Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

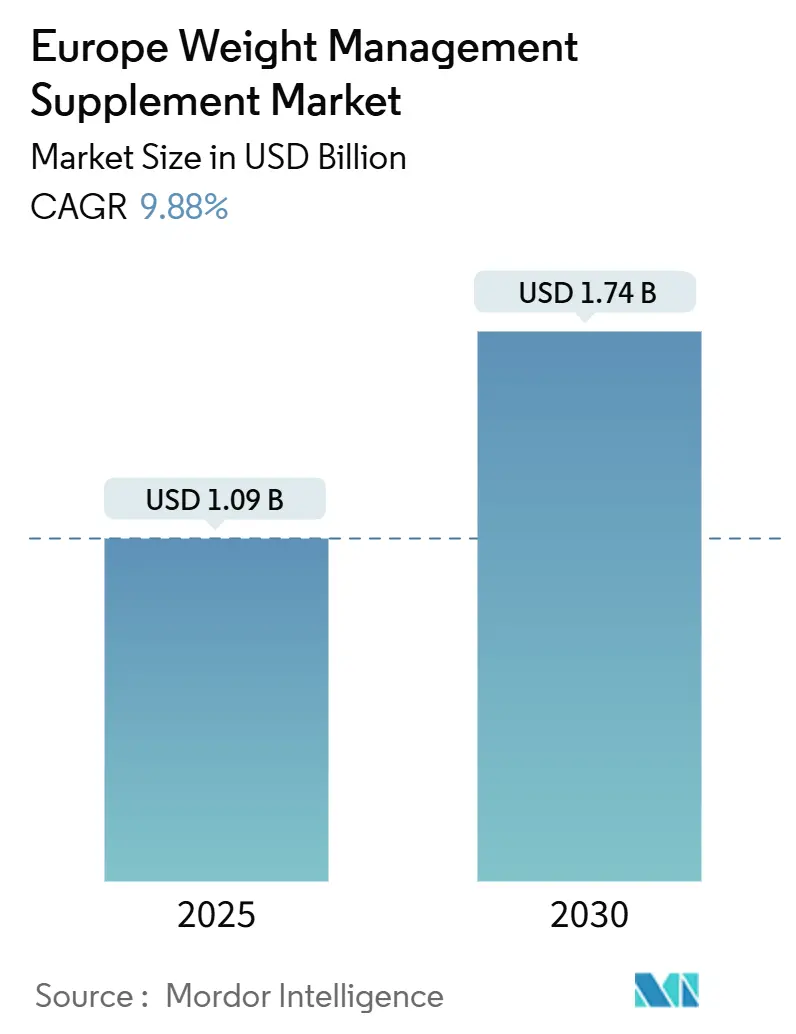

| Market Size (2025) | USD 1.09 Billion |

| Market Size (2030) | USD 1.74 Billion |

| Growth Rate (2025 - 2030) | 9.88% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Weight Management Supplement Market Analysis by Mordor Intelligence

The Europe weight management supplement market size is valued at USD 1,091.32 million in 2025 and is projected to reach USD 1,748.38 million by 2030, registering a 9.88% CAGR over the forecast period. The market's growth is primarily driven by increasing obesity rates, the rapid adoption of GLP-1 medications that highlight emerging nutritional gaps, and a rising consumer preference for bioactive compounds. These compounds play a crucial role in influencing satiety, enhancing thermogenesis, and maintaining gut microbiome balance. The shift in consumer behavior from simple calorie restriction to more comprehensive, multifunctional approaches has created opportunities for premium supplements. These advanced supplements often integrate muscle-preserving amino acids, botanicals that support hormonal health, and targeted micronutrients to address specific needs. Additionally, the rise of digital retail platforms and subscription-based services is reducing distribution costs, enabling emerging brands to scale their operations across borders while maintaining profitability. At the same time, stricter regulatory oversight is reshaping the competitive landscape. Companies that emphasize in-house testing, transparent sourcing practices, and clinically validated products are gaining a competitive edge, driving the market towards a quality-focused consolidation.

Key Report Takeaways

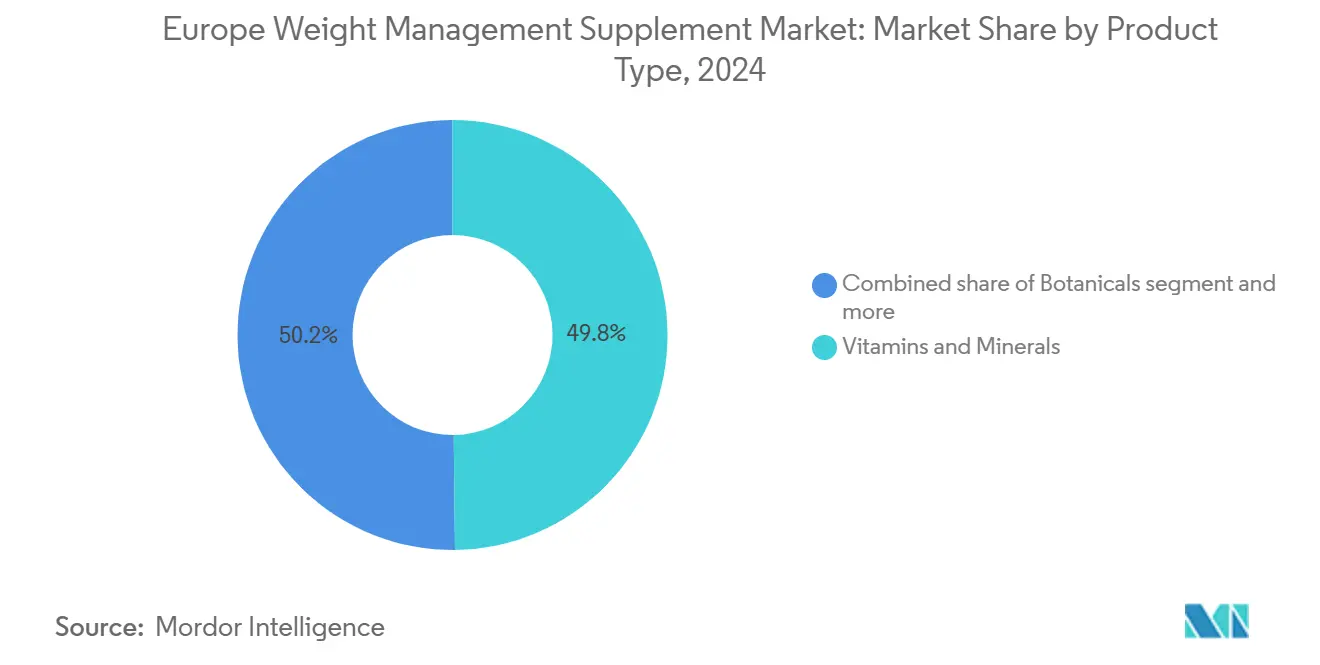

- By product type, vitamins and minerals led with 49.81% of the European weight management supplement market share in 2024; botanicals are tracking a 10.24% CAGR to 2030.

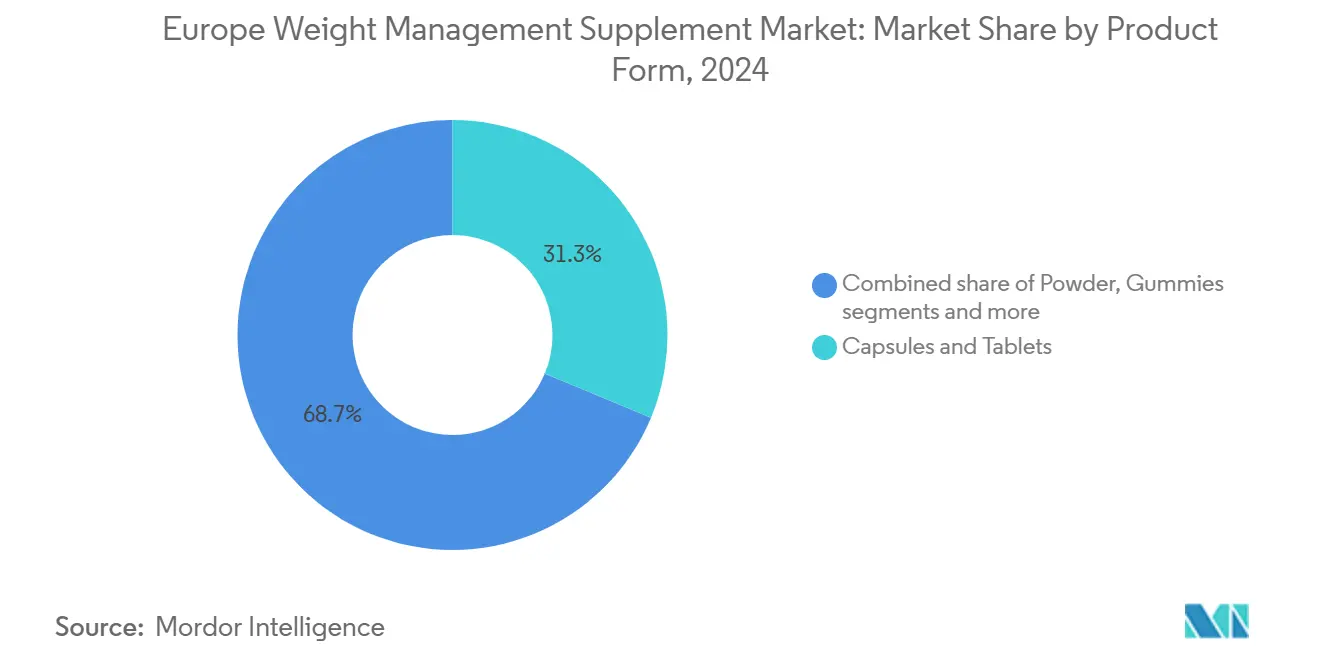

- By product form, capsules and tablets accounted for 31.28% of regional revenue in 2024, while powders are forecast to grow at a 10.24% CAGR through 2030.

- By distribution channel, supermarkets and hypermarkets captured 41.26% of sales in 2024, whereas online retail stores are advancing at a 10.35% CAGR to 2030.

- By geography, Germany contributed 23.41% of 2024 revenue; the United Kingdom is poised for the fastest expansion at a 10.17% CAGR between 2025 and 2030.

Europe Weight Management Supplement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising obesity rates and associated health concerns across Europe | +2.1% | United Kingdom, Germany, Poland | Medium term (2-4 years) |

| Aging population growth, with demand for supplements | +1.8% | Western Europe (Germany, France, Italy), Nordic countries | Long term (≥ 4 years) |

| Shift toward natural, organic, and plant-based supplements for clean-label preferences | +1.5% | United Kingdom, Germany, Netherlands, Sweden | Short term (≤ 2 years) |

| Rising demand for convenient meal replacements offering controlled nutrition | +1.3% | United Kingdom, Germany, France, urban centers across Europe | Medium term (2-4 years) |

| Surge in physical activity levels, boosting supplement demand | +1.0% | Western and Northern Europe, spill-over to Southern Europe | Short term (≤ 2 years) |

| Growth of DNA-based personalised nutrition platforms | +0.9% | Germany, United Kingdom, France, early adopters in Benelux | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising obesity rates and associated health concerns across Europe

In 2024, 53% of adults in the EU are overweight, with men and older age groups showing higher rates, as reported by the European Food Information Council (EUFIC)[1]Source: European Food Information Council (EUFIC), "Europe's obesity statistics", eufic.org. Furthermore, the OECD (Organisation for Economic Co-operation and Development) reports that 75% of men in Romania are obese in 2024[2]Source: OECD (Organisation for Economic Co-operation and Development), "OECD non-medical determinants of health" oecd.org. Obesity prevalence varies across the region. For example, Eastern European countries like Poland are experiencing rising rates due to the rapid adoption of Western dietary habits, while Southern European nations are dealing with significant childhood obesity rates. The consequences of this trend are severe: beyond appearance, obesity is associated with numerous comorbidities. Conditions such as type 2 diabetes, cardiovascular diseases, and non-alcoholic fatty liver disease are overburdening public health systems and increasing payer interest in preventive nutrition solutions. Weight management supplements are becoming the preferred initial intervention, particularly for individuals with a BMI between 25-30 who do not yet qualify for prescription medications. The post-pandemic increase in metabolic syndrome cases has further driven demand, as weight gains from lockdown-induced sedentary lifestyles persist. Regulatory bodies like the European Commission are considering taxes on ultra-processed foods, which could shift consumer spending toward functional supplements marketed as healthier options.

Aging population growth, with demand for supplements

The demand for dietary supplements is increasing as Europe's population continues to age. In 2024, Eurostat reported that 21.6% of Europeans are aged 65 or older[3]Source: Eurostat, "Ageing Europe - statistics on population developments", ec.europa.eu. Sarcopenia, the age-related decline in muscle mass and function, affects 10-16% of older Europeans and is further aggravated by weight loss strategies that emphasize calorie reduction over adequate protein intake. This demographic trend is fueling the need for supplements that combine weight management components with muscle-preserving ingredients such as leucine, HMB, and creatine. Germany, which has the largest aging population in the region, has driven the expansion of pharmacy channels offering geriatric-specific formulations. These products address polypharmacy concerns by consolidating multiple nutritional interventions into single-dose sachets. EFSA data indicates that approximately 40% of Europeans are vitamin D deficient, with rates exceeding 60% among institutionalized elderly individuals. This underscores the demand for fortified weight management products that balance caloric control with essential micronutrient replenishment. The overlap of aging and obesity, referred to as "sarcopenic obesity," represents a high-value market segment. Premium formulations targeting this dual challenge can achieve profit margins exceeding 40%.

Shift toward natural, organic, and plant-based supplements for clean-label preferences

Consumer demand for botanicals and plant-derived actives is driving changes in formulation strategies. Ingredients such as green tea extract, garcinia cambogia, and conjugated linoleic acid from safflower oil are replacing synthetic compounds. This trend is particularly prominent in Northern Europe, where organic certification and non-GMO verification are crucial for achieving premium market positioning. However, regulatory challenges are increasing as safety concerns arise. In 2024, ANSES issued warnings about ashwagandha, citing its link to hepatotoxicity and reporting cases of elevated liver enzymes in consumers after prolonged use. Similarly, berberine, promoted as "nature's Ozempic" on TikTok, has drawn regulatory attention due to its potential interactions with prescription medications and gastrointestinal side effects at commonly recommended doses. Manufacturers are addressing these issues by investing in proprietary extraction technologies that improve bioavailability and reduce the required dosage, thereby alleviating safety concerns. The partnership between DSM-Firmenich and Indena exemplifies a strategic approach, combining botanicals with postbiotics to offer "clinically validated" plant-based solutions. This strategy not only aligns with clean-label preferences but also mitigates regulatory risks through diversified ingredient portfolios.

Rising demand for convenient meal replacements offering controlled nutrition

Meal replacement products have shifted from niche diet aids to widely accepted nutrition solutions. These products attract busy professionals seeking precise macronutrient ratios without the effort of meal preparation. They are also popular among individuals using them as calorie-controlled options within structured weight loss programs. The category's growth is further driven by the rise of GLP-1 medications. Patients experiencing appetite suppression and rapid weight loss increasingly rely on fortified meal replacements to meet essential protein and micronutrient requirements. Regulatory frameworks for meal replacements differ significantly across member states. Some countries categorize them as "foods for special medical purposes," requiring pre-market notification, while others classify them as conventional foods subject only to general labeling regulations. This regulatory disparity not only adds compliance challenges but also creates opportunities for brands capable of navigating these multi-jurisdictional complexities to achieve pan-European expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent European Union regulations on permitted ingredients and novel foods | -1.4% | European Union, with spillover to UK and Switzerland | Medium term (2-4 years) |

| High product cost versus conventional foods | -1.1% | Southern and Eastern Europe (Spain, Italy, Poland, Greece) | Short term (≤ 2 years) |

| Advertising restrictions limiting claims on efficacy to avoid misleading consumers | -0.8% | European Union, particularly Germany, France, Netherlands | Long term (≥ 4 years) |

| Consumer safety risks from undeclared pharmaceuticals | -0.6% | Cross-border e-commerce channels, Eastern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent European Union regulations on permitted ingredients and novel foods

In August 2024, the European Food Safety Authority (EFSA) approved glucosyl hesperidin, a citrus-derived flavonoid, following a three-year review process. This example highlights the regulatory hurdles European manufacturers face, particularly when compared to competitors in less-regulated markets. EFSA's novel foods framework mandates pre-market authorization for ingredients without a significant consumption history, often resulting in extended approval timelines. Meanwhile, ashwagandha, commonly used in weight management products, is under increased scrutiny after ANSES issued hepatotoxicity warnings in 2024. Several European countries are now considering restrictions that could disrupt the single market. Additionally, the Rapid Alert System for Food and Feed reported multiple cases in 2024 of undeclared sibutramine and phenolphthalein in weight-loss supplements. Post-Brexit regulatory divergence has further complicated matters, as the UK is independently developing its novel foods regime. This shift requires brands seeking pan-European distribution to submit applications in both regulatory systems.

High product cost versus conventional foods

In Southern and Eastern Europe, where disposable incomes remain significantly lower than Western European averages, premium weight management supplements are priced at 2-3 times the cost of conventional foods on a per-calorie basis. This substantial price disparity creates affordability challenges for consumers in these regions. However, Poland has witnessed rapid income growth, which has expanded the potential customer base for such products. Despite this growth, a considerable share of sales occurs through online retail channels. This trend highlights consumer efforts to reduce expenses by engaging in cross-border purchasing and bulk buying, which, in turn, compresses profit margins for domestic distributors. The cost disparity in the market is further widening due to inflationary pressures. In 2024, the prices of botanical extracts are expected to increase by 10-15%, driven by climate-related harvest shortfalls in India and China. These two countries serve as the primary sourcing regions for key ingredients such as ashwagandha, garcinia, and green tea, making them critical to the supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Botanicals Outpace Vitamins Despite Safety Scrutiny

In 2024, vitamins and minerals accounted for 49.81% of the market share, highlighting their critical role in energy-restricted diets where maintaining micronutrient adequacy is challenging. At the same time, botanicals are experiencing significant growth, with a 10.24% CAGR projected through 2030. This growth is fueled by rising consumer interest in bioactive compounds that regulate satiety hormones and thermogenesis. Vitamin D formulations, particularly vegan D3 derived from lichen and algae, are gaining popularity. This trend aligns with EFSA data showing that 40% of Europeans have inadequate vitamin D levels, with deficiency rates exceeding 60% among institutionalized elderly populations. B-vitamin complexes, now incorporating methylated forms like methylcobalamin and methylfolate, are marketed for their improved bioavailability. These products specifically cater to consumers with MTHFR gene variants, which impair folate metabolism. Furthermore, iron supplements have transitioned from ferrous sulfate to ferrous bisglycinate chelate in premium formulations. This shift addresses a major adherence issue for menstruating women by reducing gastrointestinal side effects.

Although botanicals hold a smaller market share, they are driving innovation with ingredients such as ashwagandha, berberine, and green tea extract. Amino acids, the third major product category, are being integrated into hybrid formulations that combine weight management ingredients with muscle-preserving compounds like leucine and HMB. These formulations aim to address sarcopenic obesity in aging populations. The "Others" category is an emerging segment featuring ingredients like postbiotics and prebiotic fibers, which influence gut microbiome composition. Notably, DSM-Firmenich and Indena have partnered to develop and commercialize botanical-postbiotic combinations targeting metabolic endotoxemia.

By Product Form: Powders Gain Ground Through Customization and Bioavailability

In 2024, capsules and tablets accounted for 31.28% of the market share, driven by their portability, precise dosing, and consumer familiarity. However, powders are projected to grow at a 10.24% CAGR through 2030, as brands emphasize customizable serving sizes and rapid dissolution to improve bioavailability. Protein powders, once limited to sports nutrition, are now being reformulated with thermogenic ingredients like green tea extract and conjugated linoleic acid, enabling them to target both weight management and muscle preservation markets. Similarly, collagen peptide powders, initially promoted for benefits such as skin elasticity and joint health, are being repositioned. By focusing on their satiety benefits and support for lean mass during caloric restriction, they are increasingly marketed as weight management solutions.

Gummies are the fastest-growing format in the "Others" category, appealing to younger demographics with their palatability and Instagram-friendly aesthetics. To meet the rising European demand for functional confectionery, Sirio introduced XtraGummies in June 2024. However, gummy formulations face challenges, as heat-sensitive actives like probiotics and certain vitamins degrade during manufacturing, limiting the range of bioactives that can be included. Capsules and tablets continue to hold an edge in clinical credibility, as healthcare professionals prefer them for their standardized dosing and absence of added sugars. Emerging formats like sublingual strips and orally disintegrating tablets offer faster onset of action, but their premium pricing restricts adoption to early-adopter segments.

By Distribution Channel: Online Retail Disrupts Traditional Pharmacy Dominance

Supermarkets and hypermarkets accounted for 41.26% of the distribution landscape in 2024, leveraging high foot traffic and the appeal of impulse purchases. At the same time, online retail stores are growing at a 10.35% CAGR through 2030. This growth is primarily driven by direct-to-consumer brands bypassing traditional retail models and adopting subscription strategies to enhance customer lifetime value. Poland leads Europe in online retail share, fueled by cross-border e-commerce. This trend enables Polish consumers to access products not yet approved in their domestic markets and benefit from price differences across EU member states. Highlighting the shift in retail strategies, Myprotein's partnership with Holland and Barrett in September 2024 exemplifies the omnichannel approach. Digital-first brands are establishing physical stores to cater to consumers who prefer evaluating products in person, while traditional retailers are developing proprietary e-commerce platforms to protect their market share.

Health and wellness stores, the second-largest distribution channel, balance their offerings by providing specialized products and knowledgeable staff, which justify their premium pricing. However, they face margin challenges as online retailers use AI-powered recommendation systems to replicate personalized in-store guidance on a larger scale. Germany's pharmacy channel, traditionally dominant due to consumer trust in Apotheke-certified products, is losing market share as younger consumers increasingly prioritize convenience and affordability over professional endorsements. Subscription models, pioneered by brands like Huel and YFood, are transforming replenishment economics. These models reduce customer acquisition costs and enable predictive inventory management. However, high churn rates remain a challenge, as consumers often try multiple brands before settling on their preferred options.

Geography Analysis

Germany captured 23.41% of the regional revenue 2024, highlighting the robustness of its pharmacy distribution network. Apotheke certification serves as a hallmark of quality, enabling premium pricing. Germany's strict enforcement of health claims under the EU's Nutrition and Health Claims Regulation (EC) No 1924/2006 has created a compliance-intensive environment. This regulatory framework benefits established players with expertise in navigating these requirements, while smaller brands without resources for pre-approval dossiers face challenges. Rossmann, the country's second-largest drugstore chain, expanded its private-label supplement range in 2024, introducing weight management products with clinically validated ingredients such as glucomannan and chromium picolinate, thereby intensifying competition with branded manufacturers.

The United Kingdom, with a projected CAGR of 10.17% through 2030, emerges as the region's fastest-growing market. This growth is driven by post-Brexit regulatory changes that have accelerated novel ingredient approvals and strong consumer interest in functional foods. In 2024, Boots expanded its product portfolio to include DNA-based personalized nutrition kits, positioning pharmacy chains as comprehensive wellness hubs that integrate testing, consultation, and product delivery. However, trust issues have surfaced due to high-profile cases of undeclared pharmaceuticals in weight-loss supplements purchased online, prompting increased demand for mandatory third-party testing and batch certifications.

Italy's supplement market reflects significant spending concentrated in pharmacy channels, where professional recommendations support premium pricing. Conversely, mass-market retailers struggle to convert casual browsers into buyers. Spain's market is marked by price sensitivity, limiting the adoption of premium botanicals and personalized formulations, with consumers favoring affordable multivitamins and generic fiber supplements. Russia's market remains opaque due to geopolitical sanctions and limited data transparency, though anecdotal evidence suggests rising demand for domestically produced supplements as import channels narrow. Smaller but strategically important markets include Sweden, Belgium, Poland, and the Netherlands. Sweden's health-conscious population drives high per-capita supplement consumption, while Poland's growing income levels expand the market for premium products. Belgium's trilingual market requires localized labeling and marketing strategies, increasing complexity for market entry. Meanwhile, the Netherlands' liberal regulatory environment has attracted cross-border e-commerce hubs, facilitating pan-European distribution.

Competitive Landscape

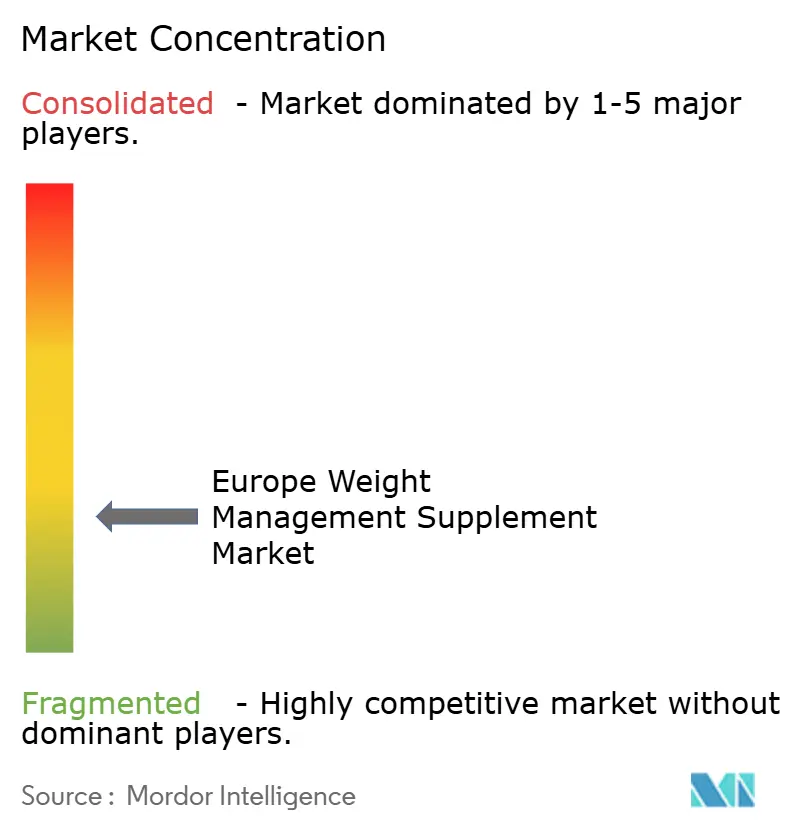

The European weight loss management market is fragmented due to the presence of numerous domestic and multinational players. Companies are adapting to consumer preferences for innovative weight loss products, such as fat burners with unique flavors and packaging. Major multinationals, including Nestlé Health Science, Glanbia, and Amway, compete with digital-native brands like Huel and YFood, as well as DNA-platform specialists such as Prevess. Consolidation is accelerating as established players acquire challenger brands to leverage subscription bases and technological intellectual property. Meanwhile, start-ups are licensing manufacturing to scale quickly without significant capital expenditure. Research and development pipelines are increasingly combining pharmaceutical precision with lifestyle branding. This trend, exemplified by Valbiotis’s ongoing TOTUM programs, emphasizes randomized trials that validate product claims and earn the trust of medical professionals.

Key players such as General Nutrition Centers Inc., Amway Corp., Glanbia PLC, Evlution Nutrition LLC, and Herbalife International are leading the regional market. Companies are strategically focusing on mergers, expansions, acquisitions, and partnerships, alongside new product developments, to enhance their brand presence. A notable segmentation is emerging: one group focuses on GLP-1 companionship, offering protein-rich shakes and micronutrient packs to counteract drug-related muscle loss and nausea. In contrast, another group targets lifestyle consumers with plant-based, low-sugar offerings, emphasizing "metabolic wellness" over traditional weight loss. While social media storytelling remains a key acquisition strategy, rising paid-ad costs are prompting companies to adopt loyalty programs and community forums to improve customer retention.

Companies are increasingly launching innovative products that incorporate naturally derived ingredients to differentiate themselves in a competitive market. Given the market's rapid evolution, product innovation has become the dominant strategy, enabling firms to respond to changing consumer demands. Regulatory expertise has become a critical competitive advantage. Companies with in-house toxicology labs can expedite EFSA dossier submissions and reduce recall risks. In contrast, those relying on third-party contractors face greater exposure to RASFF alerts for contaminants or undisclosed active pharmaceutical ingredients (APIs), which can quickly erode brand equity. In summary, the European weight management supplement industry is shifting from a fragmented landscape of niche players to a more concentrated structure. Science-driven, vertically integrated firms are setting the pace, while agile innovators introduce fresh formats and carve out specialized market positions.

Europe Weight Management Supplement Industry Leaders

-

General Nutrition Centers

-

Herbalife Nutrition

-

Evlution Nutrition LLC

-

Glanbia Plc

-

Amway Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Leanova UK has launched its evidence-based weight management product in the UK market. Leanova has introduced a nationwide plant-based weight loss supplement in the UK, designed to promote sustainable wellness by supporting appetite control and metabolism, utilizing scientifically validated vegan ingredients.

- October 2024: Myprotein has entered into a strategic partnership with Holland and Barrett to establish branded shop-in-shop sections in more than 200 UK locations. This initiative enables the digital-first brand to reach offline consumers while providing Holland and Barrett with exclusive access to Myprotein's proprietary formulations.

- June 2024: Nestlé Health Science has introduced appetite-suppressant shots in Europe, catering to consumers desiring GLP-1-like benefits without the need for prescriptions. By blending fiber, protein, and botanical extracts to influence satiety hormones, Nestlé aims to tap into the demand from those who either can't or choose not to pursue pharmaceutical weight-loss solutions.

- June 2023: Rapid Nutrition PLC announced the release of its new look and brand identity for the SystemLS weight loss products. The company also claims that it unveiled the new brand identity for the flagship SystemLS Weight Loss Brand as the product continues international expansion.

Europe Weight Management Supplement Market Report Scope

By Product Type

| Vitamins and Minerals |

| Botanicals |

| Amino Acids |

| Others |

Product Form

| Powder |

| Capsules and Tablets |

| Gummies |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Health and Wellness Stores |

| Online Retail Stores |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Sweden |

| Belgium |

| Poland |

| Netherlands |

| Rest of Europe |

| By Product Type | Vitamins and Minerals |

| Botanicals | |

| Amino Acids | |

| Others | |

| Product Form | Powder |

| Capsules and Tablets | |

| Gummies | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Health and Wellness Stores | |

| Online Retail Stores | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe weight management supplement market in 2025?

It is valued at USD 1,091.32 million and is forecast to reach USD 1,748.38 million by 2030.

Which product type is growing fastest across Europe?

Botanicals are expanding at a 10.24% CAGR, outpacing vitamins, minerals, and amino acids through 2030.

What sales channel is gaining the most share?

Online retail stores show the highest momentum with a projected 10.35% CAGR, driven by subscriptions and cross-border e-commerce.

Which country leads regional revenue?

Germany accounts for 23.41% of 2024 sales, supported by a strong pharmacy network and high spending among aging consumers.

Page last updated on: