Pigmentation Disorders Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

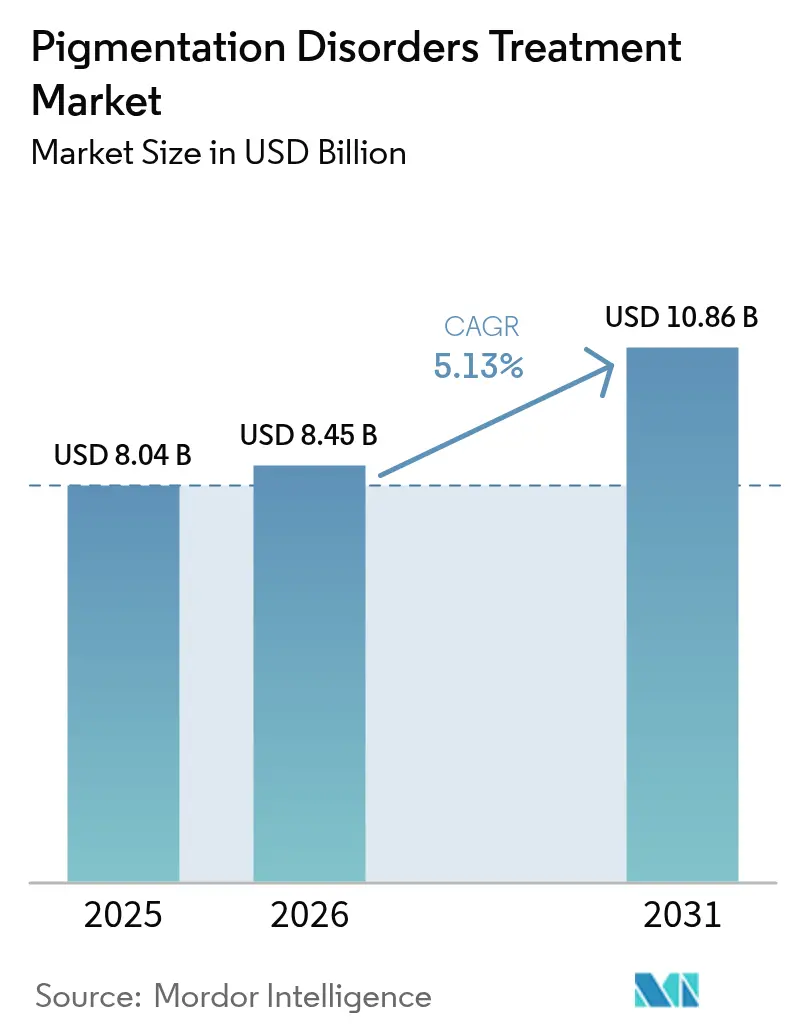

| Market Size (2026) | USD 8.45 Billion |

| Market Size (2031) | USD 10.86 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pigmentation Disorders Treatment Market Analysis by Mordor Intelligence

Pigmentation disorders treatment market size in 2026 is estimated at USD 8.45 billion, growing from 2025 value of USD 8.04 billion with 2031 projections showing USD 10.86 billion, growing at 5.13% CAGR over 2026-2031. Sustained growth is powered by rising disease prevalence, regulatory momentum behind topical and oral JAK inhibitors, increasing dermatology spending, and AI-driven diagnostic accuracy improvements. Pharmaceutical pipelines are focusing on immune-modulating pathways, while device makers refine laser safety profiles for darker skin tones. Convergence between medical dermatology and aesthetic care is widening the addressable base, and stronger social-media influence in Asia is accelerating patient awareness and therapeutic demand. Strategic acquisitions and portfolio diversification underscore a market moving toward precision medicine and omni-channel delivery models.

Key Report Takeaways

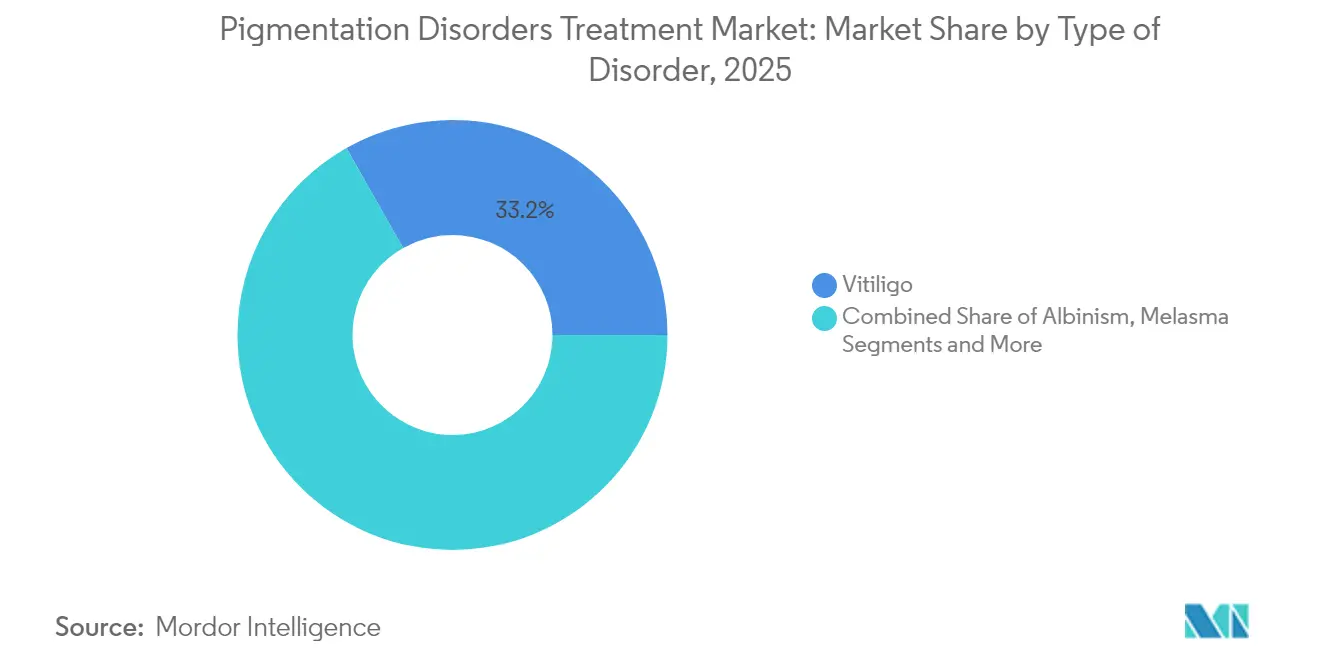

- By disorder type, vitiligo held 33.21% of the pigmentation disorders treatment market share in 2025; the segment is projected to expand at an 8.02% CAGR through 2031.

- By treatment type, laser and energy-based therapies led with 36.88% revenue share in 2025, while emerging biologics and JAK inhibitors are forecast to grow at a 8.74% CAGR to 2031.

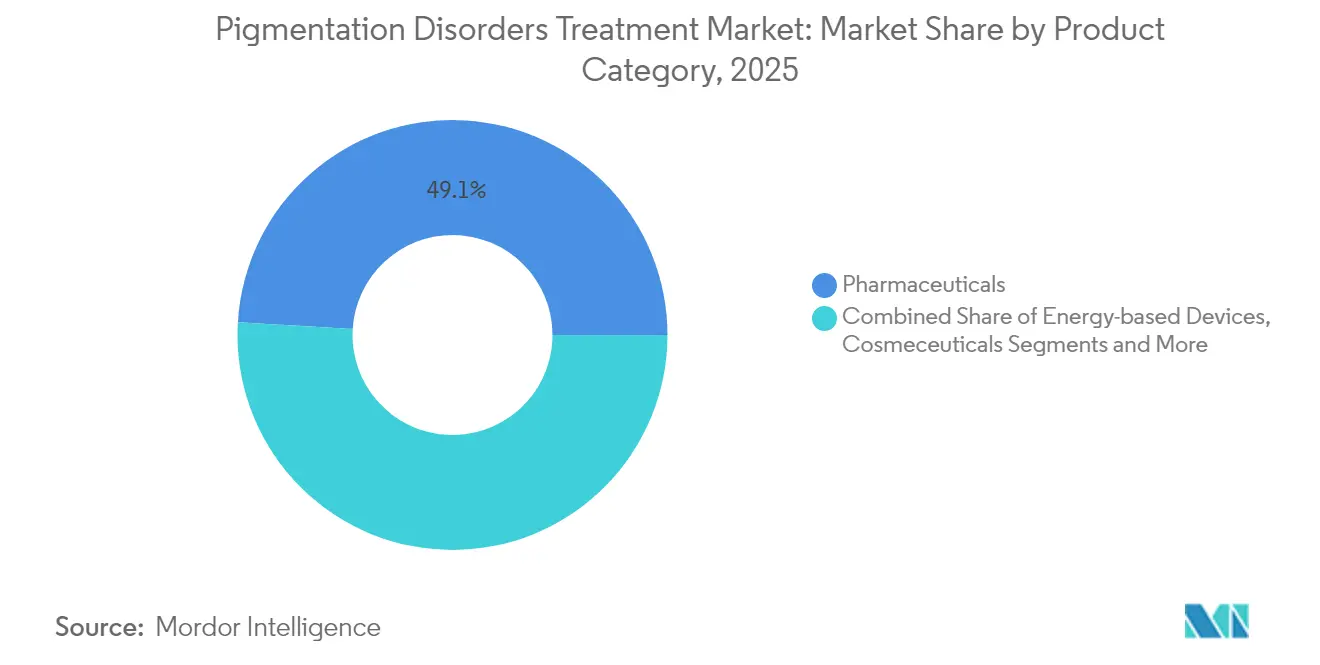

- By product category, pharmaceuticals accounted for 49.05% share of the pigmentation disorders treatment market size in 2025; energy-based devices are set to rise at a 9.22% CAGR between 2026-2031.

- By end user, dermatology clinics commanded 44.12% of 2025 revenue, whereas home-use and e-commerce customers will grow the fastest at an 8.23% CAGR through 2031.

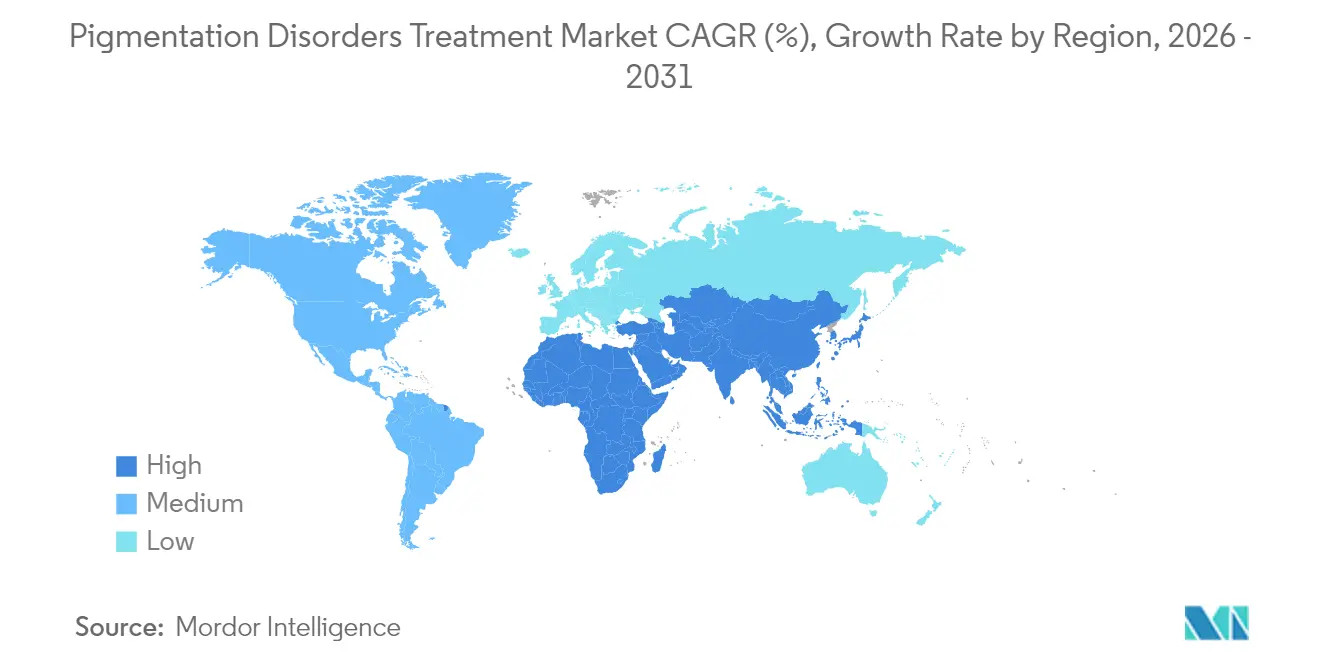

- By geography, North America dominated with 36.70% market share in 2025; Asia-Pacific is the fastest-growing region, advancing at a 7.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pigmentation Disorders Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in prevalence of pigmentation disorders | +0.8% | Global, higher incidence in APAC and MEA | Medium term (2-4 years) |

| Growing expenditure on dermatological & aesthetic procedures | +1.2% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| R&D pipeline success of topical JAK inhibitors | +1.5% | Global, led by US regulatory approvals | Medium term (2-4 years) |

| Social-media-driven demand for even-tone skin | +0.9% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| AI-enabled diagnostic imaging precision | +0.7% | North America & EU, gradual APAC adoption | Long term (≥ 4 years) |

| Pharma-aesthetic cross-over business models | +0.6% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Prevalence of Pigmentation Disorders

Global cases are climbing due to demographic changes, urban pollution, and greater diagnostic vigilance. Vitiligo affects 28.5 million people worldwide, generating a significant psychosocial burden among patients with darker skin tones who experience a higher contrast between affected and unaffected areas. Post-inflammatory hyperpigmentation is increasingly common after acne, with complete clearance seldom achieved even after treatment.[1]Touraj Khosravi-Hafshejani, “Treatment of Post-Inflammatory Hyperpigmentation in Skin of Colour: A Systematic Review,” Journal of Cosmetic Dermatology, journals.sagepub.com Melasma incidence remains high in sunny climates and among women of reproductive age, a trend exacerbated by shifts in UV exposure related to climate change. These epidemiological patterns enlarge the patient pool seeking both preventive and therapeutic solutions across regions.

Growing Expenditure on Dermatological & Aesthetic Procedures

Spending on dermatology services is rising as consumers prioritize skin health and appearance. Procedures once deemed purely cosmetic now attract reimbursement when therapeutic benefit is demonstrated, encouraging clinics to integrate lasers, peels, and combination regimens. Medical spas broaden service menus, while hospital outpatient departments adopt advanced devices to meet demand. Availability of professional-grade home-use IPL units at roughly USD 1,200 is widening access, stimulating the pigmentation disorders treatment market.

R&D Pipeline Success of Topical JAK Inhibitors

FDA approval of ruxolitinib cream marked the first targeted topical therapy for vitiligo, achieving notable facial repigmentation within 24 weeks. Oral candidates such as upadacitinib and povorcitinib have delivered encouraging phase 3 data, with upadacitinib lowering facial vitiligo area scores meaningfully. Regulatory momentum, proven mechanism of action via JAK-STAT modulation, and robust investment underscore a transformative therapeutic class for several pigmentary disorders.

AI-Enabled Diagnostic Imaging Improving Treatment Outcomes

AI systems for dermatology have demonstrated dermatologist-level accuracy on a high proportion of skin disease images, helping to reduce diagnostic gaps for darker skin tones.[2]Matthew Groh et al., “Deep learning-aided decision support for diagnosis of skin disease across skin tones,” Nature Medicine, nature.com Research findings demonstrate that leveraging deep learning decision support enhanced diagnostic accuracy by 33% for specialists and 69% for generalists.[3]J. Zhou et al., “Pre-trained multimodal large language model enhances dermatological diagnosis using SkinGPT-4,” Nature Communications, nature.com AI-guided reflectance confocal microscopy non-invasively quantifies melanin patterns, helping clinicians tailor therapy and objectively track progress. Enhanced precision translates to earlier intervention and optimized regimens, directly lifting treatment success rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket cost of cosmetic procedures | -0.9% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Limited reimbursement coverage for pigment disorders | -1.1% | North America & EU, expanding globally | Medium term (2-4 years) |

| Laser-induced PIH risk in darker skin types | -0.6% | Global, concentrated in APAC, MEA, Latin America | Long term (≥ 4 years) |

| Supply-chain dependence on Chinese hydroquinone feedstocks | -0.4% | Global, critical for North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost of Cosmetic Procedures

Many insurers classify pigmentation procedures as elective, leaving patients to shoulder costs that range from several hundred to several thousand dollars per session. Affordability issues delay treatment initiation and can lead to incomplete therapy cycles that blunt outcomes. The barrier is acute in emerging markets where disposable income lags demand for advanced aesthetic care, restraining the pigmentation disorders treatment industry’s immediate uptake despite clear clinical need.

Limited Reimbursement Coverage for Pigment Disorders

Coverage disparity is stark: 45 US states reimburse tretinoin for acne yet only 10 cover the medication for melasma or post-inflammatory hyperpigmentation. UnitedHealthcare deems several laser options “unproven and not medically necessary,” further limiting patient access. Such policies create treatment inequity, especially for skin-of-color populations that bear a disproportionate pigmentation burden.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Disorder: Vitiligo Drives Innovation Pipeline

Vitiligo accounted for 33.21% of 2025 revenue, securing the largest share of the pigmentation disorders treatment market. The segment is growing at an 8.02% CAGR, reflecting breakthrough approvals such as topical ruxolitinib and phase 3 trials of oral JAK candidates. The pigmentation disorders treatment market size for vitiligo is anticipated to climb steadily to 2031 as regulatory agencies worldwide review similar formulations. Melasma maintains significant demand within high-UV regions, while post-inflammatory hyperpigmentation remains prevalent among acne patients with skin of color. Albinism, though numerically smaller, sustains consistent therapeutic needs for photoprotection and ocular support. Completion of Clinuvel’s afamelanotide phase III trial may introduce systemic therapy that complements existing topical or phototherapy regimens.

Continued epidemiological surveillance shows pigmentary disorders intersect with psychosocial wellness, motivating health systems to assess quality-of-life indices in resource allocation. AI-driven diagnosis facilitates earlier vitiligo identification, enabling timely JAK inhibitor initiation before lesion expansion. Meanwhile, clinical researchers pursue biomarkers that forecast repigmentation likelihood, aiming to stratify patients and maximize therapeutic utility.

By Treatment Type: Energy-Based Therapies Lead Despite Emerging Competition

Laser and energy platforms captured 36.88% of 2025 revenue, retaining primacy through proven versatility across disorders. Still, biologics and JAK inhibitors are the fastest-growing class at 8.74% CAGR, heralding a precision-medicine era. The pigmentation disorders treatment market size for biologics is projected to widen as oral inhibitors secure wider indications and reimbursement frameworks adapt. Conventional topical depigmenting agents persist as foundational therapy due to ease of use and affordability. Chemical peels and dermabrasion support combination strategies that blend cosmetic refinement with clinical clearance.

Industry advances emphasize wavelength optimization and integrated cooling to mitigate PIH. Professional societies report that 1726 nm laser platforms enhance safety and permit uniform application across all Fitzpatrick skin types. Device makers also release multifunction consoles tailored to treat vascular lesions, acne, and pigmentation within one suite, raising capital-efficiency for clinics.

By Product Category: Pharmaceuticals Dominate Amid Device Innovation

Pharmaceuticals held 49.05% of sales in 2025, reflecting both prescription and over-the-counter offerings. The pigmentation disorders treatment market share within pharmaceuticals benefits from JAK inhibitor launches and next-generation tyrosinase inhibitors such as Thiamidol, which achieves near-complete melanin reduction in trials. Cosmeceutical advances complement prescription items, blending scientifically validated actives with consumer-friendly formulations. Energy-based device manufacturers outpace overall industry growth at a 9.22% CAGR by adding AI-assisted targeting, real-time temperature monitoring, and portable form factors.

Over the medium term, market observers expect increased bundling of drug and device packages to streamline therapy journeys. Partnerships between pharma companies and device makers may bundle ruxolitinib cream with low-fluence laser sessions, enhancing repigmentation velocity while expanding commercial reach.

By End User: Dermatology Clinics Lead While Home-Use Expands

Dermatology clinics generated 44.12% of 2025 revenue, underlining their central role in diagnosing and treating complex cases. Hospitals provide multidisciplinary support for refractory disease, yet clinic networks dominate day-to-day care. The home-use sub-segment is rising fastest at 8.23% CAGR as consumers purchase IPL and LED units online for maintenance or mild cases, reflecting broader digital-health adoption. The pigmentation disorders treatment market size linked to e-commerce is therefore poised for sustained expansion, although clinical oversight remains critical to manage adverse event risk.

Practitioners increasingly offer hybrid models where patients alternate between office visits and structured at-home regimens. Medical spas bridge the gap, delivering device-based interventions without the traditional hospital environment, attracting appearance-conscious but time-constrained clients.

Geography Analysis

North America retained the leading 36.70% share of the pigmentation disorders treatment market in 2025, aided by advanced insurance coverage for novel agents and broad clinician familiarity with laser protocols. Favorable reimbursement for ruxolitinib cream and ongoing phase 3 trials for oral inhibitors underpin demand momentum. High awareness among skin-of-color communities also propels service uptake, though coverage disparities persist.

Europe follows with stable growth as national health systems integrate targeted therapies alongside established topical standards. The region’s stringent device regulations encourage safety-focused innovation, reinforcing clinician trust in energy platforms. Public-funded phototherapy services remain widely accessible, creating balanced modality usage.

Asia-Pacific is the fastest-growing region at a 7.52% CAGR. Rising disposable income, strong social-media beauty influence, and deep cultural emphasis on even skin tone are catalyzing procedure volume in China, Japan, South Korea, and India. The pigmentation disorders treatment market size in Asia is set to close the gap with North America as e-commerce and medical-tourism channels proliferate. Regulatory harmonization across ASEAN countries may further streamline cross-border device distribution.

Latin America and the Middle East & Africa collectively represent an emergent frontier. Urbanization, improving dermatology infrastructure, and local manufacturing of cosmeceuticals seed steady uptake, though economic volatility and insurance gaps temper near-term scale. Government-led public-health programs to address albinism and vitiligo stigma may indirectly support therapy adoption.

Regulatory Landscape

Regulation for pigmentation-disorder therapeutics spans drug, device, and cosmetic/adjunct skincare frameworks. Topical prescription products, including depigmenting agents and topical JAK inhibitors, generally follow stringent quality and clinical evidence requirements under major regulators such as the US FDA and the European Medicines Agency (EMA). A key anchor is the EMA adoption in October 2024 of its guideline on quality and equivalence of locally applied, locally acting cutaneous products (EMA/CHMP/QWP/451535/2024), which tightens expectations around demonstrating therapeutic equivalence and can increase development and analytical burdens for both innovators and topical generics.

Harmonized quality initiatives also shape dossiers and lifecycle management. ICH progressed an extractables and leachables guideline (ICH Q3E) into public consultation in August 2025, influencing container-closure and packaging risk assessments relevant to creams, ointments, and topical solutions used for melasma, PIH, and vitiligo. In parallel, ICH initiated maintenance and modernization work for ICH Q6A/Q6B, with a targeted June 2026 timeline for completing Steps 1/2a/b. This reinforces science-based specifications and risk-based control strategies across dermatology products.

Value Chain Analysis

The value chain starts with upstream suppliers of APIs and key excipients used across depigmenting topicals and immunomodulators. It also includes component suppliers for energy-based platforms, such as laser sources, handpieces, cooling systems, and software. Midstream participants include pharmaceutical and biotech manufacturers and specialized CMOs capable of producing complex topical formulations, along with higher-complexity immunology assets where relevant. Device OEMs integrate hardware with safety features calibrated for a broader range of Fitzpatrick skin types.

Supply continuity and compliance flow through procurement, manufacturing controls, and post-market quality systems. The report scope highlights dependence on Chinese hydroquinone feedstocks as a vulnerability for global supply, which reinforces incentives for multi-sourcing, regionalization, and tighter supplier qualification. At the same time, programs advancing systemic vitiligo therapies increase the value of regulators and early scientific engagement across the value chain. AbbVie filed FDA and EMA applications for upadacitinib in non-segmental vitiligo in February 2026, and Clinuvel received final EMA scientific advice in April 2026 for its pivotal phase III vitiligo study design, increasing the importance of regulatory-ready evidence generation, scalable manufacturing plans, and specialty-channel distribution readiness.

Competitive Landscape

The market remains moderately fragmented. Key players wield extensive pipelines and global sales footprints. Galderma’s dual focus on prescription and aesthetic fillers exemplifies portfolio synergy, while AbbVie leverages immunology expertise to expand oral JAK assets. Strategic acquisitions illustrate the value of differentiated dermatology pipelines; Organon’s USD 1.2 billion purchase of Dermavant and its tapinarof platform highlights investor appetite for innovative topical mechanisms.

Mid-size specialists pursue niche paths, targeting melasma or PIH with proprietary delivery systems. Device manufacturers compete by integrating AI for lesion detection and uniform energy delivery, driving repeat purchases as clinics refresh fleets. White-space opportunities persist in therapies tailored to darker skin phototypes, an area historically underrepresented in trials. Competitive intensity fosters rapid publication of real-world evidence to secure payor acceptance and clinician adoption.

In parallel, partnerships between multinational pharma firms and cosmetic conglomerates seek to create end-to-end skin-health ecosystems. Co-marketing agreements bundle topical JAK inhibitors with nutricosmetic supplements, broadening consumer touchpoints beyond clinical settings and reinforcing brand loyalty throughout the treatment continuum.

Pigmentation Disorders Treatment Industry Leaders

Dermamed Solutions

AbbVie Inc (Allergan, Inc)

Obagi Cosmeceuticals LLC

L'Oréal SA

Merz Pharma

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is expanding systemic, immune-modulating options for non-segmental vitiligo, which extends unmet need beyond topical depigmenting agents and office-based procedures. In February 2026, AbbVie submitted regulatory applications to the FDA and EMA for upadacitinib (RINVOQ) in adults and adolescents with non-segmental vitiligo. In June 2026, the EMA CHMP issued a positive opinion recommending approval, indicating a late-stage pathway for an oral therapy class that can change treatment sequencing and reimbursement discussions. Novartis also initiated recruitment in March 2026 for a phase 2b study (NCT07431177) in adults with non-segmental vitiligo, adding competitive depth to systemic R&D and increasing demand for endpoints, imaging, and real-world evidence infrastructure in dermatology.

Differentiated offerings also have room to focus on skin-of-color safety, particularly around combination protocols for drug and device use. A June 2026 multicenter study in the Journal of the American Academy of Dermatology reported higher repigmentation rates in children with progressive vitiligo when oral JAK inhibitors were combined with 308-nm excimer laser therapy versus topical tacrolimus plus laser, supporting clinical pull for integrated drug-device regimens and clinic workflow solutions. On access, the market can build omni-channel care models that connect dermatologist-led initiation with home-use maintenance, including sun protection and adjunct skincare, supported by digital follow-up. Payor policy gaps for pigment disorders also keep affordability and evidence packages, including quality-of-life measures and durable outcomes, central to commercialization.

Recent Industry Developments

- June 2026: AbbVie announced that the EMA Committee for Medicinal Products for Human Use (CHMP) issued a positive opinion for upadacitinib (RINVOQ) in adults and adolescents with non-segmental vitiligo. The action advances a potential systemic treatment pathway and increases competitive pressure on topical-only regimens and procedural-first algorithms. It also raises the bar for payer and guideline engagement around endpoints that capture repigmentation and disease control.

- May 2025: Clinuvel Pharmaceuticals completed enrollment in its phase III afamelanotide vitiligo trial spanning more than 200 patients across three continents. Finishing enrollment reduces operational execution risk and sets up a late-stage data catalyst for a systemic approach that can complement topical and phototherapy regimens. The milestone also supports downstream planning for manufacturing, distribution, and clinician education ahead of potential registration activities.

- March 2025: Incyte reported positive TRuE-PN1 data for ruxolitinib cream 1.5% in prurigo nodularis at the 2025 AAD Annual Meeting. Although outside vitiligo, the readout reinforces the platform value of topical JAK inhibition in inflammatory skin disease and strengthens lifecycle and real-world evidence narratives around the molecule. Broader confidence in the class can accelerate clinician familiarity and formulary discussions that spill over into pigmentation-disorder treatment pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of treatments used to manage pigmentation disorders, including prescription and OTC topical drugs, oral therapies where used, in-clinic procedures (such as chemical peels and dermabrasion), and energy-based and light therapies delivered through dermatology and related care settings.

Scope exclusions: We exclude purely cosmetic color cosmetics that only conceal spots without a treatment claim, and general skincare items without a pigmentation indication.

Segmentation Overview

- By Type of Disorder

- Albinism

- Vitiligo

- Melasma

- Post-Inflammatory Hyperpigmentation (PIH)

- Other Disorders

- By Treatment Type

- Topical Agents

- Dermabrasion

- Chemical Peels

- Laser / Energy-based Therapies

- Phototherapy

- Emerging Biologics & JAK-Inhibitors

- By Product Category

- Pharmaceuticals

- Energy-based Devices

- Cosmeceuticals & Adjunctive Skin-care

- By End User

- Dermatology Clinics

- Hospital Out-patient Departments

- Medical Spas & Aesthetic Centers

- Home-use / e-commerce Customers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by pinning down the treated patient pool and the care pathways that typically apply in dermatology and aesthetic clinics, and then matching that to measurable activity signals. Public and official sources help keep inputs realistic, such as WHO skin health references, national health agencies like the US CDC, FDA public drug labels and approvals, and clinical trial registries that show what therapies are advancing. We also use peer-reviewed journals to understand standard of care shifts and typical treatment duration patterns, and trade and customs statistics where relevant for device and pharmaceutical trade flows.

On top of that, we review company filings, investor presentations, and reputable press to identify product launches and pricing direction. Where needed, a paid company financials and intelligence subscription is used to standardize revenue splits and avoid double counting across diversified portfolios, and a patent database is checked to validate the timing of technology transitions. The desk sources listed here are illustrative, and other public materials were also used to cross-check assumptions and clarify definitions.

Primary Interviews and Surveys

Primary work is used to pressure-test model inputs that desk sources do not fully answer, especially the mix shifts across topical therapies, in-clinic procedures, and device-based care. We spoke with dermatologists, clinic operators, hospital outpatient teams, distributors, and product-side executives across APAC, EMEA, and the Americas. The respondent input helped adjust assumptions on utilization, patient flow, and pricing, and we then rechecked those adjustments against the desk research totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | APAC: 41% |

| Mid tier: 51% | Functional/Unit leaders: 34% | EMEA: 35% |

| Smaller Players: 22% | Managers: 54% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool approach where prevalence signals and the likely treated share are converted into therapy volumes by care setting, and then translated into value using typical pricing ranges. To keep the math practical, we focus on repeatable inputs such as diagnosed and treated patient counts for common indications (for example, melasma, vitiligo, and post-inflammatory hyperpigmentation), average number of visits or sessions per course, procedure adoption within clinics, and product usage duration for topical regimens. Pricing is handled in local currency first where possible, then converted using consistent average exchange-rate assumptions for the year being sized.

The outputs are then corroborated with selective bottom-up checks, including sampled price lists from clinics, distributor channel checks, and supplier-side approximations of volume times average selling price for key therapy groups. When a country-level data point is missing, we proxy using comparable markets based on dermatologist density, urbanization, and aesthetic procedure penetration, and then we revisit those proxies during interviews. For forecasting, scenario analysis is applied around a base case, which is then shaped by inputs like expected therapy switching, regulatory and label expansions, and gradual price normalization as more options enter the market.

Data Validation & Update Cycle

Validation is done by comparing model totals against independent signals, such as procedure intensity in dermatology settings, device install trends, and the observed share of dermatology versus aesthetic channels in each region. If a number looks too high or too low, we trace it back to the driver level, adjust the assumption, and recheck the impact across countries and therapy types before sign-off.

Each report is refreshed annually, and interim updates are made when material events occur, such as a major approval, safety warning, or a noticeable pricing reset. Right before delivery, a final review pass is completed so the client receives the latest view, with the same assumptions checked again for internal consistency.

Mordor Intelligence's Pigmentation Disorders Treatment Market Sizing Compared With Other Published Estimates

Published market values for pigmentation disorders treatment can differ quite a bit, even when the topic name looks identical, because the scope boundaries and counting rules are not the same. The biggest swings usually come from what is included as treatment revenue, how procedure value is counted, and whether the estimate is tied to treated patient activity or broader manufacturer-side revenue logic.

In our comparisons, two gaps show up often in this space, where some estimates fold cosmeceuticals and adjacent skin-lightening retail products into the same total, and others count factory-gate device and service revenues that can overlap with clinic-level spending. The spread also widens when pricing is projected using aggressive inflation assumptions, or when currency conversion is done using a single point-in-time rate rather than an annual average and then not revisited during updates. For that reason, we keep treatment-course and session-level checks in place before finalizing the total, a discipline applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.45 B (2026) | |

| Global Consultancy A | USD 6.67 B (2025) | Uses a revenue accounting view that includes factory-gate values and related goods sold within the offering, which can understate clinic-level procedure spend and may not fully reflect patient session intensity in premium dermatology channels. |

| Industry Publisher B | USD 8.80 B (2025) | Appears to include a wider treatment basket with strong emphasis on broader modality coverage and longer horizon assumptions, which can lift the base-year total if more consumer-facing cosmeceuticals and maintenance regimens are counted as treatment value. |

Taken together, the comparison shows that market size shifts primarily on whether the estimate is built from treated patient activity and clinic procedures, or from broader revenue definitions that may mix in adjacent skincare. By keeping the steps traceable to patient flow, session counts, and realistic pricing, the final number stays easier to recreate and to stress-test when conditions change.

Key Questions Answered in the Report

What is the current size of the pigmentation disorders treatment market?

The market is valued at USD 8.45 billion in 2026 and is projected to reach USD 10.86 billion by 2031.

Which disorder type generates the highest revenue?

Vitiligo leads with 33.21% of 2025 revenue and is expanding at an 8.02% CAGR through 2031.

What treatment category is growing the fastest?

Emerging biologics and JAK inhibitors are advancing at a 8.74% CAGR, outpacing all other modalities.

Which region shows the strongest growth momentum?

Asia-Pacific is the fastest-growing region, recording a 7.52% CAGR on the back of rising disposable income and social-media influence.

What main barrier limits patient access to advanced therapies?

Limited reimbursement coverage, particularly in North America and Europe, often classifies pigmentation treatments as cosmetic, pushing costs onto patients.

Page last updated on: