VTOL UAV Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

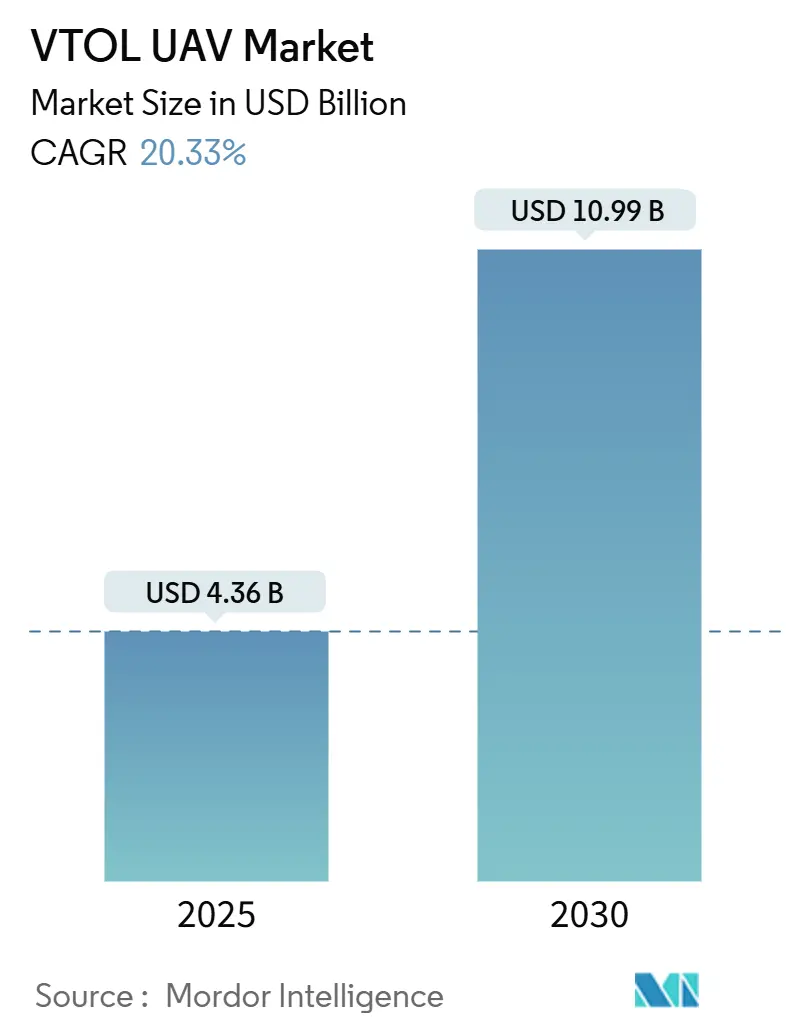

| Market Size (2025) | USD 4.36 Billion |

| Market Size (2030) | USD 10.99 Billion |

| Growth Rate (2025 - 2030) | 20.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

VTOL UAV Market Analysis by Mordor Intelligence

The VTOL UAV market size reached USD 4.36 billion in 2025 and is projected to advance to USD 10.99 billion by 2030, reflecting a 20.33% CAGR. This trajectory mirrors the shift from legacy helicopters toward unmanned vertical-lift solutions as defense forces seek runway-independent platforms that integrate seamlessly with evolving sensor-to-shooter networks.[1]USNI Staff, “Report to Congress on the Army’s Future Long-Range Assault Aircraft,” usni.org Program cancellations, such as the US Army’s FARA, redirect billions toward autonomous vertical systems. At the same time, hybrid-electric propulsion bridges conventional rotors and fully electric flight by lowering fuel burn and acoustic signatures. North America currently holds 28.65% of the VTOL UAV market share, but Asia-Pacific’s 23.47% CAGR through 2030 signals a rapid geographic rebalancing toward the Indo-Pacific theater. Technology breakthroughs in hydrogen fuel cells and lithium-sulfur batteries promise longer endurance, answering a key operational constraint for electric-only aircraft.

Key Report Takeaways

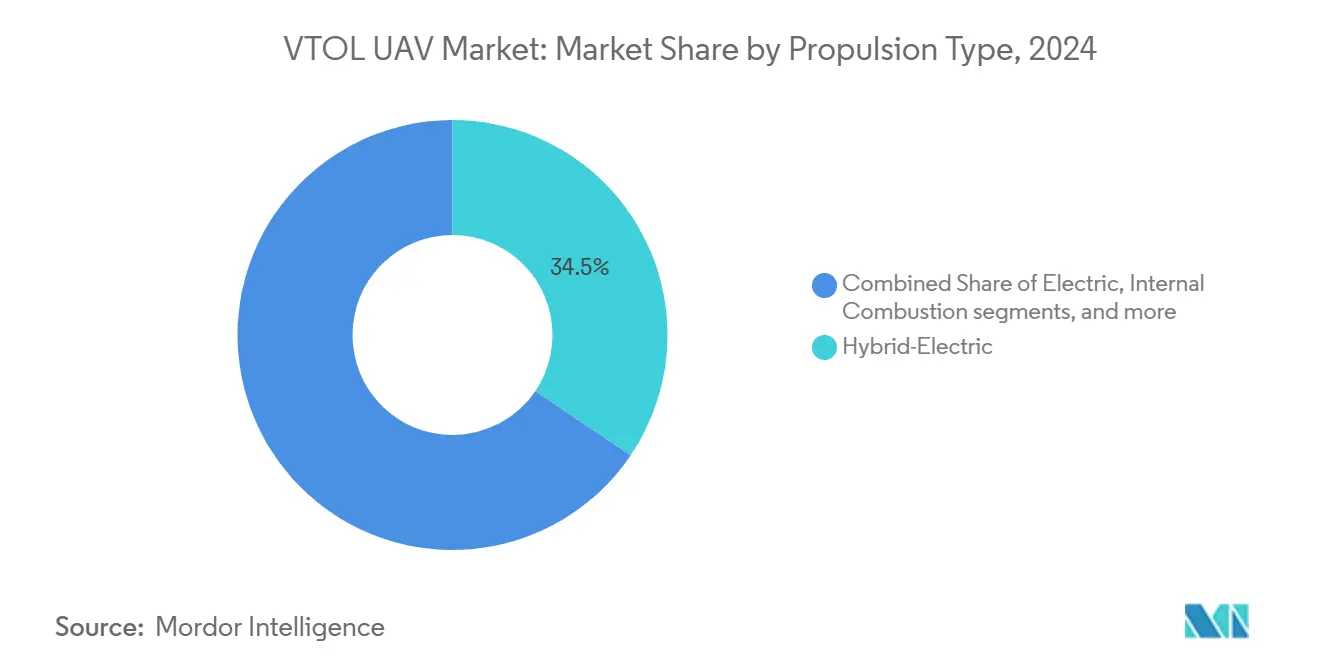

- By propulsion type, hybrid-electric platforms led with 34.45% VTOL UAV market share in 2024, whereas hydrogen fuel-cell systems are projected to expand at a 23.32% CAGR through 2030.

- By range, medium-range aircraft (100 to 500 km) captured 38.87% share of the VTOL UAV market size in 2024, while long-range models (greater than 500 km) are advancing at a 21.67% CAGR to 2030.

- By application, ISR missions accounted for a 35.95% share of the VTOL UAV market in 2024; cargo/resupply operations recorded the fastest growth at a 22.78% CAGR to 2030.

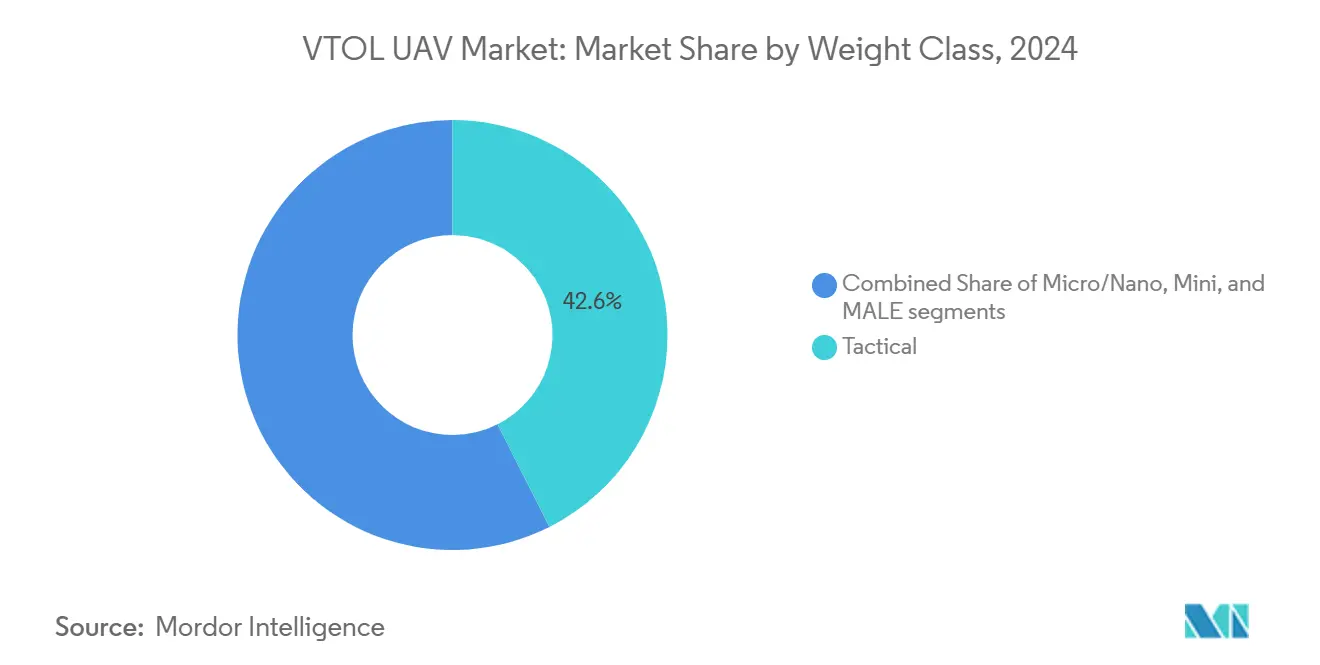

- By weight class, tactical systems (150 to 600 kg) held 42.56% of the VTOL UAV market share in 2024, whereas medium-altitude long-endurance (MALE) platforms exceeded with a 23.94% CAGR through 2030.

- By mode of operation, remotely piloted aircraft commanded a 61.14% share of the VTOL UAV market size in 2024; autonomous systems are forecasted to expand at a 22.54% CAGR to 2030.

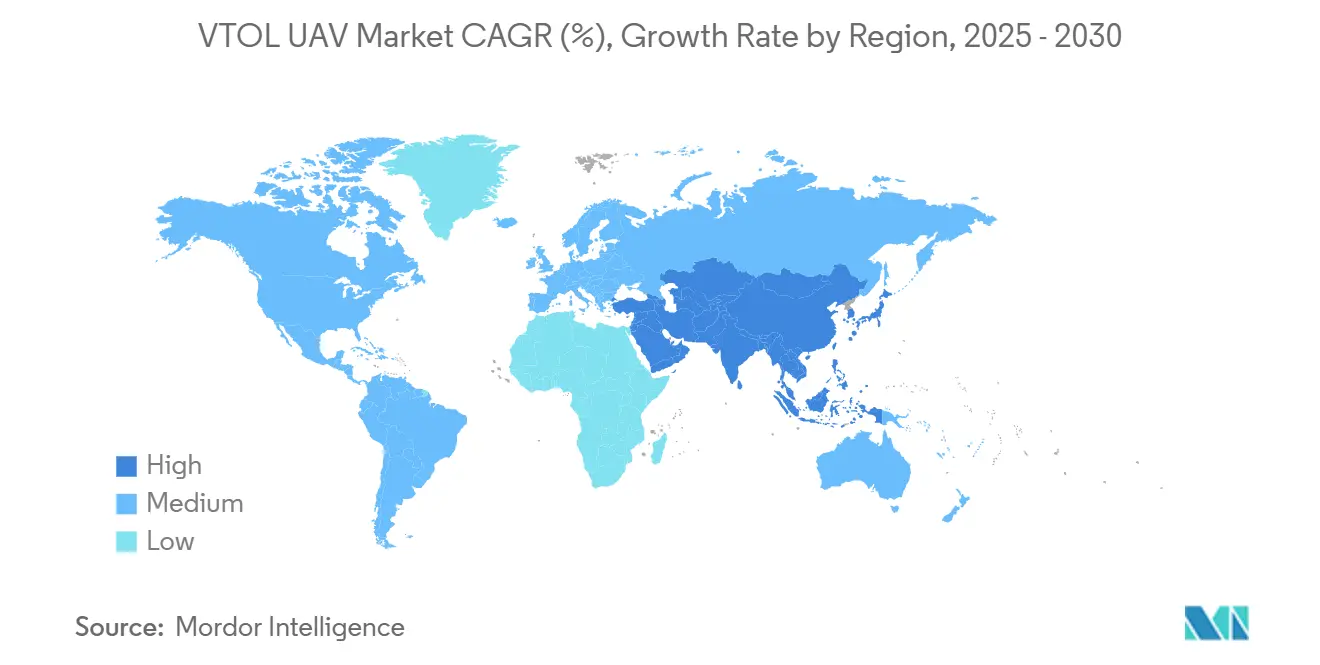

- By geography, North America led with 28.65% VTOL UAV market share in 2024, yet Asia-Pacific is projected to post the highest 23.47% CAGR through 2030.

Global VTOL UAV Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent ISR demand in contested environments | +3.20% | Global, concentrated in Asia-Pacific and Eastern Europe | Medium term (2-4 years) |

| Demand for runway-independent logistics for expeditionary forces | +2.80% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Modernization programs replacing legacy helicopters with VTOL UAVs | +4.10% | North America, Europe, selective Asia-Pacific markets | Long term (≥ 4 years) |

| Increased defense spending on unmanned combat systems | +3.50% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Modular hybrid-electric propulsion enabling acoustic stealth | +2.40% | North America and Europe, technology transfer to allies | Medium term (2-4 years) |

| NATO push for organic sensor-to-shooter VTOL swarms | +1.90% | NATO member states, partnership frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent ISR Demand in Contested Environments

Combat theaters with dense electronic-warfare activity favor VTOL UAVs that can hover, maneuver at low altitude, and operate without GPS reliance. Shield AI’s V-BAT proved this in Ukraine by detecting Buk systems and relaying coordinates for precision fires even under heavy jamming. The British Army’s Project Corvus targets 24-hour endurance to replace vulnerable MALE fixed-wing assets, underscoring how survivability and persistence now outweigh sheer altitude in ISR doctrine.[2]Defence-UA, “Shield AI Declassifies V-BAT Use in Ukraine,” defence-ua.com

Demand for Runway-Independent Logistics for Expeditionary Forces

Distributed operations compel militaries to bypass damaged or non-existent runways. VTOL UAVs carry medical supplies, ammunition, and precision loitering munitions directly to forward units. The US Marine Corps Organic Precision Fires–Loitering program funds quad-rotor systems for squad-level resupply and strike, while Heven Drones’ hydrogen-powered Raider flies 23 kg payloads for up to 12 hours in silent mode, aligning with NATO calls for resilient supply chains.

Modernization Programs Replacing Legacy Helicopters with VTOL UAVs

Budgets once earmarked for manned reconnaissance helicopters now flow to modular unmanned platforms. The Bell V-280 Valor advances at 520 km/h, but its MOSA architecture is designed for teaming with VTOL UAVs, not replacing them one-for-one. Russia’s fifth-generation manned VTOL concept similarly acknowledges that much future lift will be unmanned, illustrating a universal doctrinal pivot.

Increased Defense Spending on Unmanned Combat Systems

Taiwan’s 100,000-unit drone order, 48,000 of which are military grade, is unprecedented for manned aircraft programs. Forecasts show global military UAS spending reaching USD 23 billion by 2033, with VTOL UAV market deployments absorbing a growing share as governments prioritize attritable, networked aerial nodes.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited endurance due to battery constraints | -2.10% | Global, particularly affecting electric-only systems | Short term (≤ 2 years) |

| Regulatory hurdles for BVLOS operations in shared airspace | -1.80% | North America and Europe, regulatory framework development | Medium term (2-4 years) |

| Vulnerability to drone-kill laser systems | -1.30% | Global, concentrated in peer adversary scenarios | Medium term (2-4 years) |

| Supply-chain constraints in rare-earth motors | -1.60% | Global, Western manufacturers most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Endurance Due to Battery Constraints

Conventional lithium-ion (Li-ion) packs yield 20–35 minute multirotor endurance, forcing payload trade-offs. Solid-state and lithium-sulfur (Li-S) chemistries promise up to 60% more energy, but manufacturing scale and safety certification remain hurdles, keeping hybrid powertrains dominant in the near term.

Regulatory Hurdles for BVLOS Operations in Shared Airspace

Although the FAA finalized powered-lift rules in 2024, it continues to delay a unified BVLOS framework. Waiver volumes are rising but remain case-by-case, adding cost and uncertainty for operators. Europe’s EASA has raised MTOW limits to 12,500 lb, yet detect-and-avoid requirements are still evolving, slowing commercial adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Hybrid-Electric Dominance, Hydrogen Upswing

Hybrid-electric aircraft led the VTOL UAV market with a 34.45% share in 2024, reflecting their balance between quiet electric lift and fuel-efficient cruise. This share translates into USD 1.5 billion of the market's size, while hydrogen fuel-cell platforms, though smaller today, are forecasted to post a 23.32% CAGR through 2030.

Hybrid propulsion attracts procurement because it addresses endurance caps that pure electric craft face and reduces acoustic signatures compared with internal-combustion engines. Successful demo flights, including VerdeGo Aero's 60% fuel-saving VH-3, prove feasibility for long-range ISR patrols. Hydrogen propulsion's faster growth owes to its higher energy density; United Therapeutics flew the first piloted hydrogen VTOL in 2025, showcasing zero-emission endurance beyond 600 km, a critical factor for covert cargo runs.[3]EV-tol News, “World’s First Piloted Hydrogen VTOL,” evtol.news

By Range: Tactical Medium-Range Leadership, Long-Range Acceleration

Medium-range models (100 to 500 km) captured 38.87% of the VTOL UAV market share in 2024, anchoring USD 1.7 billion of the market's size. Their supremacy aligns with battalion-level logistics and ISR needs inside the theater.

However, long-range systems above 500 km are clocking a 21.67% CAGR to 2030 as militaries seek standoff ISR and strike beyond adversary A2/AD bubbles. Upgrades such as satellite datalinks on Shield AI's V-BAT extend flight radius without ground stations, shifting procurement toward deeper-reach platforms.

By Application: ISR Core, Cargo Momentum

ISR remains the largest mission, with a 35.95% share in 2024—roughly USD 1.6 billion of the VTOL UAV market size—owing to legacy investments in airborne surveillance.

Cargo and resupply, though smaller, will outpace all other uses with a 22.78% CAGR. Austere deployments in the Indo-Pacific drive demand for unmanned delivery of munitions and medical kits. Programs like the US Marine Corps OPF-Loitering integrate VTOL cargo drones into squad tactics, signaling a doctrinal upgrade that shifts unmanned aircraft from “eyes” to “lifeline”.

By Weight Class: Tactical Sweet Spot, MALE Growth

Tactical UAVs (150 to 600 kg) held 42.56% of the VTOL UAV market share in 2024, translating to USD 1.9 billion. Their footprint fits shipboard elevators and austere landing pads while supporting 50 kg payloads.

Medium-altitude long-endurance (MALE) UAVs weighing above 600 kg are projected to grow 23.94% annually. Sikorsky’s rotor-blown-wing UAS trials show heavy platforms can blend airplane cruise with helicopter VTOL, expanding the load and range envelopes needed for long-endurance maritime ISR.

By Mode of Operation: Remote Control Today, Autonomous Tomorrow

Remotely piloted aircraft held a 61.14% market share in 2024 as commanders demanded human-in-the-loop assurance. This equates to USD 2.7 billion in the VTOL UAV market.

Autonomous modes clock a 22.54% CAGR through 2030. Ukraine’s mass-produced AI-enabled drones illustrate how autonomy preserves mission continuity under jamming. Northrop Grumman’s partnership with Merlin advances certifiable autonomy for heavier aircraft, signaling mainstream adoption.

Geography Analysis

North America controlled 28.65% of the VTOL UAV market share in 2024, buoyed by sustained R&D funding and regulatory clarity. The new FAA powered-lift rule and Special Federal Aviation Regulation 120 provide pathways for early commercial services, reinforcing regional leadership. However, continued rare-earth supply concerns and Buy-American magnet mandates could temper growth in the decade's second half.

Asia-Pacific is advancing at a 23.47% CAGR to 2030, driven by escalating Indo-Pacific tensions. Taiwan’s record order of 48,750 military-grade drones underscores the region’s urgency, while Chinese tilt-rotor prototypes hint at future peer-to-peer competitions in vertical lift. Commercial projects in Japan and South Korea further widen the customer base beyond defense.

Europe enjoys steady adoption under a harmonized EASA framework adopted in 2024. Sweden’s NATO-aligned swarm program and the UK’s BVLOS corridor approvals show that alliance requirements and progressive regulation coexist with comparatively modest defense budgets. Environmental mandates shape European requirements toward hydrogen and hybrid platforms, influencing OEM roadmaps.[4]European Union Aviation Safety Agency, “VTOL Operations Package,” easa.europa.eu

Competitive Landscape

The VTOL UAV market sits at a moderate concentration level where defense primes and agile startups coexist. Northrop Grumman, Lockheed Martin, and Textron leverage deep supply chains and certification experience, but pure plays such as Shield AI and AeroVironment demonstrate faster iteration in autonomy. Partnerships dominate strategy: Joby pairs with L3Harris for sensorized hybrids; Northrop Grumman teams with Merlin for autonomous flight stacks; and VerdeGo collaborates with the US Air Force on hybrid power modules. Rare-earth diversification, battery breakthroughs, and swarm AI represent the chief battlegrounds for differentiation.

Western OEMs hedge geopolitical risks by investing in alternative magnet chemistries and domestic processing. Startups exploit gaps by offering mission packages that large primes cannot rapidly certify. The result is a market where innovation cycles shorten even as regulatory overhead rises, encouraging joint ventures over vertical integration.

VTOL UAV Industry Leaders

Northrop Grumman Corporation

Schiebel Corporation

AeroVironment, Inc.

Textron Inc.

Israel Aerospace Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Joby Aviation and L3Harris Technologies, Inc., began joint flight testing of a gas-turbine hybrid VTOL tailored for defense ISR missions.

- July 2025: Taiwan confirmed the acquisition of 48,750 military-grade UAVs, including 350 VTOL units annually to 2027.

- June 2025: ANT unveiled the MERCURY VTOL while Skyeton expanded EU production capacity amid heightened Ukrainian demand.

- May 2025: Lyten launched US-made Li-S batteries targeting drone propulsion for national security missions.

Global VTOL UAV Market Report Scope

| Electric |

| Hybrid-Electric |

| Internal Combustion |

| Hydrogen Fuel-Cell |

| Short-Range (Less than 100 km) |

| Medium-Range (100 to 500 km) |

| Long-Range (Greater than 500 km) |

| Intelligence, Surveillance, and Reconnaissance (ISR) |

| Cargo/Resupply |

| Anti-Submarine Warfare (ASW) |

| Others |

| Micro/Nano (Less than 20 kg) |

| Mini (20 to 150 kg) |

| Tactical (150 to 600 kg) |

| Medium-Altitude Long-Endurance (MALE) (Greater than 600 kg) |

| Autonomous |

| Remotely Piloted |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Propulsion Type | Electric | ||

| Hybrid-Electric | |||

| Internal Combustion | |||

| Hydrogen Fuel-Cell | |||

| By Range | Short-Range (Less than 100 km) | ||

| Medium-Range (100 to 500 km) | |||

| Long-Range (Greater than 500 km) | |||

| By Application | Intelligence, Surveillance, and Reconnaissance (ISR) | ||

| Cargo/Resupply | |||

| Anti-Submarine Warfare (ASW) | |||

| Others | |||

| By Weight Class | Micro/Nano (Less than 20 kg) | ||

| Mini (20 to 150 kg) | |||

| Tactical (150 to 600 kg) | |||

| Medium-Altitude Long-Endurance (MALE) (Greater than 600 kg) | |||

| By Mode of Operation | Autonomous | ||

| Remotely Piloted | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the VTOL UAV market?

The VTOL UAV market size stands at USD 4.36 billion in 2025 and is projected to hit USD 10.99 billion by 2030.

Which propulsion type leads sales in VTOL UAVs?

Hybrid-electric platforms dominate with a 34.45% share, balancing quiet electric lift and extended hybrid range.

Which region is growing the fastest for VTOL UAV deployment?

Asia-Pacific is advancing at a 23.47% CAGR through 2030 due to defense modernization and Indo-Pacific security needs.

How are battery limitations being addressed?

Manufacturers are shifting to hybrid-electric systems and exploring lithium-sulfur (Li-S) chemistries that promise 60% higher energy density.

What applications are expanding beyond ISR?

Cargo and resupply missions show a 22.78% CAGR as forces seek runway-free delivery of supplies to dispersed units.

How strict are current US regulations for VTOL UAVs?

The FAA has issued a powered-lift rule, but full BVLOS operations still require individual waivers, limiting large-scale commercial use.

Page last updated on: