Market Overview

| Study Period | 2019 - 2031 |

|---|---|

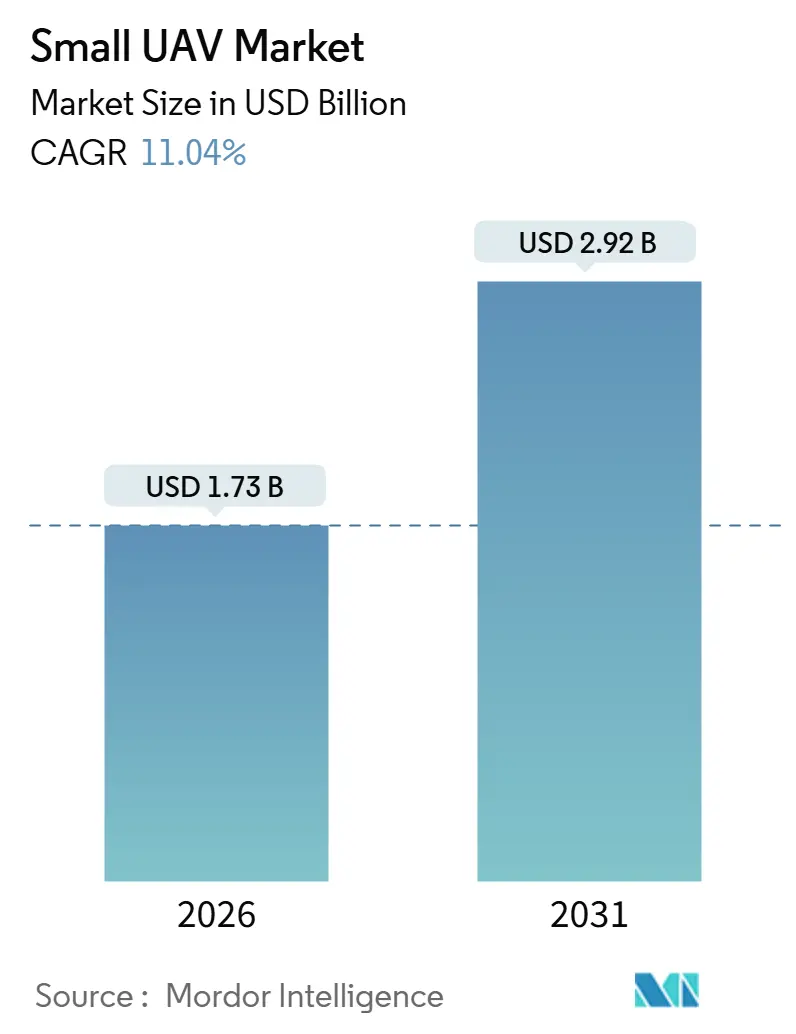

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.92 Billion |

| Growth Rate (2026 - 2031) | 11.04% CAGR |

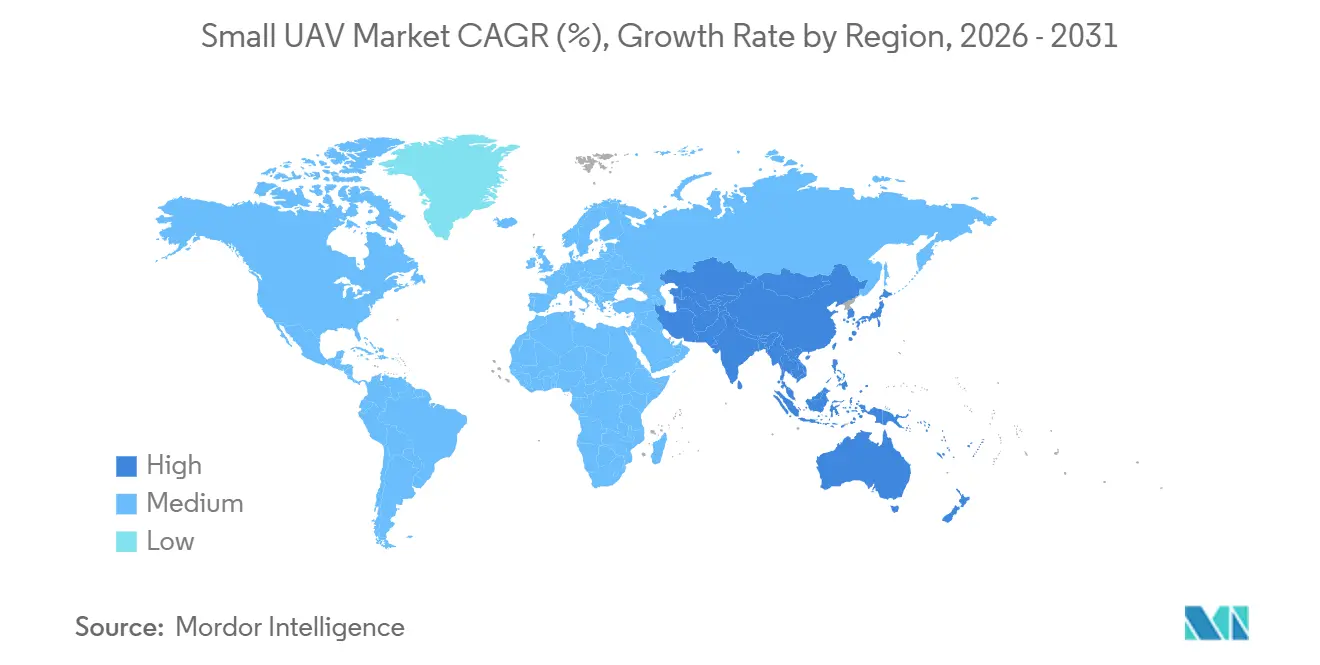

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

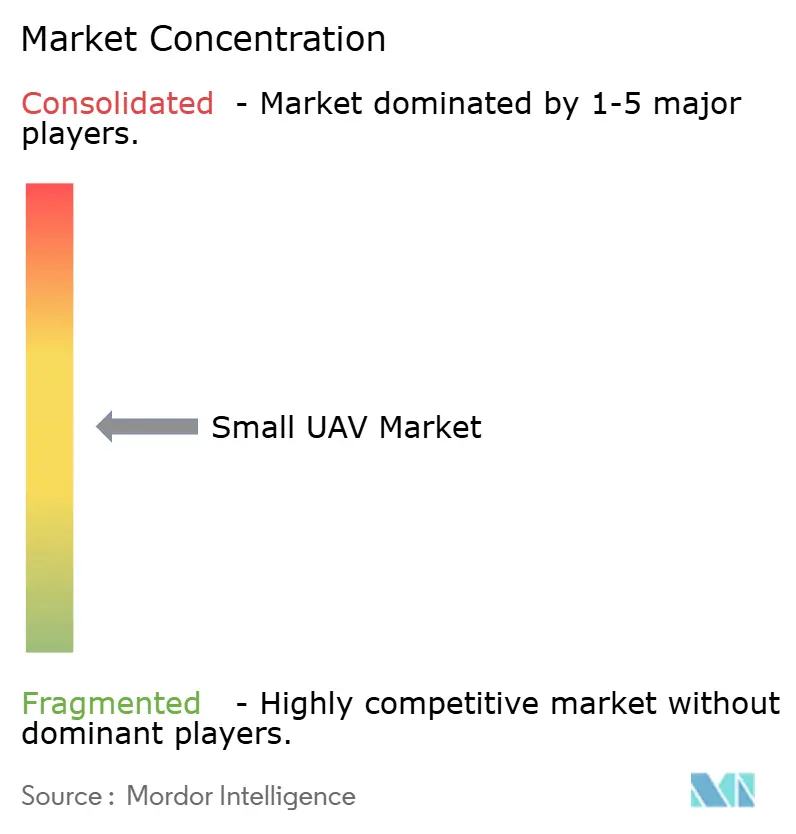

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small UAV Market Analysis by Mordor Intelligence

The small UAV market size is projected to reach USD 2.92 billion by 2031, expanding at an 11.04% CAGR over the forecast period, from USD 1.73 billion in 2026. Growth stems from the rapid transition away from crewed reconnaissance aircraft toward compact, expendable platforms that deliver real-time intelligence at far lower operating costs. Fixed-wing airframes currently hold the largest revenue share, yet demand is steadily shifting toward hybrid vertical-takeoff designs that eliminate runway dependence and reduce launch cycles. Weight-class preferences are also shifting: mini drones, weighing between 2 kilograms and 20 kilograms, dominate shipments, while nano and micro variants, weighing below 2 kilograms, are gaining traction within infantry squads for pocket-launched scouting. Mission sets continue to diversify; intelligence, surveillance, and reconnaissance (ISR) still lead volumes, but combat roles using loitering munitions are outpacing every other application following battlefield validation in Eastern Europe. North America anchors demand on the back of rising Pentagon budgets, whereas the Asia-Pacific emerges as the fastest-growing region, as China, India, and South Korea accelerate indigenous production.

Key Report Takeaways

- By wing type, fixed-wing platforms held 53.65% of the small UAV market share in 2025, while hybrid vertical-takeoff designs are forecasted to expand at a 13.92% CAGR through 2031.

- By size class, the mini category accounted for a 56.76% share of the small UAV market size in 2025, whereas nano and micro drones are projected to grow at a 11.45% CAGR through 2031.

- By application, ISR dominated with a 64.98% revenue share in 2025; however, combat missions deploying loitering munitions are projected to record the highest CAGR of 12.85% through 2031.

- By propulsion, battery systems captured 61.89% of the small UAV market size in 2025, while fuel-cell platforms are expected to advance at a 13.83% CAGR through 2031.

- By geography, North America led with a 46.91% revenue share in 2025, and the Asia-Pacific region is the fastest-growing, with a 12.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Small UAV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for real-time ISR in contested environments | +3.2% | Global, concentrated in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Force-multiplier value vs. crewed aircraft | +2.8% | Global, especially North America and Middle East | Long term (≥ 4 years) |

| DoD-funded soldier-borne and squad-level drone programs | +2.1% | North America, spillover to NATO allies | Short term (≤ 2 years) |

| AI-enabled autonomous swarming capability | +1.9% | North America, Asia-Pacific | Medium term (2-4 years) |

| DARPA projects for GPS-denied navigation | +1.5% | North America with allied tech transfer | Long term (≥ 4 years) |

| Rapid fielding of expendable loitering munitions | +2.3% | Global, early uptake in Europe and Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for Real-Time ISR in Contested Environments

Peer air-defense networks pose an unacceptable risk to crewed reconnaissance, so brigade commanders now rely on small UAV market platforms that cost one-tenth as much per flight hour as manned aircraft.[1]U.S. Army, “FY 2025 Future Tactical UAS,” ARMY.MIL The US Army earmarked USD 487 million for the Future Tactical UAS program in FY 2025, specifying a six-hour endurance and automatic target recognition capability to replace the legacy Shadow aircraft. Operational data from Ukraine indicated that small drones executed 78% of artillery-targeting missions in 2024, confirming their centrality to kill-chain closure. Consequently, procurement officers favor expendable systems fitted with sub-1 kilogram multi-spectral payloads such as the Puma 3 AE, which delivers targeting-quality imagery from 5 kilometers. The resulting budget reallocation from exquisite, crewed platforms to mass-produced drones is restructuring the ISR value chain.

Force-Multiplier Value vs Crewed Aircraft

Lifecycle analyses show a 10-to-1 operating-cost advantage for small UAV market fleets over helicopters, a ratio that is reshaping force designs.[2]RAND Corporation, “Cost Comparison of Manned vs. Unmanned ISR,” RAND.ORG A four-ship detachment of RQ-11 Ravens costs approximately USD 1.2 million per year to operate, compared to USD 12 million for a single reconnaissance helicopter of similar coverage. Reflecting this calculus, the US Marine Corps began retiring light-attack helicopter squadrons in 2025 in favor of infantry-organic drone companies. Japan plans to equip all 13 rapid-deployment brigades with mini-UAV platoons by 2027 without expanding pilot schools. The widened sensor envelope allows junior officers to call precision fires within seconds, further increasing combat efficiency.

DoD-Funded Soldier-Borne and Squad-Level Drone Programs

The FY 2025 US budget allocates USD 874.30 million to soldier-borne reconnaissance and lethal miniature aerial missile systems, pushing capability to the nine-soldier squad. AeroVironment won a five-year indefinite-delivery contract in March 2024 to provide Switchblade drones, ensuring every squad carries two organic loitering munitions. Separate DARPA field trials reduced operator cognitive load by 40%, enabling one soldier to control four drones simultaneously.[3]Defense Advanced Research Projects Agency, “Squad X Trials,” DARPA.MIL NATO interoperability standards issued in 2025 require member states to integrate squad-level drone datalinks with battlefield-management software, harmonizing procurement specifications. These requirements fuel demand for nano-class airframes, such as the 33-gram Black Hornet 4, which provides thermal imaging for 25 minutes.

AI-Enabled Autonomous Swarming Capability

The US Air Force Collaborative Combat Aircraft program demonstrated 20-drone autonomous swarms that routed threat radars with distributed jamming in 2025, validating edge-AI processors that allow on-board decision-making. DARPA’s Offensive Swarm-Enabled Tactics tests in 2024 showed 30 quadcopters clearing a 12-building complex in 18 minutes, proving collaborative autonomy in dense urban terrain. Anduril’s Ghost-X utilized Lattice software to assign ten drones to seven targets in a single salvo, reducing engagement time by 60% compared to human control.[4]Anduril Industries, “Ghost-X Fact Sheet,” ANDURIL.COM China’s People’s Liberation Army revealed similar launches during 2024 coastal exercises, indicating rapid technology diffusion. Defense agencies now prize software-defined platforms that can receive algorithm updates, tilting competitive advantage toward AI-centric vendors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber/EW vulnerability and counter-UAS proliferation | -2.1% | Global, acute in Europe and Middle East | Short term (≤ 2 years) |

| Short endurance and limited lethal payload | -1.4% | Global, affects extended-range Asia-Pacific missions | Medium term (2-4 years) |

| Export-control (ITAR/MTCR) hurdles | -0.9% | Exporting nations in North America/Europe; importing nations in Middle East/Africa | Long term (≥ 4 years) |

| Semiconductor and Li-ion cell supply-chain risk | -1.2% | Global, concentrated in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber/EW Vulnerability and Counter-UAS Proliferation

Adversaries employ jammers, lasers, and cyber exploits that compromise the effectiveness of the small UAV market, forcing manufacturers to invest in encrypted, frequency-hopping radios, which add USD 8,000-12,000 to each unit. Russian Pole-21 systems degraded GPS to 50 m CEP and severed quadcopter links along the Ukrainian front in 2024, triggering NATO anti-jam mandates. The US Naval Postgraduate School demonstrated that machine-learning (ML) jammers autonomously denied 92% of drone control links in trials, foreshadowing AI-driven counter-UAS networks. Directed-energy weapons are also maturing; Israel’s Drone Dome laser achieved 1,000 intercepts at a marginal USD 2 per shot in 2025. A higher attrition risk compels buyers either to pay for survivability upgrades or treat drones as disposable, thereby compressing margins.

Short Endurance and Limited Lethal Payload

Battery-powered craft rarely exceed 90 minutes aloft, limiting deep-strike or persistent ISR missions unless launch teams operate within 20 kilometers of targets, exposing them to enemy fire. The Army’s 2024 RQ-11 assessment led to the cancellation of 40% of sorties due to a lack of loiter time, thereby accelerating fuel-cell R&D efforts aimed at achieving six-hour endurance. Intelligent Energy’s 800-watt module hit 5.2 hours in 2025 tests but added 1.8 kilograms, reducing payload headroom. Warhead mass also constrains lethality; a 0.5-kilogram Switchblade 300 charge is effective only on soft targets, while the 18-kilogram Switchblade 600 requires vehicle transport, limiting infantry portability. The market bifurcates between ultra-light nano craft and heavier mini-UAVs, neither of which fully satisfies operational requirements, tempering adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wing Type: Hybrid Designs Accelerate Runway-Free Missions

Hybrid VTOL platforms are expanding at a 13.92% CAGR, the fastest pace among airframe architectures, as armies and navies seek drones that can launch without catapults or recovery nets, a decisive benefit in austere bases and ship decks. Fixed-wing craft still generated 53.65% of 2025 revenue on the strength of long-endurance ISR, cementing the segment’s lead in the small UAV market. Yet tiltrotors, such as Textron’s Aerosonde HQ, now win maritime contracts precisely because they can land back on small vessels despite the sea state, a feat that fixed-wing UAVs cannot match.

Hybrid configurations also dominate next-generation loitering munitions because vertical launch enables immediate response to fleeting targets. Anduril’s Roadrunner lifts off vertically, then sprints at Mach 0.6 for 100 minutes, pairing VTOL launch flexibility with jet endurance. Compliance with NATO STANAG 4703 airworthiness rules, which require controlled recovery, further favors platforms that can descend vertically into tight landing zones.[5]NATO, “Small-UAS Anti-Jam Requirements,” NATO.INT As a result, analysts expect hybrid models to command 25% of new procurement spending by 2028, steadily eroding the fixed-wing lead in the small UAV market.

By Size Class: Nano and Micro Variants Proliferate at Squad Level

Nano and micro drones weighing under 2 kilograms are projected to grow at an 11.45% CAGR through 2031, reflecting doctrinal moves to embed organic surveillance within every infantry squad. The mini segment retained 56.76% revenue share in 2025, demonstrating the slight market size advantage that larger airframes hold for multi-sensor payloads and three-hour endurance.

Teledyne FLIR shipped its 12,000th 33-gram Black Hornet 4 in September 2025, marking a 40% annual production increase that reflects steep battlefield demand for pocket-launched ISR. Meanwhile, India’s ideaForge posted a 60% revenue growth in FY2025, driven by a surge in Switch UAV orders, illustrating how emerging-market armies are leapfrogging to indigenous nano solutions. Regulatory relief accelerates adoption: The US FAA’s 2024 rule exempts craft weighing less than 250 grams from remote ID, thereby trimming compliance costs and shortening fielding timelines. Together, these trends are expected to lift nano and micro drones to roughly one-third of the small UAV market revenue by the end of the decade.

By Application: Loitering Munitions Redefine Combat Missions

ISR dominated 64.98% of 2025 demand; however, combat applications using loitering munitions are expanding at a 12.85% CAGR, as defense planners emphasize kill-chain compression. Ukraine’s reliance on one-way attack drones demonstrated low-cost lethality against armor and fortified positions, prompting many NATO members to re-allocate budgets toward strike-capable airframes.

The DoD’s Replicator initiative aims to field thousands of autonomous loitering munitions by 2027, underscoring how the small UAV market share associated with combat roles is expected to rise rapidly. AeroVironment’s Switchblade 600 secured USD 75 million in foreign military sales in 2024, as it offers precision strike capabilities at half the cost of anti-tank missiles. Electronic attack, logistics resupply, and training targets remain niche today but attract rising R&D as miniaturized gallium-nitride transmitters and modular payload bays unlock new mission sets.

By Propulsion Type: Fuel Cells Pursue Multi-Hour Endurance

Battery packs accounted for 61.89% of 2025 revenue, as lithium-polymer (LiPo) chemistry delivers 250 Wh/kg at a low cost and fits unit logistics, thereby anchoring their lead in the small UAV market. Yet, hydrogen fuel cells are advancing at a 13.83% CAGR, which is triple the growth rate of batteries, because special operations units require six-hour endurance to penetrate denied airspace.

Intelligent Energy’s 2.4 kW stack achieved a 7.5-hour flight time on a 25-kilogram prototype in 2025, but it carried a USD 18,000 price premium and complex hydrogen cartridges. The US Special Operations Command purchased 200 Protonex modules in 2024 to test that trade-off, suggesting fuel cells will gain share in high-value, long-range missions. Developers aim to target sub-USD 10,000 per kilowatt and solid-state storage by 2027, milestones that could shift a portion of the small UAV market size toward fuel cells.

Geography Analysis

North America generated 46.91% of 2025 revenue, buoyed by USD 1.1 billion in DoD small-UAS appropriations spanning Future Tactical UAS, Short-Range Reconnaissance, and Lethal Miniature Aerial Missile System lines. The US Army’s March 2024 indefinite-delivery award to AeroVironment for Switchblade variants typifies bulk procurement that anchors regional dominance. Canada devoted CAD 320 million (USD 166.81 million) in 2024 to mini-UAVs for Arctic patrol, employing drones instead of patrol aircraft for cost-effective polar coverage. Mexico followed in 2025 with a USD 45 million purchase of quadcopters for counter-narcotics missions, signaling growing homeland security demand.

The Asia-Pacific region is projected to post the highest growth at a 12.45% CAGR through 2031, led by indigenous programs in China, India, and South Korea that aim for strategic autonomy while reducing their exposure to Western export controls. China’s Aviation Industry Corporation introduced the Blowfish A3 loitering munition in 2024 for potential deployment in Taiwan-strait scenarios. South Korea signed a KRW 85 billion (approximately USD 57.68 million) quadcopter contract with Firstec in 2024 to enhance border surveillance and reduce overseas dependence. Australia chose Textron’s Aerosonde HQ VTOL drones for shipboard ISR in 2025, signaling maritime-focused demand.

Europe accounted for 28% of 2025 sales, inflated by wartime Ukrainian orders yet hampered by ITAR constraints that complicate US technology transfer. The UK Ministry of Defence funded GBP 75 million of domestic QinetiQ drones in 2024, emphasizing sovereignty over supply chains. In the Middle East, Israel Aerospace Industries, Turkey’s Baykar, and the UAE’s EDGE Group exploit permissive export rules to win contracts that Western firms cannot pursue under the ITAR, thereby enlarging their regional share to 12% of the small UAV market. South America and Africa remain nascent at 6%, but Brazil’s 2024 rainforest-surveillance program indicates wider internal-security adoption is imminent.

Competitive Landscape

The small UAV market features moderate fragmentation: the top five vendors, Northrop Grumman Corporation, AeroVironment, Inc., Teledyne Technologies Incorporated, Elbit Systems Ltd., and Lockheed Martin Corporation, captured a significant share of the 2025 defense revenue. Incumbents leverage installed fleets and sustainment contracts but confront margin pressure as buyers demand open-architecture systems that commoditize airframes. Venture-backed Anduril and Skydio erode share by bundling edge-AI software that bypasses GPS jamming, a differentiator that legacy suppliers retrofit at a higher cost.

Strategic moves center on vertical integration and software mergers and acquisitions. Teledyne’s 2024 USD 180 million battery acquisition secures cell supply amid 12-month lead times for Li-ion cells. Northrop Grumman invested USD 200 million to triple its Mississippi production space by 2025, indicating rising demand for autonomous strike platforms. Meanwhile, Baykar and the EDGE Group leverage export policy flexibility to serve African and Middle Eastern buyers who are restricted from US supply, reshaping geographic competition.

Patent activity corroborates the shift toward autonomy: the US Patent and Trademark Office granted 340 small-UAV autonomy patents in 2024, a 25% increase year-over-year, with Anduril, Shield AI, and Skydio accounting for 40% of the awards. Compliance barriers also rise; NATO STANAG 4703 airworthiness rules and the US National Defense Authorization Act’s Section 848 ban on Chinese electronics require transparent supply chains that favor established defense primes. Start-ups that combine AI software with compliant hardware stand to capture incremental share in the small UAV market.

Small UAV Industry Leaders

Northrop Grumman Corporation

AeroVironment, Inc.

Teledyne Technologies Incorporated

Lockheed Martin Corporation

Elbit Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: The US Army awarded Skydio a USD 7.9 million contract under the SRR Tranche 2 program to supply domestically manufactured X10D small UAS. The contract also includes provisions for support and training to improve close-range tactical reconnaissance capabilities for frontline units.

- August 2025: The US Army commenced production of the second tranche of short-range reconnaissance unmanned aircraft systems. Two vendors have been selected to provide networked SRR platforms designed to enhance battlefield situational awareness for Transformation in Contact units.

- June 2025: The Indian Army signed a USD 16.4 million contract with ideaForge for the procurement of hybrid mini-UAVs. This initiative aims to enhance drone capabilities using indigenous technology, mitigate supply chain vulnerabilities, and reduce dependence on foreign systems, thereby supporting secure and self-reliant defense strategies in the context of escalating geopolitical tensions.

- February 2025: AeroVironment, a global provider of multi-domain robotic systems, received its third delivery order, valued at USD 288 million, for Switchblade loitering munitions under the US Army’s Directed Requirement for Lethal Unmanned Systems. This order is part of a USD 990 million multi-year contract awarded in August 2024, bringing total awards to USD 471.3 million.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Small unmanned aerial vehicles are defined by Mordor Intelligence as remotely piloted or autonomous airframes that weigh up to 25 kg, fly below 400 ft, and rely on onboard batteries, fuel cells, or small combustion engines for propulsion. These craft serve civil, commercial, and defense tasks ranging from crop scouting and asset inspection to loitering munitions.

Scope exclusion: Platforms above 25 kg maximum takeoff weight and tethered drones lie outside this study.

Segmentation Overview

- By Wing Type

- Fixed Wing

- Rotary Wing

- Hybrid

- By Size Class

- Nano/Micro (Less than 2 kg)

- Mini (2 to 20 kg)

- Small (20 to 150 kg)

- By Application

- Intelligence, Surveillance, and Reconnaissance (ISR)

- Combat – Loitering Munition

- Logistics and Resupply

- Electronic Warfare (EW)

- Training and Simulation

- By Propulsion Type

- Internal Combustion Engine

- Batteries

- Fuel Cells

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Israel

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor's team interviewed drone assemblers, avionics suppliers, precision ag pilots, and procurement officers across North America, Europe, and Asia Pacific. These conversations validated price curves, mission mix shifts, and regulatory timelines that were only partly visible in public data.

Desk Research

Our analysts began with open datasets from regulators and trade bodies such as the FAA drone registry, EASA remote ID filings, UN Comtrade export codes 880220/880230, and SIPRI defense import logs, which together outline fleet additions and cross-border flows. Reports from IEEE Xplore, AUVSI, USDA crop spraying trials, and peer-reviewed journals on battery energy density trends added technical and demand context. Company 10-Ks and investor decks revealed unit shipments and ASP shifts, while curated feeds on Dow Jones Factiva and D&B Hoovers supplied timely contract awards. The sources cited illustrate the range consulted; many further references informed granular checks and clarifications.

Market Sizing and Forecasting

A top-down reconstruction starts with annual production plus net imports of sub-25 kg airframes, converted to value through region-weighted average selling prices, then cross-checked against sampled supplier revenues and fleet census growth. Variables such as military micro drone contract volume, FAA commercial registration counts, lithium-ion cost per Wh, sensor payload price erosion, and BVLOS waiver issuances feed the model. Multivariate regression combined with scenario analysis projects each driver to 2030, after which selective bottom-up roll-ups adjust anomalies before finalization.

Data Validation and Update Cycle

Outputs pass variance and outlier screens, peer review, and a final analyst sign-off. The model refreshes every twelve months, with interim updates triggered by sizeable regulatory or procurement events.

Why Mordor's Small UAV Baseline Earns Stakeholder Trust

Published estimates often diverge because firms pick dissimilar weight cutoffs, bundle services, or stretch forecast horizons. Our disciplined segmentation and annual refresh cadence narrow those gaps for decision makers.

Key gap drivers include wider weight ceilings adopted elsewhere, optimistic uptake assumptions for delivery drones, and currency conversions frozen at older rates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.56 B (2025) | Mordor Intelligence | - |

| USD 6.37 B (2025) | Global Consultancy A | Includes craft up to 150 kg and service revenues |

| USD 13.57 B (2024) | Industry Journal B | Uses list prices without regional ASP weighting |

| USD 27.34 B (2025) | Research Publisher C | Combines small, mini, and tactical classes plus accessories |

These contrasts show how Mordor's tight scope, variable-level cross-checks, and timely updates provide a balanced, transparent baseline that clients can replicate and defend.

Key Questions Answered in the Report

What is the current value of the small UAV market?

The small UAV market is valued at USD 1.73 billion in 2026 and is projected to reach USD 2.92 billion by 2031 at a CAGR of 11.04%.

Which size class leads procurement today?

Mini UAVs weighing 2 to 20 kilograms held 56.76% of 2025 revenue due to their balance of endurance and payload capacity.

Why are hybrid VTOL designs gaining popularity?

They remove the need for runways or launch gear, enabling reconnaissance and strike missions from ships and austere bases.

What propulsion trend is most disruptive?

Hydrogen fuel-cell systems, growing 13.83% annually, promise six-hour endurance for deep ISR despite higher cost and logistics complexity.

Which region is growing fastest?

Asia-Pacific is expanding at a 12.45% CAGR to 2031, driven by indigenous programs in China, India and South Korea.

What technology is helping small UAVs stay operational when GPS signals are jammed?

Defense buyers are fitting drones with AES-256 encrypted, frequency-hopping radios and onboard AI navigation, upgrades that add USD 8,000–12,000 per unit but keep control links intact in electronic-warfare environments.

Page last updated on: