North America Unitary Heater Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

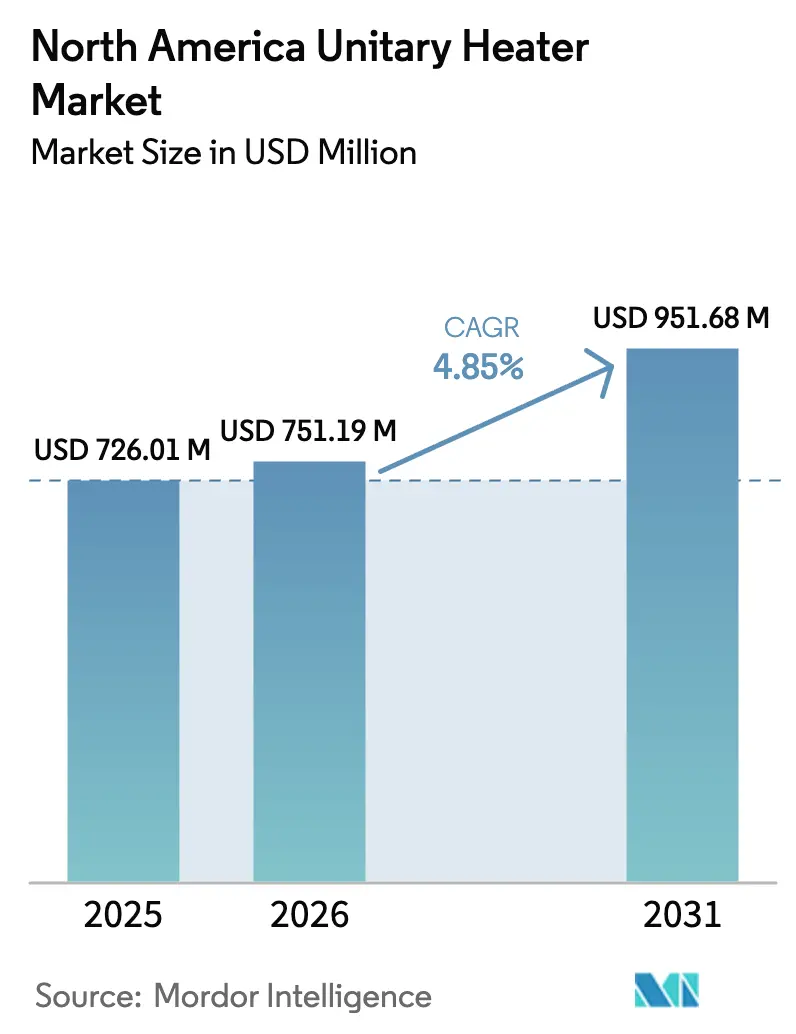

| Base Year Market Size (2025) | USD 726.01 Million |

| Market Size (2026) | USD 751.19 Million |

| Market Size (2031) | USD 951.68 Million |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

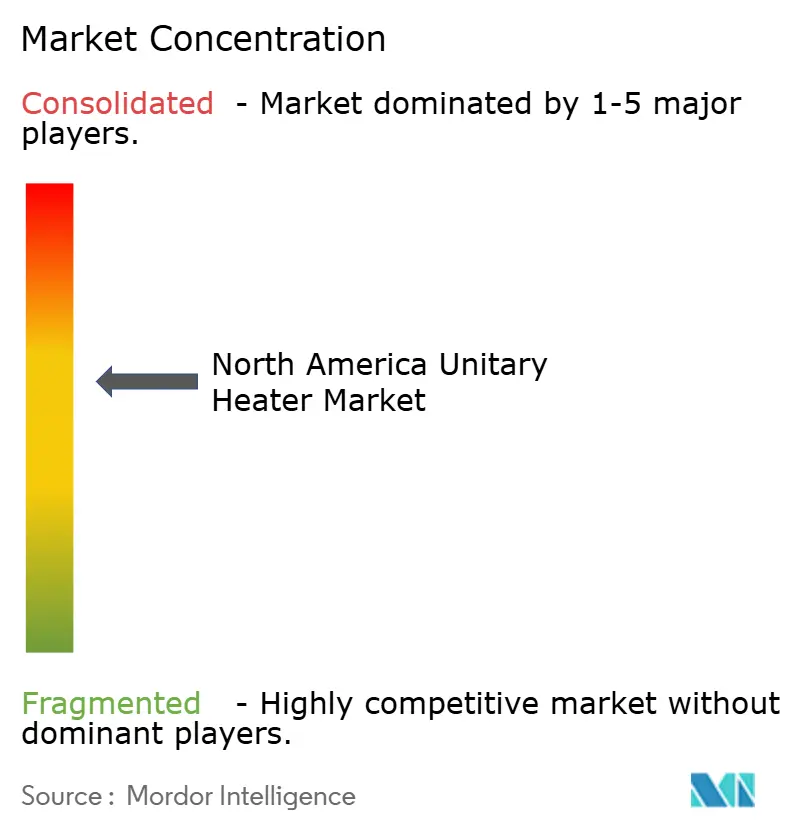

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Unitary Heater Market Analysis by Mordor Intelligence

The North America unitary heater market size was valued at USD 726.01 million in 2025 and is estimated to grow from USD 751.19 million in 2026 to reach USD 951.68 million by 2031, at a CAGR of 4.85% during the forecast period (2026-2031). Strong warehouse construction, federal and state electrification incentives, and breakthroughs in cold-climate heat pumps are reshaping end-user preferences across industrial, commercial, and residential segments. Gas-fired systems keep dominance through favorable fuel costs and rapid heat delivery in large footprints, yet steady policy pressure is channeling capital toward high-efficiency condensing models and electric infrared units. At the same time, e-commerce fulfillment enlarges the base of suspended heaters in high-bay buildings, while portable and wall-mounted formats gain traction in garages and small shops. Competitive intensity is rising as legacy combustion specialists integrate controls and IoT features to defend share against electric-heating entrants.

Key Report Takeaways

- By product type, gas-fired heaters led the North America unitary heater market with 63.42% share in 2025, whereas electric heaters are projected to advance at a 5.77% CAGR through 2031.

- By installation type, suspended systems captured 38.89% revenue share in 2025, while wall-mounted and portable units are forecast to post a 5.49% CAGR through 2031.

- By application, warehouses and distribution centers held 41.32% of market share in 2025 and are on track for a 5.34% CAGR to 2031.

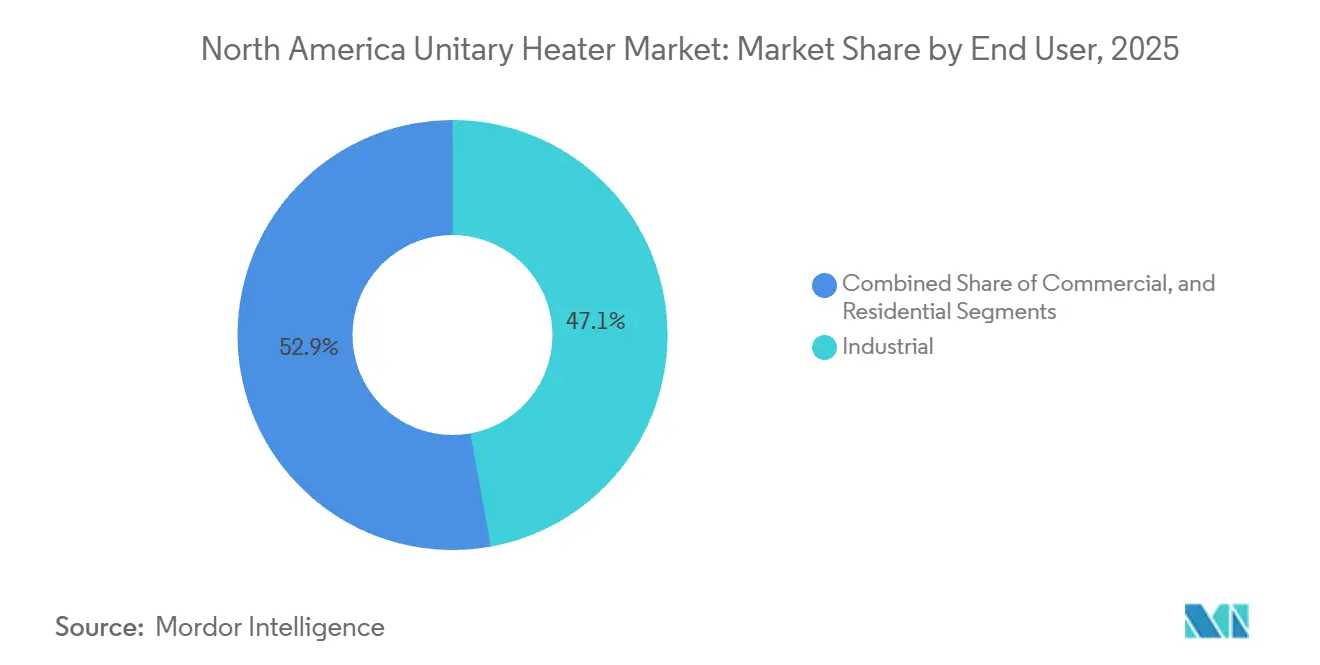

- By end user, industrial facilities accounted for 47.14% of the share in 2025, yet commercial buildings are the fastest mover with a 6.01% CAGR over the outlook period.

- By distribution channel, HVAC distributors maintained a 52.75% share in 2025, whereas online retail is set to expand at a 5.82% CAGR through 2031.

- By country, the United States commanded 78.64% of demand in 2025, while Mexico represents the quickest expansion at a 6.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Competitive positioning in North america includes both locally based firms and those operating across multiple regions. The market landscape in the global unitary heater industry research shows how these players are arranged internationally.

North America Unitary Heater Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Energy-Efficient Unit Heaters | +1.2% | United States, Canada | Medium term (2-4 years) |

| Growth of Warehouse and Logistics Infrastructure | +1.5% | United States, Mexico, Canada | Short term (≤ 2 years) |

| Regulatory Incentives for High-Efficiency Heating Technologies | +0.9% | United States, Canada | Long term (≥ 4 years) |

| Electrification Trend and Shift Toward Low-Carbon Heating | +1.1% | United States, Canada with spillover to Mexico | Long term (≥ 4 years) |

| Integration of Smart Controls and IoT in Building Heating Systems | +0.6% | United States, Canada | Medium term (2-4 years) |

| Rise of Cold-Climate Heat Pump Innovation for Northern States | +0.4% | United States (northern states), Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of Warehouse and Logistics Infrastructure

Automated fulfillment and cold-chain expansion are fueling large purchase orders for high-capacity suspended heaters capable of maintaining tight temperature bands in facilities exceeding 500,000 square feet. Lineage Logistics alone placed equipment orders after committing USD 1 billion to add 50 million cubic feet of refrigerated space, specifying gas-fired units with modulating burners that handle −20 °F to 35 °F zones. Similar buildouts by Americold and regional third-party logistics operators have shifted purchasing from central hydronic systems to flexible unitary designs that reduce downtime during 24/7 operations. New nearshoring plants in Mexico further enlarge addressable volume, illustrated by Tesla’s Nuevo León Gigafactory, which installed 200 suspended units for final-assembly climate control. Suppliers that bundle integrated controls and destratification fans, such as Trane’s 2024-launched ARU series, now win a growing share of bid lists. As e-commerce parcel throughput rises, regional developers favor pre-engineered heater layouts that scale quickly across multistate footprints, sustaining elevated order books through 2027.

Increasing Demand for Energy-Efficient Unit Heaters

Federal appliance standards that took effect in 2024 raised minimum efficiencies for commercial warm-air furnaces to 90%, essentially phasing out legacy non-condensing gas units in new construction. In response, manufacturers now ship condensing models with heat exchangers in stainless steel and control boards that adjust firing rates in 5% steps, trimming cycling losses by up to 20%. Electric infrared options add a zero-flue-loss pathway, directing heat to occupied zones and cutting warm-up times in high-ceiling warehouses. The American Council for an Energy-Efficient Economy determined that 27-60% of U.S. commercial floor space can electrify space heating at paybacks below seven years once Inflation Reduction Act deductions of up to USD 5 per square foot are considered.[1]American Council for an Energy-Efficient Economy, “Commercial Building Electrification Potential Study,” aceee.org Combined with renewable-heavy power grids in the West, that economics shift accelerates electric conversion programs among distribution centers and grocery chains.

Regulatory Incentives for High-Efficiency Heating Technologies

Section 25C and Section 179D tax credits slice upfront costs for owners adopting condensing gas furnaces or heat pumps, delivering 20-30% capital relief and, in many cases, immediate expensing on retrofit work.[2]Internal Revenue Service, “Section 179D Energy-Efficient Commercial Buildings Deduction,” irs.gov California’s Self-Generation Incentive Program added USD 150 million of carve-outs in 2024, driving subsidy checks of up to USD 3,500 per commercial unit. Natural Resources Canada mirrors that approach, funding 25% of project costs for heat-pump retrofits in public facilities. Together, these grants crowd-in private capital, shorten payback horizons, and make premium-efficiency models the default specification in RFPs for office renovations, municipal buildings, and data centers. As programs lock in through 2032, they underpin a predictable demand floor for both combustion and electric product lines.

Electrification Trend and Shift Toward Low-Carbon Heating

Local Law 97 in New York City sets building-level carbon caps that effectively prohibit new on-site combustion without offsets, penalizing non-compliance at USD 268 per metric ton of CO2e. Similar rules in Seattle and Denver plus corporate net-zero commitments are tipping procurement toward resistance heaters and, increasingly, cold-climate heat pumps. The Department of Energy’s Electrification Roadmap targets 5 million residential heat-pump installs per year by 2030, implying a wholesale migration away from fossil heat in moderate regions. Progress on vapor-injection compressors now allows coefficients of performance of 2.5 at −15 °F, removing a historic barrier in northern states and Canadian provinces. Manufacturers such as Rheem and Daikin expect commercial releases by 2026, amplifying competitive pressure on mid-floor gas units. Facility owners weigh operating-cost volatility in natural-gas markets against stable electricity contracts, favoring dual-fuel or all-electric pathways when tariffs permit.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Natural Gas and Electricity Prices | -0.8% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Stringent Emission Standards Increasing Compliance Costs | -0.6% | United States, Canada | Medium term (2-4 years) |

| Competition from Alternative Heating Technologies | -0.4% | United States, Canada | Long term (≥ 4 years) |

| Skilled Labor Shortage for Installation and Maintenance | -0.5% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Natural Gas and Electricity Prices

Henry Hub spot prices are projected to oscillate between USD 3.10 and USD 4.59 per million British thermal units through 2027, prompting buyers to hedge with dual-fuel systems or defer projects. [3]U.S. Energy Information Administration, “Short-Term Energy Outlook, Natural Gas Prices,” eia.gov A 50% gas-price spike can lift heating bills for a 200,000-square-foot warehouse by one-third, eroding the cost edge that long favored gas-fired units. Conversely, electricity tariffs in California surged to USD 0.18 per kilowatt-hour during 2024 grid congestion, negating savings from electric infrared heaters. Facility managers react by layering thermal storage or demand-response contracts, but those add USD 15,000-50,000 to budgets. In Mexico, a 12% tariff jump in 2024 pushed several nearshoring manufacturers to retain gas technologies despite national electrification incentives. Until price swings stabilize, procurement committees will continue to demand flexible fuel arrangements, slowing pure-electric adoption.

Stringent Emission Standards Increasing Compliance Costs

Stricter NOx and CO emission ceilings in the United States and Canada raise compliance outlays for gas-fired equipment, especially in California’s South Coast air district where low-NOx burners and secondary catalytic treatments are compulsory. Retrofitting older suspended heaters with compliant burners often costs 25-30% of new-unit price, encouraging owners to postpone upgrades. Condensing models meet limits but require corrosion-resistant venting and condensate drainage, adding labor hours and materials. Emission reporting and permitting fees now consume a larger share of operating budgets, nudging architects toward electric alternatives in new construction even when lifecycle costs are higher. While the trend aligns with decarbonization goals, near-term cash-flow constraints can slow replacement cycles, trimming volume growth for the North America unitary heater market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gas Dominance Meets Electric Momentum

In 2025, gas-fired heaters dominated the North American unitary heater market, capturing 63.42% of the market. Meanwhile, electric heaters are set to grow at a 5.77% CAGR through 2031. These heaters solidified their significance in high-bay warehouses, especially where existing natural-gas piping facilitates rapid warm-ups. Condensing variants with 90-98% annual fuel-utilization efficiency are dislodging legacy non-condensing models under post-2024 federal standards, and Reznor, Modine, and Sterling collectively held an estimated 48% share of those replacements. Electric infrared options, however, are logging the strongest unit growth as corporate carbon budgets favor zero-flue-loss solutions. Detroit Radiant’s HDI series cut energy use 25% in a 400,000-square-foot parts facility by heating workers rather than air columns.

A parallel innovation stream in cold-climate heat pumps is poised to expand the addressable pool for electric products once −25 °F-rated models enter mass production in 2026. Hydronic and oil-fired categories, together under 5% of the North America unitary heater market, retain niche relevance in institutional greenhouses and remote sites without pipeline gas. Overall, the product mix is projected to include one electric unit for every two combustion units by the end of the decade, lifting electric models from a 2025 base of 21.6% to nearly 30% by 2031.

By Installation Type: Suspended Systems Lead, Portables Surge

Suspended units delivered 38.89% of 2025 revenues, leveraging ceiling real estate in distribution centers where floor space commands premium lease rates. Trane’s ARU platform integrates destratification fans that reduce vertical temperature gradients by 10-15 °F, lowering total heating loads. Horizontal ducted units find favor in offices and retail chains that value acoustic discretion and alignment with existing air-handling layouts. In contrast, wall-mounted and portable heaters recorded a 5.49% CAGR baseline, thanks to DIY-oriented garages, pop-up retail, and on-site construction needs requiring plug-and-play flexibility.

The North America unitary heater market size for portable units is forecast to double between 2026 and 2031 as remote work pushes homeowners to convert unfinished spaces into conditioned studios. Manufacturers answer with cord-and-plug designs rated for 240-volt supply, avoiding gas piping and vent penetrations. Vertical floor-set units remain a retrofit choice in heritage buildings where structural ceilings cannot bear suspended loads, yet their share is gradually ceded to slimline wall models that offer Wi-Fi scheduling and predictive maintenance diagnostics.

By Application: Warehouses Dominate, Greenhouses Emerge

Warehouse and distribution facilities generated 41.32% of 2025 revenues and are projected to post a 5.34% CAGR through 2031, fueled by 250 million square feet of new space added in the United States during 2024. Automated storage and retrieval systems necessitate tight thermal regimes to protect electro-mechanical equipment, causing spec writers to favor unitary gas heaters with modulating capability over less responsive central systems. Greenhouses, although smaller in absolute format, are on a high trajectory as controlled-environment agriculture scales in Canada and northern U.S. states. Ouellet’s hydronic heaters maintain ±2 °F accuracy critical for lettuce and specialty crops.

Commercial offices, retail, and institutional buildings account for a rising slice of the North America unitary heater market, powered by municipal electrification mandates that accelerate installation of heat-pump or infrared options during tenant-improvement cycles. Residential garages and creative workshops add long-tail volume with portable electric models priced under USD 800, a figure within reach of do-it-yourself installers. Institutional campuses with central boilers keep hydronic units alive, but budgeted phase-outs position electric replacements as the long-run winner.

By End User: Industrial Anchors, Commercial Accelerates

Industrial enterprises absorbed 47.14% of 2025 shipments as assembly lines, paint booths, and cold storage demanded rugged gas and hydronic equipment capable of integrating process and comfort heating. Tesla’s 2024 expansion in Nuevo León, requiring 200 suspended units, illustrates how nearshoring amplifies industrial volumes. Yet commercial real estate has become the fastest-moving slice of the North America unitary heater market, expanding at 6.01% CAGR on the back of retrofit tax incentives and emissions caps. ACEEE modeling finds 27-60% of U.S. commercial space can electrify profitably when Section 179D deductions are stacked with utility rebates.

Residential demand remains niche but steady, linked to housing completions and growth of gig-economy workshops needing winter comfort. Big-box stores and e-commerce sites supply the majority of these units, dominated by portable or wall-mounted 5-15 kW heaters. Institutional users such as schools and hospitals are pivoting toward heat pumps aligned with carbon-neutral pledges, opening retrofit revenue for contractors specialized in boiler plant phase-outs.

By Distribution Channel: Distributors Hold, Online Gains

Traditional HVAC distributors safeguarded 52.75% of the North America unitary heater market in 2025, offering inventory depth, credit terms, and technical training valued by mechanical contractors. Consolidators like Watsco acquired eight regional outlets in 2024 to expand to 680 branches, enhancing last-mile availability and raising the barrier for pure-play e-commerce rivals. Still, online portals such as EDEN are scaling quickly; the platform processed USD 45 million in equipment sales within six months by providing instant quotes, 3D selection tools, and direct-to-jobsite shipping.

Direct sales remain a go-to option for mega-warehouses and manufacturing complexes where volume discounts and custom configurations justify bypassing distribution layers. Big-box retailers secure share in the residential and small business arena through in-store merchandising and loyalty perks for licensed tradespeople. Over the forecast, hybrid models that marry online ordering with distributor pickup are expected to gain momentum, especially in Sun Belt states where fast-track construction schedules reward high service levels.

Geography Analysis

The United States contributed 78.64% of 2025 demand, underpinned by stringent Department of Energy efficiency rules and a deep warehousing pipeline centered in Texas, California, Pennsylvania, and Georgia. Builders in those states added 250 million square feet of climate-controlled space in 2024 alone, selecting suspended gas heaters for 65% of new bays thanks to lower capital cost and ubiquitous gas hookups. Cold-climate heat-pump pilots in Minnesota showed coefficients of performance of 2.5 at −15 °F, persuading northern operators to shift away from combustion in selected zones. Municipal ordinances, notably New York City’s Local Law 97, layer financial penalties onto carbon budgets, making electric infrared equipment the default for many large urban projects. California’s USD 150 million Self-Generation Incentive tranche supported a 22% bump in state-level electric heater sales the same year.

Hydronic units dominate greenhouses and institutional campuses, while heat-pump retrofits attract federal grants covering one-quarter of project costs. Eight million square feet of additional greenhouse space erected in 2024 demanded precision heaters able to swing between seed-germination and mature-crop regimes. Provincial policies such as British Columbia’s CleanBC program set aggressive sales targets for heat pumps by 2030, yet softness in commercial real estate tempers aggregate growth to the mid-single digits.

Mexico, recording the bloc’s fastest growth at a 6.24% CAGR, benefits from nearshoring of automotive and electronics supply chains. Twelve new plants broke ground in 2024, each outfitted with 50-200 suspended gas heaters. While federal incentives exist for electrified space conditioning, a 12% industrial electricity tariff hike in 2024 bolstered the cost advantage of pipeline gas, keeping combustion units at an 85% share in the industrial niche. Demand clusters in Nuevo León, Coahuila, and Chihuahua, regions that enjoy established cross-border distribution corridors into Texas.

Mordor Intelligence tracks the unitary heater market across other major regions such as Asia, Europe, and Latin America.

Competitive Landscape

The market is moderately concentrated with brands such as Modine, Reznor, Lennox, Trane, and others. Modine reported USD 423 million in Climate Solutions revenue for Q1 fiscal 2025, an 8% year-on-year increase spurred by data-center and modular HVAC projects. Carrier’s USD 3 billion purchase of Nortek Global HVAC combined Reznor gas technology with Carrier heat-pump portfolios, establishing a one-stop platform able to ride the electrification wave without cannibalizing legacy lines. Trane extends its reach through its ARU series, which captured 12% of new warehouse placements within six months by embedding controls that integrate with warehouse management systems.

Product differentiation is migrating from burner efficiency, largely commoditized around 90-plus AFUE, to control ecosystems. Honeywell’s Forge suite, embedded in several Lennox and Trane models, leverages machine learning to forecast heating loads 4 hours ahead, resulting in 12-18% energy savings during variable-occupancy periods.

Electric-specialist challengers such as Detroit Radiant and King Electrical exploit faster delivery lead times and direct-to-contractor pricing that undercuts distributor mark-ups by 10-15%. Added white-space opportunities lie in cold-climate electric heat pumps, dual-fuel units that toggle based on real-time prices, and IoT-linked zoning arrays for multitenant warehouses. Suppliers able to cross-sell service agreements and performance analytics are expected to widen EBITDA margins even as hardware prices normalize.

North America Unitary Heater Industry Leaders

Trane Inc. (Trane Technologies PLC)

Reznor LLC (Madison Air)

Modine Manufacturing Company

Lennox International, Inc.

Sterling HVAC (Mestek, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Rheem launched the Prestige Series cold-climate heat pump rated for −25 °F, COP 2.8, eligible for up to USD 2,000 IRA tax credit and targeting 15,000 first-year sales.

- January 2026: Daikin completed Carrier China HVAC integration and announced a 40% capacity boost at its Houston heat-pump plant (200,000 ft², 150 jobs) by Q4 2026.

- December 2025: Lennox posted USD 4.8 billion 2025 revenue (+7%) and committed USD 75 million to expand its Marshalltown, Iowa factory for 95% AFUE gas unit heaters by Q3 2026.

- November 2025: Trane introduced the Precedent modular HVAC system with predictive IoT controls, booking USD 120 million in retrofit orders within 60 days and cutting energy use 30%.

North America Unitary Heater Market Report Scope

A unit heater is a self-contained, non-ducted heating device that provides localized heating without a central HVAC system. These appliances can be independently installed to heat specific areas, such as garages, workshops, or large spaces. The study tracks revenue from sales of the North America Unitary Heater Market offered by market vendors worldwide.

The North America Unitary Heater Market Report is Segmented by Product Type (Gas-Fired Heaters, Electric Heaters, Hydronic Heaters, and Oil-Fired Heaters), Installation Type (Horizontal Mounting, Vertical Mounting, Suspended Mounting, and Wall-Mounted/Portable Units), Application (Warehouses and Distribution Centers, Greenhouses and Agricultural Buildings, Commercial Buildings, Residential Garages and Workshops, and Institutional Facilities), End User (Residential, Commercial, and Industrial), Distribution Channel (Direct Sales, HVAC Distributors, Online Retail, and Big-Box Retail), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Gas-Fired Heaters |

| Electric Heaters |

| Hydronic Heaters |

| Oil-Fired Heaters |

| Horizontal Mounting |

| Vertical Mounting |

| Suspended Mounting |

| Wall-Mounted/Portable Units |

| Warehouses and Distribution Centers |

| Greenhouses and Agricultural Buildings |

| Commercial Buildings |

| Residential Garages and Workshops |

| Institutional Facilities |

| Residential |

| Commercial |

| Industrial |

| Direct Sales |

| HVAC Distributors |

| Online Retail |

| Big-Box Retail |

| United States |

| Canada |

| Mexico |

| By Product Type | Gas-Fired Heaters |

| Electric Heaters | |

| Hydronic Heaters | |

| Oil-Fired Heaters | |

| By Installation Type | Horizontal Mounting |

| Vertical Mounting | |

| Suspended Mounting | |

| Wall-Mounted/Portable Units | |

| By Application | Warehouses and Distribution Centers |

| Greenhouses and Agricultural Buildings | |

| Commercial Buildings | |

| Residential Garages and Workshops | |

| Institutional Facilities | |

| By End User | Residential |

| Commercial | |

| Industrial | |

| By Distribution Channel | Direct Sales |

| HVAC Distributors | |

| Online Retail | |

| Big-Box Retail | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America unitary heater market in 2026?

The market is valued at USD 751.19 million in 2026, with a forecast CAGR of 4.85% through 2031.

Which product category currently dominates sales?

In 2025, gas-fired heaters held 63.42% market share, supported by widespread natural-gas infrastructure and lower upfront costs.

Why are electric heaters gaining popularity?

Tax credits, stricter efficiency rules, and cold-climate heat-pump advances are shortening payback periods, lifting electric category growth to 5.77% CAGR.

Which application segment offers the largest revenue pool?

In 2025, warehouses and distribution centers generated 41.32% of demand, driven by the e-commerce fulfillment boom and cold-chain investments.

What is the fastest-growing geography?

Mexico leads with a 6.24% CAGR, as nearshoring accelerates industrial plant construction that relies on suspended gas heaters.

How are distribution channels evolving?

HVAC distributors still handle most volume, but online portals are capturing share by providing instant pricing and direct shipping, growing at 5.82% CAGR.

Page last updated on: