Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

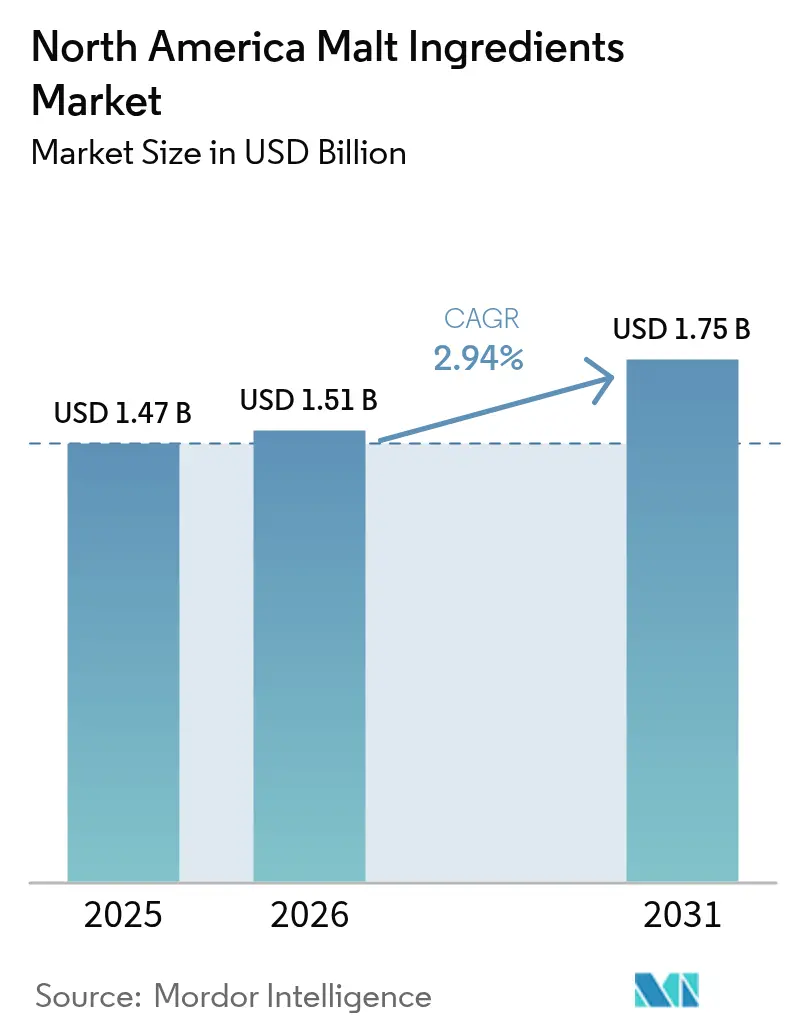

| Base Year Market Size (2025) | USD 1.47 Billion |

| Market Size (2026) | USD 1.51 Billion |

| Market Size (2031) | USD 1.75 Billion |

| Growth Rate (2026 - 2031) | 2.94% CAGR |

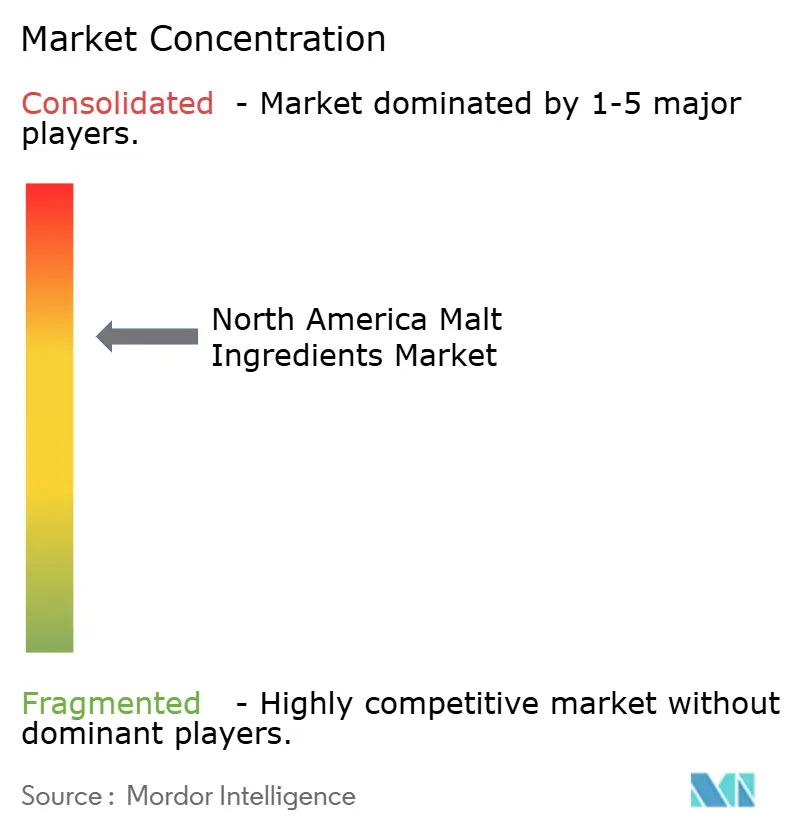

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Malt Ingredients Market Analysis by Mordor Intelligence

The North America malt ingredients market size is expected to grow from USD 1.47 billion in 2025 to USD 1.51 billion in 2026 and is forecast to reach USD 1.75 billion by 2031 at 2.94% CAGR over 2026-2031. Barley has long served as the primary source for malt ingredients in North America. Yet, as brewers and food formulators increasingly seek gluten-tolerant and clean-label alternatives, the demand for wheat and rice malts is on the rise. Craft producers predominantly favor dry malt formats for their shelf stability. This shift not only underscores the importance of compliance but also offers a competitive edge to established maltsters. Furthermore, integrated grain sourcing spanning the United States, Canada, and Mexico not only mitigates raw material volatility but also caters to a diverse application base in the food, beverage, and pharmaceutical sectors. While alcoholic beverages continue to dominate, the market is witnessing a diversification in end uses. Non-alcoholic malt-based drinks are emerging as a popular choice, with consumers gravitating towards them as natural energy boosters and healthier alternatives to sugary sodas. In this realm, dry malt extracts are favored for their solubility and nutritional benefits. The pharmaceutical industry also values malt ingredients, utilizing them as excipients and flavoring agents in syrups and tonics. These ingredients cater to formulations that demand a mild sweetness and specific viscosity. Such cross-industry demand underscores North America's status as a mature yet dynamic malt ingredients market, with projections indicating wheat and liquid malt extracts will experience the most significant growth rates.

Key Report Takeaways

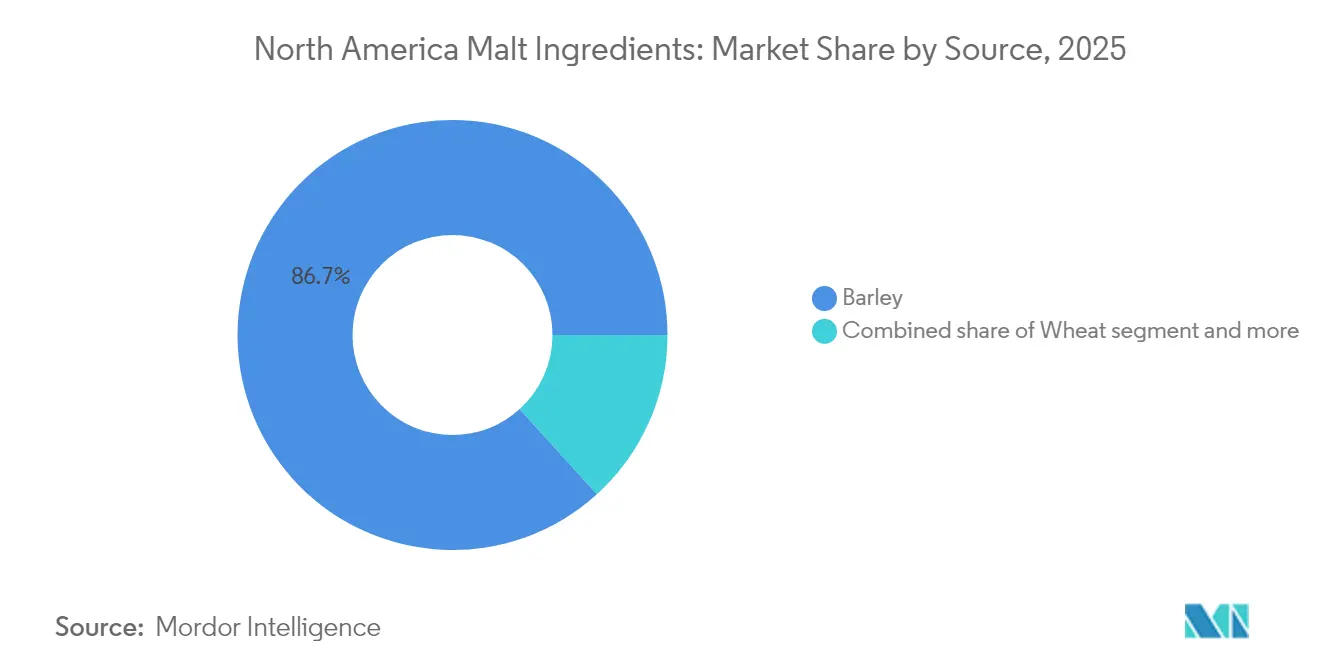

- By source, barley commanded 86.72% of the North America Malt Ingredients market share in 2025; wheat is forecast to post the highest 4.35% CAGR through 2031.

- By form, the dry malt segment held 59.12% of the North America Malt Ingredients market size in 2025, while liquid extracts are projected to expand at a 5.85% CAGR to 2031.

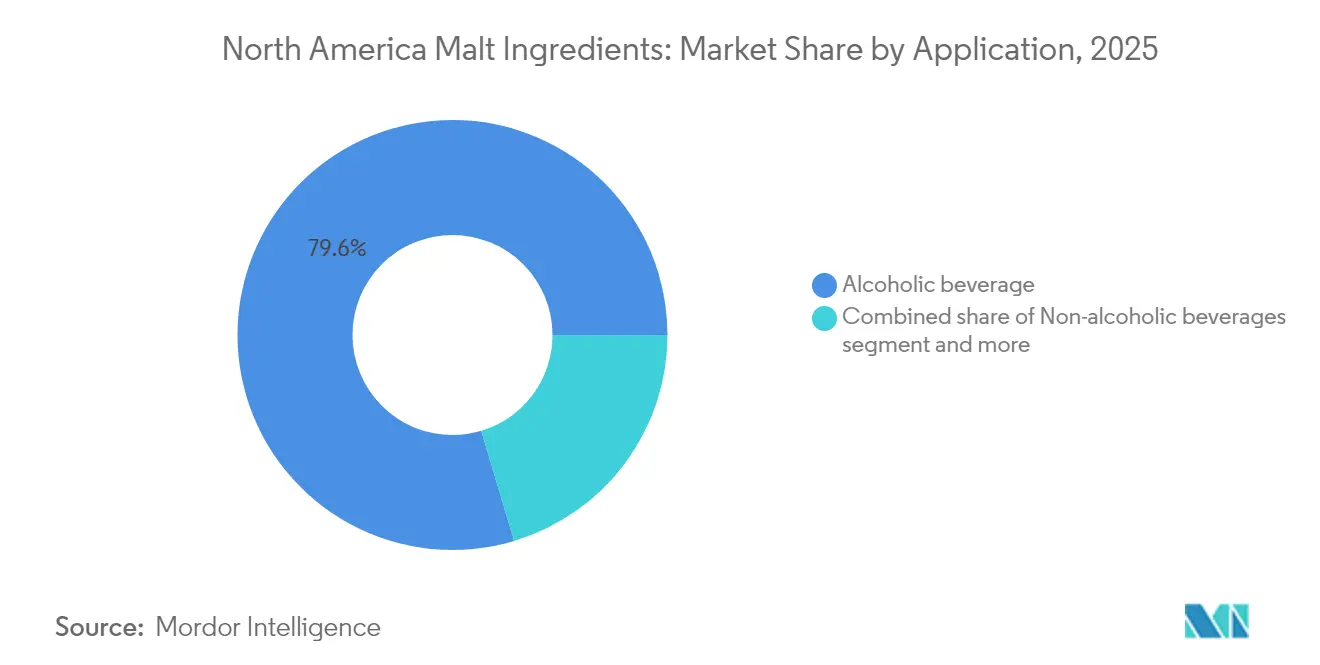

- By application, alcoholic beverages commanded 79.63% revenue in 2025; the food segment is advancing at a 5.72% CAGR through 2031.

- By geography, the United States captured 56.88% of the North America Malt Ingredients market size in 2025; Mexico is the fastest-growing territory at a 5.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Malt Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of craft beer and microbreweries | +1.5% | United States and Canada, spillover to Mexico | Medium term (2-4 years) |

| Growing preference for natural and clean label ingredients | +0.8% | Global, with premium focus in United States urban markets | Long term (≥ 4 years) |

| Expansion of non-alcoholic malt beverage and health tonics | +0.6% | North America core, early adoption in metropolitan areas | Medium term (2-4 years) |

| Technological advancements in malt roasting and enzymatic conversion | +0.4% | United States and Canada manufacturing hubs | Long term (≥ 4 years) |

| Utilization in distilled spirits industry | +0.3% | United States bourbon/whiskey regions, Canada rye production | Short term (≤ 2 years) |

| Increased preference for slow-digesting carbohydrates | +0.2% | North America health-conscious demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Craft Beer and Microbreweries

In North America, the surging popularity of craft beer and the proliferation of microbreweries are fueling robust growth in the malt ingredients market. As consumers increasingly gravitate towards unique, flavorful, and artisanal beers, microbreweries and craft brewers are diversifying their malt selections, turning to specialty and premium malts to set their products apart. In contrast to large-scale commercial breweries that often resort to adjuncts like corn or rice for cost-cutting, craft brewers emphasize flavor complexity and authenticity. They lean heavily on high-quality malts to shape both the foundational and specialty characteristics of their beers. This paradigm shift has spurred a surge in demand for malt ingredients, with craft breweries representing a substantial share of total malt consumption. The microbrewery landscape is witnessing exponential growth, with a steady influx of new entrants each year, intensifying the demand for varied malt profiles. For instance, data from the Brewers Association highlights that in 2024, the United States boasted 9,796 operational craft breweries. This tally included 2,029 microbreweries, 3,552 brewpubs, 3,936 taproom breweries, and 279 regional craft breweries [1]Source: Brewers Association, “Brewers Association Reports 2024 U.S. Craft Brewing Industry Figures”, brewersassociation.org.

Growing Preference for Natural and Clean Label Ingredients

Regulatory changes promoting clean labeling are increasing the value of malt ingredients that emphasize transparency and traceability while maintaining functionality. The Food and Drug Administration (FDA)'s updated Current Good Manufacturing Practice regulations under the Food Safety Modernization Act (FSMA) require malt processors to conduct thorough hazard analyses and implement preventive controls. This positions compliant processors to meet the needs of food manufacturers seeking reliable and verified supply partners. Barley, with its 80% complex carbohydrate content, meets consumer demand for natural ingredients that provide functional benefits without synthetic additives. According to the Brewers Association, the TTB's decision to withdraw its proposed ingredient labeling rule has created regulatory stability for alcoholic beverages. This allows malt suppliers to focus on voluntary transparency initiatives that help differentiate their premium products. The current regulatory environment benefits established processors with strong quality systems while creating challenges for smaller players lacking compliance infrastructure.

Expansion of Non-Alcoholic Malt Beverage and Health Tonics

North America's malt ingredients market is witnessing a surge, driven by the rising popularity of non-alcoholic malt beverages and health tonics. This trend mirrors a broader shift in consumer lifestyles, where wellness, sobriety, and functional nutrition are taking center stage. Millennials and Gen Z, in particular, are gravitating towards alcohol alternatives that not only tantalize the taste buds but also offer health benefits. These malt-based beverages, touted for their rich content of vitamins B and E, amino acids, antioxidants, and soluble fiber, are being promoted as both nutritious and energy-boosting. In these drinks, malt serves a dual purpose: acting as a natural sweetener and enhancing the body, making it a perfect fit for beverages that seek to replicate beer's full-bodied mouthfeel without the alcohol. Industry giants, including Heineken (with Heineken 0.0), Athletic Brewing Co., and Budweiser Zero, are pouring significant investments into non-alcoholic malt beverages, prioritizing high-quality malt to ensure authentic flavor.

Technological Advancements in Malt Roasting and Enzymatic Conversion

In North America, improvements in malt roasting technology and enzymatic conversion are enhancing the quality and functionality of malt ingredients in food and beverages. The advanced roasting systems provide precise control over color, flavor, and aroma, enabling manufacturers to produce customized malts for various products, from dark stouts to light breakfast cereals. This capability enables maltsters to deliver consistent, high-quality ingredients that serve both craft brewers and large food manufacturers. The optimization of enzymatic conversion through controlled germination increases extract efficiency while maintaining functional compounds, helping processors achieve higher yields from premium barley varieties. The development of disease-resistant barley cultivars, supported by a USD 2.1 million investment from the Saskatchewan Barley Development Commission in 2024, reduces processing variations and maintains enzymatic activity for efficient conversion [2]Source: Barley Bin, “Farmers Struggle With Pre-Harvest Sprouting,” Barley Bin, barleybin.ca . These technological improvements enhance the capabilities of processors using precision equipment and help standardize malt production processes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing trend towards gluten-free diets | -0.4% | United States and Canada health-conscious segments | Medium term (2-4 years) |

| Limited consumer awareness about malt benefits in non-beverage applications | -0.3% | North America beyond traditional brewing regions | Long term (≥ 4 years) |

| Strict FDA guidelines on labeling | -0.2% | United States food and beverage manufacturers | Medium term (2-4 years) |

| Traceability mandates under Food Safety Modernization Act (FSMA) | -0.1% | United States grain processing facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Trend Towards Gluten-Free Diets

As consumers increasingly avoid gluten, ingredient choices in the food and beverage sectors are shifting. This trend not only pressures traditional barley-based malts but also paves the way for alternative grain processing. While rice malt is pricier to produce than its barley counterpart, it boasts advantages in gluten-free brewing and niche applications, where compliance with regulations can justify its premium price. In the United States, domestic malting barley production falls short of meeting local demand, leading to imports and a resultant supply vulnerability, especially in light of the rising trend towards gluten-free substitutes. Hemp seeds, with their high protein content and essential fatty acids, emerge as functional alternatives, stepping into roles traditionally held by malt, especially in providing protein and flavor depth. Yet, rice, with its superior yields and malting qualities, presents a sustainable avenue for processors ready to pivot towards alternative grains. However, the regulatory constraints surrounding THC content in hemp products curtail their immediate potential as substitutes.

Limited Consumer Awareness About Malt Benefits in Non-Beverage Applications

Malt ingredients are underutilized in food, pharmaceutical, and nutraceutical applications because their functional benefits are not widely recognized. Whole grains highlight the advantages of dietary fiber, protein, and phenolic acids in preventing chronic diseases, creating opportunities for malt-based ingredients. However, consumers are more familiar with established whole grains like quinoa and oats. The Association of American Feed Control Officials emphasizes the need for accurate labeling and ingredient representation in feed applications [3]Source: AAFCO Communications, “AAFCO and K-State Olathe Seek SMEs for New SRIS Process,” Association of American Feed Control Officials, aafco.org. This regulatory focus could help expand malt usage, but consumer education remains insufficient. Efforts to promote sustainability, such as using brewery waste for animal feed and energy production, showcase malt's role in a circular economy. However, public awareness of these environmental benefits is still limited. Investing in consumer education could increase demand for malt in functional foods. Additionally, targeted B2B communication with food formulators and nutritionists could quickly raise awareness and drive adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Barley Dominance Faces Alternative Grain Pressure

In 2025, barley grain commanded a dominant 86.72% share of North America's malt ingredients market. This stronghold stems from barley's established agronomic foundation, its high diastatic power, and its consistent performance in both brewing and food applications. Two-rowed barley stands out as the top choice for malting, thanks to its uniform kernel size, dependable enzyme production, and versatility in both large-scale and craft brewing. While traditional varieties like CDC Copeland have long been staples, they're now being overshadowed by advanced cultivars such as CDC Fraser and AAC Connect. These newer varieties boast superior disease resistance and enhanced processing traits, mirroring the industry's pivot towards efficiency and resilience in the face of climate challenges.

Wheat malt, despite its smaller market share, is on an upward trajectory, forecasted to expand at a robust 4.35% CAGR through 2031. Wheat malt's rising prominence drives this surge in gluten-tolerant brewing and its role in refining beer's mouthfeel, head retention, and overall product distinction. With its clean-label allure and versatile functionality, wheat malt is carving out a significant niche in both the craft brewing arena and the specialty food domain. As consumers increasingly gravitate towards texture-rich and premium products, wheat malt is solidifying its status as a pivotal growth catalyst. This trend is especially evident among processors who are diversifying their sourcing strategies and honing specialized processing techniques.

By Form: Liquid Extracts Accelerate Amid Processing Convenience

In 2025, dry malt extracts commanded a leading 59.12% share of North America's malt ingredients market. Their dominance stems from advantages like an extended shelf life, reduced transportation costs, and versatility across various end-use scenarios. Being lightweight and stable, dry malts are especially favored by small to mid-sized breweries, food processors, and export markets prioritizing logistics efficiency. Their cost-effectiveness, coupled with easy storage and minimized spoilage risk, has led to widespread adoption in craft brewing and packaged food sectors. Moreover, the flexibility in formulation further cements dry malt's status as a go-to ingredient in industries prioritizing stability and storage convenience.

On the other hand, liquid malt extracts are set to outpace the competition, with projections indicating a robust 5.85% CAGR through 2031. Their appeal lies in processing convenience and reliable sugar profiles. Such consistency is paramount in industrial brewing and food manufacturing, where operational efficiency is key. Liquid extracts streamline the process, reducing steps and allowing for meticulous control over enzymatic conversion. This precision enables manufacturers to tailor sugar compositions for niche applications, including pharmaceuticals. Moreover, advancements in concentration and preservation techniques are bolstering the stability and quality of liquid malts. This enhancement makes liquid malts a more appealing option, even with their higher initial costs, especially in scenarios demanding rapid processing and standardization.

By Application: Food Segment Emerges as Growth Engine

In 2025, alcoholic beverages commanded a significant 79.63% share of North America's malt ingredients market, underscoring the region's rich brewing heritage and the pivotal role of malt in crafting beer and spirits. The established infrastructure, coupled with consumer loyalty and continuous product innovation, bolsters the prevalent use of malt in both craft and mainstream brewing. Malt is essential in alcoholic beverage formulations, playing a crucial role in fermentation, flavor enhancement, and body development. As craft brewing experiences a resurgence and premiumization trends gain momentum, malt's importance in the sector is further solidified, ensuring its dominance among both large-scale and artisanal producers.

On the other hand, food applications are set to witness the most rapid growth, with a projected CAGR of 5.72% through 2031, fueled by an increasing consumer focus on health and wellness. Thanks to their slow-digesting carbohydrate profile and benefits for glycemic control, malt-derived ingredients are becoming popular in sports nutrition, meal replacements, and products catering to diabetics. The rising appetite for clean-label, functional ingredients in both packaged and fresh foods is broadening malt's role, extending well beyond its traditional brewing applications. Furthermore, malt's versatility shines through its applications in non-alcoholic beverages, pharmaceuticals, and animal feed, diversifying the market. This diversification empowers processors to craft specialized, value-added products, lessening their reliance on the alcoholic beverage sector.

Geography Analysis

In 2025, the United States commands a dominant 56.88% share of the North American malt ingredients market, bolstered by concentrated craft brewing hubs and a robust distilled spirits sector. This sector, as highlighted by the Distilled Spirits Council, consumed a staggering 2.8 billion pounds of grains. Meanwhile, Mexico is on the rise, with projections indicating a robust 5.11% CAGR growth rate through 2031. This surge is largely attributed to a burgeoning craft beer scene and a boost in disposable incomes. Urban centers, backed by a strong distribution network, are witnessing a notable shift in consumer behavior, leading to increased experimentation with craft brewing.

Canada, the fifth-largest global barley producer, holds a strategic position, ranking third in malt barley exports and sixth in total barley exports. By 2025, as per the United States Department of Agriculture (USDA), Canada is set to export 36% of its annual barley output, making up 7.5% of the global barley trade. Meanwhile, other North American nations, despite having limited local processing facilities, are seeing a growing appetite for specialty malt imports, catering to niche and premium brewing needs.

North America, with its advanced agricultural prowess and a strong consumer inclination towards craft and specialty beverages, boasts the largest regional market share globally. Significant investments in processing technology further bolster this position. The region's seasoned brewing industry, coupled with easy access to top-tier raw materials and streamlined distribution channels, cements its status as a frontrunner in malt ingredient production and innovation. This robust foundation not only ensures a steady supply but also fosters the development of premium malt varieties, reinforcing the market's enduring competitive edge.

Competitive Landscape

Strategic acquisitions are reshaping competitive dynamics in the market, leading to moderate consolidation. These acquisitions are enhancing processing capabilities and expanding geographic reach, allowing companies to strengthen their market positions. Notable players making their mark include Malteurop Malting Company, Rahr Corporation, Briess Malt & Ingredients Co., and InVivo Group, which continue to influence the competitive landscape through innovation and strategic initiatives.

Beyond traditional brewing, the market is witnessing a surge in growth opportunities, especially in alternative grain processing and niche applications. The gluten-free allure of rice malt is driving demand among health-conscious consumers, while the rising trend of hemp-based ingredients is opening doors to new product categories, particularly in the functional food and beverage sectors. Initiatives like ReGenMalt™ not only champion regenerative farming practices but also empower processors to stand out in the eyes of eco-conscious consumers by aligning with sustainability trends. These programs provide a dual advantage of environmental stewardship and market differentiation, which are increasingly critical in today's competitive environment.

While technology partnerships grant smaller processors a foothold in advanced capabilities sans hefty investments, larger processors are leveraging vertical integration to maintain quality and manage costs effectively. Vertical integration allows these companies to oversee the entire supply chain, ensuring consistency and reducing dependency on external suppliers. These regulatory requirements demand significant investments in quality systems and operational adjustments, inadvertently favoring established players with well-oiled compliance mechanisms. As a result, smaller processors face entry barriers, while larger, established companies continue to consolidate their positions in the market.

North America Malt Ingredients Industry Leaders

Malteurop Malting Company

Rahr Corporation

Briess Malt & Ingredients Co.

InVivo Group

Boortmalt

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: LD Carlson established a partnership with the Malting Company of Ireland (MCI) to distribute traditional Irish malts to U.S. craft brewers. The partnership enables American brewers to access MCI's sustainably sourced malts, produced in Cork, Ireland, with support from over 600 local barley growers.

- April 2025: Blue Ox Malthouse, located in Lisbon Falls, Maine, expanded its specialty malt portfolio by introducing seven new roasted malts. As the largest traditional floor maltster outside Europe, the company launched Chocolate Rye, Crystal 90, Crystal 120, Golden Triticale, Roasted Barley, Roasted Oats, and Roasted Wheat. The company developed these floor-malted products in collaboration with craft breweries, including Maine Beer Co. and Tributary Brewing, using premium grains from Northeast family farms.

- November 2024: French & Jupps, the UK's oldest maltster, formed a partnership with TBI Pro Brew Supply to reintroduce its malts to the American craft brewing market. These products were previously known in the U.S. as William Crisp Malt. The partnership utilizes TBI's distribution network to strengthen French & Jupps' market presence in the United States.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North America malt ingredient market as the total value of dry and liquid malted-grain extracts, flours, and syrups manufactured or imported into the United States, Canada, Mexico, and the Rest of North America, then sold for brewing, distilled spirits, soft drinks, bakery, confectionery, animal feed, and nutraceutical uses.

Scope exclusion: flavorings synthesized without a malt base and enzyme blends with no fermentable malt solids are outside our count.

Segmentation Overview

- By Source

- Barley

- Wheat

- Others

- By Form

- Liquid

- Dry

- By Application

- Alcoholic beverages

- Non-alcoholic beverages

- Food

- Pharmaceuticals

- Animal Feed

- By Geography

- United States

- Canada

- Mexico

- Rest of North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple touchpoints with maltsters, craft brewers, food formulators, feed compounders, and logistics brokers across the United States, Canada, and Mexico helped us validate usage ratios, typical contract prices, export premiums, and seasonality. Expert conversations also tested early model outputs and refined scenario boundaries.

Desk Research

We first mapped the demand pool through publicly available datasets such as USDA-NASS barley acreage and yield reports, Alcohol & Tobacco Tax and Trade Bureau beer production filings, UN Comtrade HS-1107 malt trade records, FAOSTAT grain balances, and Brewers Association craft brewery censuses. Company 10-Ks, investor decks, and trade association briefs supplied price corridors and end-use mix insights. Paid repositories, including D&B Hoovers for revenue splits and Volza for shipment drill-downs, added depth. This list is illustrative; many other open and licensed sources supported evidence gathering and cross-checks.

Market-Sizing & Forecasting

A top-down production and trade reconstruction estimated the regional malt supply, which is then reconciled with application-level consumption coefficients before selective bottom-up sanity checks from sampled capacity roll-ups and ASP × volume calculations. Key variables like barley harvest volume, average extract recovery rate, beer output per hectoliter, craft brewery openings, and import duty shifts shape the baseline. Forecasts through 2030 rely on ARIMA models blended with scenario inputs vetted by interviewees; gaps in bottom-up datapoints are bridged by weighted averages from adjacent comparable facilities.

Data Validation & Update Cycle

Analysts at Mordor Intelligence pass every draft through variance scans versus historical series, peer ratios, and independent indicators. Outliers trigger re-contact with respondents or desk-source re-checks. The model refreshes each year, with interim revisions after material regulatory or crop events. A final analyst pass occurs just before release so clients receive the latest view.

Why Mordor's North America Malt Ingredients Baseline Commands Reliability

Published figures can diverge because firms adopt different ingredient scopes, apply inconsistent price ladders, or refresh at uneven cadences.

Key gap drivers include whether by-product sweeteners are bundled, if wholesale margins are marked up, and the treatment of Mexico's emerging craft segment. Mordor's disciplined scope alignment, annual refresh, and dual-track validation keep our number a dependable starting point for planners.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.47 B (2025) | Mordor Intelligence | - |

| USD 2.50 B (2024) | Regional Consultancy A | Adds brewer's spent grains value and wholesale mark-ups |

| USD 8.00 B (2024) | Global Consultancy B | Uses global to region split ratios and blends feed-grade extracts |

| USD 3.50 B (2024) | Sector Research Firm C | Omits Mexico yet counts specialty malted flours |

In sum, while others widen or narrow definitions, Mordor's clearly bounded scope, transparent variable set, and recurring validation give decision-makers a balanced, traceable baseline they can build on with confidence.

Key Questions Answered in the Report

What is the current size of the North America Malt Ingredients Market?

The market is valued at USD 1.51 billion in 2026 and is projected to reach USD 1.75 billion by 2031.

Which source segment dominates the market?

Barley holds 86.72% share, although wheat is growing the fastest with a 4.35% CAGR through 2031.

Why are liquid malt extracts gaining popularity?

Large brewers favor liquid extracts for dosing precision and reduced processing steps, driving a 5.85% CAGR to 2031.

How is regulatory change influencing market dynamics?

FSMA traceability mandates and clean-label expectations are pushing maltsters to invest in digital tracking and preventive-controls compliance.

Page last updated on: