Wide Band Gap Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

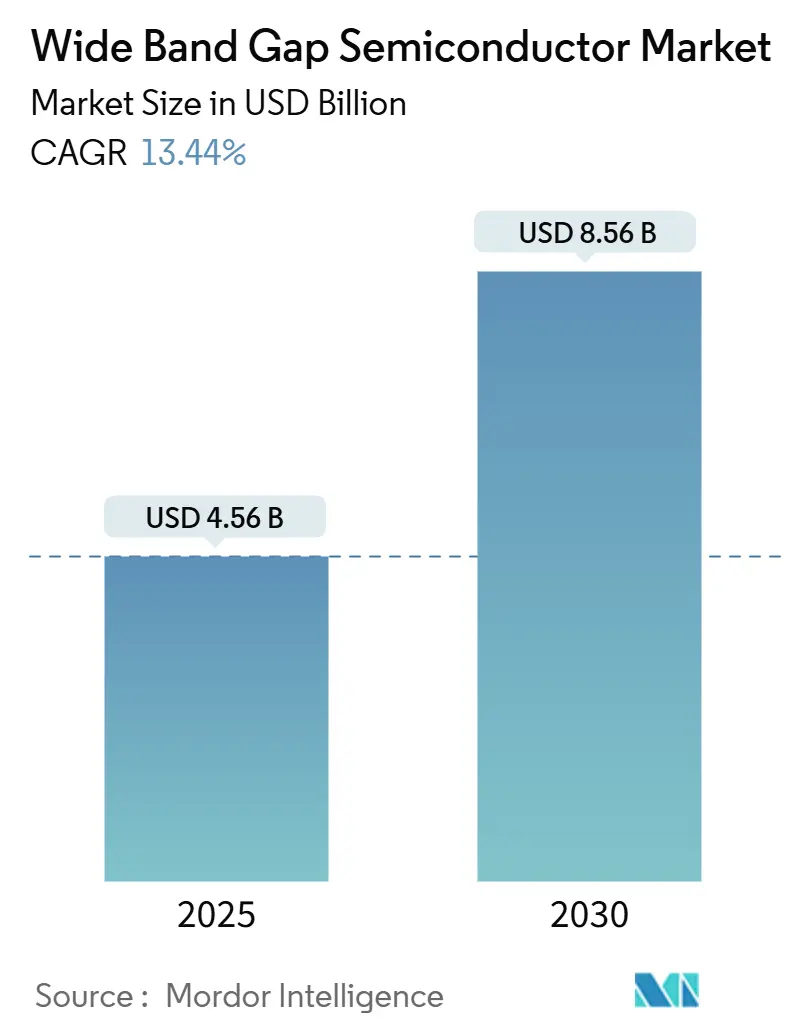

| Market Size (2025) | USD 4.56 Billion |

| Market Size (2030) | USD 8.56 Billion |

| Growth Rate (2025 - 2030) | 13.44% CAGR |

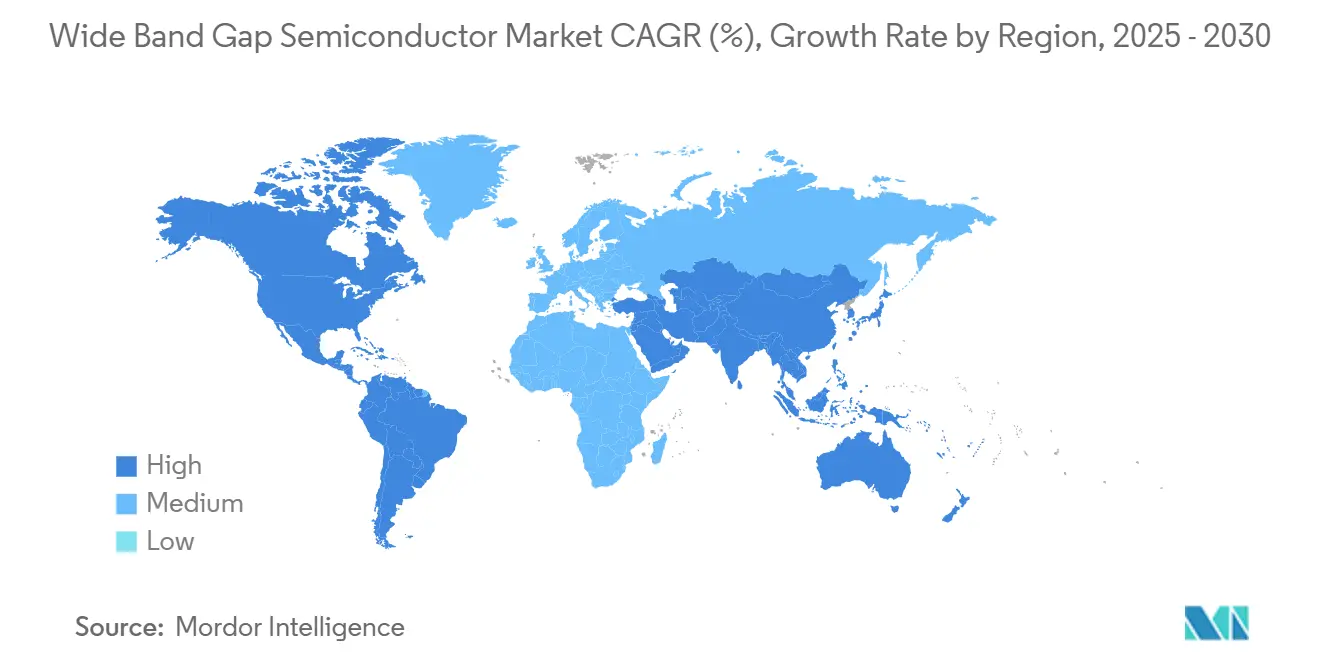

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

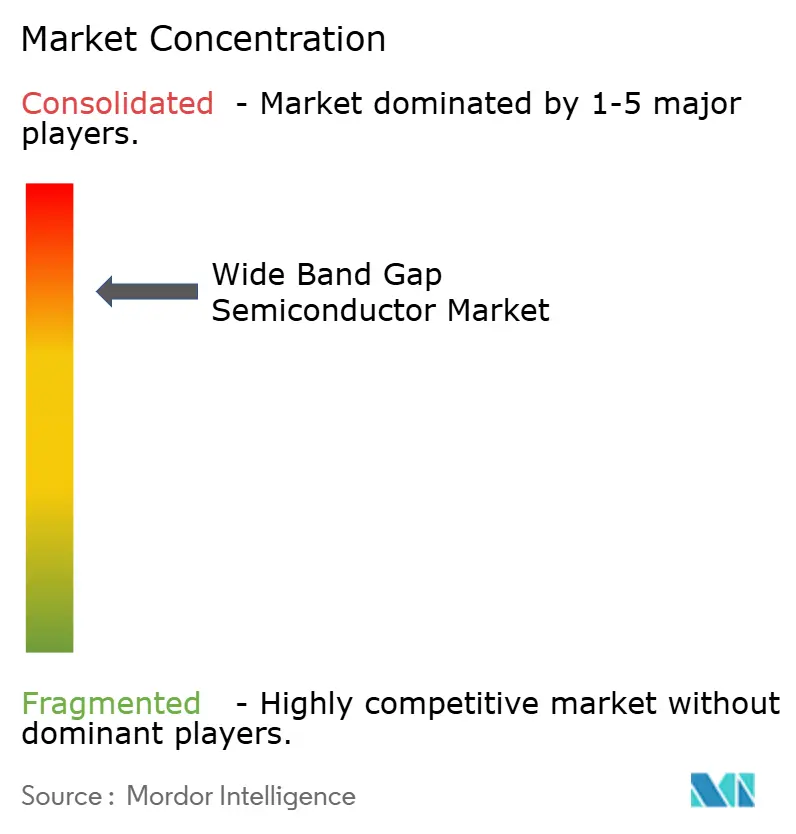

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wide Band Gap Semiconductor Market Analysis by Mordor Intelligence

The Wide Band Gap Semiconductor market size reached USD 4.04 billion in 2024 and is forecast at USD 4.56 billion for 2025 before climbing to USD 8.56 billion in 2030, reflecting a 13.44% CAGR over 2025-2030. Robust demand for high-voltage electric-vehicle traction inverters, steep cost declines in silicon-carbide substrates, and rising 5G base-station deployments are expanding addressable volumes across automotive, industrial, and telecom segments. Government subsidies under the U.S. CHIPS Act, Japan’s METI program, and parallel initiatives in Europe accelerate domestic capacity build-outs, reducing supply-chain concentration while keeping capital intensity elevated.[1]Source: U.S. Department of Commerce, “Biden-Harris Administration Announces Preliminary Terms with Wolfspeed to Solidify U.S. Technological Leadership in Silicon Carbide Manufacturing,” commerce.gov Competitive strategies center on vertical integration, 200 mm wafer conversion, and material innovation, particularly diamond and gallium nitride, to improve yield, thermal performance, and switching efficiency. Momentum is strongest in Asia-Pacific, where foundry ecosystems enable rapid production scale, while South America’s abundant critical minerals provide a new sourcing option, attracting greenfield investment.[2]Source: DIGITIMES Asia, “China’s aggressive SiC price war set to halve cost by 2025,” digitimes.com

Key Report Takeaways

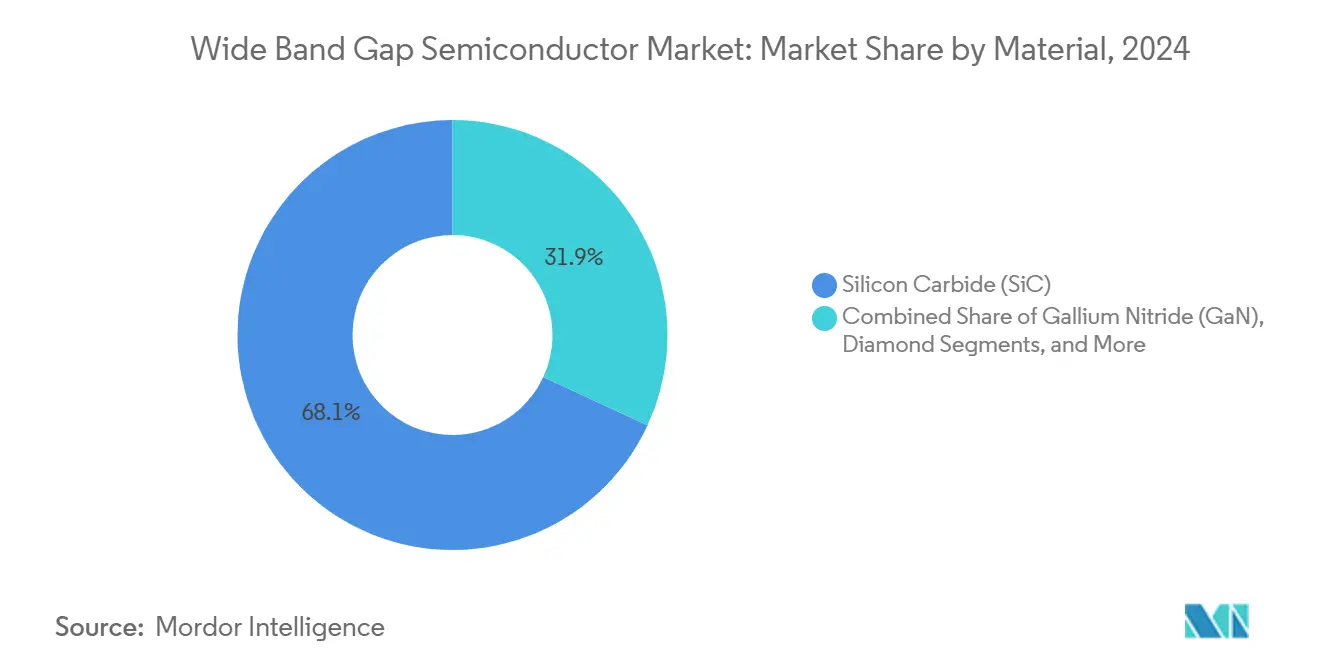

- By material, silicon carbide held 68.1% of the Wide Band Gap Semiconductor market share in 2024; diamond is advancing at a 13.3% CAGR through 2030.

- By device type, power modules captured 47.6% revenue share in 2024; power GaN is projected to expand at a 13.2% CAGR over 2025-2030.

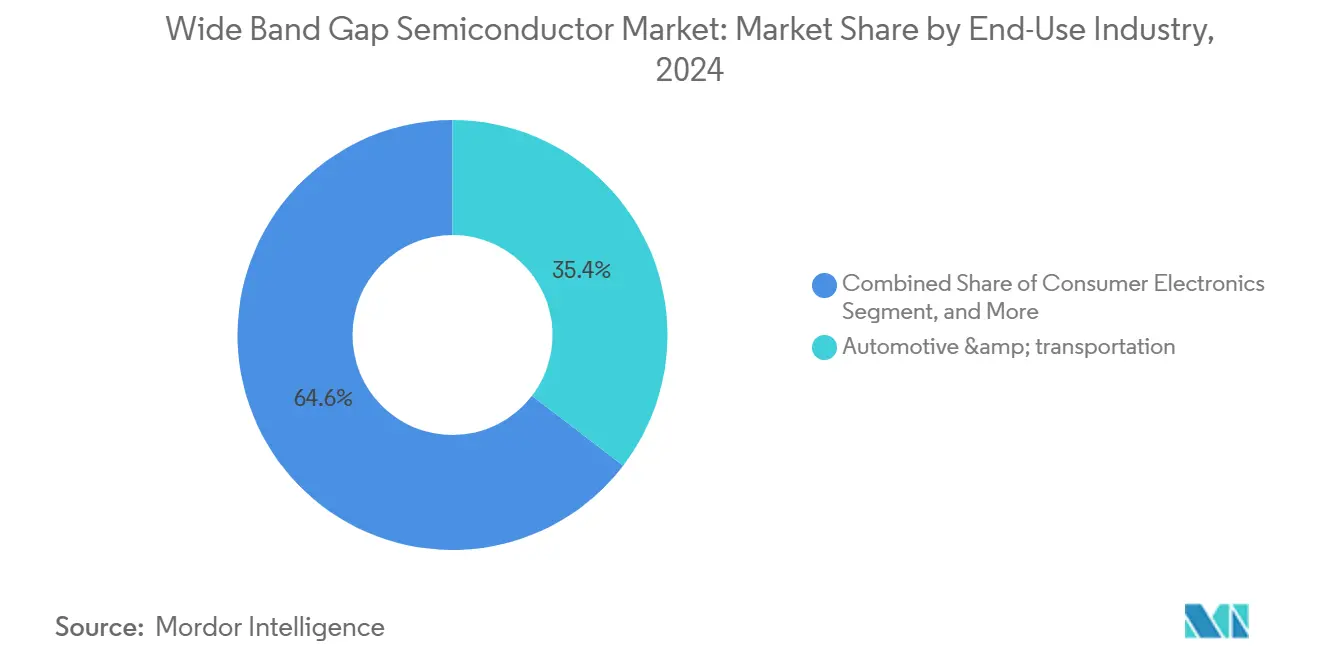

- By end-use industry, automotive and transportation led with 35.4% of the Wide Band Gap Semiconductor market size in 2024, whereas aerospace and defense are on track for a 13.1% CAGR to 2030.

- By geography, APAC commanded 53.1% of 2024 revenue; South America shows the highest regional CAGR of 13.1% through 2030.

- STMicroelectronics, Wolfspeed, Infineon Technologies, onsemi, and Renesas collectively controlled more than 90% of 2024 SiC power revenue, underscoring a highly concentrated landscape.

Global Wide Band Gap Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SiC cost curve drops below USD 0.08/A in power MOSFETs | +2.8% | China first; wider APAC follow-on | Medium term (2-4 years) |

| Rapid EV adoption of >800 V traction inverters | +3.2% | Europe & China lead; North America scaling | Short term (≤ 2 years) |

| 5G base-station RF front-ends shift to GaN HEMTs | +1.9% | APAC-centric with global deployments | Medium term (2-4 years) |

| Government SiC wafer-fab subsidies | +2.1% | U.S., EU, Japan; spillovers worldwide | Long term (≥ 4 years) |

| Solid-state circuit breakers for renewable micro-grids | +1.4% | Europe & North America pioneer | Long term (≥ 4 years) |

| Ultra-high-temperature aerospace electronics | +1.0% | North America & Europe defense hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Silicon-Carbide Cost Curve Inflection Drives Mass-Market Adoption

Manufacturing costs for SiC power MOSFETs are trending toward a USD 0.08/A threshold that enables mainstream automotive and industrial penetration. Chinese substrate vendors have already cut wafer prices by nearly 50% since 2024, a trajectory expected to continue into 2026.[3]Source: Infineon Technologies AG, “Infineon opens the world’s largest and most efficient SiC power semiconductor fab in Malaysia,” infineon.com Infineon’s automated 200 mm line in Kulim delivers 1.8× more die per wafer, while Wolfspeed’s New York facility targets 30% incremental capacity through lights-out processing. Yield gains from 99% defect-free epi-layers on 150 mm wafers demonstrate process stability, and early 200 mm pilot runs indicate gradual yield parity. As cost and yield converge, power-device makers can broaden design-ins across inverters, chargers, and industrial drives, reinforcing the scale economies now underway.

EV Traction-Inverter Architecture Shifts Accelerate 800 V Adoption

Automakers are standardizing 800 V battery platforms to halve charging times and reduce cabling losses, a shift that materially increases SiC demand per vehicle. Volkswagen’s multiyear supply agreement with onsemi for EliteSiC-based power boxes exemplifies the trend, covering multiple vehicle classes through 2030.[4]Source: onsemi, “onsemi Selected to Power Volkswagen Group’s Next-Generation Electric Vehicles,” onsemi.com Hitachi’s volume production of 800 V inverters delivers 2.7× higher power density than earlier 400 V units, demonstrating SiC’s efficiency edge. With leading OEMs transitioning entire EV portfolios, system-level design wins now bundle modules, diodes, and gate drivers, locking in multi-year silicon-carbide road maps.

5G Infrastructure Deployment Catalyzes GaN HEMT Expansion

Massive-MIMO 5G base stations require compact, high-efficiency RF front ends; GaN HEMTs offer up to 8 percentage-point efficiency gains over LDMOS at 2.6 GHz. Mitsubishi Electric’s 16 W GaN amplifier modules further lower system power and cooling overheads, making GaN the de-facto standard in upcoming 5G macro cells. Foundry realignment is reshaping supply as TSMC exits GaN by 2027; Powerchip and UMC are scaling 200 mm GaN lines to fill the gap, preserving APAC’s production dominance.

Government Semiconductor Subsidies Reshape Global Supply Chains

Public spending is driving a geographic rebalance of the Wide Band Gap Semiconductor market. Wolfspeed secured USD 750 million in CHIPS Act incentives for a North Carolina SiC mega-fab, complementing its New York device plant. Japan’s METI allocated JPY 70.5 billion to Denso–Fuji Electric for mass-production lines targeting 310,000 wafers annually by 2027. In Europe, Bosch obtained USD 225 million in U.S. CHIPS funding for its California SiC operation that will supply both U.S. and EU customers. These commitments shorten lead times, diversify sourcing, and strengthen the policy link between energy transition goals and domestic semiconductor capacity.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SiC boule yield losses keep >150 mm wafers below 35% | -1.8% | Global; highest in new fabs | Medium term (2-4 years) |

| Limited GaN epi-wafer supply outside Taiwan | -1.2% | North America & Europe exposed | Short term (≤ 2 years) |

| Reliability qualification gaps for automotive ECUs | -0.9% | Europe & Japan stringent | Medium term (2-4 years) |

| IP consolidation limits new fab entrants | -0.7% | Emerging markets most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Manufacturing Yield Challenges Constrain SiC Substrate Scaling

SiC crystal growth still wrestles with micropipes and basal-plane dislocations that cap 150 mm yield below 35% in many fabs. Moving to 200 mm increases defect propagation risk, necessitating tighter process control and new in-situ monitoring. Onsemi’s multistage quality-reliability protocol mitigates substrate defectivity yet underscores the need for cross-functional R&D alliances to sustain defect density below critical thresholds. Until yields stabilize, wafer supply remains tight, tempering the otherwise steep cost-down trajectory.

GaN Supply-Chain Concentration Creates Strategic Vulnerabilities

More than 70% of GaN epi-wafer output is clustered in Taiwan, leaving Western OEMs susceptible to geopolitically driven disruptions. TSMC’s scheduled withdrawal exacerbates single-source risk; alternative suppliers like WIN and Powerchip are adding 200 mm capacity, but meaningful diversification is still two to three years away. U.S. policy advisers now flag GaN as a “strategic material,” urging federal incentives for domestic epi growth and allied gallium sourcing. Until such programs mature, design engineers must dual-source or stockpile critical RF inventory, adding cost and complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Silicon Carbide Dominance with Diamond on the Horizon

Silicon carbide secured 68.1% of 2024 revenue, underscoring its entrenched position in traction inverters and industrial drives; this equates to the largest single slice of the Wide Band Gap Semiconductor market share. At a projected 13.3% CAGR, diamond is positioned as the fastest-growing material, buoyed by breakthrough doping methods that produce both n-type and p-type films suitable for extreme-environment electronics.

Consistent supply, established automotive qualification, and a robust tooling ecosystem keep SiC as the default choice for high-voltage power trains. Yet diamond’s 5 × thermal conductivity and 2 × bandgap catalyze R&D for aerospace and AI data-center modules where heat removal is paramount. Japan’s Saga University powered a 50 kW diamond circuit, while Orbray targets 4-inch substrates by 2027, signaling pending commercialization. As pilot lines mature, the Wide Band Gap Semiconductor market will start allocating niche-critical applications to diamond, incrementally reducing SiC’s share past 2030.

By Device Type: Power Modules Lead, Power GaN Races Ahead

Power modules delivered 47.6% of 2024 revenue, reflecting extensive use of multi-chip SiC assemblies in EV traction and industrial motor drives; they form the largest block within the overall Wide Band Gap Semiconductor market. Power GaN, although smaller today, shows the steepest growth slope at 13.2% CAGR as AI data centers and fast chargers chase higher switching speeds and efficiency.

Packaging innovation is a major differentiator. Infineon’s CoolSiC module achieves 30% lower conduction loss, while onsemi’s third-generation M3e devices reduce turn-off losses by 50%. RF and microwave GaN retain strong telecom pull-through, especially as base-station OEMs shift to integrated multi-chip modules. The transition to 200 mm GaN wafers will unlock further cost reduction, tightening competition between SiC and GaN at mid-power nodes.

By End-Use Industry: Automotive Keeps Lead, Aerospace Sets the Pace

Automotive and transportation accounted for 35.4% of 2024 sales, the single largest slice of the Wide Band Gap Semiconductor market. Aerospace and defense, though smaller, leads growth at 13.1% CAGR on demand for electronics exceeding 600 °C operating temperatures and directed-energy weapons.

EV traction inverters now specify SiC as the default for ≥800 V platforms, a trend validated by Volkswagen’s multi-year sourcing pact with onsemi. In aerospace, NASA’s SiC and diamond programs aim for Venus-class temperature survivability, while the U.S. Navy’s USD 10.9 million contract with Wolfspeed showcases defense traction. As qualification hurdles fall, military and space platforms will capture a larger share of the Wide Band Gap Semiconductor market by value, though automotive retains volume leadership.

Geography Analysis

Asia-Pacific dominated the Wide Band Gap Semiconductor market in 2024 with a 53.1% revenue share underpinned by Taiwan’s foundry ecosystem and China’s domestic-capacity push. China’s price-led strategy has already cut SiC wafer costs in half, influencing global pricing and accelerating adoption. Japan’s METI subsidies strengthen domestic supply while fostering diamond-based R&D, reinforcing the region’s materials leadership.

Europe remains integral through Infineon’s Malaysian 200 mm fab, which supports global automotive decarbonization goals. EU safety standards such as ISO 26262 elevate device qualification thresholds, benefiting vendors with mature quality-reliability frameworks.

North America leverages CHIPS Act incentives to build end-to-end SiC capacity. Wolfspeed’s North Carolina crystal-growth complex and Bosch’s Roseville expansion will collectively supply a substantial share of U.S. automotive demand from 2026 onward.

South America, although only a mid-single-digit contributor today, exhibits the highest regional CAGR at 13.1% as governments monetize lithium, copper, and rare-earth reserves essential for wafer production. Early renewable-energy projects already specify SiC for solid-state circuit breakers, hinting at localized demand expansion.

The Middle East and Africa leverage solar and grid-storage build-outs to justify SiC inverter imports, while joint ventures explore local packaging lines to mitigate logistics costs. Across regions, policy, critical minerals access, and existing semiconductor clusters determine growth trajectories and influence supply-chain resilience strategies in the Wide Band Gap Semiconductor market.

Competitive Landscape

Five companies, STMicroelectronics, Infineon Technologies, Wolfspeed, onsemi, and Renesas, held more than 90% of 2024 SiC power revenue, underscoring market concentration. STMicroelectronics leads with a 32.6% share via substrate-to-package vertical integration, maintaining cost and supply security. Infineon’s USD 830 million acquisition of GaN Systems elevates its mid-power portfolio while its Kulim SiC mega-fab scales 200 mm output.

Wolfspeed continues to dominate SiC materials and secured USD 750 million in federal funding for its North Carolina expansion; the company also divested its RF unit to MACOM, sharpening its focus on SiC. Onsemi accelerated portfolio depth by acquiring Qorvo’s SiC JFET IP for USD 115 million and broadening its Czech and U.S. fabs.

Renesas completed the USD 339 million Transphorm takeover to gain GaN access for EV and AI power supplies. Emerging challengers leverage niche materials: Diamond Quanta targets aerospace power modules, while Element Six spearheads DARPA’s LADDIS program for ultra-wide bandgap devices. Overall, scale economics, patent control, and government incentives dictate competitive positioning within the evolving Wide Band Gap Semiconductor market.

Wide Band Gap Semiconductor Industry Leaders

Wolfspeed, Inc.

Infineon Technologies AG

ROHM Co., Ltd.

ON Semiconductor Corporation

STMicroelectronics N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Onsemi finalized the USD 115 million purchase of Qorvo’s SiC JFET business, expanding its EliteSiC range for AI data centers.

- January 2025: Wolfspeed topped out its USD 6 billion North Carolina crystal-growth facility, marking the world’s largest SiC materials plant.

- February 2025: Infineon introduced its first production SiC devices on 200 mm wafers out of Villach, targeting renewable-energy and mobility platforms.

- December 2024: Bosch secured USD 225 million in CHIPS Act funding to enlarge its California SiC fab, slated for 200 mm production in 2026.

Global Wide Band Gap Semiconductor Market Report Scope

| Silicon Carbide (SiC) |

| Gallium Nitride (GaN) |

| Diamond |

| Others (AlN, Ga2O3, etc.) |

| Power Devices (Diodes, MOSFETs, Modules) |

| RF and Microwave Devices (HEMTs, MMICs) |

| Optoelectronic and UV Devices |

| Automotive and Transportation |

| Consumer Electronics |

| Industrial and Motor Drives |

| Energy and Power (Renewables, Grid) |

| Telecommunications and Datacom |

| Aerospace and Defense |

| Healthcare and Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Taiwan | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Material | Silicon Carbide (SiC) | ||

| Gallium Nitride (GaN) | |||

| Diamond | |||

| Others (AlN, Ga2O3, etc.) | |||

| By Device Type | Power Devices (Diodes, MOSFETs, Modules) | ||

| RF and Microwave Devices (HEMTs, MMICs) | |||

| Optoelectronic and UV Devices | |||

| By End-use Industry | Automotive and Transportation | ||

| Consumer Electronics | |||

| Industrial and Motor Drives | |||

| Energy and Power (Renewables, Grid) | |||

| Telecommunications and Datacom | |||

| Aerospace and Defense | |||

| Healthcare and Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Taiwan | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Wide Band Gap Semiconductor market today?

The Wide Band Gap Semiconductor market size was USD 4.04 billion in 2024 and is projected at USD 4.56 billion for 2025.

What is driving the shift toward 800 V EV systems?

Automakers adopt 800 V architectures to cut charging times and reduce cable weight, and silicon-carbide MOSFETs enable the required high-voltage, high-efficiency switching.

Which material currently leads in market share?

Silicon carbide leads with 68.1% of 2024 revenue, benefiting from mature supply chains and automotive qualification.

Why is diamond gaining interest in power electronics?

Diamond offers 5 × thermal conductivity and a wider bandgap than SiC, making it attractive for extreme-temperature aerospace and defense systems.

Page last updated on: