Herpes Simplex Virus Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

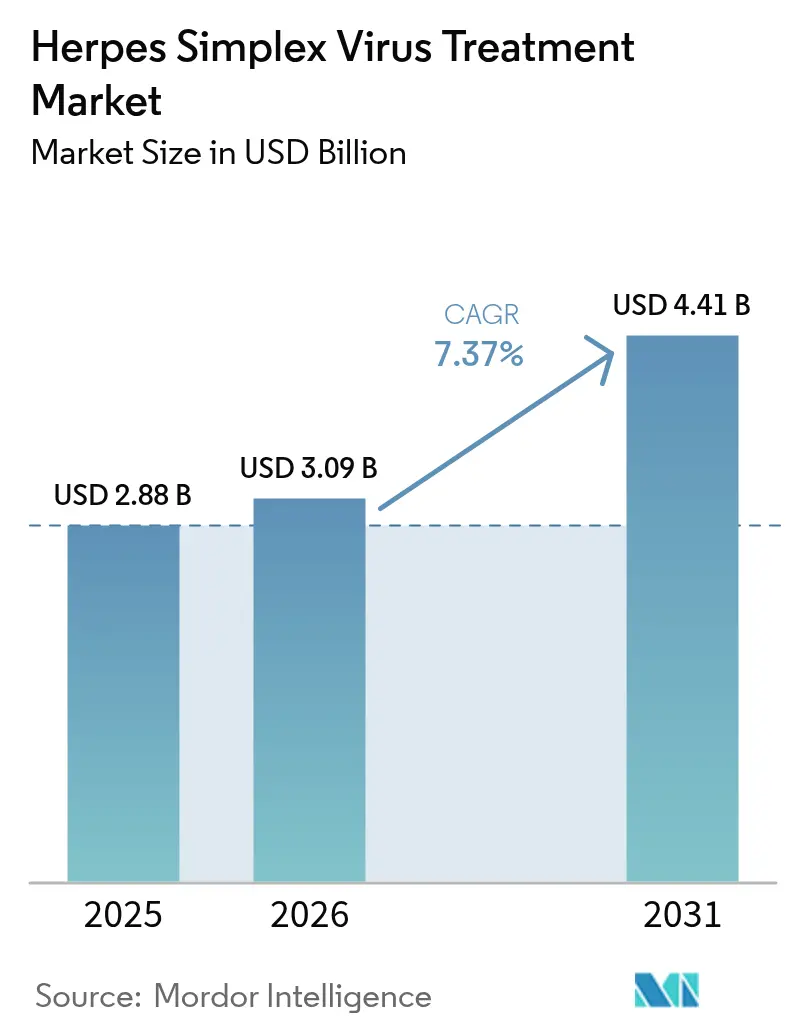

| Market Size (2026) | USD 3.09 Billion |

| Market Size (2031) | USD 4.41 Billion |

| Growth Rate (2026 - 2031) | 7.37% CAGR |

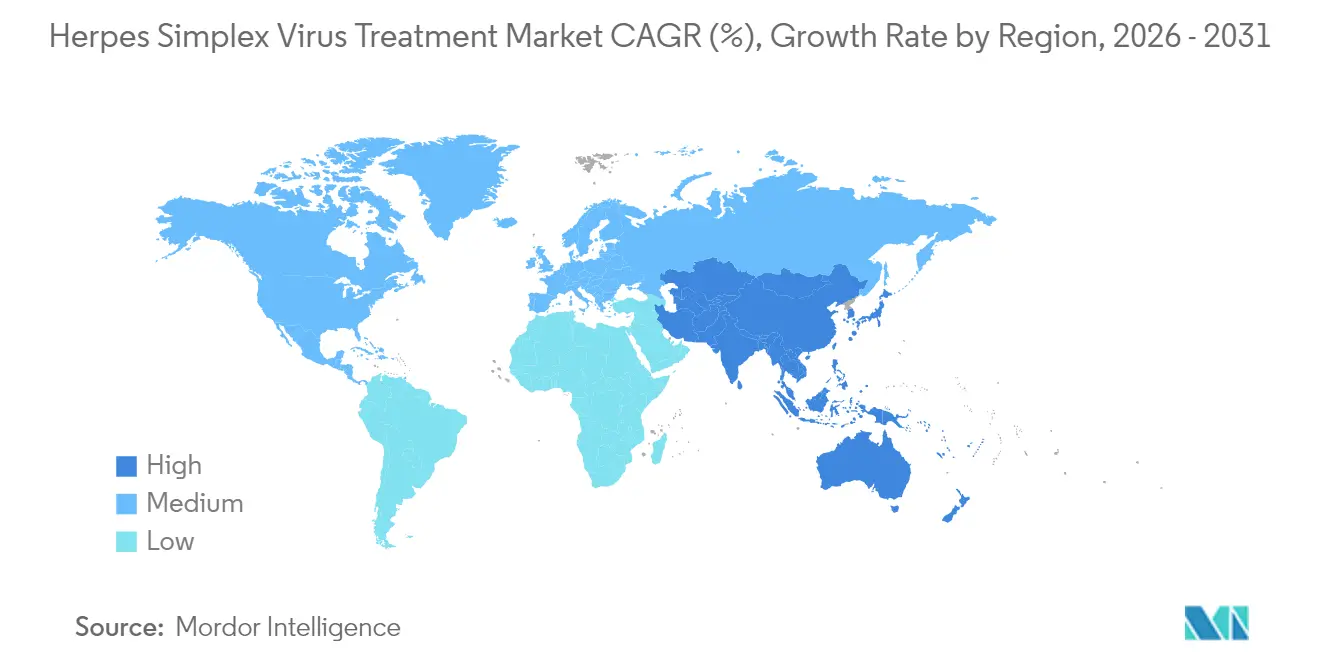

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Herpes Simplex Virus Treatment Market Analysis by Mordor Intelligence

The herpes simplex virus treatment market size in 2026 is estimated at USD 3.09 billion, growing from 2025 value of USD 2.88 billion with 2031 projections showing USD 4.41 billion, growing at 7.37% CAGR over 2026-2031. Demand is being sustained by the dual spread of HSV-1, which remains ubiquitous, and HSV-2, whose faster incidence growth is tied to improved diagnostics and rising sexual-health awareness. Increasing acyclovir resistance in immunocompromised patients is pushing R&D toward helicase-primase inhibitors and gene-editing modalities. At the same time, telemedicine platforms are reducing stigma-driven care delays, lifting prescription volumes for first-line antivirals and topical over-the-counter (OTC) options. Investment momentum is strongest around long-acting oral candidates, CRISPR-enabled curatives, and topical innovations that promise once-daily dosing.

Key Report Takeaways

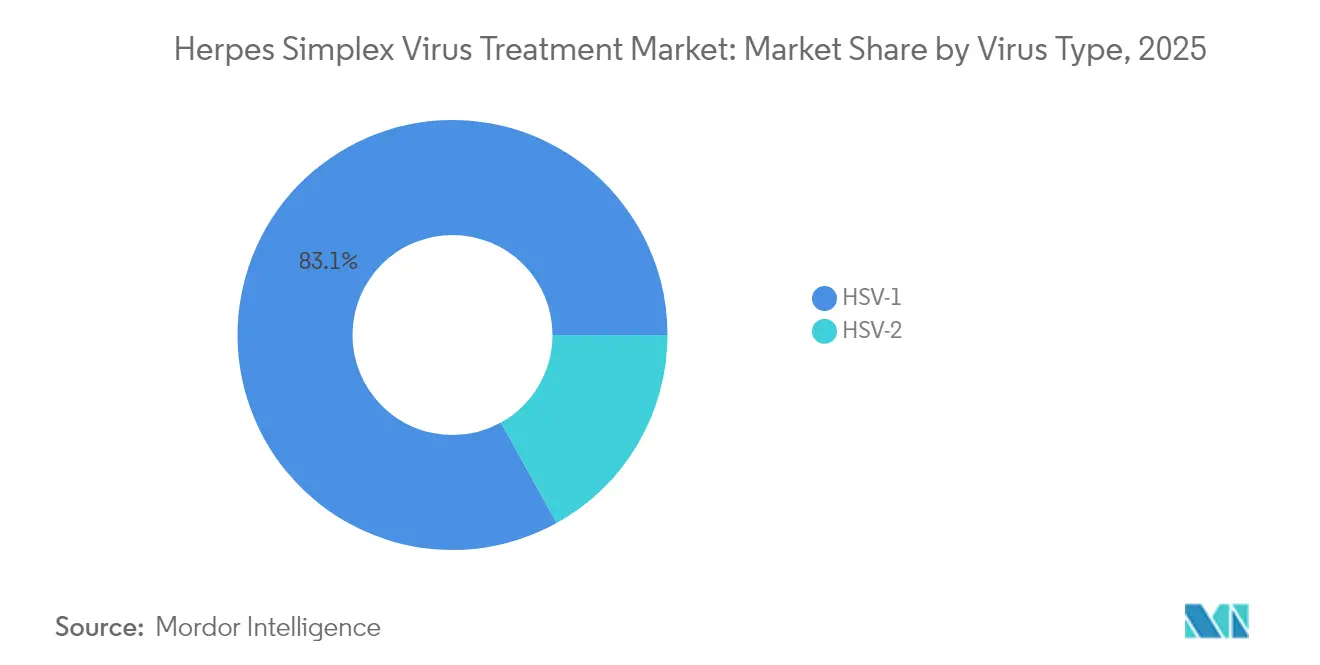

- By virus type, HSV-1 led with 83.05% revenue share in 2025, while HSV-2 is projected to expand at a 9.21% CAGR through 2031.

- By drug, valacyclovir captured 28.78% share in 2025; acyclovir is set to post a 5.55% CAGR over 2026-2031.

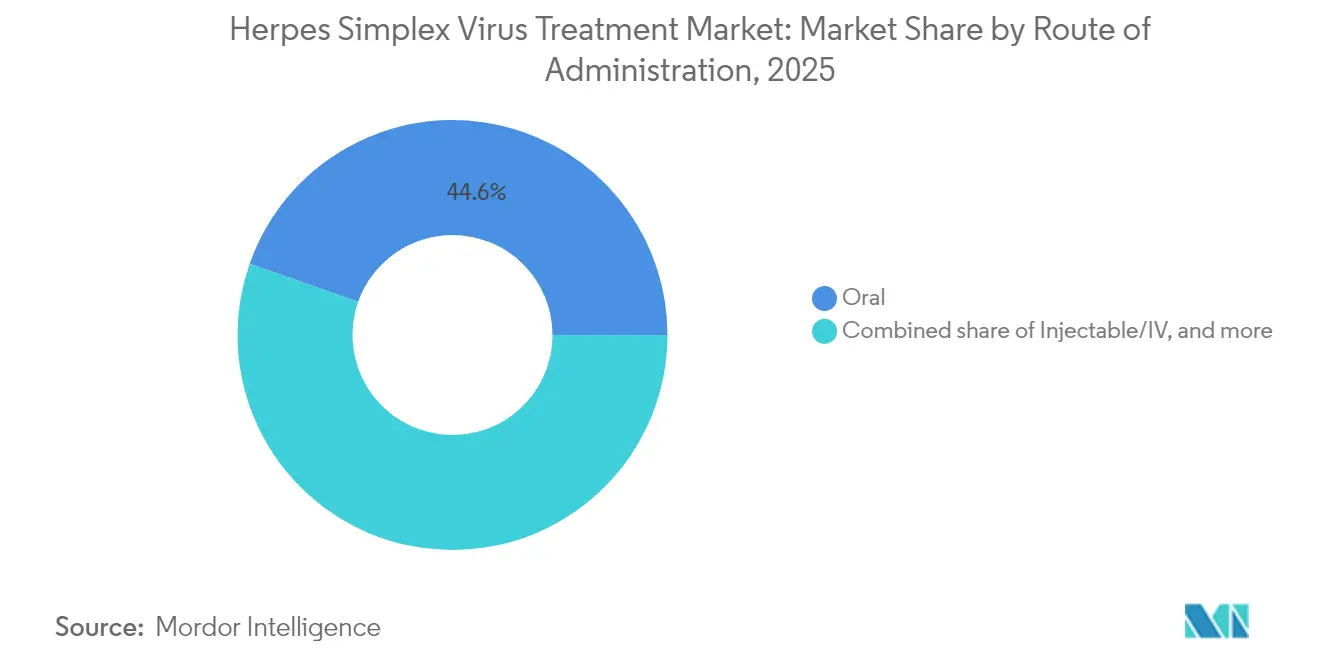

- By route of administration, the oral segment accounted for 44.62% share of the Herpes Simplex Virus Treatment market size in 2025 and is advancing at a 7.02% CAGR through 2031.

- By distribution channel, retail pharmacies and drug stores held 44.75% share in 2025, while online pharmacies are forecast to register the fastest 10.95% CAGR during 2026-2031.

- By geography, North America commanded 31.98% of the Herpes Simplex Virus Treatment market share in 2025, whereas Asia Pacific is poised to grow at a 8.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Herpes Simplex Virus Treatment Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acyclovir resistance reaching 14% in immunocompromised cohorts | +1.3% | North America, Europe | Medium term (2-4 years) |

| Telemedicine adoption lifting HSV prescription volumes by double-digits | +1.1% | Global | Short term (≤ 2 years) |

| OTC corridor expansion for low-dose topicals | +0.6% | North America, Asia Pacific | Short term (≤ 2 years) |

| CRISPR-based programs showing >99.99% viral DNA reduction in preclinical models | +2.4% | Global | Long term (≥ 4 years) |

| Collaboration between sexual-health apps & pharma enhancing patient adherence | +0.5% | Global | Short term (≤ 2 years) |

| Federal NIH funding spike for mRNA-based HSV vaccines boosting U.S. clinical pipeline | +1.0% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Acyclovir Resistance Fuels Demand for New Mechanisms

Resistance rates to acyclovir now reach 14% among immunocompromised patients, compared with <1% in healthy adults. Mutations in the UL23 thymidine-kinase gene drive this trend, prompting drug developers to test helicase-primase inhibitors such as pritelivir and ABI-5366. The CHARMD database has catalogued the accelerating mutation spectrum, underlining the need to diversify antiviral targets. A citizen petition filed with the FDA seeks expanded access to pritelivir, illustrating clinician urgency[1]U.S. Food and Drug Administration, “Citizen Petition for Pritelivir,” fda.gov.

Telemedicine Shortens Time-To-Treatment and Boosts Prescription Counts

Virtual platforms such as Lemonaid Health and Wisp provide discreet consultations that bypass stigma barriers. Patients secure same-day scripts for valacyclovir suppressive therapy or outbreak packs, often completing the care loop in under 24 hours. The format is especially valuable for uninsured users who avoid in-office visits; early data from telehealth providers show a double-digit year-on-year jump in HSV consultations, which translates to higher antiviral volumes and more consistent adherence.

OTC Switches Widen the Retail Funnel

Docosanol-based OTC creams generated USD 1.6 billion in 2021 sales and continue to expand thanks to self-care trends. Roughly half of cold-sore sufferers prefer non-prescription remedies, boosting shelf-space allocation in retail chains. Theralase’s photodynamic topical Ruvidar™ healed HSV-1 lesions in animal models after once-daily application, signalling pipeline competition within the OTC corridor.

CRISPR-Enabled Programs Reshape the Long-Term Vision

Excision BioTherapeutics reported a >99.99% cut in latent viral DNA and near elimination of shedding in rabbit keratitis studies with its EBT-104 construct. Fred Hutch researchers achieved >90% clearance of latent HSV-1 using multiplexed gRNAs delivered via AAV vectors. The NIH has placed curative strategies at the core of its 2023-2028 HSV research roadmap, ensuring multi-year funding continuity[2]National Institutes of Health, “Strategic Plan for Herpes Simplex Virus Research 2023–2028,” niaid.nih.gov.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EMA viral-load endpoint demands extend pivotal trials by 18-24 months | −0.8% | Europe | Medium term (2-4 years) |

| Generic penetration eroding brand margins in mature settings | −0.7% | North America, Europe | Short term (≤ 2 years) |

| Persistent social stigma curtailing testing uptake | −0.6% | Middle East & Africa | Long term (≥ 4 years) |

| Cold-chain logistics constraints limiting vaccine rollout | −0.5% | Rural Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EMA Virologic Benchmarks Prolong Approvals

European regulators now insist on durable suppression metrics in HSV trials, a bar that requires prolonged follow-up and larger cohorts. Assembly Biosciences must first complete Phase 1b shedding-rate read-outs for ABI-5366 before entering pivotal studies, extending launch timing by roughly two years[3]Assembly Biosciences, “Phase 1a Results for ABI-1179,” assemblybio.com. Smaller biotech firms face capital-intensive extensions that can stall programs or push them toward partnership deals.

Wide Generic Availability Compresses Brand Economics

Acyclovir and valacyclovir lost exclusivity years ago, and in the United States most prescriptions are filled with generics priced at single-digit USD per day. This price ceiling discourages incremental reformulations and redirects investment toward differentiated modalities such as vaccines or biologics. GSK, for example, is repositioning resources after pausing its subunit vaccine candidate GSK3943104 following disappointing Phase 2 data.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Virus Type: HSV-1 Prevalence Anchors Demand While HSV-2 Drives Incremental Growth

The Herpes Simplex Virus Treatment market size for HSV-1 is underpinned by 3.7 billion carriers, making it the dominant treatment universe. Although many infections are subclinical, periodic reactivations sustain topical-therapy sales and motivate suppressive oral prescriptions among high-outbreak patients. Education campaigns in Asia and Africa are lifting recognition of ocular and neonatal sequelae, which historically went untreated.

HSV-2, while infecting a smaller absolute pool of 846 million adults, generates stronger forward momentum because the virus remains a co-factor in HIV acquisition and produces more symptomatic recurrences. Rising syndromic testing uptake among sexually transmitted infection (STI) clinics in South-East Asia enriches the diagnosis funnel, translating to faster prescription growth. Clinical associations now recommend starting suppressive therapy after the second annual episode, an update that widens eligibility.

By Drug: Nucleoside Analogs Stay Central as Long-Acting Candidates Enter

First-line therapy continues to revolve around valacyclovir, whose favorable bioavailability profile supports twice-daily dosing, a key adherence advantage over five-times-daily acyclovir tablets. In practice, prescribers reserve famciclovir for patients with mild renal impairment because it maintains efficacy at lower renal-clearance thresholds.

Pipeline attention is shifting toward helicase-primase inhibitors, led by ABI-1179 and ABI-5366, which showed plasma half-lives of about four days in early studies. A weekly-pill schedule could materially raise adherence and reduce pill burden for chronic suppressive users. Gene-editing therapeutics may eventually displace chronic antivirals, but consensus among investigators places curative timelines at least five years out, given delivery-vector and immunogenicity hurdles.

By Route Of Administration: Oral Remains Preferred, Injectable and Topical Carve Niches

Oral regimens dominate the Herpes Simplex Virus Treatment market, mirroring patient preferences for convenient self-administered options. Tablets enable rapid systemic exposure needed during prodromal phases, which is crucial for suppressing replication before vesicle eruption. Hospitals reserve IV formulations for severe disseminated disease or neonatal herpes, situations requiring high systemic acyclovir levels delivered under close renal monitoring.

Topical solutions target labial outbreaks and supplemental lesion care. Ruvidar is among next-generation creams in development, leveraging photodynamic activation to accelerate lesion clearance after once-daily application. Ophthalmic gels remain a micro-market focused on herpes keratitis, where corneal scarring risk necessitates rapid local virus suppression.

By Distribution Channel: Brick-And-Mortar Leads, E-Pharmacy Accelerates

Retail chains handle the majority of herpes antiviral scripts because patients can secure therapy immediately after virtual or in-person consults. Pharmacists increasingly offer point-of-care counseling on prophylactic dosing, especially for women contemplating pregnancy.

Online pharmacies, linked tightly with telemedicine portals, are the fastest-advancing channel in the Herpes Simplex Virus Treatment market. Automated prescription fulfillment and discreet packaging align with consumer expectations of privacy. API integrations that push e-prescriptions directly into mail-order workflows shorten the time between diagnosis and drug receipt to ≤48 hours in most urban zip codes.

Geography Analysis

North America remains the revenue leader in the Herpes Simplex Virus Treatment market because of high insurance coverage, widespread HSV testing and large specialty-care networks. The NIH’s 2023-2028 strategic plan earmarks multi-year grants for curative approaches, reinforcing a deep discovery pipeline. Generic pricing pressure persists, but branded spend holds steady among suppressive-therapy users seeking convenience packs that bundle refills with telehealth follow-ups.

Asia Pacific is the fastest-growing territory. Urban populations in China and India are turning to smartphone-based teleconsultations for STI management, partly offsetting the shortage of infectious-disease specialists. Local manufacturers produce low-cost acyclovir and valacyclovir, but multinational firms are scaling co-marketing deals to introduce branded long-acting tablets as disposable incomes climb. Government-backed public-health campaigns have also broadened HSV awareness, lifting testing rates in tertiary hospitals.

Europe represents a mature but innovation-oriented landscape. EMA requirements lengthen trial timelines, yet the region hosts advanced virology labs focusing on ApoE-mediated viral-cell interactions and next-generation capsid inhibitors. Cost-effectiveness protocols drive high generic use, but national systems reimburse premium-priced options where superior suppression or adherence data exist.

Competitive Landscape

Market concentration remains moderate. GlaxoSmithKline retains a leading antiviral franchise but is reallocating resources toward next-generation biologics after halting further investment in its HSV-2 therapeutic vaccine candidate. Teva and Viatris dominate volume through extensive generic portfolios, leveraging global distribution networks to capture price-sensitive segments. Novartis ranks highest in the 2024 Access to Medicine Index for broadening treatment access in lower-income regions.

Biotechnology entrants are intensifying competition. Excision BioTherapeutics is advancing CRISPR-based curative constructs and has secured FDA orphan-drug designation for its ocular program, ensuring seven-year market exclusivity upon approval. Assembly Biosciences’ helicase-primase pipeline targets weekly oral dosing, a differentiation lever that could re-set patient adherence expectations. Moderna and BioNTech are applying validated mRNA platforms to prophylactic vaccines, adding a preventive dimension to the competitive field.

Strategic collaboration activity is rising. Assembly Biosciences inked an R&D pact with Gilead to co-develop long-acting antivirals, gaining milestone-based funding and option payments. GSK and Novartis have issued tiered-pricing commitments in selected African markets, improving availability of suppressive therapy. Meanwhile, academic-industry alliances—such as Fred Hutch linking with private-sector vector manufacturers—are accelerating translational gene-editing studies.

Herpes Simplex Virus Treatment Industry Leaders

GlaxoSmithKline plc

Teva Pharmaceutical Industries Ltd.

Viatris Inc.

Novartis AG

Fresenius SE & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Assembly Biosciences released positive Phase 1a data for ABI-1179, confirming a four-day half-life supportive of weekly dosing.

- April 2025: Theralase reported Ruvidar cleared HSV-1 lesions with once-daily topical use in mice, outperforming market-leading creams.

- February 2025: Fred Hutch researchers engineered 3D-printed skin organoids to screen 20 anti-HSV compounds, identifying several candidates with minimal cytotoxicity

- October 2024: Fred Hutch demonstrated HSV gene-drive feasibility, advancing curative gene-therapy science

- September 2024: GSK confirmed continued development of its therapeutic HSV vaccine after Phase I/II interim review

- June 2024: Assembly Biosciences dosed the first participant in its ABI-5366 Phase 1a/b study targeting recurrent genital herpes

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the herpes simplex virus (HSV) treatment market as the worldwide sales value of prescription and over-the-counter antivirals, chiefly acyclovir, valacyclovir, famciclovir, and penciclovir, formulated to suppress active or latent infections caused by HSV-1 and HSV-2 and distributed through hospital, retail, and online pharmacies. We track revenues at ex-manufacturer level, then adjust for parallel trade and typical channel margins before publishing the final figure.

Scope Exclusion: Pipeline vaccines, gene-editing cures, over-the-counter herbal or nutraceutical remedies, and diagnostic kits fall outside our sizing.

Segmentation Overview

- By Virus Type

- HSV-1

- HSV-2

- By Drug

- Acyclovir

- Valacyclovir

- Famciclovir

- Other Drugs

- By Route of Administration

- Oral

- Injectable / IV

- Topical / Dermal

- Ocular

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Drug Stores

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with infectious-disease physicians, retail pharmacists, and regional wholesalers across North America, Europe, Asia-Pacific, and Latin America help us validate utilization rates, typical treatment durations, and evolving average selling prices. Follow-up surveys with hospital procurement teams let us refresh discount assumptions and flag sudden demand swings.

Desk Research

We begin with a wide scan of reputable open data, drawing on sources such as the World Health Organization, the US Centers for Disease Control and Prevention, Eurostat trade records, ClinicalTrials.gov, and peer-reviewed journals in BMC Infectious Diseases for prevalence estimates, prescription volumes, and emerging therapy counts. Industry expenditure and shipment values are then cross-checked with customs statistics, regulatory filings, and annual reports filed to the US SEC.

To enrich numeric depth, Mordor analysts mine Dow Jones Factiva for price movements, D&B Hoovers for manufacturer financials, and Questel patent families that indicate near-term launches. This list is not exhaustive; many additional public and proprietary references inform our evidence base.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-patient build estimates demand by linking seroprevalence, symptomatic share, and treatment penetration; results are then balanced with a sampled bottom-up roll-up of leading supplier revenues to fine-tune totals. Key model drivers include diagnosed HSV incidence, median therapy days per episode, generic erosion curves, pharmacy channel mix, and regional reimbursement shifts. Multivariate regression mixed with scenario analysis projects 2026-2030 growth, with elasticities derived from our expert panel informing each variable. Where bottom-up data are patchy, we interpolate using nearby country analogs and documented launch timelines.

Data Validation & Update Cycle

Before sign-off, outputs face variance checks against insurer claims data and tender awards. An internal two-step peer review resolves anomalies, after which the model is locked. Mordor refreshes every twelve months, yet extraordinary events, such as regulatory approvals and major resistance alerts, trigger interim updates, ensuring clients receive the latest view.

Why Mordor's Herpes Simplex Virus Treatment Baseline Stands Firm

Published estimates rarely align because firms pick different product baskets, price points, and refresh cadences. Our model, anchored on treated-patient math and corroborated by supplier revenue samples, narrows uncertainty that often clouds antiviral markets.

Key gap drivers versus other publishers include: some studies fold pipeline vaccines into current value, a few assume uniform global pricing without generic discounts, while others stretch forecasts from older historical baselines that were never re-benchmarked for COVID-era telehealth uptake.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.88 B (2025) | Mordor Intelligence | |

| USD 2.80 B (2024) | Global Consultancy A | Includes candidate vaccines and relies on list prices without channel discounts |

| USD 2.56 B (2024) | Industry Research B | Excludes online pharmacy sales and assumes flat generic penetration after 2022 |

The comparison shows how our disciplined scope selection and annually refreshed assumptions yield a balanced, transparent baseline that decision-makers can retrace with confidence.

Key Questions Answered in the Report

What is driving current growth in the Herpes Simplex Virus Treatment market?

Rising acyclovir resistance, expanded telemedicine access and investment in gene-editing candidates are the primary catalysts.

How large is the Herpes Simplex Virus Treatment market today?

Recent company data place the market at USD 3.09 billion in 2026 with a forecast to reach USD 4.41 billion by 2031, a 7.37% CAGR over 2026-2031.

Which drug class is most prescribed for genital herpes?

Valacyclovir retains the widest use because twice-daily dosing achieves high plasma levels with reliable safety.

Are curative therapies close to commercial reality?

CRISPR-based programs have shown >99% latent-virus reduction in preclinical models, but human efficacy proof and delivery optimization remain multi-year hurdles.

Why are online pharmacies gaining share in herpes treatment distribution?

They dovetail with virtual consultations, offering discreet, rapid medication delivery that appeals to patients seeking privacy and convenience.

How do European regulatory requirements differ from the United States?

The EMA demands longer demonstration of sustained viral suppression, lengthening trial durations by up to two years relative to FDA pathways.

Page last updated on: