Edible Fungus Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

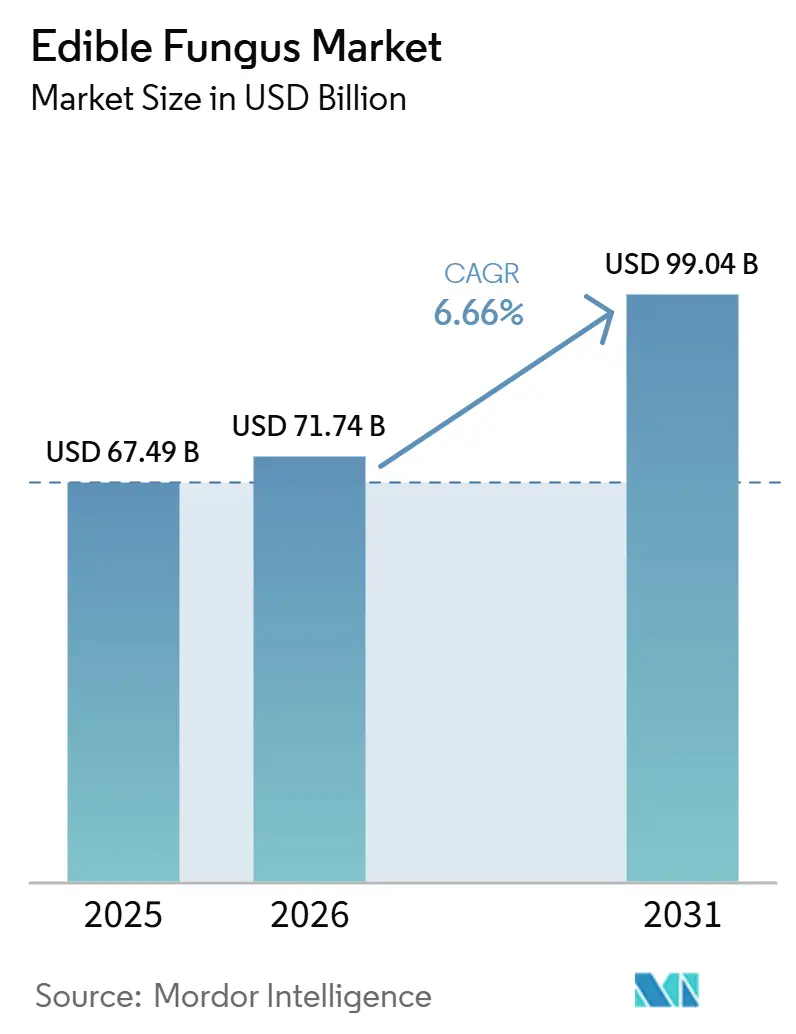

| Market Size (2026) | USD 71.74 Billion |

| Market Size (2031) | USD 99.04 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

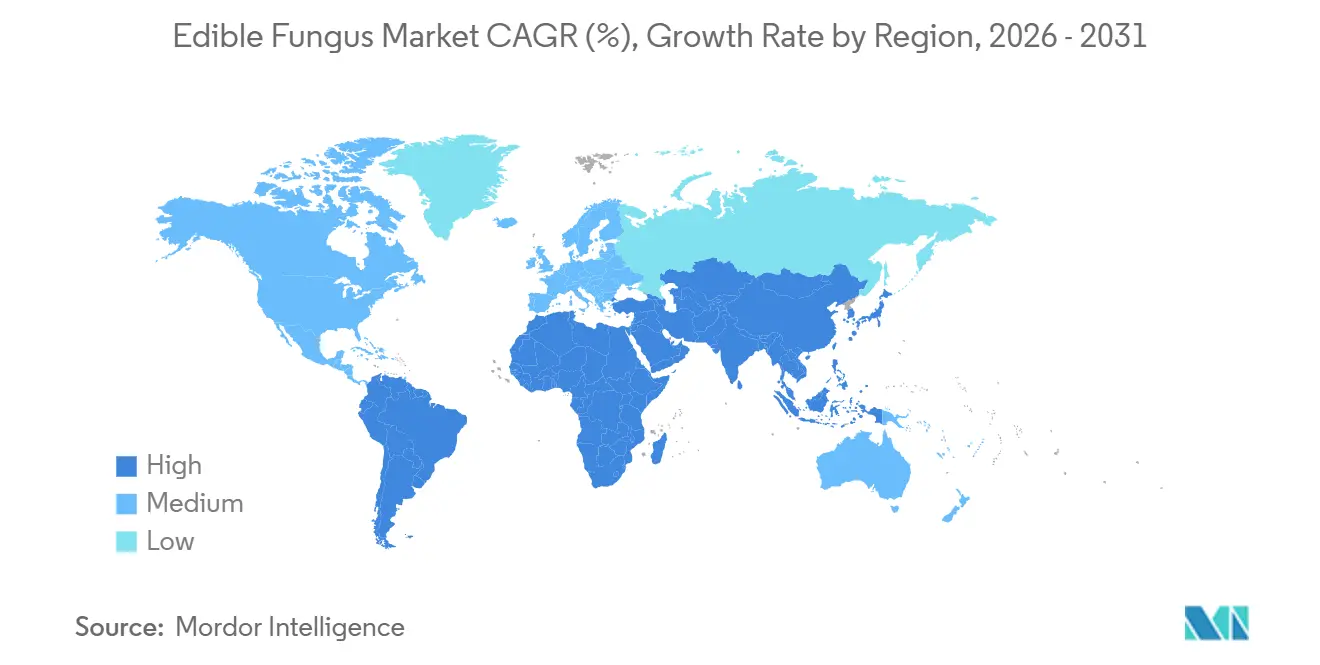

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Edible Fungus Market Analysis by Mordor Intelligence

The Edible Fungus Market size is expected to grow from USD 67.49 billion in 2025 to USD 71.74 billion in 2026 and is forecast to reach USD 99.04 billion by 2031 at 6.66% CAGR over 2026-2031. Increasing consumer demand for complete-protein foods, regulatory approvals for mycoprotein platforms, and advancements in automated climate-controlled farms are driving the transformation of mushroom cultivation from a cottage industry to an industrial protein source. Producers are utilizing spent mushroom substrate to generate biogas and improve soil quality, adopting a circular approach that reduces production costs and appeals to sustainability-focused investors. While Asia-Pacific dominates regional demand, the edible fungus market is also expanding in the Middle East and Africa, supported by government investments in refrigerated logistics to reduce post-harvest losses. Competitive intensity is increasing as growers vertically integrate into substrate manufacturing and value-added processing to mitigate commodity price volatility.

Key Report Takeaways

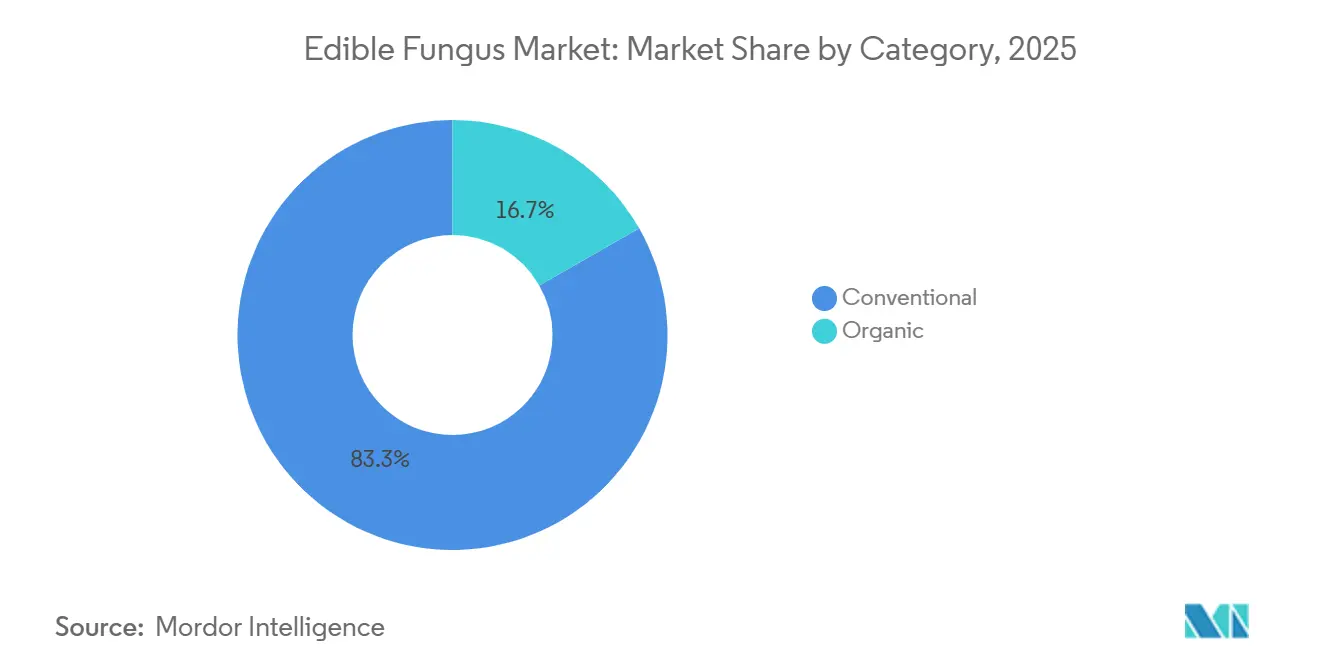

- By category, conventional cultivation accounted for 83.26% edible fungus market share in 2025; organic methods will register the fastest 7.84% CAGR through 2031.

- By mushroom type, button varieties dominated with 60.39% of 2025 volume, whereas reishi is projected to grow at a 7.29% CAGR to 2031.

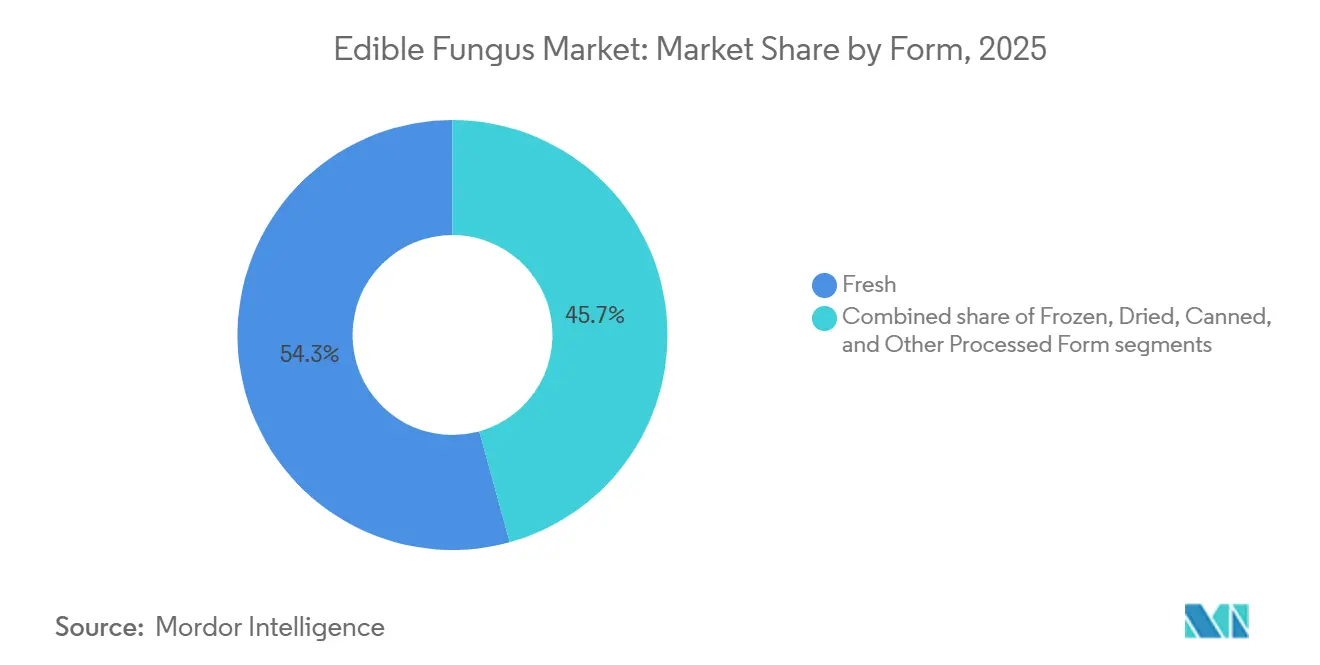

- By form, the fresh segment captured 54.29% of 2025 sales, and dried mushrooms are on track for a 7.48% CAGR through 2031.

- By distribution channel, off-trade retail held 64.78% of 2025 revenue; on-trade foodservice will advance at a 7.54% CAGR through 2031.

- By geography, Asia-Pacific held 50.47% of 2025 revenue, while the Middle East and Africa is forecast to expand at an 8.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Edible Fungus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High consumer shift to plant-based proteins | +1.2% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising health consciousness and functional food adoption | +1.0% | Global, led by North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Expansion of cold-chain and retail infrastructure in emerging economies | +0.9% | Middle East and Africa, South America, Southeast Asia | Long term (≥ 4 years) |

| Technological innovations in controlled-environment agriculture | +0.8% | North America, Europe, China, Japan | Short term (≤ 2 years) |

| Valorization of agri-waste substrates lowering production costs | +0.7% | Global, with early adoption in Europe, China, India | Medium term (2-4 years) |

| Mycelium-based ingredient commercialization in alt-meat and biomaterials | +0.6% | North America, Europe, with pilot projects in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High consumer shift to plant-based proteins

As dietary preferences shift toward plant-based proteins, fungi are becoming a preferred source, offering all nine essential amino acids and achieving protein densities of up to 22% on a dry-matter basis. In 2025, Enifer made a notable move by submitting its PEKILO mycoprotein to the FDA for a Generally Recognized as Safe (GRAS) designation. With a target composition of 50% protein and 35% fiber, PEKILO is designed to replace soy isolates in meat alternatives. This regulatory milestone highlights a broader trend in the food industry: manufacturers are expanding their protein sources to reduce reliance on soy and address concerns over price volatility and allergens. Retail data reflects this shift: in 2024, U.S. per-capita mushroom availability reached 3.5 pounds, with organic mushrooms accounting for 8% of the volume despite higher prices. In May 2025, innovations such as texturized pea-shiitake protein blends, developed through high-moisture extrusion, demonstrated fungi's potential to improve mouthfeel and umami flavor in plant-based products. These advancements tackle the texture issues that previously limited consumer acceptance. The rising vegan population is further driving mushroom demand, as seen in the UK, where the number of vegans increased by 1.1 million between 2023 and 2024, reaching 2.5 million or approximately 4.7% of the adult population, according to the Jewish, Vegan, Sustainable Organization[1]Source: Jewish, Vegan, Sustainable Organization, "Veganism on the Rise in the UK", jvs.org.uk .

Rising health consciousness and functional food adoption

Specialty mushrooms are evolving from culinary ingredients to therapeutic adjuncts, driven by clinical evidence that links their bioactive compounds to immune modulation and neuroprotection. In 2024, the US Department of Agriculture reported that per capita fresh mushroom consumption in the United States reached 3.3 pounds[2]Source: US Department of Agriculture, "Economic Research Service", usda.gov. Human trials have demonstrated that Hericium erinaceus, at doses of up to 1 gram per day for 16 weeks, stimulates nerve growth factor pathways and improves mild cognitive impairment scores. Preclinical studies have revealed the hypoglycemic and anticancer potential of Ganoderma lucidum's triterpenes and polysaccharides, prompting supplement manufacturers to standardize ganoderic acid content. Reflecting the industry's focus on quality-controlled extracts, Real Mushrooms acquired Mushroom Science in February 2026, consolidating two leading functional supplement brands. Controlled studies have also shown that shiitake polysaccharides can mitigate obesity-related cognitive impairment by modulating the gut microbiota, emphasizing the importance of the gut-brain axis.

Expansion of cold-chain and retail infrastructure in emerging economies

In the Middle East, Africa, and parts of South America, the lack of adequate refrigeration between farm and retail results in post-harvest losses of up to 50% of annual mushroom production. This deficiency in cold-chain infrastructure limits mushroom consumption in these regions. FAO data from 2024 shows that global post-harvest losses from harvest to retail average 13.8%. However, in Sub-Saharan Africa, losses for fruits and vegetables range between 20-50%, with mushrooms being particularly vulnerable due to their shelf life of less than 4 days at ambient temperature. Governments in the Middle East are investing in refrigerated logistics as part of their food security strategies. For instance, the UAE and Saudi Arabia are allocating funds to develop temperature-controlled distribution hubs, which not only extend produce shelf life but also support the import of specialty varieties. Similarly, in South America, Brazil and Chile are enhancing port facilities to better accommodate perishable cargo. These infrastructure improvements aim to unlock latent demand for mushrooms in regions where they are culturally valued but logistically challenging to access. The economic benefits are significant: extending a mushroom's shelf life from 3 to 7 days doubles the grower's service radius, effectively increasing the addressable market area fourfold.

Technological innovations in controlled-environment agriculture

Controlled-environment agriculture is removing the dependence of mushroom production on seasonal and geographic factors, enabling consistent year-round cultivation in urban areas closer to consumers. In 2025, China's Quzhou smart mushroom farm utilized IoT sensors, automated climate controls, and real-time yield optimization algorithms to produce 49,100 tonnes. These technologies adjusted temperature and humidity to meet species-specific requirements. In land-constrained markets, container-based cultivation systems are becoming increasingly popular: modular units can produce 500 kilograms of oyster mushrooms per month in a single 40-foot container, with vertical stacking significantly increasing output per square meter. Aeroponics trials are showing 30% faster mycelial colonization compared to traditional substrate bags by delivering nutrients through mist rather than solid media. Japan's agricultural input price index, benchmarked at 100 in 2020, rose to 130.0 in 2024, driven by higher electricity and heating fuel costs. These increases have tightened margins for substrate-based cultivation, which typically requires fruiting temperatures of 15-20°C. To address these challenges, the sector is adopting hybrid models that combine renewable energy with cultivation facilities and focusing on genetic selection for strains that can tolerate a wider range of temperatures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short shelf-life and post-harvest losses | -0.9% | Global, acute in Sub-Saharan Africa, Southeast Asia, parts of South America | Short term (≤ 2 years) |

| Energy and raw-material price volatility | -0.7% | Europe, Japan, North America (high energy costs); global for substrate inputs | Short term (≤ 2 years) |

| Stringent pesticide-residue compliance | -0.4% | Europe (EFSA), North America (FDA), Japan (MHLW) | Medium term (2-4 years) |

| Skilled-labour shortages in specialty fungi | -0.5% | Japan, Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Short shelf-life and post-harvest losses

Perishability is a critical challenge for the sector. Fresh mushrooms, for example, have a shelf life of less than four days at ambient temperatures, and post-harvest losses can reach up to 50% in regions without refrigerated logistics. FAO data indicates that global post-harvest losses from harvest to retail average 13.8%. However, in Sub-Saharan Africa, fruits and vegetables experience losses ranging from 20-50%, with mushrooms being particularly affected due to their high moisture content and susceptibility to enzymatic browning. On-site cold storage can reduce losses by 13.2 percentage points, but the significant capital investment required for refrigeration infrastructure excludes smallholder producers in emerging markets. This issue is further exacerbated by the fact that mushrooms achieve premium pricing only when they remain visually pristine. Quality degradation within 48 hours of harvest often forces growers to either discount or discard their produce. To address this, growers are adopting modified-atmosphere packaging, which extends shelf life to 7-10 days, and are utilizing dehydration or freeze-drying techniques to stabilize products for export markets. However, these measures increase production costs by 15-25%, compressing margins unless retail prices are adjusted upward.

Energy and raw-material price volatility

Energy expenses, which vary based on geography and facility design, represent 16-77% of operating costs in controlled-environment agriculture. This variability leaves growers vulnerable to electricity price shocks that can threaten profitability within a single billing cycle. In vertical farming, optimized leafy greens require energy consumption ranging from 150-350 kWh per kilogram. Similarly, mushrooms demand comparable energy inputs, particularly for climate control during their fruiting phase. In 2024, Japan's agricultural input price index increased to 130.0 from a 2020 baseline of 100. This rise, driven by inflation in electricity and heating fuels, compressed margins for substrate cultivation, which requires fruiting temperatures of 15-20°C. Substrate input costs, including wheat straw, sawdust, and chicken manure, remain highly volatile, influenced by agricultural commodity cycles and livestock production volumes. A life-cycle costing study conducted across three European climate regions highlighted significant differences: Northern operations incurred EUR 209.13 per tonne for spent substrate due to elevated horse manure costs, while Mediterranean operations achieved negative EUR 30.27 per tonne, benefiting from favorable wheat straw-chicken manure blends and higher yields. Growers are adopting strategies such as long-term substrate supply contracts and on-site renewable energy installations to mitigate risks, but the high capital requirements limit these measures to larger operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Organic Premiums Offset Yield Penalties

In 2025, conventional production held a commanding 83.26% market share, thanks to its cost advantages and well-established supply chains that ensure consistent quality at scale. Growers using conventional methods leverage synthetic fertilizers and pesticides, boosting yields and curbing crop losses. This strategy allows them to set price points that appeal to the mass market. On the other hand, organic cultivation is on an upward trajectory, projected to grow at 7.84% through 2031. This growth is attributed to maturing certification frameworks and the ability to command premium prices, even if it means accepting lower yields. In 2024, U.S. organic mushrooms accounted for 8% of the volume, a dip from the 9-10% range in previous years. Notably, Agaricus varieties made up 80% of this organic volume, underscoring the dominance of button mushrooms in certified production.

The organic segment grapples with a structural challenge: the certification process mandates a 3-year transition period. During this time, growers bear the costs of organic inputs but miss out on premium pricing, leading to cash-flow challenges that can sideline smaller operators. Moreover, integrated pest management systems, which swap out synthetic fungicides for biological controls, necessitate increased labor and agronomic expertise, driving up costs. Despite these challenges, consumers, especially in North America and Europe, continue to pay a premium for organic mushrooms. Their willingness is fueled by health perceptions and environmental concerns, with organic foods making up over 10% of grocery spending in these regions. While conventional production thrives in price-sensitive markets and foodservice channels, where cost per serving is paramount, organic growers in Europe tap into premium retail channels and direct-to-consumer sales, justifying their higher production costs. Meanwhile, in the Asia-Pacific, conventional producers benefit from low labor costs and intensive substrate formulations.

By Mushroom Type: Button Dominance Meets Functional Variety Surge

In 2025, button mushrooms captured 60.39% of the market, thanks to their versatile flavor, ease of mechanical harvesting, and established roles in pizzas, pastas, and burgers. Decades of selective breeding have enhanced button mushrooms' yield, disease resistance, and shelf life, establishing a cost advantage that's tough for competitors to challenge. Meanwhile, reishi mushrooms are on a growth trajectory, projected to rise at 7.29% through 2031. This surge is fueled by mounting clinical evidence linking triterpenes to benefits in neurological health and immune modulation. A May 2025 review in Nutrients highlighted the hypoglycemic and anticancer properties of Ganoderma lucidum polysaccharides in preclinical models, prompting supplement manufacturers to standardize ganoderic acid content.

The intersection of functional mushrooms and nutraceuticals is becoming pronounced: In April 2026, Vietnam began commercializing reishi products, including dried mushrooms, extracts, and wine sourced from Ta Dung National Park. Additionally, intercropping pilots beneath cashew trees produced a yield of 128 kilograms, fetching 250,000 VND per kilogram. This diversification is reshaping the market landscape, with growers gravitating towards varieties that resonate with regional culinary traditions or health claims, rather than merely competing on the price of commodity button mushrooms.

By Form: Fresh Convenience Versus Dried Shelf Stability

In 2025, fresh mushrooms represented 54.29% of sales, driven by consumers' preference for their texture and visual appeal in sautéed, grilled, and raw dishes. Fresh mushrooms can achieve premium pricing when quality is maintained. However, their perishability limits their distribution radius, requiring growers to operate within 200 miles of major retail markets. The fresh segment is also a focal point for product innovation: value-added formats such as pre-sliced, marinated, and ready-to-cook mushrooms are increasingly gaining shelf space in refrigerated produce sections. Meanwhile, dried mushrooms are expected to grow at 7.48% through 2031. Their extended shelf life of 12-24 months, enabled by dehydration, creates export opportunities to markets without cold-chain infrastructure.

Dried mushrooms are also used as functional ingredients in soups, sauces, and seasoning blends. When rehydrated, they regain their texture, and the umami compounds, which concentrate during dehydration, enhance flavor. Frozen mushrooms offer a middle ground: they preserve texture better than drying and have a shelf life of 6-12 months. However, they require a continuous cold-chain, which increases logistics costs. Canned mushrooms primarily serve institutional food services and long-term pantry storage but are losing retail share as consumers shift toward fresh and minimally processed options. Cultural preferences influence the form mix: Asian markets consume significant volumes of dried mushrooms for traditional medicine and culinary uses, while North American and European consumers predominantly prefer fresh mushrooms for salads and sautés. Processing technology continues to advance: freeze-drying, which retains more bioactive compounds than conventional dehydration, is creating opportunities for premium dried products targeting the functional food market.

By Distribution Channel: Foodservice Recovery Outpaces Retail Maturity

In 2025, off-trade retail dominated sales with a 64.78% share, underscoring the pivotal role of supermarkets and hypermarkets, where a significant 90% of Canadian consumers turn to purchase their mushrooms. These retail giants not only anchor the off-trade channel but also entice shoppers with a diverse selection, competitive pricing, and eye-catching visual merchandising, all of which spur impulse buys of fresh produce. While convenience and grocery stores cater to quick, fill-in purchases, their limited space and turnover constraints mean they typically offer just the button and portobello mushroom varieties. Online retail, the fastest-growing segment of the off-trade, is witnessing a surge as e-grocery platforms pour investments into cold-chain fulfillment and same-day delivery, ensuring product quality is upheld. This growth is further amplified by the deepening internet penetration. For instance, the International Telecommunication Union (ITU) reported a notable uptick in global internet access: 74% of the global population was using the internet in 2025, a rise from 71% in 2024[3]Source: International Telecommunication Union (ITU), "Individuals Using Internet", itu.int. Meanwhile, the on-trade foodservice sector is set to expand at a rate of 7.54% through 2031. This growth is attributed to restaurant operators incorporating specialty mushroom varieties into their plant-forward menus and a resurgence in consumer dining out, post-pandemic.

Foodservice sub-channels are charting distinct growth paths: lodging and casino outlets anticipate an 11.4% volume CAGR, while recreation venues are eyeing a 12.2% uptick. This surge is largely driven by the rising demand for premium ingredients, such as lion's mane and maitake, spurred by the trend of experiential dining. Quick-service and full-service restaurants, holding the title of the largest absolute volume channels, are witnessing a dollar growth surge in dishes like burgers, pizzas, and pasta, thanks to the inclusion of white mushrooms. The on-trade channel not only offers growers a premium per-pound pricing but also fosters direct relationships, allowing for tailored variety customization. However, this comes with the caveat of needing consistent quality and a year-round supply, a challenge for many smaller producers. Meanwhile, mass merchandisers and club stores are capitalizing on bulk packaging and private-label programs, resonating well with cost-conscious households. The channel dynamics are also evolving: some retailers are strategically positioning mushrooms near meat counters, a tactic that has shown promise in pilot programs by boosting basket sizes through encouraging substitution and complementary purchases. While online penetration faces hurdles due to the demands of temperature-controlled last-mile delivery, a burgeoning niche channel is emerging: subscription models for specialty and functional mushrooms, which deftly sidestep traditional retail avenues.

Geography Analysis

In 2025, Asia-Pacific, driven by substantial production in China, Japan, and India, contributed 50.47% of the global revenue. India, Thailand, and Indonesia are significantly increasing their production capacities to meet both domestic consumption and export demands. However, the region faces notable challenges. Japan experienced an 8.0% decline in its producer count in 2025, underscoring persistent labor shortages. Furthermore, rising energy costs have led to inflation, which has compressed profit margins, particularly for substrate cultivation processes that require climate-controlled environments.

The Middle East and Africa region stands out as the fastest-growing market, with a compound annual growth rate (CAGR) of 8.01%. Cold-chain infrastructure developments in the UAE and Saudi Arabia are playing a pivotal role in extending the shelf life of products and facilitating smoother import operations. In Nigeria, pilot farming initiatives have demonstrated that mushroom intercropping can generate an additional income of USD 7,406 per hectare compared to millet cultivation. Despite these advancements, the region continues to face significant hurdles, as inadequate infrastructure remains a bottleneck. In some sub-Saharan areas, spoilage rates still exceed 40%, highlighting the need for further investment in logistics and storage solutions.

In 2024, North America recorded an output of 669.9 million lb, valued at USD 1.1 billion. Pennsylvania emerged as the leading contributor, supplying 69% of the Agaricus mushrooms in the region. Canada fulfilled 25% of U.S. consumption through imports, while Mexico is actively scaling up its production capacity to offer cost-competitive fresh exports. In Europe, Germany produced 75,700 tonnes of mushrooms in 2024, with 98% of the output being button mushrooms. However, the number of growers in the region has dwindled to just 25, primarily due to challenges related to labor shortages and escalating energy costs. In South America, Brazil and Chile are driving market expansion, but the region faces a critical need for consumer education to shift mushrooms from being perceived as a specialty product to becoming a staple food item.

Competitive Landscape

The edible fungus market, defined by a combination of large-scale industrial producers and specialized regional operators, continues to exhibit a fragmented structure. This dynamic enables major players like Monaghan Mushrooms and Costa Group to capitalize on their extensive operational scale and robust distribution networks, thereby reinforcing their dominant positions in the market. Concurrently, this fragmentation creates opportunities for smaller producers who concentrate on niche segments, such as premium mushroom varieties, organic certifications, and direct consumer interactions, to carve out their own space in the market.

Labor shortages, which have reached a critical 20% vacancy rate across the industry, are driving companies to adopt automation technologies to maintain efficiency and competitiveness. Robotic harvesting systems, now capable of matching the productivity levels of skilled human workers, can harvest approximately 2,000 mushrooms per hour with precision and consistency. The industry's strategic priorities are increasingly shifting toward vertical integration and the adoption of advanced technologies. A notable example is the growing interest in mycelium-based ingredient commercialization, which allows companies to expand their applications beyond traditional food products. Infinite Roots' EUR 58 million Series B funding in 2024, the largest mycelium investment in Europe to date, exemplifies the sector's transition toward industrial biotechnology, particularly in the fields of alternative proteins and biomaterials.

Producers are actively exploring untapped opportunities, such as substrate diversification and waste valorization, to enhance sustainability and cost efficiency. By utilizing unconventional resources like bourbon stillage, oil palm residues, and recycled spent mushroom substrates, they are not only reducing input costs but also significantly lowering their environmental impact. At the same time, emerging disruptors are reshaping industry norms through innovations like controlled-environment agriculture and direct-to-consumer business models. By eliminating traditional supply chain intermediaries, these disruptors can command higher prices, leveraging their focus on superior quality and strong brand positioning. Demonstrating a commitment to innovation, Monterey Mushrooms has submitted a request to the FDA for approval to produce vitamin D2 mushroom powder, showcasing how established players are advancing value-added processing techniques to remain competitive in the evolving market landscape.

Edible Fungus Industry Leaders

-

Monaghan Mushrooms

-

Costa Group

-

Monterey Mushrooms

-

Okechamp

-

Shanghai Finc Bio-Tech

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Enifer completed construction of its commercial-scale mycoprotein factory in Finland, producing 3 million kilograms annually, equivalent to protein from 30,000 cows, marking the largest mycelium production facility in Europe and demonstrating industrial scalability of fungal protein manufacturing.

- January 2025: Infinite Roots received USD 58 million in Series B funding, led by Dr. Hans Riegel Holding. This represents the largest mycelium investment in Europe and enables the company to scale production through partnerships with existing fermentation infrastructure providers, including Bitburger Brewery Group.

- December 2024: Monterey Mushrooms submitted an FDA petition to produce vitamin D2 mushroom powder through UV light exposure of Agaricus bisporus mushrooms. This development expanded their processing capabilities and showcased their focus on functional food ingredients.

Global Edible Fungus Market Report Scope

Edible fungi are macrofungi (visible to the naked eye) with fleshy, edible fruiting bodies that are consumed for their nutritional value, flavor, and texture. The edible fungus market report is segmented by category, mushroom type, form, distribution channels, and geography. By category, the market is segmented into organic and conventional. By mushroom type, the market is segmented into button, shiitake, oyster, reishi, enoki, and other. By form, the market is segmented into fresh, frozen, dried, canned, and other. By distribution channel, the market is segmented into on-trade and off-trade. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. Market forecasts are provided in value (USD) and volume (tons).

| Organic |

| Conventional |

| Button Mushroom |

| Shiitake |

| Oyster |

| Reishi |

| Enoki |

| Other Types |

| Fresh |

| Frozen |

| Dried |

| Canned |

| Other Processed Form |

| On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets |

| Convenience and Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Category | Organic | |

| Conventional | ||

| By Mushroom Type | Button Mushroom | |

| Shiitake | ||

| Oyster | ||

| Reishi | ||

| Enoki | ||

| Other Types | ||

| By Form | Fresh | |

| Frozen | ||

| Dried | ||

| Canned | ||

| Other Processed Form | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets | |

| Convenience and Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global sales of edible fungi be by 2031?

The edible fungus market size is projected to reach USD 99.04 billion by 2031 at a 6.66% CAGR from 2026.

Which region grows the fastest?

The Middle East and Africa is forecast to expand at an 8.01% CAGR as cold-chain investments reduce post-harvest losses.

What share do button mushrooms hold?

Button varieties accounted for 60.39% of global volume in 2025, the largest share among mushroom types.

Why are energy costs a concern for growers?

In European controlled-environment farms electricity can reach 77% of operating expenses, exposing margins to price spikes.

Page last updated on: