Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 47.24 Billion |

| Market Size (2031) | USD 61.21 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

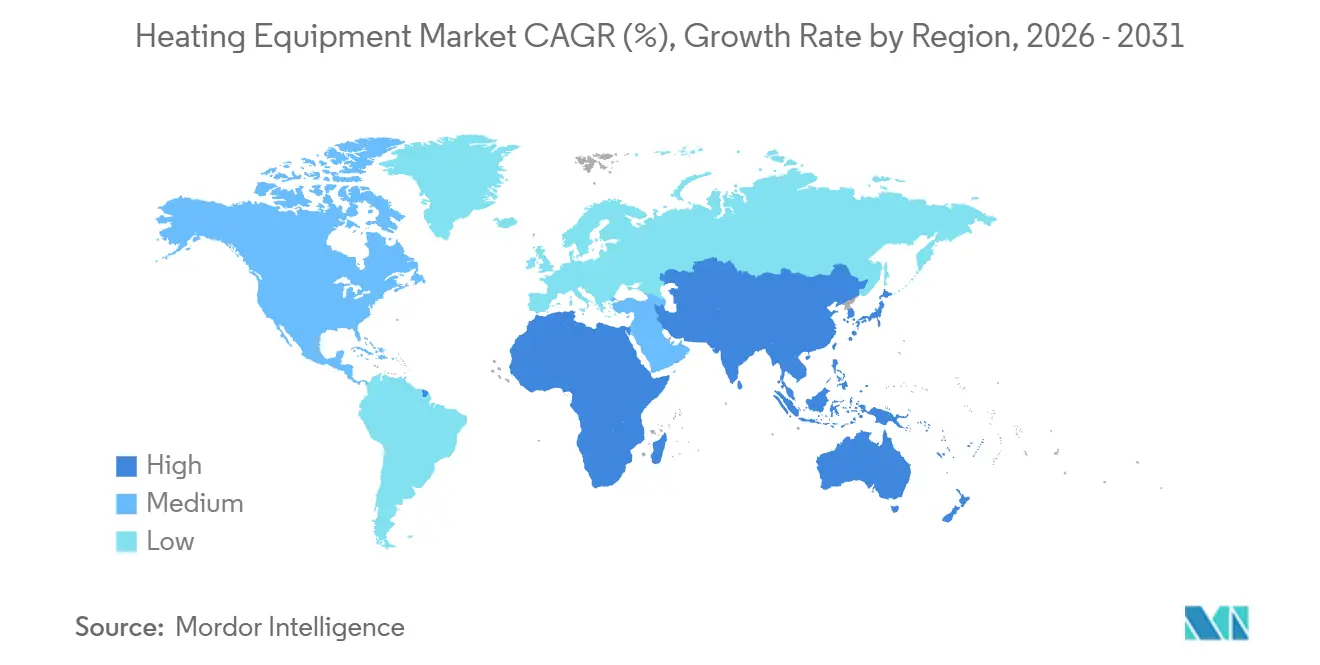

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heating Equipment Market Analysis by Mordor Intelligence

The heating equipment market size is expected to increase from USD 45.14 billion in 2025 to USD 47.24 billion in 2026 and reach USD 61.21 billion by 2031, growing at a CAGR of 5.32% over 2026-2031. Growth reflects performance-based building codes, corporate decarbonization pledges, and electrification programs that favor heat pumps over combustion appliances. Heat pumps now offer year-round comfort as single assets, while hydrogen-ready boilers give building owners a phased decarbonization path. District-energy operators are pairing waste-heat loops with centralized heat pumps to offset natural-gas demand, and manufacturers are investing in modular compressors that shorten installation time. Policy-linked rebates continue easing first-cost barriers, yet grid planners must manage coincident winter peaks as more dwellings electrify.

Key Report Takeaways

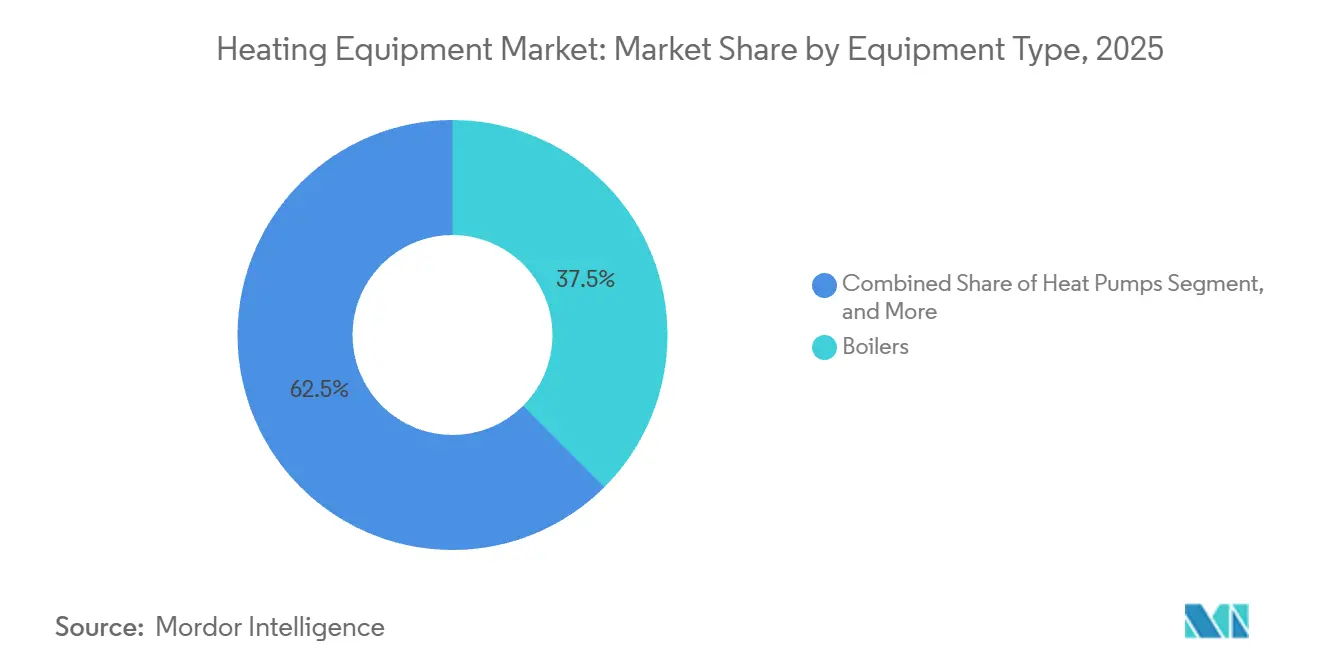

- By equipment type, boilers retained 37.54% of heating equipment market share in 2025 while heat pumps are advancing at a 6.38% CAGR through 2031.

- By end-user industry, the residential segment commanded 57.83% of the heating equipment market size in 2025 and is projected to post a 6.42% CAGR to 2031.

- By fuel type, electricity-based systems captured 54.72% share in 2025, whereas hydrogen-ready configurations represent the fastest growing slice at a 6.63% CAGR.

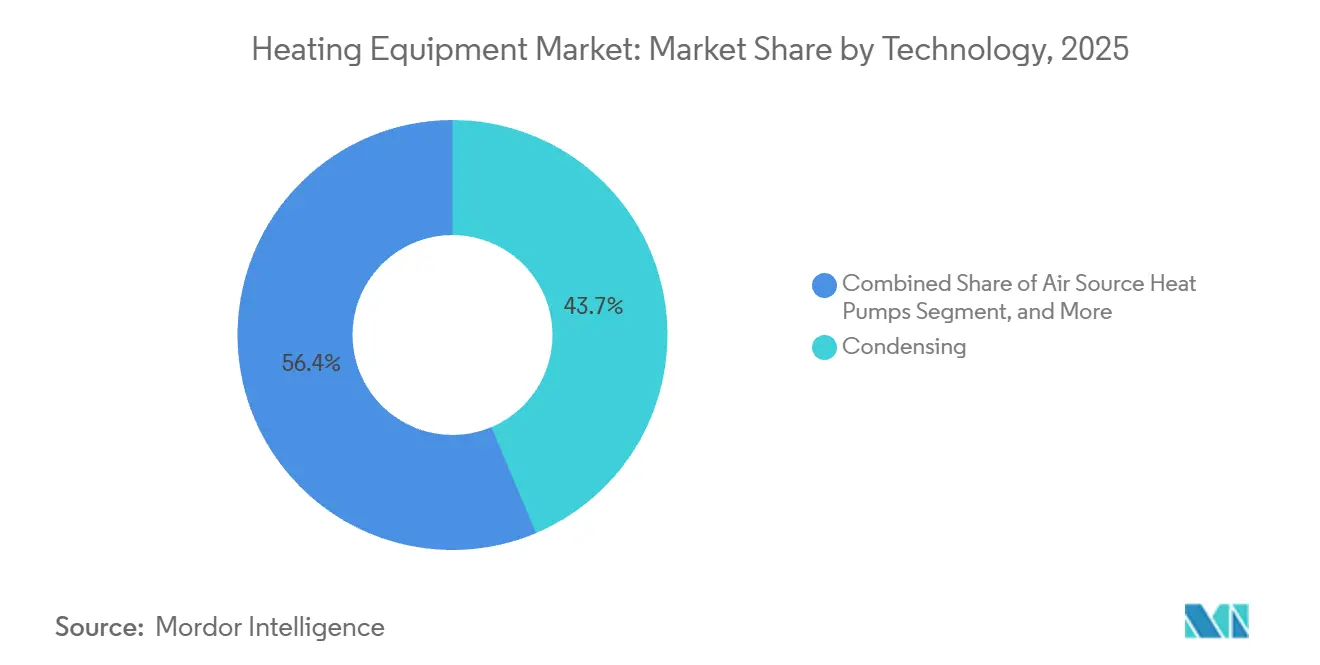

- By technology, condensing boilers accounted for 43.65% of the heating equipment market size in 2025, yet air-source heat pumps are on track for a 7.67% CAGR.

- By installation type, replacement and retrofit activity represented 70.32% of market share in 2025, while new installations are forecast to rise at a 6.89% CAGR through 2031.

- By geography, Asia-Pacific led with a 40.19% revenue share in 2025, whereas the Middle East and Africa region is positioned for the fastest 7.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Heating Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification Push in Cold-Climate Retrofit Programs | +1.2% | North America and Europe, spillover to Northeast Asia | Medium term (2-4 years) |

| Carbon-Neutral Corporate Campuses Demand On-Site Heat Pumps | +0.8% | Global, concentrated in North America and Western Europe | Short term (≤ 2 years) |

| Gas-Phase Heat Pump Innovations for High-Temperature Industrial Drying | +0.6% | Europe and Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Performance-Based Building Codes Accelerating Boiler Replacement | +1.0% | Europe and select North American cities | Medium term (2-4 years) |

| Waste-Heat-to-Heat-Pump Integration in District Energy | +0.5% | Northern Europe, China, South Korea | Long term (≥ 4 years) |

| Green Hydrogen Blending Pilots in Commercial Boilers | +0.4% | Germany, Netherlands, United Kingdom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification Push in Cold-Climate Retrofit Programs

Sub-zero regions now direct public money toward heat-pump retrofits that displace fuel-oil and propane systems. New York’s Clean Heat program allocated USD 250 million in 2025 for 100,000 residential conversions, while Quebec earmarked CAD 300 million (USD 222 million) to leverage surplus hydro power.[1]New York State Energy Research and Development Authority, “Clean Heat Program,” nyserda.ny.gov Hardware is ready; Mitsubishi’s Zuba-Central ducted unit maintains full output at minus-30 °C, and Carrier pairs water-source heat pumps with glycol loops to prevent frosting. The choke point has shifted from technology readiness to installer capacity and utility rate design that still lags hardware innovation by roughly two years.

Carbon-Neutral Corporate Campuses Demand On-Site Heat Pumps

Corporations pursuing Science Based Targets swap boilers for large water-source or ground-source systems to erase Scope 1 emissions. Microsoft retrofitted 12 data-center campuses, cutting natural-gas use 85% and retiring offset purchases.[2]Microsoft, “2025 Sustainability Report,” microsoft.com Amazon specified ground-source units for German and Polish warehouses, and Unilever is electrifying 40 factories by 2030. Each job often exceeds 500 kW, carries multi-year service revenue, and favors heat-pump-as-a-service contracts in which OEMs bill per delivered kilowatt-hour rather than equipment sales.

Gas-Phase Heat Pump Innovations for High-Temperature Industrial Drying

Industrial lines needing 120 °C-plus supply now test gas-phase units driven by natural gas or biogas. A German textile mill pilot cut primary energy 40% and delivered under-four-year payback, spurring European and Japanese funding rounds.[3]German Federal Ministry for Economic Affairs and Climate Action, “Industrial Heat-Pump Funding,” bmwk.de Bosch and Johnson Controls are engineering modular systems up to 2 MW, positioning for upcoming revisions to the European Industrial Emissions Directive that could mandate such solutions.

Performance-Based Building Codes Accelerating Boiler Replacement

Regulators now cap building energy intensity rather than prescribing equipment ratings. The United Kingdom’s Future Homes Standard bans fossil heating in new homes from 2026, Germany’s GEG forces 65% renewable heat in replacements, and France’s RE2020 imposes carbon caps that de facto eliminate gas-only boilers. These rules shorten upgrade cycles to five-to-seven-year windows, pushing both heat-pump makers and boiler brands to rush hydrogen-ready models that satisfy interim thresholds while hedging future fuel mixes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-Capacity Bottlenecks in Electrified Neighborhoods | -0.9% | North America and Europe, urban clusters | Short term (≤ 2 years) |

| Skilled-Labor Shortages for Multi-Technology Retrofits | -0.7% | Global, acute in Germany, United Kingdom, United States | Medium term (2-4 years) |

| Volatile Nickel Prices Inflating Advanced Heat-Pump BOM | -0.4% | Global, supply-chain exposure in Asia-Pacific | Short term (≤ 2 years) |

| Fragmented Residential Rebate Administration | -0.3% | United States and European Union member states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Capacity Bottlenecks in Electrified Neighborhoods

Rapid electrification can double winter peaks, overloading transformers and feeders sized for gas-heated homes. National Grid flagged 22% of low-voltage circuits in Greater London for reinforcement, with upgrade costs near GBP 4,000 (USD 5,200) per household and lead times stretching 18 months. Eversource delayed 1,200 applications in Massachusetts because substations lacked spare capacity. German utilities estimate EUR 50 billion (USD 54 billion) of network investment by 2035, expenses that ultimately raise delivered electricity prices. Demand-response curtailments help, but add installation complexity when contractors must enroll customers and commission smart thermostats.

Skilled-Labor Shortages for Multi-Technology Retrofits

Heat-pump rollouts demand HVAC, electrical, and plumbing competence, yet training pipelines lag. The United Kingdom needs 30,000 certified installers by 2030, but had roughly 3,000 in 2025. Germany faces a 60,000-technician shortfall, and only 15% of U.S. contractors are proficient in cold-climate commissioning. OEMs respond with VR simulators and community-college curricula, yet these moves take two-plus years to yield field-ready talent, lengthening project queues and dampening consumer confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Heat Pumps Erode Boiler Dominance

Boilers still hold 37.54% market share in 2025, anchored by industrial steam and district-energy loads requiring 90 °C-plus output. Heat pumps, however, are advancing at a 6.38% CAGR and increasingly cannibalize forced-air furnace replacements in North America and hydronic radiators in Europe. Furnaces linger in ducted U.S. housing but now face direct substitution via ducted inverter heat pumps. Niche devices such as radiant panels capture specialty applications yet carry premium margins. The competitive divide shows residential and light-commercial customers pivoting hard toward electrification, while high-temperature industrial lines retain boilers until gas-phase technology or hydrogen blending scales. Hybrid heat-pump-plus-boiler packages ease adoption by allowing 80% electrified annual load with fossil backup for extreme peaks, smoothing grid impact and homeowner cost.

Strategic differentiation revolves around software. Trane’s Tracer platform forecasts occupancy and weather, pre-heats during off-peak tariffs, and unlocks utility incentives for demand shedding. These features move the heating equipment market from hardware margin to lifetime service value, raising barriers for price-only entrants and encouraging incumbents to bundle analytics with warranty and maintenance.

By End-User Industry: Residential Volume Versus Industrial Value

In 2025, residential buyers made up 57.83% of the market share and are projected to grow at a CAGR of 6.42% through 2031. This growth is bolstered by U.S. tax credits, European retrofit mandates, and China's transition from coal to electricity. Meanwhile, commercial property managers, focusing on total cost of ownership, command a share of about 25%, showing a preference for units primed for building-automation integration.

Industrial customers, at 12%, value 120 °C-plus capability and custom engineering, often paying more than USD 100,000 per 500-kW unit; Thermax leveraged this specialization to win pharmaceutical and dairy waste-heat projects. Public facilities adopt early due to policy mandates despite longer paybacks. Purchase behavior thus varies, residential sales hinge on rebate simplicity and financing, commercial deals on demand-response and warranty, and industrial contracts on process integration depth.

By Fuel Type: Electricity Leads as Hydrogen Hedges

Electricity-based systems held 54.72% market share in 2025, reflecting cheap hydro in Scandinavia and Quebec and falling rooftop solar costs. Natural gas lingers where pipeline access keeps delivered cost lower than retail power. Oil use shrinks as subsidies vanish, while biomass boilers serve off-grid sites with forestry residues.

Hydrogen-ready models grow at a 6.63% CAGR, hedging grid decarbonization. Bosch launched a boiler certified for 100% hydrogen yet deployable today on gas networks, offering owners forward compatibility. Viessmann’s burner can convert in two hours, minimizing downtime once 20% blending becomes standard. Economics depend on green-hydrogen price trajectories that IRENA expects below USD 2/kg by 2030, a threshold that could reset comparative fuel costs.

By Technology: Air-Source Units Accelerate, Condensing Boilers Hold Installed Base

Condensing boilers captured 43.65% share in 2025 because they retrofit easily into existing hydronic loops while meeting efficiency rules. Air-source heat pumps, though, post a 7.67% CAGR as R-32 and R-454B refrigerants cut global-warming potential without sacrificing low-temp capacity. Ground-source systems boost seasonal performance but face high drilling cost barriers.

Hybrid solutions blend the two, popular in the United Kingdom and Netherlands where gas infrastructure persists. Variable-speed inverter compressors represent the core technology leap, with Panasonic’s dual-rotary design retaining full capacity at -20 °C and Daikin’s high-temperature model delivering 70 °C water for legacy radiators. Smart sensors and cloud diagnostics turn equipment into grid-interactive assets eligible for balancing-market revenue.

By Installation Type: Retrofit Dominance with New-Build Upswing

Retrofits accounted for 70.32% of 2025 activity as Europe and North America tackled boiler fleets aged 15 years or more. New installations, however, are climbing at a 6.89% CAGR during the forecast period. This is because developers must now meet performance certificates that ban non-condensing units from day one.

Retrofits are complex, often needing electrical-panel upgrades and envelope improvements; new builds integrate heat pumps with heat-recovery ventilation to minimize system size. Programs such as Germany’s EUR 13 billion Federal Funding for Efficient Buildings and France’s MaPrimeRénov grants compress replacement cycles but create policy-driven demand spikes when budgets lapse.

Geography Analysis

Asia-Pacific held 40.19% of 2025 revenue as China converted coal boilers, India’s middle class upgraded to ducted heat pumps, and Japan subsidized inverter units. Europe followed at roughly 30% as German, French, and United Kingdom mandates converged, though grid limits and labor shortages temper growth. North America represented about 20%; Inflation Reduction Act credits up to USD 2,000 per home accelerated adoption in cold states, while Canadian provinces leaned on hydro surplus. The Middle East and Africa lead in growth at a 7.78% CAGR amid giga-projects like NEOM that specify solar-thermal-heat-pump hybrids. South America remains small but gains momentum in Brazil’s hydro-rich southern states where social housing now opts for split heat-pump systems.

China’s market splits between centralized district heating in the north and individual split units in the south, forcing OEMs to tailor product lines. India logged Daikin sales growth of 18% in 2025 as apartment construction boomed. Japan’s trade ministry targets 5 million residential units by 2030 to curb liquefied natural-gas imports. In the Middle East, Dubai’s district-cooling network pilots heat-recovery chillers to supply hotel hot water, underlining that heating demand exists even in hot climates.

Europe accounted for roughly 30% of the heating equipment market share in 2025 as retrofit grants and rising carbon prices converged to accelerate boiler replacement, yet sustained expansion hinges on clearing installer backlogs and reinforcing urban distribution grids, particularly in cities such as London and Munich that face 18-month transformer lead times. North America held about 20% of 2025 demand, with Inflation Reduction Act tax credits of up to USD 2,000 per household and provincial cold-climate rebates in Canada boosting residential uptake. Data-center waste-heat recovery offers fresh upside across the United States hyperscale corridor, where operators are evaluating absorption-heat-pump pairings to curb diesel-boiler runtime. Latin America remains a niche today, yet Brazil’s hydro-rich southern states are piloting tariff structures that reward heat-pump load shifting to off-peak periods, laying groundwork for future scaling.

Competitive Landscape

The heating equipment market displays fragmentation with players like Daikin, Carrier, Bosch, Trane, NIBE and Others. Demand-response readiness shapes differentiation; Daikin filed 2025 patents for occupancy-led pre-heating algorithms. NIBE bought 14 European contractors to lock in service revenue and ensure installation quality, while Chinese rivals Gree and Midea push into Europe with 20-30% price discounts but thinner support networks. Waste-heat recovery in data centers and factories is an emerging battleground as OEMs bundle absorption chillers with high-lift heat pumps. Hybrid systems pit Bosch and Viessmann’s integrated packages against Carrier and Trane’s modular add-ons, letting customers migrate in stages.

Residential competition intensifies as rebate schemes lower effective purchase price, compelling incumbents to highlight extended warranties and smart-home integration. Industrial high-temperature projects remain fragmented, allowing Thermax and Mayekawa to secure projects that demand process-specific engineering. Software-only disruptors such as Sense retrofit legacy boilers with IoT controllers, threatening replacement-driven sales models by extracting demand-response value from existing assets.

Alliances between equipment makers, energy utilities, and cloud-platform vendors are deepening as each side seeks recurring software and balancing-market revenue. Boiler incumbents are co-developing hydrogen-combustion trials with pipeline operators to secure early mover status once 20% blending becomes mainstream. At the same time, venture capital is funding start-ups that layer predictive maintenance analytics onto any brand of heat pump, eroding brand-lock advantages that traditional manufacturers long enjoyed. These dynamics signal a shift toward ecosystem competition where hardware, fuel supply, and data services converge, favoring players that can orchestrate the full stack rather than excel at a single component.

Heating Equipment Industry Leaders

Robert Bosch GmbH

Daikin industries ltd

Carrier Global Corporation

Trane Technologies plc

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Daikin earmarked EUR 200 million (USD 217 million) to expand its Ostend, Belgium factory, lifting heat-pump capacity to 800,000 units per year by 2027.

- December 2025: Carrier partnered with Schneider Electric to connect AquaEdge heat pumps to EcoStruxure software for predictive maintenance and demand-response participation.

- November 2025: NIBE acquired a 75% stake in a Polish HVAC distributor for EUR 45 million (USD 48.8 million), adding 22 service centers and 180 installers.

- October 2025: Bosch unveiled hydrogen-ready condensing boilers certified for 100% hydrogen, with burners convertible in two hours.

Global Heating Equipment Market Report Scope

The heating equipment market is witnessing significant growth, driven by increasing demand for energy-efficient solutions, advancements in heating technologies, and the rising adoption of renewable energy sources. The market is also influenced by stringent government regulations aimed at reducing carbon emissions and promoting sustainable practices across various industries.

The Heating Equipment Market Report is Segmented by Equipment Type (Boilers, Furnaces, Heat Pumps, Radiators, and Other Heater Types), End-User Industry (Residential, Commercial, Industrial, and Public/Institutional), Fuel Type (Natural Gas, Electricity, Oil, Biomass, and Hydrogen-Ready), Technology (Condensing, Non-Condensing, Air Source Heat Pumps, Ground Source Heat Pumps, Hybrid Systems, and Smart Connected Systems), Installation Type (New Installation, and Replacement/Retrofit), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Equipment Type

| Boilers |

| Furnaces |

| Heat Pumps |

| Radiators |

| Other Heater Types |

By End-User Industry

| Residential |

| Commercial |

| Industrial |

| Public/Institutiona |

By Fuel Type

| Natural Gas |

| Electricity |

| Oil |

| Biomass |

| Hydrogen-Ready |

By Technology

| Condensing |

| Non-Condensing |

| Air Source Heat Pumps |

| Ground Source Heat Pumps |

| Hybrid Systems |

| Smart Connected Systems |

By Installation Type

| New Installation |

| Replacement/Retrofit |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Equipment Type | Boilers | ||

| Furnaces | |||

| Heat Pumps | |||

| Radiators | |||

| Other Heater Types | |||

| By End-User Industry | Residential | ||

| Commercial | |||

| Industrial | |||

| Public/Institutiona | |||

| By Fuel Type | Natural Gas | ||

| Electricity | |||

| Oil | |||

| Biomass | |||

| Hydrogen-Ready | |||

| By Technology | Condensing | ||

| Non-Condensing | |||

| Air Source Heat Pumps | |||

| Ground Source Heat Pumps | |||

| Hybrid Systems | |||

| Smart Connected Systems | |||

| By Installation Type | New Installation | ||

| Replacement/Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the heating equipment market in 2026?

The heating equipment market size is USD 47.24 billion in 2026, with a forecast 5.32% CAGR through 2031.

Which equipment type is growing fastest?

Heat pumps are expanding at a 6.38% CAGR, benefitting from mandates and cold-climate technology advances.

Why are hydrogen-ready boilers gaining attention?

They let owners operate on natural gas today yet switch to up to 100% hydrogen when grids decarbonize, protecting long-term asset value.

What region shows the highest growth rate?

The Middle East and Africa region is projected for a 7.78% CAGR to 2031 as giga-projects specify solar-thermal-heat-pump hybrids.

What limits heat-pump adoption in urban areas?

Grid-capacity bottlenecks force utilities to upgrade transformers and feeders, delaying interconnection approvals and raising costs.

Page last updated on: