Hospital Infection Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

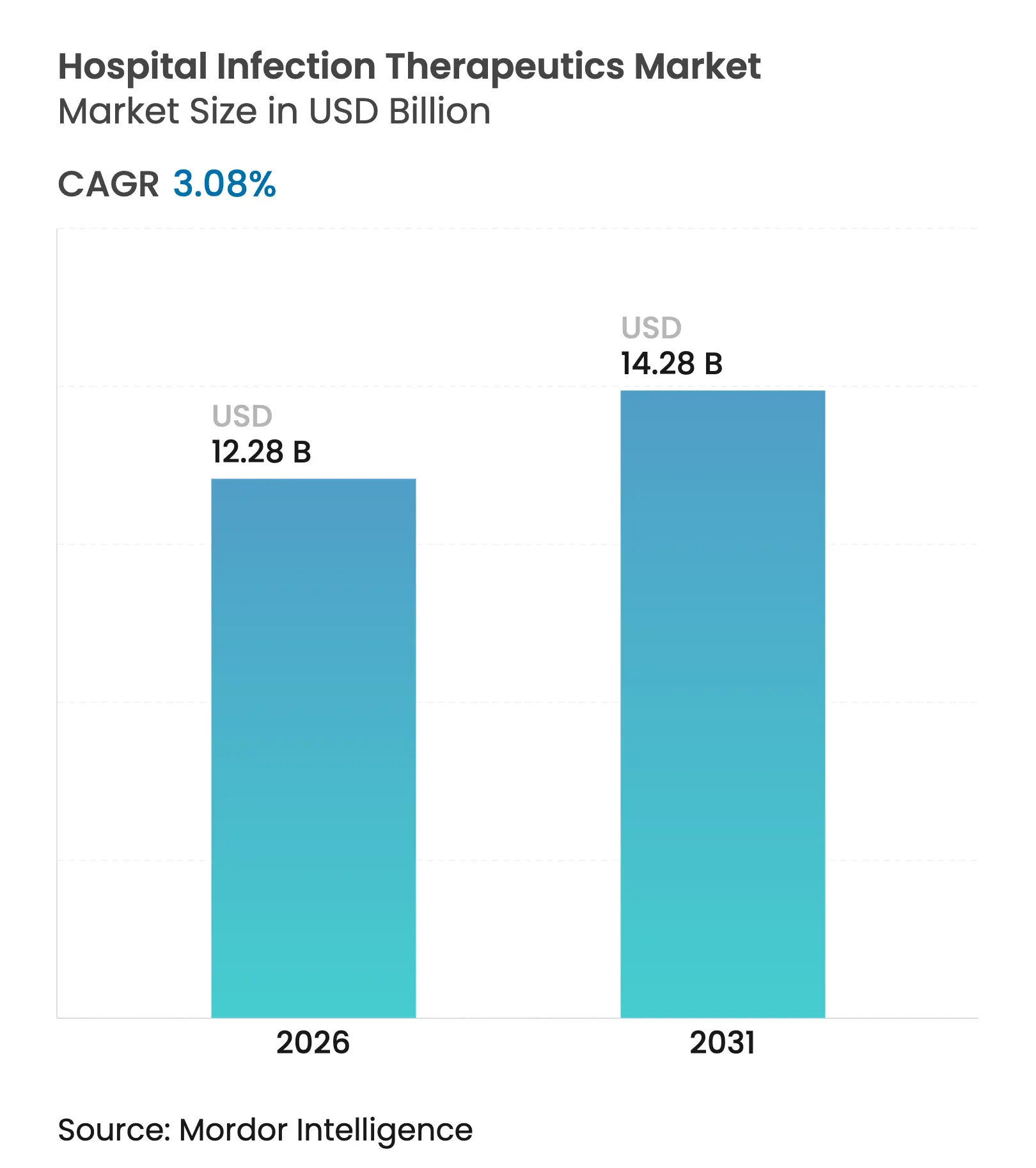

| Market Size (2026) | USD 12.28 Billion |

| Market Size (2031) | USD 14.28 Billion |

| Growth Rate (2026 - 2031) | 3.08 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Hospital Infection Therapeutics Market Analysis by Mordor Intelligence

The Hospital Infection Therapeutics market size is expected to grow from USD 11.91 billion in 2025 to USD 12.28 billion in 2026 and is forecast to reach USD 14.28 billion by 2031 at 3.08% CAGR over 2026-2031. Demand continues to track rising healthcare-associated infection (HAI) incidence, although wider adoption of infection-prevention technologies tempers growth potential. Mortality linked to carbapenem-resistant Acinetobacter baumannii now exceeds 40% in intensive-care settings, intensifying clinical urgency for effective agents.[1]Source: World Health Organization, “2023 Antibacterial Agents in Clinical and Preclinical Development,” who.int Governments are injecting fresh capital into antimicrobial pipelines; BARDA alone committed more than USD 500 million to resistance countermeasures in 2024. Parallel advances in artificial-intelligence (AI) drug discovery accelerate asset identification, while subscription-style reimbursement proposals such as the PASTEUR Act promise steadier revenue visibility for innovators.

Key Report Takeaways

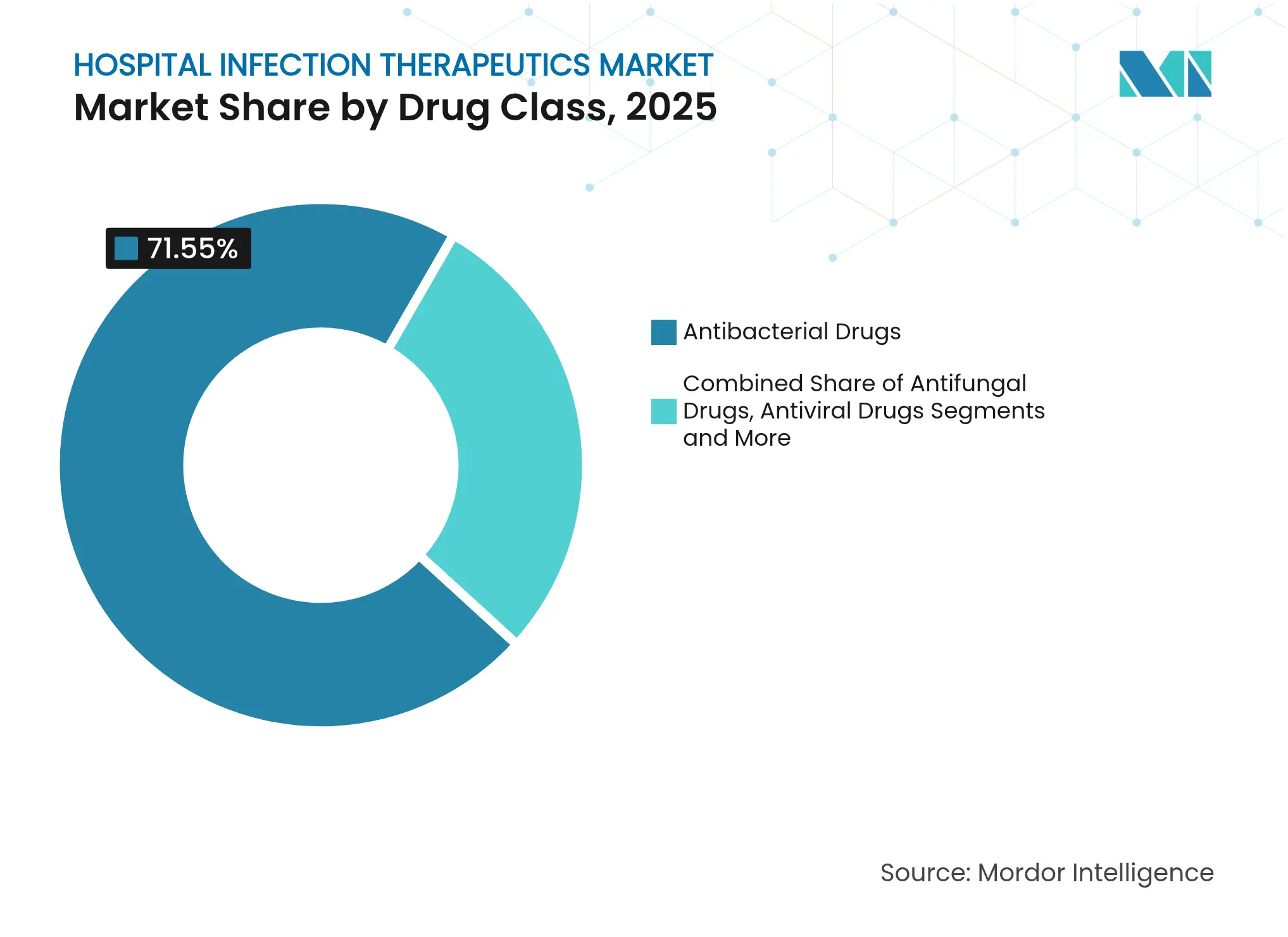

- By drug class: Antibacterials led with 71.55% revenue share in 2025, whereas antivirals are forecast to expand at a 3.65% CAGR to 2031.

- By infection type: Bloodstream infections captured 30.28% of hospital infection therapeutics market share in 2025; surgical site infections are set to rise at a 3.38% CAGR through 2031.

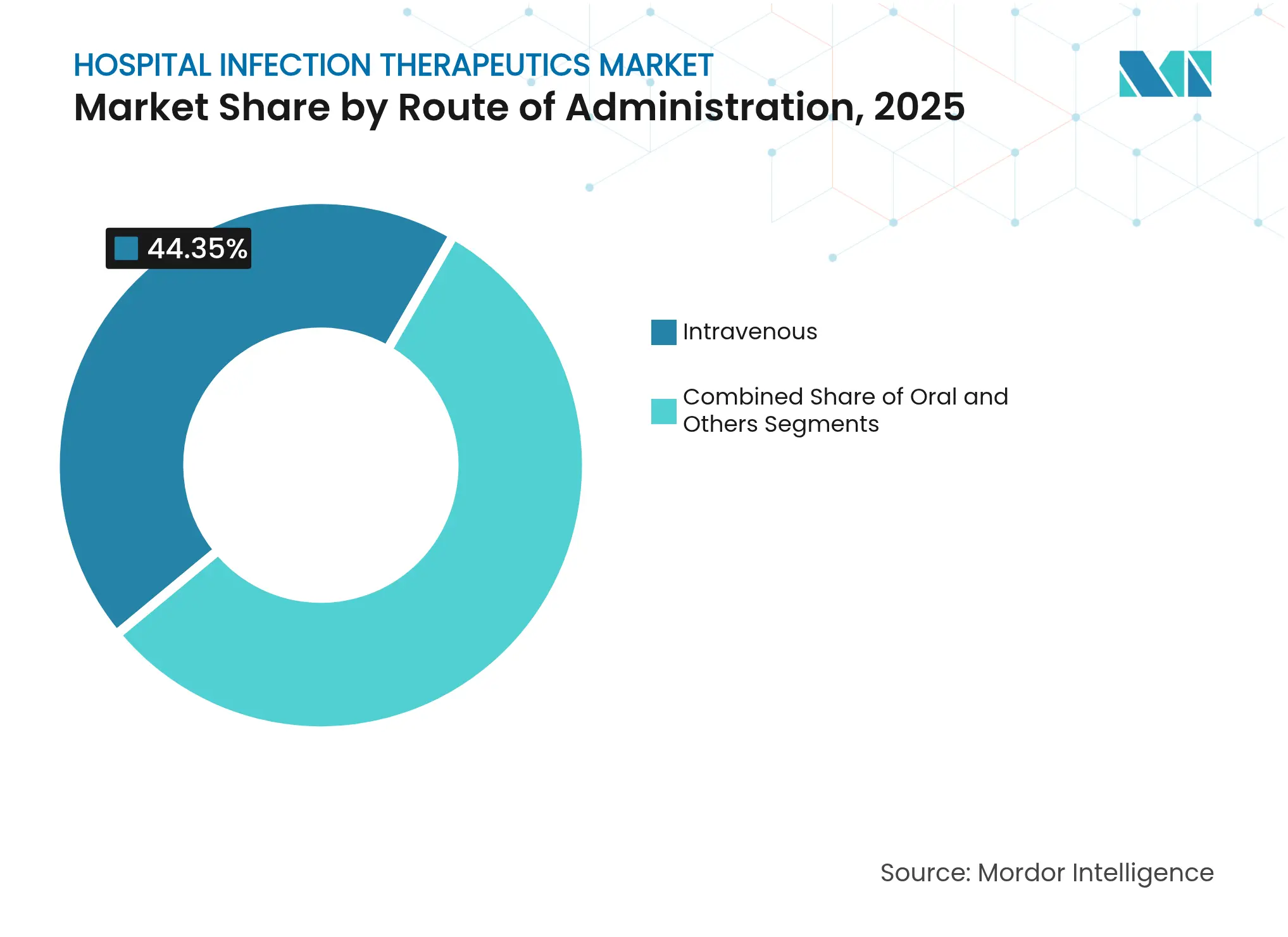

- By route of administration: Intravenous products commanded 44.35% of the hospital infection therapeutics market size in 2025, while oral formulations are advancing at a 3.95% CAGR between 2026-2031.

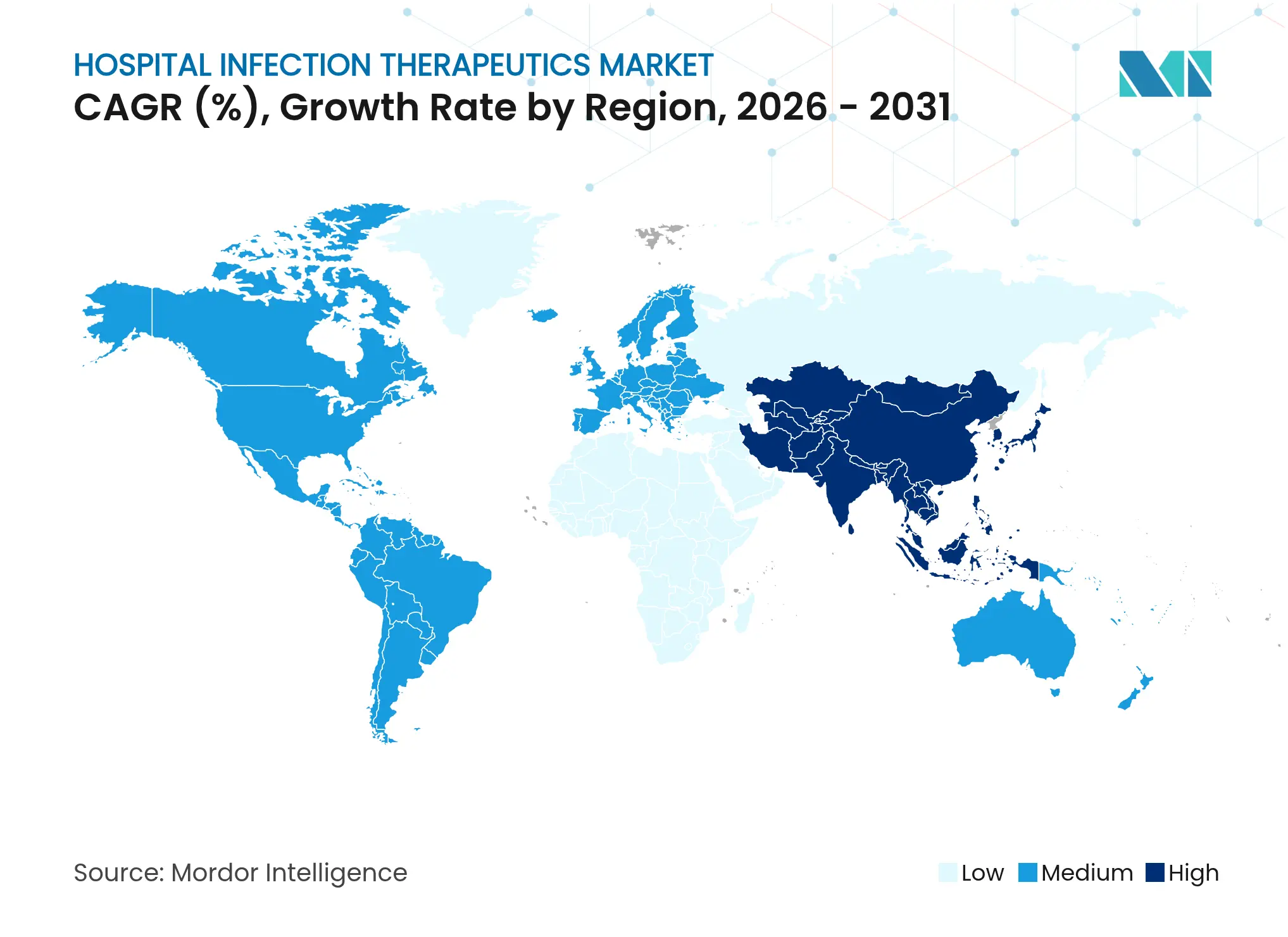

- By geography: North America held 37.30% of 2025 revenues, whereas Asia-Pacific is forecast to register the fastest 4.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hospital Infection Therapeutics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Escalating Prevalence of HAIs

Escalating Prevalence of HAIs

| +0.8% | Global, with acute impact in North America and Europe | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+0.8%

|

Geographic Relevance

:

Global, with acute impact in North America and Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

Growing Surgical Procedure Volume

Growing Surgical Procedure Volume

| +0.6% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) | |||

Rising Antimicrobial Resistance Crisis

Rising Antimicrobial Resistance Crisis

| +1.2% | Global, with critical hotspots in Asia-Pacific and MEA | Short term (≤ 2 years) | |||

Government Subscription Incentives for Novel Antibiotics

Government Subscription Incentives for Novel Antibiotics

| +0.4% | North America and EU, expanding to APAC | Medium term (2-4 years) | |||

AI-Enabled Rapid Antibiotic Discovery

AI-Enabled Rapid Antibiotic Discovery

| +0.3% | Global, concentrated in North America and EU | Long term (≥ 4 years) | |||

Infection-Surveillance Analytics Adoption

Infection-Surveillance Analytics Adoption

| +0.2% | North America and EU, early adoption in APAC urban centers | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating Prevalence of HAIs

Roughly 1 in 31 hospitalized U.S. patients acquires an HAI daily, and bloodstream infections alone account for more than 71,000 deaths each year. Hypervirulent carbapenem-resistant Klebsiella pneumoniae strains now infect both immunocompromised and healthy individuals, challenging conventional antibacterial regimens. In developing neurosurgical centers, spine-surgery infection rates reach 11.7%, lengthening median hospital stay to 36.5 days from 23 days for uninfected patients and directly raising therapeutic demand. Tertiary hospitals in Southwest China report the highest HAI incidence in hematology, cardiology, and neurology wards, where Klebsiella pneumoniae and Escherichia coli predominate. Collectively, these patterns reinforce consistent global need for potent, broad-spectrum agents within the hospital infection therapeutics market.

Growing Surgical Procedure Volume

Ambulatory surgery centers handle millions of outpatient operations under CDC-mandated surveillance protocols that heighten early detection of surgical site infections (SSIs). Asia-Pacific records the sharpest procedure growth, buoyed by infrastructure expansion and ageing populations pursuing complex interventions. Evidence links lumbar and thoracolumbar surgeries to elevated SSI risk, particularly when patients are admitted within 48 hours pre-operatively. Multimodal interventions across Sub-Saharan Africa have lowered SSI rates by as much as 95%, highlighting scope to curb downstream drug volumes when preventive protocols mature. Nonetheless, absolute procedure expansion still underpins steady unit sales in the hospital infection therapeutics market.

Rising Antimicrobial Resistance Crisis

Antimicrobial resistance (AMR) causes an estimated 1.27 million deaths annually, and models project 10 million deaths by 2050 without corrective measures. ESKAPE pathogens exhibit escalating multidrug resistance that forces clinicians toward last-resort options such as colistin, despite nephrotoxicity concerns. Carbapenem-resistant Acinetobacter baumannii now necessitates combination therapy after monotherapy failures, increasing treatment cost and complexity. The United States alone shoulders an economic burden above USD 4.6 billion per year due to resistant infections that extend length of stay and require premium agents. These dynamics elevate intensity of use within the hospital infection therapeutics market even as stewardship programs fight overuse.

Government Subscription Incentives for Novel Antibiotics

The proposed PASTEUR Act would authorize multiyear subscription contracts that delink revenue from volume, creating predictable cashflow for developers of critical-need antimicrobials. BARDA disbursed over USD 500 million in 2024 for resistance countermeasures including ceftobiprole and sulbactam-durlobactam. The National Institute of Allergy and Infectious Diseases (NIAID) released a USD 7.25 million call in 2025 for therapeutics targeting carbapenem-resistant Gram-negative bacteria. CARB-X opened its 2025 funding round aimed at early-stage assets in priority pathogens. These programs collectively increase R&D momentum, supporting pipeline renewal essential for the hospital infection therapeutics industry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Accelerating AMR Eroding Drug Efficacy

Accelerating AMR Eroding Drug Efficacy

| -0.9% | Global, with severe impact in hospital-dense regions | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

Global, with severe impact in hospital-dense regions

|

Impact Timeline

:

Short term (≤ 2 years)

|

High Development Costs and Lengthy Trials

High Development Costs and Lengthy Trials

| -0.5% | Global, particularly affecting smaller biotech firms | Long term (≥ 4 years) | |||

Preventive Technologies Curbing Drug Demand

Preventive Technologies Curbing Drug Demand

| -0.3% | North America and EU, expanding to APAC | Medium term (2-4 years) | |||

Tight Discharge Rules on Antibiotic Manufacturing

Tight Discharge Rules on Antibiotic Manufacturing

| -0.2% | Global, with stringent enforcement in EU and North America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Accelerating AMR Eroding Drug Efficacy

Vancomycin-resistant Enterococcus and methicillin-resistant Staphylococcus aureus remain entrenched threats in intensive-care units.[2]Source: University of Vienna, “New Hope Against Superbugs,” univie.ac.at Many pipeline candidates do not address WHO priority pathogens, leaving treatment gaps. Resistance to recently launched combinations such as ceftazidime-avibactam has already emerged within a few years of market entry. Rising failure rates prompt combination regimens that raise toxicity and procurement costs. This erosion pressures sustainable growth in the hospital infection therapeutics market.

High Development Costs and Lengthy Trials

Antibacterial programs face median outlays near USD 1.5 billion with uncertain return, deterring large-pharma participation. Ethical restrictions complicate placebo use in severe infections, inflating sample requirements and prolonging enrolment. Regulatory authorities require safeguards against rapid resistance development, adding post-approval commitments that elevate total expense. Many small biotech firms struggle to finance Phase 3 studies, creating attrition in the hospital infection therapeutics industry pipeline.

Segment Analysis

By Drug Class: Antibacterials Maintain Scale While Antivirals Accelerate

Antibacterials held 71.55% of global revenue. Intravenous agents such as ceftobiprole address Staphylococcus aureus bacteremia with 79.1% composite response rates, reinforcing the clinical dominance of β-lactam classes. Chinese sponsors now control 20 antibacterial programs in clinical evaluation, deepening supply resilience and competitive intensity. Generous NIAID grants targeting carbapenem-resistant Acinetobacter and Pseudomonas further stimulate antibacterial innovation.

Antivirals, though smaller today, are projected to grow at a 3.65% CAGR, reflecting broadened adoption of hospital-focused antivirals and immunomodulators. Precision-medicine workflows now match viral resistance genotypes with tailored therapy, improving outcomes and justifying price premiums. Antifungals meanwhile benefit from rezafungin approval for candidemia, filling a longstanding gap for once-weekly dosing in critical care. Bacteriophage and monoclonal-antibody therapies in the “others” cluster could add differentiated revenue streams, though manufacturing and regulatory complexities must be resolved before significant contributions accrue to the hospital infection therapeutics market.

Note: Segment shares of all individual segments available upon report purchase

By Infection Type: Bloodstream Leads, Surgical Sites Surge

Bloodstream infections generated USD 3.61 billion in 2025, equal to 30.28% of the hospital infection therapeutics market share. Early switch protocols from intravenous to oral regimens now shorten hospitalization without compromising efficacy, yet high mortality sustains willingness to pay for premium agents. Approximately 3.6 million U.S. patients suffer urinary tract infections annually, prompting 626,000 hospitalizations that drive recurring demand for oral agents such as gepotidacin and pivmecillinam.

Surgical site infections are projected to grow substantially, representing the fastest 3.38% CAGR within the hospital infection therapeutics market. Rising orthopedic and spine procedures in Asia-Pacific fuel this growth, while adherence to multimodal prevention bundles in lower-income settings remains inconsistent. Hospital-acquired and ventilator-associated pneumonias continue to necessitate novel β-lactamase inhibitor combinations such as aztreonam-avibactam, recently endorsed by the European Medicines Agency.

By Route of Administration: Intravenous Still Dominates, Oral Gains Momentum

Intravenous formats represented 44.35% of the 2025 hospital infection therapeutics market size. Regimens such as ceftobiprole (667 mg every 6-8 hours) or cefepime-enmetazobactam (2.5 g every 8 hours) remain standard of care for severe, inpatient infections. Critical-care reliance on high steady-state serum concentrations assures ongoing need for IV products even as outpatient care expands.

Oral agents are expected to grow at a 3.95% CAGR from 2026 to 2031. Gepotidacin’s first-in-class mechanism displays non-inferiority to nitrofurantoin in phase III urinary-tract infection trials, signalling renewed innovation in oral formats. Pivmecillinam demonstrates a 62% composite response versus 10% for placebo, improving outpatient management options. Specialized delivery systems—nebulized, topical, or intramuscular—comprise a modest but growing “others” segment targeting niche infections such as biofilm-associated device contamination.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America held 37.30% of global revenue of hospital infection therapeutics market in 2025. The CDC’s National Healthcare Safety Network entrenches mandatory HAI-reporting policies that sustain high therapeutic vigilance. BARDA funding underpins rapid translation of pipeline assets, culminating in recent FDA approvals such as ceftobiprole and cefepime-enmetazobactam. Pfizer is investing USD 150 million to modernize an Australian plant intended to supply more than 60 export markets, illustrating regional leadership in responsible manufacturing upgrades. The pending PASTEUR Act may further stabilize cashflows, shaping procurement strategies across hospitals.

Asia-Pacific is forecasted to post a 4.25% CAGR to 2031, the fastest among major regions. China’s regulatory reforms and the National Mega-Project for Innovative Drugs have propelled 17 companies with 20 antibacterial trials, contributing pipeline breadth and domestic pricing competition. India is enforcing a code of conduct for medical device marketing that strengthens infection-control standards, yet pharmaceutical effluent management remains a pressing challenge, with high antibiotic residues detected in industrial wastewater. Varied infrastructure maturity across ASEAN and South Asia yields heterogeneous demand, though rising procedure volumes create broad upward momentum within the hospital infection therapeutics market.

Europe benefits from coordinated AMR initiatives such as GSK’s £45 million Fleming Centre partnership. The European Medicines Agency’s positive opinion on aztreonam-avibactam marks the first β-lactam/β-lactamase inhibitor combination targeting metallo-β-lactamase producers, filling a therapeutic void. The Aurobac joint venture among Boehringer Ingelheim, Evotec, and bioMérieux adds diagnostic-therapeutic integration capabilities that may shorten time-to-effective therapy. Stringent environmental discharge rules and joint procurement initiatives help harmonize supply chain quality, though they also elevate compliance costs for entrants into the hospital infection therapeutics market.

Competitive Landscape

Market Concentration

The market remains moderately concentrated. Merck & Co., Inc., F. Hoffmann-La Roche AG, and others anchor the antibacterial segment through a mix of legacy brands and late-stage assets. Roche’s zosurabalpin, now in Phase 3, represents the first novel agent for carbapenem-resistant Acinetobacter baumannii in decades. Shionogi’s acquisition of Qpex Biopharma expands access to boronic acid derivatives and novel β-lactamase inhibitors.

AI partnerships are multiplying. Eli Lilly’s collaboration with OpenAI aims to accelerate in-silico lead generation, while smaller specialists such as Infex Therapeutics and Centauri Therapeutics pursue immunotherapies, peptides, and phage cocktails for multidrug-resistant pathogens. Environmental stewardship is now a competitive differentiator; Pfizer integrates AMR Industry Alliance standards into supplier audits and publicly reports progress on effluent targets.

White-space opportunities include precision-diagnosis linked therapies, hospital stewardship-aligned subscription contracts, and alternative modalities targeting biofilm and device-associated infections. Market entrants must, however, navigate capital-intensive clinical programs and evolving reimbursement policies that prioritize true novelty. Overall, rivalry is intensifying as public-private incentives lower financial risk and as AI compresses discovery timelines in the hospital infection therapeutics market.

Hospital Infection Therapeutics Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: CARB-X launched its 2025 funding round targeting global infectious-disease threats, allocating new grants to early-stage antimicrobials.

- February 2024: The FDA approved Exblifep (cefepime/enmetazobactam) for complicated urinary-tract infections, demonstrating a 79.1% composite response rate.

- March 2023: Hikma Pharmaceuticals PLC launched its Cefazolin for Injection. The drug is intended for the treatment of certain infections caused by bacteria, including urinary tract infections, skin, respiratory tract, lining of heart chambers and heart valves, joint, genital, bone, blood, biliary tract, and for perioperative prophylaxis.

- January 2023: Alkem launched the antibiotic Zidavi, which is a combination of ceftazidime and avibactam. The drug is intended for the management of hospital-acquired pneumonia (HAP) and complicated intra-abdominal infections (IAIs).

Table of Contents for Hospital Infection Therapeutics Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Escalating Prevalence of HAIs

- 4.2.2Growing Surgical Procedure Volume

- 4.2.3Rising Antimicrobial Resistance Crisis

- 4.2.4Government Subscription Incentives for Novel Antibiotics

- 4.2.5AI-Enabled Rapid Antibiotic Discovery

- 4.2.6Infection-Surveillance Analytics Adoption

- 4.3Market Restraints

- 4.3.1Accelerating AMR Eroding Drug Efficacy

- 4.3.2High Development Costs and Lengthy Trials

- 4.3.3Preventive Technologies Curbing Drug Demand

- 4.3.4Tight Discharge Rules on Antibiotic Manufacturing

- 4.4Regulatory Landscape

- 4.5Pipeline Analysis

- 4.6Porter’s Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Drug Class

- 5.1.1Antibacterial Drugs

- 5.1.2Antifungal Drugs

- 5.1.3Antiviral Drugs

- 5.1.4Others

- 5.2By Infection Type

- 5.2.1Blood Stream Infections

- 5.2.2Urinary Tract Infections

- 5.2.3Surgical Site Infections

- 5.2.4Pneumonia (HAP/VAP)

- 5.2.5Others

- 5.3By Route of Administration

- 5.3.1Oral

- 5.3.2Intravenous

- 5.3.3Others

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1AbbVie Inc.

- 6.3.2Merck & Co., Inc.

- 6.3.3Teva Pharmaceutical Industries Ltd.

- 6.3.4Viatris Inc.

- 6.3.5F. Hoffmann-La Roche AG

- 6.3.6Bayer AG

- 6.3.7GlaxoSmithKline plc

- 6.3.8Aurobindo Pharma Ltd (Eugia)

- 6.3.9Sanofi S.A.

- 6.3.10Pfizer Inc.

- 6.3.11Melinta Therapeutics

- 6.3.12Hikma Pharmaceuticals PLC

- 6.3.13Glenmark Pharmaceuticals Ltd.

- 6.3.14Basilea Pharmaceutica Ltd.

- 6.3.15Shionogi & Co., Ltd.

- 6.3.16Paratek Pharmaceuticals Inc.

- 6.3.17Spero Therapeutics Inc.

- 6.3.18Iterum Therapeutics plc

- 6.3.19Theravance Biopharma, Inc.

- 6.3.20Cipla Ltd.

- 6.3.21Seres Therapeutics Inc.

- 6.3.22Venatorx Pharmaceuticals Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Hospital Infection Therapeutics Market Report Scope

As per the scope of the report, hospital infection therapeutics are anti-infective agents or medications that are used to treat hospital-acquired infections (HAIs) or nosocomial infections. These infections are acquired by the patient at healthcare facilities such as hospitals due to the presence of infectious pathogens in the facility, instruments, infected patients, and others. The drugs used for treatment include antibacterial, antiviral, antifungal, or others based on the infection. The hospital infection therapeutics market is segmented By drug type (antibacterial drugs, anti-fungal drugs, antiviral drugs, and other drugs), by indication (bloodstream infections, urinary tract infections, surgical site infections, pneumonia, and other indications), and by geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.