Phage Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

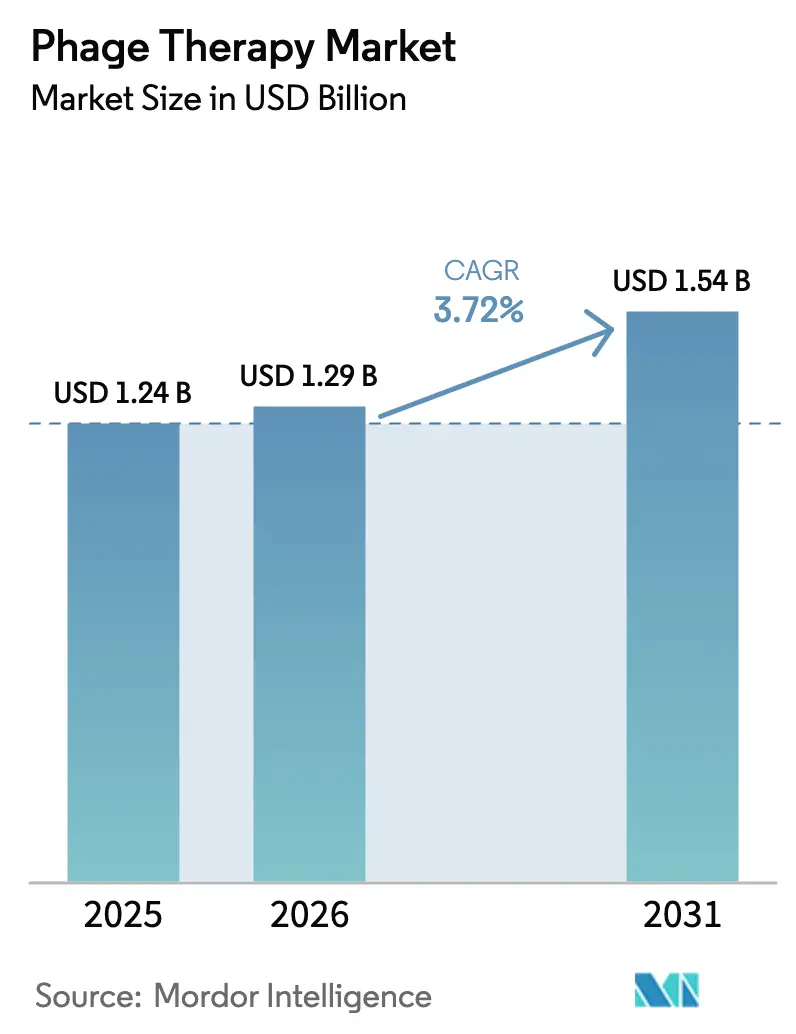

| Market Size (2026) | USD 1.29 Billion |

| Market Size (2031) | USD 1.54 Billion |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

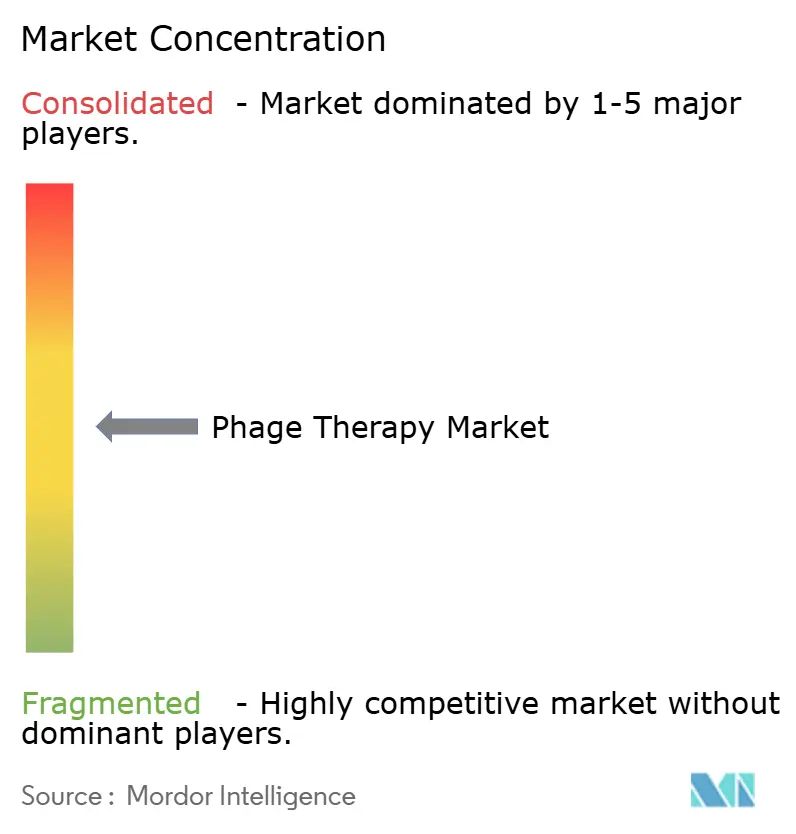

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Phage Therapy Market Analysis by Mordor Intelligence

phage therapy market size in 2026 is estimated at USD 1.29 billion, growing from 2025 value of USD 1.24 billion with 2031 projections showing USD 1.54 billion, growing at 3.72% CAGR over 2026-2031. This steady expansion marks the shift from experimental use toward routine clinical care as antimicrobial resistance escalates and regulatory authorities introduce clearer pathways for live biotherapeutic products.[1]European Medicines Agency, “Development and Manufacture of Human Medicinal Products Specifically Designed for Phage Therapy,” ema.europa.eu Growing evidence in cystic fibrosis, diabetic foot osteomyelitis, and refractory urinary tract infections confirms therapeutic value and encourages investment.[2]National Institute of Allergy and Infectious Diseases, “NIH-Supported Clinical Trial of Phage Therapy for Cystic Fibrosis Begins,” niaid.nih.gov Purpose-built GMP sites in Belgium, South Korea, and the United States demonstrate meaningful scale-up progress, while synthetic-biology platforms shorten discovery timelines and broaden bacterial coverage. Investor confidence remains resilient, highlighted by USD 50 million in fresh capital that accompanied BiomX’s acquisition of Adaptive Phage Therapeutics in March 2024. Collectively, these developments establish an expanding yet disciplined growth trajectory for the phage therapy market.

Key Report Takeaways

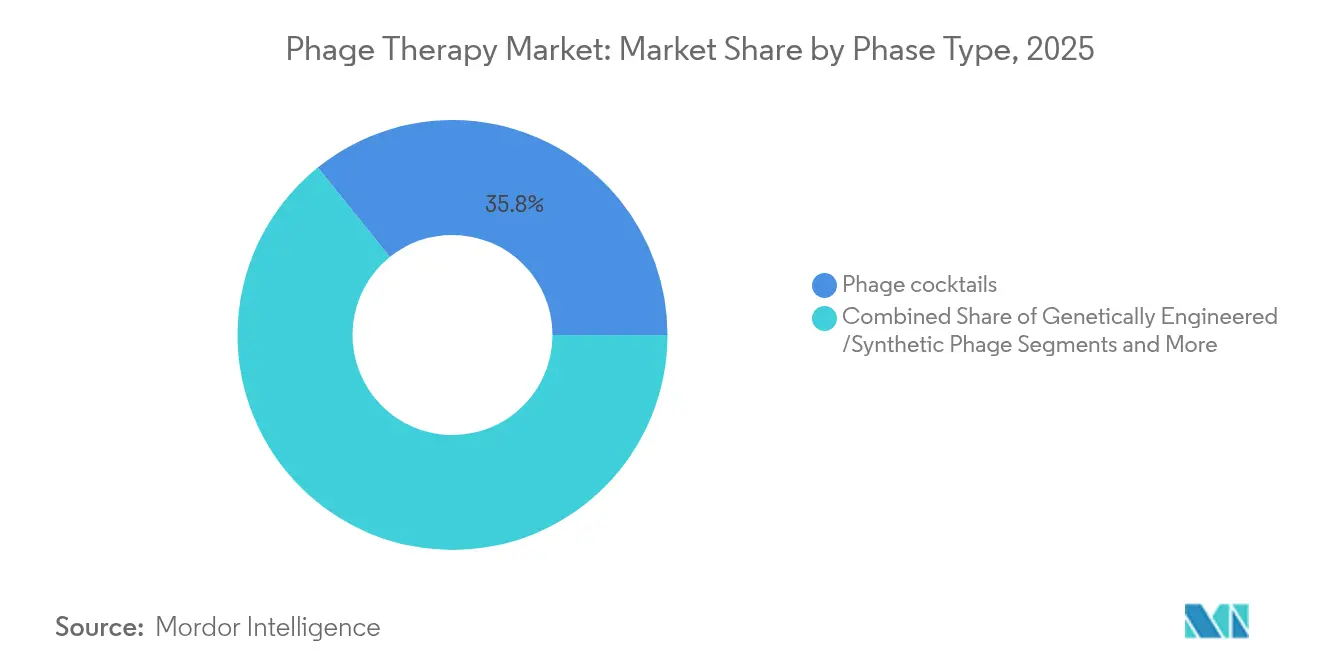

- By phage type, phage cocktails led with 35.78% of phage therapy market share in 2025.

- By targeted bacteria, Pseudomonas aeruginosa accounted for 26.88% share of the phage therapy market size in 2025, while Klebsiella pneumoniae is projected to expand at a 6.02% CAGR between 2026-2031.

- By mode of administration, injectable routes commanded 44.63% of the phage therapy market size in 2025; inhalation approaches are advancing at a 6.18% CAGR to 2031.

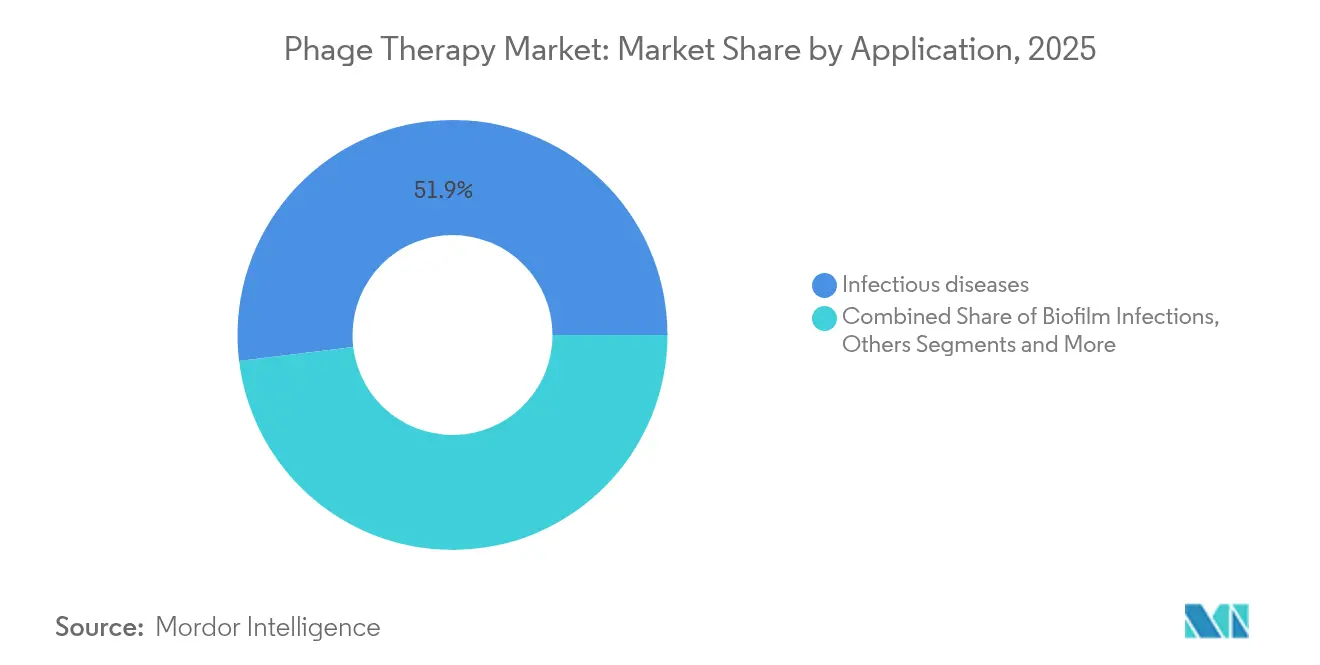

- By application, infectious diseases maintained 51.93% revenue share in 2025; antibacterial resistance mitigation is forecast to post the fastest 7.02% CAGR through 2031.

- By disease indication, cystic fibrosis lung infections held 26.31% of phage therapy market share in 2025 and continue to grow at 6.05% through 2031.

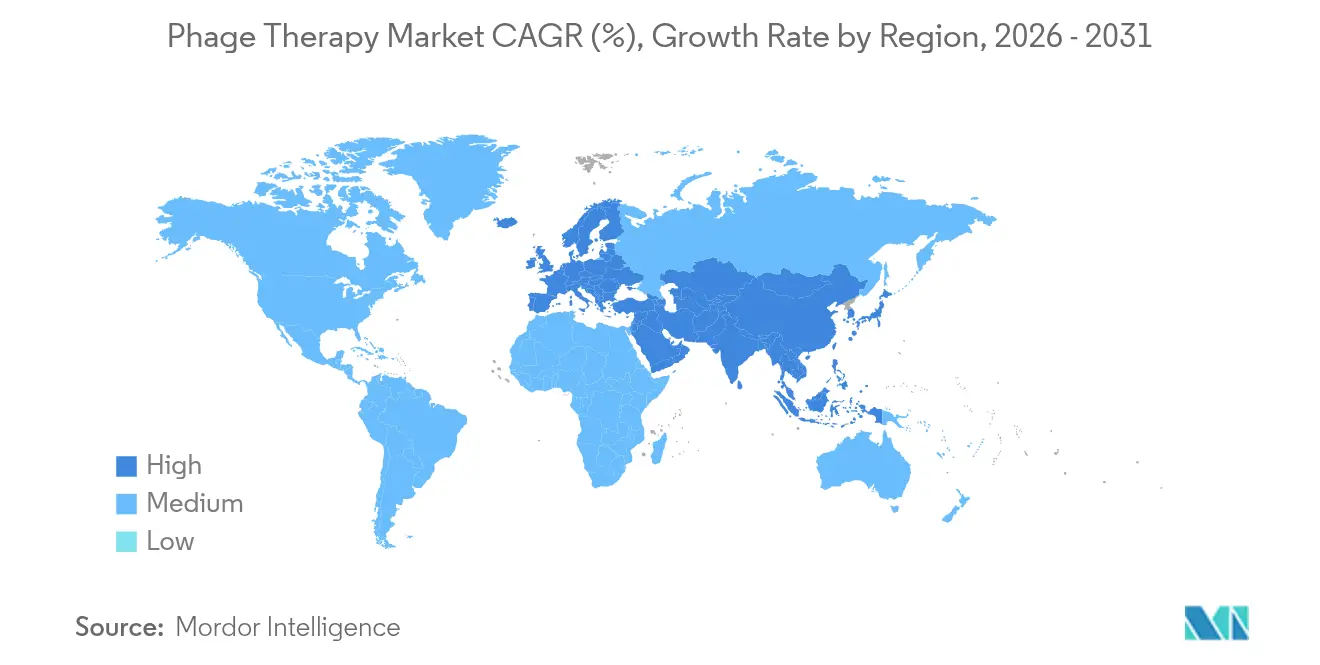

- By geography, North America retained leadership with 33.85% of phage therapy market size in 2025, while Asia-Pacific is pacing ahead at 6.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Phage Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of multidrug-resistant infections | +1.2% | Global with highest pressure in North America and Europe | Medium term (2-4 years) |

| Expansion of clinical-stage phage pipelines and funding rounds | +0.8% | North America and Europe core, expanding in Asia-Pacific | Short term (≤ 2 years) |

| Establishment of national phage banks and compassionate-use networks | +0.6% | Europe, North America, selective Asia-Pacific | Medium term (2-4 years) |

| Synthetic-biology-enabled designer phages entering trials | +0.9% | North America and Europe | Long term (≥ 4 years) |

| Regulatory fast-track designations for phage therapeutics | +0.5% | North America and Europe | Short term (≤ 2 years) |

| Growth of precision-microbiome medicine platforms | +0.7% | Global with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing prevalence of multidrug-resistant infections

Surveillance data from 2024 revealed Salmonella enterica isolates with 100% streptomycin resistance and 89.5% erythromycin resistance in cattle and humans in Egypt, underscoring the urgency for alternative modalities.[3]Shimaa El Baz, “Pan-drug Resistant Salmonella enterica Isolates in Egypt,” ann-clinmicrob.biomedcentral.comHospitals worldwide now consider bacteriophages essential tools against ESKAPE pathogens, a priority reinforced by the NIH Centers for Accelerating Phage Therapy initiative. Focused programs target biofilm-laden wounds, ventilator-associated infections, and immunocompromised patients, where conventional antibiotics falter.

Expansion of clinical-stage phage pipelines and funding rounds

BiomX absorbed Adaptive Phage Therapeutics in 2024, adding two Phase 2 assets and USD 50 million in new capital. BARDA awarded USD 23.9 million to Locus Biosciences for the first Phase 2 trial of a CRISPR-engineered phage therapeutic, LBP-EC01. More than 90 active interventional studies listed on ClinicalTrials.gov in 2024 illustrate pipeline breadth.

Establishment of national phage banks and compassionate-use networks

Belgium’s magistral preparation system permits pharmacists to custom-prepare phages within a regulated setting. The Israeli Phage Therapy Center reported positive outcomes across 100 compassionate-use cases over five years. The UK Citizen Phage Library can isolate clinically relevant phages within four days, streamlining emergency responses.[4]Julie Fletcher, “The Citizen Phage Library: Rapid Isolation of Phages,” mdpi.com McMaster University’s room-temperature storage technology further eases global distribution constraints.

Synthetic-biology-enabled designer phages entering trials

Locus Biosciences couples lytic activity with CRISPR-Cas3 genome shredding to enhance antibacterial potency. Northwestern University’s engineered phage induces self-destruction in Pseudomonas aeruginosa by sabotaging DNA replication. Gladstone Institutes advanced high-throughput genome editing, generating large variant libraries for rapid screening.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heterogeneous global regulatory frameworks | −0.7% | Global with widest gaps in emerging markets | Medium term (2-4 years) |

| Limited GMP manufacturing capacity for personalized phages | −0.9% | Worldwide, acute in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Emergence of phage-resistant bacterial mutants | −0.6% | Global | Long term (≥ 4 years) |

| Uncertain reimbursement and intellectual-property models | −0.8% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heterogeneous global regulatory frameworks

Belgium allows magistral preparations while many European Union members treat phages as advanced therapy medicinal products, demanding distinct dossiers. The United States requires IND filings; Georgia and Poland offer broader access with fewer hurdles, forcing companies to navigate divergent pathways that increase development costs.

Limited GMP manufacturing capacity for personalized phages

Traditional biologics plants are built for large, uniform batches, not the rapid, patient-specific runs phage therapy requires. Process changeovers and sterility testing can exceed the treatment window, delaying supply. The UK Parliament recommended converting the Rosalind Franklin Laboratory into a shared GMP site to bridge this gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Phage Type: Cocktails Lead Market Penetration

Phage cocktails captured 35.78% of phage therapy market share in 2025, reflecting clinical preference for blends that cover multiple bacterial receptors and suppress resistance. Natural lytic formulations continue to serve urgent-use settings, while endolysins and other phage-derived enzymes advance through late-stage trials such as exebacase for bloodstream infections. Mathematical modelling now guides bolus versus infusion dosing and has trimmed empirical trial-and-error cycles. As clinical familiarity grows, hospitals integrate cocktail regimens into stewardship protocols that once relied only on antibiotics.

Genetically engineered synthetic phages post the fastest 7.35% CAGR to 2031 as CRISPR payloads allow programmable genome degradation, broadening host range without sacrificing specificity. These dual-mode constructs expand phage therapy market size for hard-to-treat infections while easing supply constraints because the same scaffold can be rapidly retargeted. Pipeline depth now spans respiratory, orthopedic, and gastrointestinal applications, ensuring cross-indication revenue resilience. The convergence of natural and synthetic approaches also creates co-formulation opportunities in single-vial products, supporting streamlined hospital logistics and reinforcing cocktail leadership momentum.

By Targeted Bacteria: Pseudomonas Dominance with Klebsiella Growth

Pseudomonas aeruginosa infections commanded 26.88% of phage therapy market share in 2025, driven by prevalence in cystic fibrosis, ventilator-associated pneumonia, and chronic wound settings. NIH funding prioritizes ESKAPE organisms, channelling resources toward Pseudomonas-focused cocktails that now neutralize 96% of clinical isolates. Hospitals adopt these formulations as first-line adjuncts where carbapenem resistance limits antibiotic options. Klebsiella pneumoniae shows the fastest 6.02% CAGR as hypervirulent and carbapenem-resistant strains surge across intensive-care wards, elevating clinical demand.

Staphylococcus aureus retains meaningful share through prosthetic joint and osteomyelitis programs, while Escherichia coli assets target recurrent urinary tract infections. AI-driven matching platforms tailor phage mixes to local resistance panels, shortening time-to-therapy and cutting empirical antibiotic exposure. Beyond hospital pathogens, Salmonella and Streptococcus projects support veterinary and food-safety markets, expanding the total phage therapy market size into non-clinical revenue channels. Collectively, the shifting pathogen landscape underpins a diversified bacterial-target portfolio that balances mature and emerging revenue streams.

By Mode of Administration: Injectable Routes with Inhalation Innovation

Injectables retained 44.63% of phage therapy market size in 2025 as systemic infections such as bacteremia and endocarditis require rapid drug exposure. Intravenous formulations now pair phage cocktails with low-dose antibiotics to leverage synergy and delay resistance. Hospitals appreciate the predictable pharmacokinetics and established infusion infrastructure, sustaining injectable dominance.

Inhalation delivery is the fastest-growing route at 6.18% CAGR, propelled by cystic fibrosis programs where nebulized BX004 lowered bacterial burden without pulmonary toxicity. Encapsulated dry-powder devices promise home-use adherence, widening addressable patient pools. Topical sprays like TP-102 advance in diabetic foot ulcers, offering targeted biofilm penetration. Oral micro-encapsulation enables GI tract applications, while rectal enemas are under exploration for ulcerative colitis. Each platform diversification alleviates capacity risk in any single route and enlarges overall phage therapy market share across care settings.

By Application: Infectious Diseases Core with Resistance Focus

Infectious diseases remained the largest slice at 51.93% in 2025, encompassing acute and chronic bacterial indications where antibiotics fail. Physicians now prescribe phage cocktails alongside debridement in non-healing wounds and as adjuncts in prosthetic joint salvage, improving limb-preservation rates. These successes drive inclusion of phages in local antimicrobial guidelines, reinforcing core revenue stability.

Antibacterial resistance mitigation registers the fastest 7.02% CAGR as stewardship programs allocate budgets to preserve antibiotic efficacy. Biofilm disruption forms a critical sub-segment because phages and endolysins penetrate extracellular matrices unreachable by small-molecule drugs. Veterinary, aquaculture, and crop-protection deployments reduce agricultural antibiotic use and tie into One-Health objectives. Early studies in microbiome modulation for metabolic and inflammatory disorders hint at future white-space, signalling upside beyond current infection-centric models and increasing long-term phage therapy market size.

By Disease Indication: Cystic Fibrosis Leadership with Sustained Growth

Cystic fibrosis lung infections held 26.31% of phage therapy market share in 2025 and maintain a 6.05% growth outlook as chronic Pseudomonas colonization remains a leading morbidity driver. Multicenter trials such as WRAIR-PAM-CF1 validate safety and pulmonary delivery across diverse genotypes. Positive data underpin insurance discussions and encourage earlier therapeutic integration in standard care.

Urinary tract infections follow, backed by the ELIMINATE Phase 2 program targeting multidrug-resistant E. coli. Bone and joint infections, particularly prosthetic cases, leverage intra-articular phage depots that eradicate biofilms while preserving implants. Chronic otitis and dental applications benefit from pathogen specificity that leaves commensal flora intact, reducing dysbiosis complications. Exploratory work in ulcerative colitis and microbiome repair adds pipeline breadth, ensuring that future indications continue to expand phage therapy market size despite the dominance of cystic fibrosis today.

Geography Analysis

North America held 33.85% of phage therapy market size in 2025. FDA emergency programs and federal grants such as BARDA and CARB-X streamline translation from bench to bedside. Centers like UC San Diego’s IPATH provide curated phage libraries that clinicians can access within days. Canada and Mexico contribute through academic clusters and emerging contract manufacturing.

Europe benefits from the 2023 EMA guideline, which harmonizes quality and clinical expectations and supports investments across Belgium, France, and Germany. Belgium’s magistral system accelerates personalized supply, and the UK Citizen Phage Library strengthens rapid response. Eastern European programs supply long-term compassionate use data that feed Western regulatory dossiers.

Asia-Pacific posts the highest 6.6% CAGR to 2031. China’s prolific publication record aligns with new bioproduction sites, Japan leverages its regenerative medicine framework, and South Korea’s Hwaseong plant scales GMP capacity. India drafts compassionate-use guidance, while Australia deploys robust clinical-trial infrastructure. Early-stage interest across Brazil and South Africa points to widening access, although funding and regulatory gaps limit near-term uptake.

Competitive Landscape

The phage therapy market shows moderate concentration. BiomX, Armata Pharmaceuticals, and Locus Biosciences headline late-stage pipelines. BiomX’s acquisition of Adaptive Phage Therapeutics added proprietary matching algorithms and a 2,400-strain collection. Locus pairs CRISPR-Cas3 technology with BARDA support, while Armata focuses on inhaled phage therapies for respiratory infections.

Entry barriers include curated strain libraries, GMP compliance, and regulatory navigation. Yet opportunity remains in pediatric use, rapid diagnostics, and antibiotic-phage co-formulation. Academic spin-offs exploring AI-driven matching and synthetic scaffolds could disrupt incumbent models. Financial risk remains tangible as shown by PHAXIAM Therapeutics entering receivership in 2025. Strategic alliances between academia, government, and industry therefore remain crucial for sustaining the phage therapy market.

Phage Therapy Industry Leaders

Armata Pharmaceuticals

Locus Biosciences

BiomX

Intralytix

Adaptive Phage Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BiomX reported positive Phase 2 topline results for BX211 in diabetic foot osteomyelitis, confirming safety and clinical benefit.

- March 2024: BiomX completed a USD 50 million acquisition of Adaptive Phage Therapeutics, expanding its Phase 2 portfolio.

- January 2024: Locus Biosciences secured USD 23.9 million from BARDA to advance CRISPR-engineered LBP-EC01 for drug-resistant E. coli urinary tract infections.

Global Phage Therapy Market Report Scope

As per the scope of the report, phage therapy employs bacteriophages to combat bacterial infections. These phages are adept at pinpointing and eliminating harmful bacteria, presenting a promising substitute for traditional antibiotics. This targeted approach safeguards beneficial bacteria and curtails potential side effects. The primary cell culture market is segmented by targeted bacteria, mode of administration, application, disease indication, and geography. By targeting bacteria, the market is segmented into Escherichia coli, Staphylococcus aureus, Streptococcus, Pseudomonas aeruginosa, Salmonella, and Other Bacteria. By mode of administration, the market is segmented into oral, topical, and injectable. By application, the market is segmented into infectious diseases, antibacterial resistance, biofilm infections, veterinary applications, and others. By disease indication, the market is segmented into urinary tract infections, chronic otitis, dental extraction, chronic ulcerative colitis, bone infection, wound and skin infections, cystic fibrosis, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Natural lytic phages |

| Genetically engineered / synthetic phages |

| Phage cocktails |

| Endolysins & phage-derived enzymes |

| Escherichia coli |

| Staphylococcus aureus |

| Streptococcus spp. |

| Pseudomonas aeruginosa |

| Salmonella spp. |

| Klebsiella pneumoniae |

| Other bacteria |

| Oral |

| Topical |

| Injectable (IV/IM) |

| Inhalation / Nebulized |

| Infectious diseases |

| Antibacterial resistance mitigation |

| Biofilm infections |

| Veterinary applications |

| Aquaculture & agriculture |

| Others |

| Urinary tract infections |

| Chronic otitis |

| Dental & oral infections |

| Chronic ulcerative colitis |

| Bone & joint infections |

| Wound & skin infections |

| Cystic fibrosis lung infections |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Phage Type | Natural lytic phages | |

| Genetically engineered / synthetic phages | ||

| Phage cocktails | ||

| Endolysins & phage-derived enzymes | ||

| By Targeted Bacteria | Escherichia coli | |

| Staphylococcus aureus | ||

| Streptococcus spp. | ||

| Pseudomonas aeruginosa | ||

| Salmonella spp. | ||

| Klebsiella pneumoniae | ||

| Other bacteria | ||

| By Mode of Administration | Oral | |

| Topical | ||

| Injectable (IV/IM) | ||

| Inhalation / Nebulized | ||

| By Application | Infectious diseases | |

| Antibacterial resistance mitigation | ||

| Biofilm infections | ||

| Veterinary applications | ||

| Aquaculture & agriculture | ||

| Others | ||

| By Disease Indication | Urinary tract infections | |

| Chronic otitis | ||

| Dental & oral infections | ||

| Chronic ulcerative colitis | ||

| Bone & joint infections | ||

| Wound & skin infections | ||

| Cystic fibrosis lung infections | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the phage therapy market?

The phage therapy market was valued at USD 1.29 billion in 2026 and is projected to climb to USD 1.54 billion by 2031.

Which bacterial target holds the largest share?

Pseudomonas aeruginosa leads with 26.88% share of phage therapy market revenue in 2025, driven by its role in cystic fibrosis and hospital-acquired infections.

Why are phage cocktails preferred over single-phage preparations?

Cocktails combine multiple phages to broaden host range and reduce resistance, giving them 35.78% share of the phage therapy market in 2025.

Which region is growing fastest?

Asia-Pacific is the fastest-growing geography, advancing at a 6.6% CAGR through 2031 as manufacturing capacity and regulatory clarity improve.

Which administration route is gaining momentum?

Inhalation delivery is advancing fastest at 6.18% CAGR as cystic fibrosis programs demonstrate safety and efficacy for nebulized phage formulations.

Page last updated on: