 8.97% CAGR through 2030.

- By age group, adults (16-60 years) generated 61.38% of demand in 2024, while the geriatric cohort is projected to advance at a 7.34% CAGR through 2030.

- By geography, the Middle East and Africa captured 38.41% of 2024 revenue, whereas Asia-Pacific is the fastest-growing region with a 6.68% CAGR through 2030.

Global Yellow Fever Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanisation-Driven Mosquito Habitat Expansion | +0.6% | Global, concentrated in Sub-Saharan Africa and South America | Medium term (2-4 years) |

| Intensifying International Travel To Endemic Regions | +0.8% | Global, with spillover from endemic to non-endemic regions | Short term (≤ 2 years) |

| WHO's EYE Strategy Vaccine Stockpile Funding | +0.5% | Africa and South America, with GAVI-eligible countries prioritized | Medium term (2-4 years) |

| Advances In Single-Dose Thermostable Vaccines | +0.6% | Global, particularly beneficial for remote endemic areas | Long term (≥ 4 years) |

| mRNA-Based Multivalent Flavivirus Pipeline Vaccines | +0.5% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Climate Change Expanding Mosquito Range Into Temperate Regions | +0.5% | Asia-Pacific, Europe, and North America expansion zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urbanization-Driven Mosquito Habitat Expansion

Quick urban build-outs in endemic countries create breeding grounds for Aedes aegypti, shifting transmission from sylvatic to urban settings. Colombia’s 2025 outbreak—with 114 lab-confirmed cases and a 42.9% fatality rate, centered in Tolima and Putumayo—underscored surveillance blind spots where urban reservoirs evolve faster than public health monitoring systems.[2]Pan American Health Organization, “Yellow Fever: How three monkey deaths sparked a critical health alert in Colombia,” PAHO.ORG Informal water storage, construction debris, and inadequate waste disposal sustain year-round high densities of larvae. Such conditions shorten response windows, compelling national health agencies to pivot from reactive ring vaccination toward broad, city-wide immunization campaigns. Demand therefore shifts toward larger block procurements through government channels, reinforcing the dominance of the yellow fever treatment market while magnifying supply tension.

Intensifying International Travel To Endemic Regions

Global travel rebounded sharply after pandemic restrictions, expanding vaccination demand beyond expatriate professionals to leisure tourists and business travelers. The CDC logged more yellow fever alerts across Brazil, Bolivia, Colombia, and Peru in 2024 than in any year on record.[3]Centers for Disease Control and Prevention, “Yellow Fever Vaccine Information for Healthcare Providers,” CDC.GOV In 2024, the WHO updated the International Certificate of Vaccination requirements, adding Djibouti, the Philippines, and Qatar, while removing several lower-risk states, illustrating the WHO's dynamic risk mapping. Heightened demand has outpaced stockpile allocations at many travel medicine clinics, creating a gap for private-sector distribution networks and alternative vaccine platforms that could relieve pressure on government inventories.

WHO’s EYE Strategy Vaccine Stockpile Funding

The EYE initiative secured fresh Gavi financing under its 2026-2030 strategy, aiming to protect over 1 billion people while addressing production bottlenecks. Between 2017 and 2024, emergency stockpiles supplied 80 million doses for 77 outbreaks, yet reserves of 6 million doses remain insufficient for parallel multi-country incidents. Brazil’s Bio-Manguinhos expansion, underwritten through a Gavi agreement, exemplifies a shift towards regional capacity that reduces reliance on European manufacturers and bolsters local supply resilience. Success, however, still hinges on attaining 95% vaccination coverage in remote counties where campaign logistics remain complex.

Advances In Single-Dose Thermostable Vaccines

A 2025 study demonstrated that new thermostable formulations retain potency at higher temperatures, which is critical for regions where electricity and cold-chain infrastructure remain limited. Single-dose vials simplify field deployment by community health workers who rely on mobile fridges or passive cooling. The same technology supports fractional dosing practices, which, in Kenya’s HIV-positive cohort, achieved 96% seroconversion with one-fifth volume shots. These efficiencies enlarge the reachable population and buffer supplies during multi-country emergencies, strengthening the growth trajectory of the yellow fever treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Number Of WHO-Prequalified Manufacturers | -0.3% | Global, acute in Africa and South America | Short term (≤ 2 years) |

| Periodic Vaccine Supply Chain Disruptions | -0.3% | Global, concentrated in GAVI-eligible countries | Medium term (2-4 years) |

| Genotype-Specific Vaccine Escape Concerns | -0.2% | Endemic regions with high viral diversity | Long term (≥ 4 years) |

| Low Commercial Incentives For Antiviral R&D | -0.2% | Global, affecting pipeline development | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Number Of WHO-Prequalified Manufacturers

Fewer than six WHO-approved producers dominate supply, creating a fragile ecosystem evident during the eightfold surge in Americas cases in 2025. Outbreaks quickly exhaust the International Coordinating Group’s 6 million-dose buffer, forcing fractional dosing and risk-based prioritization. Such concentration also discourages newcomers because regulatory authorities lean toward incumbent producers with decade-long safety records. Until regional accelerators bring new capacity online, constrained production will temper growth prospects for the yellow fever treatment market.

Periodic Vaccine Supply Chain Disruptions

The live-attenuated 17D process requires embryonated eggs and lengthy QC steps, stretching batch cycles to 6-12 months. When unanticipated demand spikes, as seen in Latin America in 2025, the pipeline cannot respond quickly. Cold-chain gaps in remote districts further delay last-mile delivery, while competing claims between routine programs and outbreak drives complicate allocation. These weaknesses dampen sales visibility and inject cost uncertainty for both private and public buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Live-Attenuated Vaccines Dominate Despite Innovation Push

Live-attenuated vaccines generated 91.23% of the 2024 revenue, underscoring their entrenched role in the yellow fever treatment market size. Inactivated and recombinant options are projected to rise at an 8.26% CAGR through 2030, as safety profiles improve for immunocompromised travelers. Rapidly produced mRNA constructs and bivalent flavivirus candidates entered Phase 2 trials in 2025, signaling a potential future redistribution of market share. Yet, regulatory hurdles and concerns about cost parity mean that incumbents will likely retain their volume leadership in the near term. Health agencies continue to rely on 17D because longitudinal data support the concept of lifelong immunity after a single dose, keeping alternative platforms in a complementary rather than a replacement role.

Advances in thermostable coatings, single-dose presentations, and validated protocols for fractional doses further reinforce the incumbent platform’s utility. However, as novel pipeline candidates win emergency-use authorizations, the competitive field could widen. In that scenario, authorities might blend conventional and novel vaccines to cushion shortages, nudging overall growth for the yellow fever treatment market while imposing pricing pressure on established suppliers.

By Route of Administration: Subcutaneous Injection Faces Intradermal Innovation

Subcutaneous delivery accounted for 90.57% of 2024 administrations, solidifying its position as the standard practice for public campaigns. The intradermal route is growing at a 7.35% CAGR, driven by dose-sparing efficiency, which is crucial during outbreaks that strain stockpiles. Jet injectors eliminate needle-stick hazards and reduce biohazardous waste, gaining favor among frontline healthcare workers. The WHO's 2024 endorsement of intradermal dosing during emergencies altered procurement specifications, prompting countries to allocate funds for new devices.

Intravascular and oral formulations remain theoretical, but the steady adoption of intradermal techniques signals a gradual remapping of delivery norms. Broader deployment hinges on training, device maintenance, and local biomedical engineering capacity. If these barriers are overcome, intradermal options could secure a larger share of the yellow fever treatment market over the forecast horizon.

By Distribution Channel: Government Procurement Dominance Challenged by Retail Expansion

Governments' Procurement has a 68.92% share by distributional channel in 2024, a testament to the public-health thrust of immunization programs. Retail and online pharmacies, however, are advancing at an 8.97% CAGR as telemedicine frameworks streamline pre-travel consultations. International agencies now account for roughly one-quarter of global distribution, but their proportion could decline as private chains develop cold-chain capabilities and as travel health clinics proliferate in airports and major urban centers.

Digital scheduling tools, electronic certificates, and real-time inventory dashboards underpin this channel shift. Still, strict storage regulations and the need for physician oversight prevent vaccines from being sold directly to consumers through e-commerce. Over time, hybrid models—such as click-and-collect with clinic administration—may establish a new norm, leading to a more diversified yellow fever treatment market that balances public and private demand.

By Age Group: Adult Segment Leads While Geriatric Growth Accelerates

Adults aged 16-60 accounted for 61.38% of the 2024 value, driven by occupational and travel exposures; however, the geriatric cohort is projected to grow at a 7.34% CAGR through 2030. An aging global traveler base continues to explore endemic zones, prompting broader vaccination guidelines despite slightly higher adverse event rates in seniors. In contrast, pediatric immunization remains conservative outside endemic hot spots because risk-benefit models favor older children and adolescents.

Regulators now recommend pre-vaccination screening for those over 60 to mitigate viscerotropic and neurotropic risks. Even so, seniors value simplified travel protocols, which fuels uptake. Pediatric coverage is set to expand only as evidence from ongoing trials builds confidence. The shift in demographics represents a sizable increase in per-dose revenue potential, as older travelers often seek combination travel-health packages, contributing to the sustained expansion of the yellow fever treatment market.

Geography Analysis

The Middle East and Africa captured 38.41% of 2024 sales, thanks to sustained endemic cycles and the rollout of campaigns that vaccinated 62 million people across 13 nations. While Nigeria, Uganda, and the Democratic Republic of Congo remain priority territories, coverage still lags the 95% benchmark required for herd immunity, leaving periodic flare-ups unavoidable. Donor agencies fund bulk procurement, but internal logistics—from last-mile cold-chain to real-time case reporting—continue to challenge program reach.

Asia-Pacific, with a forecast 6.68% CAGR to 2030, signals a fundamental recalibration of risk. Climate models anticipate broader vector ranges across India, southern China, and Southeast Asia, motivating policymakers to pre-position stockpiles and integrate yellow fever into wider vector-borne disease strategies. Japan and Australia have increased their border-screening budgets and now recommend yellow fever shots for select outbound travelers, incrementally expanding demand for the yellow fever treatment market in a region historically classified as non-endemic.

South America faces persistent sylvatic transmission cycles, particularly in Brazil, Colombia, and Peru, which together recorded an eightfold increase in confirmed cases during 2025 compared to 2024. Fiocruz remains the prime regional supplier but still falls short when multiple countries need emergency allocations. North America and Europe represent smaller but steady travel-immunization niches. As mosquito habitats expand north due to warming climates, authorities are reevaluating yellow fever as a latent domestic threat, prompting modest increases in strategic reserves and contributing to a globally integrated yellow fever treatment market.

Competitive Landscape

The yellow fever treatment market is highly concentrated, with Sanofi SA, Bio-Manguinhos/Fiocruz, and Instituto Butantan controlling the bulk of WHO-prequalified output. Their collective dominance shapes procurement calendars and influences global stockpile policies. High fixed costs, live virus handling, and intricate egg-based production processes deter new entrants. Even Bavaria Nordic’s investigational candidates and other biotech pipeline assets remain in mid-stage development, limiting competitive disruption for the current forecast window.

Strategic movements emphasize regional self-reliance. Brazil’s capacity expansion, partly underwritten by Gavi’s health-sovereignty vision, reduces reliance on European plants and buffers South American demand. Sanofi announced over EUR 1 billion in manufacturing investments aimed at modernizing bioprocesses and increasing yield. Meanwhile, technology partnerships target mRNA and thermostable initiatives, keeping pipeline momentum alive despite limited revenue upside.

White-space opportunities cluster around antiviral therapeutics. A targeted-protein-degradation approach demonstrated broad flavivirus activity in 2024 lab studies; however, the absence of clinical pathways and an uncertain market size dampen immediate commercialization prospects. Digital health integrations—electronic certificates, blockchain-verified supply chains, and AI-driven outbreak mapping—offer lower-barrier competitive entry points. Still, the core vaccine segment will likely stay consolidated for the foreseeable future, shaping pricing power and manufacturing priorities within the yellow fever treatment market.

Yellow Fever Treatment Industry Leaders

Bio-Manguinhos / Fiocruz

Sanofi SA

Chumakov Institute

Instituto Butantan

Bharat Biotech

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: PAHO issued an epidemiological alert after recording 221 confirmed cases and 89 deaths across the Americas, an eightfold surge versus 2024.

- March 2025: PAHO released its first 2025 alert with 131 confirmed cases and 53 deaths, urging countries to review vaccine stocks and rapid-response plans as infections appeared in new locales.

Global Yellow Fever Treatment Market Report Scope

| Live-attenuated Vaccines |

| Inactivated / Recombinant Vaccines |

| Antiviral Therapeutics (Investigational) |

| Supportive Care Drugs & Consumables |

| Subcutaneous Injection |

| Intramuscular Injection |

| Intradermal Jet Injection |

| Government Procurement Agencies |

| International Agencies (UNICEF, PAHO) |

| Retail & Online Pharmacies |

| Paediatric (9 m – 15 y) |

| Adult (16 – 60 y) |

| Geriatric ( More Than 60 y) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Live-attenuated Vaccines | |

| Inactivated / Recombinant Vaccines | ||

| Antiviral Therapeutics (Investigational) | ||

| Supportive Care Drugs & Consumables | ||

| By Route of Administration | Subcutaneous Injection | |

| Intramuscular Injection | ||

| Intradermal Jet Injection | ||

| By Distribution Channel | Government Procurement Agencies | |

| International Agencies (UNICEF, PAHO) | ||

| Retail & Online Pharmacies | ||

| By Age Group | Paediatric (9 m – 15 y) | |

| Adult (16 – 60 y) | ||

| Geriatric ( More Than 60 y) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current valuation of the yellow fever treatment market?

The yellow fever treatment market size was USD 397.64 million in 2025 and is forecast to reach USD 488.78 million by 2030.

How fast is the subcutaneous delivery segment growing?

Subcutaneous delivery remains dominant but is projected to grow modestly as intradermal jet injection encroaches at a 7.35% CAGR.

Which region holds the largest market share?

The Middle East and Africa led with 38.41% of 2024 revenue thanks to endemic transmission and large-scale vaccination drives.

Why is the geriatric segment important for future growth?

Travelers over 60 show the highest CAGR at 7.34% because aging populations remain active and vaccination guidelines have broadened.

What role does climate change play in yellow fever risk?

Warming temperatures expand Aedes mosquito habitats into temperate zones, prompting Asia-Pacific and parts of Europe to bolster preparedness.

Page last updated on: