Market Overview

| Study Period | 2021 - 2031 |

|---|---|

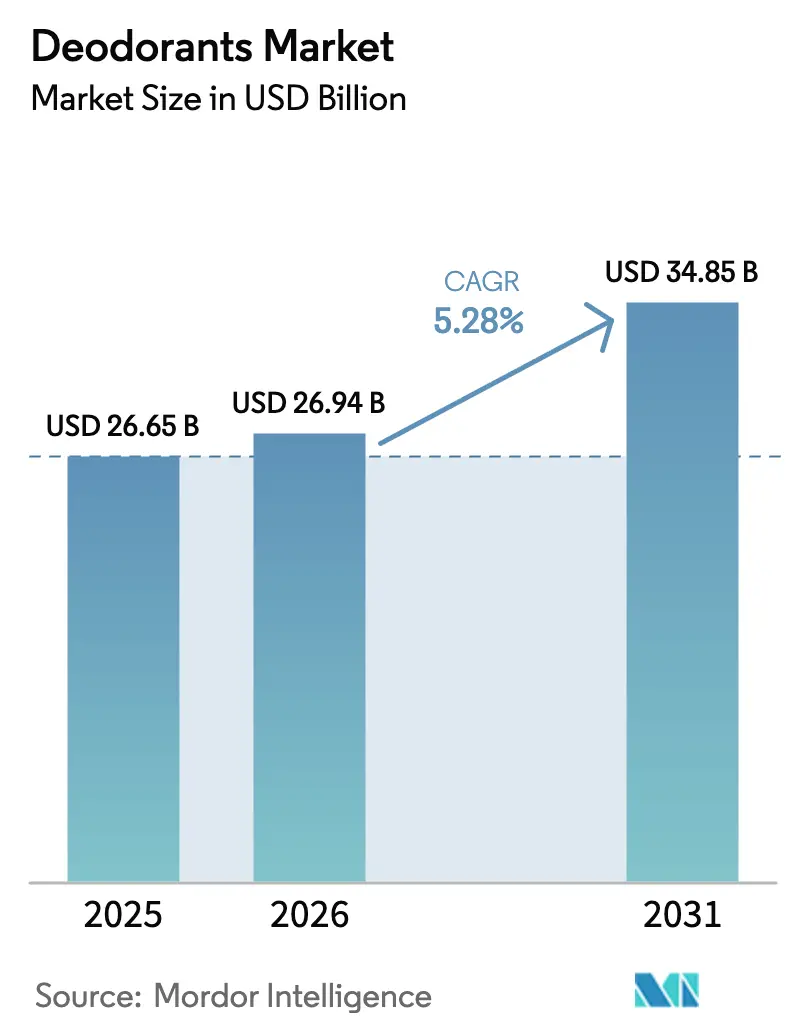

| Market Size (2026) | USD 26.94 Billion |

| Market Size (2031) | USD 34.85 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

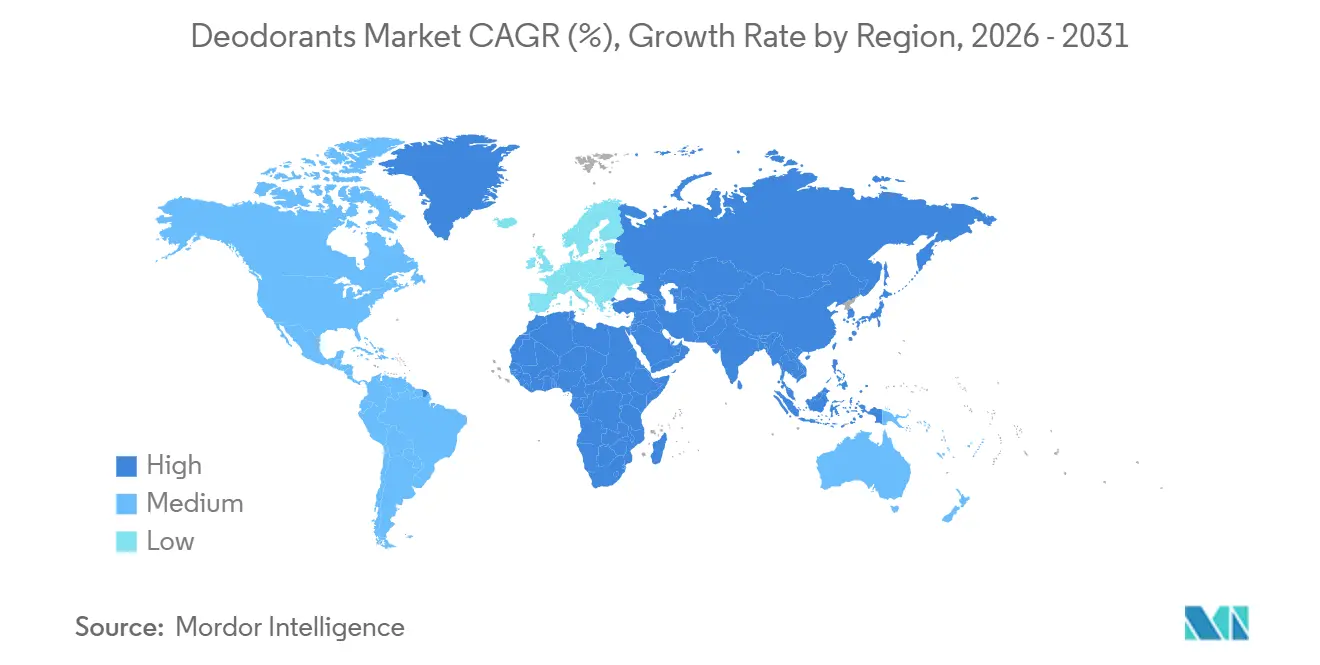

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Deodorants Market Analysis by Mordor Intelligence

The Deodorants Market size was valued at USD 26.65 billion in 2025 and is estimated to grow from USD 26.94 billion in 2026 to reach USD 34.85 billion by 2031, at a CAGR of 5.28% during the forecast period (2026-2031). Consumers are increasingly expanding their odor-control routines beyond traditional underarm applications, driving the adoption of whole-body deodorant formats and contributing to higher per-capita usage. Innovations such as precision roll-on applicators, formulations featuring natural ingredients, and the introduction of refillable packaging are gaining traction among health-conscious and environmentally aware consumers. Additionally, direct-to-consumer (DTC) subscription models are transforming retail economics by offering convenience and fostering customer loyalty. The growing penetration of e-commerce is further emphasizing a structural shift toward digital platforms for product discovery and replenishment. To maintain their market share, established multinational companies are actively acquiring start-ups that prioritize sustainability. However, the market faces challenges such as the prevalence of counterfeit products, complex regulatory landscapes, and competition from substitutes like body sprays, which are collectively tempering the overall growth momentum.

Key Report Takeaways

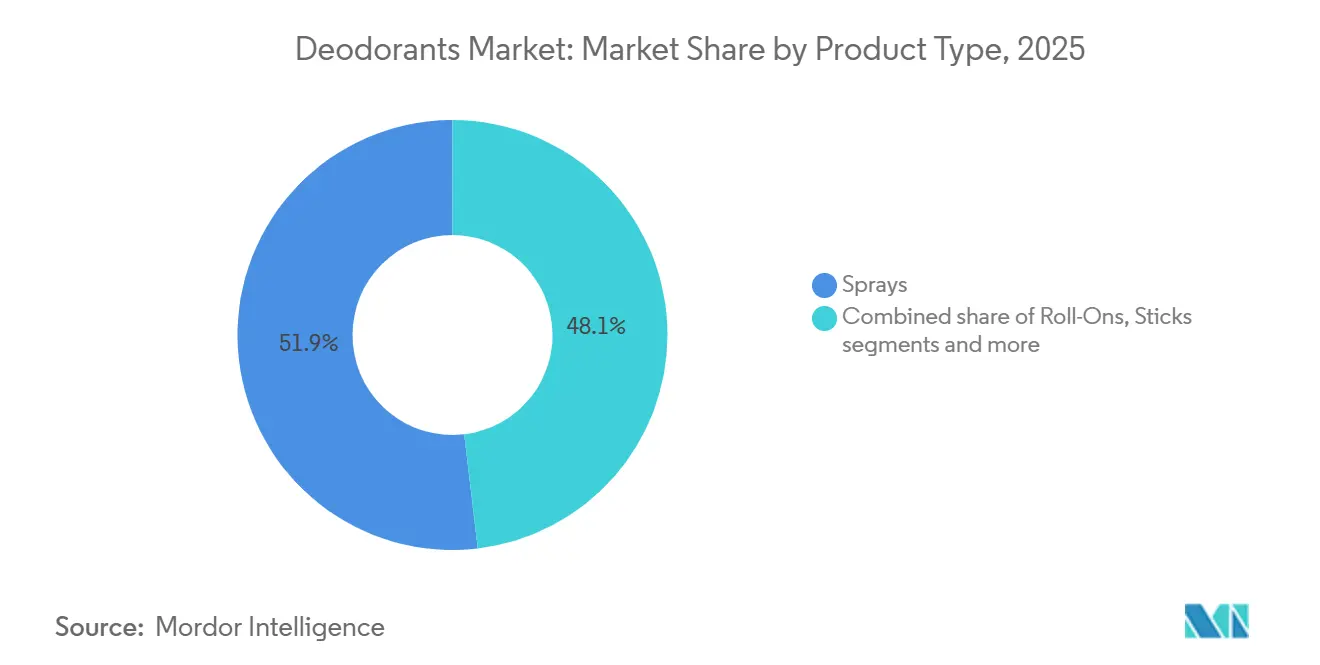

- By product type, sprays led with 51.87% revenue share in 2025; roll-ons are forecast to expand at a 5.87% CAGR through 2031.

- By category, mass offerings held 92.45% of the deodorants market share in 2025, while premium variants are advancing at a 5.64% CAGR to 2031.

- By ingredient source, conventional formulations accounted for 85.15% of the deodorants market size in 2025, and natural/organic options are projected to grow at a 6.25% CAGR through 2031.

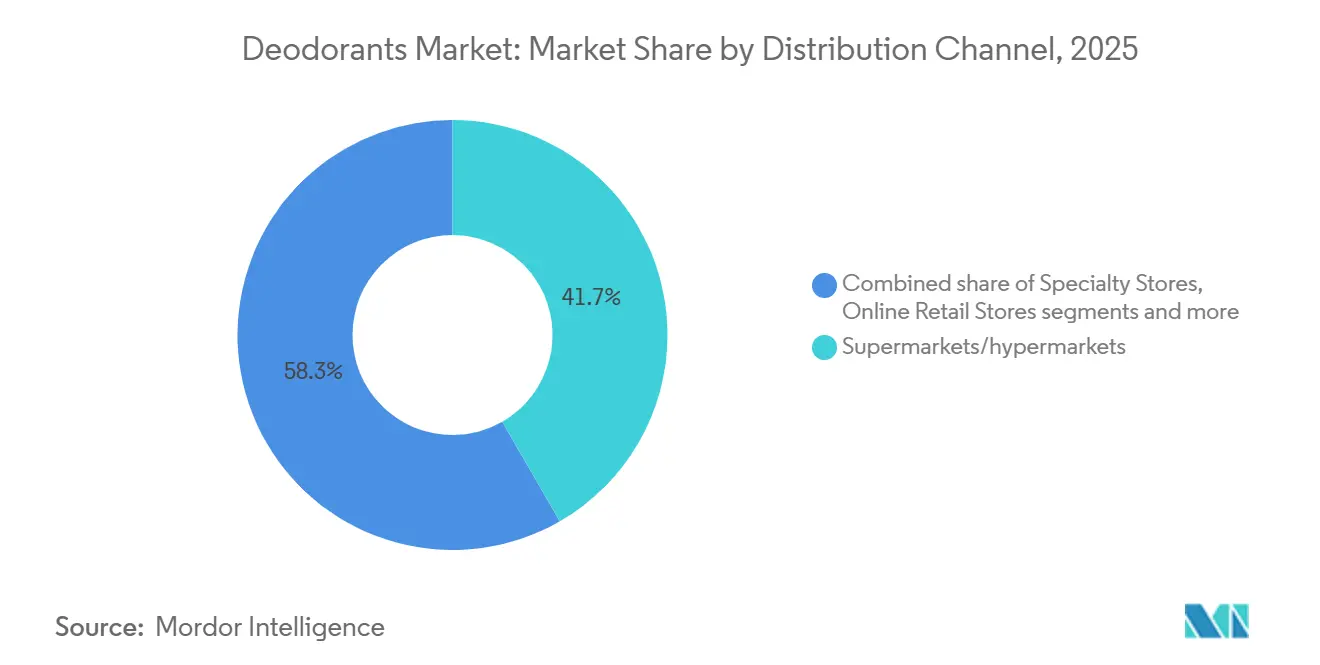

- By distribution channel, supermarkets and hypermarkets captured 41.69% of sales in 2025; online retail is rising at a 6.54% CAGR through 2031.

- By geography, North America commanded 32.92% of the 2025 value, whereas the Asia-Pacific is set to record the fastest 6.39% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Deodorants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising focus on hygiene driven by active, fitness-based lifestyles | +0.8% | Global, with pronounced uptake in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Growing demand for natural and aluminum-free products | +1.2% | North America and Europe lead; Asia-Pacific following as health awareness rises | Long term (≥ 4 years) |

| Growth of whole-body deodorants beyond underarm use | +1.5% | North America pioneer; Europe and Asia-Pacific early adopters | Short term (≤ 2 years) |

| Influence of social media and celebrity endorsement | +0.7% | Global, strongest in North America and Europe where influencer penetration is highest | Short term (≤ 2 years) |

| Effective promotional and marketing strategies | +0.6% | Global, with digital-first campaigns in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Premiumization elevating fragrances as lifestyle products | +0.9% | North America, Europe, and affluent Asia-Pacific urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising focus on hygiene driven by active, fitness-based lifestyles

The global focus on personal hygiene and wellness is driving significant growth in the deodorant market. Consumers increasingly associate physical activity with self-care, leading to a rising demand for long-lasting, high-performance deodorants. The growing participation in sports, fitness routines, and outdoor activities has amplified the need for products that provide reliable sweat and odor protection. This trend highlights a shift from basic hygiene to a modern emphasis on maintaining freshness, confidence, and overall well-being throughout the day. According to the United States Bureau of Labor Statistics, in 2024, approximately 23.6% of men and 19.4% of women in the United States engaged daily in sports, exercise, or recreational activities[1]Source: Bureau of Labor Statistics, "American Time Use Survey", bls.gov. This consistent participation reflects the adoption of health-conscious, active lifestyles, which directly correlates with increased consumption of high-performance deodorants and antiperspirants. Deodorant brands are capitalizing on this trend by aligning their products with active lifestyles and the growing focus on health and wellness. For instance, in March 2025, SheaMoisture launched the 'We Set The Pace' initiative, a campaign encouraging Black women to embrace fitness and personal empowerment. By promoting running and exercise, SheaMoisture positioned itself as a brand that supports wellness while addressing hygiene needs linked to physical activity. This initiative not only emphasizes the importance of fitness but also demonstrates how personal care brands are integrating wellness and hygiene into their narratives, further connecting fitness with the demand for effective deodorant products.

Growing demand for natural and aluminum-free products

The rising demand for natural and aluminum-free products has become a significant market driver. With growing awareness of personal health, sustainability, and the potential risks of synthetic chemicals, consumers are increasingly choosing natural deodorants that exclude aluminum-based compounds and artificial ingredients. This trend stems from concerns about the health risks linked to traditional deodorants, a preference for eco-friendly options, and a demand for greater transparency in ingredient sourcing and product formulation. Awareness of the potential health risks associated with aluminum compounds in conventional antiperspirants is a key factor in this shift. Aluminum compounds, which block sweat glands, have raised concerns about skin absorption and possible links to breast cancer due to their proximity to breast tissue, as well as Alzheimer’s disease, given aluminum's known neurotoxicity at high exposure levels. For instance, the Alzheimer’s Association 2025 Facts and Figures report states that over 7 million Americans are living with Alzheimer’s dementia[2]Source: Alzheimer's Association, "Alzheimer's Disease Facts and Figures", alz.org. This statistic has heightened public scrutiny of everyday aluminum exposure, including through deodorants, as consumers seek preventive hygiene options that avoid pore-blocking agents to reduce perceived long-term risks. Wellness trends and the clean beauty movement have further driven the demand for natural deodorants, particularly among millennials and Gen Z consumers. These groups value ingredient transparency and sustainable consumption. They prefer deodorants made with plant-based or mineral ingredients, such as coconut oil, shea butter, baking soda, and magnesium hydroxide, which neutralize odors without interfering with the body’s natural sweating process.

Growth of whole-body deodorants beyond underarm use

Notable shifts in consumer lifestyles and environmental conditions are propelling the adoption of whole-body deodorants, underscoring their significance in the global deodorants market. Rising temperatures, heightened humidity, and an uptick in heatwaves, often linked to climate change, are amplifying concerns about sweat and body odor in numerous regions. As a result, consumers are now seeking solutions that address perspiration beyond just underarm protection. This shift has spurred demand for products that promise long-lasting freshness, boast antibacterial properties, and offer skin-soothing benefits, even in tough climatic conditions. In response, brands are crafting products that not only ensure comprehensive odor protection but also deliver delightful and personalized fragrance experiences. This has spurred a surge in product launches, showcasing a spectrum of scent profiles from refreshing and clean to warm and tropical, allowing companies to appeal to a wider array of consumer tastes. For example, in January 2024, Native made a significant move by launching its Whole-Body Deodorant range. This new line promises enduring odor protection for various body parts and debuted in four unique scents: Coconut and Vanilla, Cucumber and Mint, Lilac and White Tea, and an exclusive Unscented stick format. Additionally, a growing emphasis on personal confidence, self-expression, and holistic wellness is fueling this segment's expansion. Consumers are increasingly recognizing odor management as not just a hygiene routine, but a vital component of their mental and social well-being. Whole-body deodorants, by offering comprehensive freshness, bolster comfort in social, professional, and intimate interactions. This sentiment resonates particularly with younger demographics and urban dwellers who place a premium on grooming and personal aesthetics.

Influence of social media and celebrity endorsement

In 2024, Jason Momoa effectively utilized his 17 million Instagram followers in a strategic partnership with Native, positioning the brand as rugged and eco-conscious. This collaboration highlighted the brand's alignment with sustainability and an adventurous lifestyle, resonating strongly with its target audience. Similarly, Justin Bieber's collaboration with Schmidt's Naturals for the Peaches line leveraged his extensive 295 million followers to appeal directly to Gen Z consumers. This partnership emphasized the brand's youthful and trendy image, creating a strong connection with a younger demographic. Megan Rapinoe's endorsement of Secret Whole Body not only associated the product with athletic performance but also underscored its commitment to gender inclusivity, making it particularly appealing to progressive and socially conscious audiences. TikTok has emerged as a transformative discovery platform, playing a critical role in brand growth. Dr. Shannon Klingman, founder of Lume, skillfully used the platform to explain the science behind whole-body odor, generating millions of views. Her content effectively converted viewers into buyers without relying on paid media, showcasing the power of organic reach. Similarly, Glossier's community-driven approach has been instrumental in its success. By turning customers into enthusiastic brand ambassadors, the company has fostered organic growth and strengthened its brand loyalty. These innovative strategies bypass traditional retail gatekeepers, enabling emerging brands to scale rapidly. As a result, competition for shelf space and consumer attention has intensified, reshaping the dynamics of the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over chemicals, increasing scrutiny, and skepticism | -0.5% | Global, most pronounced in North America and Europe where health activism is strongest | Long term (≥ 4 years) |

| Regulatory restrictions complicate formulations and can slow product launches | -0.4% | North America (FDA) and Europe (EU cosmetics regulations); emerging markets face uneven enforcement | Medium term (2-4 years) |

| Counterfeits eroding brand trust and safety | -0.3% | Asia-Pacific, Middle East, Africa, and Latin America where enforcement is weakest | Medium term (2-4 years) |

| Competition from substitutes dilutes the deodorant category demand | -0.6% | Global, with body sprays and perfumes competing most intensely in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health concerns over chemicals, increasing scrutiny, and skepticism

Scientific articles and public discussions have scrutinized traditional deodorant ingredients, such as aluminum compounds, synthetic preservatives, and fragrance chemicals, due to potential health concerns. While authoritative bodies like the United States Food and Drug Administration and the European Scientific Committee on Consumer Safety haven't established definitive causal links between these deodorant ingredients and serious diseases, public perception has shifted. Consumers are now gravitating towards “clean”, aluminum-free, and minimally-chemical alternatives. This evolving preference has dampened demand for certain mainstream deodorant formats, prompting the industry to reformulate products, alter labeling, and adopt risk mitigation strategies. Many consumers, swayed by perceived (though not conclusively proven) health risks, have turned away from aluminum-salt antiperspirants, opting instead for aluminum-free options. Concerns about aluminum's potential estrogen-like effects, especially given its proximity to breast tissue and historical ties to cancer and neurodegenerative diseases, have fueled this precautionary shift. Consequently, while demand for traditional aluminum-containing antiperspirants has waned, aluminum-free deodorants have gained traction, impacting unit sales of mainstream clinical deodorants in select markets. For example, Native deodorant, prominently marketed as aluminum-free, targets health-conscious consumers wary of controversial antiperspirant salts. Ingredients like parabens and phthalates, once common as preservatives and fragrance stabilizers, are now highlighted in scientific and public health discussions as endocrine disruptors. These substances can disrupt hormonal balance, even in minimal doses. Despite regulatory agencies deeming their low-concentration use as safe, the perceived risks have led consumers to favor paraben-free and phthalate-free products, diminishing the demand for older formulations. Tom’s of Maine deodorants, for instance, capitalize on this trend, marketing themselves as free from parabens and phthalates to attract health-conscious buyers.

Regulatory restrictions complicate formulations and can slow product launches

In recent years, key markets like the European Union, the United States, and Canada have tightened regulations on cosmetics, including deodorants and antiperspirants. These regulations aim to bolster consumer safety by restricting or banning specific chemicals, mandating safety assessments, and enforcing detailed labeling. While these measures enhance consumer protection, they also complicate formulations, lengthen product development timelines, and elevate compliance costs. Consequently, product innovation has decelerated, and barriers to market entry have intensified, dampening the overall demand for deodorant products. In the European Union, deodorants must adhere to the Cosmetic Products Regulation (EC) 1223/2009, which mandates ingredient safety and allergen disclosure. Manufacturers are tasked with ensuring safety, adhering to strict lists of prohibited or restricted substances, and maintaining a Responsible Person, along with a safety assessment file. A recent amendment (Regulation (EU) 2023/1545) broadened the list of fragrance allergens that need to be disclosed on labels once they surpass certain concentrations (e.g., ≥0.001 % in leave-on products). Given that deodorants fall under the category of leave-on products, Lush's European deodorants, such as the “Tea Tree” variant, utilize natural fragrances in alignment with EU allergen thresholds. In Japan, the Pharmaceuticals and Medical Devices Act (PMD Act) governs deodorants only if they assert functional efficacy, distinguishing between odor suppression and odor masking. Basic deodorants, devoid of therapeutic claims, are classified as cosmetics, necessitating compliance with safety and labeling mandates. Even these basic deodorants face stringent labeling and ingredient restrictions, complicating and delaying product introductions for international brands. Ban Deodorant, a product of Lion Corp. in Japan, underscores its commitment to local standards by emphasizing odor control with safe fragrance blends. Across the globe, deodorant regulations prioritize ingredient safety, allergen disclosure, and labeling, leading to heightened formulation complexities and prolonged compliance timelines. These challenges have collectively decelerated product launches and curtailed market demand by hindering the pace and consistency of new deodorant introductions worldwide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Precision Application Drives Roll-On Gains

Roll-On deodorants are projected to grow at an annual rate of 5.87% through 2031, surpassing Sprays in growth rate, even though Sprays held a 51.87% market share in 2025. Roll-Ons attract consumers who value precise application, reduced waste, and skin-friendly contact, particularly those with sensitive skin or concerns about aerosol propellants. While Sprays remain dominant due to their convenience, quick-drying properties, and the refreshing sensation of a cooling mist, increasing environmental concerns about aerosol packaging are driving a shift toward roll-on and stick formats. Sticks, appreciated for their portability and ease of use, maintain a stable position in the market. Other Product Types, such as creams, gels, and wipes, address niche needs, including whole-body coverage and travel-friendly convenience. Procter and Gamble's 2024 launch of Secret Whole Body, a cream format, highlights innovation in this segment by combining moisturizing benefits with odor control. The growing preference for Roll-Ons reflects a broader consumer trend toward sustainable packaging and targeted application, reshaping product development priorities across the category.

Sprays continue to dominate, primarily due to their association with freshness and the sensory experience of application. However, brands are adapting by reformulating products to address environmental concerns, replacing hydrofluorocarbons with compressed-air propellants. Unilever's Dove and Rexona lines have introduced eco-friendly aerosols that maintain performance while reducing carbon footprints. Sticks benefit from their solid form, which prevents liquid spills and complies with airline carry-on regulations, making them a preferred choice for frequent travelers. The Other Product Types segment is expanding, driven by the rising popularity of whole-body deodorants: creams and gels enable full-body application without the overspray linked to aerosols, while wipes offer single-use convenience for gym-goers and outdoor activities. This diversification of product types underscores the category's evolution from a single-use commodity to a versatile personal-care essential.

By Category: Premium Gains Reflect Ingredient and Fragrance Upgrades

Premium deodorants are expected to grow at a 5.64% CAGR through 2031, closely mirroring the overall market trend. In 2025, mass offerings maintained a dominant 92.45% market share. The growth in premium deodorants is driven by consumers increasingly willing to pay for natural ingredients, luxurious fragrances, and sustainable packaging. In 2024, Unilever's investor communications highlighted the strong performance of its premium personal-care brands, which achieved mid-single-digit growth, surpassing their mass-market counterparts. This growth is largely attributed to consumers opting for premium products during the economic recovery. While mass-market products, recognized for their affordability and extensive distribution, continue to serve the majority of consumers, particularly in emerging markets with high price sensitivity, the narrowing growth gap between mass and premium offerings indicates a significant shift. As disposable incomes increase and health awareness expands, more consumers are prioritizing ingredient transparency and brand values over price considerations.

The premium segment's appeal goes beyond affluent consumers, attracting health-conscious individuals who seek aluminum-free and organic formulations, even at higher price points. Brands such as Native, Schmidt's, and Weleda have effectively positioned natural deodorants as premium products, leveraging certifications like USDA Organic and cruelty-free labels to justify their price premiums. In response, mass-market brands are introducing "masstige" lines, products that combine affordability with premium features, to capture consumers transitioning from entry-level offerings. This competitive environment is narrowing price tiers and compelling brands to differentiate through innovation, whether in fragrance complexity, packaging design, or sustainability credentials. The premium segment's projected 5.64% CAGR highlights its role as the industry's innovation driver, where new formats, ingredients, and marketing strategies are tested before being adopted by mass-market lines.

By Ingredient Source: Clean Beauty Accelerates Natural Formulations

Natural or Organic deodorants are projected to experience an annual growth rate of 6.25% through 2031, outpacing all other ingredient sources. This surge comes even as Conventional or Synthetic formulations commanded a dominant 85.15% market share in 2025. This shift is largely attributed to rising consumer skepticism towards aluminum-based antiperspirants and synthetic preservatives, a sentiment amplified by social media and health advocacy. Notably, while the Cleveland Clinic's 2024 guidance deemed aluminum salts safe, public perception hasn't aligned with this scientific viewpoint, bolstering the appeal of natural alternatives. Furthermore, the United States Food and Drug Administration's antiperspirant monograph endorses aluminum compounds, yet many brands are preemptively reformulating to cater to the growing demand for "clean" ingredients. Meanwhile, stringent European Union cosmetics regulations on synthetic preservatives and fragrances are pushing manufacturers towards natural alternatives, lest they face market exclusion.

Despite the rise of natural alternatives, Conventional or Synthetic formulations continue to dominate, due to their proven effectiveness, cost efficiency, and extended shelf life, qualities that resonate with price-sensitive consumers in emerging markets. While aluminum-based antiperspirants excel in sweat reduction, a benchmark where natural alternatives often fall short, this has limited the latter's appeal among performance-driven consumers. Yet, the gap in efficacy is narrowing as brands innovate: by integrating probiotics, enzymes, and mineral salts, they're bolstering odor control while maintaining their "clean" image. The burgeoning demand for Natural or Organic deodorants highlights their significance as a growth catalyst, especially in North America and Europe, regions marked by heightened health awareness and regulatory clarity. With advancements in natural formulations and increasing consumer education, this segment is set to expand its market share, compelling conventional players to either adapt or risk losing ground.

By Distribution Channel: E-Commerce Rewrites Retail Economics

Forecasts predict that online retail channels will grow at an annual rate of 6.54% through 2031, outpacing supermarkets and hypermarkets, which commanded a 41.69% market share in 2025. The rise of e-commerce mirrors a fundamental shift in consumer shopping habits, a change hastened by pandemic lockdowns and bolstered by the allure of home delivery and a wider product selection than physical stores offer. Brands like Native, Fussy, By Humankind, and OffCourt have capitalized on this trend, sidestepping traditional retail gatekeepers and adopting subscription models for steady revenue. Wild, a leading refillable deodorant brand from the UK, built its clientele entirely through online subscriptions. Acquired by Unilever in April 2025, Wild's online success paved the way for its entry into physical retail. A 2024 analysis by FTI Consulting highlighted the rising customer-acquisition costs for direct-to-consumer brands, leading many to adopt omnichannel strategies that merge online sales with selective wholesale partnerships.

Supermarkets and hypermarkets dominate as the primary distribution channel, offering convenience, immediate product access, and in-store brand comparisons. Yet, their market share is dwindling as consumers gravitate towards online platforms. These platforms provide personalized recommendations, subscription discounts, and access to niche brands absent from physical stores. While specialty stores cater to premium and natural deodorant enthusiasts, they occupy a stable niche but lack the scale to rival mass-market channels. Other distribution avenues, like pharmacies, convenience stores, and direct sales, cater to specific needs, such as travel-sized products and impulse buys. The growth of online retail underscores its structural advantages: reduced overhead costs, advanced data analytics, and precise targeting of micro-segments. As e-commerce infrastructure strengthens in emerging markets, this growth trajectory is set to steepen, altering competitive landscapes and compelling traditional retailers to bolster their digital capabilities or face obsolescence.

Geography Analysis

North America accounted for 32.92% of the market share in 2025, highlighting its established market presence and its role as a hub for innovation in whole-body deodorants and premium formulations. The U.S. remains the largest market, with its value historically estimated at approximately USD 3 billion and annual growth rates exceeding 6% in recent years. Sticks were the dominant format due to their convenience and ease of use. Procter and Gamble's Secret Whole Body, introduced in 2024, leveraged consumer interest in multi-zone applications, with its clinical claims of 72-hour protection appealing to fitness enthusiasts and individuals managing hyperhidrosis. Canada and Mexico contribute to incremental growth, with Mexico's growing middle class driving higher deodorant penetration rates. As the region matures, growth is propelled by premiumization, format innovation, and a shift toward natural ingredients rather than volume expansion, positioning North America as a global trend leader.

Asia-Pacific is projected to grow at an annual rate of 6.39% through 2031, making it the fastest-growing region. Urbanization, rising disposable incomes, and increased awareness of personal hygiene are key drivers of this growth. The shift toward premiumization and the rise of e-commerce are reshaping consumer demand, with individuals opting for brands that convey status and effectiveness. China, the largest market in the region, is driven by urban millennials and Gen Z adopting Western grooming practices. Asia-Pacific's growth reinforces its role as the primary engine of market expansion, while North America's maturity and Europe's focus on sustainability position them as global innovation hubs.

European consumers are increasingly favoring eco-friendly packaging and organic ingredients. This trend is supported by rising personal care consumption, which is driving deodorant demand. According to 2024 data from the Office for National Statistics (UK), consumer spending on personal care in the United Kingdom reached GBP 41.9 billion[3]Office for National Statistics (UK), Consumer spending on personal care in the United Kingdom (UK), www.ons.gov.uk. The United Kingdom's Wild, acquired by Unilever in April 2025, exemplifies this trend, having built a loyal customer base with its refillable aluminum cases and plastic-free refills. Germany, France, and the UK lead European demand, with consumers prioritizing ingredient transparency and sustainable packaging. While the Middle East and Africa are smaller markets, they are expanding as urbanization and Western grooming norms gain traction. The UAE and Saudi Arabia lead regional demand, driven by affluent consumers seeking premium fragrances and long-lasting protection in hot climates. South Africa, Nigeria, Egypt, Morocco, and Turkey represent emerging opportunities, although penetration rates remain below global averages.

Competitive Landscape

The deodorants market exhibits moderate fragmentation, with global incumbents such as Unilever Plc, The Procter and Gamble Company, Natura and Co. Holding SA, The Colgate Palmolive Company, and Beiersdorf AG holding a significant share of the deodorants market, leveraging their shelf space and brand equity. However, they face growing competition from direct-to-consumer brands that capitalize on social media and subscription-based models. Unilever's acquisition of Wild, the UK's leading refillable deodorant brand, in April 2025 highlights the increasing importance of sustainability-focused challengers. This acquisition aligns with a broader trend in the personal care market, where established companies acquire innovative startups to access new customer bases. Brands like Fussy, By Humankind, and OffCourt are disrupting traditional retail by bypassing intermediaries, utilizing influencer marketing, and offering subscription services for consistent revenue. These brands focus on natural ingredients, refillable packaging, and transparent supply chains, appealing to younger, value-conscious consumers.

Innovation in the deodorant market is centered around three key areas: expanding application zones beyond underarms, addressing health concerns with natural and aluminum-free formulations, and introducing refillable packaging to reduce plastic waste. The Procter and Gamble's Secret Whole Body and Unilever's Dove Whole Body Deo lead the way in expanding application zones, using clinical claims and skincare benefits to support premium pricing. Brands such as Native, Schmidt's, and Weleda are driving the adoption of natural formulations, backed by USDA Organic and cruelty-free certifications. Meanwhile, Wild and Salt of the Earth are advancing refillable packaging solutions, offering aluminum cases and cardboard refills to eliminate single-use plastics.

Celebrity endorsements have become a crucial strategy for brand growth: Jason Momoa's partnership with Native, Justin Bieber's Peaches line with Schmidt's, and Megan Rapinoe's collaboration with Secret significantly boost brand visibility through their extensive social media followings. Opportunities remain in underserved demographics, including men's grooming, seniors managing age-related body chemistry changes, and individuals with hyperhidrosis seeking clinical-strength solutions. Emerging markets also offer growth potential, with penetration rates still below 50%. The competitive landscape is transitioning from a focus on shelf-space dominance to a digital-first, values-driven approach, where agility, authenticity, and sustainability are critical for gaining market share.

Deodorants Industry Leaders

-

Unilever Plc

-

Natura and Co. Holding SA

-

Beiersdorf AG

-

The Procter and Gamble Company

-

The Colgate Palmolive Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Unilever collaborated with former NFL player Marshawn Lynch to launch two Dove Men+Care whole body deodorant sprays: Marine + Blue Cypress and Fig + Suede. The deodorants contain glycerin for skin conditioning and zinc for odor control, providing full-body protection against body odor.

- January 2025: Unilever introduced Sure Whole Body Deodorant and Lynx Lower Body Spray. These products are designed for multiple body areas, incorporating Unilever's odor-adapt technology that responds to different types of body odors.

- December 2024: Degree brand launched a new line of whole-body deodorants for men and women. The product features odor-adapt technology that offers 72-hour protection. The products are aluminum-free and dermatologically tested.

- April 2024: NIVEA Men expanded its deodorant portfolio by introducing the Cool Kick Roll-on deodorant in Canada, broadening its product range from women's to men's care through a global partnership with Real Madrid.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the deodorants market as the total yearly value of all antiperspirant and deodorant products, including sprays, roll-ons, sticks, creams, gels, and wipes, sold for personal odor control through retail and professional channels worldwide. The model tracks product movement from brand owner to first point of sale (factory gate plus private-label manufacturing transfers) and is expressed in constant 2025 US dollars.

Scope exclusion: we intentionally omit fragrance-only body mists, talcum powders, and industrial odor neutralizers to avoid inflating demand beyond under-arm and whole-body deodorant use.

Segmentation Overview

-

By Product Type

- Sprays

- Sticks

- Roll-On

- Other Product Types

-

By Category

- Premium

- Mass

-

By Ingredient Source

- Conventional/Synthetic

- Natural/Organic

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online retail Channels

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple interviews and pulse surveys with deodorant formulators, contract packers, dermatologists, and leading e-commerce retailers across North America, Europe, Asia-Pacific, and Latin America allowed us to validate consumption habits, refill adoption rates, and pricing corridors. We then refined model assumptions that desk work alone could not settle.

Desk Research

We began with public datasets, including UN Comtrade shipment codes for HS 330720, Eurostat Prodcom 20422030, and national household budget surveys, which help us size baseline consumption and cross-check trade flows. Trade association white papers from bodies such as Cosmetics Europe and the Personal Care Products Council provided category penetration ratios, while peer-reviewed journals on aluminum-free formulations guided ingredient trend weights. Company 10-Ks and investor decks supplied average selling prices and regional mix. Finally, our analysts tapped paid assets like D&B Hoovers for brand revenue splits and Dow Jones Factiva for recent price hikes. This list is illustrative; many other public and paid sources underpinned data checks.

Market-Sizing & Forecasting

A top-down build applies deodorant spend per capita to the adult population, adjusted for urbanization, sweat-prone climate zones, and gender grooming intensity. Results are reconciled with selective bottom-up roll-ups of supplier volumes and sampled average selling prices to calibrate totals. Key variables include per-capita disposable income, online share of beauty sales, spray format share, aluminum-free penetration, and refill pack uptake. We forecast through multivariate regression that links these drivers to category spend, and scenario analysis captures upside from premiumization. Gaps in bottom-up inputs are bridged with regional channel checks before sign-off.

Data Validation & Update Cycle

Outputs pass a two-step analyst review that flags any variance beyond ±5% versus historical series or fresh primary feedback. We update every twelve months, and interim refreshes trigger after material events like major recalls or regulatory shifts, ensuring clients receive the latest view.

Why Mordor's Deodorants Baseline Stands Reliable

Published figures often diverge because firms pick different product baskets, price bases, and update cadences. We anchor our baseline on a clear scope, live price trackers, and yearly refreshes, so decision-makers know exactly what the number covers.

Key gap drivers include whether creams and wipes are counted, the use of factory-gate versus retail margins, one-time currency conversions, and the frequency with which assumptions are re-tested with experts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 26.65 B (2025) | Mordor Intelligence | - |

| USD 28.52 B (2025) | Global Consultancy A | counts body mists and applies retail mark-ups, inflating value |

| USD 28.90 B (2025) | Trade Journal B | converts local currencies at fixed 2023 rates and updates every two years |

These comparisons show that Mordor's disciplined scoping and annual validation deliver a balanced, transparent baseline clients can replicate and trust.

Key Questions Answered in the Report

How large will global deodorant sales be by 2031?

The deodorants market size is projected to reach USD 34.85 billion by 2031, reflecting a 5.28% CAGR.

Which format is growing quickest?

Roll-on deodorants are advancing at a 5.87% CAGR through 2031, outpacing sprays and sticks.

Why are natural formulations gaining share?

Consumer skepticism of aluminum compounds and stricter EU ingredient rules are driving a 6.25% CAGR for natural and organic options.

How is e-commerce reshaping category growth?

Online sales are forecast to expand at a 6.54% CAGR, fueled by DTC subscriptions and rising global internet penetration.

Page last updated on: