Residential Air To Water Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

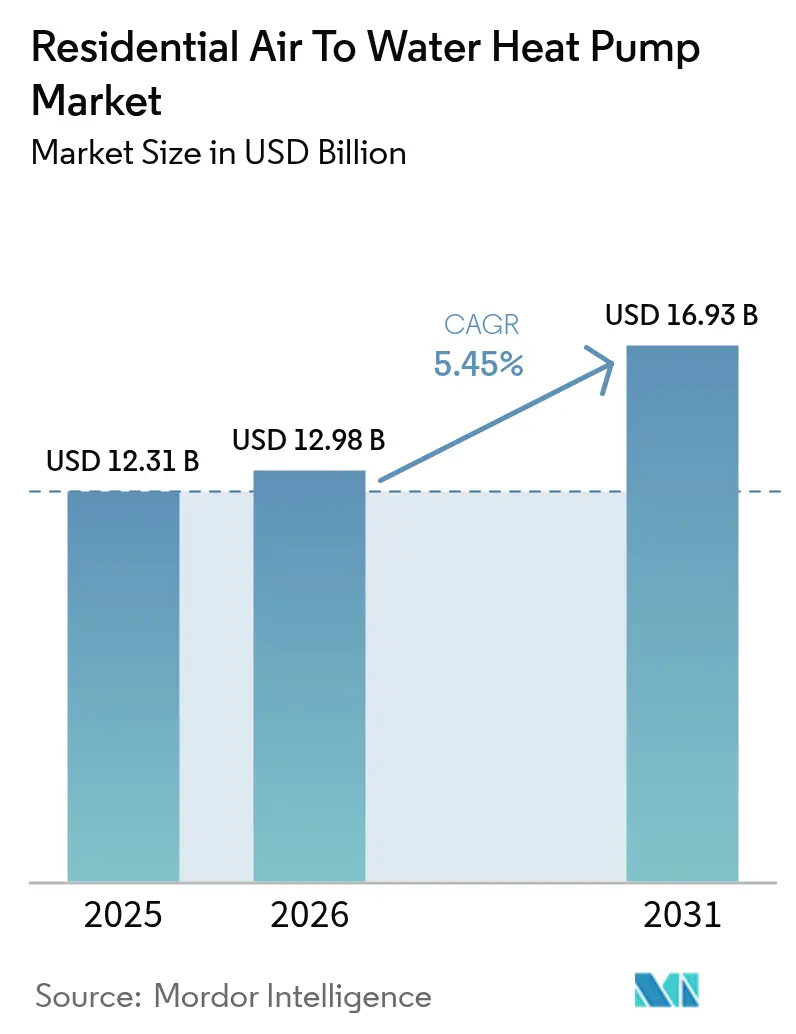

| Market Size (2026) | USD 12.98 Billion |

| Market Size (2031) | USD 16.93 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Residential Air To Water Heat Pump Market Analysis by Mordor Intelligence

The residential air-to-water heat pump market size is expected to grow from USD 12.31 billion in 2025 to USD 12.98 billion in 2026 and is forecast to reach USD 16.93 billion by 2031 at 5.45% CAGR over 2026-2031. Rising policy pressure to decarbonize home heating, widening total cost-of-ownership advantages over gas boilers, and generous fiscal incentives are propelling this residential air-to-water heat pump market toward mainstream adoption. Manufacturers are scaling local component plants while natural-refrigerant models meet tightening F-Gas rules and improve seasonal COP. Hybrid configurations gain early favor because they reassure homeowners of fallback capacity during extreme cold, yet performance gains in inverter-driven units are narrowing that perceived reliability gap. Bottlenecks remain—grid interconnection queues in dense suburbs, installer shortages and municipal noise ordinances on outdoor units—but none appear large enough to derail the long-run trajectory of this residential air to water heat pump market.

Key Report Takeaways

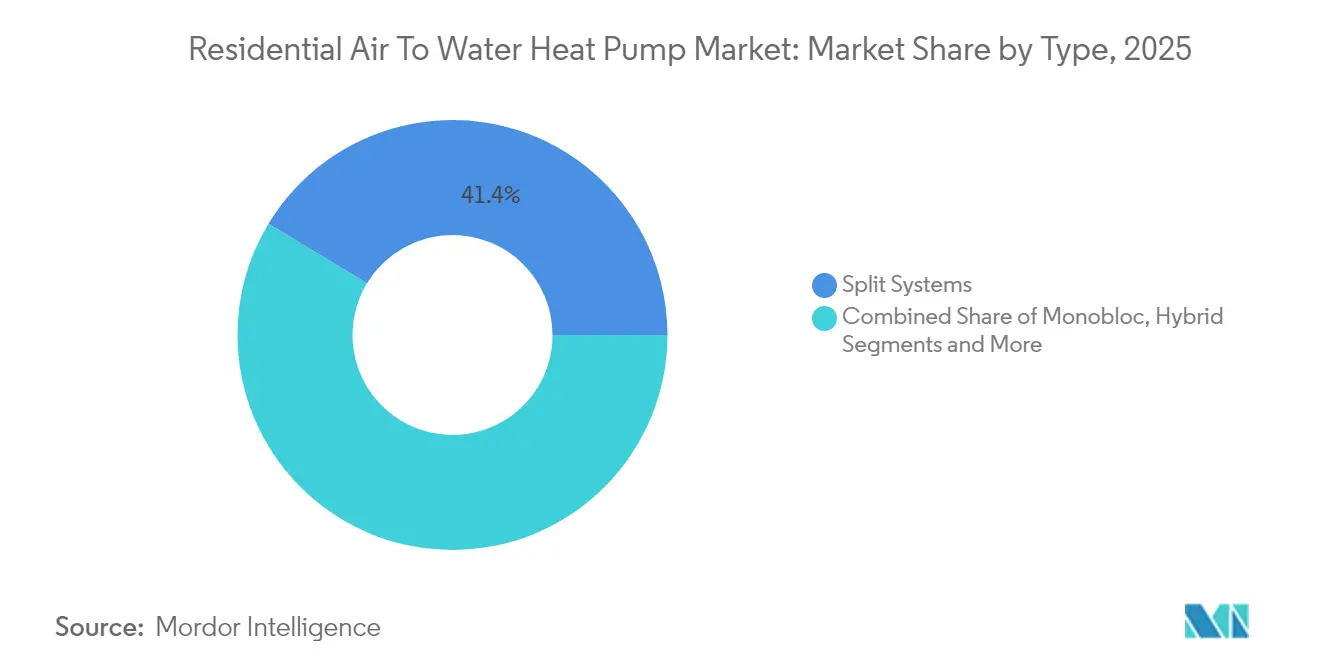

- By type, split systems led with 41.35% revenue share in 2025; hybrid combinations are projected to grow at a 8.83% CAGR through 2031.

- By capacity, < 10 kW units captured 54.30% of the residential air to water heat pump market share in 2025, while > 20 kW systems are set to expand at an 8.14% CAGR to 2031.

- By application, single-family homes accounted for 67.40% share of the residential air to water heat pump market size in 2025; multi-family residences are advancing at a 7.28% CAGR through 2031.

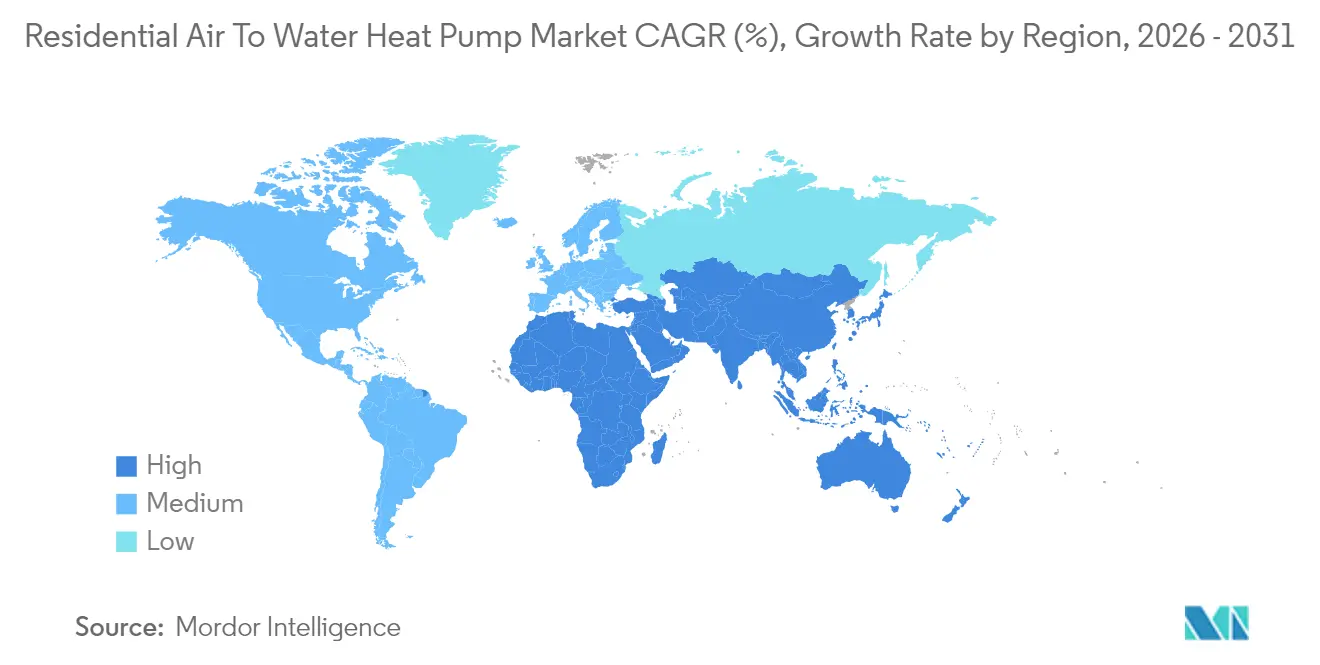

- By geography, Europe commanded 33.60% share in 2025; the Middle East is the fastest-growing region at 7.82% CAGR to 2031.

- Carrier’s acquisition of Viessmann Climate Solutions, Daikin, Mitsubishi Electric, Bosch and Trane collectively held about 48% of global shipments in 2024, underscoring moderate concentration in the residential air to water heat pump market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Residential Air To Water Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| EU-wide ban on fossil-fuel boilers accelerating heat-pump retrofits | +1.2% | Europe, with spillover to UK and Norway | Medium term (2-4 years) |

| Post-Ukraine gas-price volatility widening TCO gap in Europe | +0.8% | Europe, particularly Germany and Netherlands | Short term (≤ 2 years) |

| U.S. Inflation Reduction Act rebates for ≥15 SEER heat pumps | +0.9% | North America, primarily United States | Medium term (2-4 years) |

| Low-GWP R290 / R32 models easing F-Gas Phase-Down compliance | +0.6% | Global, with early adoption in Europe and Japan | Long term (≥ 4 years) |

| Inverter compressors lifting seasonal COP in sub-zero climates | +0.7% | Northern Europe, Canada, Northern US states | Long term (≥ 4 years) |

| Rooftop solar parity unlocking self-consumption heating in China | +0.5% | APAC core, particularly China and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU-wide ban on fossil-fuel boilers accelerating heat-pump retrofits

Mandatory phase-outs that start in 2025 for new homes and extend to replacements by 2040 remove any remaining ambiguity over the preferred hydronic heating solution. This hard deadline locks in multi-decade demand for air-to-water units able to deliver high flow temperatures via existing radiators. Subsidies covering up to 30% of installed cost in markets such as the Netherlands sweeten the economics for homeowners. Instead of sporadic incentive spikes, a predictable compliance calendar now guides OEM capacity planning and distributor stocking levels. The policy also shortens payback periods because gas-boiler replacements face higher carbon levies each year. Taken together, the measure pushes the residential air to water heat pump market toward default-technology status across Europe.[1]Bricknest, “New Rules for Heat Pumps in the Netherlands 2025-2026,” bricknest.nl

Post-Ukraine gas-price volatility widening TCO gap in Europe

Spot gas prices across northwest Europe ran three times above the pre-2022 average, tilting lifetime costs sharply in favor of heat pumps. Government analysis shows German households can cut annual heating bills by up to 60% after switching. Such savings resonate with middle-income owners who previously viewed heat pumps as a green luxury. Volatility is structural, not cyclical, because EU energy policy seeks permanent diversification away from pipeline gas. That dynamic deepens the comparative advantage of the residential air to water heat pump market every winter.

US Inflation Reduction Act rebates for ≥ 15 SEER heat pumps

Income-based rebates of up to USD 8,000 offset upfront premiums and unlock demand in states with modest heating loads where air-to-water solutions historically struggled to compete. The multiyear window gives manufacturers certainty to localize production, as shown by Mitsubishi Electric’s USD 143.5 million compressor plant in Kentucky. Aggregated rebate pipelines also create contiguous clusters of installs that cut logistics and training costs, helping the residential air to water heat pump market gain critical mass in North America.

Low-GWP R290 / R32 models easing F-Gas phase-down compliance

From January 2025, the EU bars refrigerants above 750 GWP in new hydronic systems. R290’s GWP of 20 and efficiency boost of 5-10% position adopters to capture share. Panasonic and Vaillant already sell propane-charged lines, signalling a wider portfolio migration. Early movers gain first-mover loyalty among installers, and they insulate themselves from future price shocks on legacy refrigerants. Consequently, regulatory alignment and performance gains combine to reinforce demand in the residential air to water heat pump market.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Grid-capacity caps delaying hook-ups in dense EU suburbs | -0.4% | Europe, particularly Germany and Netherlands | Short term (≤ 2 years) |

| Shortage of hydronic-skilled installers inflating labor cost | -0.6% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Urban noise-regulation setbacks on outdoor-unit placement | -0.2% | Global urban centers, particularly Asia-Pacific | Long term (≥ 4 years) |

| Consumer preference for gas boilers in East-Asian multi-family | -0.3% | APAC, particularly Japan and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-capacity caps delaying hook-ups in dense EU suburbs

Distribution feeders built for low electrification levels face sharp peak-load jumps as entire streets add 6-10 kW units. Germany’s 500,000-unit annual target could raise peak winter demand by 10 GW, forcing utilities to triage connections. Rural tie-in fees climb above EUR 1,200 per dwelling, while urban districts fare better. This mismatch slows early-stage volumes for the residential air to water heat pump market in grid-constrained neighbourhoods until reinforcement work catches up.[2]Clean Energy Wire, “Heat Pump Installation Plans May Overburden Germany’s Grid,” cleanenergywire.org

Shortage of hydronic-skilled installers inflating labor cost

Training throughput is rising—UK certifications grew 166% in 2024—but remains well short of policy targets. Poorly balanced loops or undersized buffer tanks cut expected COP and risk reputational damage. North American utilities sponsor six-month boot camps, yet workforce gaps linger because plumbing apprenticeships take years. Elevated labor premiums add 15-20% to final invoices, tempering the residential air to water heat pump market’s price competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type – Hybrid systems extend reliability perception

Split units held 41.35% of revenue in 2025 as installers value familiar component layouts that mirror legacy boiler circuits. That dominance translates into a sizeable slice of the residential air to water heat pump market. Hybrid pump-and-boiler packages, however, are racing ahead at a 8.83% CAGR as households want backup combustion during polar cold snaps. The segment’s growth reflects behavioral risk aversion more than technical necessity, because modern R290 models sustain 65 °C supply water at -20 °C ambient. Over time, as field data validates pure-pump reliability, hybrid appeal is likely to plateau. Monobloc and all-in-one variants court space-constrained retrofits, adding useful breadth to this residential air to water heat pump market.

Split offerings benefit from mass-production economics that compress hardware costs, keeping entry prices competitive. Conversely, hybrids command premium pricing but deliver perceived peace of mind, a value proposition resonating in cold continental climates. OEMs are bundling connected thermostats and intelligent switchover algorithms to optimize operating points automatically. This software layer differentiates brands and nudges the residential air to water heat pump industry toward service-centric revenue streams.

By Capacity – Large residential blocks unlock scale economies

< 10 kW units represented 54.30% of installs in 2025, a natural fit for typical detached homes. At the other end, > 20 kW machines posted the quickest 8.14% CAGR as developers of multi-dwelling blocks and luxury residences opt for central plants. That surge means the > 20 kW slice of the residential air to water heat pump market size could double by 2031. Viessmann’s 40 kW Vitocal 250-A PRO illustrates how high-output propane units tackle older buildings where radiator delta-T demands are high.

Systems in the 10-20 kW tier bridge suburban villas and small apartment houses. As carbon caps tighten, this mid-range is broadening fastest in France, Italy and parts of Canada. With flow temperatures climbing to 70 °C, the capacity brackets converge, raising questions about future segmentation relevance. Nevertheless, installer workflows, refrigerant charge limits and grid-connection forms still differ enough to keep the capacity bands meaningful within the residential air to water heat pump market.

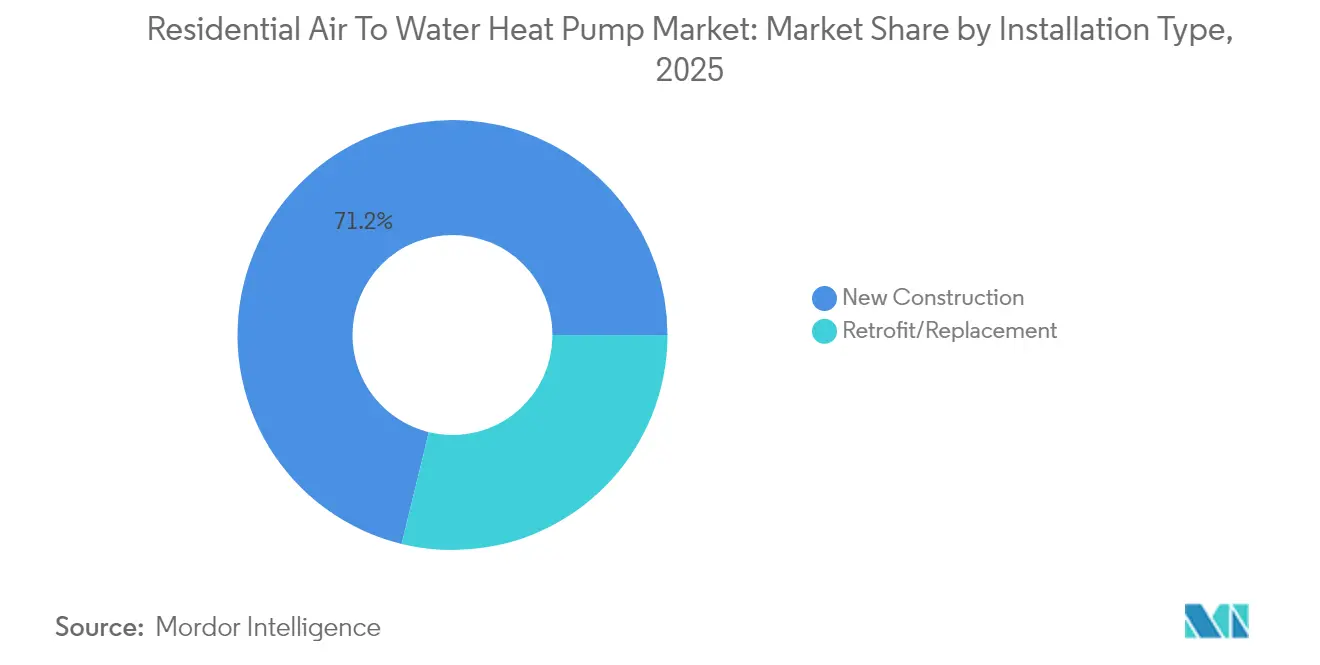

By Installation Type – New construction dominates early roll-outs

New builds accounted for 71.20% of 2025 shipments, reflecting the ease of integrating hydraulic loops and buffer tanks when architects can design around the equipment footprint at the blueprint stage. Most European building codes now require renewable primary heating; the UK’s Future Homes Standard, effective 2025, obliges heat-pump installation in every new dwelling. Forward-planning lets developers right-size emitters, minimise flow temperatures and optimise pump COP from day one, raising the share of the residential air to water heat pump market secured at the planning-permission stage.

Retrofit and replacement work makes up the remaining 28.80% but will grow faster once ageing boilers reach end-of-life and subsidy schemes sweeten paybacks. Hybrid kits and monobloc chassis simplify change-outs because installers can hook units onto existing radiator circuits without rewiring the entire home. Municipal grant programmes in Germany and France now cover up to EUR 9,000 of retrofit cost, narrowing the up-front gap with gas-boiler swaps. As component prices fall and workforce skills deepen, retrofit volume is expected to close the sales gap with new-builds after 2028, broadening the addressable residential air to water heat pump market while relieving cyclical dependence on the construction sector.

By Refrigerant – Propane (R290) leads the low-GWP shift

R410A still equips most legacy models because of supply-chain familiarity, but its >2,000 GWP rating brings phase-down risk and future servicing costs. From January 2025 the EU bans refrigerants above 750 GWP in new hydronic systems, accelerating the pivot toward R32 (GWP 675) and, more decisively, R290 with a GWP of 20. Early adopters such as Vaillant and Panasonic report 5-10% seasonal COP gains from higher latent-heat capacity in propane charge, creating both compliance and efficiency upside for the residential air to water heat pump market.

CO₂ (R744) is carving out a niche in multi-family blocks demanding 80 °C domestic-hot-water service, while next-gen magnetocaloric units in laboratory trials hint at a refrigerant-free future. Safety codes now permit up to 1 kg of propane under EN 378 when the outdoor unit sits outside the building envelope, alleviating earlier flammability concerns. Component vendors are scaling hermetically sealed compressors, and charge-reduction heat-exchanger designs keep hydrocarbon mass below critical thresholds. As a result, R290 models are forecast to lift their slice of the residential air to water heat pump market size to 46.70% by 2031, overtaking both R410A and R32 in mainstream volume sales.

Geography Analysis

Europe retained 33.60% of global revenue in 2025 thanks to dense hydronic infrastructure and aggressive carbon policy. Nevertheless, macro headwinds and regulatory ambiguity shaved 22% off unit sales during 2024. National subsidy resets in France and Italy weighed on consumer sentiment, illustrating policy sensitivity inside the residential air to water heat pump market. Still, Brussels sees 60 million cumulative European installs as a 2030 milestone, implying a steep climb from today's base.

North America rebounded late-2024 with a 15% jump in shipments. Federal and state rebate stacks have pushed total incentives toward USD 10,000 in some ZIP codes, driving momentum in the residential air to water heat pump market. Local content rules are re-shaping supply chains; for example, the new Kentucky compressor plant will cut lead times by 30%. Canadian provinces add cold-climate tiers that spur R&D on vapor-injection compressors, raising seasonal efficiencies in frigid Prairies.

Asia-Pacific posts the fastest 7.82% CAGR led by China’s scale and rising electrification quotas. Domestic producers shipped 13% more units in 2024, even as export orders softened, highlighting robust internal momentum. The Middle East, while small today, matches that 7.82% growth rate as district-cooling operators retrofit reversible water-loop systems for winter service. Japan and South Korea remain technologically advanced but culturally attached to gas boilers in multi-family blocks, explaining a more modest uptake pace in that slice of the residential air to water heat pump market.

Competitive Landscape

Competition is moderate: the top five vendors hold around 48% of shipments, signalling neither monopoly nor fragmentation. Carrier’s USD 13 billion Viessmann deal accelerates portfolio diversification toward hydronic solutions, while Bosch’s USD 8 billion purchase of Johnson Controls-Hitachi expands Asian reach. Daikin, long the global share leader, earmarks 30% European share by 2030 through expanded Polish and Czech plants.

Technological differentiation revolves around refrigerant choice, acoustic engineering and control ecosystems. Mitsubishi Electric leans on variable-speed compressor IP, now being localized in the United States. Trane and LG stress low-GWP credentials, securing early procurement preferences from green-mortgage lenders. Vaillant adds installer apps and predictive diagnostics, shifting value toward after-sales services within the residential air to water heat pump industry.

Strategic moves include capacity build-outs—Aira’s EUR 300 million Polish factory can output 500,000 units annually—and vertical integration into compressors and electronics to hedge component risk. Some players explore magnetocaloric prototypes that could eliminate synthetic refrigerants entirely, signalling disruptive potential beyond 2030. Private equity interest is rising in mid-tier regional assemblers, suggesting continued consolidation across the residential air to water heat pump market.

Residential Air To Water Heat Pump Industry Leaders

-

Daikin Industries Ltd

-

Mitsubishi Electric Europe B.V

-

Panasonic Corp.

-

Vaillant Group

-

NIBE Industrier AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vaillant showcased updated residential air-to-water heat pump portfolio at ISH 2025 featuring natural refrigerant R290, quiet operation technology, and iQconnect electronic platform for simplified residential installation and operation, targeting both new and existing residential building applications.

- April 2025: Mitsubishi Electric Trane HVAC US unveiled residential air-to-water heat pumps utilizing low global warming potential refrigerant R-454B, featuring GWP nearly 78% lower than R-410A and enhanced cold climate heating performance with advanced connectivity features for residential applications.

- March 2025: LG Electronics won 2025 AHR Innovation Award for residential cold climate air-to-water heat pump, recognizing advancements in residential heating technology and demonstrating continued innovation in extreme weather performance for residential applications.

- February 2025: Carrier launched Domestic Hot Water Air-to-Water Heat Pump at International Builders' Show, marking entry into residential AWHP market in North America with sustainable solution achieving COP up to 4.9 and featuring lower GWP refrigerants for residential applications.

Global Residential Air To Water Heat Pump Market Report Scope

Air-to-water heat pumps can provide adequate heating and cooling for houses, particularly in a moderate climate. After proper installation, an air-to-water heat pump can give one and a half to three times more thermal energy to a home than the electricity it uses. Air-to-water heat pumps do not work very well under freezing temperatures. Air-to-water heat pumps specially designed for cold climates have started to provide encouraging results.

The residential air-to-water heat pumps are segmented by geography (United States, China, France, Italy, and the Rest of the World). The market also includes an assessment of the impact of COVID-19 on the market. For each segment, the market sizing and forecasts have been provided on the basis of value (in USD million) and volume (in metric tons).

| Split Systems |

| Monobloc Systems |

| All-in-One Integrated |

| Hybrid (HP + Boiler) |

| Less than 10 kW |

| 10 - 20 kW |

| Greater than 20 kW |

| R410A |

| R32 |

| R290 (Propane) |

| CO2 (R744) |

| Single-Family Homes |

| Multi-Family Residences |

| New Construction |

| Retrofit / Replacement |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Italy | |

| United Kingdom | |

| Spain | |

| Rest of Europe | |

| Middle East | UAE |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Australia | |

| India | |

| Rest of Asia-Pacific |

| By Type | Split Systems | |

| Monobloc Systems | ||

| All-in-One Integrated | ||

| Hybrid (HP + Boiler) | ||

| By Capacity (kW) | Less than 10 kW | |

| 10 - 20 kW | ||

| Greater than 20 kW | ||

| By Refrigerant | R410A | |

| R32 | ||

| R290 (Propane) | ||

| CO2 (R744) | ||

| By Application | Single-Family Homes | |

| Multi-Family Residences | ||

| By Installation Type | New Construction | |

| Retrofit / Replacement | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| United Kingdom | ||

| Spain | ||

| Rest of Europe | ||

| Middle East | UAE | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Australia | ||

| India | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current size of the residential air to water heat pump market?

The market is valued at USD 12.98 billion in 2026 and is projected to reach USD 16.93 billion by 2031.

Which region leads global demand for residential air-to-water units?

Europe holds 33.60% of global revenue, driven by mature hydronic infrastructure and strict decarbonization policy.

Why are hybrid heat pump and boiler systems growing so quickly?

They address homeowner concerns about backup heating during extreme cold and are expanding at a 8.83% CAGR through 2031.

How do government incentives affect adoption in North America?

US Inflation Reduction Act rebates of up to USD 8,000 remove upfront cost barriers, spurring a double-digit rebound in 2024 sales.

What role do natural refrigerants play in future growth?

R290 and R32 models meet upcoming F-Gas limits and improve efficiency, positioning early adopters for regulatory compliance and market share gains.

What challenges could slow near-term expansion?

Grid capacity constraints in dense suburbs and shortages of hydronic-skilled installers can delay projects and inflate costs, trimming the forecast CAGR by about 1 percentage point combined.

Page last updated on: