Europe Semiconductor Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

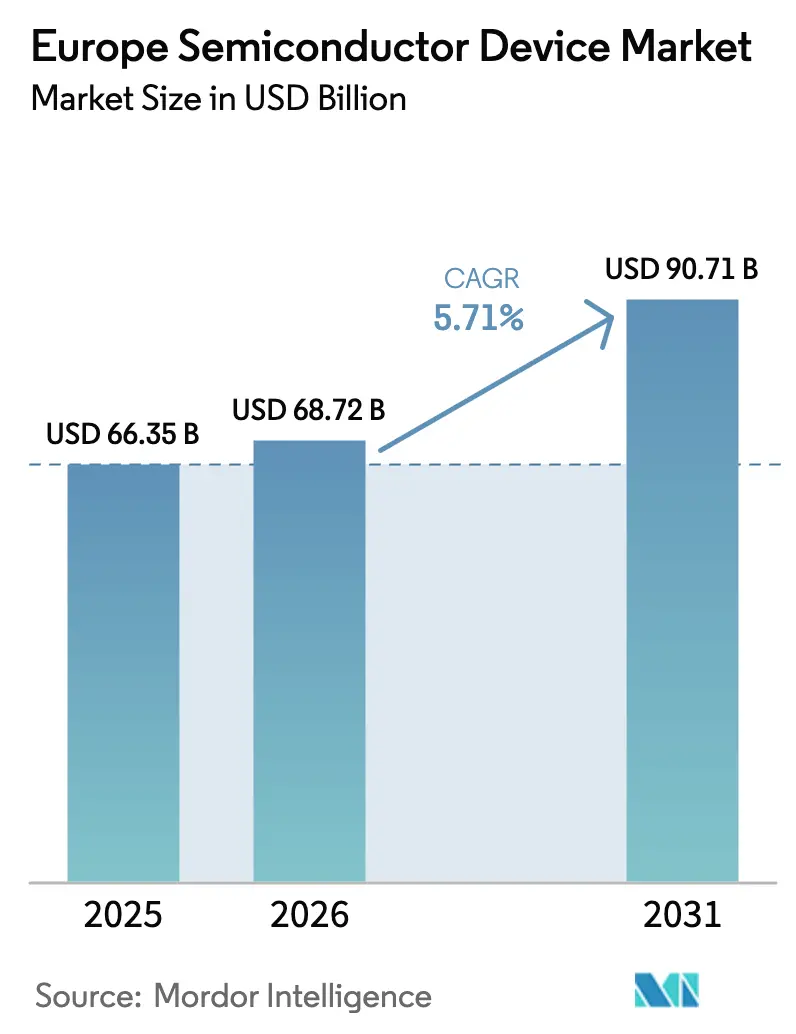

| Base Year Market Size (2025) | USD 66.35 Billion |

| Market Size (2026) | USD 68.72 Billion |

| Market Size (2031) | USD 90.71 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Semiconductor Device Market Analysis by Mordor Intelligence

The Europe Semiconductor Device Market size is projected to be USD 66.35 billion in 2025, USD 68.72 billion in 2026, and USD 90.71 billion by 2031, growing at a CAGR of 5.71% from 2026 to 2031. This advance is underwritten by the EU Chips Act, which is mobilizing EUR 43 billion (USD 48.6 billion) in combined public and private funding to double the region’s global production share by 2030. Four Integrated Production Facilities and Open EU Foundries (ESMC and Infineon in Dresden, ams-OSRAM in Regensburg, and STMicroelectronics in Catania) were designated in October 2025, strengthening local capacity for logic, power, and sensor fabrication. Mature-node automotive microcontrollers, silicon carbide traction inverters, and wide-bandgap power discretes continue to anchor volumes, yet hyperscale datacenters, quantum-computing pilot lines, and photonics-enabled medical sensors are expanding the addressable base of high-margin applications. Competitive intensity remains pronounced as incumbents race to secure EU Chips Act subsidies and lock in multi-year automotive design wins, while fabless start-ups exploit X-FAB and GlobalFoundries' open foundry services to prototype application-specific integrated circuits.

Key Report Takeaways

- Integrated circuits commanded 61.72% of Europe semiconductor device market share in 2025. Sensors and microelectromechanical systems are forecast to expand at a 6.11% CAGR through 2031.

- Integrated device manufacturers held 67.33% of Europe semiconductor device market share in 2025. Design and fabless vendors are projected to grow at a 5.89% CAGR through 2031.

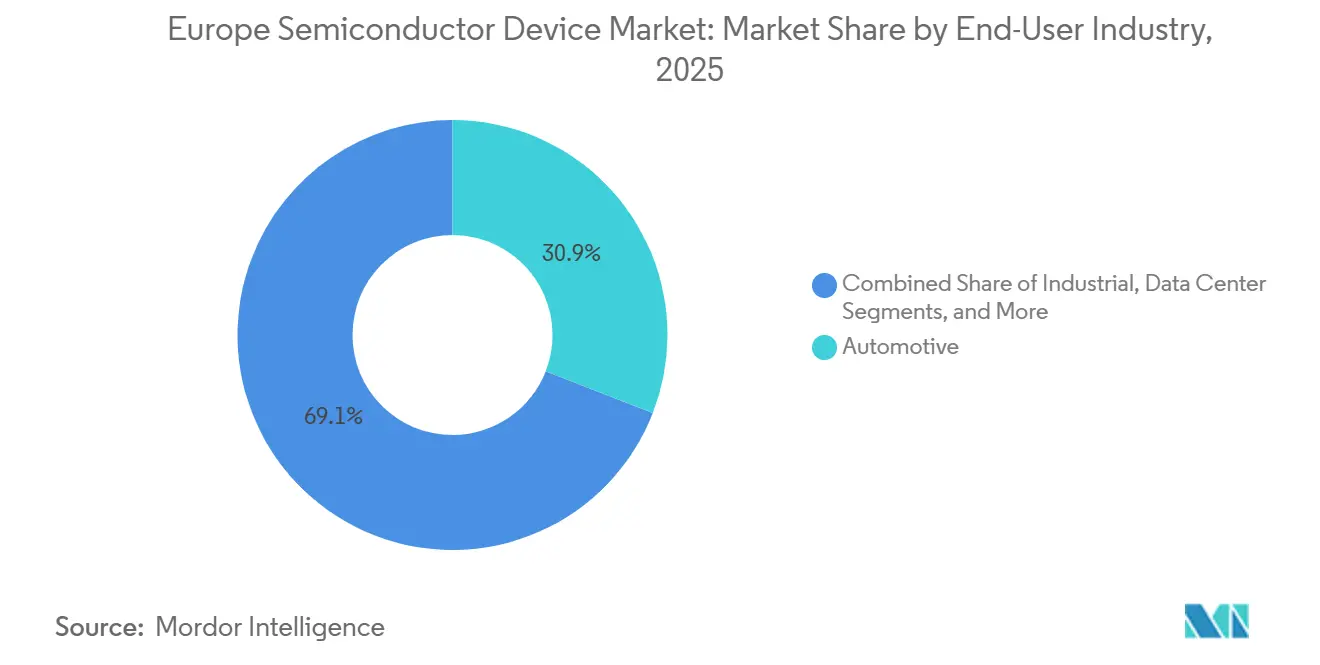

- Automotive captured 30.91% of Europe semiconductor device market share in 2025. Artificial-intelligence workloads are forecast to expand at a 7.02% CAGR through 2031.

- Technology nodes of 28 nm and above accounted for 36.08% of Europe semiconductor device market size in 2025. Five-nanometer processes are projected to grow at a 6.43% CAGR through 2031.

- Germany held 27.89% of Europe semiconductor device market share in 2025. The Netherlands is forecast to register the fastest 6.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Proportional positioning is established by comparing regional contributions against the global total, including that of Europe. The semiconductor device market share in our global report expresses these relative weights.

Europe Semiconductor Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-optimized logic IC demand from European hyperscale data centers | +1.2% | Germany, Netherlands, Ireland, France | Medium term (2-4 years) |

| Electric vehicle power electronics pulling SiC devices in Germany and France | +1.0% | Germany, France, Italy, Spain | Medium term (2-4 years) |

| Rapid 5G SA roll-outs elevating RF front-end module content per smartphone | +0.8% | Germany, United Kingdom, France, Spain | Short term (≤ 2 years) |

| EU Chips Act-funded 300mm fab expansions lowering local sourcing risk | +0.9% | Germany, France, Italy, Netherlands | Long term (≥ 4 years) |

| Quantum computing pilot lines spurring cryogenic CMOS controller demand in Finland and Netherlands | +0.4% | Finland, Netherlands, Germany | Long term (≥ 4 years) |

| Silicon photomultiplier adoption in medical imaging start-ups accelerating niche sensor volumes | +0.3% | Germany, France, United Kingdom, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Optimized Logic IC Demand From European Hyperscale Datacenters

Hyperscale operators are tripling artificial-intelligence server capacity across Europe, consolidating clusters in Germany and the Netherlands where renewable-energy credits and dense fiber interconnects reduce total cost of ownership.[1]Financial Times. “Europe to Triple AI Datacenter Capacity by 2027.” ft.com Nvidia’s June 2025 “sovereign AI” pitch persuaded policymakers to prioritize on-premise inference accelerators, reducing dependence on extra-regional clouds. Infineon expects AI-related power-management revenue to reach EUR 1.5 billion (USD 1.7 billion) in fiscal 2026 as silicon-carbide uninterrupted-power-supply modules scale to hyperscale deployments. By targeting the power and mixed-signal periphery rather than leading-edge logic, European fabs secure higher value capture even when wafer volumes migrate offshore. This dynamic also enlarges design-win opportunities for regional analog specialists that co-engineer thermal and voltage-regulation stacks with datacenter architects.

Electric-Vehicle Power Electronics Pulling SiC Devices in Germany and France

Automotive semiconductor content rose sharply after major German and French brands adopted 800-volt battery-electric architectures that mandate silicon-carbide traction inverters for fast-charging and reduced cable mass. Infineon and Stellantis signed a memorandum of understanding in 2025 to co-develop SiC power modules, accelerating CoolSiC ramp-up at Infineon’s Dresden expansion backed by EU Chips Act incentives.[2]Infineon Technologies. “CoolSiC Modules Target Datacenter UPS.” infineon.com France-based Soitec supplies Power-SOI substrates that remain foundational for low-loss power management despite fiscal-2025 inventory corrections. Multi-year wafer-supply agreements now bundle raw-wafer, epitaxy, and device procurement in a bid to secure scarce SiC capacity, tightening supplier lock-in and raising switching costs across the Europe semiconductor device market.

Rapid 5G SA Roll-outs Elevating RF Front-End Module Content per Smartphone

More than 10 European countries launched commercial 5G standalone networks by late 2025, and Ericsson, together with EE, demonstrated Advanced RAN Coordination in the United Kingdom, dynamically aggregating mid-band and millimeter-wave spectrum. Standalone deployments boost filter, switch, and power-amplifier counts per handset, lifting average selling prices for RF front-end modules. European handset brands source RF-SOI wafers from Soitec and gallium-arsenide dies from regional design houses, thereby shortening lead times and localizing value-addition. Analog IC providers further monetize this shift by integrating envelope-tracking and impedance-tuning circuits that cut power draw in spectrum-sharing scenarios.

EU Chips Act–Funded 300 mm Fab Expansions, Lowering Local Sourcing Risk

The European Semiconductor Manufacturing Company joint venture- supported by EUR 5 billion (USD 5.65 billion) in German aid- broke ground in Dresden in August 2024 and will ship 40,000 300 mm wafers monthly of 28 nm and 22 nm automotive logic by 2027. Infineon secured EUR 920 million to EUR 1 billion (USD 1.04 billion–USD 1.13 billion) for its contiguous 300 mm power-semiconductor expansion in February 2025, targeting silicon-carbide module output. While Intel’s Magdeburg project endured subsidy cuts, aggregate capacity additions meaningfully derisk long-haul supply chains for European automakers and industrial OEMs, compressing lead times and limiting exposure to geopolitical shipping disruptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight EU27 Talent Pipeline for Analog and Mixed-Signal Design Engineers | -0.6% | Germany, France, Netherlands, Italy | Medium term (2-4 years) |

| Capital-intensity barrier for new SiC and GaN substrate lines | -0.4% | Germany, France, United Kingdom | Long term (≥ 4 years) |

| PFAS phase-out under REACH raising dielectric material re-qualification costs | -0.5% | EU27-wide | Medium term (2-4 years) |

| Fragmented sub-200mm foundry ecosystem limiting IoT prototyping scalability | -0.3% | Germany, France, Italy, Spain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tight EU27 Talent Pipeline for Analog and Mixed-Signal Design Engineers

SEMI Europe’s October 2024 “Skills for Chips” report warned that 1 million semiconductor jobs must be filled by 2030, with analog and mixed-signal specialists in shortest supply.[3]SEMI. “SEMI Europe Skills for Chips Report.” semi.org Although the European Chips Skills Academy targets 100,000 trainees, the curriculum refresh lags rapid shifts toward cryogenic CMOS and wide-bandgap power modeling. German automotive suppliers cite 18-month hiring lead times for senior analog engineers, compelling reliance on contract design houses outside the region. The scarcity inflates acquisition premiums, exemplified by STMicroelectronics paying USD 950 million for NXP’s MEMS unit partly to secure 200 sensor-design engineers. Absent accelerated workforce development, fab ramps may be bottlenecked by IP validation cycles rather than equipment installations.

Capital-Intensity Barrier For New SiC And GaN Substrate Lines

Wolfspeed paused construction of its Ensdorf 200 mm SiC wafer fab in October 2024 owing to funding gaps, resuming only in January 2025 after bridge financing was secured. A greenfield SiC substrate line requires USD 1 billion-USD 1.5 billion in up-front capital, deterring venture-backed entrants. Infineon’s 300 mm GaN pilot leverages brownfield infrastructure, but full-scale GaN production still requires dedicated crystal-growth and epitaxy capacity. EU Chips Act allocations prioritize logic and sensor lines, leaving wide-bandgap substrate funding comparatively thin and forcing European device makers to import wafers from Asia-Pacific vendors, embedding currency-translation and geopolitical risk into bills of material.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Anchor Revenue, Sensors Outpace Growth

Integrated circuits held 61.72% of Europe semiconductor device market share in 2025, supported by entrenched design wins in automotive body control, industrial PLCs, and datacenter voltage regulation. STMicroelectronics’ STM32V8 microcontroller family, launched in November 2025 on an 18 nm process, targets advanced driver-assistance and electric-vehicle zone controllers.[4]STMicroelectronics. “STM32V8 Microcontroller Family Launches on 18 nm.” st.com Optoelectronics maintained a mid-teens slice, buoyed by ams-OSRAM’s EUR 5 billion (USD 5.65 billion) in 2025 design-win announcements for 2D direct time-of-flight sensing. Discrete power devices continued migrating from silicon IGBTs to silicon-carbide MOSFETs as 800-volt battery-electric platforms scale.

Sensors and microelectromechanical systems are projected to grow at a 6.11% CAGR, the fastest among device classes. Melexis posted EUR 222.2 million (USD 251.1 million) in Q3-2025 revenue, driven by rising demand for magnetic-position and current sensors. Fraunhofer IMS crossed the 1-million-unit mark for its digital silicon-photomultiplier in December 2025, validating research-institute-to-fab transfer pathways. As centralized vehicle architectures proliferate, distributed sensing becomes the primary data source, explaining why the Europe semiconductor device market size attached to sensor content is expanding faster than logic or memory subsectors.

By Business Model: IDMs Retain Scale, Fabless Vendors Gain Agility

Integrated device manufacturers controlled 67.33% of 2025 revenues. Infineon’s Dresden expansion, backed by EU Chips Act grants, underscores the sovereign-manufacturing advantage inherent in the IDM model. ON Semiconductor’s Czech site serves image-sensor and SiC-diode demand for European automakers, contributing to USD 1.76 billion Q3-2025 corporate revenue.

Design and fabless vendors will nonetheless expand at a 5.89% CAGR as X-FAB and GlobalFoundries open foundry portals democratize application-specific integrated circuit tape-outs. X-FAB’s Q3-2025 revenue reached USD 166.4 million despite soft consumer end markets, a testament to sustained automotive and industrial prototype demand. The European semiconductor device industry is witnessing hybrid strategies: Renesas’ 2024 acquisition of design-automation firm Altium illustrates vertical integration moves by microcontroller suppliers, while fabless start-ups negotiate forward-capacity contracts to protect margins in tight allocation cycles.

By End-User Industry: Automotive Dominates, Artificial Intelligence Surges

Automotive applications captured 30.91% of 2025 revenues, reinforcing Europe’s legacy in premium vehicle platforms. Melexis derived 91% of Q3-2025 revenue from automotive clients, while Elmos secured EUR 289.9 million (USD 327.6 million) in nine-month 2025 sales from ultrasonic parking-assist ICs. Analog front-ends for radar and battery-management systems drove Texas Instruments’ USD 4.15 billion Q3-2025 worldwide revenue, a meaningful portion of which flowed to European OEMs.

Artificial-intelligence datacenters represent the fastest-growing vertical at a 7.02% CAGR. Nvidia’s sovereign-AI strategy is accelerating the procurement of inference accelerators in Germany, the Netherlands, and Ireland. Infineon targets EUR 1.5 billion (USD 1.7 billion) AI-power revenue by fiscal 2026, confirming that power-management and thermal solutions, rather than digital logic, capture the incremental value pool. The Europe semiconductor device market size tied to datacenter power discretes is therefore converging with that of automotive modules.

By Technology Node: Mature Nodes Anchor Volume, Advanced Nodes Gain Share

Technology nodes greater than or equal to 28 nm produced 36.08% of 2025 revenue, reflecting automotive and industrial customers’ preference for long-lifecycle processes. The ESMC venture will ship 28 nm and 22 nm wafers beginning in 2027, consolidating Europe’s hold on mature-node automotive controllers. X-FAB remains the go-to for 180-nm to 350-nm analog prototypes, favoring design flexibility over transistor density.

Five-nanometer processes are forecast to expand at a 6.43% CAGR, driven by AMD’s Instinct MI300 accelerators and Intel’s Gaudi 3 AI chips, which are sampling with European hyperscalers. While sub-3-nm production remains concentrated in Asia-Pacific, Europe secures margins via power, analog, and sensor devices that tolerate larger geometries- even as it chips away at its leading-edge dependence through ASML’s EUV equipment monopoly.

Geography Analysis

Germany generated 27.89% of 2025 regional revenue thanks to a tight automotive-semiconductor cluster within a 200-km radius of Stuttgart and Munich. Infineon’s Dresden power-device expansion, funded by up to EUR 1 billion (USD 1.13 billion), will supply silicon-carbide modules to Volkswagen and Mercedes-Benz beginning 2026. The ESMC 28 nm-22 nm fab strengthens Germany’s dominance in mature nodes, yet documented talent shortages by SEMI Europe risk delaying volume ramps. The United Kingdom captured a mid-teens share on the back of Ericsson’s 5G infrastructure deployments and ams-OSRAM’s Regensburg optoelectronics output.

France matched the United Kingdom’s mid-teens share in 2025, propelled by STMicroelectronics’ Crolles 300 mm logic line and Soitec’s RF-SOI production. Soitec’s fiscal-2025 Q2 revenue fell to EUR 185 million (USD 209.0 million), yet Power-SOI substrates remain non-substitutable for automotive electrification. Italy and Spain each held mid-single-digit stakes, with STMicroelectronics’ Catania facility receiving Integrated Production Facility status under the EU Chips Act to reinforce power-discrete independence.

The Netherlands is forecast to advance at a 6.06% CAGR through 2031, driven by ASML’s EUR 7.5 billion (USD 8.48 billion) Q3-2025 revenue from EUV tools and ASM International’s EUR 747 million (USD 844.1 million) contribution from atomic-layer-deposition systems. Eindhoven-based NXP anchors RF and automotive-MCU design, while SemiQon’s EUR 15 million (USD 16.95 million) grant for cryogenic controllers highlights quantum-computing momentum. Smaller markets- Belgium, Finland, Austria- delivered a combined low-double-digit share, each carving defensible niches such as Melexis’ magnetic sensors and VTT’s Q50 quantum-computer pilot.

Mordor Intelligence examines the semiconductor device market across diverse other regional markets as well, including Asia, while also offering granular country-level perspectives for South Korea, China, and Japan and more.

Competitive Landscape

Top-five IDMs- Infineon, STMicroelectronics, NXP, ams-OSRAM, ON Semiconductor- together captured most of 2025 revenue, indicating moderate concentration. STMicroelectronics’ planned USD 950 million acquisition of NXP’s MEMS unit bolsters its sensor depth for automotive and industrial-Internet-of-Things platforms. Infineon is reallocating R&D toward AI datacenter power modules, aiming for EUR 1.5 billion (USD 1.7 billion) in fiscal-2026 AI power sales. Research institutes keep pressure on incumbents: Fraunhofer IMS has already produced 1 million digital SiPM dies, while SemiQon targets 200-qubit cryogenic CMOS controllers by 2027, hinting at future fabless IDM alliances.

Technology differentiation centers on wide-bandgap power devices, cryogenic analog design, and silicon photonics. Infineon began 300 mm GaN sampling in Q4-2025 to halve die cost for 48-volt converters, whereas ASML’s EUV systems extend Europe’s choke-point leverage in global logic scaling. Regulatory changes pose downside risks as SEMI forecasts EUR 500 million to EUR 1 billion in dielectric requalification costs due to the PFAS phase-out, and fragmented sub-200 mm capacity still hampers Internet-of-Things prototyping. Overall, the Europe semiconductor device market balances sovereign-manufacturing ambitions with a rich ecosystem of specialty fabs and design houses.

Europe Semiconductor Device Industry Leaders

Infineon Technologies AG

STMicroelectronics N.V.

NXP Semiconductors N.V.

ON Semiconductor Corporation

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Fraunhofer IMS announced its digital silicon-photomultiplier platform surpassed 1 million units produced, achieving a 180 kHz/mm² dark-count rate for PET and ToF imaging.

- November 2025: STMicroelectronics launched the STM32V8 microcontroller family on an 18 nm process for electric-vehicle body controllers and ADAS.

- October 2025: Infineon introduced 100-V automotive-qualified GaN power transistors for 48-V mild-hybrid converters.

- October 2025: The European Commission designated ESMC, ams-OSRAM, Infineon, and STMicroelectronics as Integrated Production Facilities under the EU Chips Act.

- September 2025: Ericsson and EE deployed Advanced RAN Coordination across United Kingdom 5G standalone networks.

Europe Semiconductor Device Market Report Scope

The Europe Semiconductor Device Market Report is Segmented by Device Type (Discrete Semiconductors, Optoelectronics, Sensors and MEMS, Integrated Circuits), Business Model (IDM, Design/Fabless Vendor), End-User Industry (Automotive, Communication, Consumer, Industrial, Computing, Data Center, AI, Government), Technology Node, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Semiconductors | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Optoelectronics | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Other Sensors and MEMS | |||

| Integrated Circuits | By IC Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| Integrated Device Manufacturer (IDM) |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Center |

| Artificial Intelligence |

| Government |

| Less than or Equal to 3nm |

| 5 nm |

| 7 nm |

| 16 nm |

| Less than or Equal to 28nm |

| Germany |

| United Kingdom |

| France |

| Italy |

| Netherlands |

| Spain |

| Rest of Europe |

| By Device Type | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Semiconductors | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Optoelectronics | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Other Sensors and MEMS | ||||

| Integrated Circuits | By IC Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Business Model | Integrated Device Manufacturer (IDM) | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Center | ||||

| Artificial Intelligence | ||||

| Government | ||||

| By Technology Node | Less than or Equal to 3nm | |||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| Less than or Equal to 28nm | ||||

| By Country | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Netherlands | ||||

| Spain | ||||

| Rest of Europe | ||||

Key Questions Answered in the Report

Which country generated the highest semiconductor-device revenue in Europe in 2025?

Germany led with 27.89% share, powered by its automotive-centric ecosystem.

What CAGR is forecast for sensors and MEMS through 2031?

Sensors and MEMS are projected to grow at 6.11% annually, outpacing all other device types.

How will the EU Chips Act influence regional capacity?

Chips Act incentives are funding multiple 300 mm fabs that will reduce sourcing risk for automotive and industrial customers from 2027 onward.

Which end-user segment is expected to grow fastest?

Artificial-intelligence datacenters are forecast to register a 7.02% CAGR as hyperscale operators triple server capacity.

What is the main restraint on Europe’s semiconductor expansion?

A shortage of analog and mixed-signal design engineers is slowing IP validation and new-product ramps.

Page last updated on: