Wood Vinegar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.91 Billion |

| Market Size (2031) | USD 7.60 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wood Vinegar Market Analysis by Mordor Intelligence

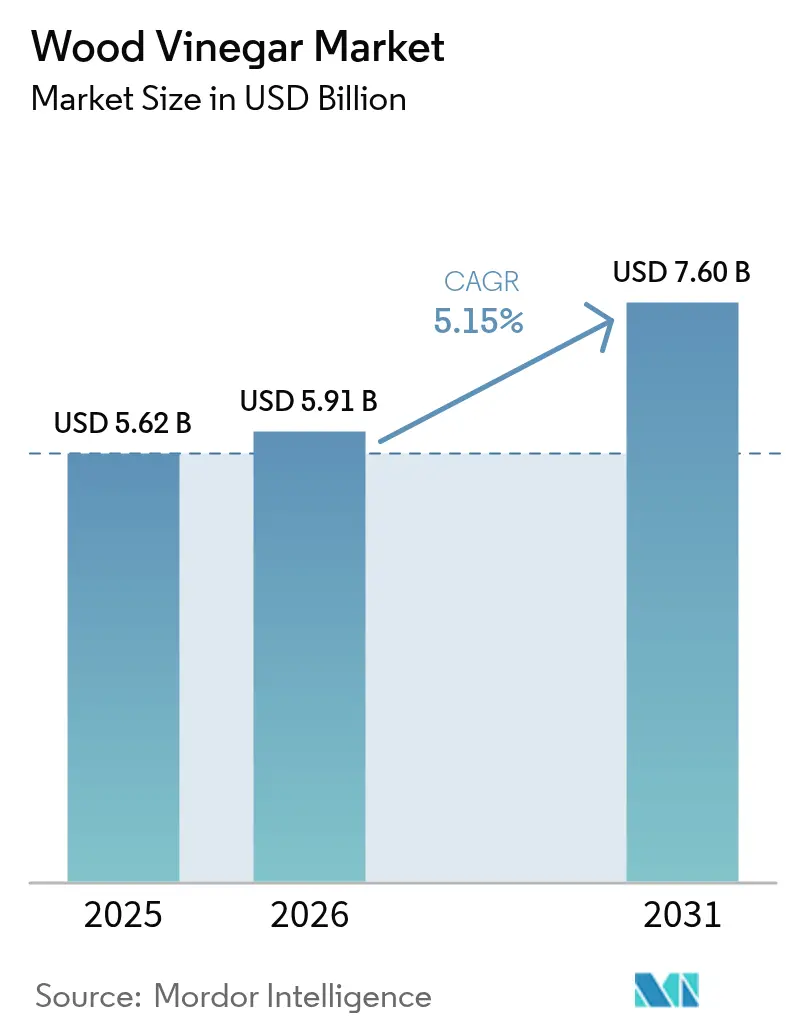

The wood vinegar market size was valued at USD 5.62 billion in 2025 and estimated to grow from USD 5.91 billion in 2026 to reach USD 7.6 billion by 2031, at a CAGR of 5.15% during the forecast period (2026-2031). Rising demand for bio-based inputs in agriculture, food processing, and specialty chemicals is the primary catalyst, reinforced by tightening environmental regulations that discourage synthetic chemical use. Strong policy support for circular‐economy business models, rapid technology upgrades in pyrolysis systems, and expanding end-use cases in aquaculture and cosmetics further broaden commercial prospects. Asia-Pacific continues to anchor global revenues through well-established production clusters in China, Japan, and Southeast Asia, while Middle East and Africa registers the quickest uptake due to sustainable-farming initiatives and targeted donor programs. Key competitive dynamics include persistent fragmentation, ample room for vertical integration, and escalating patent activity in high-temperature pyrolysis reactors and sequential distillation systems.

Key Report Takeaways

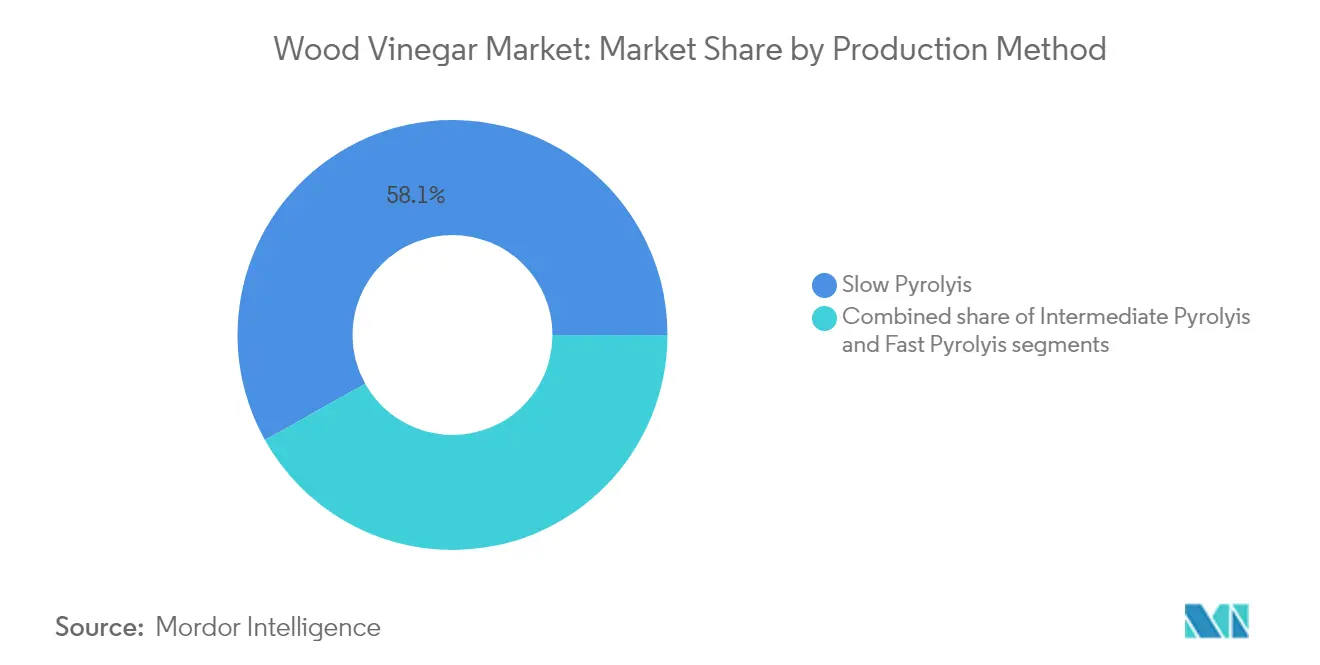

- By production method, slow pyrolysis led with 58.12% revenue share in 2025; fast pyrolysis is set to expand at 7.14% CAGR between 2026-2031.

- By feedstock, hardwood accounted for 28.05% of the wood vinegar market size in 2025, whereas coconut shells are forecast to climb at 7.45% CAGR to 2031.

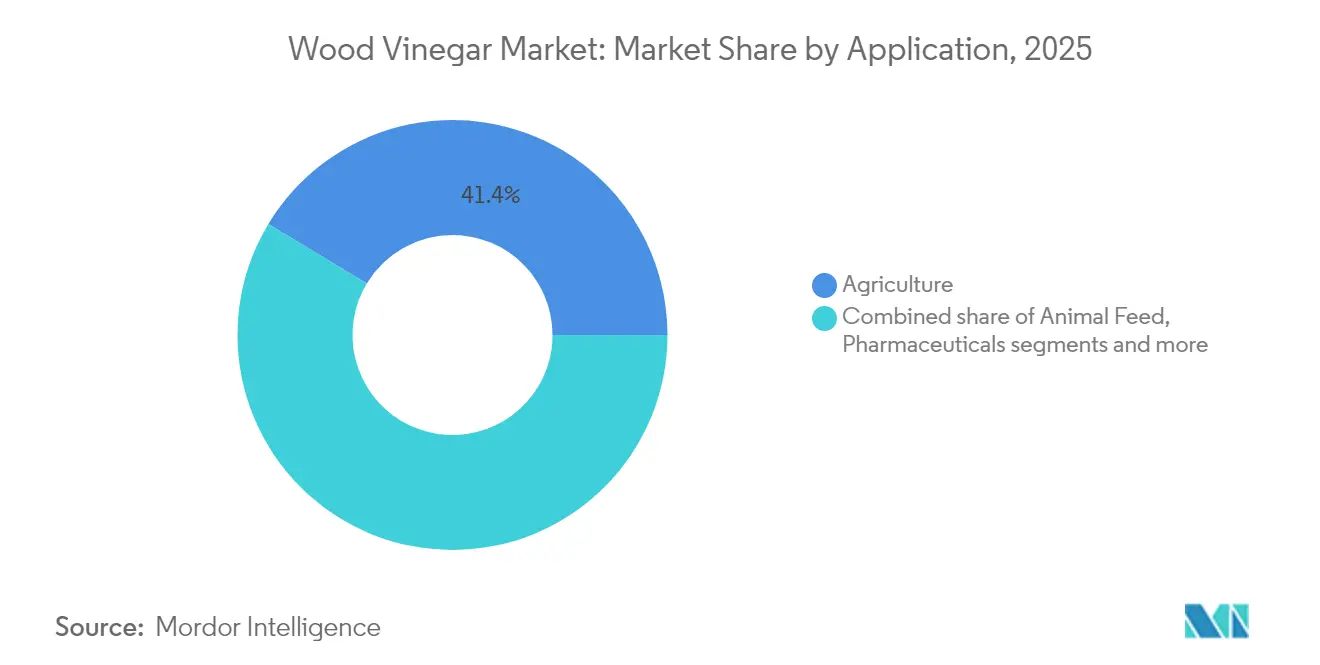

- By application, agriculture commanded 41.37% of the wood vinegar market share in 2025; pharmaceuticals is projected to grow at 7.66% CAGR through 2031.

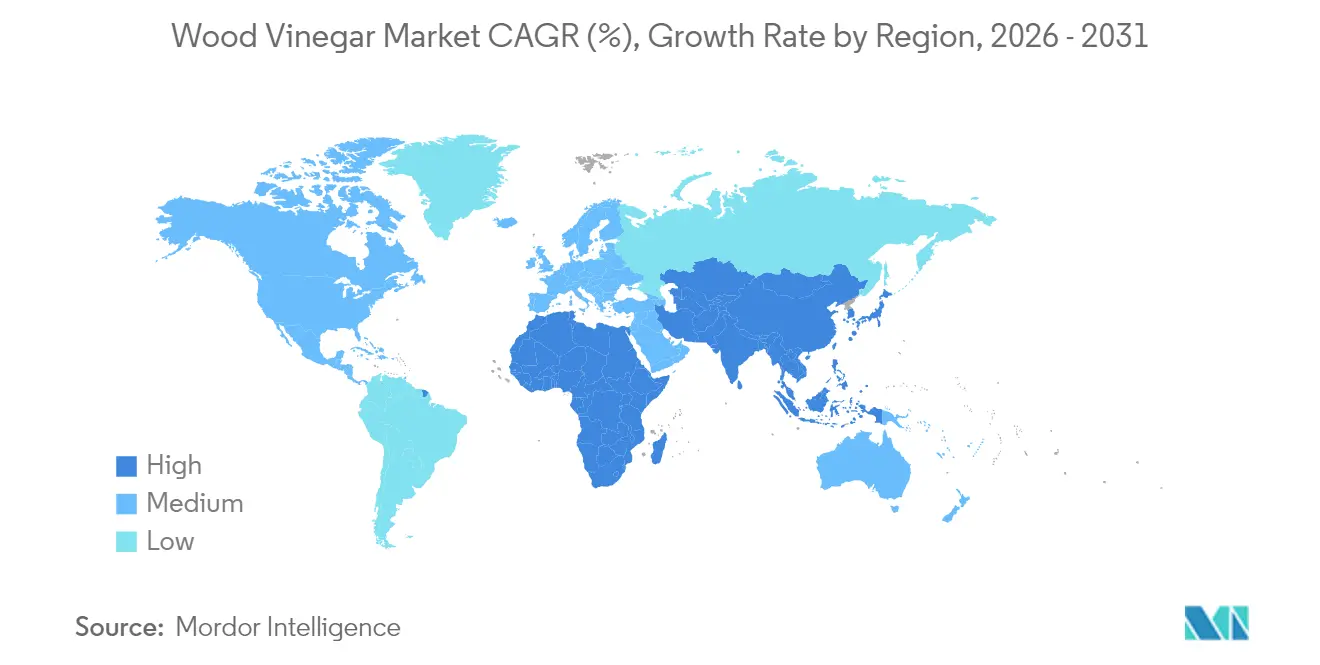

- By geography, Asia-Pacific held 39.87% of global revenues in 2025, while Middle East and Africa is advancing at a 7.72% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wood Vinegar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for natural food preservatives and flavor enhancers | +0.8% | Global, with strong adoption in North America and Europe | Medium term (2-4 years) |

| Supportive government policies and environmental regulations | +1.2% | Global, particularly strong in Europe, China, and emerging markets | Long term (≥ 4 years) |

| Shift toward organic and sustainable agriculture | +1.0% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Long term (≥ 4 years) |

| Rising demand for bio-based pesticides | +0.9% | Global, with accelerated adoption in regions phasing out synthetic pesticides | Medium term (2-4 years) |

| Advancements in wood vinegar production technology | +0.7% | Developed markets initially, scaling to emerging markets | Short term (≤ 2 years) |

| Expanding use in aquaculture | +0.6% | Asia-Pacific dominance, expanding to coastal regions globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for natural food preservatives and flavor enhancers

The food and beverage industry's pivot toward natural preservatives is reshaping wood vinegar demand dynamics, with the FDA's GRAS framework providing regulatory clarity for food applications. Wood vinegar's antimicrobial properties, primarily attributed to its acetic acid content and phenolic compounds, offer food manufacturers a natural alternative to synthetic preservatives in canned foods, sauces, and dairy products. Recent research demonstrates that wood vinegar from Litchi chinensis exhibits broad-spectrum antibacterial activity comparable to vitamin C, with significant antioxidant properties that extend shelf life while maintaining food safety standards. The compound's natural origin aligns with consumer preferences for clean-label products, driving adoption rates that exceed traditional preservative alternatives. This trend is particularly pronounced in premium food segments where natural ingredients command price premiums, creating sustainable revenue streams for wood vinegar producers. The regulatory approval of bamboo vinegar for cosmetic applications in China signals broader acceptance of wood vinegar derivatives in consumer products, potentially expanding market opportunities beyond traditional food applications.

Supportive government policies and environmental regulations

Regulatory frameworks increasingly favor bio-based alternatives over synthetic chemicals, creating structural demand drivers for wood vinegar across multiple jurisdictions. The European Union's initiative promoting wood vinegar as a natural bio-herbicide in Castilla-La Mancha, Spain, demonstrates government support for sustainable agricultural practices, with over 3,000 liters applied in various trials showing effectiveness against weeds while maintaining safety for human health [1]Source: Interreg Europe, "Wood vinegar as a natural bio-herbicide", www.interregeurope.eu. Environmental regulations targeting synthetic pesticide reduction are accelerating wood vinegar adoption, particularly in regions implementing stringent chemical residue limits in food products. Government incentives for circular economy practices further support wood vinegar production from agricultural waste, addressing both waste management and sustainable agriculture objectives. These policy frameworks create long-term market stability and encourage investment in production capacity expansion.

Rising demand for bio-based pesticides

The global pesticide market's shift toward natural alternatives is creating substantial opportunities for wood vinegar applications in crop protection. Wood vinegar's herbicidal properties against nitrophilous plant communities demonstrate its potential as a sustainable weed management solution, with research showing effective control of invasive species while maintaining soil health. The compound's antifungal properties against wood-destroying fungi and insects provide additional pest control benefits, with higher concentrations significantly reducing weight loss from fungal attacks and increasing larval mortality rates. Regulatory pressure to reduce synthetic pesticide residues in food products is accelerating wood vinegar adoption, particularly in export-oriented agricultural regions where residue limits are becoming increasingly stringent. The technology's safety profile for beneficial insects and soil organisms provides a competitive advantage over broad-spectrum synthetic pesticides.

Expanding use in aquaculture

The expanding use of wood vinegar in aquaculture is emerging as a significant driver in the wood vinegar market. Wood vinegar, known for its natural antibacterial and antifungal properties, is increasingly being utilized as a sustainable alternative to synthetic chemicals in aquaculture practices. For instance, it is used to improve water quality, enhance fish health, and reduce the prevalence of diseases in aquaculture systems. According to the Food and Agriculture Organization (FAO), the fisheries and aquaculture production in 2022 surged to 223.2 million tonnes, a 4.4% increase from the year 2020 [2]Source: Food and Agriculture Organization, "Global fisheries and aquaculture production reaches a new record high", www.fao.org. Moreover, Aquaculture farming in the EU yielded almost 1.1 million tonnes of aquatic organisms in 2023, worth EUR 4.8 billion [3]Source: Eurostat, "Aquaculture statistics", www.ec.europa.eu highlighting the sector's rapid growth and the increasing demand for sustainable inputs like wood vinegar. In countries like Japan and Thailand, where aquaculture is a significant industry, wood vinegar is being adopted as a cost-effective and eco-friendly solution to address environmental concerns and improve productivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs | -1.1% | Global, particularly impacting emerging market adoption | Short term (≤ 2 years) |

| Competition from synthetic alternatives | -0.9% | Developed markets with established synthetic chemical infrastructure | Medium term (2-4 years) |

| Low scientific validation and research | -0.7% | Global, with stronger impact in regulated markets requiring extensive documentation | Long term (≥ 4 years) |

| Distribution and scale-up challenges | -0.8% | Emerging markets and rural areas with limited infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from synthetic alternatives

Established synthetic chemical industries present formidable competition through mature supply chains, standardized products, and proven efficacy profiles that challenge wood vinegar market penetration. Synthetic pesticides and preservatives benefit from decades of research and development investment, resulting in highly optimized formulations with predictable performance characteristics that many end-users prefer over natural alternatives. The synthetic chemical industry's economies of scale enable competitive pricing that wood vinegar producers struggle to match, particularly in commodity agricultural applications where cost considerations often outweigh sustainability benefits. Regulatory approval processes for synthetic chemicals are well-established and understood by industry participants, while wood vinegar applications often require novel regulatory pathways that create uncertainty and delay market entry. The performance consistency of synthetic alternatives provides risk mitigation for commercial users who cannot afford crop failures or product quality issues associated with unproven natural alternatives.

High production costs

Wood vinegar production faces significant cost challenges that limit market penetration, particularly in price-sensitive agricultural segments where synthetic alternatives maintain cost advantages. The sequential vacuum distillation process required to remove contaminants and achieve pharmaceutical-grade quality adds substantial processing costs, with research indicating that multiple distillation stages are necessary to eliminate polycyclic aromatic hydrocarbons and volatile organic Feedstock procurement and transportation costs further impact production economics, with studies on biochar production in iron and steel industries highlighting supply chain factors as key cost drivers. The need for specialized equipment and skilled operators increases operational complexity and labor costs compared to conventional chemical production. Quality control and testing requirements for food and pharmaceutical applications add regulatory compliance costs that can represent significant portions of total production expenses, particularly for smaller manufacturers lacking dedicated quality assurance infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Method: Slow Pyrolyis Dominates, Fast Pyrolysis Accelerates

In 2025, slow pyrolysis holds a commanding 58.12% share of the wood vinegar market, leveraging its established infrastructure and superior yields of wood vinegar. This method has traditionally dominated the market due to its ability to maximize liquid product recovery while minimizing energy consumption. Slow pyrolysis is particularly favored for large-scale commercial operations, as it ensures consistent output and cost efficiency. Its widespread adoption is further supported by its compatibility with existing systems, making it a reliable choice for producers aiming to meet growing demand without significant operational overhauls.

Conversely, fast pyrolysis is experiencing rapid growth in the wood vinegar market, with a projected CAGR of 7.14% during the forecast period of 2026-2031. This growth is driven by technological advancements that enhance production efficiency and improve product quality. Innovations in reactor design and process optimization are key factors propelling the adoption of fast pyrolysis, as they significantly reduce processing time while maintaining high-quality standards. These advancements make fast pyrolysis an increasingly attractive option for producers seeking to scale operations and meet evolving market demands efficiently.

By Feedstock: Hard Wood Leads, Coconut Shells Gain Momentum

In 2025, hardwood commands a dominant market share of 28.05%, thanks to its well-established supply chains and a consistent chemical makeup that ensures high-quality wood vinegar with reliable properties. Hardwood's predictable performance and widespread availability make it a preferred choice for manufacturers aiming to produce wood vinegar with uniform characteristics, catering to various industrial applications. Furthermore, its ability to deliver stable yields and meet stringent quality standards positions hardwood as a reliable feedstock in the wood vinegar market. The durability and versatility of hardwood also make it suitable for large-scale production, ensuring its continued dominance in the market.

Yet, coconut shells are rapidly gaining traction as the feedstock with the highest growth rate, boasting a 7.45% CAGR from 2026 to 2031. This surge is largely attributed to circular economy initiatives that transform agricultural waste into sought-after bio-products. The pivot towards coconut shell feedstock underscores its recognized sustainability advantages and its plentiful availability in tropical regions, where significant waste streams arise from coconut production. Additionally, the use of coconut shells aligns with global efforts to reduce environmental impact by utilizing renewable and underutilized resources. The growing adoption of coconut shells is further supported by advancements in pyrolysis technology, which enhance the efficiency of converting this feedstock into high-quality wood vinegar.

By Application: Pharmaceuticals Show Breakthrough Potential

Agriculture commanded a 41.37% market share in 2025, underscoring wood vinegar's pivotal role in crop protection, soil enhancement, and organic farming. Wood vinegar's effectiveness in boosting soil health, managing pests, and naturally elevating crop yields solidifies agriculture's lead, aligning seamlessly with sustainable farming practices. Additionally, its compatibility with organic certification standards and its ability to reduce dependency on synthetic chemicals further strengthen its adoption in modern agricultural systems. The increasing global emphasis on sustainable agriculture and the rising demand for organic produce are expected to further drive the adoption of wood vinegar in this segment.

Meanwhile, the pharmaceutical sector is witnessing the swiftest growth, projected at a 7.66% CAGR from 2026 to 2031, fueled by heightened research into wood vinegar's antimicrobial properties and its applications in drug development. The growing interest in natural and sustainable ingredients for pharmaceutical formulations is driving innovation in this segment. Furthermore, its potential in developing alternative therapies and enhancing the efficacy of existing drugs positions wood vinegar as a promising component in pharmaceutical advancements. The increasing prevalence of antibiotic resistance and the demand for natural antimicrobial agents are further propelling research and development activities in this sector.

Geography Analysis

In 2025, the Asia-Pacific region commands a dominant 39.87% market share, bolstered by its long-standing agricultural applications and a production infrastructure that has transitioned from traditional charcoal manufacturing to integrated biorefinery operations. This growth is further fueled by robust government backing for organic farming and bio-based pesticides. Japan sets global standards in wood vinegar production with its cutting-edge pyrolysis technologies and stringent quality control systems. Meanwhile, Southeast Asian nations capitalize on their rich reserves of coconut shells and bamboo, crafting efficient and cost-effective production systems. Additionally, the region's aquaculture sector is emerging as a pivotal growth engine, with studies highlighting wood vinegar's role in enhancing water quality and fish health, particularly in shrimp farming.

The Middle East and Africa lead the pack with the highest growth rate, achieving a notable 7.72% CAGR from 2026 to 2031. This surge is largely attributed to the region's growing acknowledgment of wood vinegar's efficacy in tackling agricultural hurdles, such as bolstering drought resilience and combating soil degradation. Furthermore, the region's plentiful date palm residues serve as a sustainable feedstock for wood vinegar. Research underscores the successful transformation of agricultural waste into valuable bio-products, enhancing soil properties and championing circular economy principles. Bolstered by government policies that advocate for sustainable agriculture and organic farming, the region fosters a conducive environment for wood vinegar adoption. Additionally, international development programs bolster this momentum, offering both technical assistance and funding to enhance production capacities.

North America and Europe, with their mature markets, grapple with stringent regulatory landscapes. These regions prioritize premium applications of wood vinegar, especially in food, pharmaceuticals, and high-value agriculture. In the U.S., the FDA's GRAS framework delineates a clear path for wood vinegar's entry into food applications. Across the Atlantic, European regulations are increasingly leaning towards bio-based alternatives, sidelining synthetic chemicals. Meanwhile, South America's agricultural landscape is ripe with growth potential. Countries in the region are not only championing organic farming but are also on the lookout for sustainable substitutes to synthetic pesticides, especially as these face mounting regulatory scrutiny. With its rich biomass resources and a well-established agricultural framework, South America is poised for a robust market expansion.

Competitive Landscape

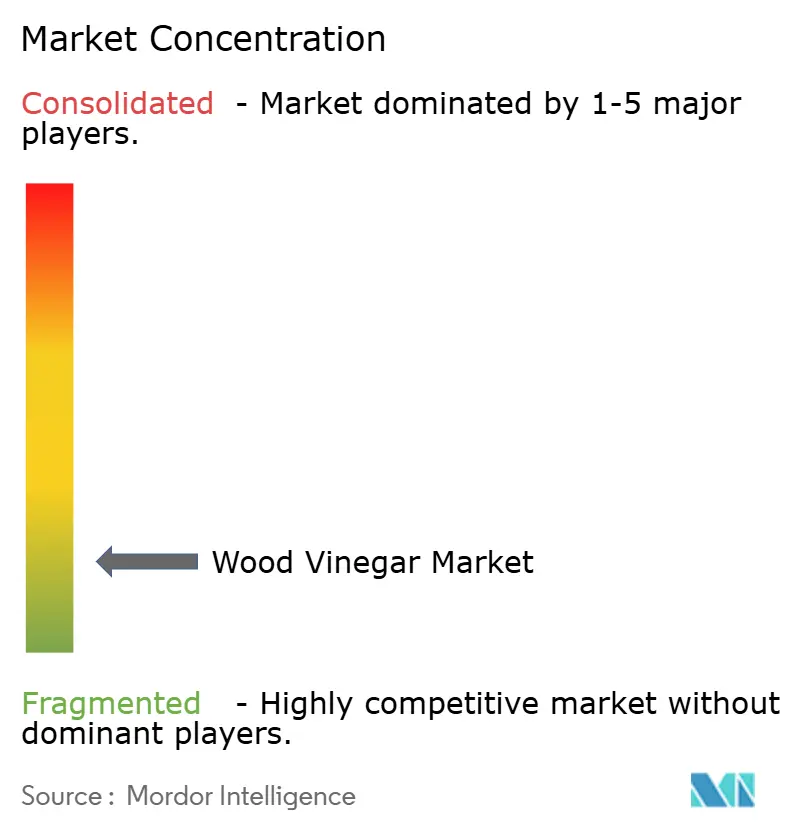

The wood vinegar market operates within a fragmented competitive landscape, reflected by a concentration score of 2 out of 10. This low concentration indicates a market where numerous small-scale producers coexist with emerging industrial-scale operations. The industry's evolution from traditional charcoal byproducts to advanced bio-based chemical production has created a dynamic environment. This fragmentation presents both challenges and opportunities for market participants aiming to establish a dominant position, as competition remains diverse and widespread. Companies must navigate this fragmented structure strategically to gain a competitive edge.

The low concentration in the market allows niche players to capitalize on regional expertise and cater to specialized applications. These smaller players often focus on localized production and unique product offerings, which enable them to maintain a competitive edge. At the same time, the fragmented nature of the market creates opportunities for consolidation, particularly for companies with significant capital resources and advanced technological capabilities. Such firms can leverage their strengths to expand their market presence and streamline operations, positioning themselves as key players in the industry.

Innovation in biomass conversion technologies is further shaping the competitive landscape. Recent patent applications highlight advancements in organic solid biomass conversion methods, particularly those utilizing methane-containing gas environments and catalyst structures. These innovations aim to improve production efficiency and enhance product quality, signaling ongoing efforts to refine processes and meet the growing demand for bio-based chemicals. As technological advancements continue, they are expected to drive further differentiation and competitiveness within the market. The focus on innovation underscores the industry's commitment to sustainability and long-term growth.

Wood Vinegar Industry Leaders

-

Nettenergy B.V.

-

Ace (Singapore) Pte Ltd

-

PyroAg Wood Vinegar

-

Merck KGaA

-

Tagrow Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Seneca Farms Biochar has unveiled a new name for its Wood Vinegar product, rebranding it as pyGrow+, underscoring its distinct advantages for the agricultural sector. Originally intended for herbicide use, the product's remarkable ability to boost seed germination and promote plant growth led to a strategic pivot. Setting itself apart from traditional wood vinegars, pyGrow+™ boasts a formulation devoid of undesirable compounds like methanol and tar.

- April 2023: The Shire of Collie, located in Western Australia, partnered with the startup Renergi Pty Ltd to establish a USD 10.4 million energy-from-waste (pyrolysis) plant. This facility was designed to transform biomass into biochar, pyrolysis oil, and wood vinegar. Dubbed the Collie Resource Recovery Centre, the project aimed to convert municipal solid waste and biomass into valuable products such as biochar and bio-oil.

Global Wood Vinegar Market Report Scope

Wood vinegar is a red-brown liquid that is prepared by the distillation of wood, containing acetic acid, methanol, acetone, wood oil, and tars. The market study covers segmentation by application and geography. On the basis of application, the market is segmented into agriculture, food & beverage, animal feed, and other applications. The agricultural application is further segmented into crop nutrition and crop protection, and food & beverage is further bifurcated into canned food, sauces, dairy products, and other food & beverages. The market is segmented by geography into North America, Europe, Asia-Pacific, South America, Middle East & Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Slow Pyrolysis |

| Intermediate Pyrolysis |

| Fast Pyrolysis |

| Bamboo |

| Hardwood |

| Softwood |

| Agricultural Residues |

| Coconut Shells |

| Others |

| Agriculture | Crop Nutrition |

| Crop Protection | |

| Food and Beverage | Canned Food |

| Sauces | |

| Dairy Products | |

| Other Food and Beverage Applications | |

| Animal Feed | |

| Pharmaceuticals | |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Columbia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Egypt | |

| Morocco | |

| Nigeria | |

| Turkey | |

| Rest of Middle East and Africa |

| By Production Method | Slow Pyrolysis | |

| Intermediate Pyrolysis | ||

| Fast Pyrolysis | ||

| By Feedstock | Bamboo | |

| Hardwood | ||

| Softwood | ||

| Agricultural Residues | ||

| Coconut Shells | ||

| Others | ||

| By Application | Agriculture | Crop Nutrition |

| Crop Protection | ||

| Food and Beverage | Canned Food | |

| Sauces | ||

| Dairy Products | ||

| Other Food and Beverage Applications | ||

| Animal Feed | ||

| Pharmaceuticals | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Columbia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Egypt | ||

| Morocco | ||

| Nigeria | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected growth rate of the wood vinegar market to 2031?

The market is forecast to grow at a 5.15% CAGR, rising from USD 5.62 billion in 2025 to USD 7.6 billion in 2031.

Which region currently leads the wood vinegar market?

Asia-Pacific dominates with 39.87% of global revenues, supported by extensive agricultural demand and mature production networks.

Why is fast pyrolysis gaining traction versus slow pyrolysis?

Advances in reactor design have shortened processing cycles and improved energy recovery, driving a 7.14% CAGR for fast pyrolysis installations.

How does wood vinegar benefit organic agriculture?

It delivers natural antimicrobial action, enhances soil microbial activity, and stimulates plant growth, enabling growers to reduce synthetic inputs while maintaining yields.

What limits faster adoption of wood vinegar in price-sensitive crops?

High production costs and the lower unit prices of synthetic pesticides remain short-term obstacles, though policy incentives and technology improvements are narrowing the gap.

Page last updated on: