Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.56 Billion |

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.15 Billion |

| Growth Rate (2026 - 2031) | 5.48% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Malt Ingredient Market Analysis by Mordor Intelligence

Europe malt ingredients market size in 2026 is estimated at USD 1.65 billion, growing from 2025 value of USD 1.56 billion with 2031 projections showing USD 2.15 billion, growing at 5.48% CAGR over 2026-2031. As demand surges for premium craft beer and non-alcoholic brews increasingly seek flavor-rich malts, the long-term growth of malted barley, rye, wheat, and oats remains robust. This growth is further bolstered by expanded Scotch and continental distilling capacities. Clean-label demands from bakers and breakfast cereal makers, coupled with the broader availability of organic raw materials under EU Regulation 2018/848, present amplified opportunities across the value chain[1]Source: European Commission, "Organic production and products", agriculture.ec.europa.eu. Additionally, brewers are showing heightened interest in certified low-carbon supply chains. Key innovation themes include energy-efficient kilning, custom blends that give brewers a unique edge, and liquid malt extracts that streamline bakery operations. However, challenges persist: drought-induced fluctuations in barley yields and rising electricity and natural gas prices jeopardize margins for smaller maltsters. This scenario accentuates the competitive advantage for players who have embraced vertical integration and invested in decarbonization.

Key Report Takeaways

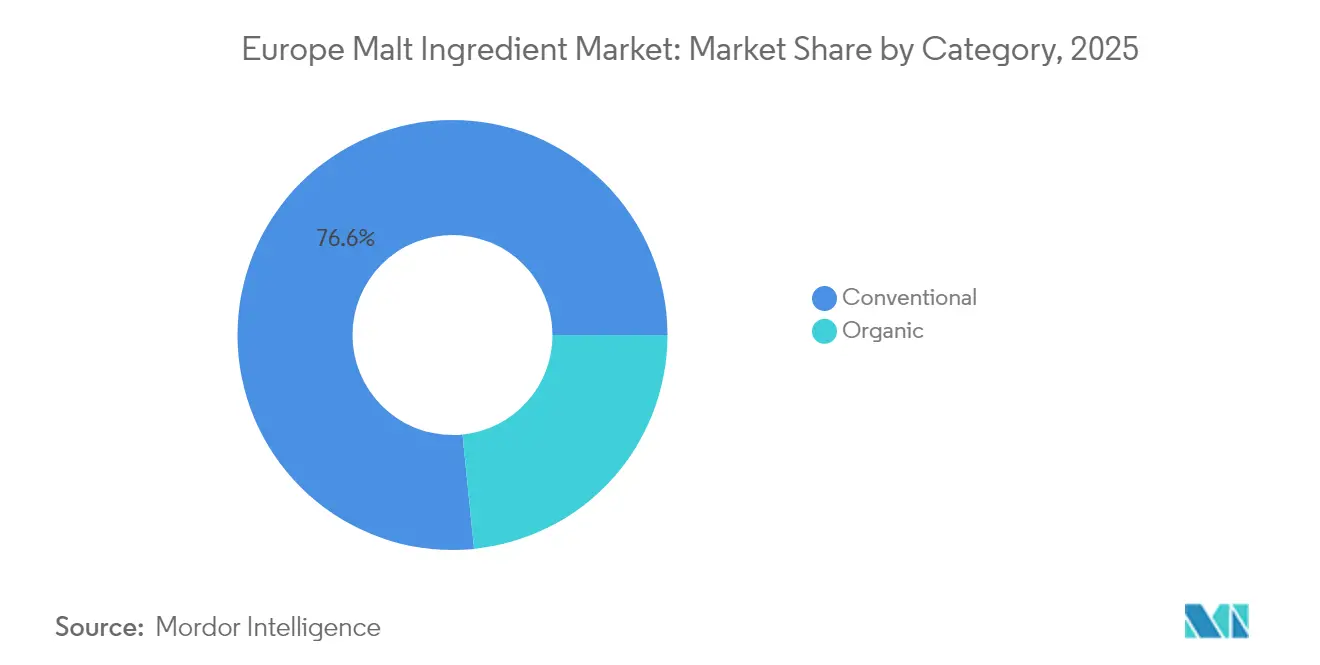

- By category, conventional products captured 76.60% of the Europe malt ingredients market share in 2025, while organic variants are set to expand at a 6.85% CAGR through 2031.

- By source, barley led with 47.80% share in 2025; rye malt is poised for the fastest 5.92% CAGR through 2031.

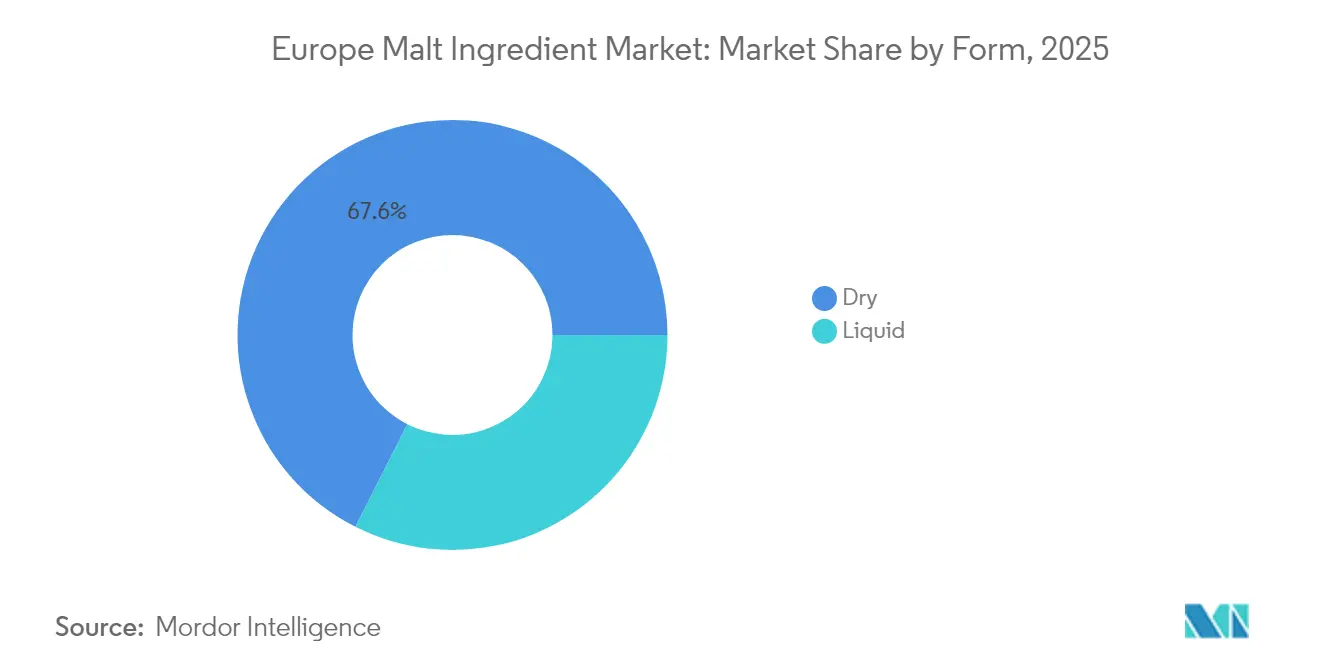

- By form, dry malt commanded 67.55% revenue share in 2025, yet liquid malt extract is projected to rise at a 7.15% CAGR to 2031 on bakery and contract-brewing uptake EUROMALT.EU.

- By application, beverages accounted for 82.65% share in 2025, whereas breakfast cereals will record the top 6.86% CAGR through 2031.

- By geography, Germany generated 23.35% of 2025 revenue; Spain is set for the highest 6.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Malt Ingredient Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Europe’s craft brewery proliferation and premiumization | +1.2% | Germany, United Kingdom, Netherlands, Belgium, France | Medium term (2-4 years) |

| Non-alcoholic and low-alcohol beer surge needs flavor-rich malts | +0.9% | Germany, United Kingdom, Spain, Nordics | Short term (≤ 2 years) |

| Scotch and European distilling capacity additions | +0.7% | United Kingdom (Scotland), Ireland, France | Long term (≥ 4 years) |

| Clean-label reformulation in bakery, cereals, and RTD beverages | +0.8% | Germany, France, United Kingdom, Italy, Netherlands | Medium term (2-4 years) |

| Custom blends and specialty malts accelerating brewer innovation | +1.0% | Germany, Belgium, United Kingdom, Netherlands, Poland | Short term (≤ 2 years) |

| Decarbonization budgets and low-carbon malt procurement | +0.6% | EU-wide led by Germany, France, Netherlands, Belgium | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Europe's craft brewery proliferation and premiumization

Even as the number of breweries stabilizes in certain regions, thousands of small breweries are actively reshaping the malt ingredients market in Europe. These surviving breweries are pivoting towards higher-margin lagers and IPAs, utilizing roasted and caramel malts to enhance the ingredient value per hectoliter. In Germany, craft labels command a premium, with drinkers shelling out 15-20% more. This trend has led malt houses, like Weyermann, to expand their portfolios, introducing a wider range of smoked and acidulated malts. Meanwhile, Belgian abbey traditions sustain a robust demand for richly colored malts. In the UK, brewers are turning to organic pale ale malt, catering to the clean-label trend, a demand met by Viking Malt’s launch in January 2025. Today, emphasizing malt provenance on packaging is integral to premium brand narratives, fostering multi-year supply commitments. Maltsters that provide a diverse range, ensure traceability, and offer brew-house support are reaping the benefits with higher margins.

Non-alcoholic and low-alcohol beer surge needs flavor-rich malts

In 2024, the mainstreaming of the 0.0% ABV category is underscored by production upgrades at Guinness. Brewers, noting that fermentation imparts less flavor, turn to specialty roasted and high-enzyme diastatic malts to enrich their 0.0% ABV recipes and achieve a balanced taste profile. Germany and the Nordics continue to dominate per-capita consumption due to their established beer culture and preference for innovative brewing techniques. Meanwhile, Spain's hospitality resurgence, driven by increased tourism and consumer spending, is fueling a significant surge in off-trade sales. Techniques that halt fermentation require 10-15% more malt per hectoliter, meaning even a stable beer volume results in heightened malt demand. This creates opportunities for suppliers who can customize malt specifications for low-alcohol brewing, allowing them to capitalize on this burgeoning premium niche and cater to the evolving preferences of health-conscious consumers.

Scotch and European distilling capacity additions

GlenDronach invests USD 38 million to expand its warehouse capacity, underscoring the ongoing commitment to malt-based spirits and ensuring sufficient storage for future production needs. New regulations in Irish whiskey now require traceable malted barley, leading to a surge in certified supply programs aimed at maintaining quality and compliance with these tightened standards. Meanwhile, craft houses in Cognac and Armagnac are venturing into barley and rye spirits, diversifying their product offerings to cater to evolving consumer preferences. Additionally, rising trends in rye whisky across Germany and Poland are boosting the demand for rye malt, driven by increasing consumer interest in unique and regionally influenced spirits. Furthermore, extended barrel aging not only secures future malt usage but also provides maltsters with clearer visibility into long-term demand, reinforcing their barley contracts with cooperatives like Axéréal and ensuring a stable supply chain.

Clean-label reformulation in bakery, cereals, and rtd beverages

In 2024, FoodDrinkEurope advocates for the use of malted cereals, emphasizing their ability to provide natural sweetness and enhance dough functionality, making them a versatile ingredient in various applications. The EU's approval of partially hydrolyzed barley protein in breakfast cereals further highlights malt's potential as a protein-rich and functional component in the food industry. To meet stringent acrylamide benchmarks without compromising crust color, industrial bakeries in Germany and the Netherlands are increasingly replacing synthetic colorants with malt extract, showcasing its dual role in safety and aesthetics. In Spain and Italy, ready-to-drink beverage producers are reintroducing malt-based soft drinks, leveraging malt's distinct maltose content and umami profile to cater to evolving consumer preferences for unique and nostalgic flavors. Additionally, suppliers who provide comprehensive documentation for allergen, organic, and vegan compliance are gaining priority in reformulation processes, reflecting the growing demand for transparency and adherence to dietary standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Barley yield/price volatility and climate shocks | -0.8% | Northwest Europe; offset by Spain, Romania | Short term (≤ 2 years) |

| Energy- and carbon-intensive kilning economics | -0.6% | Germany, France, Belgium, Netherlands, Poland | Medium term (2-4 years) |

| Europe beer volume decline and on-trade share loss | -0.5% | Germany, United Kingdom, France, Italy | Medium term (2-4 years) |

| Acrylamide rules constrain malt use in bakery | -0.3% | Germany, France, Netherlands, United Kingdom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Barley yield/price volatility and climate shocks

In France and Germany, a severe drought in Northwest Europe slashed 2024 spring barley yields by as much as 15%[2]Source: European Commission, "JRC MARS Bulletin - Crop monitoring in Europe - July 2024 - Vol. 32 No 7", publications.jrc.ec.europa.eu. This has tightened the supply of malting-grade barley and driven up spot premiums. While surpluses in Spain and Romania help stabilize the region's overall barley availability, they also increase freight distances to malting hubs in Belgium and Germany. Currently, malting-barley commands a premium of 15-20% over feed barley, a gap that widens when there's a dip in protein or germination quality. The EU Common Market Organisation for cereals provides public intervention mechanisms and private storage aid for barley, yet these tools are rarely activated and offer limited relief during acute shortages[3]Source: European Commission, "Cereals, oilseeds, protein crops and rice", agriculture.ec.europa.eu. Given that public intervention tools are slow to activate, maltsters are turning to forward contracts with farmer cooperatives like Axéréal and VIVESCIA as a risk buffer. However, with climate-adapted barley varieties still over five years from a significant market release, the European malt ingredients market faces vulnerabilities in the short term.

Energy- and carbon-intensive kilning economics

In H1 2024, electricity prices averaged 197 EUR/MWh, while natural gas prices fluctuated between 30-40 EUR/MWh. These figures represent a stark increase, ranging from double to quadruple, compared to pre-pandemic benchmarks. The kilning process, essential for reducing green malt moisture from 45-50% to nearly 4%, accounts for approximately two-thirds of the total energy consumption at the site. The volatility introduced by LNG imports poses challenges, especially for mid-sized maltsters lacking heat-recovery systems or biomass integration. While EU tax reforms offer relief for electrified heating, this benefit won't be realized until post-2026, leaving a window of short-term cost exposure. Furthermore, brewers find it challenging to pass on these surcharges, especially with the competitive pressure from Canadian and Australian malt imports, which enjoy lower energy costs. This dynamic is further compressing margins across the European malt ingredients market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Organic Certification Unlocks Premium Channels

In 2025, conventional grades dominated the European malt ingredients market, securing 76.60% of total revenues. Their stronghold is attributed to well-established supply chains, reduced production costs, and versatility across brewing, baking, and food processing, all without the constraints of certification timelines. Major maltsters leverage scale advantages in conventional sourcing, ensuring consistent volumes for mainstream brewers and distillers. Yet, as organic regulations tighten, conventional players feel the squeeze, prompting them to adopt hybrid strategies to navigate rising compliance demands.

Organic grades are the market's fastest-growing segment, projected to advance at a 6.85% CAGR through 2031, driven by Regulation 2018/848's stipulation of 95% organic content in processed foods. A three-year land conversion window leads to supply scarcity, sustaining 35% price premiums. Meanwhile, initiatives like Viking Malt’s 2025 organic Brewer’s Pale Ale, aimed at premium German, Dutch, and Scandinavian brewers, command a 20–30% shelf markup. Germany, France, and the Netherlands spearhead the organic movement, buoyed by affluent consumers and deep retail penetration. This momentum is further fueled by the looming December 2024 deadline for non-organic yeast transitional allowances. Maltsters adept in agronomy, certification, and multi-crop rotations are seizing high-margin opportunities, especially with integrated malt-yeast traceability solutions.

By Source: Rye Malt Gains in Craft Distilling and Bakery

In 2025, barley dominated the European malt ingredients market, securing 47.80% of total revenues. This stronghold is attributed to barley's superior enzymatic strength and its long-standing role in brewing mainstream lagers and ales. Barley’s versatility in brewing processes, coupled with its ability to produce consistent flavor profiles, further reinforces its dominance. Even with stagnant growth in the wheat-beer segment, established supply chains and the ability to scale operations keep barley at the forefront. Suppliers ensure profitability by leveraging a cereal processing infrastructure specifically designed for barley's unique germination needs, which allows for efficient production and cost management.

Rye malt is the market's fastest-growing segment, projected to grow at a 5.92% CAGR through 2031, driven by its sought-after peppery flavor. Craft distillers in Poland, Germany, and Ireland are ramping up rye whisky initiatives, capitalizing on the growing consumer preference for unique and premium spirits. Simultaneously, artisan bakers in Germany and the Netherlands are infusing rye malted flour into their sourdough and crisp breads, catering to the rising demand for artisanal and health-focused baked goods. While dedicated rye malting lines are scarce, requiring unique steeping and germination methods, maltsters like Palatia (BESTMALZ) are strategically reallocating their capacity to seize premium pricing opportunities. This agile shift in product mix not only boosts supplier margins but also positions rye ahead of the slower-growing oat and wheat alternatives, reflecting its increasing importance in both the beverage and bakery industries.

By Form: Liquid Malt Extract Gains in Bakery and Brewing Convenience

In 2025, dry malt dominated the European malt ingredients market, securing 67.55% of total revenues. With a moisture content of just 4–5%, dry malt boasts efficient silo storage and an extended shelf life. This makes it a preferred choice for high-volume operations in brewing, baking, and food processing. Additionally, its ability to maintain quality and stability under varying conditions makes it highly reliable for manufacturers. Furthermore, specialty roasted flavors lean towards dry formats, ensuring precise control and stability during transport and formulation. Even with the rise of liquid alternatives, established infrastructure, including widespread availability and established supply chains, bolsters dry malt's leading position.

Liquid malt extract is the market's fastest-growing segment, projected to grow at a 7.15% CAGR through 2031. Large bakeries are turning to pumpable concentrated wort, not only for streamlined handling but also to avoid synthetic colorants. This choice helps maintain enzyme activity during mashing and evaporation, ensuring optimal crust development while staying within acrylamide limits. The convenience of liquid malt extract also reduces operational complexities, making it an attractive option for large-scale production. Meanwhile, contract brewers lacking mash tuns are opting for liquid formats. They’re willing to pay a premium of 10–15% more per extract unit, valuing the superior consistency it offers. This growth in liquid malt extract complements the overall product mix, yet it doesn't overshadow dry malt's dominant volume leadership.

By Application: Breakfast Cereals Leverage Functional Malt Ingredients

In 2025, beverages dominated the European malt ingredients market, accounting for a substantial 82.65% of total revenues. This stronghold is underscored by the EU's production of 34.7 billion liters of beer and a significant output of Scotch whisky, both of which depend on malt for enzymatic conversion and flavor. The enduring demand for lagers bolsters the processing infrastructure of mainstream breweries, ensuring consistent high-volume production. Additionally, non-alcoholic beer variants utilize 10–15% more malt per hectoliter compared to their alcoholic counterparts, presenting a notable growth opportunity even as alcoholic beer consumption remains stagnant. This trend highlights the evolving preferences of consumers and the adaptability of malt producers in catering to these shifts.

Breakfast cereals are emerging as the fastest-growing sector, projected to grow at a 6.86% CAGR through 2031. This surge follows the novel-food approval for using up to 5 g of partially hydrolyzed barley protein per 100 g. Prominent cereal brands in Germany and the UK are now blending malted barley flour into their health-focused products, enhancing them with beta-glucan fiber and a natural honey-like sweetness. These formulations align with the increasing consumer demand for nutritious and functional foods. While bakery applications experience limited growth due to acrylamide regulations, this is somewhat balanced by the increasing adoption of liquid extracts, which offer versatility and ease of use in various recipes. Dairy applications, on the other hand, remain a niche market, primarily driven by specialty products. This diversification beyond traditional beverage applications bolsters malt producers' revenue stability, even as alcohol consumption trends evolve.

Geography Analysis

In 2025, Germany accounted for 23.35% of the revenue, bolstered by its extensive maltster network, adherence to the Reinheitsgebot barley standard, and its closeness to Central European breweries. With a notable craft premiumization trend, specialty malt throughput has solidified Germany's position as the primary market. Meanwhile, Spain is on a rapid ascent, boasting the fastest CAGR at 6.98%. With a beer output of 41.1 million hl in 2024 and 279 breweries tapping into caramel and roasted grades for their premium lagers, Spain is making its mark. The UK, blending its Scotch distilling heritage with a lively craft segment, continues to drive demand for specialty products from renowned suppliers like Simpsons and Crisp Malt.

France enjoys the advantage of robust barley harvests, aided by parent cooperatives VIVESCIA and InVivo, which mitigate risks associated with raw material imports. While Italy primarily sources malt for its bakery and pasta industries, its lower per-capita beer consumption curtails any significant beverage-driven growth. Belgium produces more malt than it consumes, strategically directing its plants towards exports, thanks to the logistical advantages of the Antwerp port. To ensure a steady supply of malt ingredients across Europe, the Netherlands, Belgium, and Northern ports import barley from Canada and Australia, safeguarding against climatic uncertainties. Poland's geographical positioning allows it to channel its barley surplus eastward while catering to demand centers in the west. However, limitations in rail and silo capacities temper its growth. In Scandinavia, there's a notable surge in the adoption of organic and zero-alcohol beers, positioning the region as a testing ground for sustainable malt production. Spain's bountiful barley harvest in 2024 underscored its potential as a contingency supply source, especially when Northwest Europe grapples with droughts, enhancing its strategic significance. While Germany's robust beer demand remains central to the landscape, Spain is poised to outstrip its counterparts, buoyed by a resurgence in tourism and an expanding craft beer market.

Competitive Landscape

In the European malt ingredients market, moderate consolidation is evident. Soufflet Malt, Boortmalt, and Malteurop dominate the landscape, yet they contend with specialty rivals like Simpsons, Weyermann, and Viking. Soufflet's acquisition of United Malt in 2023, followed by a rebranding in 2024, has positioned it as the world's largest maltster, boasting a capacity of 3.7 million tonnes. With an eye on the future, Soufflet is now pivoting towards low-carbon barley supply chains and exploring adjacent food markets. Meanwhile, Boortmalt has forged a partnership with Soil Capital, aiming to cut down 200,000 tonnes of CO2 emissions and source two-thirds of its barley regeneratively by 2030. This move not only underscores Boortmalt's commitment to sustainability but also enhances its standing in brewer tenders that prioritize Scope 3 reporting.

Through farmer-cooperative ownership, vertical integration ensures a steady barley supply and cost efficiencies. Regional players carve out niches with organic certifications, unique cereals, and collaborative recipe development via pilot roasters. Opportunities abound in organic malt, rye for distilling, and liquid malt extract, all outpacing the average growth of the European malt ingredients market.

Investments in technology spotlight energy-efficient kilns, digital batch tracing, and automated steeping processes. Simpsons Malt's announcement of an April 2025 capacity extension, incorporating heat-recovery systems, underscores the industry's push towards utility efficiency. While farmer co-ops eye partial downstream ventures, specialty houses are winning over craft brewers, ensuring a competitive landscape and thwarting any drift towards monopoly.

Europe Malt Ingredient Industry Leaders

-

Malteries Soufflet

-

Boortmalt

-

Malteurop

-

Viking Malt

-

Holland Malt

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: ORF Genetics secured €5 million to boost production of its barley-derived MESOkine growth factors. The company aims to amplify its capacity by 14 times by 2027 and a staggering 10,000 times by 2032, all in support of the burgeoning cultivated meat market. This funding not only accelerates the rollout of its Orfeus barley expression system but also slashes growth factor costs through streamlined purification. Furthermore, it strengthens ORF's ties with cultivated meat industry leaders, including Vow.

- June 2025: Carlsberg unveiled “Grobund,” its inaugural beer crafted solely from regeneratively grown barley malt. This launch underscores Carlsberg's commitment to regenerative agriculture. Currently piloting Grobund, the company has ambitious plans: aiming to brew 100 million liters using regenerative barley by 2025, backed by a fresh 14,800-ton malt supply agreement. Looking further ahead, Carlsberg envisions a future where, by 2040, all its grains will be sourced regeneratively.

- June 2022: Teijin forged a partnership with Emilio Peña SA, a Spanish ingredient supplier, to introduce its high-fiber BARLEYmax super barley to Europe. The initial focus is on bread and cereal manufacturers in Spain and Portugal. BARLEYmax boasts nearly 40 times the dietary fiber of white rice, featuring multiple slowly digested fibers and essential micronutrients that promote gut health and healthier formulations.

Europe Malt Ingredient Market Report Scope

Europe malt ingredient market is segmented by Application into Brewing, Distilling, Bakery, Beverages (Non-Alcoholic), Confectionery and Others; by Geography

By Source

| Barley |

| Wheat |

| Rye |

| Oats |

| Others |

By Form

| Dry |

| Liquid |

By Category

| Organic |

| Conventional |

By Application

| Bakery and Confectionery |

| Beverages |

| Breakfast Cereals |

| Dairy |

| Others |

Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Source | Barley |

| Wheat | |

| Rye | |

| Oats | |

| Others | |

| By Form | Dry |

| Liquid | |

| By Category | Organic |

| Conventional | |

| By Application | Bakery and Confectionery |

| Beverages | |

| Breakfast Cereals | |

| Dairy | |

| Others | |

| Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What are the current size and forecast value for the Europe malt ingredients market?

The Europe malt ingredients market size stands at USD 1.65 billion in 2026 and is expected to reach USD 2.15 billion by 2031.

Which segment will grow fastest between 2026 and 2031?

Breakfast cereals will post the fastest 6.86% CAGR, supported by novel-food approval for partially hydrolyzed barley protein.

How big is rye malt’s opportunity?

Rye malt is forecast to advance at 5.92% CAGR as craft distillers and artisan bakers seek peppery flavor profiles.

Why is Spain the fastest-growing geography?

Spain couples a 41.1 million hl beer base with a hospitality recovery and 279 breweries that upgrade to specialty malts, driving a 6.98% CAGR.

Page last updated on: