Wireless Connectivity Chipset Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.04 Billion |

| Market Size (2031) | USD 14.57 Billion |

| Growth Rate (2026 - 2031) | 7.72% CAGR |

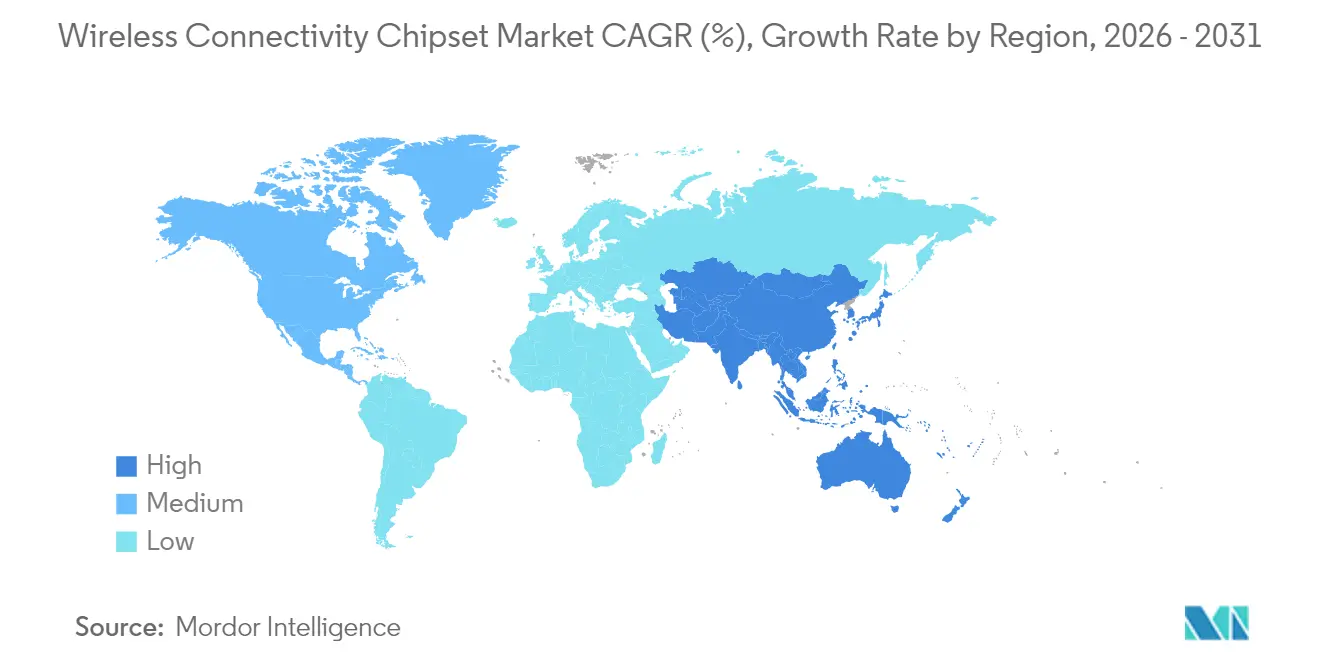

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

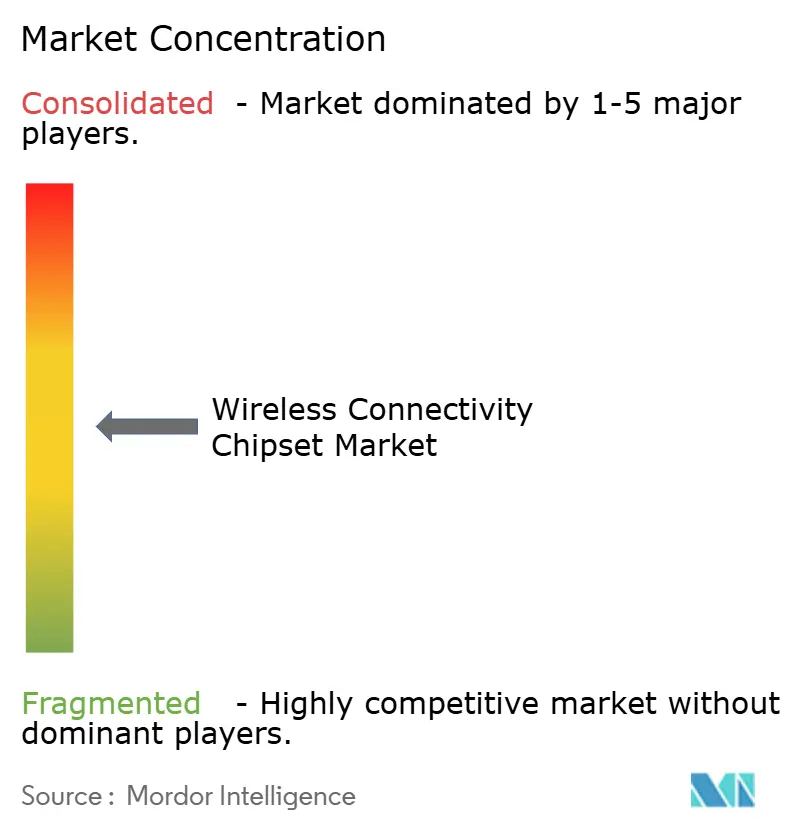

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wireless Connectivity Chipset Market Analysis by Mordor Intelligence

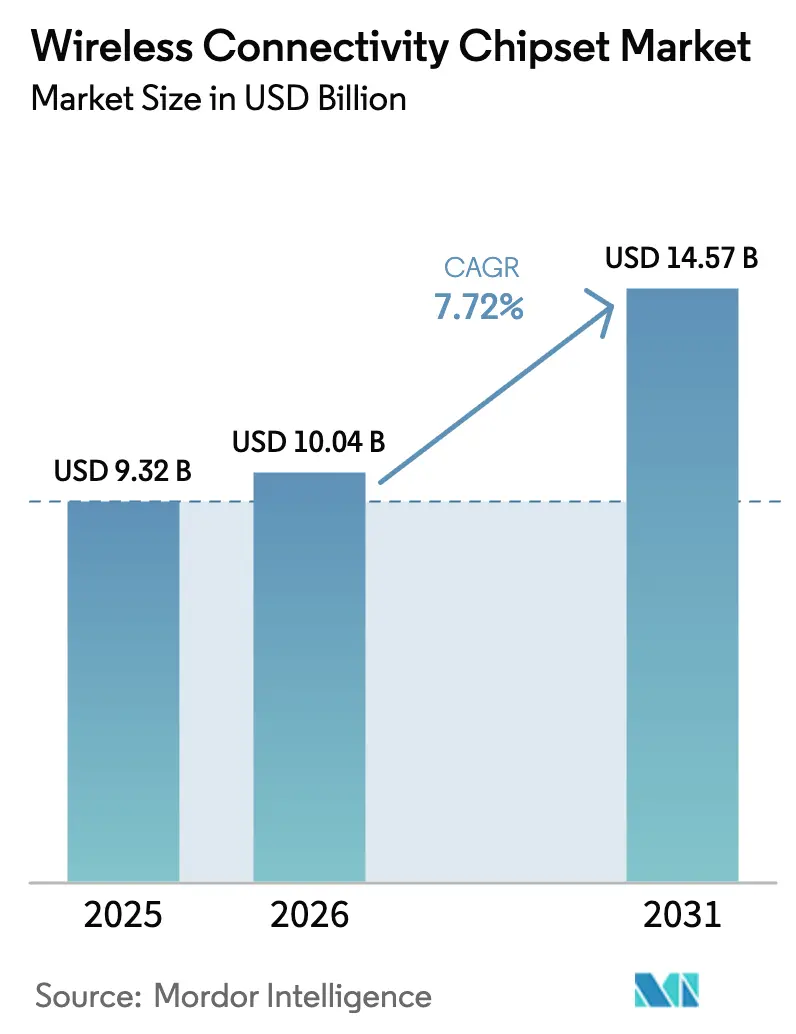

The wireless connectivity chipset market size is expected to grow from USD 9.32 billion in 2025 to USD 10.04 billion in 2026 and is forecast to reach USD 14.57 billion by 2031 at 7.72% CAGR over 2026-2031. This steady rise reflects the rapid integration of multi-protocol functionality into single-chip solutions, the increasing demand for edge-AI processing, and the surge in automotive telematics design wins. Device makers in consumer electronics, industrial automation, and mobility are converging around combo SoC platforms that lower bill-of-materials costs and shorten design cycles. In parallel, vendor consolidation and scale-driven cost reductions are reshaping competitive dynamics as suppliers race to incorporate neural-processing accelerators and meet new cybersecurity mandates, such as WPA3 and ISO 21434.

Asia-Pacific maintained a 57.30% revenue share in 2024 and is expanding at an 11.37% CAGR through 2030, buoyed by China’s large-volume IoT manufacturing clusters and Japan’s connected-vehicle innovations. Wi-Fi + Bluetooth combo silicon captured 80.30% of 2024 revenue, illustrating the market’s pivot toward integration. Low-power wireless ICs, optimized for extended battery life in IoT nodes, represent the fastest-growing product type at 9.38% CAGR. While consumer electronics still account for 52.90% of total shipments, automotive telematics and V2X endpoints are advancing at a 10.98% CAGR, signaling mobility’s growing pull on chipset roadmaps.

Key Report Takeaways

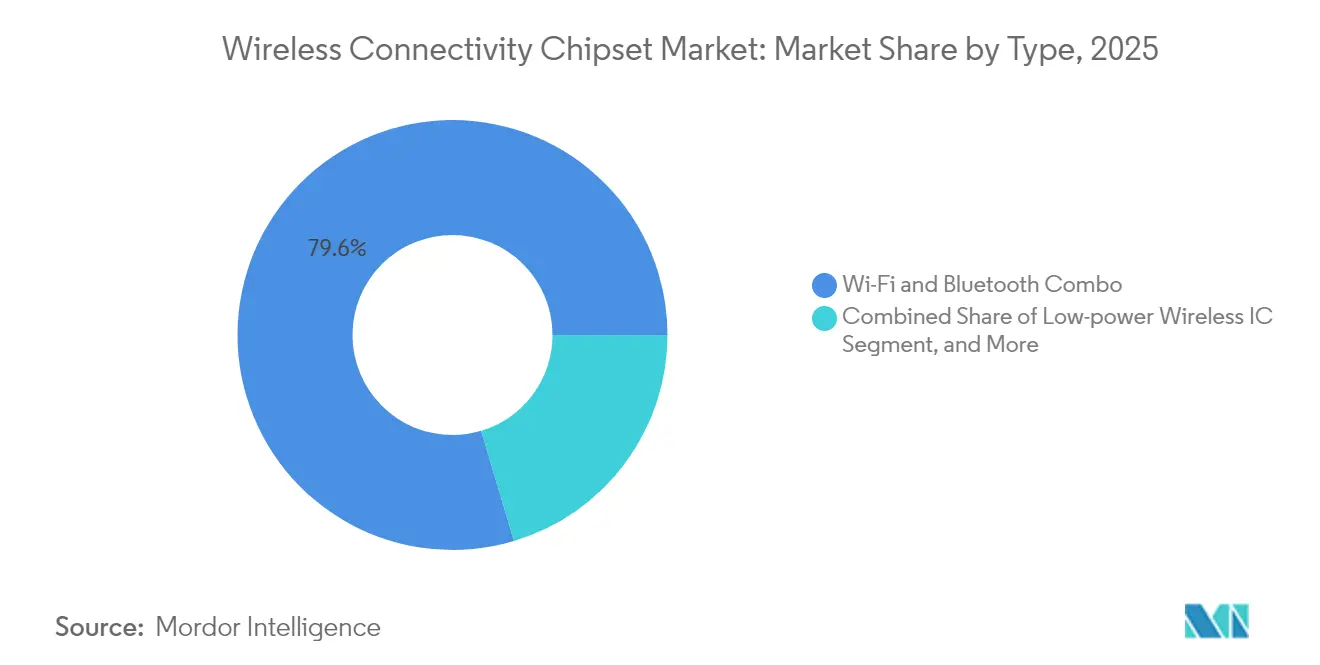

- By type, Wi-Fi + Bluetooth combo solutions held 79.62% of wireless connectivity chipset market share in 2025; low-power wireless ICs are set to post the highest 9.02% CAGR through 2031.

- By technology, Wi-Fi 5 dominated with 62.35% revenue contribution in 2025, whereas Wi-Fi 7 is forecast to grow at 9.18% CAGR between 2026-2031.

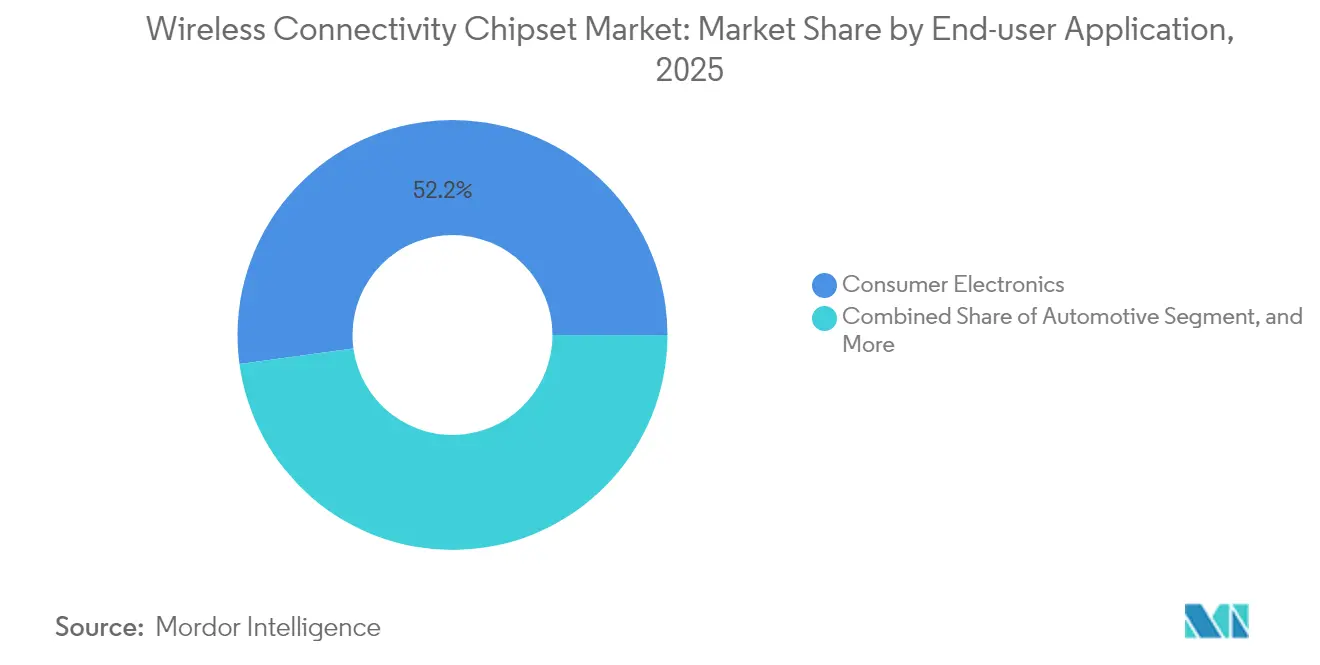

- By application, consumer electronics commanded 52.15% share of the wireless connectivity chipset market size in 2025 and automotive telematics is projected to expand at a 10.52% CAGR to 2031.

- By device category, smartphones and tablets accounted for 45.10% deployments in 2025, while automotive control units will register the fastest 10.17% CAGR through 2031.

- By geography, Asia-Pacific contributed 56.65% revenue in 2025; it will also record the quickest 10.96% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wireless Connectivity Chipset Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging IoT-device volumes across consumer and industrial sectors | +1.80% | Global, with APAC leading deployment density | Medium term (2-4 years) |

| Accelerated roll-out of Wi-Fi 6/6E/7 and Bluetooth 5.x/LE Audio | +1.50% | North America and Europe early adoption, APAC volume scaling | Short term (≤ 2 years) |

| Growth of automotive 5G/ C-V2X telematics design-wins | +1.20% | Global, with China and EU regulatory leadership | Long term (≥ 4 years) |

| Edge-AI demand for combo SoCs with integrated neural accelerators | +1.00% | North America and APAC technology centers | Medium term (2-4 years) |

| Subsidised smart-home programs and green-building regulations | +0.80% | EU and North America policy-driven markets | Long term (≥ 4 years) |

| Vendor consolidation unlocking scale-driven cost declines | +0.70% | Global supply chain optimization | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging IoT-device volumes across consumer and industrial sectors

Factory automation now specifies deterministic wireless plus traditional Wi-Fi/Bluetooth in the same die, enabling mission-critical sensor loops that previously relied on wired links.[1]Industrial Internet Consortium, “Industrial Connectivity Framework Release,” iiconsortium.org Smart-home shipments topped 1.4 billion units in 2024; each gadget embeds at least one wireless chipset, accelerating scale economies. Vendors therefore pursue unified reference designs that cater to both consumer and industrial firmware stacks, compressing development expense while widening addressable markets.

Accelerated roll-out of Wi-Fi 6/6E/7 and Bluetooth 5.x/LE Audio

Wi-Fi 7’s multi-link operation simultaneously spans 2.4, 5, and 6 GHz, creating new throughput and latency benchmarks that pull advanced RF front-ends into mainstream client devices.[2]Wi-Fi Alliance, “Wi-Fi CERTIFIED 7 Program Launches,” wi-fi.org Enterprises are refreshing access-point fleets to Wi-Fi 6E, monetizing 6 GHz spectrum for congestion-free high-density campuses. Bluetooth LE Audio’s LC3 codec, meanwhile, prompts head-unit redesigns in vehicles to offer multi-stream playback and hearing-aid compatibility, raising DSP requirements inside connectivity SoCs.

Growth of automotive 5G / C-V2X telematics design-wins

China fielded more than 200,000 C-V2X-equipped vehicles across major metro corridors in 2024, accelerating chipset design activity.[3]China Society of Automotive Engineers, “C-V2X Deployment Accelerates Across Major Cities,” sae-china.org European OEMs now mandate C-V2X readiness on new platforms, while U.S. infrastructure pilots broaden. These programs elevate the need for integrated safety isolation, secure boot, and functional-safety diagnostics directly in the radio silicon, favoring incumbents with robust automotive IP libraries.

Edge-AI demand for combo SoCs with integrated neural accelerators

Video doorbells, smart cameras, and industrial vision nodes increasingly require on-device inference to preserve privacy and trim backhaul fees. Connectivity vendors are embedding small TOPS-class NPUs next to Wi-Fi/Bluetooth radios, shrinking system BOM by removing a discrete AI coprocessor.[4]IEEE Computer Society, “Edge AI Processing in Connectivity SoCs,” computer.org Balancing heat, cost, and RF coexistence drives new layout techniques and encourages migration to 6 nm and below.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying RF-spectrum congestion in 2.4 GHz ISM band | -0.90% | Global, with urban density hotspots most affected | Short term (≤ 2 years) |

| Persistent supply-chain lead-time volatility for advanced nodes | -1.10% | Global semiconductor manufacturing constraints | Medium term (2-4 years) |

| Rising cybersecurity-compliance costs (WPA3, ISO 21434, Matter) | -0.70% | Global regulatory requirements with regional variations | Long term (≥ 4 years) |

| Inter-stack interoperability gaps slowing multi-protocol adoption | -0.60% | Global technology integration challenges | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying RF-spectrum congestion in the 2.4 GHz ISM band

Bluetooth and Wi-Fi signals collide in dense apartment blocks, pushing vendors to implement agile channel hopping and coexistence firmware. Industrial sites deploying hundreds of sensors per floor report retries that sap battery life, nudging migration toward 5 GHz and 6 GHz but adding BOM cost for tri-band front-ends.[5]FCC Office of Engineering and Technology, “RF Spectrum Congestion Analysis 2024,” fcc.gov

Persistent supply-chain lead-time volatility for advanced nodes

Limited 6 nm/7 nm capacity means connectivity parts share wafer starts with flagship mobile processors; allocation favors higher ASP segments. Lead times stretch past 30 weeks, delaying automotive ECU releases and raising buffer-stock burdens for OEMs.[6]Semiconductor Industry Association, “Global Semiconductor Sales Report Q3 2024,” semiconductors.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Combo Solutions Drive Integration Efficiency

Wi-Fi + Bluetooth combo silicon captured 79.62% wireless connectivity chipset market share in 2025. Low-power wireless ICs, although smaller today, are expected to post a 9.02% CAGR as battery-operated IoT nodes scale. Combo designs shrink PCB area and streamline certifications, letting appliance and wearables vendors ship global SKUs with uniform RF behavior.

The appetite for combo SoCs also stems from smart-home ecosystems adopting Matter, which prescribes concurrent Wi-Fi and Thread/BLE for commissioning and control. Integrating both radios into one SoC eliminates extra crystal oscillators and power rails, lowering USD cost targets for sub-USD 5 smart plugs.

By Technology Standard: Wi-Fi 7 Emergence Accelerates Performance Migration

Legacy Wi-Fi 5 still accounts for 62.35% of revenue, given its low ASPs and broad certification base, but Wi-Fi 7 chipsets will experience a 9.18% CAGR as multi-gigabit mesh and cloud gaming drive demand. Automotive infotainment is already skipping Wi-Fi 6 in favor of Wi-Fi 6E, which is 6 GHz-enabled, for interference-free back-seat streaming.

Bluetooth LE Audio is ramping up on true-wireless earbuds and infotainment, replacing classic A2DP headsets. Vendors differentiating on multipoint or Auracast broadcast features bundle new baseband logic and memory, lifting silicon content per unit.

By End-user Application: Automotive Connectivity Transforms Market Dynamics

Consumer electronics accounted for 52.15% of 2025 revenue; however, automotive telematics and V2X endpoints are expected to expand at a 10.52% CAGR, outpacing all other verticals. Electric-vehicle charging piles now require Wi-Fi for the billing back-end and PLC for grid handshakes on a single board, adding socket opportunities.

Industrial automation customers pursue deterministic wireless backbones to phase out fieldbus wiring. Connectivity silicon with time-sensitive networking extensions, therefore, gains traction in PLC controllers and robot arms.

By Device Category: Automotive Control Units Drive Next-Generation Connectivity

Smartphones and tablets currently represent 45.10% of installations, yet automotive control units are expected to enjoy a 10.17% CAGR. Software-defined vehicles rely on over-the-air updates and high-bandwidth sensor fusion, which require dual Wi-Fi plus 5G radios on zonal gateways. Vendors that harden combo chipsets for an ambient temperature range of –40 °C to 125 °C and AEC-Q100 Grade 1 qualification are prioritized first.

Wearables and hearables add ultra-low-power sub-GHz telemetry for continuous health monitoring, fuelling innovation in dual-radio minidies that pair BLE with proprietary 915 MHz backhaul.

Geography Analysis

Asia-Pacific delivered 56.65% of 2025 revenue, benefitting from China’s IoT manufacturing clusters and Japan’s connected-car R&D leadership. Government smart-city pilots drove over 500 million device activations last year. South Korea’s 5G URLLC trials underpin industrial private networks that prefer Wi-Fi 7 back-ups. India’s rural broadband schemes adopt combo chipsets in low-cost CPE, albeit with strict price caps.

North America ranks second as early Wi-Fi 6E and Wi-Fi 7 enterprise roll-outs amplify chipset refresh cycles. The FCC’s release of the full 1.2 GHz to 6 GHz band accelerated orders for tri-band access points. Canada’s critical-infrastructure projects demand FIPS-certified silicon, while Mexico’s near-shoring boom pushes automotive tier-1s to localize connectivity module lines.

Europe’s market grows steadily under sustainability and cyber-resilience mandates. The EU Cyber Resilience Act compels hardware-root-of-trust and SBOM features inside connectivity silicon, rewarding suppliers with security IP portfolios. Germany’s Industrie 4.0 labs are piloting Wi-Fi 7 deterministic scheduling, whereas the U.K. is pursuing sovereign chip design grants post-Brexit.

Competitive Landscape

Moderate consolidation characterizes the sector as scale benefits intensify at sub-7 nm. Broadcom, Qualcomm, MediaTek, and NXP leverage multi-protocol roadmaps, along with automotive-grade variants, to protect their gross margins. Smaller specialists pivot to niche domains such as satellite IoT or ultra-wideband-plus-BLE co-packaging, often licensing digital basebands from incumbents.

Technology leadership hinges on compute-connectivity fusion. FastConnect 7900 and comparable platforms embed NPU blocks to satisfy edge-video analytics, boosting ASPs but raising thermals. Patent portfolios around multi-link operation, spatial-stream management, and secure key storage shield incumbents from fast followers. Partnerships with TSMC or Samsung Foundry secure premium node access, buffering supply shocks.

White-space remains in automotive safety-certified radios meeting ISO 26262 ASIL-B/C. Early movers bundle dual CAN, Gigabit Ethernet, and Wi-Fi 7 on the same die, offering zonal ECU makers a one-vendor BOM. Extended-temperature industrial SoCs with BLE 5.4 plus 802.15.4 sidebands attract PLC vendors seeking wired-to-wireless migration paths.

Wireless Connectivity Chipset Industry Leaders

Broadcom Inc.

Qualcomm Incorporated

Intel Corporation

Texas Instruments Incorporated

MediaTek Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Broadcom committed USD 2.8 billion to expand Wi-Fi 7 and automotive C-V2X production at 6 nm, aiming to secure Tier-1 design-wins while lowering unit costs through internal capacity scale.

- September 2024: Qualcomm unveiled FastConnect 7900 integrating Wi-Fi 7, Bluetooth 5.4, and UWB, a strategic bid to anchor premium smartphone sockets and upsell automotive infotainment platforms.

- August 2024: MediaTek partnered with TSMC on 4 nm connectivity SoCs that fuse NPUs, securing early-node access to outpace rivals in power efficiency.

- July 2024: Intel acquired European connectivity IP for USD 450 million, deepening its automotive radio stack to complement Mobileye ADAS silicon.

Global Wireless Connectivity Chipset Market Report Scope

A wireless chipset is designed to be a part of the internal hardware of wireless communication procedures to allow computers or systems to communicate with each other through wireless means, such as Wi-Fi, Bluetooth, or a combination of both.

The Wireless Connectivity Chipset Market Report is Segmented by Type (Wi-Fi Standalone, Bluetooth Standalone, Wi-Fi and Bluetooth Combo, Low-power Wireless IC), Technology Standard (Wi-Fi 4, Wi-Fi 5, Wi-Fi 6/6E, Wi-Fi 7, Bluetooth Classic, Bluetooth Low-Energy 5.x), End-user Application (Consumer Electronics, Enterprise Infrastructure, Mobile Handsets, Automotive, Industrial and IIoT, Others), Device Category (Smartphones and Tablets, PCs and Laptops, Smart-Home/IoT Nodes, Networking Infrastructure, Wearables and Hearables, Automotive Control Units), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Wi-Fi Standalone |

| Bluetooth Standalone |

| Wi-Fi and Bluetooth Combo |

| Low-power Wireless IC (BLE, Zigbee, UWB) |

| Wi-Fi 4 (802.11n) |

| Wi-Fi 5 (802.11ac) |

| Wi-Fi 6 / 6E (802.11ax) |

| Wi-Fi 7 (802.11be) |

| Bluetooth Classic |

| Bluetooth Low-Energy 5.x |

| Consumer Electronics |

| Enterprise Infrastructure |

| Mobile Handsets |

| Automotive (Telematics, V2X, Infotainment) |

| Industrial and IIoT |

| Others (Healthcare, Wearables, Smart-City) |

| Smartphones and Tablets |

| PCs and Laptops |

| Smart-Home / IoT Nodes |

| Networking Infrastructure (Routers, APs) |

| Wearables and Hearables |

| Automotive Control Units |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Type | Wi-Fi Standalone | ||

| Bluetooth Standalone | |||

| Wi-Fi and Bluetooth Combo | |||

| Low-power Wireless IC (BLE, Zigbee, UWB) | |||

| By Technology Standard | Wi-Fi 4 (802.11n) | ||

| Wi-Fi 5 (802.11ac) | |||

| Wi-Fi 6 / 6E (802.11ax) | |||

| Wi-Fi 7 (802.11be) | |||

| Bluetooth Classic | |||

| Bluetooth Low-Energy 5.x | |||

| By End-user Application | Consumer Electronics | ||

| Enterprise Infrastructure | |||

| Mobile Handsets | |||

| Automotive (Telematics, V2X, Infotainment) | |||

| Industrial and IIoT | |||

| Others (Healthcare, Wearables, Smart-City) | |||

| By Device Category | Smartphones and Tablets | ||

| PCs and Laptops | |||

| Smart-Home / IoT Nodes | |||

| Networking Infrastructure (Routers, APs) | |||

| Wearables and Hearables | |||

| Automotive Control Units | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will wireless connectivity chipset revenue become by 2031?

The market is projected to reach USD 14.57 billion in 2031, reflecting an 7.72% CAGR between 2026 and 2031.

Which region will contribute the fastest incremental revenue?

Asia-Pacific posts the quickest 10.96% CAGR, powered by China's high-volume IoT production and Japan's connected-vehicle roll-outs.

What product class ships in the highest volumes today?

Wi-Fi + Bluetooth combo solutions hold 79.62% of 2025 revenue and remain the default architecture for most consumer and industrial devices.

Which end-use segment shows the strongest growth momentum?

Automotive telematics and V2X modules expand at a 10.52% CAGR as vehicle platforms embed multi-gigabit wireless links and edge-AI processing.

What technology migration is driving higher average selling prices?

The shift from Wi-Fi 5 toward Wi-Fi 6E and Wi-Fi 7, combined with adoption of Bluetooth LE Audio, lifts silicon content and premium ASPs.

How is advanced-node capacity risk influencing vendor strategy?

Ongoing 6 nm/7 nm supply tightness pushes suppliers to secure multi-foundry agreements and invest in additional in-house capacity to limit lead-time shocks.

Page last updated on: