Residential HVAC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

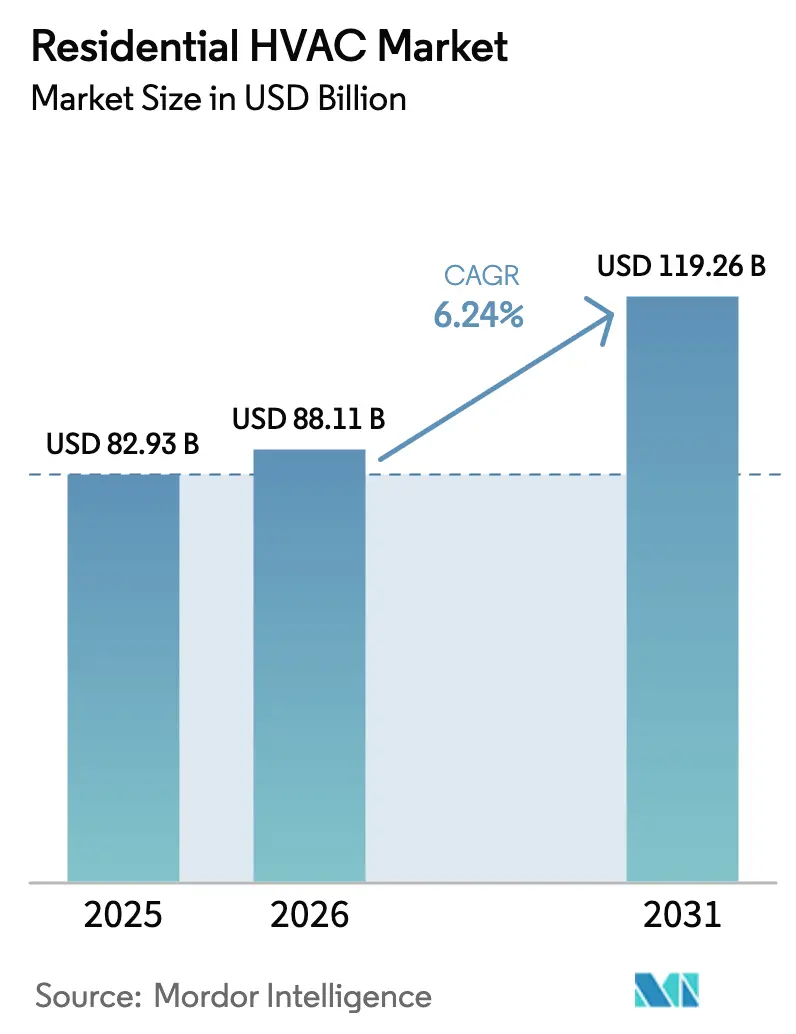

| Market Size (2026) | USD 88.11 Billion |

| Market Size (2031) | USD 119.26 Billion |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Residential HVAC Market Analysis by Mordor Intelligence

The residential HVAC market size is expected to grow from USD 82.93 billion in 2025 to USD 88.11 billion in 2026 and is forecast to reach USD 119.26 billion by 2031 at 6.24% CAGR over 2026-2031. Rising electrification mandates, pervasive smart‐home adoption, and post-pandemic home-improvement cycles are propelling revenue growth as households migrate toward high-efficiency, grid-interactive solutions. Regulatory pressure to eliminate high-GWP refrigerants, expanding utility incentive programs, and innovative financing models that minimize up-front costs are further stimulating demand. Cooling and ventilation equipment remains the largest revenue generator, while heat pumps outpace legacy gas systems in temperate and cold climates. Competitive intensity is accelerating as global manufacturers deploy mergers and acquisitions to deepen geographic penetration, enhance component supply chains, and secure leadership in connected-equipment ecosystems.[1]International Energy Agency, “Is a Turnaround in Sight for Heat Pump Markets?,” iea.org

Key Report Takeaways

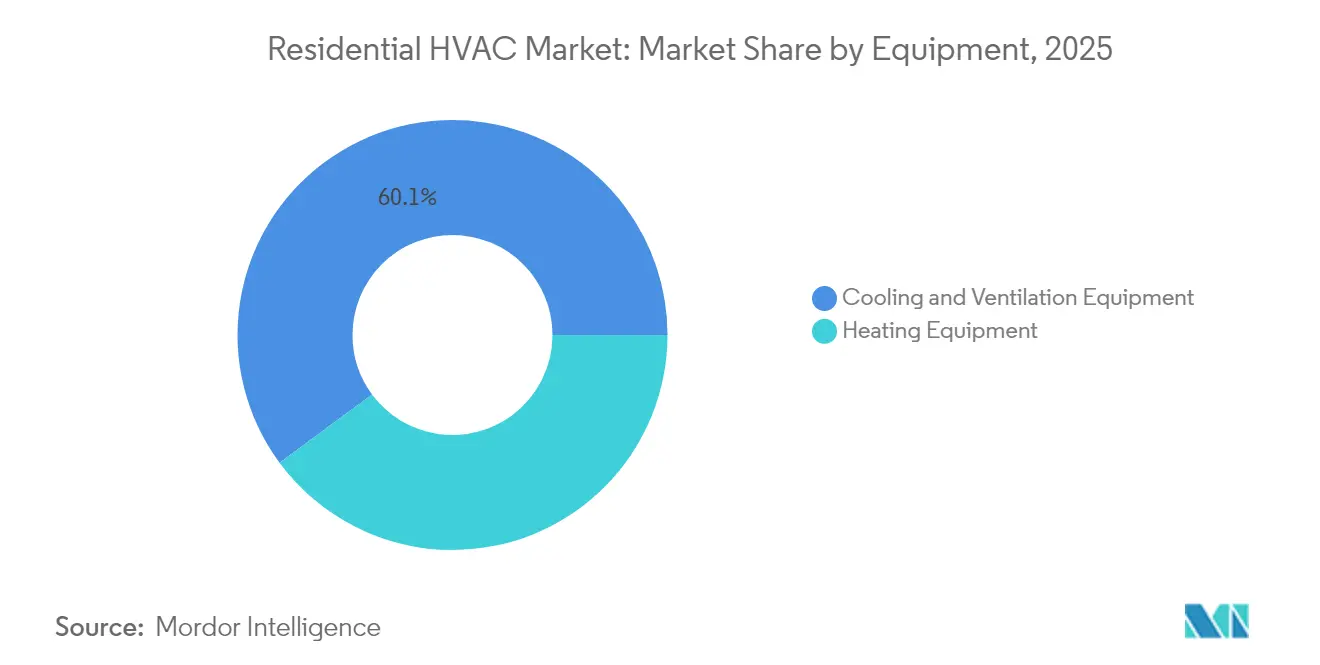

- By equipment, cooling and ventilation accounted for 60.12% of residential HVAC market share in 2025. By equipment, heating equipment is projected to expand at a 7.05% CAGR through 2031.

- By technology, conventional R 410A/R 22 systems retained 69.85% residential HVAC market share in 2025. By technology, low-GWP refrigerant systems are forecast to grow at a 7.32% CAGR to 2031.

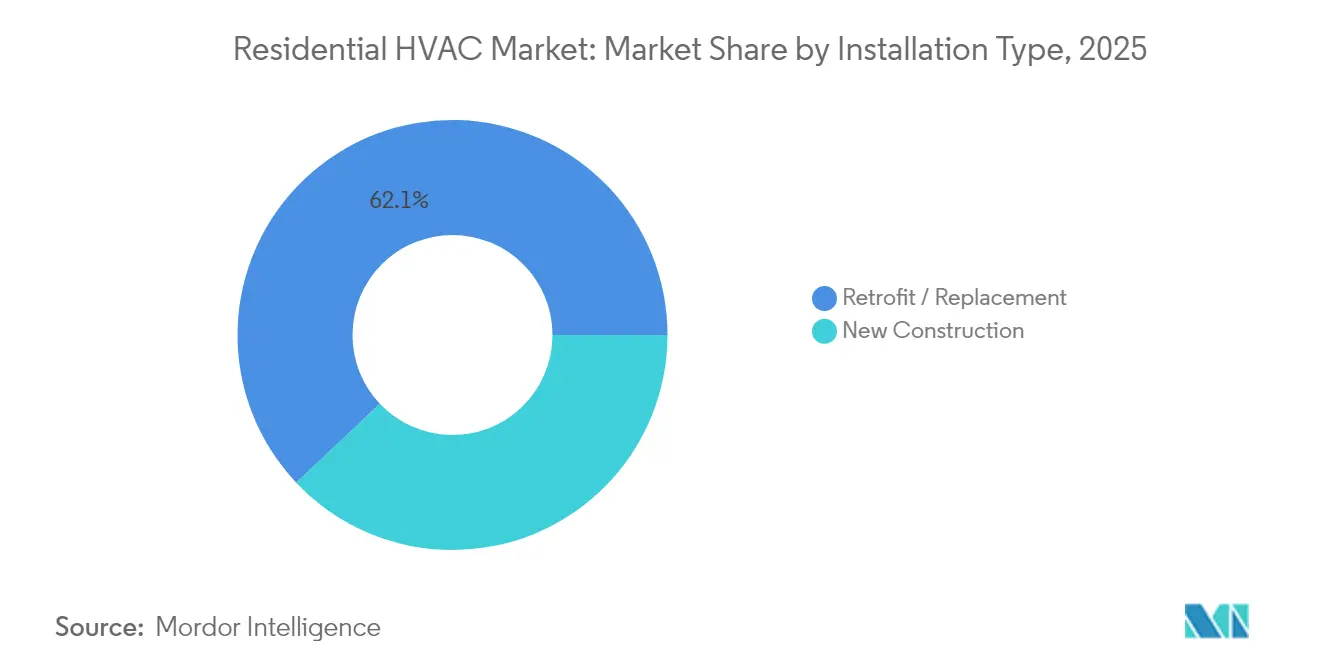

- By installation, retrofit and replacement commanded 62.05% residential HVAC market size in 2025. By installation, new-construction adoption is projected to increase at a 7.06% CAGR through 2031.

- By housing type, single-family homes captured 71.10% of residential HVAC market size in 2025. By housing type, multi-family dwellings are expected to advance at a 7.38% CAGR through 2031.

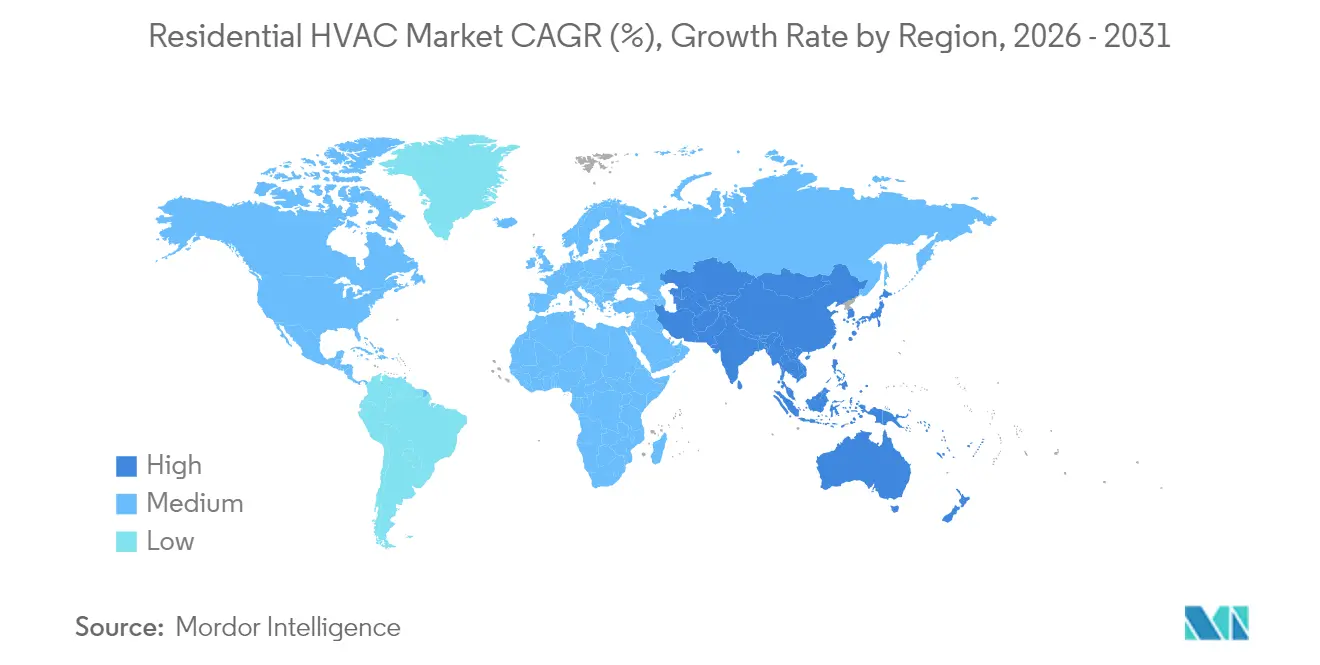

- By geography, North America commanded 37.55% revenue share in 2025; APAC is projected to record the quickest expansion at a 6.82% CAGR through 2031.

- Carrier, Trane, and Daikin collectively held an estimated 35-40% share of global 2024 shipments, reflecting a moderately consolidated field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Residential HVAC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decarbonisation mandates accelerating electric-heat-pump adoption | +1.5% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Shift toward inverter-driven variable-speed compressors | +1.8% | Global, led by Asia Pacific manufacturing | Long term (≥ 4 years) |

| Surge in home-improvement and retrofit cycles post-pandemic | +1.2% | North America and Europe core markets | Short term (≤ 2 years) |

| Growing penetration of smart thermostats and IoT-enabled HVAC controls | +0.8% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Grid-interactive efficient buildings (GEB) incentives from utilities | +0.4% | North America, pilot programs in EU | Long term (≥ 4 years) |

| Home electrification financing models (PACE, on-bill) gaining traction | +0.5% | North America, emerging in select EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Decarbonization Mandates Accelerating Electric-Heat-Pump Adoption

Federal tax incentives and state‐level building codes are pushing heat pumps into mainstream residential applications. California’s 2024 Title 24 requirements and Washington’s USD 14,000 rebates have slashed consumer payback periods, while the Inflation Reduction Act’s 30% credit offsets up-front costs by as much as 60%.[2]California Energy Commission, “Title 24 Building Energy Efficiency Standards,” energy.ca.gov Technology enhancements now enable operation down to –20 °F, allowing deployment in historically furnace-dominant northern markets. Multi-state procurement coalitions aggregate demand, reducing per-unit manufacturing costs. Combined federal, state, and utility programs create a layered incentive stack that positions heat pumps as lifecycle-cost-competitive with gas furnaces even where natural-gas tariffs remain low. Manufacturers are scaling cold-climate compressors to capture this expanding residential HVAC market opportunity.

Shift Toward Inverter-Driven Variable-Speed Compressors

Variable-speed compressors have migrated from premium to mainstream status, underpinning the next wave of efficiency gains in the residential HVAC market. Daikin’s joint venture with Copeland targets North American heat-pump applications, while Lennox’s SL22KLV achieves a 21.1 SEER2 rating through wide-range capacity modulation.[3]Lennox International, “Product Innovation and Development,” lennoxinternational.com Modulation between 25-100% reduces cycling losses, improves humidity control, and cuts energy use by 20-30% compared with single-stage units. China supplies more than 95% of global compressor output, granting OEMs early-access cost advantages. Utilities value equipment that can throttle demand in real time, enhancing homeowner earnings via emerging demand-response markets.

Surge in Home-Improvement and Retrofit Cycles Post-Pandemic

Retrofit projects dominate residential HVAC replacements as homeowners use accrued equity and tax credits to upgrade functional systems. Retrofit volume reached 62.52% of total shipments in 2024, reflecting loftier indoor-air-quality priorities and rising energy-efficiency awareness. Federal rebates and low-interest financing shorten payback horizons, prompting early retirement of aging R 410A systems. Comprehensive retrofits often bundle electric-service upgrades, elevating project values above USD 15,000 and encouraging heat-pump adoption in legacy housing stock. Widespread PACE programs encompassing 2,000 jurisdictions underpin capital access, spreading repayments across property-tax bills.

Growing Penetration of Smart Thermostats and IoT-Enabled HVAC Controls

Connected controls have reached roughly 40% of U.S. households, enabling remote diagnostics, predictive service alerts, and participation in demand-response tariffs. Carrier’s cloud platform links homeowner data to dealer networks, reducing service-call frequency and elevating customer retention. Smart scheduling and occupancy sensing cut energy bills by 10-15%, while utility programs offer USD 50-200 annual bill-credits for automated load-curtailment. Tech-sector entrants such as Google and Amazon now vie with incumbent OEMs for ownership of the residential energy interface, expanding competitive pressure across the residential HVAC market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in refrigerant regulations and phasedown schedules | -0.9% | Global, most acute in developed markets with strict EPA and F-Gas compliance | Short term (≤ 2 years) |

| Up-front cost premium of high-efficiency equipment | -0.6% | Global, varying by regional incentive availability and financing access | Medium term (2-4 years) |

| Skilled-labour shortage for proper installation and commissioning | -0.8% | North America and EU core markets, spreading to APAC urban centers | Medium term (2-4 years) |

| Electrical-service upgrade constraints in legacy housing stock | -0.5% | North America and Europe, concentrated in pre-1980 housing stock | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Refrigerant Regulations and Phasedown Schedules

EPA Technology Transition timelines require OEMs and contractors to juggle dual refrigerant inventories while navigating A2L safety protocols.[4]U.S. Environmental Protection Agency, “Technology Transition Rule,” epa.gov Divergent EU F-Gas rules amplify complexity, delaying product launches by up to 12 months under AHRI certification processes. The switch to R 32 or R 454B drives unit-level compliance costs of USD 500-1,000 for leak-detection hardware and technician training. Transitional uncertainty inflates consumer prices and strains supply chains, slowing early-cycle demand.

Up-Front Cost Premium of High-Efficiency Equipment

Cold-climate heat pumps command 40-60% premiums over conventional gas furnaces, with installed costs regularly topping USD 15,000 once electric-panel upgrades are included. Variable-speed compressors and advanced electronics remain supply-constrained, sustaining elevated component pricing. Labor shortages widen the cost gap: installer wages grew 15-20% year-over-year in 2024 across many metropolitan areas. Although lifecycle economics favor high-efficiency systems, budget limitations deter lower-income households absent robust incentive stacking.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment: Cooling Systems Drive Market Evolution

Cooling and ventilation captured 60.12% of 2025 revenue. Strong urbanization, warmer climate trends, and rising middle-class incomes in emerging economies continue to lift air-conditioning adoption. The residential HVAC market size for cooling equipment is projected to expand at a 6.98% CAGR through 2031 as variable-refrigerant flow and ductless mini-split platforms penetrate single-family retrofits and multi-family projects. Rooftop and packaged systems remain niche but serve manufactured housing and low-rise multi-family complexes where centralized maintenance offers cost advantages. Heating-equipment demand is undergoing a structural shift toward electric heat pumps, reinforced by decarbonization mandates. Cold-climate models now handle sub-zero temperatures, shrinking the addressable market for legacy gas furnaces. Furnaces still dominate replacement sales in regions with entrenched natural-gas infrastructure, but hybrid heat-pump/furnace installations are emerging as transitional solutions to meet efficiency codes while maintaining resilience.

The heating segment’s rapid transformation is directly tied to electrification policy stacking. Federal rebates equalize capital outlays between mid-tier heat pumps and gas furnaces, accelerating the share shift within the residential HVAC market. OEMs are reallocating R&D resources from condensing gas technology toward inverter-driven heat-pump platforms, anticipating cost parity within five years. Grid-interactive capabilities embedded in next-generation hydronic and forced-air heat pumps further differentiate these products, opening recurring revenue streams via demand-flexibility programs and extending value beyond upfront equipment margins.

By Technology: Low-GWP Transition Accelerates Innovation

Conventional R 410A and legacy R 22 units still represent 69.85% of the installed base, yet regulatory caps on production and imports are tightening supply and inflating service costs. The resulting scarcity is propelling accelerated retirement of aging systems, shifting replacement demand toward low-GWP alternatives. R 32’s 68% lower global-warming potential allows manufacturers to leverage existing production lines with minimal hardware changes, supporting smoother transitions and lighter bill-of-materials. R 454B introduces additional handling requirements but offers even lower GWP, aligning long-term compliance paths in the residential HVAC market.

Low-GWP refrigerant systems are forecast to post a 7.32% CAGR through 2031. OEMs are bundling these refrigerants with inverter drives, smart diagnostics, and cloud-integrated controls, elevating per-unit revenue. Enhanced sealing technology and lower charge volumes mitigate flammability concerns. As fixed-speed compressors decline, variable-speed adoption lifts average selling prices yet reduces lifecycle operational costs, dovetailing with both regulatory and homeowner economic priorities.

By Installation Type: New-Construction Standards Drive Efficiency

Retrofits account for 62.05% of current shipments, underscoring the scale of stock turnover in mature housing markets. Replacement cycles are being compressed by refrigerant phasedowns and compelling rebate structures, accelerating rollout of next-generation systems. The residential HVAC market share linked to retrofits benefits from homeowner demand for improved indoor air quality, comfort, and lower utility bills.

New-construction applications, although smaller, are projected to grow at a 7.06% CAGR. Title 24 in California mandates heat pumps in most new homes, and similar efficiency codes are advancing in other U.S. states and Canadian provinces. Builders leverage lower installation costs in new structures to integrate centralized ductless or hydronic heat-pump solutions, future-proofing properties against evolving code requirements. Smart wiring, thermal storage, and two-way communications hardware are easier to embed during construction, enhancing grid-interaction functionality that is more expensive to retrofit later.

By Housing Type: Multi-Family Electrification Gains Momentum

Single-family residences controlled 71.10% of the 2025 residential HVAC market size. Tax credits and streamlined contractor sales cycles reinforce this dominance. However, market saturation and slowing new-home construction push OEMs and contractors to develop tailored multi-family offerings.

Multi-family installations, growing at a 7.38% CAGR, benefit from density-driven economies of scale. Centralized heat-pump water-loop systems and packaged terminal heat pumps are replacing legacy steam or hydronic boilers in older apartment blocks. Local Law 97 compliance in New York City alone forces thousands of buildings to invest in HVAC electrification by 2031, opening a sizable pipeline for contractors. Green lending frameworks from Fannie Mae and Freddie Mac offer preferential financing for energy-efficient multi-family retrofits, improving project economics for property owners.

Geography Analysis

North America represented 37.55% of 2025 global revenue. Federal incentives under the Inflation Reduction Act, combined with state rebates, drove a 15% surge in U.S. heat-pump sales by November 2024. Canadian federal programs provide up to CAD 5,000 (USD 3,700) per installation, while provincial add-ons can double total rebate values. Mexico’s HVAC export output reached USD 7.6 billion in 2024, underscoring the region’s supply-chain integration. Single-family replacement demand remains vigorous, but multi-family electrification is accelerating as building performance standards tighten.

Asia Pacific is the fastest-growing region with a 6.82% CAGR through 2031. China accounts for roughly 30% of global heat-pump installations and controls more than 95% of compressor production capacity, enabling aggressive pricing and rapid product iterations. India’s rising middle-class and blistering urban heat islands propel air-conditioning shipments, while governmental Bureau of Energy Efficiency regulations drive new inverter adoption. Japan’s 2024 replacement market returned to 5% growth by year-end as pandemic backlogs cleared.

Europe faces near-term turbulence. Low natural-gas prices and construction slowdowns slashed first-half 2024 heat-pump sales by 50% in Germany. Yet REPowerEU’s target of 10 million additional residential heat pumps by 2027, supported by grants of EUR 3,000-15,000, is poised to restore double-digit growth from 2025 onward. The region’s retrofit potential remains vast as nearly three-quarters of building stock predates modern efficiency codes.

The Middle East and Africa exhibit cooling-dominant demand yet slower penetration of high-efficiency models due to subsidized electricity tariffs. Nevertheless, Gulf Cooperation Council utilities are piloting high-SEER rebate schemes to curb peak-season grid stress, signaling future upside for premium cooling products in the residential HVAC market.

Competitive Landscape

Global leadership is shared among Carrier, Daikin, Trane Technologies, Lennox International, Bosch, and Johnson Controls. Their combined 2024 shipment share approximated 40%, yielding a moderate concentration profile. Bosch’s USD 8 billion purchase of Johnson Controls’ residential HVAC division added 26,000 employees across 16 factories, positioning the company to integrate variable-speed heat-pump technology across European and North American portfolios. Trane’s collaboration with the U.S. Department of Energy on advanced commercial‐to‐residential heat-pump designs strengthens its cold-climate credentials.

Distribution consolidation intensifies bargaining power: Watsco and Ferguson expanded acquisition pipelines, while private-equity investors aggregate regional contractors into multi-state platforms to secure parts availability and negotiate OEM volume discounts. Product differentiation increasingly pivots on software ecosystems, predictive maintenance algorithms, and integration with home-energy–management platforms rather than purely thermodynamic efficiency metrics. Firms that embed secure over-the-air updates and monetizable grid-services APIs stand to capture recurring revenue and long-term customer loyalty within the residential HVAC market.

OEM strategies also prioritize refrigerant readiness. Carrier’s refrigerant-agnostic coil designs and Lennox’s R 454B-ready side-discharge products enable smoother inventory transitions amid phasedown uncertainty. Competitive advantage accrues to players that de-risk regulatory timelines and alleviate installer training burdens through modular service platforms and augmented-reality support tools.

Residential HVAC Industry Leaders

Daikin Industries, Ltd.

Midea Group Co., Ltd.

Gree Electric Appliances, Inc.

Trane Technologies plc

Carrier Global Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Lennox launched the Elite Series EL18KSLV side-discharge heat pump for space-constrained urban homes, featuring cold-climate performance down to –15 °F and enhanced grid-interactive controls.

- June 2025: Lennox and Ariston Group formed a joint venture to co-develop high-efficiency residential water-heating products for the North American market.

- January 2025: Bosch finalized its USD 8 billion acquisition of Johnson Controls’ global residential and light commercial HVAC assets, creating a combined operation exceeding EUR 9 billion in annual sales and strengthening its presence in North America and Europe.

- February 2024: Comfort Systems USA acquired J & S Mechanical Contractors, adding USD 150 million in annual revenue and expanding service capacity in the Mountain West region.

Global Residential HVAC Market Report Scope

The residential heating, ventilation, and air conditioning (HVAC) systems are used for air handling and thermal comfort for residents. The market study covers heating, air conditioning, and ventilation equipment such as heat pumps, VRF, Single Splits and multi-splits, and air handling units.

The Residential HVAC market is segmented by equipment (air conditioning/ventilation equipment (type (single splits/multi splits(ducted/ductless), vrf, air handling units, other types [fan coils, rooftops, etc.])) and heating equipment (type (boilers/radiators/furnaces & other heaters, heat pumps)) and by geography (North America [United States, Canada], Europe [United Kingdom, Italy, Germany, France, Spain, Eastern Europe, Benelux, Nordics, Rest of Europe], Asia Pacific [China, India, Japan, Rest of Asia Pacific], Latin America, Middle East & Africa). The report offers the market size in value terms in USD for all the abovementioned segments.

| Cooling and Ventilation Equipment | Ducted Split Systems |

| Ductless Split Systems | |

| VRF Systems | |

| Air-Handling Units | |

| Rooftops and Fan-Coils | |

| Heating Equipment | Furnaces and Boilers |

| Heat Pumps |

| Conventional (R410A/R22) |

| Low-GWP Refrigerants (R32, R454B, CO₂, Propane) |

| Fixed-speed |

| Inverter / Variable-speed |

| Smart / Connected |

| New Construction |

| Retrofit / Replacement |

| Single-family Homes |

| Multi-family Apartments and Condominiums |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Benelux | ||

| Eastern Europe | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Equipment | Cooling and Ventilation Equipment | Ducted Split Systems | |

| Ductless Split Systems | |||

| VRF Systems | |||

| Air-Handling Units | |||

| Rooftops and Fan-Coils | |||

| Heating Equipment | Furnaces and Boilers | ||

| Heat Pumps | |||

| By Technology | Conventional (R410A/R22) | ||

| Low-GWP Refrigerants (R32, R454B, CO₂, Propane) | |||

| Fixed-speed | |||

| Inverter / Variable-speed | |||

| Smart / Connected | |||

| By Installation Type | New Construction | ||

| Retrofit / Replacement | |||

| By Housing Type | Single-family Homes | ||

| Multi-family Apartments and Condominiums | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Benelux | |||

| Eastern Europe | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| ASEAN | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the residential HVAC market?

The residential HVAC market size reached USD 88.11 billion in 2026.

How fast is the global residential HVAC market expected to grow?

It is projected to register a 6.24% CAGR, reaching USD 119.26 billion by 2031.

Which equipment segment leads revenue?

Cooling and ventilation equipment held 60.12% of 2025 revenue.

Which region is the fastest-growing for residential HVAC adoption?

Asia Pacific is forecast to grow at a 6.82% CAGR through 2031.

What technology trend is shaping future product design?

Low-GWP refrigerants paired with inverter-driven variable-speed compressors are accelerating innovation.

How are utilities influencing residential HVAC purchases?

Time-of-use rates and demand-response incentives reward homeowners who install grid-interactive heat pumps and smart controls.

Page last updated on: