Warm Air Heaters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

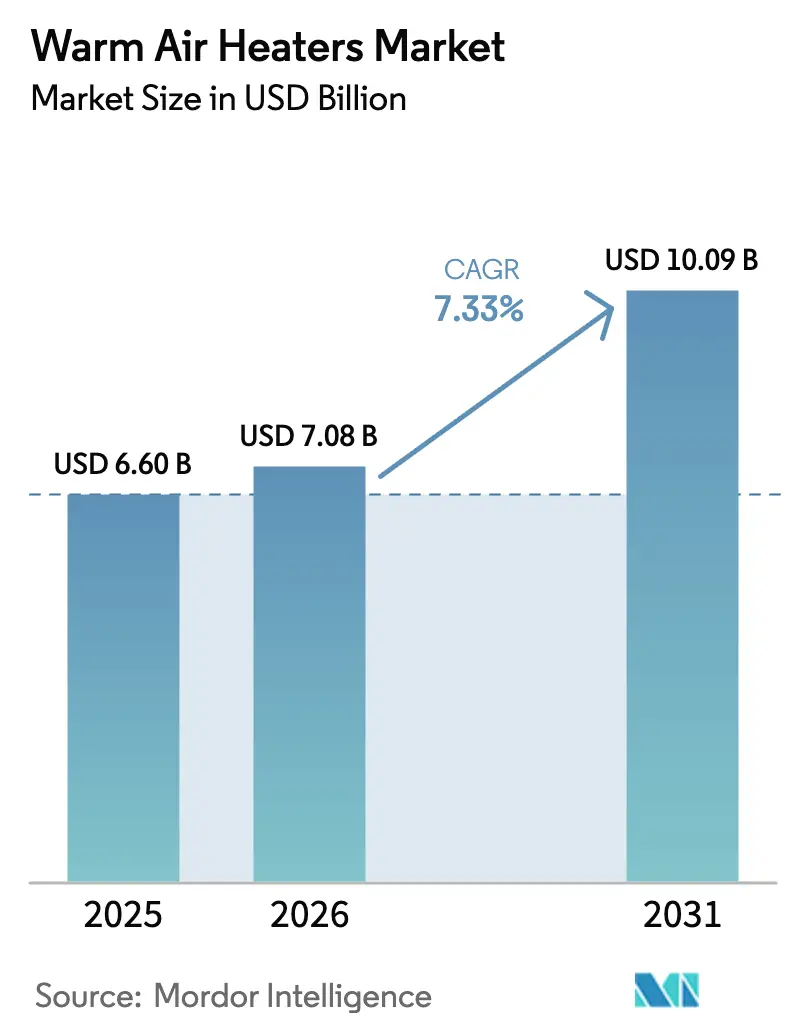

| Market Size (2026) | USD 7.08 Billion |

| Market Size (2031) | USD 10.09 Billion |

| Growth Rate (2026 - 2031) | 7.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Warm Air Heaters Market Analysis by Mordor Intelligence

The Warm Air Heaters Market size was valued at USD 6.6 billion in 2025 and estimated to grow from USD 7.08 billion in 2026 to reach USD 10.09 billion by 2031, at a CAGR of 7.33% during the forecast period (2026-2031). This expansion reflects the technology’s vital role in ensuring operational continuity across residential, commercial, industrial, and transportation settings. Heightened building-energy codes, rapid cold-chain logistics build-out, and industrial decarbonization mandates are amplifying replacement demand, while renewable-powered models carve new opportunities. Competitive focus has shifted toward smart controls, Internet-of-Things-enabled efficiency upgrades, and hybrid fuel flexibility that derisks customers from fossil-fuel price shocks. Despite intensifying heat-pump competition in small buildings, the warm air heaters market continues to prosper because it delivers rapid temperature ramp-up, low installation complexity, and dependable performance in high-load industrial processes.

Key Report Takeaways

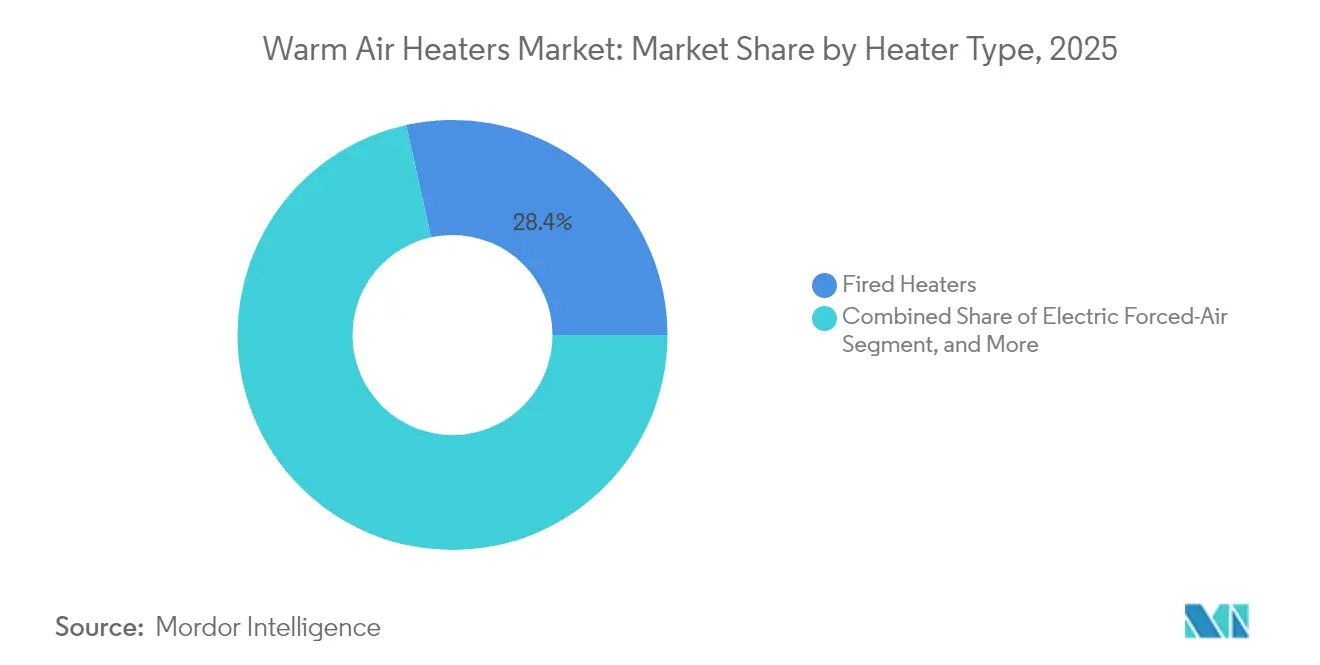

- By technology, fired heaters led with 28.45% of warm air heaters market share in 2025, whereas electric forced-air heaters are projected to grow at a 8.72% CAGR through 2031.

- By end user, industrial facilities accounted for 44.70% revenue share in 2025, while transportation applications record the fastest 8.05% CAGR through 2031.

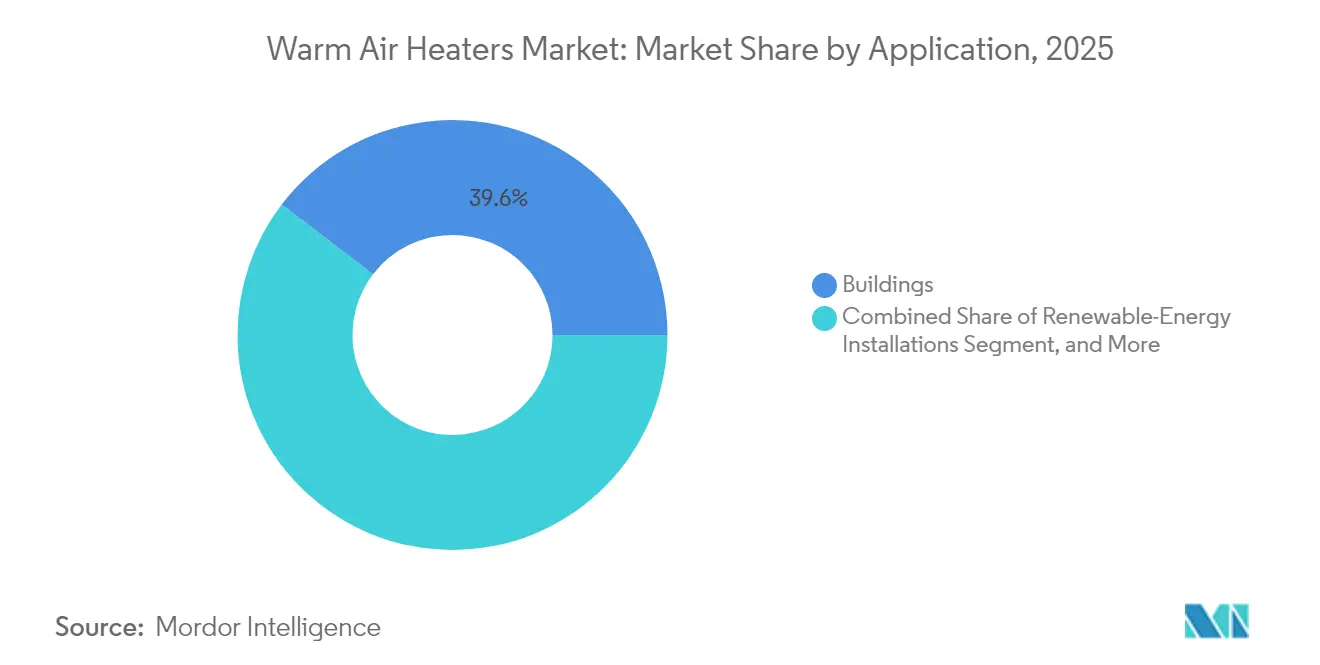

- By application, buildings commanded 39.62% share of the warm air heaters market size in 2025, whereas renewable-energy installations are poised to expand at an 8.41% CAGR by 2031.

- By fuel and power source, gas-fired units retained 35.10% share in 2025, but solar-powered systems are expected to post the strongest 9.12% CAGR to 2031.

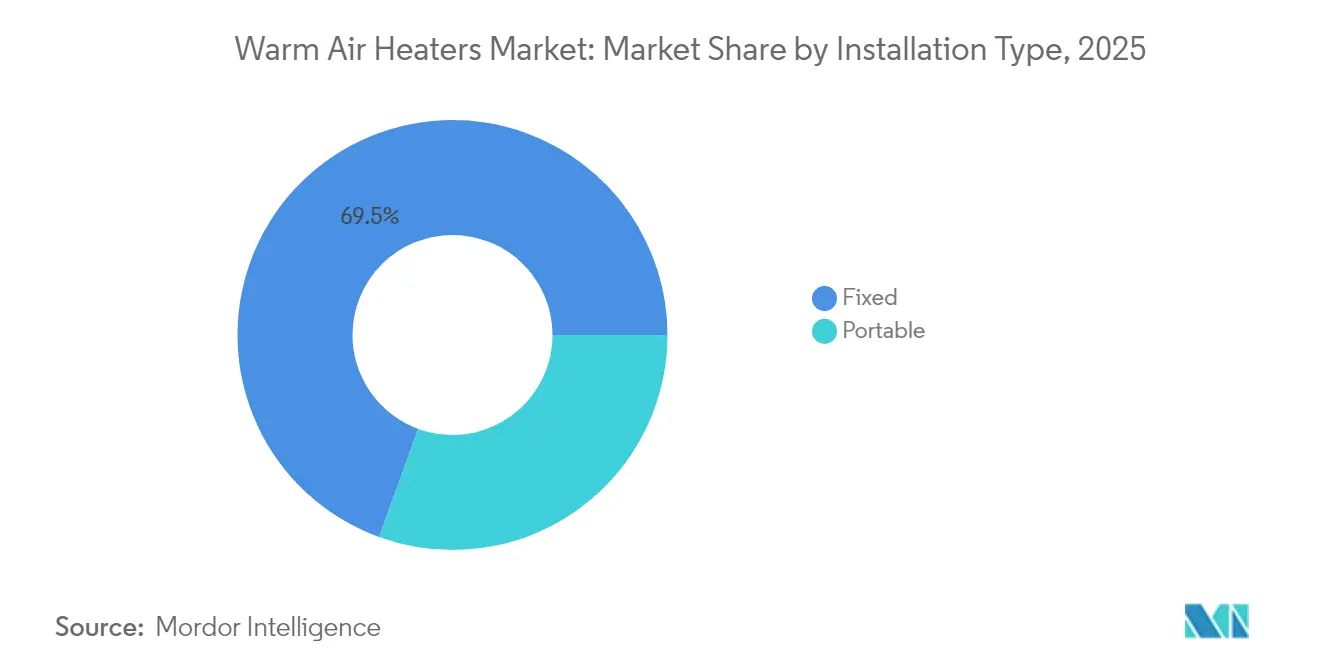

- By installation type, fixed systems held 69.45% of 2025 revenue, while portable heaters are advancing at a 7.78% CAGR through 2031.

- By power output, the 20-60 kW range captured 50.05% of 2025 sales, yet sub-20 kW units are set to grow the quickest at an 7.84% CAGR over the forecast horizon.

- By sales channel, OEM deliveries represented 59.55% share in 2025, but aftermarket and retail transactions are accelerating at a 8.93% CAGR to 2031.

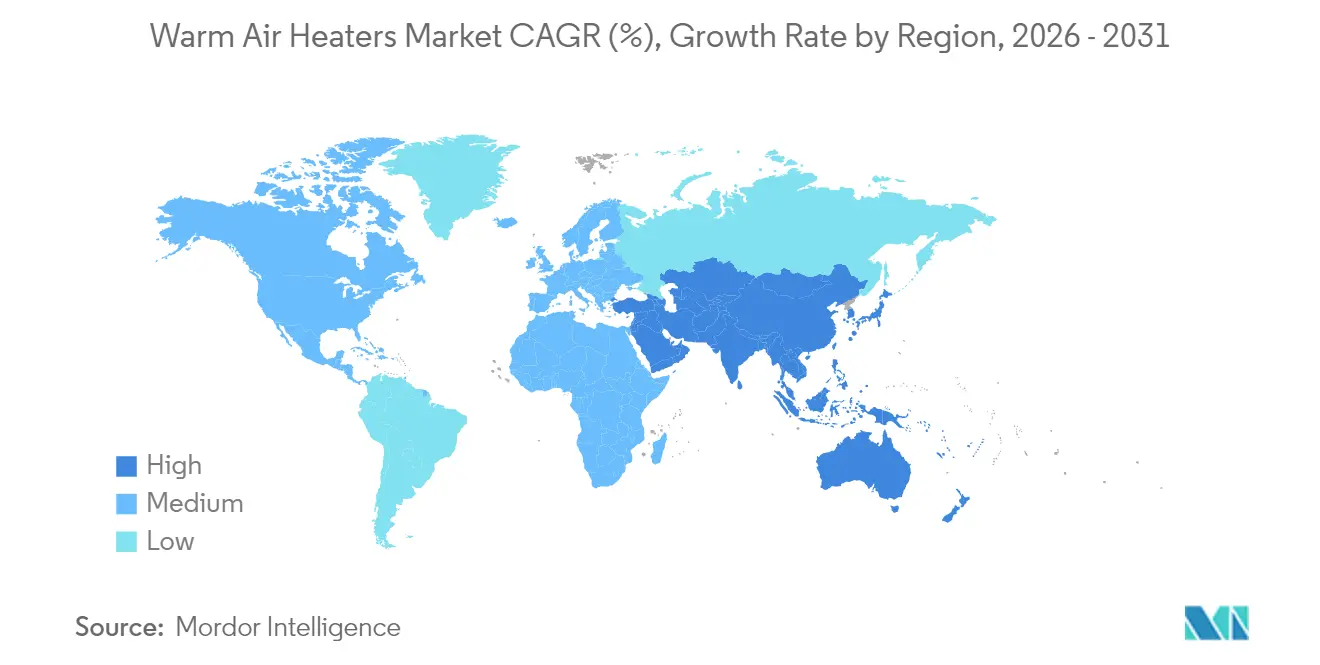

- By geography, Europe dominated with 29.70% share in 2025, whereas Asia-Pacific is projected to be the fastest-growing region at an 8.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Warm Air Heaters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter building-energy codes (global) | +1.20% | Global, with early adoption in EU and North America | Medium term (2-4 years) |

| Electrification incentives for space heating | +0.90% | North America and EU core, spillover to APAC | Long term (≥4 years) |

| Industrial decarbonisation mandates | +1.10% | Global, concentrated in developed markets | Long term (≥4 years) |

| Cold-chain expansion in food and pharma | +0.80% | Global, with APAC and MEA acceleration | Medium term (2-4 years) |

| Portable heating demand at construction sites | +0.60% | Global, seasonal variations by region | Short term (≤2 years) |

| Aftermarket IoT-based optimisation retrofits | +0.70% | North America and EU early adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Building-Energy Codes Drive Market Transformation

New construction and retrofit mandates now require higher seasonal efficiency ratings. The European Union’s Energy Performance of Buildings Directive obliges all new structures to meet near-zero-energy criteria from 2024, pushing buyers toward advanced warm air heaters equipped with condensing combustion or variable-speed fans.[1]European Commission, “Energy Performance of Buildings Directive,” energy.europa.eu Similar code tightness is spreading through North American jurisdictions under ASHRAE 90.1, expanding the addressable retrofit base. As a result, manufacturers prioritize R&D in high-efficiency heat exchangers and smart controls that automatically modulate firing rates to satisfy compliance audits. Widespread coverage 70% of global floor area by 2025 translates into a multibillion-dollar opportunity for premium-efficiency models.[2]International Energy Agency, “Heat Pumps Report 2024,” iea.org The driver is medium-term because many national building codes update on three- to five-year cycles, but once enacted, they trigger immediate procurement.

Electrification Incentives Reshape Heating Technology Mix

North America and Europe have earmarked large rebates that favour electric heating. For example, the U.S. Inflation Reduction Act allocates USD 4.3 billion for electric appliance incentives, directly subsidizing electric forced-air heater adoption in low-temperature industrial applications.[3]European Commission, “Energy Efficient Buildings,” energy.europa.eu Where heat pumps cannot deliver the necessary temperature delta or ramp-rate, electric warm air heaters fill the gap. Vendors are launching higher watt-density coils and silicon-controlled rectifier firing boards to exploit this funding window. The effect is long-term because rebate programs stretch over a decade and dovetail with grid-decarbonization targets that raise the renewable fraction in delivered electricity.

Industrial Decarbonization Mandates Accelerate Adoption

Post-COP28 commitments require industries to cut scope 2 emissions dramatically, encouraging a shift to electric, solar, or biomass warm air heaters. The European Union’s Carbon Border Adjustment Mechanism prices embedded CO₂ in imported goods, enlarging the compliance burden on exporters and accelerating heater upgrades.[4]International Renewable Energy Agency, “Tripling Renewable Power by 2030,” irena.org Multinationals are therefore specifying renewable-ready heaters with photovoltaic pre-heating or solar thermal boosters. The driver’s impact is global yet most acute in developed markets that enforce decarbonization disclosures.

Cold-Chain Infrastructure Expansion Generates Specialized Demand

Global refrigerated storage capacity expanded 18% in 2024, especially for pharmaceuticals and perishable foods. Warm air heaters serve frost-free zone management, defrost cycles, and emergency backup. Pharmaceutical warehouses must meet FDA validation for consistent ±2 °C ranges, spurring demand for redundant electric heaters with remote sensors. Asia-Pacific shows the swiftest capacity build, placing premium on scalable, modular heater designs that can be installed inside tight logistic timelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile fossil-fuel prices | -0.80% | Global, with regional variations | Short term (≤2 years) |

| Rising heat-pump substitution threat | -1.10% | North America and EU primarily | Medium term (2-4 years) |

| OEM margin pressure from commodity metals | -0.40% | Global manufacturing regions | Short term (≤2 years) |

| Safety recalls and regulatory liabilities | -0.30% | North America and EU regulatory focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Fossil-Fuel Prices Create Market Uncertainty

European natural-gas benchmarks swung between EUR 25 and EUR 45 per MWh (USD 28 – USD 50 per MWh) in 2024, distorting payback calculations for gas-fired heaters. Similar volatility in Brent crude increases hesitation toward oil-fired models. Buyers delay replacement cycles, waiting for price clarity, which depresses short-term demand even though many eventually adopt higher-efficiency or hybrid systems to hedge future volatility.

Rising Heat-Pump Substitution Threat Intensifies Competition

Global heat-pump shipments jumped 35% in 2024 to 20 million units, extending performance down to -25 °C and eroding warm air heater penetration in new residential builds. Generous subsidies up to USD 14,000 per home in the United States tilt the cost equation, encouraging consumers to bypass traditional combustion heaters. The restraint’s medium-term effect is strongest in Europe and North America where energy-efficiency labelling steers end-user choice.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Heater Type: Electric Momentum Challenges Fired Heater Leadership

The fired heater category retained a commanding 28.45% share of the warm air heaters market in 2025, largely because industrial furnaces and heavy-duty processes rely on direct-combustion units for rapid heat transfer. However, electric forced-air models are scaling quickly, benefiting from policy alignment with grid decarbonization and proving attractive in temperature-critical food and pharmaceutical lines. That shift translates into a 8.72% CAGR for electric systems, the fastest within the category horizon. Ongoing R&D focuses on variable-frequency drives and silicon-carbide heating elements that elevate energy conversion efficiency while shortening start-up times. Convection and radiant designs cater to niche zones such as cleanrooms or open loading docks, each offering targeted thermal comfort with reduced airflow disturbance.

A key competitive battleground is controls. Vendors are bundling edge-computing gateways that synchronize heaters with building automation networks, unlocking predictive maintenance and remote optimization. Solar-hybrid and battery-integrated modules remain nascent yet draw interest from off-grid logistics hubs. As electrification incentives widen, manufacturers that enhance coil durability and lower resistance drift will capture share from legacy combustion products. Overall, the warm air heaters market will continue valuing high-temperature reliability, but incremental share shifts will accumulate around electrically powered, smart-enabled platforms.

By End-User: Industrial Scale Meets Transportation Upswing

Industrial facilities held 44.70% of the warm air heaters market in 2025 by value, reflecting diverse needs from curing ovens and packaging lines to warehouse frost prevention. Process industries prize the rapid ramp-rate and ruggedness of gas-fired or high-wattage electric units, cementing this segment’s leadership. Meanwhile, the transportation sector advances at an 8.05% CAGR, underpinned by electric-vehicle charging parks that require enclosure heating to safeguard power electronics and by expanding cross-dock logistics operations that rely on forced-air units for quick turnover.

In contrast, residential penetration is stable yet challenged by heat-pump adoption, especially in new code-compliant dwellings. Commercial offices and retail stores show modest growth tied to indoor-air-quality initiatives that prefer high-circulation warm air heaters over radiant panels. Across segments, demand is trending toward integrated airflow filtration and real-time energy dashboards, enabling facility managers to validate savings metrics for ESG reporting.

By Application: Buildings Dominate While Renewable Energy Sites Surge

Buildings captured the largest warm air heaters market share at 39.62% in 2025, encompassing schools, hospitals, shopping centers, and multifamily housing that collectively require substantial seasonal heating. Retrofit activity accelerates as property owners pursue occupancy-comfort ratings and operational-carbon disclosures. Yet the most dynamic slice is renewable-energy installations, projected to grow 8.41% annually. Solar farm operators deploy low-wattage heaters to prevent dust-induced efficiency drops on panels, while battery-storage integrators rely on compact electric units for thermal management.

Power-generation plants, particularly gas-turbine sites in cold climates, continue specifying high-output gas-fired heaters to avert blade icing and ensure fast start capability. Tunnel projects and portable building compounds represent smaller but steady niches, illustrating the technology’s adaptability across infrastructural environments.

By Fuel and Power Source: Solar Upswing Challenges Gas Predominance

Gas-fired solutions maintained 35.10% of 2025 revenue, anchored by mature distribution grids and historically favourable fuel pricing. Nevertheless, solar-powered heaters show a 9.12% CAGR as photovoltaic module costs decline and corporates pledge scope 2 carbon neutrality. Electric units are also expanding, leveraging increasing renewable share in utility grids, which enhances the perceived sustainability of resistance heating. Biomass and hybrid systems occupy specialized agricultural and campus settings where fuel availability and policy credits converge.

The transition is gradual, and many operators choose staged upgrades: condensing gas models for near-term efficiency, followed by solar pre-heat retrofits once internal hurdle rates are met. Regional fuel economics, regulatory regimes, and infrastructure readiness all moderate the pace of substitution, yet the trajectory is unmistakably toward lower-carbon inputs.

By Power Output: Mid-Range Units Dominate, Small Systems Lead Growth

Mid-range 20-60 kW heaters held 50.05% of 2025 revenue, balancing capacity and energy consumption for mainstream commercial properties. Manufacturers focus on modulatory burners and multi-stage electric elements in this class to meet diverse part-load profiles. Below 20 kW, demand is rising fastest at 7.84% CAGR as zoning strategies and modular offices emphasize fine-grained temperature control. Integration of smart thermostats and voice-assistant compatibility helps vendors differentiate within this arena.

Above 60 kW, heavy-industry buyers remain loyal due to irreplaceable thermal throughput, yet they seek condensing efficiencies and flue-gas heat recovery to temper fuel bills. The power-output segmentation indicates an overarching industry pivot toward decentralized, right-sized heating that aligns with envelope-improvement gains in new-build architecture.

By Installation Type: Fixed Base with Portable Flexibility

Fixed systems delivered 69.45% of 2025 sales thanks to permanent placement in factories, schools, and logistics hubs that require year-round heating assurance. These installations increasingly integrate with building-automation dashboards, permitting centralized load balancing and demand-response participation. Portable heaters, although smaller in initial spend, will expand 7.78% per year as construction projects, disaster-relief shelters, and pop-up retail prefer plug-and-play warmth. Lithium-ion battery packs and wireless thermostats now equip portable ranges, extending runtime and oversight.

Cost-of-ownership is the deciding factor. For long-life assets, fixed units deliver superior lifecycle efficiency once ductwork and zoning are optimized. Conversely, portable models capture customers seeking rapid deployment with minimal permit hurdles. Over time, smart firmware commonality across both formats will allow manufacturers to upsell analytics services and remote performance guarantees.

By Sales Channel: OEM Builds Give Way to Aftermarket Hustle

OEM pathways captured 59.55% of 2025 shipments because large construction and retrofit projects typically specify complete mechanical packages. However, aftermarket and retail channels are gaining momentum at a 8.93% CAGR, reflecting the growing installed base requiring replacement parts and quick-turn heater swaps. E-commerce platforms now showcase comparison dashboards that spotlight energy-consumption KPIs, expediting buyer decisions for small businesses and homeowners.

Service-oriented distributors bundle installation and periodic inspection contracts, cultivating recurring revenue beyond the initial sale. As product life cycles lengthen, remote firmware upgrades over cellular gateways will further shift value capture downstream, reinforcing the aftermarket’s strategic importance.

Geography Analysis

Europe led with a 29.70% warm air heaters market share in 2025, sustained by headline policies such as the Renovation Wave, which has earmarked EUR 150 billion (USD 165 billion) for efficiency retrofits by 2030. Industrial decarbonization targets and carbon-price pass-throughs also lift electric and solar-hybrid demand in Germany, France, and the United Kingdom. Regulators employ Ecodesign minimum-efficiency thresholds that effectively retire low-grade combustion units, securing a pipeline of replacement opportunities. Seasonal heating demand remains pronounced across Northern Europe, ensuring baseline volume even during macroeconomic slowdowns.

Asia-Pacific is the fastest-growing region, forecast at 8.28% CAGR through 2031, buoyed by China and India’s manufacturing scale-up and vast cold-chain investments. Chinas centrally financed clean-energy push allocates USD 440 billion to electrification infrastructure through 2025, stimulating adoption of large-format electric heaters in EV battery plants and semiconductor fabs. Southeast Asian logistics zones, meanwhile, opt for portable gas-fired units that suit variable tenancy terms. Local producers leverage cost-competitive labour to price aggressively, yet global brands retain an edge in high-spec industrial and pharmaceutical projects.

North America maintains solid, replacement-led growth as the Infrastructure Investment and Jobs Act provides USD 65 billion in building upgrades that prioritize hazard-free electric heating. States in the northern tier consistently experience long heating seasons, keeping demand predictable. Canada’s carbon price, escalating to CAD 170 (USD 133) per tonne CO₂ by 2030, incentivizes oil-to-gas or gas-to-electric conversions across commercial real estate portfolios. In the Middle East and Africa, construction booms in the Gulf Cooperation Council states and cold-storage projects in sub-Saharan Africa produce emerging demand pockets, albeit from a low base.

Competitive Landscape

The warm air heaters market shows moderate fragmentation. Global manufacturers such as Lennox International, Johnson Controls, and Daikin Industries compete on breadth of portfolio, international after-sales coverage, and R&D velocity. Each invests heavily in IoT platforms that unify heaters with chillers and air-handling units, allowing predictive service routines that minimize downtime. Mid-tier specialists like Modine Manufacturing target industrial niches such as paint-curing booths, focusing on ruggedization and high-temperature tolerances. Patent filings for efficiency and control methods increased 28% in 2024, signalling intensified intellectual-property jockeying.

Strategically, market leaders pursue scale and scope. Johnson Controls’ USD 2.8 billion purchase of Hitachi’s HVAC division widened its Asia-Pacific reach and injected advanced heat-pump know-how into its heater design pipeline. Trane Technologies made three acquisitions aiming at electric and renewable heaters, reflecting the urgency to align with decarbonization roadmaps. New entrants pitch AI-enabled optimization layers that retrofit onto legacy fleets, extracting energy savings without capex-heavy equipment swaps. The competitive chessboard now extends beyond hardware to encompass data analytics and energy-as-a-service contracts, reshaping revenue pools over the medium term.

Looking forward, differentiation will hinge on digital-native features, verified lifecycle emissions metrics, and supply-chain resilience to volatile metal prices. Partnerships between heater providers and renewable-integrator firms will accelerate, particularly for off-grid applications or grid-constrained industrial parks. The overall environment favours players that can balance cost competitiveness with premium features and compliance guarantees.

Recent Industry Developments

- October 2025: The European Commission published final Terms and Conditions for the first EUR 1 billion pilot auction to decarbonize industrial heat, offering five-year fixed premiums proportional to CO₂ abatement for projects using electric or renewable heat.

- September 2025: BASF broke ground on a sub-50 MW industrial heat pump at its Ludwigshafen site that will generate up to 500,000 tonnes of CO₂-free steam annually, backed by up to EUR 310 million in German Carbon Contracts for Difference funding.

- September 2025: Vonovia SE partnered with EnerCube and DFA Demonstrationsfabrik Aachen to mass-produce prefabricated Heat Pump Cubes for apartment blocks, targeting 1,000 units by 2029 to decarbonize more than 20,000 German residences.

- July 2025: Heaten secured a strategic partnership with Advent International, which will fund capacity expansion, new product launches, and potential M&A to accelerate growth in advanced heating solutions.

Global Warm Air Heaters Market Report Scope

The Warm Air Heaters Market Report is Segmented by Type (Fired Heaters, Electric Forced-Air Heaters, Convection Heaters, Radiant Heaters, Others), End-User (Residential, Commercial, Industrial, Transportation), Application (Buildings, Power Generation, Industrial Processes, Others), Fuel/Power Source (Gas-Fired, Electric, Solar Powered, Others), Installation Type (Portable, Fixed), Power Output (<20 kW, 20-60 kW, >60 kW), Sales Channel (OEMs, Aftermarket/Retail), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Fired Heaters |

| Electric Forced-Air Heaters |

| Convection Heaters |

| Radiant Heaters |

| Radiant Tube Heaters |

| Duct Heaters |

| Enclosure Heaters |

| Heat Torches and Flame Heaters |

| Room Heaters |

| Others Heater Types |

| Residential |

| Commercial |

| Industrial |

| Transportation |

| Tunnels |

| Power Generation |

| Industrial Processes |

| Buildings |

| Portable Buildings |

| Renewable-Energy Installations |

| Other Applications |

| Oil-Fired |

| Gas-Fired |

| Electric |

| Solar Powered |

| Others Fuel / Power Sources |

| More than 20 kW |

| 20 - 60 kW |

| Less than 60 kW |

| Portable |

| Fixed |

| OEMs |

| Aftermarket / Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Heater Type | Fired Heaters | |

| Electric Forced-Air Heaters | ||

| Convection Heaters | ||

| Radiant Heaters | ||

| Radiant Tube Heaters | ||

| Duct Heaters | ||

| Enclosure Heaters | ||

| Heat Torches and Flame Heaters | ||

| Room Heaters | ||

| Others Heater Types | ||

| By End-User | Residential | |

| Commercial | ||

| Industrial | ||

| Transportation | ||

| By Application | Tunnels | |

| Power Generation | ||

| Industrial Processes | ||

| Buildings | ||

| Portable Buildings | ||

| Renewable-Energy Installations | ||

| Other Applications | ||

| By Fuel / Power Source | Oil-Fired | |

| Gas-Fired | ||

| Electric | ||

| Solar Powered | ||

| Others Fuel / Power Sources | ||

| By Power Output | More than 20 kW | |

| 20 - 60 kW | ||

| Less than 60 kW | ||

| By Installation Type | Portable | |

| Fixed | ||

| By Sales Channel | OEMs | |

| Aftermarket / Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the warm air heaters market?

The warm air heaters market is valued at USD 7.08 billion in 2026, growing toward USD 10.09 billion by 2031.

Which region leads sales of warm air heaters?

Europe held the largest 29.70% share in 2025 due to stringent energy-efficiency codes and retrofit incentives.

Which application is expanding fastest?

Renewable-energy installations are the fastest-growing application, forecast to register an 8.41% CAGR through 2031.

How are electric warm air heaters gaining ground?

Electrification incentives, grid decarbonization, and improved high-wattage coil technology drive a 8.72% CAGR for electric forced-air models.

Why is the transportation sector important for future demand?

Warehouses, logistics hubs, and EV-charging enclosures need reliable forced-air warmth, propelling the transportation segment at an 8.05% CAGR.

Page last updated on: