UAV Propulsion Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.92 Billion |

| Market Size (2031) | USD 19.08 Billion |

| Growth Rate (2026 - 2031) | 9.87% CAGR |

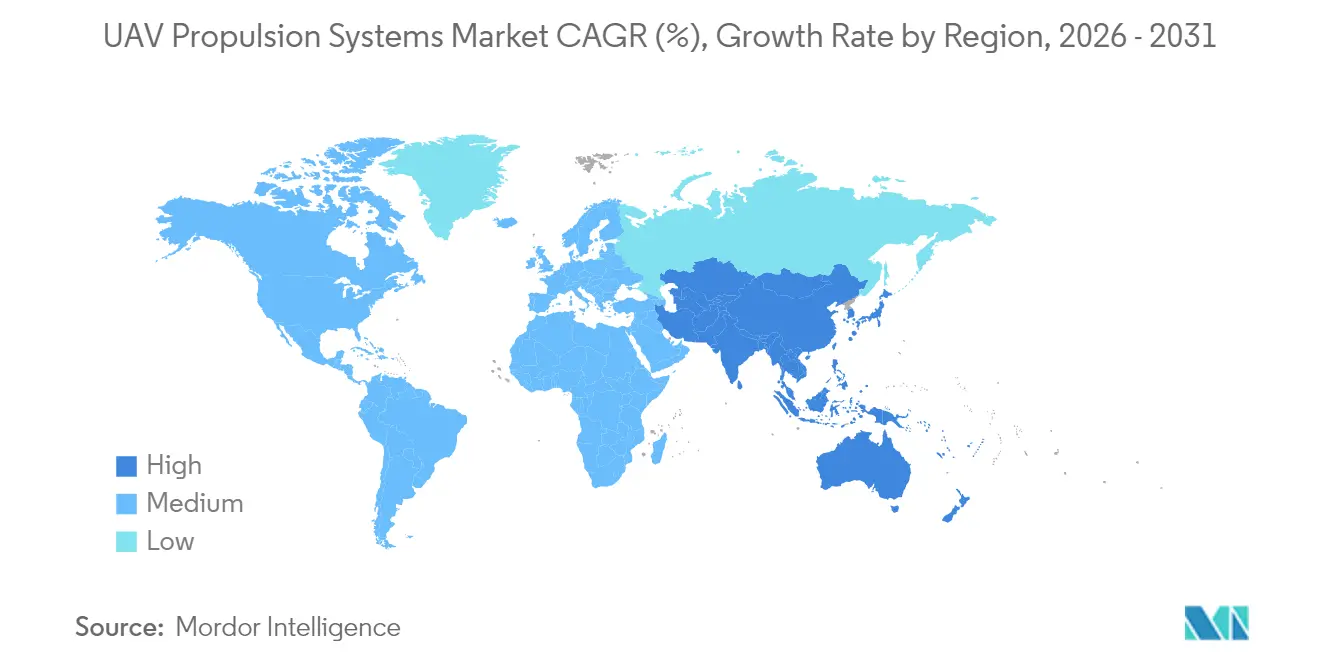

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

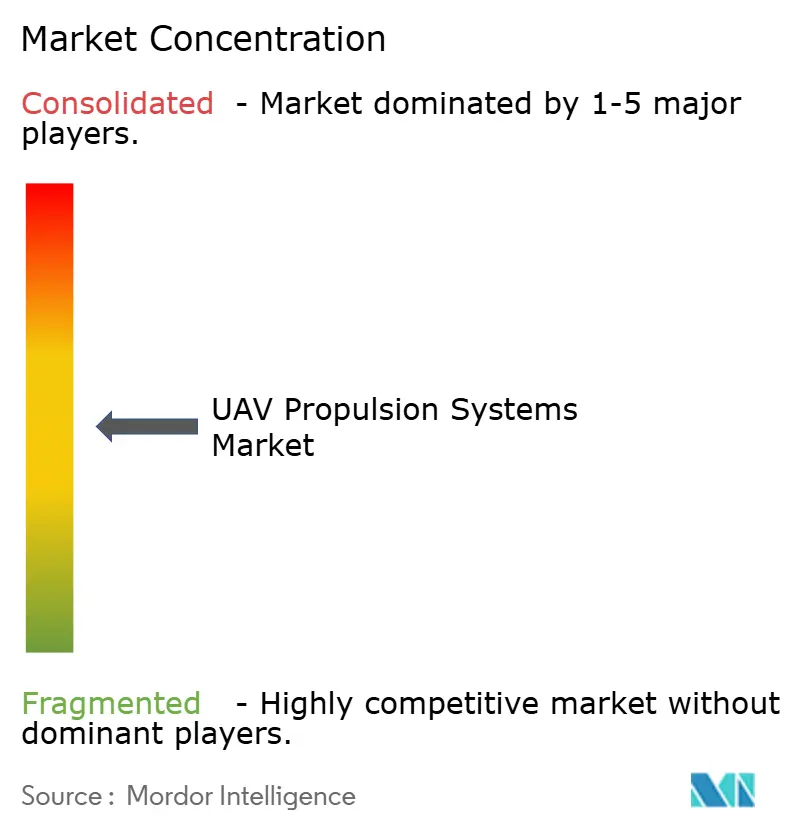

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAV Propulsion Systems Market Analysis by Mordor Intelligence

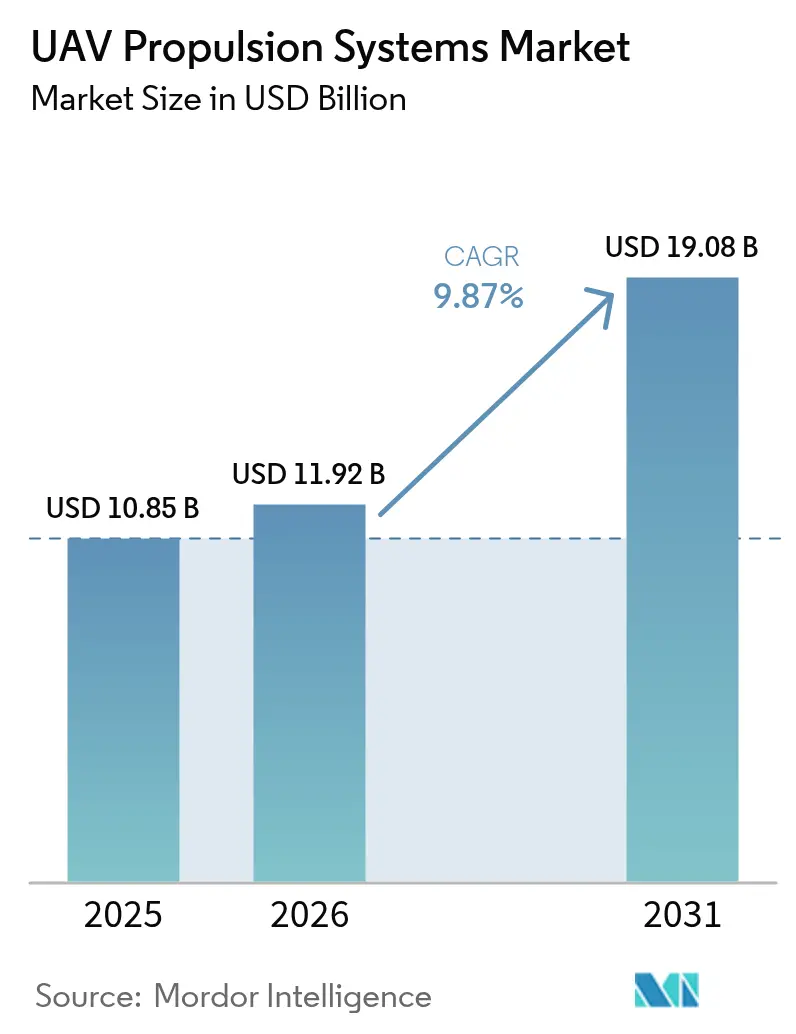

The UAV propulsion systems market size was valued at USD 10.85 billion in 2025 and estimated to grow from USD 11.92 billion in 2026 to reach USD 19.08 billion by 2031, at a CAGR of 9.87% during the forecast period (2026-2031). Growth stems from strong defense spending, rising autonomy requirements, and rapid maturation of electric-hybrid and hydrogen architectures that meet modern operations' stealth, endurance, and cost criteria. Additive manufacturing slashes turbine component counts, fuel-cell stacks gain power density, and advanced turbogenerators turn heavy-fuel logistics into electric power at remote bases. At the same time, export-control and raw-material constraints complicate sourcing, making propulsion strategy a decisive factor in program schedules and fleet readiness. Collectively, these forces re-shape platform design, maintenance models, and acquisition roadmaps across the UAV propulsion system market

Key Report Takeaways

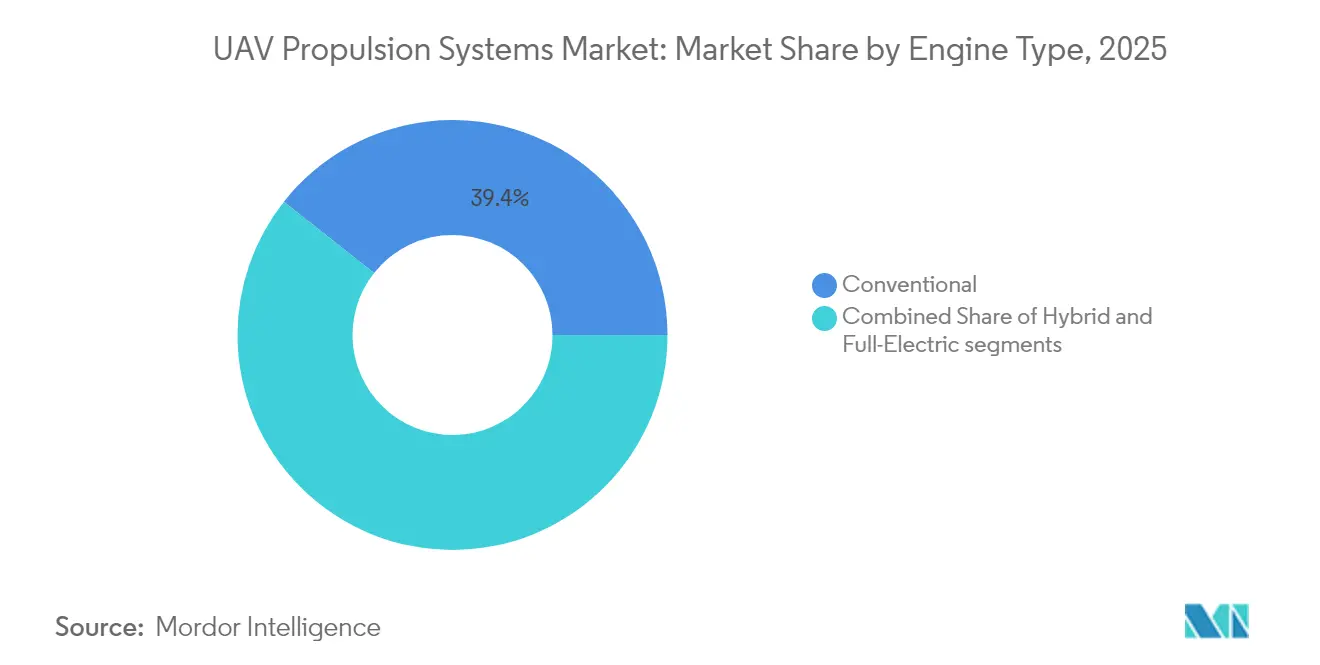

- By engine type, conventional units led the UAV propulsion systems market with 39.35% of the share in 2025; full-electric systems are projected to grow at 12.68% CAGR to 2031.

- By fuel type, gasoline captured a 43.05% share of the UAV propulsion systems market size in 2025, while hydrogen systems recorded the highest 13.08% CAGR through 2031.

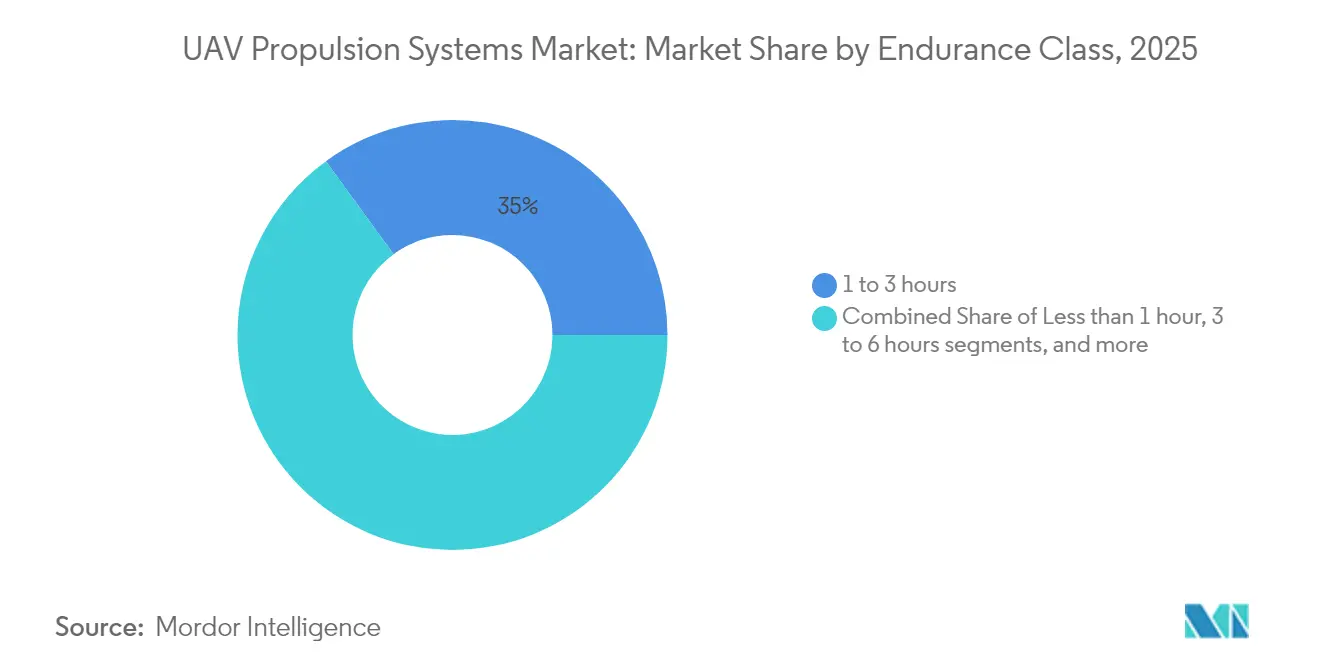

- By endurance class, the 1–3 hour category held 35.02% share in 2025; platforms exceeding 6 hours advance at a 10.12% CAGR to 2031.

- By UAV type, tactical platforms commanded 40.78% of 2025 revenue; HALE systems posted the fastest 12.06% CAGR during the forecast window.

- By geography, North America retained a 33.40% share in 2025, whereas Asia-Pacific is set to register an 11.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global UAV Propulsion Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e- and hybrid-electric demand | +2.1% | Global with early adoption in North America and Europe | Medium term (2–4 years) |

| Military swarm drone operations and autonomous combat systems | +1.8% | North America and EU leading, expanding to APAC defense markets | Short term (≤ 2 years) |

| Defense modernization budgets for MALE/HALE UAVs | +1.5% | Global, concentrated in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Drone-as-a-service retrofit kits | +0.9% | Global, focusing on existing fleet operators | Medium term (2–4 years) |

| Hydrogen fuel-cell range-extender breakthroughs | +1.2% | Europe and North America leading, Asia-Pacific following | Long term (≥ 4 years) |

| Additive-manufactured micro-turbine cost deflation | +0.7% | North America and Europe manufacturing hubs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in E- and Hybrid-Electric Demand

Electric and hybrid-electric propulsion lowers acoustic and infrared signatures, simplifies maintenance at austere bases, and trims supply-chain weight by replacing bulk liquid fuel with modular battery packs. DARPA’s XRQ-73 SHEPARD hybrid, powered by Northrop Grumman’s 1,250-lb system, illustrates how series configurations deliver multi-hour loiter without compromising stealth.[1]Defense Advanced Research Projects Agency, “XRQ-73 SHEPARD hybrid-electric demonstrator,” darpa.mil Honeywell’s 1 MW turbogenerator scales these gains for heavy cargo drones, tripling earlier power levels and enabling distributed electric motors on larger wings. Defence ministries now budget for silent ingress drones that avoid acoustic detection at border standoff ranges. Procurement offices highlight simplified line-replaceable units that cut mean-time-to-repair, making electric-hybrid propulsion central to future tenders. In turn, the UAV propulsion system market sees incumbents partner with inverter, battery, and thermal-management specialists to balance power-to-weight targets with battlefield durability.

Military Swarm Drone Operations and Autonomous Combat Systems

Swarm concepts deploy dozens to hundreds of small, networked drones that saturate defenses, demand rapid thrust response, and accept higher attrition. US Army “launched effects” experiments showcase miniature engines and electric fans engineered for mass production and pre-flight self-diagnostics.[2]Army Recognition, “US Army launched effects and Gray Eagle 25M updates,” armyrecognition.com Germany’s EUR 100 billion (USD 117.7 billion) rearmament makes loitering munitions and autonomous wingmen core spending areas, creating large-volume opportunities for identical propulsion pods that clip into disposable airframes. Powerplants need common digital interfaces so AI mission controllers can manage throttle, health, and emergency shutdown across the swarm. Standardization accelerates depot assembly lines and lowers life-cycle cost, a key metric when each mission may consume dozens of vehicles. Swarm adoption, therefore, accelerates mini-motor innovation and stretches production capacity within the UAV propulsion system market.

Defense Modernization Budgets for MALE/HALE UAVs

Armed forces allocate record funds to long-endurance surveillance and strike platforms that rely on robust propulsion. The US Army National Guard’s Gray Eagle 25M engine upgrade delivers over 40 hours at 29,000 feet and exemplifies demand for heavy-fuel efficiency at altitude. Germany’s EUR 100 billion (USD 117.9 billion) rearmament package channels fresh capital to loitering munitions and autonomous wingmen, stimulating powerplant R&D across Europe. Military buyers value extensive mean-time-between-overhaul data, standardized logistics, and field-serviceable modules. Suppliers that prove endurance under harsh climates can secure premium contracts and multiyear sustainment revenue. Defense investment thus underpins baseline volumes and learning curves that later spill into civil portions of the UAV propulsion systems market.

Hydrogen Fuel-Cell Range-Extender Breakthroughs

Hydrogen fuel cells combine silent exhaust with energy density above batteries, delivering covert endurance. Skyeton’s Raybird test flight reached a planned 15 hours on gaseous hydrogen, demonstrating military-grade viability for low-signature ISR.[3]FuelCellsWorks, “Skyeton hydrogen-powered Raybird UAV,” fuelcellsworks.comIntelligent Energy’s IE-FLIGHT F300 attains 1.5 kW/kg through high-temperature heat rejection, letting small wings carry heavier sensors without fuel penalties. Cooling fans emit minimal audio, preserving stealth during night missions. Logistics hurdles shrink as defence agencies trial mobile electrolyzers that refill composite tanks at forward outposts. Hydrogen propulsion, therefore, unlocks new mission sets and positions green logistics as a force multiplier inside the UAV propulsion system market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery energy-density plateau | -1.4% | Global, affecting all electric UAV segments | Short term (≤ 2 years) |

| Rare-earth magnet supply constraints | -0.8% | Global, with acute impact on motor producers | Medium term (2–4 years) |

| Export-control (ITAR/MTCR) restrictions | -0.6% | International markets, US-based manufacturers | Long term (≥ 4 years) |

| Ultra-low thermal-/acoustic-signature thresholds for contested airspace | -0.4% | Indo-Pacific flashpoints, Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Battery Energy-Density Plateau

Lithium-ion chemistries remain locked near 300 Wh/kg; tactical eVTOL sorties at 10–60 °C discharge trigger fast degradation and shorten battery life to under 100 combat cycles.[4]ACS Publications, “Battery performance for eVTOL conditions,” pubs.acs.org Resulting 20–30 minute flight times force armies to stock spare packs or add hybrid boosters, raising the logistical burden. Thermal spikes require liquid-cooled enclosures that add weight and lower payload. Solid-state and lithium-sulfur prototypes show promise but need scale to meet NATO safety rules. Until then, battery limits cap pure-electric adoption, moderating the expansion pace in segments of the UAV propulsion system market.

Rare-Earth Magnet Supply Constraints

High-torque motors rely on neodymium and dysprosium, 80% refined in China. Upcoming US sourcing mandates raise costs and extend lead times for domestic engine lines. Substituting ferrite magnets cuts dependence yet doubles motor volume, hurting aero efficiency. Mining projects in Australia and the US will ease pressure post-2028 but require upfront capital that smaller vendors lack. Current scarcity pushes procurement offices toward hybrid engines with reduced magnet content, slowing all-electric uptake across the UAV propulsion system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Type: Electric Architectures Drive Innovation

Conventional engines held 39.35% of the UAV propulsion system market 2025, signaling entrenched reliability for high-hot and sandy environments. Yet full-electric units expand at a 12.68% CAGR thanks to stealth, maintenance, and modular benefits that resonate with modern doctrines. Hybrid generators bridge payload gaps by handing cruise loads to heavy-fuel turbines while batteries power silent ingress. Print-to-fly micro-turbines democratize jet performance for expendable munitions, tightening competition between combustion and electric lines. Investors steer R&D toward common-core inverters and digital twins that cut unplanned downtime, reinforcing adoption curves across the UAV propulsion system market.

Platform integrators prefer engines delivered as sealed sub-systems with embedded health-monitoring that feed fleet-wide analytics. Electric motors achieve 98% efficiency at cruise, slashing infrared traces. Conversely, heavy-fuel two-strokes remain essential for Arctic and desert outposts where kilowatt-class generators power onboard heaters and de-icing kits. Procurement agencies thus request plug-and-play architecture that toggles between power modes, accelerating component reuse and lowering spares inventory exposure. This modular philosophy underpins forecast dominance of hybrid-ready designs in the UAV propulsion system market.

By Fuel Type: Hydrogen Emerges as Range Solution

Gasoline held a 43.05% share of the UAV propulsion systems market size in 2025, supported by global availability and proven cold-start reliability. Hydrogen solutions register the highest 13.08% CAGR as power density gains and green-hydrogen infrastructure scale converge to unlock extended sorties at near-silent acoustic profiles. Heavy-fuel JP-8 variants maintain relevance for defense users who prioritize logistics commonality and shipboard safety. Battery-only configurations dominate sub-10 kg payload classes where missions last under one hour. Demonstrators such as China’s liquid-hydrogen fixed-wing prototype prove that cryogenic fuel can support large UAVs, although storage and venting standards are still evolving.

Solar-assisted craft remains a narrow niche yet drives material research for ultrathin photovoltaics that could pair with hydrogen range extenders. Refueling times for compressed gas undercut battery recharge cycles, giving hydrogen an edge in availability for high sortie frequency models. Fuel selection influences cooling strategy, mission planning, and carbon accounting metrics, which now appear in European and Asian public tenders. Suppliers therefore engineer modular tanks and quick-disconnect valves that integrate with multiple airframe sizes, safeguarding residual value as technology choices shift through the UAV propulsion systems market.

By Endurance Class: Extended Operations Drive Demand

The 1–3 hour class captured the largest 35.02% share of the UAV propulsion systems market in 2025 because it matches current battery capability and common inspection routes. Platforms exceeding 6 hours grow at 10.12% CAGR as border security, maritime patrol, and construction sites seek persistent eyes in the sky. Propulsion cost scales steeply with endurance because hybrid or fuel-cell stacks add systems weight and integration complexity. However, the total cost per flight hour falls when missions replace manned helicopters or satellites, a key argument in defense budget debates. Long endurance solutions also prove valuable for telecom relay and atmospheric research, broadening the customer mix.

Hybrid-electric propellers shift loads between battery bursts for climb and internal combustion cruise, easing thermal spikes while stretching range. Fuel selection, cooling method, and redundancy architecture create divergent bill-of-material paths for OEMs, challenging supply chains. Sensors that monitor vibration and exhaust chemistry feed AI models that predict remaining useful life, a must for platforms that stay airborne multiple days. Endurance, therefore, dictates spare parts logistics, satellite bandwidth allocation, and even insurance premiums, elevating its role in purchase decisions within the UAV propulsion systems market.

By UAV Type: HALE Systems Lead Innovation

Tactical UAVs generated 40.78% revenue in 2025 due to their broad use in reconnaissance and target acquisition. HALE platforms expand at 12.06% CAGR because telecom, environmental monitoring, and defense agencies need continuous coverage that rivals satellites. High-altitude endurance requires propulsion with exceptional specific fuel consumption or hybrid fuel-cell booster modules that function in thin air. The push for solar-electric HALE concepts drives new motor insulation and low-temperature lubricant formulations.

Mini and micro UAVs rely on compact battery packs and low-noise direct-drive motors, making them ideal for urban inspection and first-response missions. MALE types occupy mid-range roles such as pipeline surveillance and maritime patrol, usually with heavy-fuel piston engines supplemented by electric starter-generators. UAV type therefore frames adhesive choices, cooling designs, and control firmware, influencing the entire procurement workflow. Vendors who field common propulsion cores across multiple UAV categories can leverage scale and simplify spares, strengthening positioning across the UAV propulsion systems market.

Geography Analysis

North America sustained 33.40% share in 2025 because Pentagon programs, FAA test corridors, and Silicon Valley capital coalesce into robust demand and swift certification pipelines. DARPA and AFWERX grants de-risk early-stage engines, while US Navy shipboard tests evaluate hydrogen refueling at sea. Policy aligns state energy credits with base microgrid upgrades, incentivizing hybrid adoption.

Asia-Pacific posts the strongest 11.32% CAGR as China’s trillion-yuan low-altitude economy charter encourages domestic propulsion lines and subsidizes fuel-cell trial fleets. India’s Atmanirbhar initiative channels offset funds into heavy-fuel piston and hybrid labs to cut reliance on imported electronics. Japan pioneers gas-turbine electric hybrids for urban eVTOL, and South Korea includes hydrogen drones in its defence-export masterplan. Diverse regulatory codes create export-variant complexity yet drive parallel innovation, expanding overall opportunity within the UAV propulsion system market.

Europe grows steadily as EASA enforces noise and CO₂ caps that tilt spending toward electric and hydrogen. France and Germany co-finance HyPoTraDe to validate cross-border hydrogen cargo corridors. The UK backs additive turbine centers that accelerate Type-Cert demonstrations for heavy-fuel engines destined for Loyal Wingman programs. Carbon pricing boosts ROI for zero-emission powerplants, and collective research networks ensure shared lessons, reinforcing continental momentum across the UAV propulsion system market.

Competitive Landscape

The UAV propulsion systems market features a blend of legacy aerospace corporations, specialist engine houses, and fast-moving startups. Rolls-Royce and General Electric adapt civil turbofan cores to lighter military drones, pairing historic reliability data with incremental weight reduction. Honeywell couples turbo-generator know-how with advanced inverters to produce turnkey hybrid-electric modules ready for cargo drone integrators. Kratos and GE’s teaming agreement merges small engine heritage with mass-production muscle, indicating an industry shift toward collaboration rather than vertical integration.[5]GE Aerospace, “Small engine partnership with Kratos,” ge.com

Additive-manufacturing disruptors such as Beehive Industries cut part numbers from thousands to under twenty, halving cost and easing sustainment. Fuel-cell pioneers Intelligent Energy and H3 Dynamics secure aerospace adaptations by proving high-power-to-weight stacks with integrated cooling. Meanwhile, magnet-free motor developers target supply-chain independence from rare earths. Competitive intensity centers on certification speed, lifecycle cost modeling, and integration support for avionics and thermal systems. Suppliers that embed digital twins and predictive maintenance analytics into propulsion packages gain an advantage through reduced operator risk and downtime, strengthening their hold on strategic contracts within the fragmented yet rapidly consolidating UAV propulsion systems market.

Market consolidation accelerates: AeroVironment acquires BlueHalo to fuse propulsion, electronic warfare, and autonomy in one catalogue; Honeywell aligns with Regal Rexnord for eVTOL actuation. Providers with vertically integrated repair networks and digital-twin analytics secure long-term performance-based logistics deals, tightening switching costs and nudging the UAV propulsion system market toward higher concentration.

UAV Propulsion Systems Industry Leaders

Honeywell International Inc.

Rolls-Royce plc

General Electric Company

UAV Engines Limited

Hirth Engines GmbH (UMS SKELDAR)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The US Army awarded Electra Aero a USD 1.9 million Small Business Innovation Research (SBIR) contract to investigate hybrid-electric propulsion benefits. The contract requires Electra Aero to conduct technology maturation and risk reduction activities to assess the aircraft's mission capabilities like its EL9 model, specifically focusing on range and fuel consumption.

- June 2025: H3 Dynamics and XSun unveiled plans for a solar-hydrogen-electric tribrid drone capable of 12 hours and 600 km range.

- June 2025: GE Aerospace and Kratos advanced their GEK800 and GEK1500 small engines under a new teaming pact.

- November 2024: The US Air Force awarded USD 12.4 million to Beehive Industries to develop additively manufactured 200-lb-thrust expendable engines.

Global UAV Propulsion Systems Market Report Scope

The propulsion system of a UAV produces and supplies the necessary power to ensure continuous flight. While conventional UAV propulsion systems store energy in the form of fuel and utilize an internal combustion (IC) engine to drive the propellers, an electric propulsion system utilizes energy storage devices, such as batteries and fuel cells. In a hybrid configuration, two propulsion technologies are integrated onboard a UAV that works in tandem to eliminate the performance limitations of individual propulsion systems. The market forecast is based on the line-fit installations of propulsion systems integrated onboard the various types of UAVs being delivered across the world.

The UAV propulsion systems market is segmented by type, application, UAV type, and geography. By type, the market is segmented into conventional, hybrid, and full-electric. By application, the market is segmented into civil, commercial, and military. By UAV type, the market is segmented into micro, mini, tactical, MALE, and HALE. The report also covers the market sizes and forecasts for the UAV propulsion systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Conventional |

| Hybrid |

| Full-Electric |

| Gasoline |

| Heavy Fuel |

| Hydrogen |

| Battery (Li-ion, Li-S) |

| Solar-Augmented |

| Less than 1 hour |

| 1 – 3 hours |

| 3 – 6 hours |

| Greater than 6 hours |

| Micro UAV |

| Mini UAV |

| Tactical UAV |

| MALE UAV |

| HALE UAV |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Engine Type | Conventional | ||

| Hybrid | |||

| Full-Electric | |||

| By Fuel Type | Gasoline | ||

| Heavy Fuel | |||

| Hydrogen | |||

| Battery (Li-ion, Li-S) | |||

| Solar-Augmented | |||

| By Endurance Class | Less than 1 hour | ||

| 1 – 3 hours | |||

| 3 – 6 hours | |||

| Greater than 6 hours | |||

| By UAV Type | Micro UAV | ||

| Mini UAV | |||

| Tactical UAV | |||

| MALE UAV | |||

| HALE UAV | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the UAV propulsion systems market?

The market is valued at USD 11.92 billion in 2026 and is projected to reach USD 19.08 billion by 2031.

Which engine type is growing fastest within this market?

Full-electric architectures are expanding at a 12.68% CAGR, outpacing conventional and hybrid systems.

Why is hydrogen gaining traction in UAV propulsion?

Hydrogen fuel cells deliver higher energy density than batteries, enabling flights beyond 15 hours while emitting only water, which meets upcoming environmental rules.

Which region will add the most new revenue through 2031?

Asia-Pacific shows the highest 11.32% CAGR, propelled by large-scale initiatives in China and indigenous manufacturing programs in India.

How do battery limitations affect UAV operations?

Lithium-ion packs cap energy density near 300 Wh/kg, restricting pure-electric flight to under one hour and prompting moves toward hybrid or hydrogen solutions.

What factors increase market concentration?

Certification complexity, supply chain control of advanced materials, and the need for integrated electric-hybrid expertise drive mergers and strategic alliances among leading propulsion suppliers.

Page last updated on: