Mobile VOIP Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

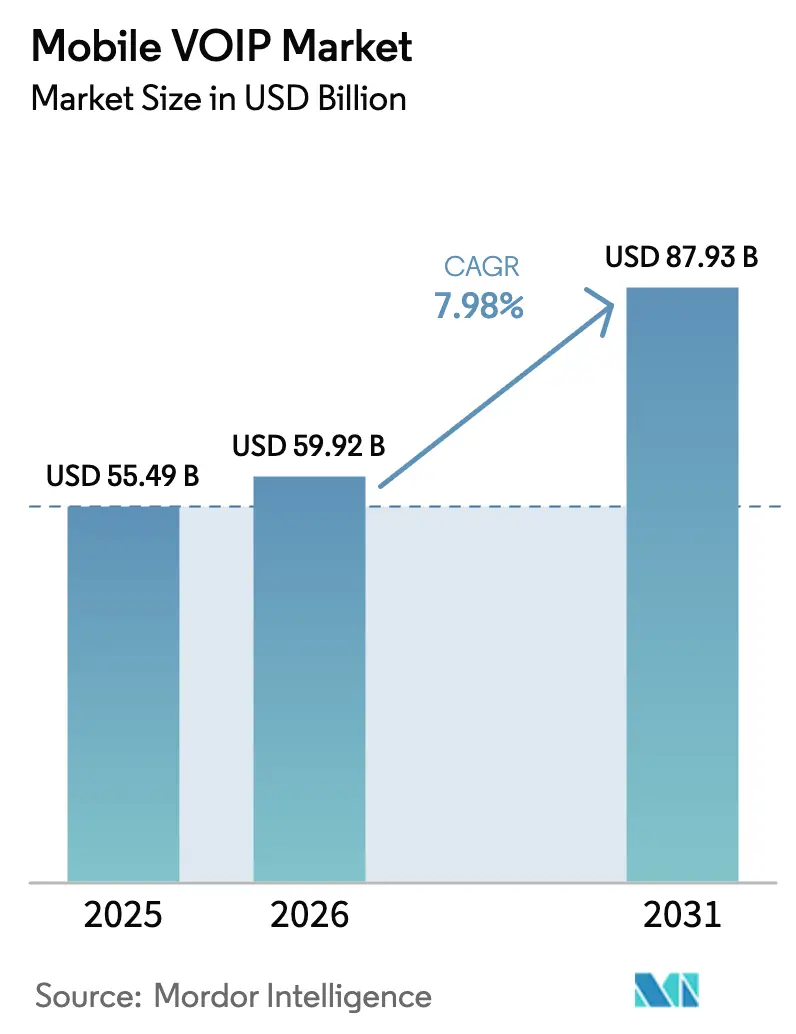

| Market Size (2026) | USD 59.92 Billion |

| Market Size (2031) | USD 87.93 Billion |

| Growth Rate (2026 - 2031) | 7.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile VOIP Market Analysis by Mordor Intelligence

The Mobile VOIP market size is expected to grow from USD 55.49 billion in 2025 to USD 59.92 billion in 2026 and is forecast to reach USD 87.93 billion by 2031 at 7.98% CAGR over 2026-2031.

Demand accelerates as enterprises retire legacy PSTN lines in favor of cloud-native voice services that embed directly into digital workflows. Mature 5G rollouts, wider AI integration, and persistent cost-saving imperatives that spread during the remote-work surge are reinforcing adoption momentum. Platform vendors now bundle voice, video, and messaging within broader productivity suites, creating switching costs that extend well beyond basic telephony. Competitive intensity is rising, yet a clear shift toward ecosystem-centric strategies is cementing the dominance of suppliers able to blend high-quality voice with analytics, security, and workflow automation.

Key Report Takeaways

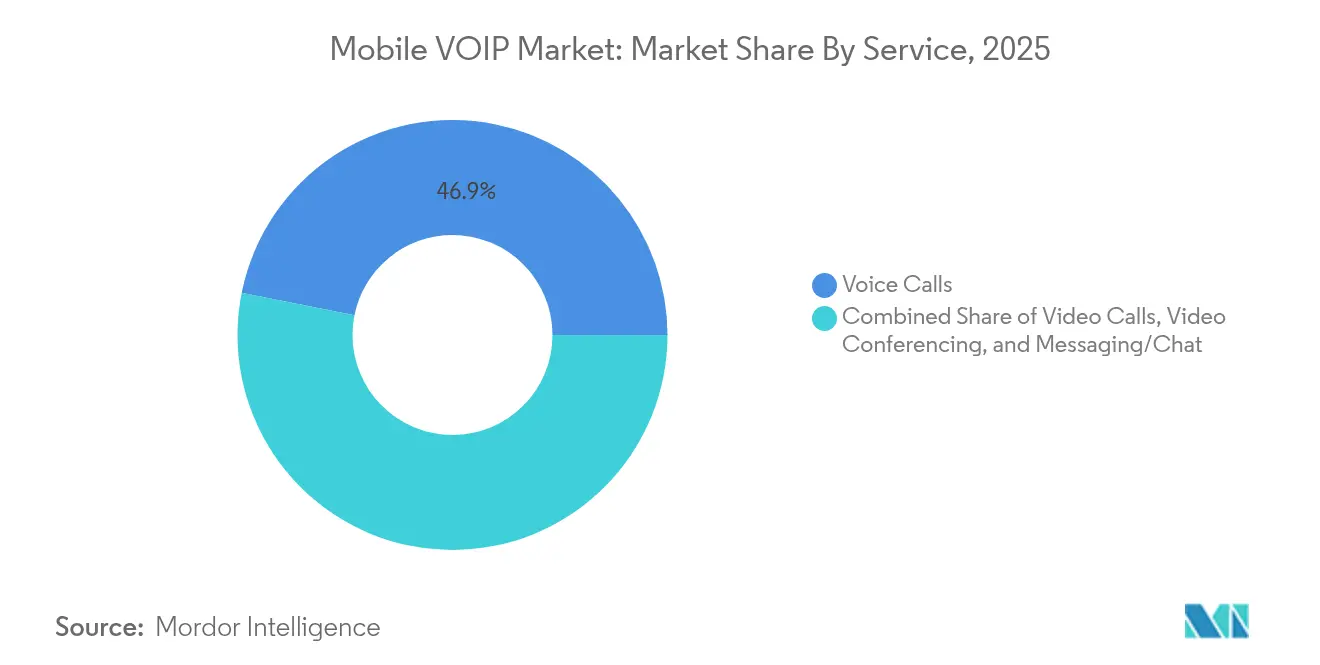

- By service, voice calls led with 46.85% revenue share in 2025, while video conferencing is poised to expand at a 24.1% CAGR to 2031.

- By platform, Android captured 71.70% of the Mobile VoIP market share in 2025, whereas iOS adoption is forecast to grow at a 16.88% CAGR, thanks to tight security integration.

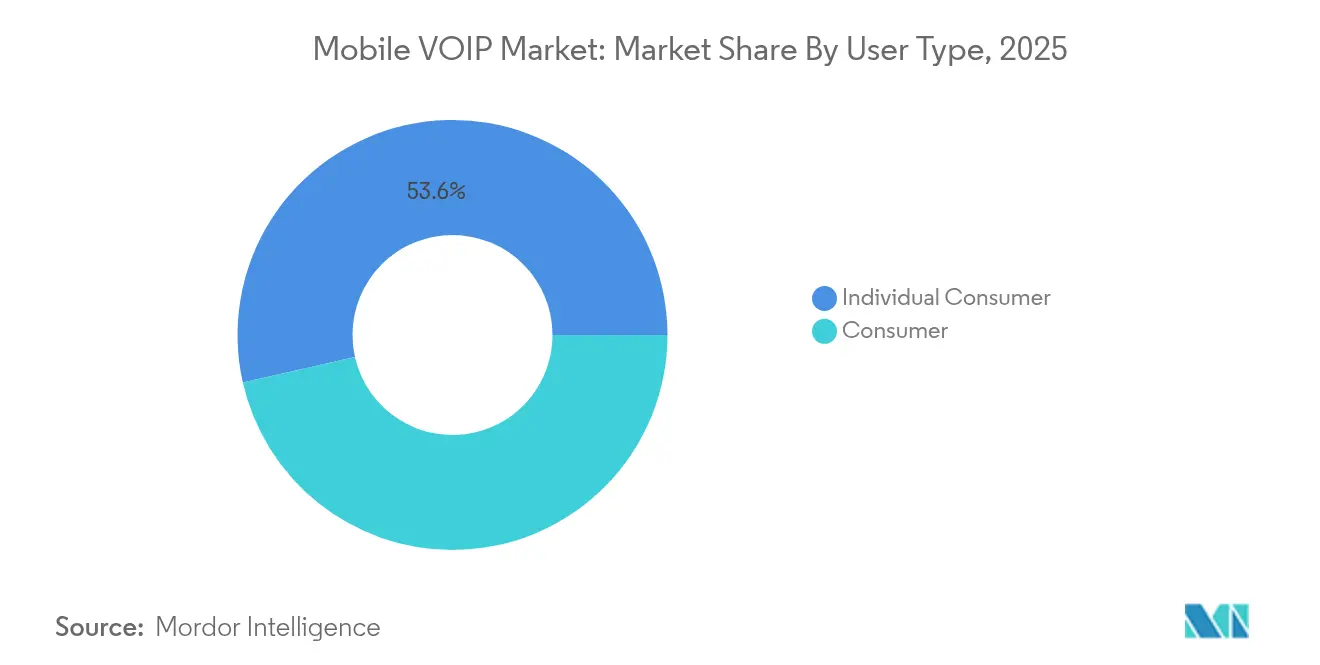

- By user type, individual consumers accounted for 53.55% of the Mobile VoIP market size in 2025, yet enterprise users represent the fastest-growing cohort at 14.7% CAGR.

- By industry vertical, IT and Telecom dominated with a 34.05% share in 2025, while healthcare is projected to advance at a 12.66% CAGR on the back of telemedicine rollouts.

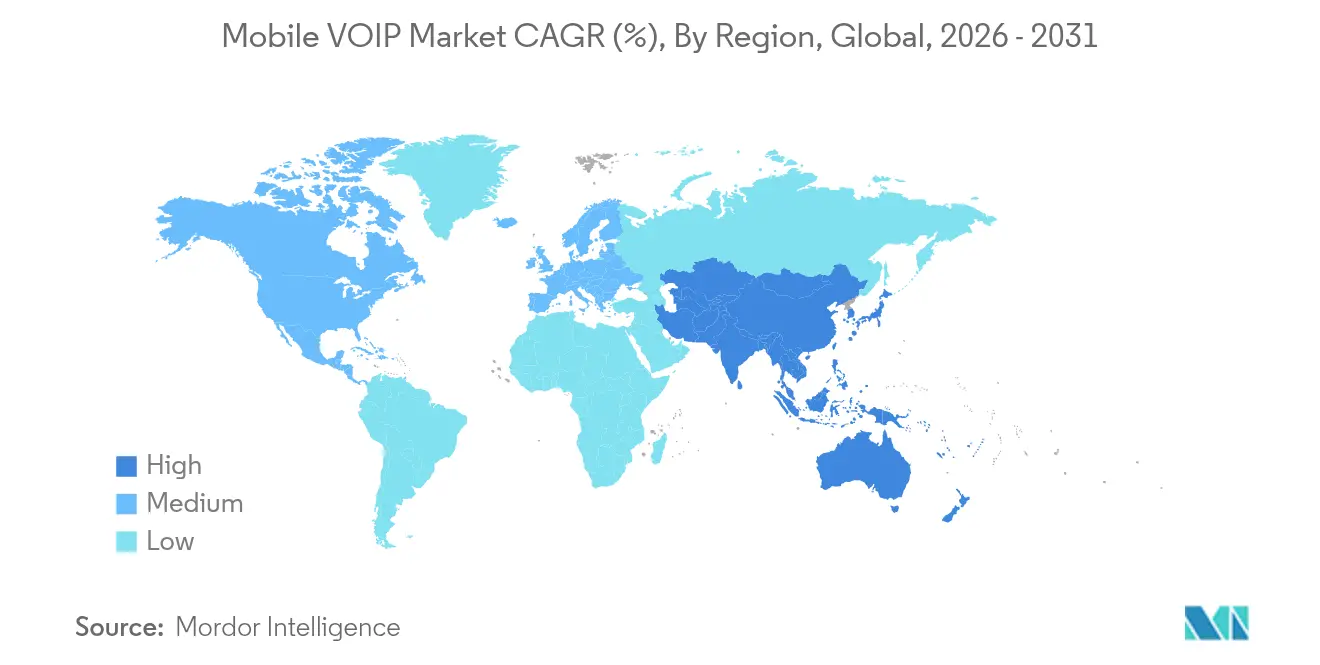

- By geography, North America held a 37.85% share in 2025; Asia Pacific records the highest forecast CAGR at 20.62% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile VOIP Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-savings versus PSTN & SMS | 2.10% | Global, strongest in emerging markets | Short term (≤ 2 years) |

| Remote & hybrid-work adoption | 2% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Global 5G rollouts enable HD voice/video | 1.50% | APAC core; spill-over to North America & Europe | Medium term (2-4 years) |

| Private 5G / CBRS integration for Industry 4.0 | 0.90% | North America & Europe manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-savings versus PSTN and SMS

Organizations cutting over to mobile VoIP services typically report voice cost reductions of 40–60% compared with circuit-switched telephony. International calling savings are even starker as per-minute fees disappear, making VoIP attractive for globally distributed teams. Healthcare facilities such as JFK Medical Center realized operational savings while improving cross-department coordination after deploying VoIP recording solutions. Growth also stems from SMS displacement; WhatsApp Business Platform posted 55% revenue growth in 2024 as firms switched customer outreach to richer IP-based messaging. Manufacturers and logistics providers see the strongest near-term upside because they can scale call volumes without proportional network-hardware spending. Eliminating PBX maintenance contracts and leveraging existing broadband makes the economic case increasingly compelling.

Remote and hybrid-work adoption

Persistent hybrid-work policies are normalizing voice, video, and messaging inside unified apps. Enterprises that moved 5,000 PSTN users onto Microsoft Teams reported 40% productivity gains and annual savings of USD 360,000. Healthcare platforms such as Doximity reduce patient wait times through intelligent call management designed for clinicians on the move. A mobile-first posture now dominates procurement checklists as staff expect professional-grade communications on any device. Beyond basic calls, enterprises value voicemail-to-email delivery, dynamic call routing, and delegation features without extra hardware outlays. Consequently, unified cloud voice is maturing from a cost tool into an engagement and workflow backbone.

Global 5G rollouts enable HD voice/video

Widespread 5G coverage is reshaping user expectations around latency and reliability. Network slicing permits prioritized channels for voice and video, driving sub-10 ms latency, five to ten times lower than typical 4G conditions. Vodafone UK and Nokia recorded 1.05 ms latency on L4S trials, proving that immersive video collaboration is feasible on mobile links[4]Vodafone UK, “L4S Technology Trial Results,” ispreview.co.uk. Private 5G in factories and hospitals further unlocks crisp voice for safety-critical workflows, keeping packets on site to avoid public-network congestion. Operators now upsell premium SLAs that guarantee jitter-free voice, while device makers embed voice-enhancement chips that thrive on the lower-latency fabric.

Private 5G/CBRS integration for Industry 4.0

Manufacturers installing CBRS or 5G LANs overlay VoIP handsets and wearables onto the same spectrum that powers robots and sensors. The arrangement consolidates network spend, simplifies mobility policies, and supports real-time analytics at the edge. Voice reliability becomes an operational-safety metric, not merely an IT function. Early adopters in the automotive and aerospace sectors highlight incident-response gains because supervisors remain reachable even during Wi-Fi outages. Over the long term, integrated spectrum licenses and falling radio costs will bring dedicated industrial voice deeper into mid-market plants, reinforcing the Mobile VoIP market growth path.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| QoS & bandwidth limitations in last-mile links | -1.40% | Global, particularly rural and developing regions | Short term (≤ 2 years) |

| VoIP-blocking & licensing barriers | -1.10% | APAC emerging markets, selective global restrictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

QoS and bandwidth limitations in last-mile links

Many rural backhaul routes still suffer from packet loss and congestion that degrade call experience. The European Commission estimates that EUR 200 billion in extra investment is needed to deliver universal gigabit connectivity by 2030[2]European Commission, “Digital Infrastructure White Paper,” ec.europa.eu. Operators deploy DSCP tagging and traffic shaping, yet scarce fiber loops and reliance on microwave links cause jitter spikes during peak periods. Rising video-call traffic intensifies these constraints because a single HD stream occupies several times the bandwidth of a voice session. In markets where LTE dominates but 5G remains patchy, enterprises keep fallback PSTN circuits, lowering the Mobile VoIP market addressable base in the short term.

VoIP-blocking and licensing barriers

Regulatory headwinds persist. India now blocks inbound international calls that spoof domestic numbers, impacting legitimate VoIP channels alongside fraudsters. California’s updated licensing statute forces VoIP providers to secure public-utility certificates, adding legal costs for new entrants. Vietnam’s Telecommunications Law imposes wholesale obligations and retains foreign-ownership caps that complicate expansion strategies. These hurdles most affect mid-tier suppliers that lack dedicated compliance teams, driving consolidation and slightly tempering overall Mobile VoIP market growth.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Video Conferencing Drives Growth

Voice calls captured 46.85% of the Mobile VoIP market share in 2025 because of universal handset compatibility and low bandwidth needs. Yet video conferencing is advancing at a 24.1% CAGR through 2031 as firms view visual collaboration as essential to hybrid operations. The segment benefits from 5G-enabled HD streams and camera enhancements that no longer drain batteries.

Video traffic now embeds in customer-facing channels; Zoom secured an enterprise contact centre win for more than 20,000 seats that integrates live video into support flows. Messaging is also evolving into a service hub as WhatsApp Business adds voice calling, proving that asynchronous and real-time modes can coexist fluidly. Healthcare uses this full quartet of voice, video, chat, and recording to knit appointment scheduling, diagnostics, and follow-ups into a single mobile experience.

By Platform: iOS Monetization Accelerates

Android dominates the Mobile VoIP market with 71.70% unit share in 2025, thanks to its extensive device portfolio. However, iOS revenues grow faster at 16.88% CAGR because enterprises prioritize the platform’s built-in security modules, MDM controls, and tight native app integration. Apple patents covering peer-to-peer voice using on-device intelligence hint at exclusive features that could further tilt premium buyers toward iOS.

Other operating systems, notably KaiOS and HarmonyOS, tackle cost-sensitive segments where basic VoIP matters more than advanced collaboration. Even so, Samsung’s augmented-reality voice patents suggest competition may arrive from yet-to-launch spatial-computing devices, widening platform choice over the coming decade.

By User Type: Enterprise Transformation Accelerates

Individual consumers represented 53.55% of the Mobile VoIP market size in 2025, but enterprise seats are expanding at a 14.7% CAGR as firms embed voice inside broader workflow engines. Microsoft’s USD 42.4 billion cloud tally underscores how bundled voice drives wider platform spending.

Enterprises are importing customer-relationship data into call flows, routing VIP customers to skilled agents, and pairing real-time sentiment analysis with knowledge-base prompts. Hospitals use intelligent call managers to shorten triage queues, while retailers surface order history during outbound calls to improve conversion. Consumers still flock to social-media-linked voice, yet enterprise adoption delivers higher ARPU and steadier contracts, anchoring long-run revenue visibility.

By Industry Vertical: Healthcare Innovation Leads

IT & Telecom held 34.05% of the Mobile VoIP market size in 2025 because carriers and MSPs naturally integrate IP voice early. Healthcare, though smaller, is growing at 12.66% CAGR as telemedicine shifts from pilot to mainstream. Hospitals such as Mayotte Hospital Centre replaced DECT with voice-over-WLAN to keep clinicians reachable across campus.

Banking’s priority is fraud-proof voice authentication, prompting AI-augmented call monitoring that flags spoofed speech patterns. Education favors remote-lecture streaming, while retail links click-to-call widgets to e-commerce carts. Vertical specialization is therefore the new competitive front, encouraging vendors to tailor compliance templates, analytics dashboards, and CRM connectors to sector-specific jargon and workflows.

Geography Analysis

North America accounted for 37.85% of the Mobile VoIP market in 2025, buoyed by widespread 5G rollout, enterprise cloud budgets, and clear regulatory pathways that legitimize IP telephony across sensitive sectors such as healthcare and finance. Customers there expect voice, video, and messaging within one pane of glass, forcing providers to deliver seamless integration with identity, productivity, and security stacks. Competitive rivalry centers on ecosystem depth rather than call minutes, pushing players toward AI-rich analytics and developer APIs.

Asia Pacific records the fastest growth at 20.62% CAGR through 2031, driven by smartphone penetration above 63% and USD 880 billion in mobile-network investment pipelines. India remains a paradox: it ranks as the second-largest telecom market by revenue, yet it intensifies scrutiny of inbound VoIP traffic to limit spam and fraud. Vietnam’s wholesale access rules may lower entry barriers for foreign partners, though ownership caps persist. Meanwhile, manufacturing hotspots in China, Japan, and South Korea install private 5G to support Industry 4.0 voice services, reinforcing regional momentum.

Europe balances stringent data-privacy mandates with aggressive infrastructure targets. Regulation 2024/1309 requires fiber-ready ducting in new construction, aligning building codes with gigabit-capable networks. Voice termination caps at EUR 0.2 per minute, narrow carrier margins, nudging enterprises to embrace VoIP for international calling. The European Commission’s 2030 gigabit agenda unlocks public-private funds for rural rollouts, gradually easing last-mile bottlenecks that have constrained quality in less-dense regions. Elsewhere, the Middle East & Africa see expanding data-center footprints and lower handset prices, pointing to accelerating, though uneven, adoption curves.

Competitive Landscape

The Mobile VoIP market remains moderately fragmented. Large platform owners build sticky ecosystems where voice is one module among many. Meta’s 55% WhatsApp Business Platform revenue surge in 2024 proves that a chat foundation can effortlessly upsell calling. Microsoft’s USD 42.4 billion cloud haul signals that voice, when packaged with Teams, SharePoint, and Azure AI, anchors multi-year enterprise deals.

Product roadmaps across leaders converge on AI. Apple patents disclose on-device inference that gates microphone streams based on user attention, an approach that can trim bandwidth without human intervention[3]Apple Inc., “Machine-Learning Optimized Voice Transmission Patent,” patents.google.com. Google boosts transcription accuracy via multimodal cues, marrying camera feeds to speech decoding for noisier environments. Start-ups exploit niches: some focus on end-to-end encrypted voice over blockchain, others on edge-accelerated noise suppression for factory floors. Consolidation is active IPFone’s TelNet Worldwide buy adds 8,000 corporate accounts, and Ericsson’s Vonage acquisition pulls carrier-grade APIs into a 5G-core portfolio.

White-space remains in vertical-specific compliance, especially in healthcare and banking. Vendors that preload HIPAA or PCI templates gain speed-to-contract advantages. The next battleground is quality-of-experience SLAs; enterprises increasingly penalize jitters above 30 ms, rewarding providers that can wield private network slices or intelligent last-mile routes. As AI agents answer routine queries, voice minute volumes may flatten, but higher-value analytics fees keep revenue climbing.

Mobile VOIP Industry Leaders

Apple Inc.

Google LLC

Microsoft Corporation

RingCentral Inc.

Nextiva Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Microsoft reported record quarterly cloud revenue of USD 42.4 billion, citing a strong uptake of AI-enhanced Teams voice services.

- March 2025: IPFone agreed to acquire TelNet Worldwide, adding nearly 100,000 subscribers and 8,000 corporate accounts.

- December 2024: Zadarma acquired VoIPVoIP, bringing advanced cloud PBX, speech recognition, and CRM links to North American customers.

- November 2024: Sangoma Technologies purchased VoIP Innovations to expand its service catalog and market reach.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the mobile VoIP market comprises all voice, video, and messaging services that are delivered over packet-switched data networks to handheld devices such as smartphones, tablets, and feature phones. The study tracks paid and freemium traffic carried through stand-alone apps as well as operator-branded softphone clients, measured at end-user spend plus in-app revenues.

Scope Exclusion: fixed desktop VoIP endpoints and traditional circuit-switched voice plans are excluded from our sizing.

Segmentation Overview

- By Service

- Voice Calls

- Video Calls

- Video Conferencing

- Messaging/Chat

- By Platform

- Android OS

- iOS

- Others (KaiOS, HarmonyOS)

- By User Type

- Enterprise

- Individual Consumer

- By Industry Vertical

- IT and Telecom

- BFSI

- Healthcare

- Education

- Retail and eCommerce

- Hospitality and Travel

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Africa

- South Africa

- Nigeria

- Kenya

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We conduct structured interviews with mobile operators, over-the-top app publishers, and enterprise communication integrators across North America, Europe, Asia-Pacific, and the Gulf. These conversations clarify active user ratios, regional ARPU shifts, and expected latency improvements, letting us challenge or confirm desk-derived assumptions before numbers are locked.

Desk Research

Our analysts first gather supply and demand indicators from reputable, open-access bodies such as the International Telecommunication Union, GSMA Intelligence, the World Bank's mobile broadband dataset, and national telecom regulators, which reveal subscriber bases, 4G/5G coverage, and average data prices. Trade associations like the Internet Society, peer-reviewed papers on codec efficiency, and listed carrier 10-Ks add traffic volumes and price elasticity signals. Select paid tools, Dow Jones Factiva for deal pipelines and D&B Hoovers for operator financial splits, round out trend direction. This list is illustrative; numerous other public and proprietary sources support validation throughout the project.

Market-Sizing & Forecasting

Our model begins with a top-down reconstruction of global mobile data traffic, which is then parsed by VoIP usage shares derived from ITU time-use surveys, median minutes per active, and price differentials versus circuit voice. Results are corroborated with selective bottom-up checks from sampled paid subscriber counts and prevailing in-app average selling prices to fine-tune totals. Key variables include smartphone penetration, 4G/5G population coverage, average mobile data cost per GB, enterprise BYOD adoption, international call price spread, and monthly active user churn. Five-year projections apply multivariate regression blended with scenario analysis so volume, pricing, and tech-upgrade lags move in step with historical elasticity patterns validated by experts.

Data Validation & Update Cycle

Before sign-off, outputs run through variance checks against independent traffic benchmarks; any anomaly above preset thresholds triggers re-contact of sources. A senior reviewer signs off, and the dashboard refreshes annually, with interim updates whenever spectrum auctions, regulatory fee changes, or large-scale app bans materially shift the outlook.

Why Mordor's Mobile VOIP Baseline Remains the Reliable Choice

Published estimates can diverge because firms adopt different service baskets, base years, and currency conversions, and because some refresh less often than the fast-moving telecom landscape demands.

Key gap drivers include whether messaging-only apps are counted, if enterprise-only spend is isolated, the treatment of ad-funded minutes, and whether shadow conversion from local currencies to USD uses rolling or fixed rates. Mordor's model aligns variable selection with measurable telecom statistics and refresh cadence, producing a balanced midpoint between bullish and conservative takes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 55.49 B (2025) | Mordor Intelligence | - |

| USD 50.78 B (2024) | Global Consultancy A | Excludes ad-supported calling, older base year |

| USD 38.00 B (2025) | Trade Journal B | Counts consumer minutes only, omits enterprise traffic |

| USD 46.90 B (2024) | Industry Association C | Bundles fixed-line VoIP, different FX base |

The comparison shows that once scope, traffic source, and currency choices are normalized, Mordor's disciplined blend of transparent variables and frequent updates offers decision-makers a figure they can trace and reproduce with confidence.

Key Questions Answered in the Report

What is the current Mobile VoIP market size?

The Mobile VoIP market stands at USD 59.92 billion in 2026 and is projected to reach USD 87.93 billion by 2031.

Which service segment is growing fastest?

Video conferencing is the fastest-growing service, expanding at a 24.1% CAGR through 2031.

Why is Asia Pacific the fastest-growing region?

The region combines smartphone penetration above 63% with USD 880 billion in 5G network investment, driving a 20.62% CAGR.

How much cost can VoIP save compared with PSTN?

Enterprises commonly report 40–60% voice cost reductions after migrating from traditional PSTN lines.

What are the main restraints to Mobile VoIP growth?

Quality-of-service issues in rural last-mile links and regulatory VoIP-blocking or licensing rules in some emerging markets slow adoption.

Which vertical is forecast to expand the most?

Healthcare leads to future growth with a 12.66% CAGR as telemedicine normalizes.

Page last updated on: