Edible Flakes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

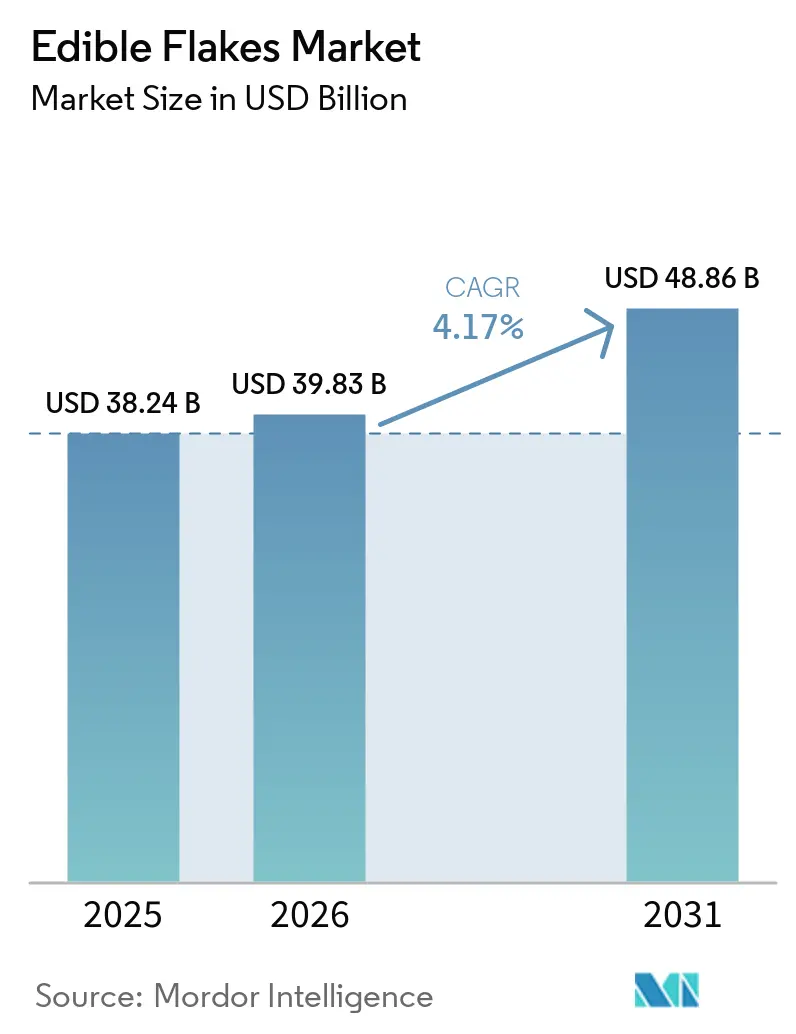

| Market Size (2026) | USD 39.83 Billion |

| Market Size (2031) | USD 48.86 Billion |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

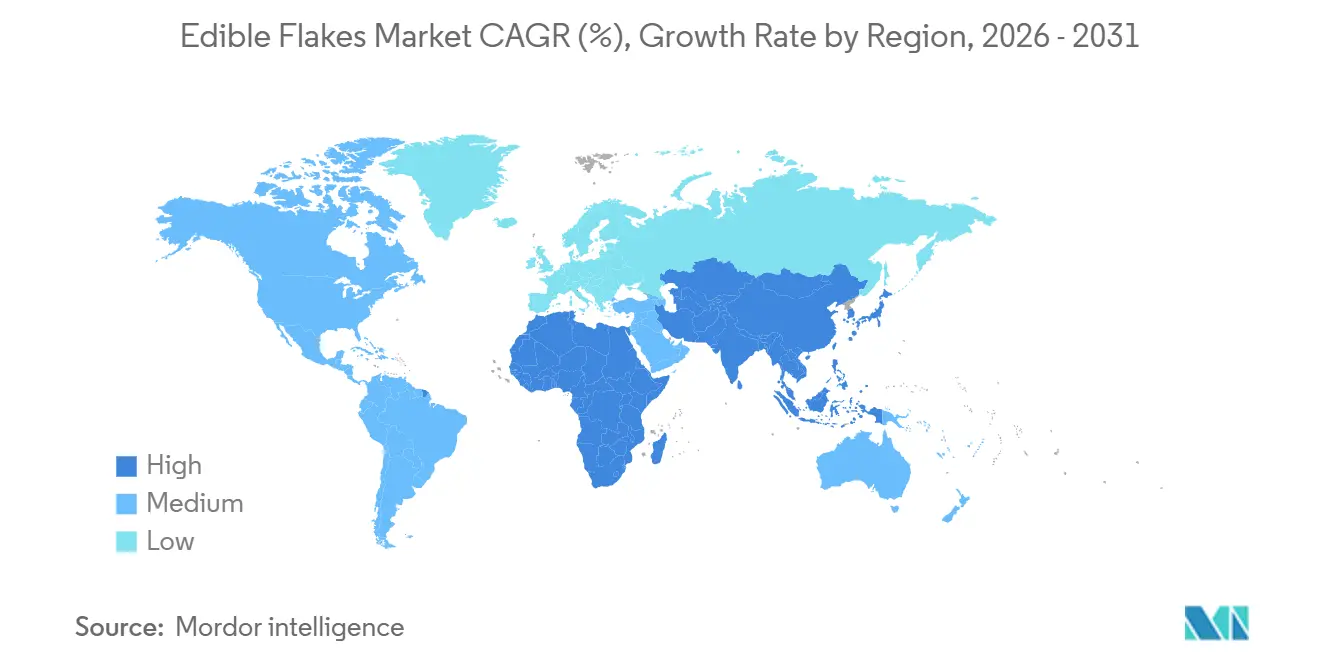

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Edible Flakes Market Analysis by Mordor Intelligence

The edible flakes market is projected to grow from USD 38.24 billion in 2025 to USD 39.83 billion in 2026, eventually reaching USD 48.86 billion by 2031. This growth represents a compound annual growth rate (CAGR) of 4.17% during the forecast period of 2026-2031, according to Mordor Intelligence. The demand for edible flakes is shifting toward functional, protein-enriched, and organic cereals that cater to modern consumer preferences for convenience and health benefits. While overall breakfast consumption is increasing at a modest pace, these product categories are driving significant growth. In 2025, North America dominated the market in terms of sales. However, rapid urbanization in countries such as China and India is driving substantial growth in the Asia-Pacific region. Regulatory developments are also playing a key role in shaping the market. The market remains moderately consolidated, with a few key players holding significant market shares.

Key Report Takeaways

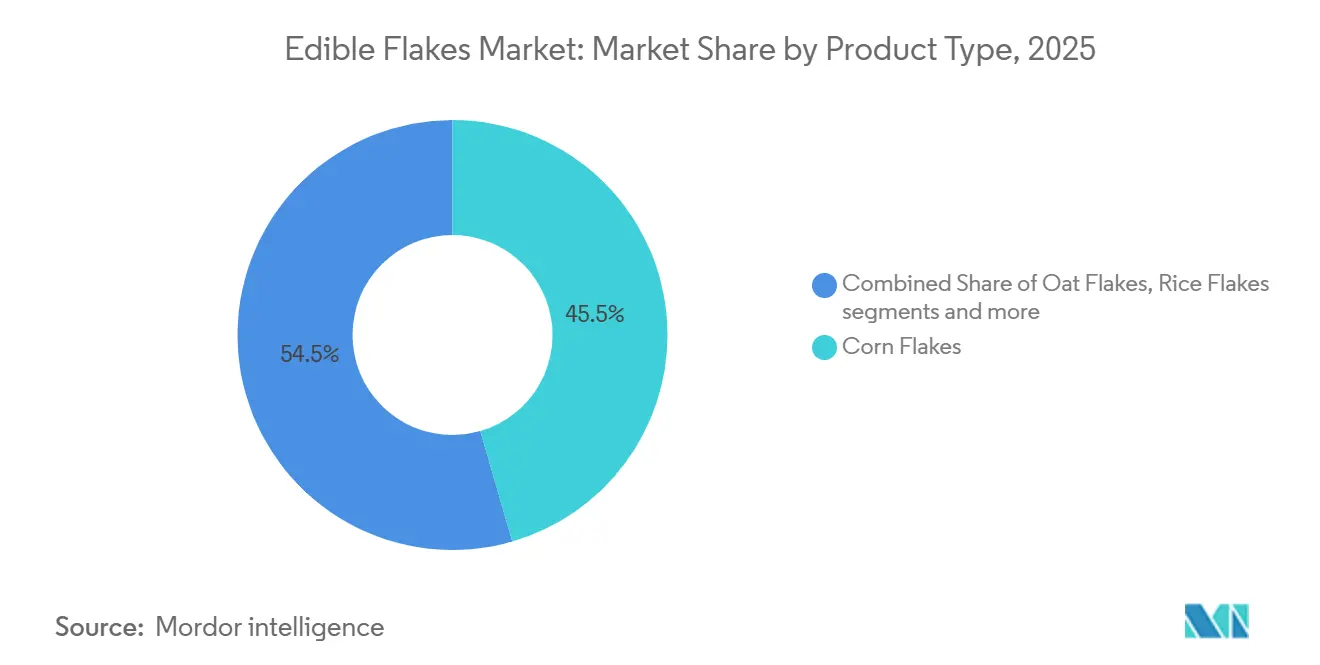

- By product type, corn flakes captured 45.52% of the edible flakes market share in 2025, while oat flakes are projected to expand at a 5.02% CAGR through 2031.

- By nature, conventional variants held 68.61% of the edible flakes market share in 2025; the organic segment is advancing at a 6.15% CAGR during 2026-2031.

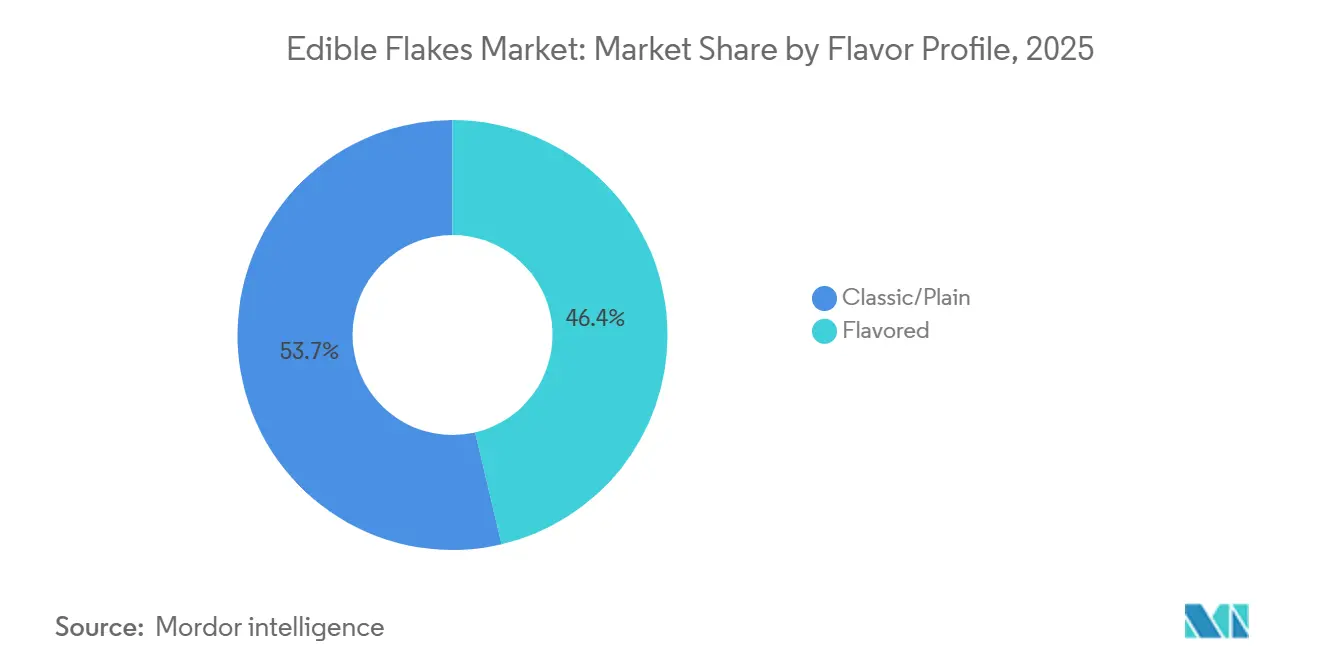

- By flavor profile, classic/plain flavor accounted for 53.65% of the edible flakes market in 2025, yet flavored is growing at a 4.85% CAGR through 2031

- By format, ready-to-eat cold flakes accounted for 64.17% share of the edible flakes market size in 2025, whereas hot and instant flakes are forecast to grow at a 5.45% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets accounted for 44.35% of the edible flakes market in 2025, yet online retail is growing at a 5.21% CAGR through 2031.

- By geography, North America retained a 37.54% share in 2025, while Asia-Pacific is set to register the highest 6.36% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Edible Flakes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient and ready-to-eat foods | +0.9% | Global, with peak intensity in North America, urban China, and India metros | Medium term (2-4 years) |

| Growing awareness of breakfast importance in daily life | +0.5% | Global, strongest in Asia-Pacific emerging markets | Long term (≥ 4 years) |

| Increasing demand for weight management and low-calorie diets | +0.7% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Increasing demand for gluten-free and allergen-friendly options | +0.4% | North America, Western Europe | Short term (≤ 2 years) |

| Influence of western culture and media exposure | +0.8% | Asia-Pacific (China, India, Indonesia), Latin America | Long term (≥ 4 years) |

| Sustainable packaging and eco-friendly initiatives | +0.3% | Europe (regulatory-driven), North America (consumer-driven) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient and ready-to-eat foods

The growing demand for convenient, ready-to-eat foods is a major driver of the edible flakes market. As people lead busier lives, they increasingly prefer meal options that require little to no preparation. This trend is especially noticeable in countries like China, where changing lifestyles are boosting the demand for shelf-stable breakfast products that fit into hectic daily schedules. Innovations in packaging, such as resealable designs, are making these products more user-friendly while also helping them stay fresh longer. Leading companies, such as General Mills Inc., are addressing this demand by introducing high-protein and functional cereal options that combine convenience with nutritional benefits. In India, companies like Tata Consumer Products Ltd are investing in expanding production capacity to meet the rising demand for convenient food products.

Growing awareness of breakfast importance in daily life

Awareness about the importance of breakfast as a crucial daily meal is significantly driving the growth of the global edible flakes market. Public health campaigns and updated dietary guidelines are encouraging people to view breakfast as a structured, nutritious meal, emphasizing whole grains and fiber. This trend is particularly noticeable among younger age groups. For instance, a study published in Poland on PubMed Central found that 62% of children aged 10–12 eat breakfast daily in 2025, highlighting the growing demand for convenient, healthy options such as cereal flakes[1]Source: PubMed Central, "Breakfast Frequency, Lifestyle-Related Factors And Their Association with Body Weight Status Among Polish Primary School Children Aged 10 to 12 Years", pmc.ncbi.nlm.nih.gov. Major companies, such as Nestlé S.A., are focusing on aligning their product packaging and messaging with nutritional goals, particularly emphasizing fiber content. In markets like the United States, evolving dietary guidelines are pushing manufacturers to reformulate their products to meet healthier standards.

Increasing demand for weight management and low-calorie diets

The growing focus on weight management and low-calorie diets is a key factor driving the edible flakes market. Consumers are increasingly looking for foods that help them feel full, maintain healthy blood sugar levels, and support overall well-being. This trend is further fueled by rising obesity rates. According to data from the American Society for Metabolic and Bariatric Surgery, based on the Centers for Disease Control and Prevention, obesity in the United States reached 40.3%, with severe obesity at 9.4% as of 2025[2]Source: American Society for Metabolic and Bariatric Surgery, "2025 Fact Sheet -- Obesity In America", asmbs.org. These statistics highlight the growing need for healthier food options, driving demand for functional ingredients such as oat beta-glucan, known for its health benefits. Oat-based flakes, in particular, are gaining popularity due to their nutritional value. Additionally, regulatory support, such as the European Food Safety Authority's approval for broader health claims, is encouraging manufacturers to reformulate their products to meet these demands.

Increasing demand for gluten-free and allergen-friendly options

The growing demand for gluten-free and allergen-friendly products is a significant factor driving the global edible flakes market. This trend is fueled by increasing consumer awareness of food allergies and intolerances, as well as changing dietary preferences. Governments and regulatory bodies in regions like the European Union, the United States, and Canada have introduced clear guidelines for gluten-free labeling. These regulations have encouraged manufacturers to develop products made with alternative grains, such as oats, rice, and corn, to meet this demand. In the United States alone, data from Food Allergy Research & Education highlights that over 27 million adults have food allergies. Notably, nearly half of these individuals develop at least one allergy during adulthood, with 21% experiencing all their allergies after the age of 18[3]Source: Food Allergy Research & Education, "National Indicator Report on Food Allergy", foodallergy.org. This growing prevalence of food allergies has led to a rising need for safer, allergen-conscious food options, including edible flakes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing competition from alternative breakfast options | -0.6% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) |

| Perception of high sugar and low nutritional value in some products | -0.5% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Regulatory scrutiny on labeling and health claims | -0.4% | Europe (EFSA-driven), North America (FDA-driven), spillover to Asia-Pacific | Medium term (2-4 years) |

| Concerns regarding additives and preservatives | -0.3% | North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing competition from alternative breakfast options

The edible flakes market is facing challenges due to growing competition from alternative breakfast options. Consumers are increasingly opting for more convenient, protein-rich options such as protein bars, yogurt cups, and smoothie pouches. These alternatives are popular because they offer higher protein per calorie than other options and are easy to consume on the go. For example, emerging brands such as Magic Spoon have successfully attracted attention by focusing on low-carb, keto-friendly products that are disrupting the traditional cereal market. Innovations like high-protein smoothie pouches are reshaping how people approach breakfast, directly competing with conventional edible flakes. To address this shift, established companies are adapting by launching new products that combine traditional cereal elements with snack-like features. These hybrid offerings aim to keep consumers engaged while allowing brands to compete in adjacent categories, ensuring they remain relevant in a rapidly evolving market.

Perception of high sugar and low nutritional value in some products

The perception that edible flakes are high in sugar and lack nutritional value remains a major challenge for the global market. Consumers are increasingly concerned about the health impacts of processed foods, which directly affects their purchasing decisions. Although manufacturers are reformulating products to reduce sugar content, many items still fail to meet recommended levels, leading to ongoing doubts among health-conscious consumers. Retailers are also raising their standards, with major players like Target and Walmart demanding the removal of artificial additives and synthetic dyes. This has forced manufacturers to accelerate their transition to clean-label products, which are free of artificial ingredients. Regulatory bodies such as the United States Food and Drug Administration are introducing stricter rules, including limits on the use of certain artificial colorants. These regulations are driving up reformulation costs for manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Corn Still Leads, Oats Accelerate

Corn flakes were the leading segment in the edible flakes market in 2025, holding a significant 45.52% share. Their popularity stems from being an affordable, convenient, and easy-to-prepare breakfast option. Consumers across both developed and emerging markets widely prefer corn flakes due to their familiarity and accessibility. Additionally, manufacturers have introduced fortified and flavored variants to cater to evolving consumer preferences, helping maintain their strong market position and driving repeat purchases.

Oat flakes are expected to grow at a CAGR of 5.02% over the forecast period from 2026 to 2031. This growth is primarily driven by rising consumer health awareness, as consumers seek high-fiber, heart-healthy breakfast alternatives. Oat flakes are gaining traction as they are minimally processed and rich in nutrients, making them a preferred choice for health-conscious individuals. The growing adoption of fitness-oriented diets and rising concerns about cholesterol management and digestive health are expected to further boost demand for oat flakes in the coming years.

By Nature: Conventional Dominates, Organic Outperforms

Conventional variants dominated the edible flakes market in 2025, accounting for 68.61% of the market. This dominance is largely due to their affordability, widespread availability, and the strong consumer trust they have built over time. These products are produced on a large scale, helping manufacturers keep costs low and ensuring they are easily accessible in both urban and rural areas. Additionally, their consistent taste and longer shelf life make them a preferred choice for consumers who prioritize cost-effectiveness and convenience.

On the other hand, organic variants are projected to grow significantly, with a CAGR of 6.15% during the forecast period of 2026–2031. This growth is fueled by increasing consumer demand for clean-label products made with natural, chemical-free ingredients. As people become more health-conscious, they are willing to spend more on organic options that are perceived to offer better nutritional value. The growing availability of organic products in retail stores and supportive government regulations promoting sustainable practices are further driving the expansion of this segment. This trend reflects a shift in consumer preferences toward healthier and environmentally friendly food choices.

By Flavor Profile: Classic Retains Hold, Flavored Innovations Surge

Classic or plain edible flakes accounted for 53.65% of the market value in 2025, the largest share, due to their simplicity and widespread appeal. These products are popular because they can be easily customized with ingredients like fruits, milk, or sweeteners, making them a flexible choice for consumers. Many people view plain flakes as a healthier, less processed option, appealing to traditional and health-conscious buyers. Additionally, their affordability and strong availability across various retail channels have helped them maintain their leading position in the market.

On the other hand, flavored edible flakes are expected to grow at a steady CAGR of 4.85% through 2031, driven by rising demand for tastier and more convenient breakfast options. Younger consumers, in particular, are drawn to these products due to their variety and enhanced flavors, such as chocolate, honey, and fruit blends. Companies are focusing on innovation to introduce new flavors, which is helping attract more customers and encouraging repeat purchases. Moreover, strong marketing efforts and premium branding of flavored flakes are boosting their popularity in both developed and emerging markets, contributing to their steady growth.

By Format: Cold Rules Today, Hot Gains in Asia

In 2025, ready-to-eat cold flakes led the edible flakes market, accounting for 64.17% of total revenue. Their popularity stems from their convenience, as they require no cooking and are ideal for busy lifestyles. These flakes are a preferred choice for quick breakfasts, especially among urban populations and working professionals. Their long shelf life, wide availability, and strong marketing efforts by major brands have further boosted their demand, making them a staple in many households.

Meanwhile, hot and instant flakes are expected to grow steadily, with a projected CAGR of 5.45% during 2026–2031. This growth is driven by rising consumer preference for warm, filling meal options, particularly among health-conscious individuals and those who value traditional eating habits. The rising awareness of the health benefits of oats and multigrain cereals is also contributing to this segment's expansion. Furthermore, innovations in instant preparation methods that combine ease of use with nutritional value are likely to attract more consumers and drive market growth in the coming years.

By Distribution Channel: Store Shelves Still Matter, Online Accelerates

Supermarkets and hypermarkets held the largest share of the edible flakes market, contributing 44.35% in 2025. These retail outlets remain the preferred choice for consumers due to their wide product selection, competitive pricing, and the ability to physically inspect items before purchase. High customer foot traffic and strategic product placements on shelves encourage impulse purchases, further boosting sales. Discounts, promotional offers, and bundled deals make these stores particularly attractive to budget-conscious shoppers, ensuring their continued dominance in the market.

On the other hand, online channels are projected to grow steadily at a CAGR of 5.21% over the 2026–2031 period. This growth is fueled by increasing internet access, the rising popularity of e-commerce platforms, and the convenience of doorstep delivery. Consumers are drawn to the ability to compare prices, explore a broader range of brands, and take advantage of subscription-based services. The rapid expansion of quick commerce and advancements in digital payment systems are also expected to further drive online sales, making it a key growth area for the edible flakes market in the coming years.

Geography Analysis

In 2025, North America dominated the global edible flakes market, accounting for 37.54% of total revenue. This region benefits from high consumption rates, a well-established retail infrastructure, and the influence of major retailers like Target and Walmart, which drive product standards and packaging trends. However, as the North American market is mature, sales volume growth is limited. To address this, companies are focusing on premium products, such as protein-enriched and organic flakes, while also exploring direct-to-consumer sales channels to boost revenue.

The Asia-Pacific region is expected to grow the fastest, with a projected CAGR of 6.36% through 2031. Rapid urbanization and the growing popularity of Western-style breakfasts are driving demand in countries like China and India. Rising disposable incomes and an expanding middle class are further fueling this growth. Companies are tailoring their products to suit local preferences by introducing region-specific flavors and grains. Additionally, domestic manufacturers are scaling up production with government support, which is increasing competition and improving market penetration in the region.

Europe continues to show stable demand for edible flakes, but strict regulations heavily influence product composition and health claims. Regulatory bodies, such as the European Food Safety Authority, play a significant role in determining permissible claims and ingredient standards. In South America, countries like Brazil are driving growth due to urbanization and increasing demand for packaged foods, despite economic challenges. Meanwhile, the Middle East and Africa are emerging markets where innovations like smaller pack sizes and single-serve options are making edible flakes more accessible to a broader consumer base.

Competitive Landscape

The edible flakes market is moderately consolidated, with major players like Kellanova, General Mills Inc., Nestlé S.A., Post Holdings Inc., and PepsiCo Inc. holding significant market shares. These companies leverage their strong brand portfolios, extensive distribution networks, and partnerships with modern retail channels to maintain their dominance. Their large-scale operations give them an advantage in setting prices, influencing product placement, and driving category trends. However, the presence of smaller regional and niche players ensures that competition remains active and diverse.

The competitive landscape is evolving due to ongoing mergers, acquisitions, and product portfolio expansions. For instance, companies like Ferrero are acquiring brands to strengthen their position in the cereal segment. While global players dominate in developed markets, regions like Asia and Latin America remain fragmented, providing opportunities for local brands to thrive. These domestic players often focus on catering to regional tastes and preferences while offering competitive pricing, thereby balancing global and local competition in the market.

Innovation, health-focused products, and sustainability are becoming key drivers of competition in the edible flakes market. Leading companies are prioritizing cleaner ingredient labels, better nutritional profiles, and eco-friendly packaging to meet changing consumer demands. For example, General Mills Inc. is working to eliminate artificial additives, while Post Holdings Inc. and Kellanova are investing in sustainable packaging solutions. New direct-to-consumer brands like Magic Spoon are gaining popularity by offering unique, health-oriented products, demonstrating how innovation can quickly capture consumer interest and disrupt the market.

Edible Flakes Industry Leaders

-

Kellonova

-

General Mills Inc.

-

Post Holdings Inc.

-

Nestlé S.A.

-

PepsiCo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Kellogg’s launched a new Chocolate Peanut flavored cereal, blending its signature crunchy flakes with cocoa and peanut flavors to diversify its breakfast offerings.

- April 2025: PepsiCo unveiled its latest multigrain cereal, boasting functional benefits. Dubbed Mighty Life, the cereal comes in two flavors: Strawberry Blueberry Bliss, aimed at bolstering the immune system, and Very Vanilla, designed to promote strong bones.

- February 2025: Nestlé India unveiled its latest breakfast cereal line, Munch Choco Fills. This new product range is designed to cater to the growing demand for convenient and tasty breakfast options. It is now available across retail outlets and online platforms, ensuring accessibility for a wide consumer base.

- January 2024: WK Kellogg Co. unveiled its new cereal brand, "Eat Your Mouth Off," boasting 100% plant-based ingredients, delivering 22 grams of protein and zero grams of sugar per bowl.

Global Edible Flakes Market Report Scope

Edible flakes are cereal-based food products made by pressing grains like corn, oats, or wheat into thin, ready-to-eat, or quick-cooking forms. The global edible flakes market is segmented into product type, nature, flavor profile, format, distribution channel, and geography. Based on product type, the market is classified into corn flakes, oat flakes, wheat flakes, rice flakes, and others. Based on nature, the market is classified into organic and conventional. Based on flavor profile, the market is classified into classic/plain and flavored. Based on format, the market is classified into ready-to-eat cold flakes, hot/instant flakes, and dehydrated flakes. Based on distribution channel, the market is classified into supermarkets/hypermarkets, convenience stores/grocery stores, online retail stores, and other channels. Based on geography, the market is classified into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Corn Flakes |

| Oat Flakes |

| Wheat Flakes |

| Rice Flakes |

| Others |

| Organic |

| Conventional |

| Classic/Plain |

| Flavored |

| Ready-to-Eat Cold Flakes |

| Hot/Instant Flakes |

| Dehydrated Flakes |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Corn Flakes | |

| Oat Flakes | ||

| Wheat Flakes | ||

| Rice Flakes | ||

| Others | ||

| By Nature | Organic | |

| Conventional | ||

| By Flavor Profile | Classic/Plain | |

| Flavored | ||

| By Format | Ready-to-Eat Cold Flakes | |

| Hot/Instant Flakes | ||

| Dehydrated Flakes | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the edible flakes market in 2026?

The edible flakes market size is estimated at USD 39.83 billion in 2026.

What is the edible flakes market’s expected growth through 2031?

From 2026 to 2031 the market is projected to expand at a 4.17% CAGR, reaching USD 48.86 billion.

Which product type is expanding fastest?

Oat flakes are forecasted to grow at a 5.02% CAGR, benefiting from EFSA-approved beta-glucan health claims.

Why are organic cereals gaining share?

Organic variants avoid synthetic additives under tightening clean-label rules and are projected to post a 6.15% CAGR through 2031.

Page last updated on: