Canned Mushroom Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.35 Billion |

| Market Size (2031) | USD 13.08 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

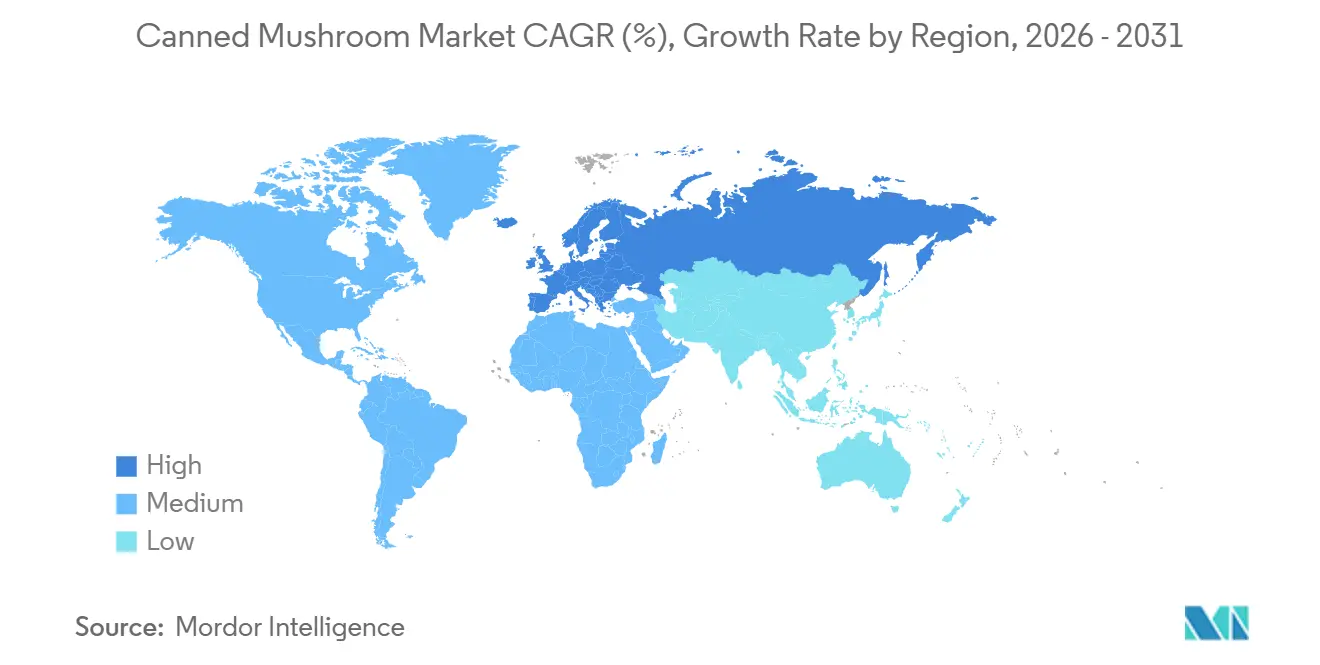

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

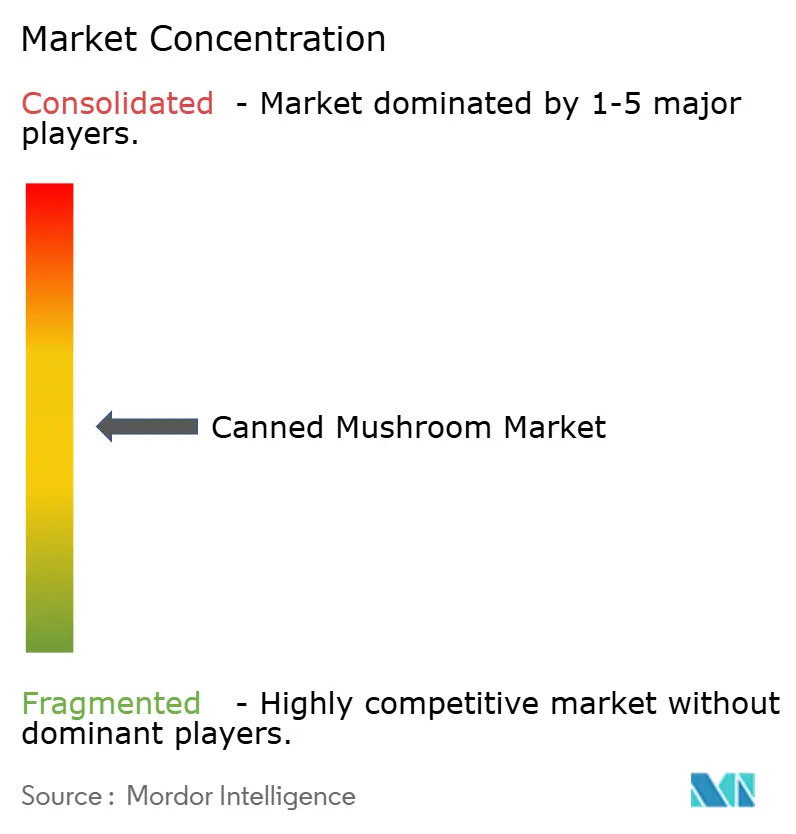

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canned Mushroom Market Analysis by Mordor Intelligence

The canned mushroom market size is expected to increase from USD 9.83 billion in 2025 to USD 10.35 billion in 2026 and reach USD 13.08 billion by 2031, growing at a CAGR of 5.46% over 2026-2031. Demand for convenient foods continues to rise, and foodservice applications are expanding, driving innovations in can-lining technologies. Regulatory changes, particularly the European Union's ban on Bisphenol A (BPA) coatings and the USDA's organic mushroom directive, create cost pressures while opening opportunities for premium pricing. Labor shortages and climate changes are causing raw material cost fluctuations, prompting the industry to invest more in automation and vertical integration. Consumers increasingly prefer plant-based diets, strengthening mushrooms' role as a popular protein alternative and boosting sales in retail and foodservice sectors. Producers are striving to meet new safety standards and differentiate themselves with organic certifications and unique product formats, creating potential for consolidation in a moderately competitive market.

Key Report Takeaways

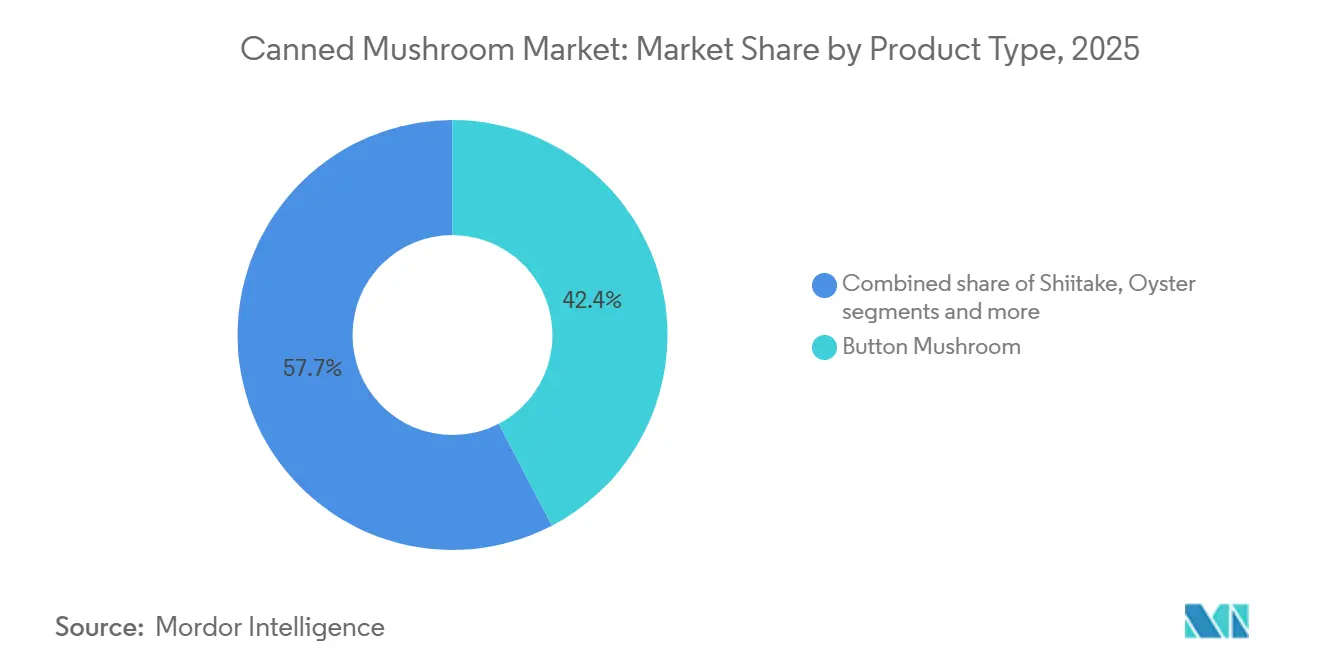

- By product type, Button mushroom held 42.35% of canned mushroom market share in 2025, whereas Shiitake posted the highest forecast CAGR at 6.28% through 2031.

- By form, Pieces and Stems captured 38.68% share of the canned mushroom market size in 2025, while Sliced mushrooms are projected to advance at a 7.05% CAGR between 2026-2031.

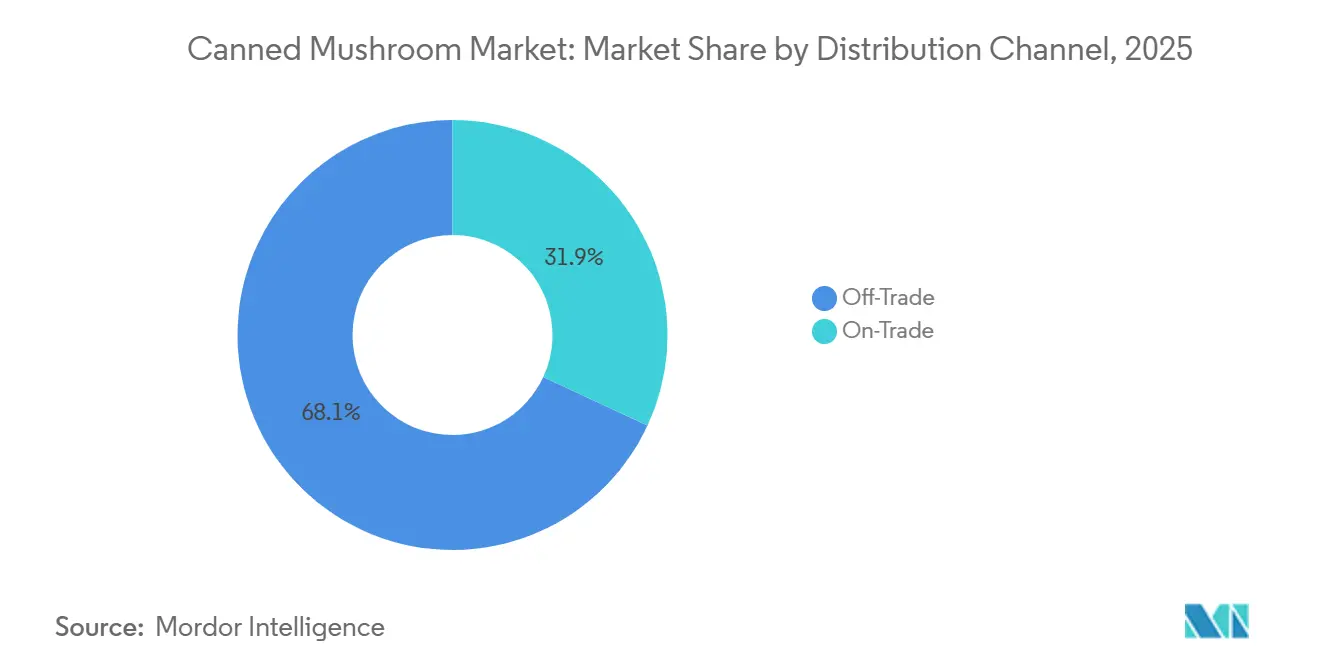

- By distribution channel, Off-Trade dominated with 68.08% revenue share in 2025, yet On-Trade is expected to expand at a 6.07% CAGR to 2031.

- By geography, Asia-Pacific led with 34.18% 2025 share, whereas Europe is forecast to register the fastest growth at 7.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Canned Mushroom Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient food products | +1.2% | Global, with urban concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Increasing adoption of canned mushrooms in foodservice establishments | +0.9% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Long shelf-life advantage over fresh and frozen options | +0.8% | Global, particularly Middle East, Africa, and Latin America with cold-chain gaps | Long term (≥ 4 years) |

| Adoption of plant-based diets and veganism | +1.0% | North America, Europe, Australia | Medium term (2-4 years) |

| Innovation in canning and processing technologies | +0.7% | North America, Europe, China | Long term (≥ 4 years) |

| Culinary versatility using canned mushrooms | +0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient food products

Rising demand for convenient food products is significantly supporting the growth of the canned mushroom market. Modern consumers are increasingly seeking ready-to-use and time-saving food ingredients that simplify meal preparation while offering longer shelf life and easy storage. Canned mushrooms are widely preferred in household cooking, restaurants, and processed food applications because they require minimal preparation and remain available year-round. The demand for convenient food products, including canned mushrooms, has increased substantially due to modern fast-paced lifestyles and changing consumption habits. According to the U.S. Census Bureau, the millennial population in the United States exceeded 74 million individuals in 2024, and this consumer group has played a major role in driving demand for convenient packaged foods[1]Source: United States Census Bureau, "National Population by Characteristics: 2020-2024", census.gov. Millennials are increasingly prioritizing quick meal solutions that align with busy work schedules and urban lifestyles.

Increasing adoption of canned mushrooms in foodservice establishments

Increasing adoption of canned mushrooms in foodservice establishments is contributing significantly to the growth of the canned mushroom market. Restaurants, hotels, cafés, quick-service restaurants, and institutional catering providers increasingly utilize canned mushrooms due to their convenience, long shelf life, and consistent year-round availability. Canned mushrooms help foodservice operators reduce preparation time, minimize food wastage, and maintain operational efficiency in high-volume kitchens. Their widespread use in pizzas, burgers, soups, pasta dishes, salads, and ready meals continues to support strong commercial demand. In addition, the growing popularity of plant-based menu offerings is further accelerating mushroom usage across foodservice applications. According to The Good Food Institute, plant-based protein sales in the U.S. foodservice industry reached USD 289 million in 2024, with mushrooms serving as a significant ingredient in plant-based recipes due to their meat-like texture and umami flavor profile[2]Source: The Good Food Institute, "Plant-based foods in U.S. foodservice", gfi.org.

Long shelf-life advantage over fresh and frozen options

Long shelf-life advantage over fresh and frozen options is playing an important role in supporting demand for canned mushrooms globally. Unlike fresh mushrooms, which are highly perishable and require immediate consumption or refrigerated storage, canned mushrooms can be stored for extended periods without significant quality deterioration. This extended shelf stability makes canned mushrooms highly suitable for household stocking, retail distribution, foodservice operations, and processed food manufacturing. In comparison to frozen mushrooms, canned products also offer easier storage and transportation without dependence on cold-chain logistics. The reduced risk of spoilage and food wastage further increases their appeal among consumers and commercial buyers. In addition, canned mushrooms provide year-round product availability regardless of seasonal cultivation fluctuations, ensuring stable supply for manufacturers and foodservice establishments. Their convenience, durability, and cost-efficiency continue to strengthen consumer preference for shelf-stable mushroom products.

Adoption of plant-based diets and veganism

Adoption of plant-based diets and veganism is significantly contributing to the growth of the canned mushroom market. Mushrooms are increasingly being used as a meat alternative due to their rich umami flavor, versatile culinary applications, and texture that closely resembles meat in various recipes. Consumers following vegan, vegetarian, and flexitarian diets are incorporating mushrooms into burgers, pasta dishes, soups, pizzas, and ready meals as part of healthier and sustainable eating habits. The growing popularity of plant-based food consumption is expanding demand for convenient mushroom products, including canned formats that offer easy storage and year-round availability. According to The Vegan Society, approximately 2.5 million people, representing nearly 3% of the population in Great Britain in 2024, followed vegan or plant-based diets[3]Source: The Vegan Society, "Nationwide trends highlight growing shift toward plant-based diets", vegansociety.com . This increasing consumer shift toward plant-based lifestyles is encouraging food manufacturers and foodservice operators to integrate mushrooms more extensively into plant-based product formulations and menu offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from fresh and frozen mushrooms | -0.8% | North America, Europe, Australia with mature cold-chain infrastructure | Short term (≤ 2 years) |

| Price volatility of raw mushrooms, metal packaging, and transportation | -1.1% | Global, acute in import-dependent markets | Short term (≤ 2 years) |

| Stringent food safety, labeling, and packaging regulations across countries | -0.5% | Europe, North America, Japan | Medium term (2-4 years) |

| Taste and texture degradation during canning | -0.4% | Global, particularly premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from fresh and frozen mushrooms

Competition from fresh and frozen mushrooms remains a major challenge for the canned mushroom market. Many consumers prefer fresh mushrooms due to their natural texture, flavor, and perception of higher nutritional quality compared to canned alternatives. Frozen mushrooms also provide longer shelf life while retaining characteristics closer to fresh products, making them attractive for both household and foodservice applications. Increasing consumer preference for minimally processed and preservative-free foods is further supporting demand for fresh and frozen mushroom categories. In addition, improvements in cold-chain logistics and refrigerated retail infrastructure have enhanced the availability and accessibility of fresh and frozen mushrooms across many regions. Foodservice operators and premium restaurants often favor fresh mushrooms for gourmet preparations and presentation quality.

Price volatility of raw mushrooms, metal packaging, and transportation

Price volatility of raw mushrooms, metal packaging, and transportation costs remains a significant challenge for the canned mushroom market. Mushroom cultivation is highly sensitive to fluctuations in labor costs, agricultural inputs, weather conditions, and energy expenses, which can directly impact raw material pricing. In addition, rising prices of steel and aluminum used for metal cans increase overall packaging costs for manufacturers. Transportation and logistics expenses have also become increasingly volatile due to fuel price fluctuations, supply chain disruptions, and international trade uncertainties. These cost pressures can reduce profit margins for canned mushroom producers and create pricing instability across retail and foodservice channels. Smaller manufacturers are particularly vulnerable to sudden increases in production and distribution costs due to limited financial flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Button Dominance Faces Shiitake Disruption

Button mushrooms accounted for the largest share of the global canned mushroom market in 2025, contributing 42.35% of total revenue. The dominance of this segment is primarily attributed to the widespread consumer acceptance of button mushrooms due to their mild flavor, versatile usage, and affordability. Button mushrooms are extensively used in pizzas, soups, pasta, salads, burgers, ready meals, and processed food products, making them highly suitable for canning applications. Their long-standing popularity across both household and foodservice consumption channels further supports strong market demand. In addition, button mushrooms have well-established cultivation and supply chain infrastructure globally, ensuring consistent production and availability for processing companies. Manufacturers also prefer button mushrooms for canned products because of their stable texture, appearance, and extended shelf-life characteristics.

Shiitake mushrooms are projected to register the fastest CAGR of 6.28% through 2031 in the canned mushroom market. Growth of this segment is largely supported by increasing consumer interest in premium, exotic, and functional food ingredients. Shiitake mushrooms are gaining popularity due to their rich umami flavor and perceived health benefits, including immune support and nutritional value. Rising adoption of Asian cuisine globally has also significantly increased demand for shiitake mushrooms in soups, noodles, sauces, and ready-to-eat meals. Food manufacturers are increasingly incorporating canned shiitake mushrooms into gourmet and premium processed food offerings to cater to evolving consumer preferences.

By Form: Sliced Gains on Labor Economics

Pieces and Stems accounted for the largest share of the canned mushroom market in 2025, representing 38.68% of total revenue. The strong market position of this segment is mainly driven by its cost-effectiveness and wide applicability across processed food and foodservice industries. Pieces and stems are extensively used in pizzas, soups, sauces, casseroles, frozen meals, and institutional catering applications where uniform appearance is less critical. Food manufacturers and restaurants prefer this form due to its lower pricing compared to whole or premium mushroom formats. The segment also benefits from high bulk demand from quick-service restaurants and large-scale food processors seeking economical mushroom ingredients for prepared meals. Additionally, easy storage, convenient handling, and compatibility with multiple cuisines continue to support strong adoption globally.

Sliced mushrooms are projected to register the fastest CAGR of 7.05% during the forecast period from 2026 to 2031. Growth in this segment is primarily supported by rising consumer preference for convenience-oriented and ready-to-use food ingredients. Sliced canned mushrooms are increasingly favored in household cooking due to their ease of use, consistent appearance, and reduced preparation time. The growing popularity of homemade pizzas, pasta dishes, salads, and quick meal preparations is also driving demand for sliced mushroom formats. Foodservice operators and ready-meal manufacturers are adopting sliced mushrooms to improve product presentation and maintain portion consistency across applications.

By Distribution Channel: Off-Trade Scale Versus On-Trade Velocity

The off-trade segment accounted for the largest share of the global canned mushroom market in 2025, contributing 68.08% of total revenue. The dominance of this channel is primarily driven by strong consumer purchases through supermarkets, hypermarkets, grocery stores, convenience stores, and online retail platforms. Off-trade channels provide consumers with easy access to a wide variety of canned mushroom products, packaging sizes, and price ranges suitable for household consumption. The increasing preference for convenient pantry staples and long shelf-life food products has further strengthened retail demand for canned mushrooms. In addition, promotional activities, bulk purchase discounts, and expanding private-label offerings across organized retail chains continue to support segment growth. Rising urbanization and growth in home cooking trends have also increased household consumption of canned mushrooms globally.

The on-trade segment is projected to register the fastest CAGR of 6.07% through 2031 in the canned mushroom market. Growth in this segment is largely supported by increasing consumption of mushrooms across restaurants, hotels, cafés, quick-service restaurants, and institutional catering services. Canned mushrooms are widely used in foodservice operations because they offer convenience, extended shelf life, and consistent year-round availability compared to fresh mushrooms. Rising global demand for pizzas, pasta, burgers, soups, and Asian cuisine dishes is also contributing to higher mushroom usage within commercial food preparation. Foodservice operators increasingly prefer canned mushrooms to reduce food wastage, simplify inventory management, and improve operational efficiency.

Geography Analysis

Asia-Pacific accounted for the largest share of the global canned mushroom market in 2025, contributing 34.18% of total revenue. The region’s dominance is primarily supported by large-scale mushroom cultivation and processing activities in countries such as China, India, Japan, and South Korea. China remains one of the world’s leading producers and exporters of canned mushrooms, benefiting from strong agricultural infrastructure and cost-effective manufacturing capabilities. Rising consumption of processed and convenience foods across urban populations is also significantly supporting market growth in the region. In addition, mushrooms are widely used in Asian cuisines, including soups, noodles, stir-fry dishes, and ready meals, which sustains strong domestic demand for canned mushroom products.

Europe is projected to register the fastest CAGR of 7.28% through 2031 in the canned mushroom market. Growth in the region is primarily driven by rising demand for convenient, shelf-stable, and healthy food ingredients among consumers. Increasing popularity of vegetarian, vegan, and flexitarian diets is encouraging higher mushroom consumption across various food applications. European consumers are also showing strong interest in gourmet cooking and international cuisines, which is increasing the use of canned mushrooms in household and foodservice preparations. The expansion of ready-to-eat meals, frozen foods, pizzas, and pasta products is further contributing to higher demand for processed mushroom ingredients.

North America represents a significant market for canned mushrooms due to high consumption of convenience foods and strong demand from quick-service restaurants and food processing industries. The United States and Canada continue to witness stable demand for canned mushrooms in pizzas, burgers, casseroles, soups, and packaged meals. South America is gradually emerging as a developing market supported by increasing urbanization, expanding retail infrastructure, and rising adoption of processed food products. In the Middle East and Africa, market growth is being supported by the increasing penetration of international food chains, rising tourism activities, and growing demand for shelf-stable imported food products.

Competitive Landscape

The canned mushroom market is moderately fragmented, with competition distributed among multinational food processing companies, regional mushroom cultivators, private-label suppliers, and specialty canned food manufacturers. Market participants compete primarily on product quality, pricing, processing capabilities, distribution reach, and supply chain efficiency. Leading companies maintain strong market positions through large-scale cultivation operations, integrated processing facilities, and extensive export networks. The market also includes numerous regional producers that cater to domestic consumption and local foodservice industries. Product differentiation is increasingly focused on mushroom variety, packaging formats, organic certifications, and clean-label positioning.

Companies operating in the canned mushroom market are increasingly investing in product innovation, operational efficiency, and geographic expansion strategies to strengthen their competitive positions. Manufacturers are introducing premium mushroom varieties such as shiitake and specialty blends to address growing consumer demand for gourmet and functional food ingredients. Many companies are also focusing on sustainable cultivation practices, energy-efficient processing technologies, and recyclable packaging solutions to align with evolving environmental regulations and consumer preferences. Strategic partnerships with supermarkets, foodservice chains, and private-label retailers are becoming important competitive approaches across key markets.

Regional competition varies significantly depending on mushroom cultivation capacity, processing infrastructure, consumer consumption patterns, and retail development. Asia-Pacific remains highly competitive due to the strong presence of large-scale producers and exporters, particularly in China, which dominates global canned mushroom supply. In Europe and North America, competition is increasingly centered around premium-quality products, organic offerings, and convenience-oriented packaging formats. Foodservice demand from restaurants, hotels, and ready-meal manufacturers is also influencing competitive strategies across developed markets.

Canned Mushroom Industry Leaders

-

Bonduelle Group

-

B&G Foods Inc.

-

Okechamp S.A.

-

Giorgio Fresh Co.

-

Del Monte Pacific Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Versilfood initiated the expansion of its Camaiore production center in Italy as part of a strategic growth plan aimed at significantly increasing industrial capacity and strengthening operational efficiency. The company announced the installation of four fully automated production lines and a new advanced processing facility designed to improve control across the entire supply chain. The expansion is expected to quadruple the company’s production capacity while supporting higher-quality processing and packaging standards for mushrooms, fruits, and vegetables.

- July 2025: Giorgi Mushroom Co., a subsidiary of The Giorgi Companies, Inc. (Giorgi), acquired a majority stake in L.F. Lambert Spawn Co. (Lambert). Lambert specialized in spawn production and agricultural innovation. This strategic move strengthened Giorgi Mushroom Co.'s operational capabilities and ensured supply chain stability for its clientele.

- July 2025: Urban Farm-It, known for its gourmet mushroom offerings, partnered with Oakland International, a key player in logistics and supply chain management. Their collaboration distributed mushrooms throughout the United Kingdom. Starting with Lion's Mane mushrooms, the partnership expanded to include a diverse range of locally sourced gourmet mushrooms tailored for UK retailers and foodservice entities.

Global Canned Mushroom Market Report Scope

Canned mushrooms are processed and preserved mushroom products that are packed in airtight metal cans or containers to extend shelf life and maintain product usability for long periods. The canned mushroom market is segmented into product type, form, distribution channel and geography. By product type, the market is segmented by button, shiitake, oyster, portobello, morel and others. By form, the market is segmented into whole, sliced, pieces and stems and others. By distribution channel, the market is segmented into on-trade and off-trade channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Button |

| Shiitake |

| Oyster |

| Portobello |

| Morel and Others |

| Whole |

| Sliced |

| Pieces and Stems |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Button | |

| Shiitake | ||

| Oyster | ||

| Portobello | ||

| Morel and Others | ||

| By Form | Whole | |

| Sliced | ||

| Pieces and Stems | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the canned mushrooms market?

The canned mushrooms market size is USD 9.83 billion in 2025 and is expected to reach USD 12.41 billion by 2030.

Which region holds the largest share of global sales?

Asia-Pacific leads with 34.07% of the canned mushrooms market thanks to China’s dominant production base.

What segment is growing fastest by product type?

Shiitake mushrooms are forecast to rise at a 6.23% CAGR through 2030, outpacing other varieties.

Why are foodservice operators increasing their use of canned mushrooms?

Extended shelf life, price stability, and suitability for plant-forward menus make canned mushrooms market products attractive amid supply-chain volatility.

Page last updated on: