Wi-Fi Chipset Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.24 Billion |

| Market Size (2031) | USD 31.27 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

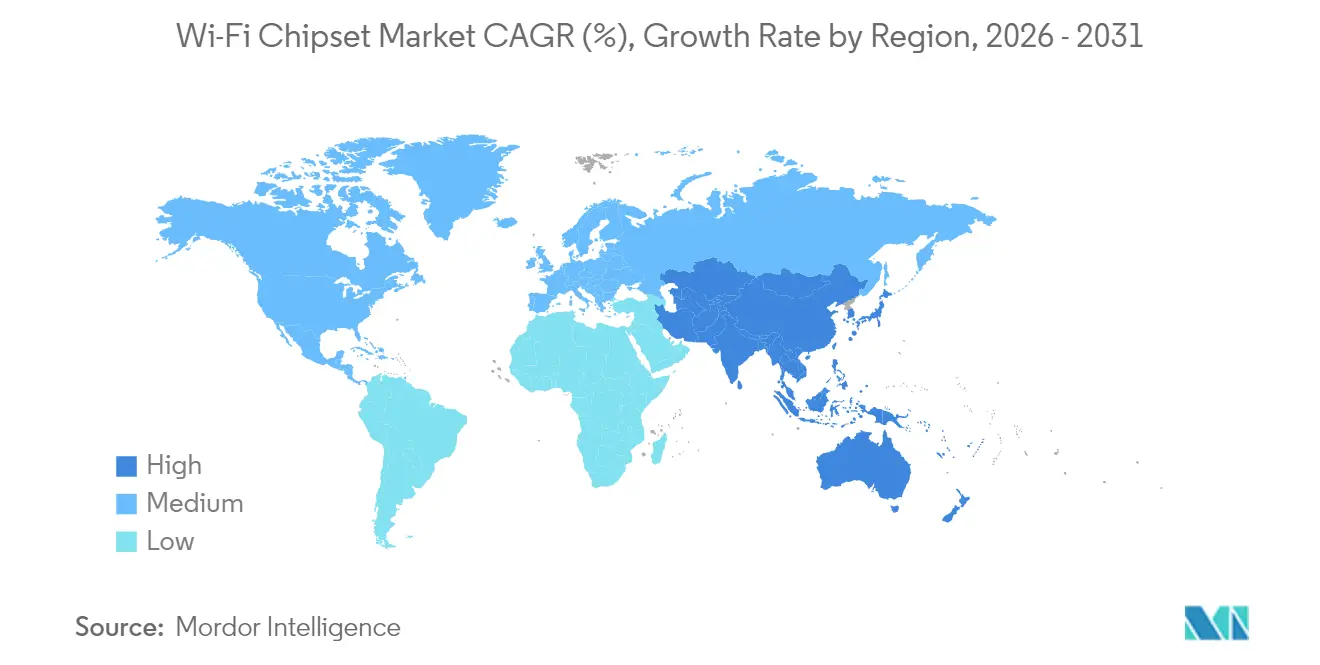

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wi-Fi Chipset Market Analysis by Mordor Intelligence

The Wi-Fi chipset market size is expected to grow from USD 21.90 billion in 2025 to USD 23.24 billion in 2026 and is forecast to reach USD 31.27 billion by 2031 at 6.12% CAGR over 2026-2031. Expansion aligns with the shift from legacy standards toward Wi-Fi 6, Wi-Fi 6E, and Wi-Fi 7, fueled by enterprise digital-first strategies, high-bandwidth consumer electronics, and the need for dense, low-latency connectivity in public venues.[1]Source: Wi-Fi Alliance, “Wi-Fi 6 and Wi-Fi 6E Drive Global Market Opportunities,” wi-fi.orgSemiconductor vendors with access to advanced process nodes secure early wins as Wi-Fi 7 design activity accelerates, while demand for power-efficient chipsets in smart-home and industrial IoT devices deepens supplier pipelines. The Asia-Pacific production ecosystem keeps bill-of-materials costs low and shortens lead times, allowing regional OEMs to launch mesh gateways and multi-user MIMO routers at price points that drive mass adoption. Automotive infotainment projects and V2X pilots are converting backlogs into volume orders, giving the Wi-Fi chipset market an additional growth lever across the latter half of the forecast period. Vendor competition centers on integrating Wi-Fi, Bluetooth, Thread, and Ultra-Wideband into single packages that simplify board layouts for device makers.

Key Report Takeaways

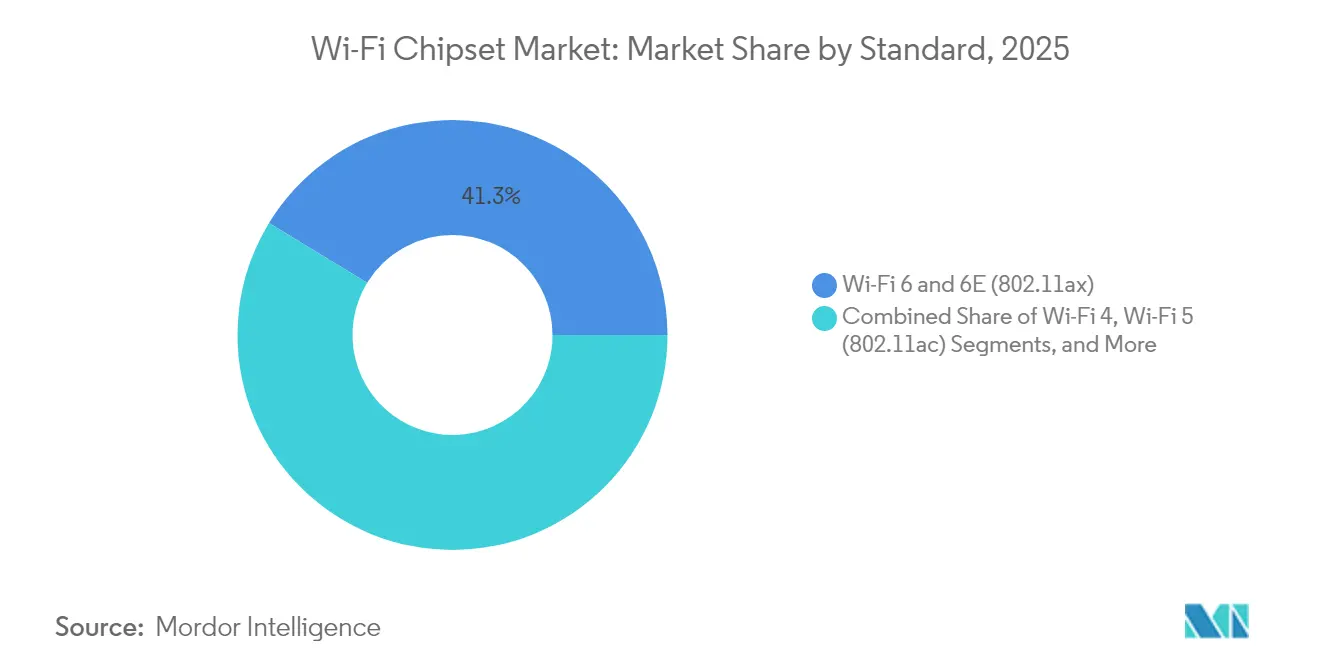

- By standard, Wi-Fi 6/6E led with a 41.27% revenue share in 2025; the “Others” category, anchored by Wi-Fi 7, is forecast to expand at a 6.72% CAGR to 2031.

- By MIMO configuration, MU-MIMO captured 60.65% of the Wi-Fi chipset market share in 2025 and also registers the highest projected 6.61% CAGR through 2031.

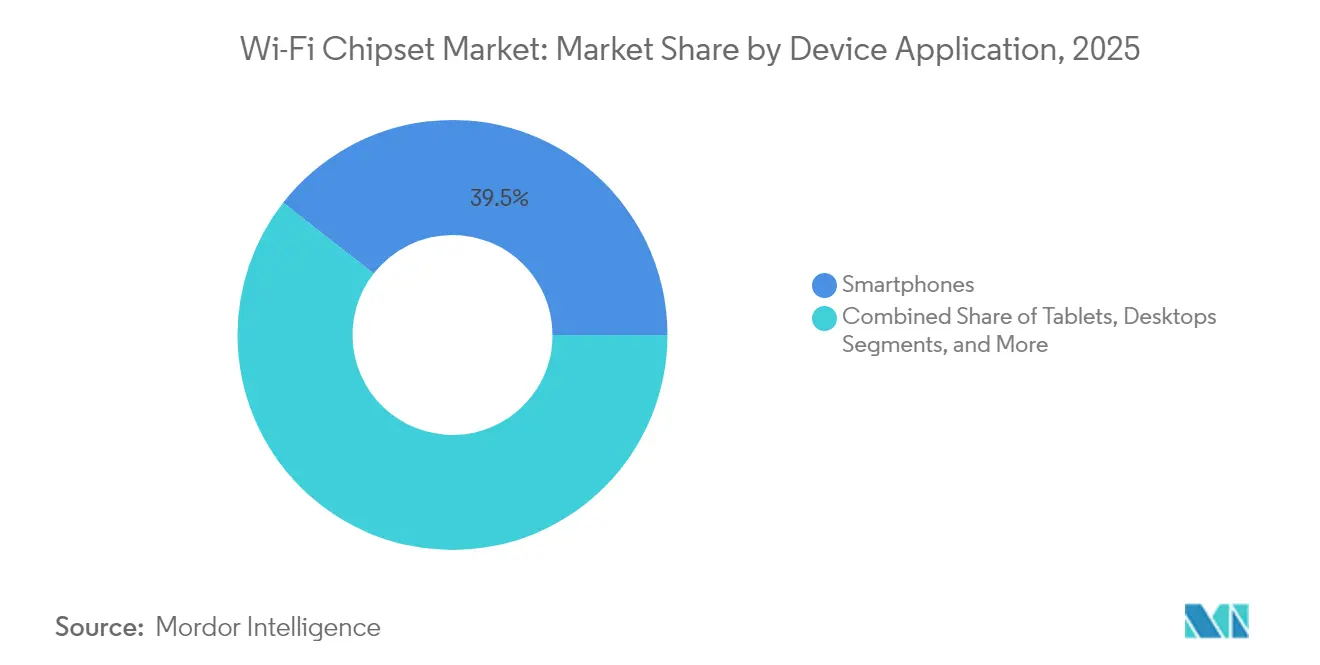

- By device application, smartphones accounted for 39.45% of the Wi-Fi chipset market size in 2025, while the router and broadband gateway segment records the fastest 7.76% CAGR over 2026-2031.

- By end-user, residential consumer electronics held a 60.82% share in 2025; automotive is poised for a 7.95% CAGR, the steepest among all categories.

- By geography, Asia-Pacific commanded 43.05% of 2025 shipments and continues to be the fastest-growing region at a 7.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wi-Fi Chipset Market Trends and Insights

Driver Imapct Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Proliferation of public Wi-Fi hotspots and IoT connections | +1.2% | Global, Asia-Pacific and North America lead | Medium term (2-4 years) |

| Rising internet penetration and demand for high-speed connectivity | +1.0% | Global, strongest in emerging markets | Long term (≥ 4 years) |

| Rapid adoption of Wi-Fi 6/6E in enterprise networks | +1.5% | North America and Europe lead, Asia-Pacific follows | Short term (≤ 2 years) |

| Growth in smart-home devices and residential mesh networking | +0.9% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Integration of Wi-Fi HaLow for low-power industrial IoT | +0.6% | Industrial hubs in North America, Europe, East Asia | Long term (≥ 4 years) |

| Regulatory opening of 6-7 GHz spectrum accelerating Wi-Fi 7 | +1.1% | North America, Europe, select Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Wi-Fi 6/6E in Enterprise Networks

Corporate campus upgrades began moving from pilot to full-scale rollouts in 2024, pushed by the 1,200 MHz of 6 GHz spectrum released by the FCC. Added channels permit larger 320 MHz widths that quintuple throughput versus Wi-Fi 5, giving IT teams capacity headroom for 8K media streams and latency-sensitive collaboration tools. More than 400 Wi-Fi 6E-certified devices had reached commercial availability by 2024, and enterprise-class access points formed the fastest-growing certification subcategory. Facilities teams report lower troubleshooting tickets as clean 6 GHz channels avoid interference created by legacy devices operating at 2.4 GHz and 5 GHz. Vendors position Wi-Fi 6E hardware as future-proof investments that accept software upgrades to Wi-Fi 7 when spectrum becomes available. Procurement cycles are shortened to under 15 months in verticals such as healthcare and finance, where always-on wireless is now an operational prerequisite.

Growth in Smart-Home Devices and Residential Mesh Networking

Household device density surpassed 30 connected endpoints in many urban dwellings during 2024, and forecasts suggest averages above 50 by 2028. That surge forces service providers to redesign gateways around tri-radio chipsets capable of dedicating 6 GHz backhaul links between mesh nodes. Wi-Fi 6E gateways thus prevent 4K streaming boxes from crowding thermostats and security cameras that still operate on 2.4 GHz. Beamforming and seamless handoff software within new chipsets sustain consistent throughput as occupants roam from room to room, addressing a top driver of support calls. Mature power-save modes extend battery life for low-duty-cycle sensors, trimming truck-roll costs for internet service providers. Broadcom quantified a double-digit drop in field-support incidents after deploying 6 GHz-enabled gateways across select North American fiber footprints.[2]Source: Broadcom, “Unprecedented Success of Opening 6 GHz Band to Wi-Fi,” broadcom.com

Integration of Wi-Fi HaLow for Low-Power Industrial IoT

Wi-Fi HaLow (802.11ah) uses sub-1 GHz frequencies to push signals more than 1 km, ten times farther than traditional Wi-Fi links while consuming under one-tenth the power. Support for up to 8,191 devices per access point scales battery-operated sensors across factories and warehouses. Penetration through concrete and metal lowers infrastructure costs because fewer access points are needed. Certifications begin in late 2024, giving industrial solution providers a standards-based alternative to proprietary LPWAN schemes. Predictive maintenance, asset tracking, and environmental monitoring are near-term beneficiaries, especially where replacement batteries are costly to access. Early evaluations show multi-year battery life for vibration sensors mounted on remote rotating equipment.

Regulatory Opening of 6-7 GHz Spectrum Accelerating Wi-Fi 7

Sixty-plus countries have assigned at least part of the 6 GHz band for license-exempt Wi-Fi use, creating a path toward global Wi-Fi 7 interoperability. Europe’s CEPT plans to authorize the 6.425–7.125 GHz range by 2027, potentially doubling continental spectrum. Japan finalized rules in 2024 that mirror U.S. allocations, unlocking local demand for tri-radio gateways. Wi-Fi 7 introduces Multi-Link Operation that bonds 2.4 GHz, 5 GHz, and 6 GHz channels, yielding headline throughput above 40 Gbps and sub-2 ms latency. Device forecasts point to 2.1 billion Wi-Fi 7 chipsets in active use by 2028, with television makers and broadband operators at the front of the adoption wave. Competitive differentiation now hinges on delivering working MLO firmware before rivals.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Network security threats and complex management | -0.8% | Global, enterprise most affected | Short term (≤ 2 years) |

| Competition from cellular 5G/LPWAN alternatives in IoT | -0.6% | Global, industrial IoT focus | Medium term (2-4 years) |

| Semiconductor fabrication capacity constraints (< 6 nm) | -0.7% | Global supply chain | Short term (≤ 2 years) |

| Fragmented regional spectrum regulations for Wi-Fi 7 | -0.5% | Mainly Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Network Security Threats and Complex Management

Transitioning to WPA3 hardens Wi-Fi networks, yet mixed-generation device fleets create compatibility gaps that slow enterprise upgrades. Multi-Link Operation in Wi-Fi 7 multiplies policy sets because each frequency link demands synchronized encryption credentials. IT administrators, therefore, invest in automated policy engines that escalate costs and lengthen deployment timetables. The influx of unmanaged IoT devices widens attack surfaces, prompting stricter network segmentation and zero-trust architectures that strain limited staff resources. Automated Frequency Coordination databases required for outdoor 6 GHz channels further complicate change-management workflows, pushing some organizations to slow rollouts until vendor tooling matures.

Semiconductor Fabrication Capacity Constraints (< 6 nm)

Sub-6 nm processes are mandatory for full-featured Wi-Fi 7 SoCs that integrate advanced MAC engines and AI-assisted network optimization blocks. Foundry output remains heavily booked by high-performance computing customers, limiting wafer availability for connectivity silicon. Lead-times beyond 40 weeks force smaller chipset suppliers to prioritize top-line components, delaying volume shipments to low-margin device categories. Cost pressures surface when capacity premiums flow downstream, raising average selling prices for consumer gateways. Suppliers with multi-year wafer agreements or in-house front-end module lines enjoy a buffer, while new entrants face steep barriers to scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Standard: Wi-Fi 7 Emergence Reshaping Technology Landscape

Wi-Fi 6 and Wi-Fi 6E together commanded 41.27% revenue share in 2025 as the preferred upgrade path for enterprise campus refresh projects. The segment benefits from backward compatibility and certified client ecosystems, anchoring the Wi-Fi chipset market through the mid-term horizon. The Others category, dominated by Wi-Fi 7 designs, is set to record the fastest 6.72% CAGR as chipmakers finalize 320 MHz channel architectures that multiply spectral efficiency. Apple’s flagship smartphones and laptop platforms are scheduled to integrate tri-band Wi-Fi 7 radios in 2025, which typically triggers accelerated LAN infrastructure investment by corporations aligning device and access-point capabilities. Filogic-based Wi-Fi 7 gateways demonstrated 4× higher uplink throughput in operator lab tests, underscoring differentiation over Wi-Fi 6E predecessors.

Growing demand for virtual reality, cloud gaming, and ultra-high-definition streaming elevates throughput expectations beyond the ceiling of Wi-Fi 6E. Early adopters place strategic orders for access points that feature Automatic Frequency Coordination clients to satisfy 6 GHz incumbent protections in outdoor venues. Market education campaigns from chipset vendors emphasize latency reduction in the single-millisecond range, critical for bidirectional XR use cases. As the Wi-Fi chipset market transitions, component suppliers that offer modular reference designs accelerate customer time-to-market and lock in design wins across CPE, PC, and smartphone verticals.

By MIMO Configuration: MU-MIMO Dominance Driven by Density Requirements

MU-MIMO solutions generated 60.65% of 2025 sales and registered a 6.61% CAGR through 2031. Eight-stream access points push simultaneous downlink and uplink data to dozens of devices, a capability vital for lecture halls and transportation hubs that often peak above 500 concurrent users. Advances in beamforming algorithms embedded inside Wi-Fi 6E and Wi-Fi 7 PHY layers sustain signal integrity even in reflective indoor environments. The Wi-Fi chipset market size attached to MU-MIMO implementations benefits from premium ASPs for high-end enterprise gear.

SU-MIMO chipsets remain in entry-level gateways and price-sensitive IoT nodes where single-threaded communication remains sufficient. Yet as IoT density rises, even consumer access points are migrating to four-stream MU-MIMO designs to minimize airtime contention. Component vendors embed AI acceleration blocks that analyze client telemetry and dynamically allocate spatial streams, assuring predictable application performance for videoconferencing apps that dominate residential upstream traffic.

By Device Application: Routers and Gateways Lead Growth Transformation

Smartphones produced 39.45% of Wi-Fi chipset market revenue in 2025, driven by cyclical refresh cycles and 5G coexistence requirements. However, router and broadband gateway designs forecast a 7.76% CAGR through 2031 as fiber-to-the-home rollouts demand tri-band gateways capable of gigabit-class throughout. Operators calibrate hardware configurations around rising numbers of 4K set-top boxes and smart appliances per household, installing two or more satellite nodes to blanket multi-story homes.

Tablets, laptops, and desktops retain a steady share but adopt Wi-Fi 7 to support higher Wi-Fi-only productivity expectations among hybrid workers. Automotive infotainment systems represent a nascent but high-growth subsegment, boosted by over-the-air firmware updates and passenger experience requirements. NXP’s AEC-Q100-qualified dual-band Wi-Fi 6 solutions set the reference standard for gigabit connectivity in connected cars, and future Wi-Fi 7 automotive platforms plan to deliver redundant links for V2X back-haul streams.

By End-User: Automotive Segment Accelerates Connected Vehicle Adoption

Residential consumer electronics captured 60.82% of 2025 shipments as mesh networking and smart-home ecosystems expanded. The Wi-Fi chipset market now prioritizes low-power operation to cater to battery-operated sensors that proliferate within homes. Enterprise demand follows digital workplace transformations that require dense access-point grids for collaboration rooms and hot-desking zones.

The automotive category is projected to post the fastest 7.95% CAGR, reflecting automakers’ push to embed Wi-Fi 6 and Wi-Fi 7 alongside 5G modems to handle high-throughput cabin entertainment and secure vehicle diagnostics. Wi-Fi Alliance projects that 95% of vehicles will ship with Wi-Fi connectivity by 2030, creating a multiyear pipeline for captive module suppliers. Industrial IoT adopters begin evaluating Wi-Fi HaLow for remote asset monitoring, while public sector deployments turn to Wi-Fi 6E for smart city video surveillance and broadband-quality public hotspots.

Geography Analysis

Asia-Pacific generated 43.05% of Wi-Fi chipset market shipments in 2025, with China, Japan, and South Korea anchoring both manufacturing and consumption. Government fiber investments across Tier-2 and Tier-3 Chinese cities stimulate demand for tri-radio gateways, although current limitations on indoor 6 GHz operation delay full-scale Wi-Fi 6E adoption. Japan’s regulatory green light for 6 GHz WLAN in 2024 sparked local OEM activity around Wi-Fi 7 routers that support 320 MHz channels, while Korean operators deploy carrier-grade Wi-Fi 6E access points inside 5G-enabled smart-city corridors. India’s surge in internet subscribers and the establishment of a Wi-Fi design center in Chennai illustrate the region’s evolving role as both an engineering hub and a high-volume consumer.

North America maintains a leadership role in enterprise deployments, leveraging the FCC’s early opening of the entire 6 GHz band. Hybrid work patterns keep demand strong for access points with dynamic channel allocation features. Service providers bundle managed Wi-Fi 7 gateways into gigabit fiber packages to reduce customer churn and differentiate beyond speed tiers. The Wi-Fi chipset market benefits from robust private-sector funding that underwrites rapid generation transitions when total cost-of-ownership models justify productivity gains. Europe experiences accelerated Wi-Fi 7 adoption among broadband operators preparing for 8 Gbps multi-gig services. CEPT’s efforts to authorize the upper 6 GHz band would double available channels and foster symmetrical gigabit performance across densely populated metro areas. Meanwhile, South America and the Middle East, and Africa deliver emerging-market growth as cost-reduced Wi-Fi 6 chipsets migrate into mass-market smartphones and fixed-wireless gateways that bridge rural connectivity gaps. Spectrum allocation diversity across these regions complicates global SKU alignment, but standards-based certifications minimize interoperability risk for multinational OEMs.

Regulatory Landscape

The regulatory environment for Wi-Fi chipsets is anchored in unlicensed spectrum policy and radio equipment compliance, with 6 GHz rules shaping Wi-Fi 6E and Wi-Fi 7 product viability across regions. In the United States, the FCC opened the full 1,200 MHz 6 GHz band for unlicensed use. In many European markets, 6 GHz allocations and operating modalities remain more limited, and harmonized requirements are referenced via ETSI standards, including ETSI EN 303 687, under the EU Radio Equipment Directive (RED). Together, these constraints limit outdoor and higher-power use cases compared with U.S. Standard Power approaches.

Standards finalization and certification requirements also feed into chipset and device roadmaps. IEEE 802.11be (Wi-Fi 7) was approved by the IEEE Standards Board in September 2024, supporting global interoperability as more countries authorize portions of 6 GHz for license-exempt Wi-Fi. In July 2026, the FCC issued updates that tighten certification conditions for Wi-Fi 7 IoT terminal devices by adding end-to-end Matter 2.4 interoperability verification as part of FCC ID pathways, with an October 1, 2026 effective date. This raises compliance and test readiness requirements for vendors selling into the North American market.

Value Chain Analysis

The Wi-Fi chipset value chain starts with IP and standards implementation (IEEE 802.11 families) and extends through SoC design (MAC/PHY, baseband, security), RF integration (front-end modules, power amplifiers, LNAs, switches), advanced packaging, module assembly, OEM device integration, certification, and channel distribution via consumer electronics and enterprise networking ecosystems. Leading chipset suppliers (including Qualcomm, Broadcom, MediaTek, Intel, and Realtek) depend on advanced-node foundry capacity to deliver high-integration Wi-Fi 6E and Wi-Fi 7 silicon, while specialized vendors focus on niches such as sub-GHz Wi-Fi HaLow and cost-optimized combo solutions.

Upstream constraints increasingly concentrate in two areas: wafer capacity for feature-rich Wi-Fi 7-class SoCs, especially sub-7 nm, and RF front-end availability. Acoustic filters (SAW/BAW) are produced by a limited supplier base that uses specialized equipment and materials. Downstream, OEM qualification cycles, often 12 to 36 months in automotive and industrial segments, slow design-win conversion even when silicon is available. At the same time, enterprise WLAN refresh activity is pulling demand toward higher-end access point silicon, shifting mix requirements from chip suppliers to module makers and further to router, gateway, and access point OEMs.

Competitive Landscape

The Wi-Fi chipset market shows moderate concentration. Qualcomm, Broadcom, and MediaTek dominate by virtue of end-to-end portfolios that span smartphones, PCs, CPE, and IoT modules. Access to sub-6 nm foundry capacity allows these firms to introduce Wi-Fi 7 silicon with integrated network-on-chip engines that offload Quality-of-Service tasks. Qualcomm partnered with STMicroelectronics to blend Wi-Fi, Bluetooth, and Thread into STM32 microcontrollers, targeting an installed base of more than 80 billion IoT devices by 2028.[5]Source: Qualcomm, “Qualcomm and STMicroelectronics Enter Strategic Collaboration in Wireless IoT,” qualcomm.com Intel integrates Wi-Fi 7 into vPro platforms, positioning desktops and laptops for 5× uplink improvements over Wi-Fi 6E.

NXP pursues vertical specialization in automotive, emphasizing AEC-Q100 qualification and UWB-assisted battery-management systems to secure design wins in connected vehicles. Vendors such as CEVA license Wi-Fi 6 IP blocks to regional fabless startups, lowering barriers for Chinese handset OEMs that seek in-house connectivity roadmaps. Component suppliers with captive front-end module lines gain margin advantages because FEM costs rise in tandem with 6 GHz coexistence filters.

Competitive intensity rises in low-power industrial IoT, where Wi-Fi HaLow creates white-space opportunities. Startups introduce sub-GHz SoCs integrating sensor controllers and power amplifiers on a single die to shrink bill-of-materials. Still, high-volume contracts go to incumbents with robust supply-chain compliance programs demanded by global industrial OEMs. Patent portfolios covering beamforming and MLO scheduling remain key bargaining chips in cross-licensing negotiations, influencing royalty structures across the ecosystem.

Wi-Fi Chipset Industry Leaders

-

Qualcomm Technologies Inc.

-

Broadcom Inc.

-

MediaTek Inc.

-

Intel Corporation

-

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is emerging from accelerating enterprise WLAN refresh cycles toward Wi-Fi 7 feature sets, including Multi-Link Operation and wider channels. This is changing the silicon mix toward higher-integration access point and gateway platforms. The shift shows up in enterprise access point revenue composition, where Wi-Fi 7 reached 44.5% of enterprise dependent access point revenues in 1Q 2026, up from 11.8% in 1Q 2025. That trajectory increases demand for chipsets that pair high-performance Wi-Fi radios with stronger processing and QoS offload.

Platform-level integration across access technologies creates additional whitespace for chipset vendors and module partners, especially in fixed wireless access and multi-gig home gateways that blend cellular and Wi-Fi connectivity. In May 2026, Broadcom announced collaboration with Samsung Electronics around an integrated 5G and Wi-Fi platform for FWA, pointing to operator-facing BOM and power optimization priorities. Supply-chain localization and strategic sourcing have also become more prominent for connectivity silicon and RF components; in July 2026, Apple announced a multiyear agreement exceeding USD 30 billion with Broadcom that includes investment tied to Broadcoms Fort Collins, Colorado facility. The commitment underlines how long-horizon supply plans support high-volume device ramps.

Recent Industry Developments

- July 2026: Apple announced a new multiyear agreement with Broadcom exceeding USD 30 billion covering wireless connectivity technologies and radio frequency components, alongside a USD 1.5 billion capital expenditure tied to Broadcoms Fort Collins, Colorado facility. The deal supports long-term supply alignment for high-volume connectivity content and reinforces the strategic importance of RF front-end and connectivity silicon capacity planning.

- May 2026: Broadcom announced a collaboration with Samsung Electronics to develop an integrated fixed wireless access platform combining Broadcoms BCM6776 Wi-Fi 8 SoC with Samsungs B1320 5G modem. The joint platform targets tighter 5G and Wi-Fi integration in operator CPE, supporting lower BOM and power while accelerating reference designs for multi-gigabit home broadband.

- October 2024: Qualcomm unveiled the Networking Pro A7 Elite platform for advanced residential and enterprise networking equipment. The platform places Wi-Fi 7-class networking silicon around higher compute and AI-assisted network optimization, supporting chipset differentiation where latency and dense-client performance influence purchasing decisions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers revenue generated from Wi-Fi chipsets used to enable Wi-Fi connectivity inside end devices and networking equipment. It is counted at the point the chipset is shipped for a Wi-Fi use case, with revenue captured at the chipset level.

Scope exclusions: We exclude non-Wi-Fi connectivity chipsets that do not support IEEE 802.11 standards and services-only revenue that sits outside chipset shipments.

Segmentation Overview

-

By Standard

- Wi-Fi 4

- Wi-Fi 5 (802.11ac)

- Wi-Fi 6 and 6E (802.11ax)

- Wi-Fi 7 (802.11be)

- Other Standards (Wi-Fi 8, Older)

-

By MIMO Configuration

- MU-MIMO

- SU-MIMO

-

By Device Application

- Smartphones

- Tablets

- Desktops

- Laptops

- Wi-Fi Router and Broadband Gateway

- TV

- IoTs

- Infotainment Systems (Automotive)

- Other Device Applications (Drones, Gaming Devices)

-

By End-User

- Residential (Consumer Electronics)

- Enterprise (Networking)

- Industrial

- Automotive

- Government and Public

- Medical

- Other End-Users (Education, Commercial)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- South-East Asia

- Rest of Asia-Pacific

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

-

Africa

- South Africa

- Egypt

- Rest of Africa

-

Middle East

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the Wi-Fi chipset value chain and the most common demand pools, then aligning those with standard definitions used in public statistics. We typically rely on sources such as ITU connectivity indicators, Wi-Fi Alliance publications on Wi-Fi generation adoption, IEEE 802.11 standard documentation, and OECD digital economy datasets to ground the technology and usage context.

For volume and demand direction, we also review public filings and investor decks from ecosystem participants, import and export trade summaries where electronics components are visible, and well tracked press coverage around Wi-Fi 6, Wi-Fi 6E, and Wi-Fi 7 device cycles. Where needed, we use paid subscriptions that provide company financials and intelligence, patent lookups, and shipment-level import and export records, which help cross-check pricing and supply signals. These sources are illustrative, and there are other public and paid references used for data collection, validation, and clarifying open questions.

Primary Interviews and Surveys

Primary work focuses on validating what gets counted as a Wi-Fi chipset sale across device categories, and how average selling prices move by standard generation, integration level, and unit volumes. We speak with chipset ecosystem participants and downstream integrators, then pressure-test assumptions across APAC, EMEA, and the Americas so regional adoption patterns are not overgeneralized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 47% |

| Mid tier: 49% | Functional/Unit leaders: 27% | EMEA: 32% |

| Smaller Players: 14% | Managers: 59% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where device shipment pools and Wi-Fi attach rates are used to reconstruct chipset demand, then converted to value using typical chipset ASP ranges by Wi-Fi generation. Once the demand pool is formed, we corroborate it with selective bottom-up approximations, such as sampled ASP multiplied by estimated unit volumes for major device classes, and channel checks on mix shifts. We then adjust totals where gaps are consistently flagged.

Key model inputs include the rollout pace of Wi-Fi 6 and Wi-Fi 6E versus legacy standards, early adoption timing for Wi-Fi 7, the mix of client devices versus routers and gateways, typical MIMO feature penetration, and regional device replacement cycles. A small change in standard mix or integration level can shift the ASP assumptions, even if unit volumes remain steady.

For forecasting, we run scenario analysis anchored to these variables. Scenarios are refined through expert consensus on timing of generation transitions and expected pricing erosion. When bottom-up signals are incomplete for certain device groups, we fill gaps using conservative ranges, then reconcile them back to the top-down totals so the final series stays traceable and repeatable.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, followed by variance checks at region and device category levels so unusual swings are caught early. If an output looks misaligned with adoption milestones for Wi-Fi 6E and Wi-Fi 7, or with observed shipment direction, we revisit assumptions and trigger interview follow-ups.

Before sign-off, the model goes through multi-step analyst reviews that focus on unit consistency, pricing logic, and currency treatment across years. Reports are refreshed annually, with interim updates when material events occur, and there is a final data pass right before delivery so the series reflects the most current view.

Mordor Intelligence's Global Wi Fi Chipset Market Estimate Compared With Other Published Estimates

Published market numbers for Wi-Fi chipsets often vary because groups do not always count the same revenue line, the same device set, or the same starting year. Differences also show up when one model relies more on shipment math while another relies more on broad value assumptions.

The main gap comes from how integrated Wi-Fi inside larger silicon is treated. Mordor Intelligence counts Wi-Fi chipset revenue only when the Wi-Fi value is separately attributable, rather than folding the full processor value into the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 23.24 B (2026) | |

| Global Consultancy A | USD 22.50 B (2025) | Uses a different base year and can apply earlier pricing erosion assumptions for legacy Wi-Fi generations, which can reduce the value total even if unit shipments are similar. |

| Industry Research Group B | USD 29.27 B (2022) | Anchors the series to an earlier year with broader device and vertical coverage described at a high level, which can overstate value if integrated silicon and adjacent connectivity revenue are not cleanly separated. |

The spread in the table is mostly explained by year choice and how cleanly the chipset revenue line is isolated from broader silicon value. By keeping the demand pool tied to device shipments, standard mix, and realistic ASP progression, the resulting market size stays easier to reproduce and to audit when assumptions change.

Key Questions Answered in the Report

What CAGR is projected for global Wi-Fi chipset sales through 2031?

The Wi-Fi chipset market is forecast to expand at a 6.12% CAGR from 2026 to 2031.

Which region currently leads demand for Wi-Fi chipsets?

Asia-Pacific held 43.05% of 2025 shipments and is also the fastest-growing region through 2031 at a 7.46% CAGR.

How will Wi-Fi 7 affect enterprise network upgrades?

Wi-Fi 7 triples available channel width and introduces Multi-Link Operation, driving enterprises to refresh access-point fleets for higher throughput and lower latency.

Why are routers and gateways the fastest-growing device segment?

Fiber-to-the-home rollouts and mesh networking spur operator demand for tri-radio gateways, resulting in a 7.76% CAGR for this category.

Page last updated on: