Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

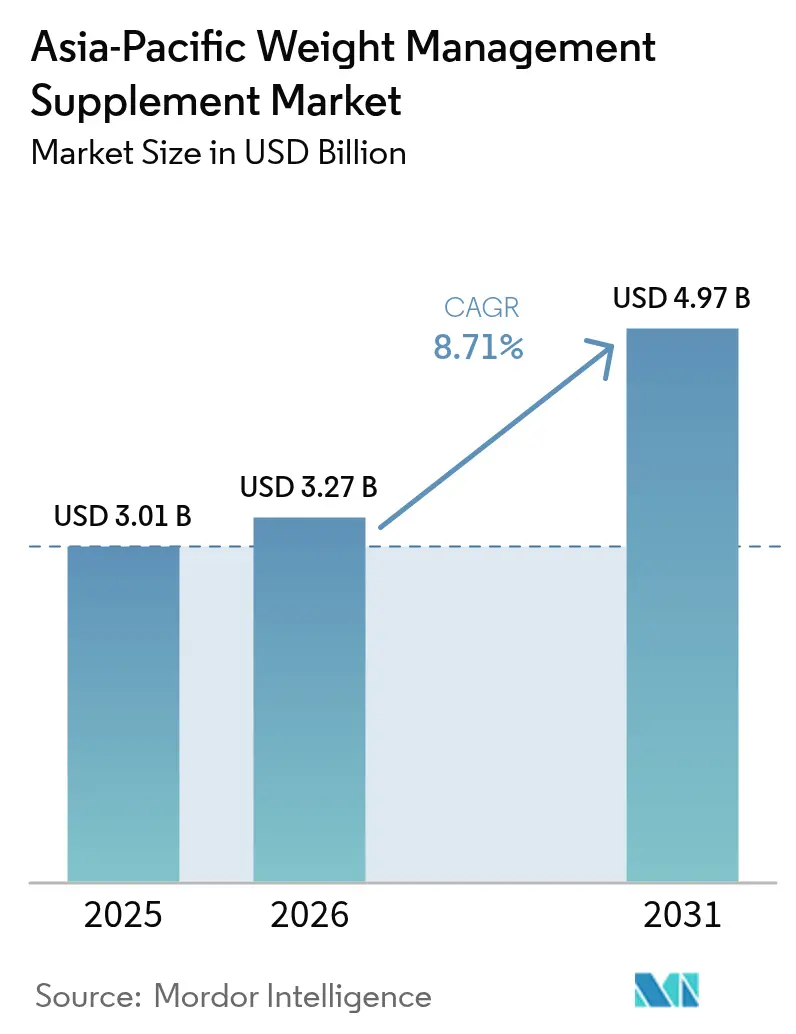

| Base Year Market Size (2025) | USD 3.01 Billion |

| Market Size (2026) | USD 3.27 Billion |

| Market Size (2031) | USD 4.97 Billion |

| Growth Rate (2026 - 2031) | 8.71% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Weight Management Supplement Market Analysis by Mordor Intelligence

Asia-Pacific weight management supplement market size in 2026 is estimated at USD 3.27 billion, growing from 2025 value of USD 3.01 billion with 2031 projections showing USD 4.97 billion, growing at 8.71% CAGR over 2026-2031. This growth is driven by the increasing adoption of urban lifestyles, which often leave individuals with less time for proper meals. Regulatory authorities are working to standardize label claims, making it easier for consumers to trust and choose products. By product type, safer amino-acid-based formulas are gaining popularity and are expected to outperform traditional multivitamins due to their perceived health benefits and safety. In terms of form, gummies are becoming a preferred choice among adults, as they combine convenience with enjoyable flavors, improving compliance. Regarding distribution channels, e-commerce platforms are disrupting traditional store-based consultation models by offering consumers greater accessibility and convenience. The competitive landscape remains highly intense, as fragmented regulations across the region make it challenging for any single company to achieve large-scale, pan-regional operations.

Key Report Takeaways

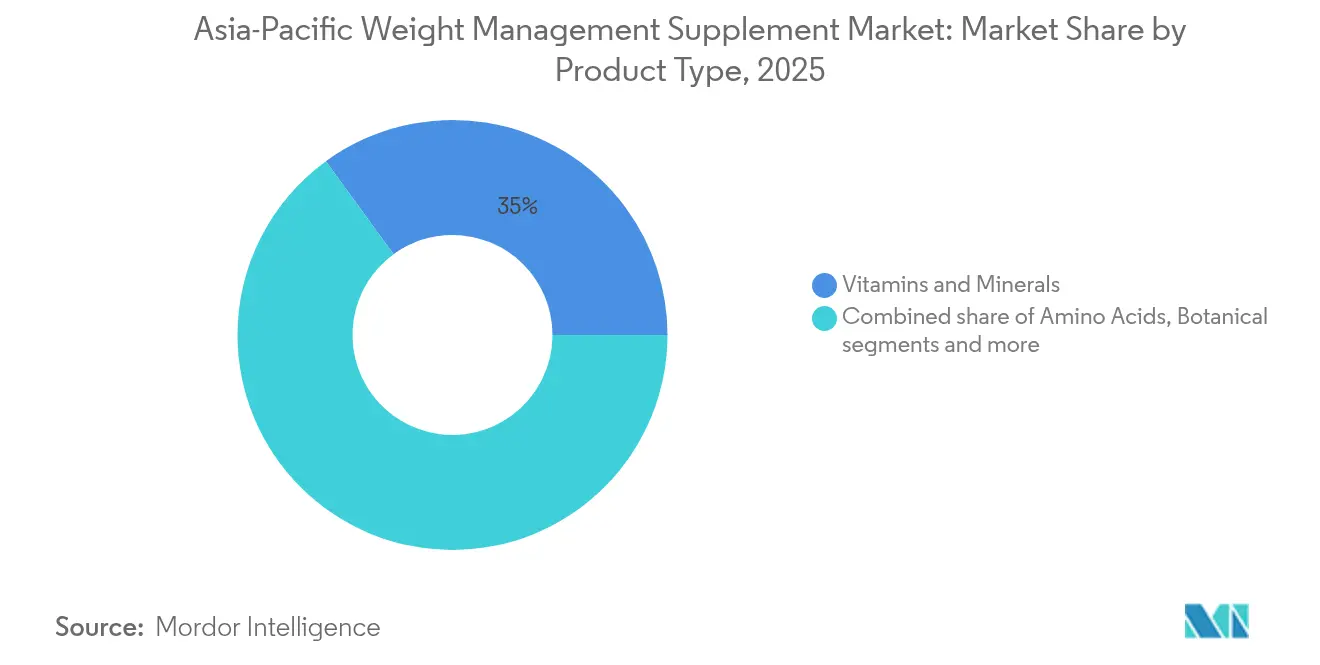

- By product type, vitamins and minerals led the Asia-Pacific weight management supplement market with a 35.02% share in 2025, while amino acids are forecast to grow at a 10.16% CAGR through 2031.

- By form, tablets/capsules captured 41.35% share of the Asia-Pacific weight management supplement market size in 2025, whereas gummies are poised to advance at a 11.62% CAGR through 2031.

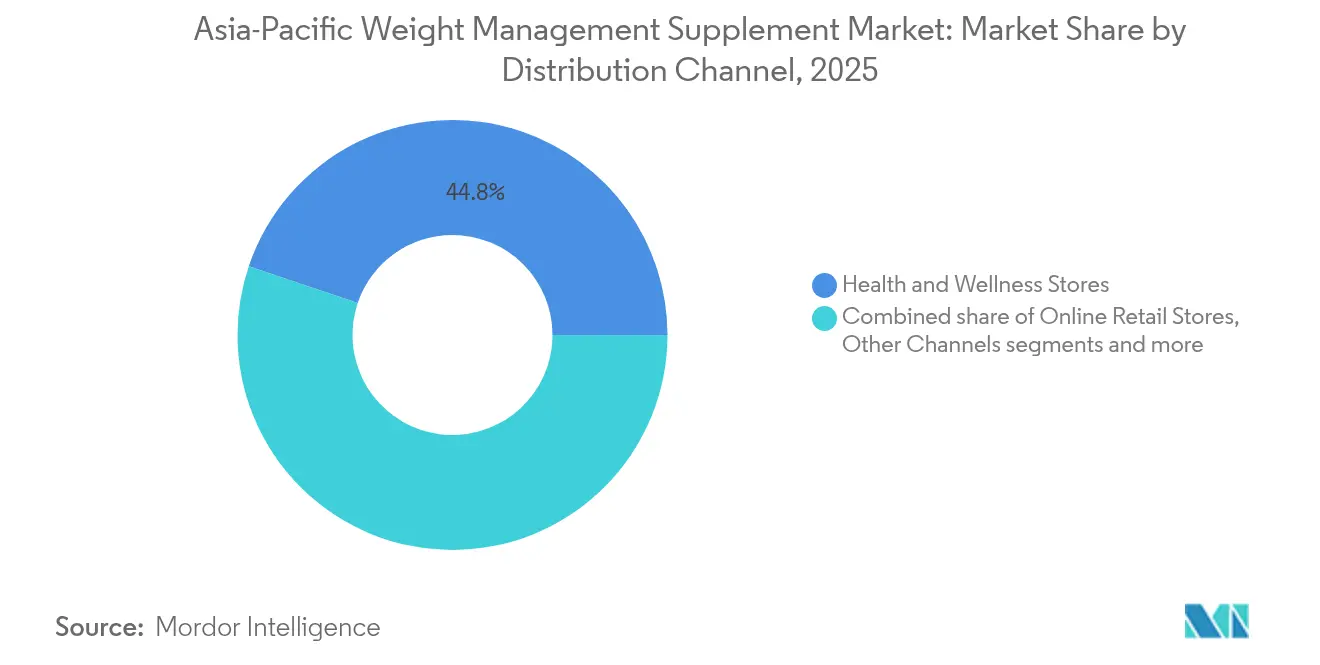

- By distribution channel, health and wellness stores accounted for 44.82% of the Asia-Pacific weight management supplement market in 2025; online retail stores are projected to log an 10.95% CAGR between 2026 and 2031.

- By country, China held 42.31% of the Asia-Pacific weight management supplement market share in 2025, and India is expected to register a 12.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Weight Management Supplement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising obesity rates and lifestyle-related health issues | +2.5% | Highest burden in China, India, Indonesia, and Australia | Long term (≥ 4 years) |

| Growing awareness of health, fitness, and body image | +1.8% | Particularly urban centers across all Asia-Pacific markets | Medium term (2-4 years) |

| Popularity of K-beauty and K-wellness trends | +1.2% | East Asia (South Korea, Japan, China), expanding to Southeast Asia | Medium term (2-4 years) |

| Higher prevalence of meal skipping and irregular eating habits | +1.0% | Urban areas in China, India, Japan, South Korea, Singapore | Short term (≤ 2 years) |

| Expanding influence of celebrity endorsements and fitness influencers | +0.8% | Strongest impact in India, Indonesia, Philippines, Thailand | Short term (≤ 2 years) |

| Rising demand for gluten-free, sugar-free, and low-calorie formulations | +1.0% | Developed Asia-Pacific markets (Japan, Australia, New Zealand, Singapore), spreading to emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising obesity rates and lifestyle-related health issues

The increasing prevalence of obesity and lifestyle-related health issues across the Asia-Pacific region is driving the growing demand for weight management supplements. These supplements are gaining popularity among both younger and older adults as more people face challenges in maintaining a healthy weight. In India, for instance, approximately 23% of men and 24% of women were classified as overweight or obese in 2023, with urban areas showing even higher rates, according to the Business Group on Health[1]Source: Business Group on Health, "Obesity and Overweight in India", businessgrouphealth.org. Consumers are increasingly seeking easy-to-use, non-stigmatizing solutions that can seamlessly integrate into their daily routines. Non-prescription weight management supplements are gaining popularity as they offer a practical and accessible option. Major companies, such as Abbott Laboratories, Herbalife Nutrition Ltd., and Nestlé Health Science, are leading the market by providing products designed for appetite control, metabolic support, and balanced nutrition.

Higher prevalence of meal skipping and irregular eating habits

Skipping meals and irregular eating habits are becoming more common across the Asia-Pacific region, leading to a growing dependence on weight management supplements. In India, a study published in January 2025 by the Journal of Medicinal and Pharmaceutical Chemistry Research revealed that 71.4% of employees regularly skip breakfast, with many doing so daily or every other day[2]Source: Journal of Medicinal and Pharmaceutical Chemistry Research, "Factors Influencing Eating Habit of Skipping Breakfast and Correlation With Nutritional Status, Quality of Sleep, and Level of Stress among Employers at Selected Tertiary Care Hospital", jmpcr.samipubco.com. This trend highlights how busy work schedules and fast-paced urban lifestyles disrupt regular eating patterns. As a result, there is an increasing demand for weight management solutions, such as vitamin supplements that promote satiety, metabolism-boosting capsules, and appetite-control products. These supplements help prevent overeating later in the day and provide consistent energy levels throughout the day. Their portability and ease of use make them a practical choice for individuals with hectic routines, allowing them to gradually integrate them into their daily lives as a convenient and effective solution for managing weight.

Popularity of K-beauty and K-wellness trends

The rising popularity of K-beauty and K-wellness trends is driving increased interest in weight management supplements across the Asia-Pacific region. In India, a January 2025 survey by the Korea Centre revealed that Korean fashion and lifestyle trends influenced 35% of respondents[3]Source: Korea Centre Org, "K-Wave in India: Its Impact on Indian Youth", koreacentre.org . This highlights how Korean pop culture is shaping consumer preferences in beauty and wellness. South Korea’s “beauty-from-within” philosophy, which combines aesthetic goals with health benefits like metabolic support, is particularly appealing to consumers. Innovative and convenient supplement formats such as stick packs, effervescent tablets, widely popularized in Korea, are gaining traction. These formats are not only easy to use but also enjoyable, making them a preferred choice over traditional pills. As these trends and products continue to spread, they are attracting a broader audience to the weight management segment by aligning with consumers’ aspirations for a healthier and more stylish lifestyle.

Growing awareness of health, fitness, and body image

Awareness of health, fitness, and body image is increasing, leading to a growing demand for weight management supplements across the Asia-Pacific region. More people are joining gyms, engaging in home workout programs, and following fitness transformation stories on social media, which keeps the focus on maintaining a healthy lifestyle. In India, the rapid growth of organized fitness centers has further boosted the use of supplements like fat burners and metabolism enhancers. Younger consumers, in particular, associate physical appearance with self-confidence and career success, prompting them to incorporate supplements into their daily routines for consistent, long-term results. This trend is expanding the market beyond individuals managing obesity to include a broader audience of health-conscious and image-focused consumers who view functional nutrition as a key part of their lifestyle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from traditional herbal remedies and home treatments | -0.8% | India (Ayurveda), China (TCM), Indonesia (Jamu), Thailand, Vietnam | Long term (≥ 4 years) |

| Increasing awareness of side effects associated with thermogenic and stimulant-based supplements | -0.6% | Australia, Japan, Singapore with stringent regulatory oversight | Medium term (2-4 years) |

| Growing scrutiny from health authorities on unverified claims | -0.5% | Singapore, Australia, India, Thailand, with spillover to other markets | Short term (≤ 2 years) |

| Inconsistent labelling practices and lack of transparency on ingredient origins | -0.4% | Southeast Asia (Indonesia, Philippines, Vietnam), emerging markets with weaker enforcement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from traditional herbal remedies and home treatments

Traditional herbal remedies and home treatments continue to pose significant competition to branded weight management supplements in the Asia-Pacific region. In India, the reliance on traditional options remains widespread. According to a June 2024 Press Information Bureau report, around 85% of rural households and 86% of urban households had at least one member familiar with medicinal plants, home remedies, or local health traditions[4]Source: Press Information Bureau, "Results of Survey on AYUSH Released", pib.gov.in. This strong cultural connection drives the continued use of Ayurvedic products, such as Triphala in India, lotus-leaf-based blends in China, and Jamu turmeric tonics in Indonesia. These traditional remedies are often viewed as cost-effective, easily accessible, and reliable, making them a preferred choice for many consumers. Their deep-rooted presence in the region's culture and healthcare practices creates a significant challenge for the adoption of modern, branded supplements.

Increasing awareness of side effects linked to thermogenic stimulants

Growing concerns about the side effects of thermogenic stimulants are slowing the growth of certain weight management supplements in the Asia-Pacific market. Regulatory bodies, such as the United States Food and Drug Administration and Australia’s Therapeutic Goods Administration, have issued warnings about unsafe or undisclosed ingredients in some weight-loss products. These warnings have made consumers more cautious, leading many to avoid supplements containing high levels of stimulants. Media reports have highlighted potential health risks, such as rapid heart rate and liver damage, associated with these products. As a result, consumers are increasingly opting for safer alternatives, such as amino-acid blends, plant-based fibers, and non-stimulant metabolism boosters. This shift in consumer preference has forced brands that rely on strong stimulants, such as caffeine or synephrine, to reformulate their products and undergo stricter testing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Safer Amino-Acid Formulas Outpace Legacy Multivitamins

Vitamins and minerals accounted for 35.02% of the Asia-Pacific weight management supplement market in 2025, demonstrating their strong appeal as a trusted and straightforward option for consumers. Multivitamin products are widely used to fill nutrient gaps caused by missed meals, strict diets, or busy schedules. Their adaptability makes them suitable for all age groups, ensuring they remain a regular part of daily health practices. This steady demand has helped the segment maintain its dominant position in the regional market.

Amino-acid-based supplements are projected to grow at a notable 10.16% CAGR from 2026 to 2031, driven by the rising preference for safer, non-stimulant options. Ingredients such as carnitine and conjugated linoleic acid are particularly popular among consumers seeking metabolic support without the side effects associated with high-caffeine products. The growing interest in gym workouts and home fitness routines has increased demand for these supplements, as they support goals such as improving physical performance and enhancing fat metabolism. This trend positions the amino-acid segment to grow faster than traditional categories, reshaping the market landscape in the region.

By Form: Gummies Redefine Adult Compliance Through Flavor And Fun

Tablets/capsules were the leading formats in the Asia-Pacific weight management supplement market in 2025, accounting for 41.35% of the market share. These formats are widely preferred due to their accurate dosing, affordability, and availability across various distribution channels, including pharmacies and online platforms. Their long shelf life and ease of use make them a convenient option for consumers, especially those with busy lifestyles. Additionally, their familiarity and accessibility have solidified their position as a go-to choice for weight management supplements in the region.

Gummies are expected to witness significant growth, with the segment projected to grow at a 11.62% CAGR through 2031. This growth is driven by their appealing taste, ease of consumption, and innovative formulations, such as low-sugar and metabolism-boosting options. Gummies are particularly popular among adults who prefer alternatives to traditional pills, as they offer a more enjoyable and less intimidating experience. With increasing innovation in functional ingredients like fiber and metabolism enhancers, gummies are becoming a preferred choice for consumers seeking both convenience and effectiveness in weight management solutions.

By Distribution Channel: E-Commerce Upsets Store-Based Consultation Models

In 2025, health and wellness stores made up 44.82% of the Asia-Pacific weight management supplement market. These stores are popular because they offer expert advice, enabling customers to compare products, verify their authenticity, and make informed purchasing decisions. Many consumers trust these stores for their curated selection of high-quality and clinically tested products. Their widespread presence in major cities ensures they remain a key choice for regular supplement purchases, especially for those who prefer in-person guidance and a hands-on shopping experience.

Online retail is expected to grow at a CAGR of 10.95% between 2026 and 2031, driven by increasing smartphone usage and the availability of faster delivery options like same-day and next-day services. Younger consumers, who prioritize convenience, are turning to e-commerce platforms influenced by social media and wellness apps. These platforms offer benefits such as transparent customer reviews, easy price comparisons, and subscription services that promote consistent usage. As a result, online retail is becoming one of the fastest-growing and most dynamic distribution channels in the region.

Geography Analysis

China was the largest contributor to the Asia-Pacific weight management supplement market in 2025, accounting for 42.31% of the total revenue. This dominance is driven by a well-organized system for approving functional ingredients and a strong consumer preference for both traditional herbal remedies and modern supplement formats. The rapid growth of digital retail platforms, particularly live commerce, has further enhanced consumer engagement and accelerated purchasing decisions. These factors have solidified China’s position as the leading market in the region.

India is expected to experience the fastest growth in the region, with a projected CAGR of 12.36% from 2026 to 2031. The introduction of stricter regulatory measures has boosted consumer trust in safe and compliant products, while traditional, heritage-based formulations continue to gain popularity among urban households. Increased domestic production and rising investments from multinational companies are reducing reliance on imports and improving product availability. These advancements are positioning India as a key driver of growth in the Asia-Pacific market.

Japan maintains steady growth due to its mature regulatory framework, which emphasizes trust and stability in product formulations. Although the aging population may limit rapid growth in demand, the high credibility of products ensures consistent usage among loyal consumer groups. Meanwhile, markets such as Australia, New Zealand, and Southeast Asia are contributing to regional growth through premium product offerings, strong regulatory enforcement, and a growing health-conscious middle class. However, differences in regulatory standards across these markets influence the pace of adoption and market expansion.

Competitive Landscape

The Asia-Pacific weight management supplement market is highly fragmented due to each country in the region having its own set of regulatory requirements. Companies must follow these specific rules, which makes it challenging to create a single strategy that works across the entire region. This has led to a market filled with a mix of local, regional, and global brands, with no single company able to dominate. As a result, the market remains highly competitive and constantly evolving.

Global brands maintain their presence by leveraging strong research capabilities, established distribution networks, and diverse product offerings. However, they face growing competition from regional players who are more agile and responsive to local consumer preferences. These smaller companies often experiment with innovative product formats, cater to specific taste preferences, and use digital marketing to engage younger audiences. Their ability to quickly adapt and operate direct-to-consumer (D2C) channels allows them to compete effectively with larger multinational firms.

Technology and regulatory compliance have become critical factors for success in this market. Companies that invest in advanced manufacturing processes, precise formulations, and transparent quality standards gain trust from both regulators and consumers. Markets like Singapore and Australia demand high-quality certifications, which often push non-compliant brands out of major online platforms. In this competitive environment, companies that prioritize agility, innovation, and strict adherence to safety and quality standards are more likely to succeed. This dynamic ensures that the market will remain fragmented throughout the forecast period.

Asia-Pacific Weight Management Supplement Industry Leaders

-

Abbott Laboratories

-

Herbalife Nutrition Ltd.

-

Nestlé SA

-

Amway Corp

-

Glanbia PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Eli Lilly planned to introduce its experimental oral weight-loss drug, orforglipron, in the Indian market. The drug belonged to a new class of GLP-1 medications designed to suppress appetite, targeting the same biological pathway as Eli Lilly's highly successful tirzepatide.

- July 2025: Herbalife Ltd. announced the launch of MultiBurn. This new dietary supplement was formulated with a blend of botanical extracts designed to promote weight loss and enhance metabolic health.

- March 2025: Eli Lilly introduced Mounjaro in India as a weight loss solution. This development was expected to provide significant benefits to millions of individuals dealing with obesity and diabetes, offering a new option for managing these chronic conditions effectively.

- August 2024: Novo Nordisk announced the launch of its Wegovy weight-loss medication in Australia, marking its availability in a total of 12 countries. The company highlighted that Wegovy has gained significant popularity due to its effectiveness in aiding weight management.

Asia-Pacific Weight Management Supplement Market Report Scope

By product type, the Asia-Pacific weight management supplement market is segmented into vitamins and minerals, botanicals, amino acids, and others. By form, the market is segmented into powders, tablets/capsules, gummies, and others. By distribution channel, the market is segmented into supermarkets/hypermarkets, health and wellness stores, online retail stores, and others. By country, the market is segmented into China, India, Japan, South Korea, Australia, Indonesia, Thailand, Vietnam, Philippines, Malaysia, Singapore, New Zealand and Rest of Asia-Pacific.

By Product Type

| Vitamins and Minerals |

| Botanicals |

| Amino Acids |

| Others |

By Form

| Powders |

| Tablets/Capsules |

| Gummies |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Health and Wellness Stores |

| Online Retail Stores |

| Other Channels |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Indonesia |

| Thailand |

| Vietnam |

| Philippines |

| Malaysia |

| Singapore |

| New Zealand |

| Rest of Asia-Pacific |

| By Product Type | Vitamins and Minerals |

| Botanicals | |

| Amino Acids | |

| Others | |

| By Form | Powders |

| Tablets/Capsules | |

| Gummies | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Health and Wellness Stores | |

| Online Retail Stores | |

| Other Channels | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Malaysia | |

| Singapore | |

| New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the 2026 value of the Asia-Pacific weight management supplement market?

It stands at USD 3.27 billion and is projected to grow at an 8.71% CAGR to 2031.

Which country currently generates the largest revenue?

China holds 42.31% of 2025 sales thanks to Blue Hat-approved fat-reduction functions.

Which product form is growing fastest?

Gummies lead with a 11.62% CAGR forecast through 2031 due to adult adoption of low-sugar, flavor-forward formats.

Why are amino-acid supplements surging?

Regulatory crackdowns on stimulants push consumers toward non-thermogenic options like CLA and carnitine, yielding a 10.16% CAGR outlook.

Page last updated on: