Fixed-Wing VTOL UAV Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

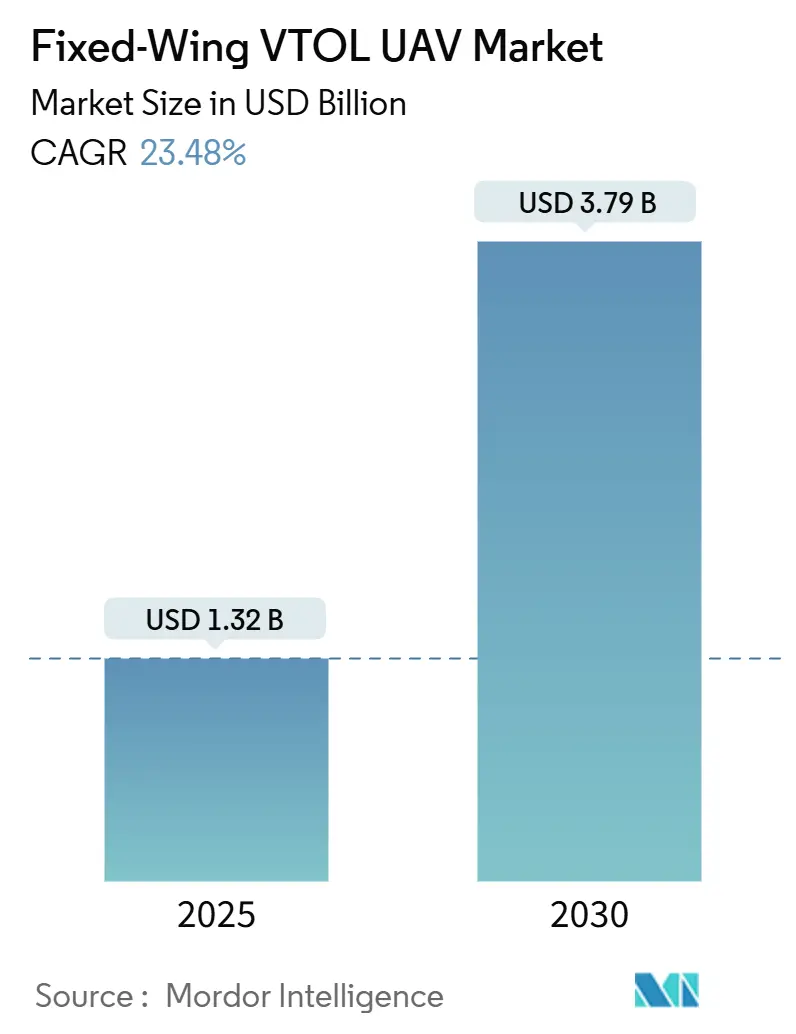

| Market Size (2025) | USD 1.32 Billion |

| Market Size (2030) | USD 3.79 Billion |

| Growth Rate (2025 - 2030) | 23.48% CAGR |

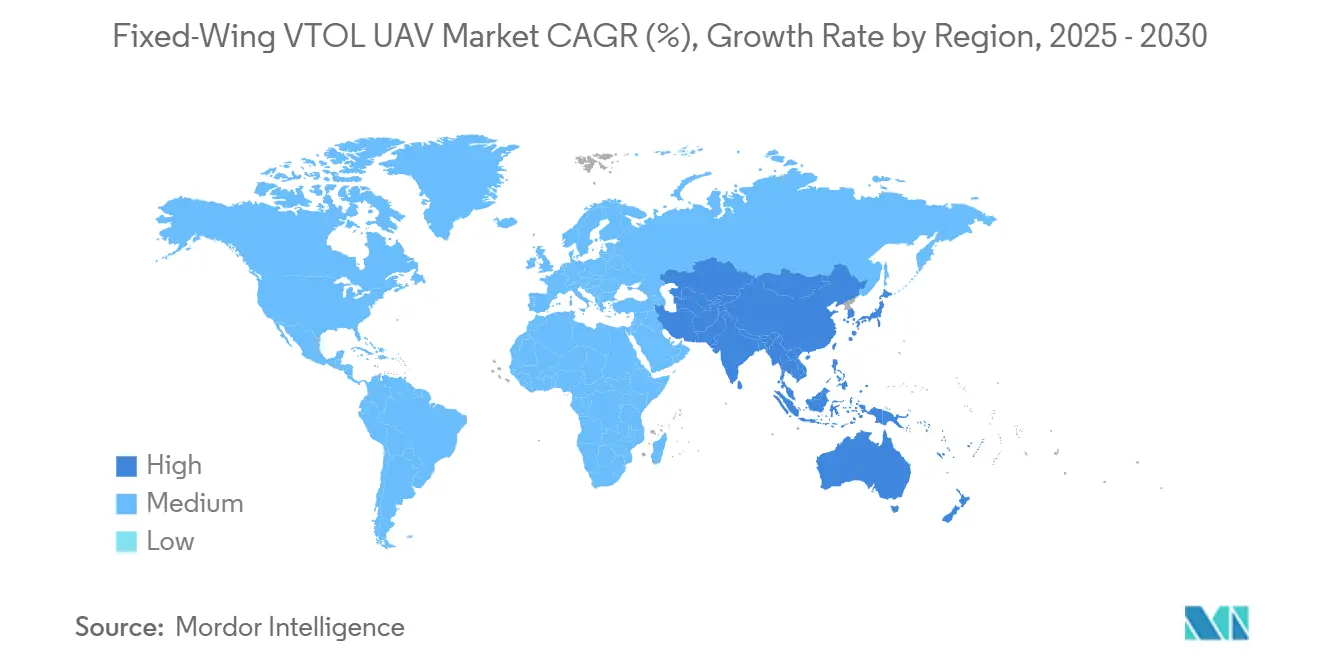

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

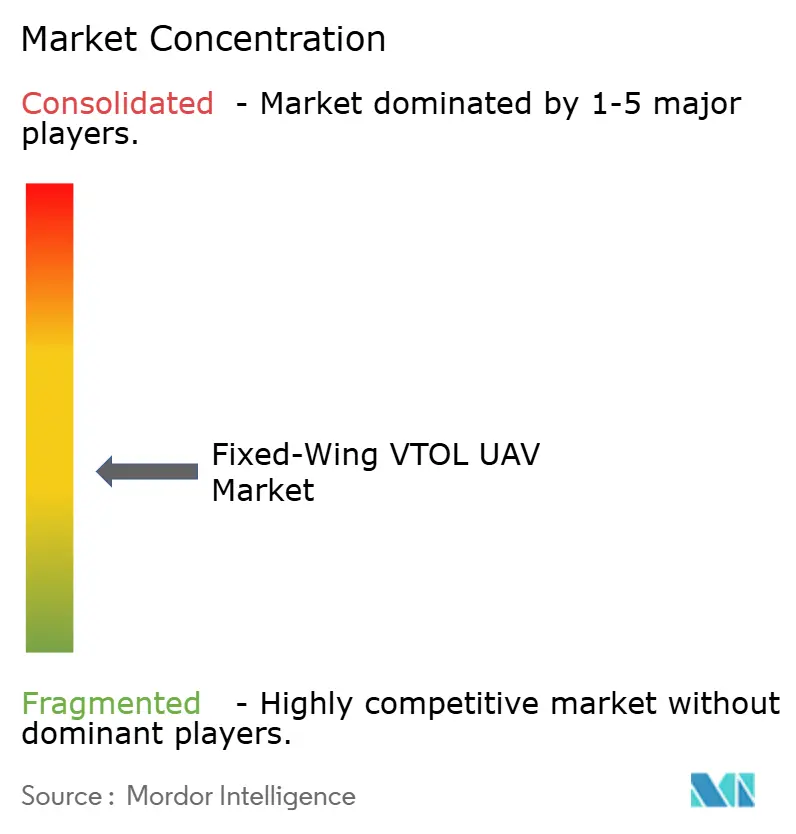

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fixed-Wing VTOL UAV Market Analysis by Mordor Intelligence

The fixed-wing VTOL UAV market size is USD 1.32 billion in 2025 and is forecasted to reach USD 3.79 billion by 2030, expanding at a 23.48% CAGR. Solid demand for runway-independent platforms, faster regulatory approvals in major economies, and breakthroughs in hybrid-electric propulsion underpin this rapid expansion. Defense agencies are scaling procurement programs, prioritizing endurance and austere-site operations, while commercial operators move from trials to fleet deployments in mapping, inspection, and package delivery. Investment flows toward larger payload classes and long-range variants, signaling a shift from niche tactical uses toward mainstream civil and dual-use missions. Competition remains moderately fragmented as incumbents seek scale through acquisitions, and specialized start-ups exploit propulsion and autonomy niches.

Key Report Takeaways

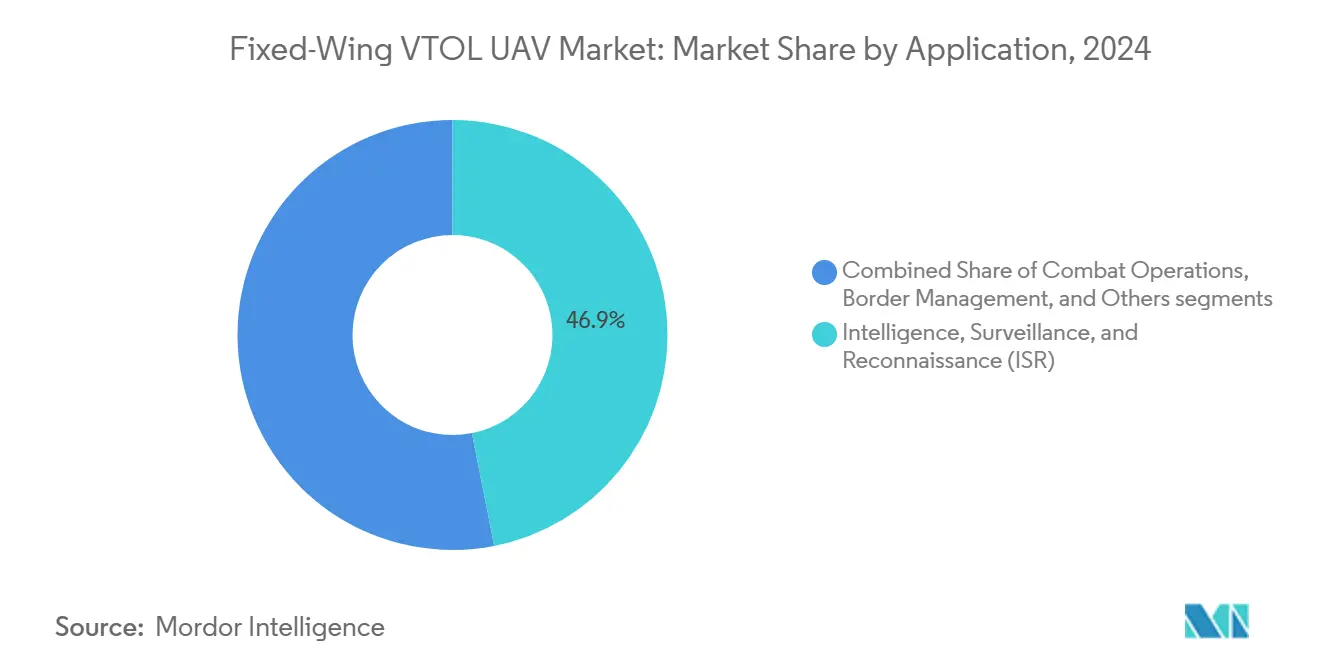

- By application, intelligence, surveillance, and reconnaissance (ISR) captured 46.89% of the fixed-wing VTOL UAV market share in 2024 and is advancing at a 25.34% CAGR through 2030.

- By propulsion type, electric systems held 53.75% of the fixed-wing VTOL UAV market size in 2024, while fuel-cell variants posted the fastest 27.56% CAGR to 2030.

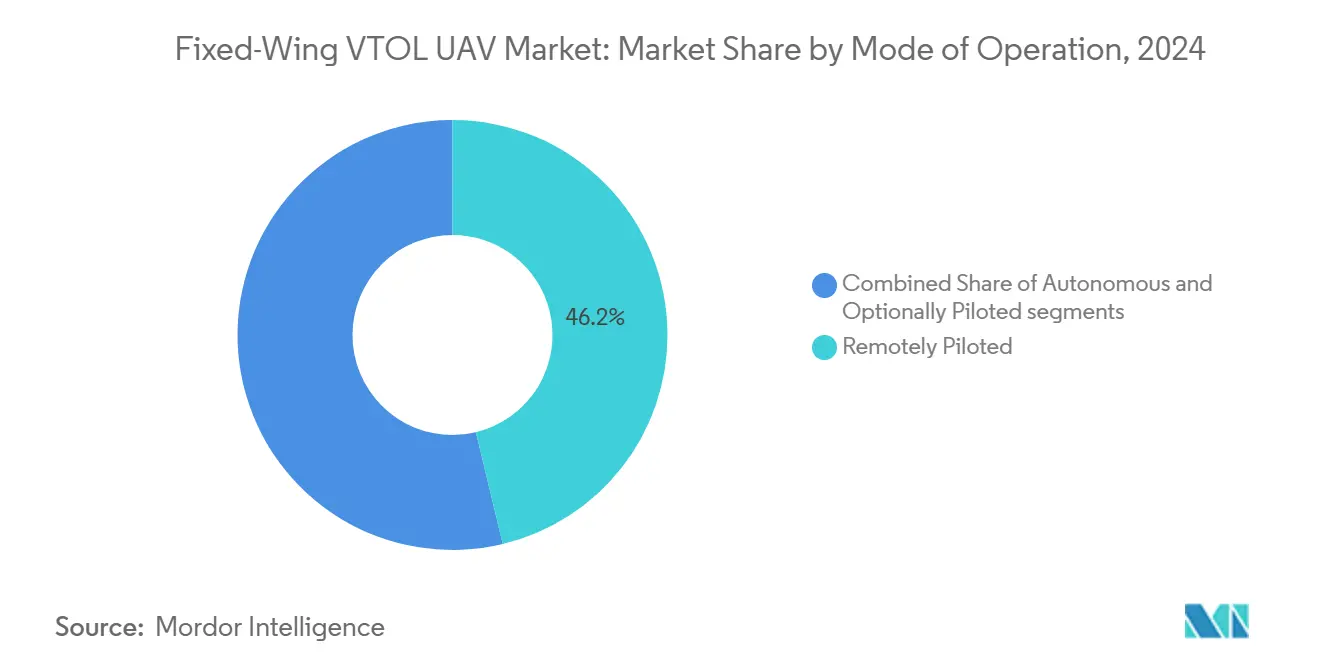

- By mode of operation, remotely piloted systems held a 46.24% share in 2024, while autonomous platforms are set for a 25.01% CAGR to 2030.

- By MTOW class, the 25 to 150 kg segment accounted for a 37.90% share of the fixed-wing VTOL UAV market size in 2024; platforms above 150 kg are progressing at a 25.78% CAGR through 2030.

- By range, medium-range aircraft led with 41.25% share in 2024, whereas long-range models are expanding at a 26.34% CAGR to 2030.

- By geography, North America commanded 36.55% of the fixed-wing VTOL UAV market share in 2024, and Asia-Pacific records the highest 24.89% CAGR through 2030.

Global Fixed-Wing VTOL UAV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global demand for runway-independent ISR and surveillance platforms | +4.2% | North America, Asia-Pacific | Medium term (2-4 years) |

| Expansion of commercial mapping and aerial surveying applications | +3.8% | North America, Europe | Short term (≤ 2 years) |

| Progress in regulatory approvals for beyond visual line-of-sight (BVLOS) operations | +5.1% | North America, European Union | Short term (≤ 2 years) |

| Technological advancements in hybrid-electric propulsion systems | +4.6% | North America, Europe | Medium term (2-4 years) |

| Adoption of UAVs for environmental monitoring in hazardous sites | +2.9% | Europe, North America | Long term (≥ 4 years) |

| Growing use of high-wind-capable UAVs for offshore wind farm inspections | +3.4% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Demand for Runway-Independent ISR and Surveillance Platforms

Armed forces increasingly favor fixed-wing VTOL UAV market solutions that avoid vulnerable runways while preserving fixed-wing endurance. Turkey’s 2025 tactical VTOL drone achieves 10-hour endurance and 1,300 km range from a 12-foot square deck, illustrating the operational leap offered by vertical launch and cruise efficiency.[1]Turkish Aerospace Industries, “TAI Presents New VTOL Drone at IDEF 2025,” armyrecognition.com Japan’s purchase of V-BAT systems for naval surveillance shows similar prioritization of confined-space operations. Border agencies deploy these aircraft to establish rapid, infrastructure-free coverage in remote sectors, and multi-fuel capabilities such as those on the APUS 25 enhance logistical resilience in dispersed missions. The dual ability to hover for target identification and sprint to new taskings is unmatched by pure rotorcraft or runway-bound fixed-wing types.

Expansion of Commercial Mapping and Aerial Surveying Applications

Surveying firms are replacing light aircraft with fixed-wing VTOL UAV market platforms that combine vertical launch ease with high-speed area coverage. XAG’s M2000 maps 533 hectares per hour during 90-minute sorties at centimeter-level accuracy, removing runway dependencies for agricultural clients.[2]XAG, “M2000 Remote Sensing Drone,” xa.com Aeromao’s VT-NAUT extends missions to altitudes of 4,900 m, reaching mountainous mining sites inaccessible by ground teams. Hydrogen-powered prototypes such as the 100 kg-MTOW DAPHNE aim for zero-emission environmental surveys, aligning with strict European sustainability mandates. Post-mining subsidence monitoring and multispectral imaging create recurring revenue streams that offset higher acquisition costs versus multirotors.

Progress in Regulatory Approvals for Beyond Visual Line-of-Sight Operations

BVLOS rules published by the FAA in 2025 authorize flights up to 400 ft for craft under 1,320 lb, directly opening US skies to heavier fixed-wing VTOL UAV market entrants. Earlier Dallas-area approvals for observer-less operations validated unmanned traffic management systems that de-risk shared airspace. EASA’s 2025 Vertical Take-Off and Landing (VTOL) Capable Aircraft classification harmonizes European certification, accelerating continent-wide deployments. Wing Aviation’s Hummingbird platform secured special class criteria that permit one pilot to supervise 20 drones, demonstrating the scalability that commercial fleets require. These converging frameworks shrink compliance costs and encourage global product strategies.

Technological Advancements in Hybrid-Electric Propulsion Systems

Hybrid-electric architectures bridge the endurance gap of pure battery aircraft while retaining green credentials. A compound-wing demonstrator using a 48 V lithium-polymer (LiPo)pack plus a 60 cc engine delivered 25 minutes of extra vertical flight time and multi-destination capability. Distributed-propulsion Super-STOL designs produce 4,300 W peak while liquid cooling maintains efficiency, permitting zero-length takeoffs for austere sites. Military users gain lower thermal signatures and multi-fuel flexibility, as the APUS 25 achieves 8-hour sorties on standard battlefield fuels while generating 300 W for sensors. Solar augmentation trims fuel burn, and emerging PEM fuel-cell stacks outperform batteries on missions longer than 2 hours.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher acquisition costs compared to multi-rotor UAV alternatives | -2.8% | Global | Short term (≤ 2 years) |

| Endurance limitations due to current battery energy density constraints | -3.2% | Global | Medium term (2-4 years) |

| Shortage of skilled talent for hybrid flight control software development | -1.9% | North America, Europe | Long term (≥ 4 years) |

| Airspace congestion challenges around vertiport infrastructure | -2.1% | Urban North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Acquisition Costs Compared to Multirotor Alternatives

Dual-mode aerostructures, complex transition flight controls, and hybrid powertrains raise unit prices to USD 98,000–500,000 for light-class aircraft, versus lower-priced multirotors. Service costs also escalate because technicians must maintain both electric and combustion subsystems. That premium narrows in endurance-driven roles where fixed-wing efficiency halves per-hour operating costs over long sorties. RAND research notes that commercial scale should eventually compress military procurement prices as production volumes rise.

Endurance Limitations Due to Current Battery Energy Density Constraints

Nickel-rich lithium cells like the INR21700-P45B lead today’s eVTOL designs, yet simulations show shortfalls during high-load transition phases. Weight penalties restrict range, and elaborate thermal management adds mass, compounding the endurance gap. Hybrid configurations now deliver 25-plus extra minutes by optimizing battery-engine energy swaps, offering a near-term fix while solid-state chemistries mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: ISR Platforms Anchor Defense Modernization

ISR platforms dominated the fixed-wing VTOL UAV market in 2024 with a 46.89% share, and their 25.34% CAGR underlines sustained procurement for runway-independent surveillance. The V-BAT’s 10-hour endurance from a 12-foot deck illustrates why navies and border forces prioritize these aircraft. Commercial off-the-shelf sensors accelerate payload upgrades, expanding use cases into signals intelligence and disaster assessment.

Combat operations constitute the fastest-rising niche within the segment, propelled by trials of air-launched precision munitions such as Hero 120 from C-130 ramp deployment. Cross-domain tactics integrate hover-and-strike payloads, turning ISR airframes into multi-mission assets. Civil operators leverage ISR-derived optics for pipeline monitoring and wildlife protection, illustrating technology spillover across markets.

By Propulsion Type: Electric Dominance Faces Fuel-Cell Disruption

Electric powertrains held 53.75% of the fixed-wing VTOL UAV market share in 2024 as regulators favored noise- and emission-free craft. Fuel-cell models, however, scale faster at 27.56% CAGR because PEM stacks offer superior energy density on 2-hour-plus sorties.[3]Energy Conversion and Management, Li et al., “Fuel Cells as UAV Power Source,” ui.adsabs.harvard.edu Operators balancing endurance and sustainability increasingly view hydrogen as a long-term solution.

Hybrid-electric remains an essential bridge technology. A compound-wing demonstrator’s 25-minute endurance gain shows how battery-engine pairing can expand the fixed-wing VTOL UAV market size for long-range mapping missions. Conventional fuel systems persist for payload-heavy military tasks where rapid refueling trumps emission targets.

By Mode of Operation: Autonomy Gains Momentum

Remotely piloted aircraft made up 46.24% of sales in 2024, reflecting current rules. Yet autonomous models are projected to outpace at a 25.01% CAGR as onboard perception, edge computing, and fail-safe algorithms mature. Wing Aviation’s special-class certification for one-pilot control of 20 units foreshadows labor-efficient fleet economics.

Optionally piloted variants satisfy mixed regulatory environments, allowing operators to fly with onboard crews in restricted airspace or switch to remote mode in approved corridors. The gradual shift mirrors broader civil-aviation automation trends while preserving human oversight during early adoption phases.

By MTOW Class: Mid-Weight Platforms Hold Sway, Heavy Segment Accelerates

Aircraft weighing 25 to 150 kg represented 37.90% of the fixed-wing VTOL UAV market share in 2024, balancing deployability and payload for ISR and commercial surveys. The APUS 25’s 10 kg payload within a 24 kg frame typifies this sweet spot. Above 150 kg, growth at 25.78% CAGR is driven by defense requirements for heavier sensors and strike payloads, enabled by improved propulsion efficiency.

Sub-25 kg models target parcel delivery and urban inspection, where regulatory thresholds ease certification. Meanwhile, ultra-heavy demonstrators like Turkey’s 120 kg VTOL highlight an emerging class that could rival manned light aircraft on endurance and range.

By Range: Long-Distance Missions Drive Innovation

Medium-range units covered 41.25% of demand in 2024, with platforms such as the XAG M2000 flying 86 km per sortie. Long-range craft now expand at 26.34% CAGR as offshore energy, border patrol, and strategic ISR call for 1,000-km-class reach. Turkey’s 1,300 km prototype underscores the technical leap underway.

Short-range systems retain relevance for urban logistics and first-responder tasks where distance is secondary to rapid vertical access. The segmentation, therefore, maps directly to mission diversity rather than a linear evolution toward longer ranges.

Geography Analysis

North America led the fixed-wing VTOL UAV market with a 36.55% share in 2024, sustained by defense outlays, early BVLOS waivers, and strong domestic manufacturing. AeroVironment posted USD 821 million revenue in fiscal 2025 and is consolidating capabilities through the USD 4.1 billion BlueHalo acquisition to scale autonomous systems.[4]AeroVironment, “Fiscal 2025 Results,” avinc.com The FAA’s powered-lift rule and Dallas BVLOS precedent position the US for widespread commercial rollouts, while Canada and Mexico benefit from trilateral supply-chain alignment under USMCA.

Asia-Pacific is the fastest-growing region, with a 24.89% CAGR. China’s tilt-rotor prototype, Japan’s USD 25 million V-BAT buy, and South Korea’s electronics expertise reinforce a robust pipeline of defense and civil programs. Agricultural drone use, disaster response needs, and growing offshore-wind assets widen the civil addressable market. Local production incentives in India and Australia enhance cost competitiveness and encourage global export ambitions.

Europe’s growth is steady, anchored by EASA’s 2025 VCA framework that standardizes certification across member states. Germany’s battery-management know-how, France’s defense industrial base, and Scandinavia’s offshore-wind focus foster diverse demand. The DAPHNE hydrogen UAV illustrates Europe’s emphasis on zero-emission surveillance for environmental stewardship. UK CAP2537 guidance advances home-grown certification while Pan-EU airspace harmonization simplifies cross-border operations.

Competitive Landscape

The fixed-wing VTOL UAV market remains moderately fragmented. Incumbents leverage scale, while specialists differentiate through propulsion or autonomy. AeroVironment’s revenue surge and FreedomWerx facility highlight a strategy of vertical integration and acquisition-driven expansion. Joby and L3Harris joined forces in 2025 to merge eVTOL expertise with defense integration, targeting hybrid military platforms.

Disruptors such as Shield AI’s tail-sitter V-BAT gain traction for ship-borne missions, bypassing complex tilt-wing mechanisms. Technology convergence is accelerating: aerospace primes partner with software houses to embed AI navigation, while electronics firms enter the airframe space. Certification expertise and regulator relationships constitute key competitive moats alongside traditional performance metrics.

Fixed-Wing VTOL UAV Industry Leaders

AeroVironment, Inc.

Lockheed Martin Corporation

Quantum-Systems GmbH

Thales Group

Textron Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The Indian Army awarded ideaForge an emergency procurement contract worth INR 137 crore (USD 16.4 million) for hybrid Mini UAVs. The agreement covers vertical takeoff and landing drones that have received certification and undergone battle testing by the Indian armed forces.

- April 2025: AeroVironment received a USD 46.6 million contract from the Italian Ministry of Defence to supply its JUMP 20 VTOL medium uncrewed aircraft system (MUAS).

- April 2025: Survey Copter, an Airbus Defence and Space subsidiary specializing in light tactical drone systems, introduced a new VTOL version of its Aliaca drone.

Global Fixed-Wing VTOL UAV Market Report Scope

| Intelligence, Surveillance, and Reconnaissance (ISR) |

| Combat Operations |

| Border Management |

| Others |

| Electric |

| Hybrid-Electric |

| Fuel-Cell |

| Conventional |

| Autonomous |

| Remotely Piloted |

| Optionally Piloted |

| Less than 25 kg |

| 25 to 150 kg |

| Greater than 150 kg |

| Short Range |

| Medium Range |

| Long Range |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Intelligence, Surveillance, and Reconnaissance (ISR) | ||

| Combat Operations | |||

| Border Management | |||

| Others | |||

| By Propulsion Type | Electric | ||

| Hybrid-Electric | |||

| Fuel-Cell | |||

| Conventional | |||

| By Mode of Operation | Autonomous | ||

| Remotely Piloted | |||

| Optionally Piloted | |||

| By MTOW Class | Less than 25 kg | ||

| 25 to 150 kg | |||

| Greater than 150 kg | |||

| By Range | Short Range | ||

| Medium Range | |||

| Long Range | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Fixed-Wing VTOL UAV sector in 2025?

The Fixed-Wing VTOL UAV market size stands at USD 1.32 billion in 2025.

What is the growth outlook through 2030?

The market is projected to reach USD 3.79 billion by 2030, registering a 23.48% CAGR.

Which application area generates the most revenue?

ISR platforms account for 46.89% of 2024 revenue and maintain the fastest 25.34% growth pace.

Which region is expanding fastest?

Asia-Pacific leads growth with a 24.89% CAGR due to rising defense procurements and commercial projects.

What propulsion technology is gaining momentum beyond batteries?

Hydrogen fuel-cell systems are the fastest-growing propulsion segment, expanding at 27.56% CAGR.

Page last updated on: