Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.98 Billion |

| Market Size (2031) | USD 12.72 Billion |

| Growth Rate (2026 - 2031) | 12.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

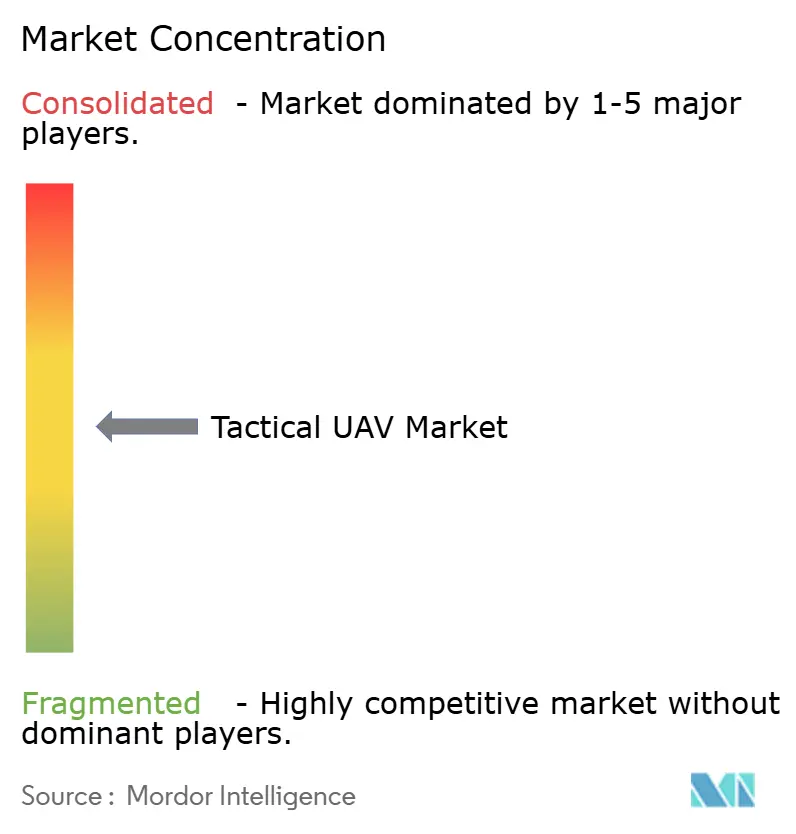

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tactical UAV Market Analysis by Mordor Intelligence

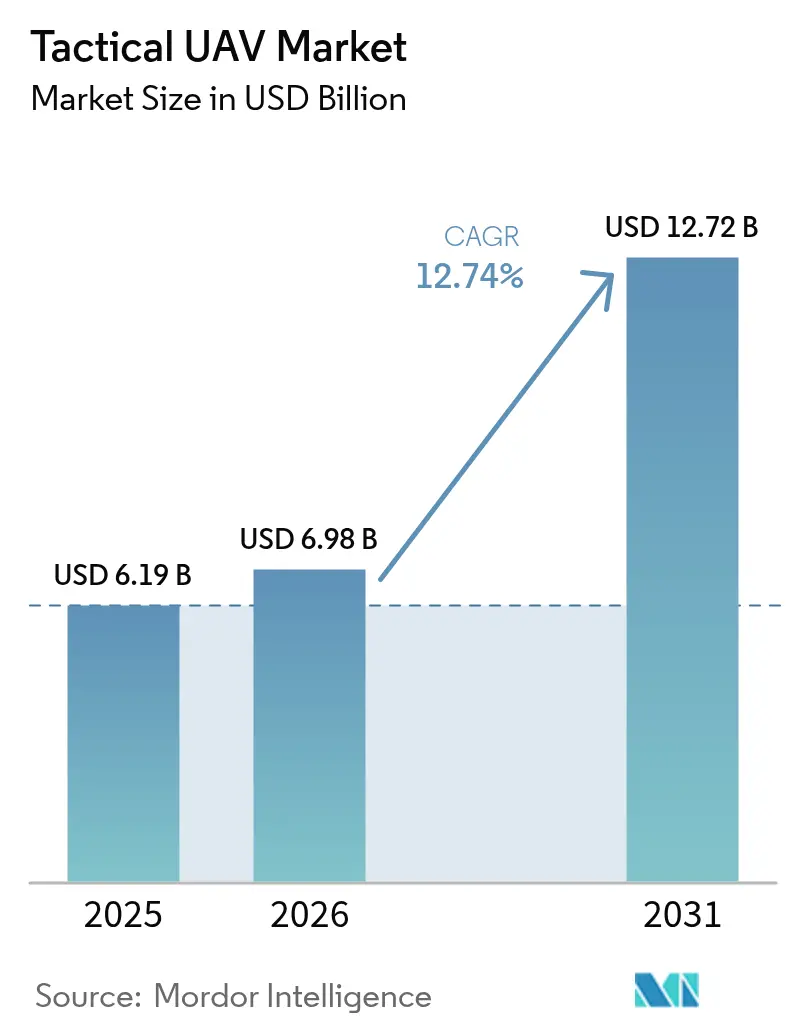

The tactical UAV market size is expected to grow from USD 6.19 billion in 2025 to USD 6.98 billion in 2026 and is forecast to reach USD 12.72 billion by 2031 at 12.74% CAGR over 2026-2031. The upward trajectory reflects global defense-modernization programs prioritizing unmanned systems for intelligence gathering, precision strike, and force-multiplication roles. Growing allocations to autonomous platforms, lessons learned from recent high-intensity conflicts, and the push to reduce aircrew risk reinforce demand. The lower life-cycle cost profile of tactical drones versus comparable manned aircraft and rapid advances in electric propulsion, miniaturized sensors, and AI-enabled autonomy also draws military buyers. At the same time, suppliers are racing to secure rare-earth component chains and to harden command-and-control links against electronic warfare, as cyber vulnerabilities and spectrum congestion threaten operational scalability.

Key Report Takeaways

- By platform, fixed-wing systems held 60.74% of the tactical UAV market share in 2025, while hybrid VTOL platforms are projected to expand at a 15.31% CAGR through 2031.

- By weight class, medium tactical UAVs accounted for 41.83% of the tactical UAV market size in 2025, whereas micro/nano drones under 5 kg are advancing at a 16.08% CAGR through 2031.

- By range, medium-range platforms (50 to 200 km) captured a 44.92% share of the tactical UAV market in 2025, but extended-range systems above 200 km led growth at a 14.72% CAGR to 2031.

- By propulsion type, conventional engines retained 63.71% share of the tactical UAV market size in 2025, while electric propulsion variants are climbing at a 15.46% CAGR to 2031.

- By application, military programs represented 79.68% of the tactical UAV market size in 2025 and are forecasted to grow at a 13.09% CAGR through 2031.

- By geography, North America led with 31.45% revenue share in 2025; Asia-Pacific registers the fastest regional CAGR at 13.18% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tactical UAV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing defense-modernization budgets | 2.80% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Soaring demand for ISR and real-time data | 1.90% | Global conflict zones and border regions | Short term (≤2 years) |

| Border security and counter-terror ops | 1.70% | North America, Europe, Middle East, Asia-Pacific borders | Short term (≤2 years) |

| Lower life-cycle cost versus manned assets | 1.40% | Cost-conscious emerging markets | Medium term (2-4 years) |

| AI-enabled swarm and teaming doctrines | 1.20% | United States, China, Europe, Israel | Long term (≥4 years) |

| Naval deck-based launch and recovery needs | 0.90% | United States, United Kingdom, China, India, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Defense-Modernization Budgets

Major armed forces are shifting procurement toward unmanned systems that augment combat power while minimizing aircrew risk. The US Department of Defense’s 2025 accelerated drone acquisition pathway illustrates this re-prioritization and channels fresh funding into domestic programs.[1]Department of Defense, “2025 Budget Overview,” defense.gov Lessons from recent Russo-Ukrainian engagements have reinforced the value of small tactical drones for target acquisition and precision strikes, prompting allied European nations to add uncrewed aerial systems to capability roadmaps. Emerging markets echo this pattern because tactical platforms offer a lower entry cost versus manned aircraft yet deliver comparable surveillance coverage. Parallel investments in secure datalinks and resilient supply chains aim to reduce exposure to single-source component risks and to comply with tightening national-security regulations. These modernization projects should collectively maintain double-digit demand growth through the end of the decade.

Soaring Demand for ISR and Real-Time Data

Commanders rely on persistent intelligence, surveillance, and reconnaissance to compress decision cycles. Tactical UAV fleets now carry multi-spectral sensors that stream encrypted video directly to mobile command posts, trimming the observe-orient-decide-act loop from hours to minutes. Swarm initiatives within several NATO member states explore hundreds of interoperable drones that share target data autonomously, broadening situational awareness over dispersed battlefields. Civil agencies adopt similar ISR capabilities for large-event crowd oversight and natural-disaster assessment, further expanding the customer base. Improvements in on-board processors permit edge-level object recognition, reducing bandwidth needs and operator workload. The resulting operational agility positions the tactical UAV market demand for sustained expansion even outside core defense niches.

Border Security and Counter-Terror Operations

National border agencies deploy small and medium tactical UAVs to monitor remote frontiers that ground patrols cannot blanket efficiently. High-resolution electro-optical and thermal imagers detect illicit crossings in real time, directing rapid-response teams to precise coordinates. Counter-terror units value low-signature drones that loiter above urban terrain, providing persistent overwatch without revealing friendly presence. Tactical UAVs also support hostage-rescue drills by supplying continuous line-of-sight footage inside buildings, increasing mission safety. The blend of affordability and covert reach underpins the technology’s rising profile inside homeland-security budgets. Secure waveforms and GPS-independent navigation improve the business case by reducing electromagnetic-warfare vulnerabilities.

Lower Life-Cycle Cost versus Manned Assets

Over a whole program life, drone fleets cost markedly less than comparable piloted aircraft because they consume less fuel, require no life-support equipment, and impose lighter maintenance loads. Flight-hour direct operating expense typically falls in the USD 1,000–5,000 band, far below the USD 15,000–50,000 range for manned fixed-wing counterparts. Training outlays are another lever; certifying a drone operator costs a fraction of qualifying military aviators, freeing scarce pilot training slots for other missions. The savings widen when platforms deploy to austere bases that lack extensive maintenance infrastructure. Budget-constrained ministries of defense, therefore, view tactical UAV market procurement as a cost-containment strategy that still delivers credible capability.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Congested spectrum and export-control limits | –1.8% | Global | Medium term (2-4 years) |

| High upfront procurement and MRO cost | –1.3% | Emerging and cash-limited markets | Short term (≤2 years) |

| Susceptibility to GPS spoofing/cyber-EW | –1.1% | Contested theaters worldwide | Short term (≤2 years) |

| Rare-earth-intensive sensor supply risks | –0.9% | China-centric supply chains | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Congested Spectrum and Export-Control Limits

Tactical UAV operations require dependable command, control, and data-link bandwidth. Proliferation of 5G networks, microwave communications, and electronic-warfare jammers crowds already busy frequency allocations, raising interference risks that could sever links mid-mission. Regulatory barriers further complicate exports; International Traffic in Arms Regulations classify many advanced UAV technologies as defense articles, obliging vendors to secure individual licenses and to engineer different variants for overseas buyers.[2]Federal Register, “Prohibition on Covered Foreign UAVs,” federalregister.gov The twin pressures of spectrum scarcity and regulatory oversight slow deal cycles, inflate compliance costs, and force some smaller suppliers out of specific foreign markets.

High Upfront Procurement and MRO Cost

State-of-the-art tactical UAV packages with secure datalinks, advanced sensors, and autonomous avionics often command unit prices from USD 500,000 to USD 5 million. Support contracts covering spare parts, software updates, and depot-level repair add multi-year financial commitments that can overwhelm developing-nation budgets. Rapid technology refresh rates introduce obsolescence risk within a single budget cycle, compelling ministries either to pay for incremental upgrades or to accept capability gaps. Consequently, several prospective buyers have postponed procurements or reduced fleet sizes, slowing the overall tactical UAV market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Versatile Hybrid VTOL Solutions Drive Growth

Fixed-wing drones dominated the tactical UAV market in 2025, capturing 60.74%, thanks to long-endurance profiles suitable for border patrol and theater-wide ISR missions. Operators value cruise efficiency that permits 8-12-hour sorties without aerial refueling. Yet hybrid VTOL designs register the fastest ascent at a 15.31% CAGR because they combine runway-free vertical lift with fixed-wing range performance. These aircraft can launch from improvised clearings or naval decks, then transition to efficient forward flight, making them attractive for special-operations forces and maritime task groups. Rotary-wing drones remain indispensable for precision hovering during hostage-rescue and urban-combat support roles, although their shorter reach confines adoption mainly to close-tactical engagements. Suppliers emphasize modular airframes that accept plug-and-play payloads, enabling customers to re-task assets between reconnaissance, electronic-warfare, and small-diameter-munition missions without purchasing new air vehicles.

The hybrid VTOL trend benefits from maturing battery energy density and compact geared-turbine engines that boost payload-to-weight ratios. Naval planners underscore the importance of vertical launch capability under sea states that preclude fixed-wing catapult operations. Land forces, meanwhile, exploit runway-independent drones to deliver ISR for dispersed units beyond established airfields, dovetailing with doctrinal shifts toward distributed operations. As a result, the tactical UAV market anticipates sustained share migration from legacy fixed-wing assets toward hybrid concepts through 2030.

By Weight Class: Micro and Nano Drones Expand Distributed Reconnaissance

Medium models in the 150 to 600 kg bracket represented 41.83% of the tactical UAV market size in 2025, striking a balance between payload capacity and expeditionary logistics. These vehicles carry multi-sensor turrets, synthetic-aperture radars, and encrypted relay nodes, supporting brigade-level situational awareness for up to 18 hours. Yet micro/nano aircraft under 5 kg are the most dynamic subset, advancing at a 16.08% CAGR as forces experiment with squad-level swarms that share imagery, map interior spaces, and execute decoy maneuvers against air defenses. Technological leaps in miniature gimbals and low-SWaP radios unlock ISR functions once reserved for larger drones, extending intelligence to the platoon echelon.

Light tactical categories (20 to 150 kg) fill niche requirements for helicopter-borne insertion units that need organic reconnaissance in dense terrain. At the high end, heavy tactical drones above 600 kg undertake long-endurance maritime patrol and stand-off strike; however, their size complicates deployment from forward locations and limits suitability for swarm tactics. Across all classes, battery innovation and lightweight composite structures are improving endurance without sacrificing stealth or payload. The miniaturization trend is set to redefine force-design principles, moving decision-quality data closer to the point of contact and amplifying the tactical UAV market’s penetration into every command level.

By Range: Extended-Range Drones Redefine Tactical Boundaries

The medium-range segment covering 50 to 200 km held 44.92% of the tactical UAV market share in 2025, furnishing enough standoff distance for most battlefield intelligence tasks while maintaining robust control-link integrity. However, extended-range platforms exceeding 200 km are climbing at a 14.72% CAGR as joint forces seek reconnaissance reach deep into contested territory without risking manned assets. Advances in high-gain antennas, satcom-on-the-move terminals, and autonomous route-planning allow longer excursions even under degraded-GPS conditions. Short-range drones under 50 km remain essential for base-perimeter security, training, and urban warfare where operators require immediate launch and recovery.

Fiber-optic tether concepts lengthen flight duration indefinitely while providing jam-resistant communications, a feature prized by electronic-warfare-exposed units. Submarine-deployed drones illustrate a complementary avenue of range extension, enabling ISR collection without revealing underwater vessel positions. The overall effect blurs tactical and operational UAV boundaries as commanders integrate multi-range fleets into layered surveillance constructs, enlarging total addressable demand for the tactical UAV market.

By Propulsion Type: Electric Power Gains Stealth and Logistic Advantages

Internal-combustion engines (ICE) preserved a 63.71% share in 2025 owing to proven endurance and rapid refueling. Nonetheless, electric propulsion enjoys a 15.46% CAGR driven by silent flight, low thermal signature, and simplified maintenance that requires fewer moving parts and no spark-ignition system. Hybrid solutions marry battery-powered take-off with fuel-burning cruise, offering the best stealth and range. Military planners value reduced acoustic output that limits detection by acoustic sensors, a decisive benefit during covert reconnaissance.

Solid-state battery development promises energy densities surpassing 400 Wh/kg, lengthening mission legs for fully electric airframes. Simultaneously, distributed-propulsion architectures place multiple small motors along wing spans, enhancing redundancy and enabling tighter turn radii—attributes beneficial for urban ISR. Logistic chains also prefer electric drones for easier field refueling via portable generators or renewable energy kits. These factors suggest a gradual migration toward electric or hybrid power plants, signaling another inflection point for the tactical UAV market.

By Application: Military Dominance with Accelerating Civil Uses

Defense customers commanded 79.68% of 2025 revenues, and funding pipelines imply a 13.09% CAGR through 2031 as armed forces replace or augment legacy manned reconnaissance fleets. Law-enforcement agencies increasingly acquire tactical drones for riot control, forensic mapping, and fugitive tracking, leveraging integrated spotlight and loud-hailer payloads. Disaster-response teams deploy watertight quadcopters to identify survivors in flooded zones and to relay real-time imagery to incident command. Environmental regulators employ fixed-wing electric drones to track wildlife, detect illegal fishing, and survey remote conservation areas with minimal ecological footprint.

Technologies pioneered for defense—such as metamaterial radar-absorbent skins and AI-enabled target recognition—reach commercial markets once export controls relax, or dual-use adaptations emerge. The cascading transfer of innovation broadens the user base, balances revenue streams, and cements enduring growth prospects for the tactical UAV industry.

Geography Analysis

North America retained 31.45% of the global tactical UAV market revenue in 2025, underpinned by the world’s largest defense appropriation, mature aerospace supply chains, and a supportive regulatory climate that now prioritizes domestic drone manufacturing. The region’s multi-year procurement programs provide predictable demand for airframe producers, sensor houses, and data-link vendors, while civilian agencies expand BVLOS operations for infrastructure inspection and wildfire monitoring. Canada’s investment in next-generation surveillance drones and Mexico’s southern-border surveillance needs further reinforcement of continental volume.

Asia-Pacific exhibits the fastest growth at a 13.18% CAGR, propelled by rising defense budgets, border skirmishes, and indigenous R&D in China, India, and South Korea. Local primes integrate cost-competitive airframes with region-specific sensor suites, capturing domestic contracts and challenging Western exporters. Partnerships between Japanese electronics firms and defense ministries accelerate AI-based navigation solutions, and Australia’s vast maritime approaches sustain demand for long-endurance oceanic patrol drones. The regional tactical UAV market thus gains momentum from both security imperatives and industrial-policy incentives.

Europe maintains steady expansion as collaborative programs under the European Defense Fund promote technology sovereignty. Member states procure micro-UAVs for urban reconnaissance and counter-UAS specialties, mitigating reliance on external suppliers. The Middle East and Africa represent emerging frontiers where territorial disputes and counter-insurgency missions spur acquisitions, often financed through energy revenue or multilateral aid. Turkish and Israeli manufacturers, benefiting from operational experience in regional conflicts, supply cost-effective systems tailored for desert environments. Collectively, these geographic dynamics diversify sales channels and underpin the long-term resilience of the global tactical UAV market.

Competitive Landscape

The tactical UAV market remains moderately fragmented, yet consolidation is progressing as incumbents integrate airframes, sensors, and autonomy software into turnkey packages. Top aerospace primes leverage established government relationships to secure flagship programs, while specialized drone makers differentiate through rapid prototype cycles and niche-mission focus. Vertical integration strategies aim to lock in rare-earth supply, proprietary datalinks, and machine-learning stacks, thereby raising barriers to entry.

Technology leadership, rather than pure scale, increasingly dictates contract awards. Vendors invest heavily in AI-driven swarm management, GNSS-independent navigation, and cyber-hardened architectures to comply with tightening defense-acquisition mandates. Collaborative frameworks between software start-ups and legacy OEMs quicken time-to-field for novel payloads, blurring traditional industry boundaries. Meanwhile, export restrictions on certain foreign manufacturers open opportunities for domestic alternatives, prompting new entrants to target allied-nation security forces seeking ITAR-unencumbered solutions. These cross-currents underpin an environment where innovation velocity, regulatory agility, and supply-chain resilience collectively shape market share trajectories.

Tactical UAV Industry Leaders

The Boeing Company

Lockheed Martin Corporation

Northrop Grumman Corporation

Israel Aerospace Industries Ltd.

Textron Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The US Department of Defense invoked an accelerated procurement pathway that channels additional funds toward domestically produced tactical UAVs.

- December 2024: The Federal Acquisition Regulation formally barred federal purchases of UAV systems from specified foreign entities, accelerating supplier diversification.

- September 2023: ISS Aerospace (UK) unveiled the tube-launched WASP M4-TL tactical UAS. The WASP is man-portable and can be deployed in less than 3 seconds. It is equipped with a high-performance gimbal-mounted EO/IR camera with a range finder and a modular payload system of up to 1.5kg.

- June 2023: India’s DRDO (Defense Research and Development Organization) conducted trial runs for the indigenously developed TAPAS 201 Medium Altitude Long Endurance (MALE) UAV. TAPAS 201 can carry out missions both day and night and can carry combinations of payloads like Medium—and Long-Range Electro-Optic, Synthetic Aperture Radar, Electronic Intelligence, Communication Intelligence, and Situational Awareness Payloads.

Global Tactical UAV Market Report Scope

Tactical UAVs find their application in reconnaissance, surveillance, and target acquisition (RSTA). They can also be used in applications like target designation, strike, chemical-bio detection, mine countermeasures, theater air missile defense, electronic warfare, and information warfare.

The tactical UAV market is segmented by application and geography. By application, the market has been segmented into military, law enforcement, and other applications. The other applications include search and rescue and firefighting. The report covers the market sizes and forecasts for the tactical UAV market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

By Platform

| Fixed-wing |

| Rotary-wing |

| Hybrid VTOL |

By Weight Class

| Micro/Nano (Less than 5 kg) |

| Mini (5 to 20 kg) |

| Light Tactical (20 to 150 kg) |

| Medium Tactical (150 to 600 kg) |

| Heavy Tactical (Greater than 600 kg) |

By Range

| Short-Range (Less than 50 km) |

| Medium-Range (50 to 200 km) |

| Extended-Range (Greater than 200 km) |

By Propulsion Type

| Electric |

| Hybrid |

| Conventional (ICE) |

By Application

| Military |

| Law Enforcement |

| Disaster and Emergency Response |

| Environmental Monitoring |

| Other Applications |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Platform | Fixed-wing | ||

| Rotary-wing | |||

| Hybrid VTOL | |||

| By Weight Class | Micro/Nano (Less than 5 kg) | ||

| Mini (5 to 20 kg) | |||

| Light Tactical (20 to 150 kg) | |||

| Medium Tactical (150 to 600 kg) | |||

| Heavy Tactical (Greater than 600 kg) | |||

| By Range | Short-Range (Less than 50 km) | ||

| Medium-Range (50 to 200 km) | |||

| Extended-Range (Greater than 200 km) | |||

| By Propulsion Type | Electric | ||

| Hybrid | |||

| Conventional (ICE) | |||

| By Application | Military | ||

| Law Enforcement | |||

| Disaster and Emergency Response | |||

| Environmental Monitoring | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the expected growth rate for the tactical UAV market to 2031?

The tactical UAV market is forecasted to post a 12.74% CAGR between 2026 and 2031, lifting value from USD 6.98 billion to USD 12.72 billion.

Which platform category is expanding the fastest?

Hybrid VTOL drones lead growth with a projected 15.31% CAGR because they combine runway-free launch with efficient cruise performance.

Why are micro and nano UAVs gaining prominence?

Technological miniaturization supports distributed swarm tactics, enabling under-5 kg drones to provide squad-level reconnaissance while advancing at a 16.08% CAGR.

How do electric propulsion systems benefit tactical UAV operations?

Electric drives cut acoustic and thermal signatures, simplify maintenance, and align with logistics-light deployments, driving a 15.46% CAGR for electric models.

What regional market is showing the highest growth?

Asia-Pacific registers the fastest expansion at a 13.18% CAGR owing to heightened security tensions and ambitious indigenous UAV programs.

How fragmented is the current supplier landscape?

The top five vendors control roughly half of global revenues, giving the market a moderate concentration score of 5 and leaving space for innovative newcomers to scale.

Page last updated on: