RF Components Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

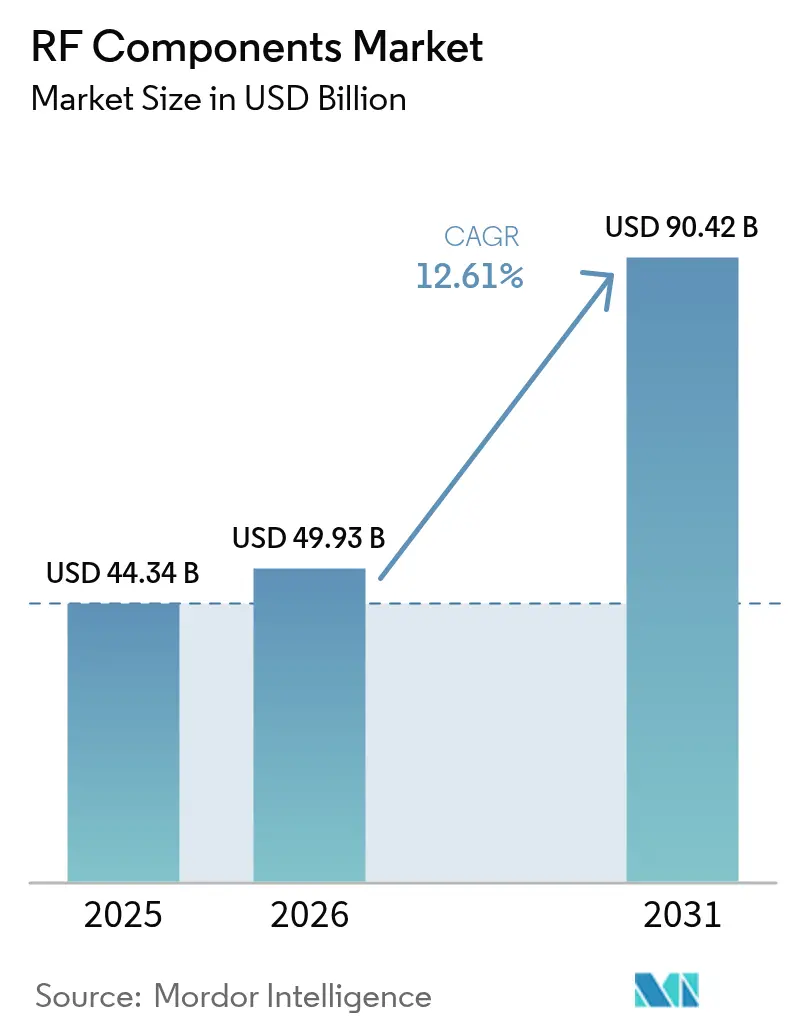

| Market Size (2026) | USD 49.93 Billion |

| Market Size (2031) | USD 90.42 Billion |

| Growth Rate (2026 - 2031) | 12.61% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

RF Components Market Analysis by Mordor Intelligence

The RF components market size is projected to be USD 44.34 billion in 2025, USD 49.93 billion in 2026, and reach USD 90.42 billion by 2031, growing at a CAGR of 12.61% from 2026 to 2031. Strong momentum stems from escalating 5G infrastructure rollouts, higher RF content per smartphone, and the diffusion of gallium-nitride power devices into base stations and automotive radar. Component vendors are repositioning portfolios toward millimeter-wave bands, where wider bandwidths unlock new revenue but intensify thermal and packaging constraints. Demand is further catalyzed by low-earth-orbit (LEO) constellations, satellite-to-smartphone links, and factory automation that relies on edge-AI mmWave sensing. Market consolidation is moderate; the top five suppliers controlled roughly 40% to 45% of global sales in 2025, and the pending Skyworks–Qorvo merger will elevate the combined share to about 25%. Simultaneously, niche specialists in tunable matching networks and gallium-nitride power amplifiers are winning share by shrinking board area and boosting efficiency. Geographically, Asia-Pacific leads on the back of China’s base-station build-out, while North America is the fastest-growing region thanks to fixed wireless access and LEO ground terminals.

Key Report Takeaways

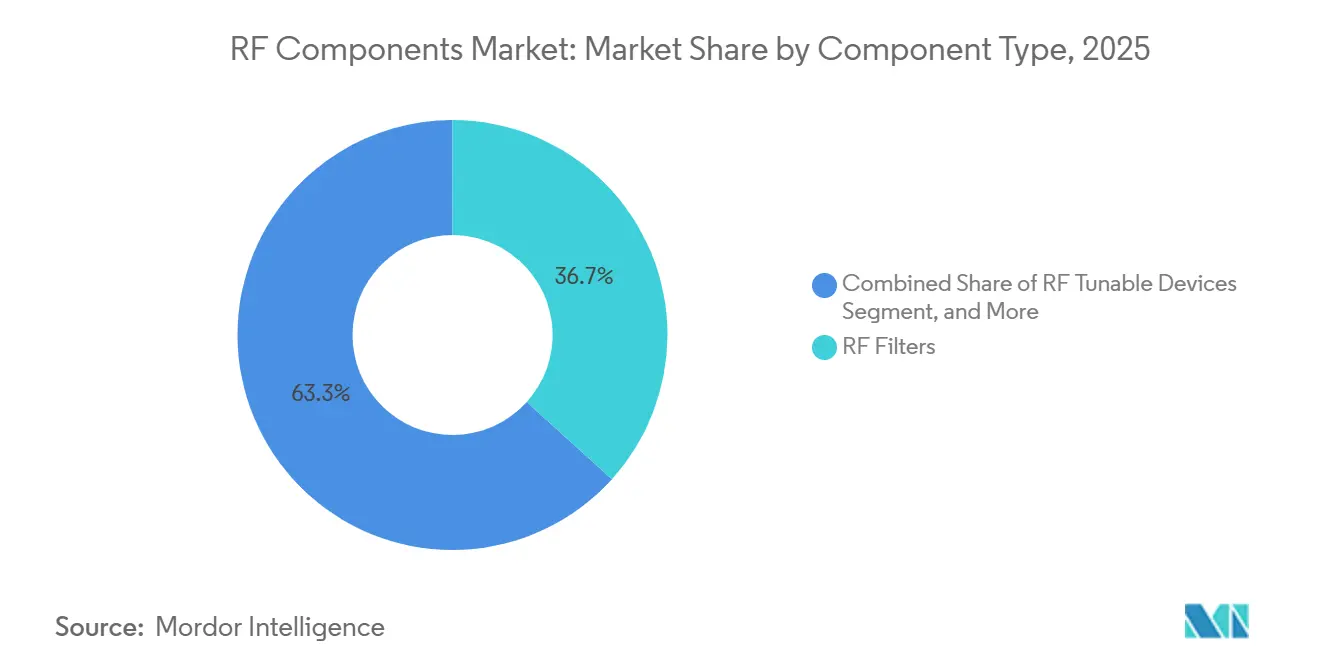

- By component type, RF filters led with 36.71% of 2025 revenue, whereas RF tunable devices are set to expand at a 13.69% CAGR to 2031.

- By frequency band, sub-6 GHz held 53.47% of the RF components market share in 2025, yet the 24-40 GHz segment is advancing at a 13.43% CAGR through 2031.

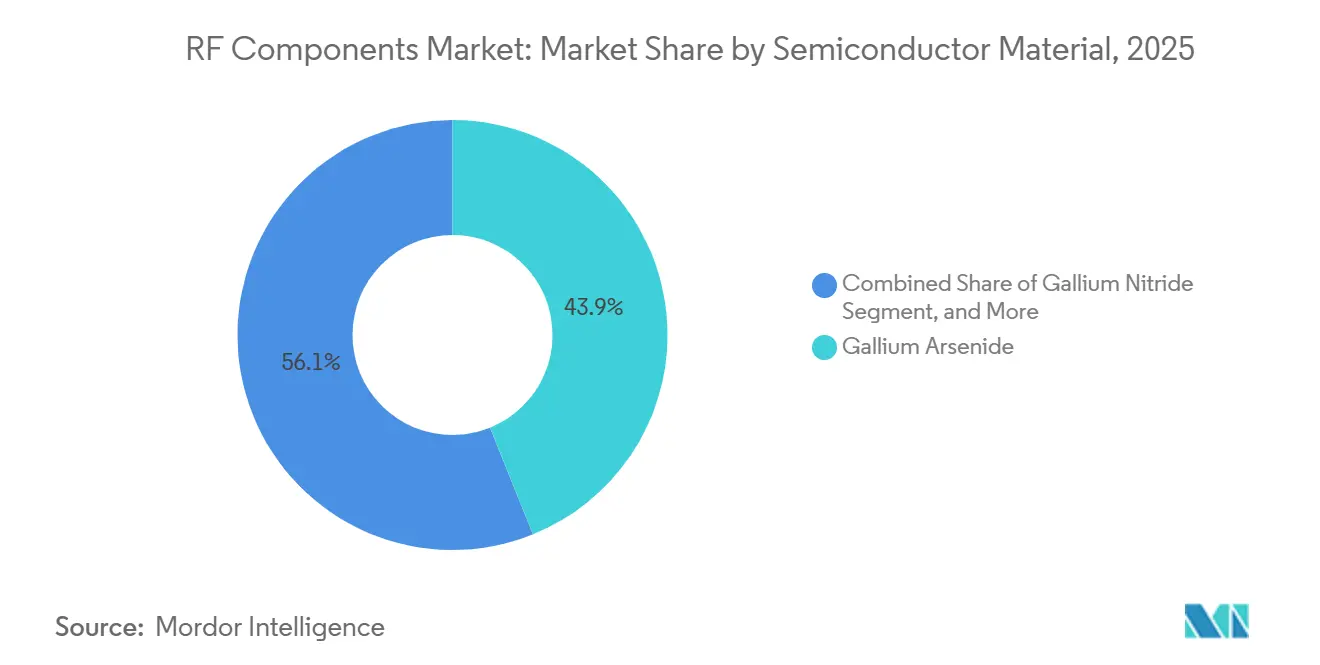

- By semiconductor material, gallium arsenide captured 43.89% of 2025 sales, while gallium nitride is progressing at a 13.47% CAGR during the forecast window.

- By end-user industry, consumer electronics accounted for 59.78% of demand in 2025, and automotive applications are climbing at a 13.66% CAGR on the strength of 77 GHz radar mandates.

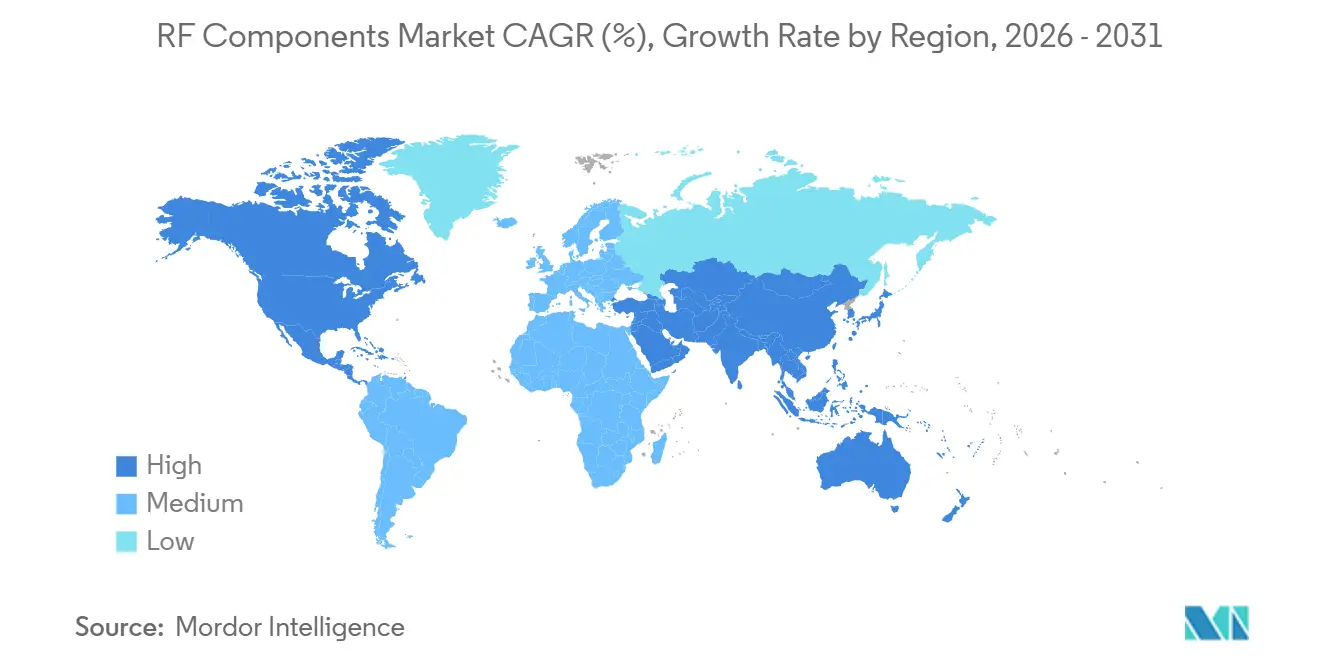

- By geography, Asia-Pacific commanded 47.71% of 2025 revenue, whereas North America is projected to record a 13.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global RF Components Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G Infrastructure Densification | +3.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Surge in RF Front-end Content per Smartphone | +2.8% | Global, led by Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Rising Automotive Radar and V2X Deployments | +2.1% | Europe, North America, China | Long term (≥ 4 years) |

| Government Funding for Space and LEO Constellations | +1.9% | North America, Europe, emerging markets | Long term (≥ 4 years) |

| Edge-AI mmWave Sensing in Smart-Factory Cobots | +1.0% | Asia-Pacific core, spill-over to Europe and North America | Medium term (2-4 years) |

| Satellite-to-Smartphone NTN Handset Design Wins | +1.6% | Global, early adoption in North America and Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Infrastructure Densification

Operators activated 1.2 million new 5G macro and small cells in 2025, and China accounted for roughly 60% of those sites.[1]GSMA Intelligence, “Global 5G Base Station Deployments and Open RAN Adoption,” gsmaintelligence.com Each massive-MIMO radio now integrates 64-256 transmit-receive chains, multiplying the number of power amplifiers, low-noise amplifiers, and antenna switches eight- to sixteen-fold compared with 4G deployments. Auctions in the 24-40 GHz range across the United States, Europe, and Japan opened 400 MHz or more of contiguous spectrum per market, which in turn is driving demand for bulk-acoustic-wave filters that can maintain low insertion loss over such wide channels. Virtualized radio access networks centralize baseband processing, enabling operators to bulk-purchase standardized RF front-ends that shorten design cycles. Small-cell build-outs along dense city corridors add another growth layer because millimeter-wave nodes need gallium-nitride power amplifiers to offset higher path loss. Together, these factors underpin a 3.2% positive swing in the market’s forecast CAGR.

Surge in RF Front-End Content Per Smartphone

Flagship 5G smartphones released in 2025 carried USD 22-28 in RF hardware, up from USD 18 in comparable 4G models, as millimeter-wave transceivers and envelope-tracking amplifiers became standard features. Mid-tier devices now embed USD 10-14 of RF content because brands are adding 5G support to handsets priced below USD 300 for growth regions such as India and Latin America.[2]Qualcomm, “Snapdragon X80 5G Modem Press Release,” qualcomm.com A single global phone must cover as many as 50 bands from 600 MHz to 41 GHz, which forces designers to add multiplexers, diplexers, and tunable aperture-matching circuits that were unnecessary a generation ago. Qualcomm’s Snapdragon X80 modem layers AI-driven impedance calibration onto this architecture, trimming insertion loss by 0.3 dB and extending battery life by 8% in field tests. Satellite connectivity agreements between AST SpaceMobile and major carriers contribute another USD 4-6 in L-band and S-band components per handset, underpinning the 2.8% uplift these devices give to the overall market CAGR.

Rising Automotive Radar and V2X Deployments

Automotive radar penetration reached 42% of global passenger-vehicle production in 2025 after the European Union mandated advanced emergency braking and lane-keeping assist for all new cars.[3]European Commission, “General Safety Regulation and Advanced Driver-Assistance Systems,” ec.europa.eu Corner and rear modules operating at 79 GHz push total radar channels per vehicle to 48-128, sharply increasing demand for silicon-germanium low-noise amplifiers with noise figures below 2 dB. Cellular-V2X modules in the 5.9 GHz band were installed in 12% of new cars in China and 8% in the United States during 2025, spurred by dedicated spectrum allocations and regulatory encouragement. The transition to 4D imaging radar doubles antenna channel counts, further accelerating unit consumption of RF front-ends. Because regulatory mandates and safety ratings make radar and V2X non-discretionary, the automotive sector adds an estimated 2.1% to the market’s compound annual growth.

Government Funding for Space and LEO Constellations

Combined public and private commitments exceeded USD 15 billion for low-earth-orbit constellations in 2025, led by Amazon’s Project Kuiper and SpaceX’s Starlink programs. The U.S. Space Force awarded USD 1.3 billion for resilient Ka- and V-band satellite-communication terminals that rely on gallium-nitride power amplifiers delivering effective isotropic radiated power above 60 dBm. Each subscriber terminal houses 256-1,024 phased-array elements, creating a step-function increase in component demand as user counts scale from tens of thousands to millions. The International Telecommunication Union’s recent spectrum allocations between 17.7 GHz and 21.2 GHz require redesigns of ground equipment with wider bandwidth filters, further boosting supplier pipelines. Handsets prepared for satellite-to-smartphone service add USD 5-8 in incremental RF content, together explaining the 1.9% positive impact this funding wave has on the market’s CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for GaN and GaAs Wafer Fabs | -1.8% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Thermal-Management Challenges above 28 GHz | -1.2% | Global, concentrated in millimeter-wave deployments | Medium term (2-4 years) |

| Export-Control Tightening on Ultra-Wideband Chips | -0.9% | Asia-Pacific, North America, Europe | Short term (≤ 2 years) |

| Shortage of High-Q Dielectric Materials | -0.7% | Global, supply chain concentrated in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for GaN and GaAs Wafer Fabs

Wolfspeed’s Mohawk Valley fab demanded USD 6.5 billion to ramp 200 mm silicon-carbide wafers, with clean rooms, epitaxial reactors, and metrology tools absorbing roughly three-quarters of that budget. Qorvo invested more than USD 1 billion to expand gallium-nitride capacity, but underutilization during ramp-up trimmed gross margin by 3 percentage points in fiscal 2025. A state-of-the-art gallium-arsenide line capable of 20,000 wafers per month costs USD 800 million-USD 1.2 billion and often needs 18-24 months to raise yields above 85%. Financing hurdles restrict new entrants, concentrating supply among a handful of incumbents and lengthening delivery lead times when demand spikes. These economic barriers cut 1.8% from the market’s projected CAGR.

Thermal-Management Challenges Above 28 GHz

Millimeter-wave power amplifiers dissipate 8-12 W per channel in continuous transmission, quickly pushing junction temperatures above 150 °C and degrading mean time to failure below 10,000 hours without enhanced cooling. Flip-chip packages with embedded copper heat spreaders shave thermal resistance but raise module thickness by 0.5 mm and assembly cost by about 20%. Graphene-enhanced interface materials offer five-fold higher conductivity than silicone pads yet remain three- to four-times more expensive, constraining their use to premium gear. Liquid-cooled radio units support power densities beyond 15 W/cm² but add USD 200-300 in site-level costs, limiting adoption to capacity-critical urban cells. These cost-thermal trade-offs subtract 1.2% from the overall market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Tunable Devices Reshape Front-End Economics

RF filters retained the largest RF components market share at 36.71% in 2025, underscoring their pivotal role in separating transmit and receive paths across more than fifty cellular and Wi-Fi bands that now coexist inside a flagship handset. Sales momentum, however, is tilting toward tunable devices, which are forecast to post a 13.69% CAGR through 2031 as dynamic impedance networks begin replacing multiple discrete filters in premium phones. Power amplifiers represented roughly 28% of 2025 revenue and are migrating from gallium-arsenide to gallium-nitride die in base stations to push efficiencies past 50%, a switch that lifts average selling prices by 40%-60%. Antenna switches, about 18% of the total, are being absorbed into single-package front-end modules, compressing discrete volumes even as board density rises. Low-noise amplifiers held near 12% but are inching upward because 5G diversity chains demand extra receive paths.

The RF components market is at an inflection point where handset makers would rather pay a premium for software-controlled tuners that collapse signal paths than keep stacking fixed filters. Qualcomm’s Snapdragon X80 modem already embeds on-die tunable capacitors that cut insertion loss by 0.3 dB and extend battery life by 8% in field tests. Standards pressure adds to the push; 3GPP Release 18 allows sixteen-carrier aggregation combinations, and Wi-Fi 7 forces coexistence filtering below 1.5 dB insertion loss, raising the bar for high-Q bulk-acoustic-wave designs. Satellite-to-smartphone features tack on L-band and S-band paths worth another USD 4-6 in components per device, further favoring reconfigurable architectures. As a result, tunable solutions are set to capture a growing slice of value even if their absolute unit count lags traditional filters.

By Frequency Band: Millimeter-Wave Momentum Accelerates

Within the RF components market size broken down by spectrum, the sub-6 GHz tier accounted for 53.47% of revenue in 2025, reflecting its coverage advantage and installed-base inertia. Yet growth in this range is moderating to single digits as operators exhaust available spectrum and chase added capacity elsewhere. The 6-24 GHz mid-band, which held roughly 22% of sales in 2025, is expanding at a mid-teens pace because C-band allocations deliver an attractive blend of reach and throughput. Even so, the spotlight is on millimeter-wave, where the 24-40 GHz slice is advancing at a 13.43% CAGR thanks to fixed wireless access rollouts and dense urban 5G nodes.

Momentum above 24 GHz stems from generous channel widths released by regulators; the Federal Communications Commission alone freed 400 MHz of contiguous spectrum in the 24.25-25.25 GHz window. Operators leverage those blocks for 800-MHz carriers that support peak speeds topping 5 Gbps, a setting that forces wideband power amplifiers and low-noise amplifiers with sub-3 dB noise figures. Customer-premises equipment is equally component-hungry, housing 256-512 phased-array elements that convert into 1,024-2,048 RF parts per unit. Automotive radar echoes the same shift, as 79 GHz systems replace 77 GHz units to secure sub-1° angular resolution in city traffic. Backhaul links in the 70-90 GHz E-band add another high-frequency pull, increasing the addressable opportunity for suppliers tuned to millimeter-wave designs.

By Semiconductor Material: GaN Gains on Efficiency Mandate

Gallium-arsenide maintained a commanding 43.89% share of 2025 revenue, supported by decades-old process knowledge and broad adoption in handset power amplifiers. Silicon devices followed close behind, near 30%, because they remain the low-cost choice for sub-6 GHz low-noise and switch applications. Silicon-germanium, at roughly 8%, is carving a profitable niche in automotive radar where its CMOS compatibility enables monolithic integration that trims module size by about one-third. Despite gallium-arsenide’s current scale, operator focus on energy savings is accelerating its displacement in infrastructure gear.

Gallium-nitride supplies the efficiency leap that base-station vendors need, and its 13.47% forecast CAGR makes it the fastest-growing slice of the RF components market. Wolfspeed’s Mohawk Valley fab is ramping 200 mm silicon-carbide wafers that boost thermal conductivity three-fold versus gallium-arsenide, enabling power densities above 10 W/mm. Qorvo’s USD 1 billion North Carolina expansion concentrates on 24-40 GHz amplifiers, shrinking lead times for OEMs. Silicon-germanium’s resurgence is also notable; its low noise figure fits 4D imaging radar, and Tier-1 suppliers appreciate the streamlined supply chain delivered by CMOS-compatible flows. Looking ahead, gallium-nitride could reach 5%-8% of handset power-amplifier units by 2028 as envelope tracking and dynamic voltage scaling narrow the cost gap.

By End-User Industry: Automotive Overtakes Telecom Growth

Consumer electronics dominated spend with 59.78% of 2025 sales, buoyed by high 5G handset volumes and a steady USD 22-28 bill of material for flagship RF sections. Replacement cycles, though, are lengthening, and RF content per premium device is plateauing, which eases its growth rate into low double digits. Telecommunication infrastructure comprised about 18% of revenue and will largely shadow overall market expansion as operators balance macro-cell upgrades with small-cell densification. Aerospace and defense, near 8%, is widening at mid-teens rates due to Ka- and V-band satcom terminals that need gallium-nitride amplifiers rated above 60 dBm EIRP.

Automotive stands out with a 13.66% CAGR through 2031, quickly narrowing the gap with consumer electronics. Radar became standard in 42% of passenger vehicles during 2025 after the European Union mandated advanced emergency braking and lane-keeping assist. Corner and rear 79 GHz units raise per-car channel counts to 48-128, swelling demand for silicon-germanium low-noise amplifiers. Cellular-V2X modules in the 5.9 GHz band reached 12% penetration in new Chinese vehicles and 8% in U.S. models amid dedicated spectrum allocations. Industrial automation, still under 6%, also chips in double-digit growth as edge-AI cobots adopt millimeter-wave sensors for collision avoidance, ensuring that the RF components market remains diversified across multiple end uses.

Geography Analysis

Asia-Pacific held the largest RF components market share at 47.71% in 2025, powered by China’s rollout of 1.2 million 5G base stations and Taiwan’s dominance in bulk-acoustic-wave filter fabrication. Beijing earmarked RMB 50 billion (USD 7 billion) in subsidies for millimeter-wave deployments that require gallium-nitride amplifiers with greater than 50% efficiency. Japan’s early allocation of 28 GHz spectrum enabled NTT Docomo and SoftBank to commercialize services in Tokyo and Osaka during 2025, lifting demand for phased-array modules that host 64-128 radiating elements. South Korea invested USD 200 million in sub-terahertz research during 2025, positioning local firms for future 6G opportunities. These developments keep the region’s RF components market size on a solid double-digit growth path through 2031.

North America is the fastest-growing geography, projected at a 13.62% CAGR as operators lean on fixed-wireless access and satellite broadband. Carriers installed more than 3 million millimeter-wave customer-premises units in 2025, each carrying 256-512 phased-array elements that translate to over 1,000 RF parts per device. Amazon’s Project Kuiper and SpaceX’s Starlink together committed in excess of USD 15 billion for low-earth-orbit constellations, a catalyst that will require millions of Ka- and V-band ground terminals by 2028. The U.S. Space Force added another USD 1.3 billion by awarding contracts for resilient satellite-communication hardware that depends on gallium-nitride power amplifiers with effective isotropic radiated power above 60 dBm.

Europe accounted for about 22% of global revenue in 2025, but spectrum fragmentation tempered uptake until the 26 GHz band was harmonized across member states in 2024. Germany’s EUR 1.2 billion (USD 1.3 billion) auction and the United Kingdom’s rural fixed-wireless trials have since sparked orders for outdoor CPE that integrate wideband filters and high-efficiency amplifiers. South America and the Middle East and Africa together remained below 10% of the RF components market size, although double-digit gains are emerging as Brazil’s Anatel and Saudi Arabia’s regulator opened 3.5 GHz and 26 GHz bands in 2024 and 2025 respectively. Continued spectrum releases and falling device costs are expected to accelerate adoption in these late-moving regions over the forecast window.

Competitive Landscape

The top five vendors Broadcom, Skyworks, Qorvo, Murata, and Qualcomm controlled roughly 40% to 45% of 2025 sales, signaling moderate concentration in the RF components market share. In October 2025 Skyworks and Qorvo announced a USD 22 billion merger that would lift the combined entity to about 25% of global revenue once regulatory approvals arrive in early 2027. This scale gives the new firm unmatched breadth across filters, amplifiers, and antenna switches. Murata continues to lead in bulk-acoustic-wave filters, while Broadcom dominates Wi-Fi front-end modules thanks to captive access to advanced packaging lines. Qualcomm retains leadership in smartphone front-end platforms through tight integration with its Snapdragon modem roadmap.

Vertical integration is the primary strategic theme as suppliers seek to own the entire signal chain from antenna to baseband. Broadcom deepened its stack by buying Brocade’s wireless assets in 2024, adding specialized RF firmware to its portfolio. NXP stepped into automotive radar the same year by acquiring a silicon-germanium design house, aligning with its microcontroller franchise. Patent filings on reconfigurable filters and tunable matching networks jumped 35% during 2024-2025, reflecting a race toward software-defined front-ends. Packaging innovation also differentiates leaders; co-packaged optics and heterogeneous system-in-package modules now lower insertion loss by up to 0.8 dB and trim thermal resistance 20%.

White-space contenders are capitalizing on niches that giants overlook. Cavendish Kinetics and WiSpry supply micro-electromechanical-system capacitors that shrink handset board area 20%-25% by replacing fixed filters. Foundries WIN Semiconductors and MACOM offer 200 mm GaAs and GaN wafers with lead times under 12 weeks, winning base-station amplifier business that integrated device manufacturers cannot serve quickly. Chinese players such as Huawei’s HiSilicon and MediaTek are investing in gallium-nitride power stages but remain bound by advanced-node export rules, which limits competition above 24 GHz. Collectively, these dynamics reinforce a moderately consolidated market where scale, process ownership, and packaging know-how determine long-term advantage.

RF Components Industry Leaders

Broadcom Inc.

Skyworks Solutions Inc.

Qorvo Inc.

Murata Manufacturing Co., Ltd.

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Skyworks and Qorvo signed a definitive USD 22 billion merger agreement, targeting closure in early 2027 and USD 300 million in annual synergies by 2028.

- September 2025: Wolfspeed opened its USD 6.5 billion Mohawk Valley fab, starting 200 mm SiC wafer output with 78% initial yields for 600-V GaN-on-SiC devices.

- August 2025: Murata committed USD 300 million to expand bulk-acoustic-wave filter capacity in Japan, boosting output 20% by mid-2026.

- July 2025: NXP released a 77-81 GHz automotive radar transceiver integrating 4 TX and 16 RX channels, cutting BOM cost 25%.

Global RF Components Market Report Scope

The RF Components Market Report is Segmented by Component Type (Power Amplifiers, RF Filters, Antenna Switches, Low-Noise Amplifiers, RF Tunable Devices), Frequency Band (Sub-6 GHz, 6-24 GHz, 24-40 GHz, 40-100 GHz), Semiconductor Material (Gallium Arsenide, Silicon, Gallium Nitride, Silicon-Germanium), End-User Industry (Consumer Electronics, Telecommunication, Automotive, Aerospace and Defense, Industrial Automation), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Power Amplifiers |

| RF Filters |

| Antenna Switches |

| Low-Noise Amplifiers |

| RF Tunable Devices |

| Sub-6 GHz |

| 6-24 GHz |

| 24-40 GHz |

| 40-100 GHz |

| Gallium Arsenide |

| Silicon |

| Gallium Nitride |

| Silicon-Germanium |

| Consumer Electronics |

| Telecommunication |

| Automotive |

| Aerospace and Defense |

| Industrial Automation |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component Type | Power Amplifiers | ||

| RF Filters | |||

| Antenna Switches | |||

| Low-Noise Amplifiers | |||

| RF Tunable Devices | |||

| By Frequency Band | Sub-6 GHz | ||

| 6-24 GHz | |||

| 24-40 GHz | |||

| 40-100 GHz | |||

| By Semiconductor Material | Gallium Arsenide | ||

| Silicon | |||

| Gallium Nitride | |||

| Silicon-Germanium | |||

| By End-User Industry | Consumer Electronics | ||

| Telecommunication | |||

| Automotive | |||

| Aerospace and Defense | |||

| Industrial Automation | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will global demand for GaN-based RF devices become by 2031?

GaN components are projected to grow at a 13.47% CAGR, outpacing the overall RF components market, as base stations above 24 GHz and automotive radar prioritize efficiency.

Which region is expected to post the fastest growth in component consumption?

North America leads with a projected 13.62% CAGR through 2031, driven by fixed wireless access rollouts and expanding ground terminals for LEO constellations.

What is driving the shift toward tunable RF front-ends in smartphones?

The need to support up to 50 bands per global device, plus emerging L- and S-band satellite links, is elevating demand for dynamic impedance matching that can replace multiple fixed filters.

How will the Skyworks–Qorvo merger affect competitive dynamics?

Once completed, the combined entity would control about 25% of worldwide revenue, giving it unmatched scale in filters and amplifiers and prompting rivals to differentiate through GaN and tunable technologies.

Which automotive trends are most supportive of RF component growth?

Mandated 77 GHz and 79 GHz radar for safety systems and increasing adoption of 5.9 GHz Cellular-V2X modules are lifting component counts to 48-128 per vehicle.

What thermal solutions are emerging for millimeter-wave radios?

Flip-chip packages with copper spreaders and, in extreme cases, liquid-cooled radio units are being deployed to manage power densities above 15 W/cm² in mmWave base stations.

Page last updated on: