Voice Picking Solution Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 6.45 Billion |

| Market Size (2030) | USD 12.44 Billion |

| Growth Rate (2025 - 2030) | 14.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

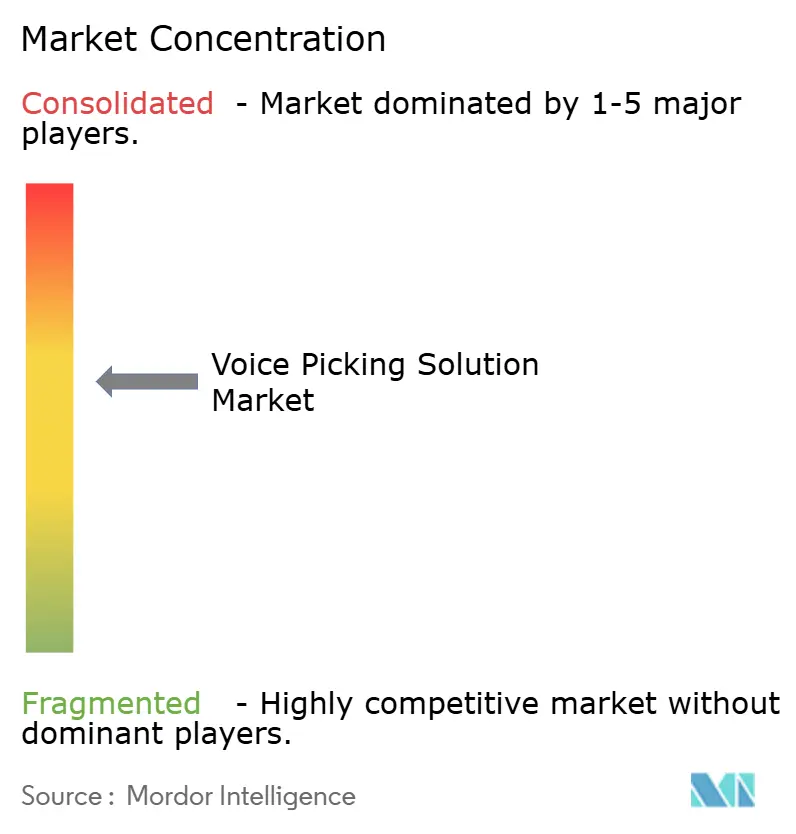

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Voice Picking Solution Market Analysis by Mordor Intelligence

The voice picking solution market size stands at USD 6.45 billion in 2025 and is forecast to reach USD 12.44 billion by 2030, delivering a 14.04% CAGR over 2025-2030. Robust e-commerce order growth, persistent warehouse labor shortages, and sharper speech-recognition accuracy combine to push voice systems from peripheral add-ons to core fulfilment infrastructure. Software platforms dominate current adoption because they orchestrate not only voice prompts but also real-time analytics and mobile-robot workflows. Accelerating cloud migration, particularly among small and mid-sized facilities, underpins subscription pricing that lowers entry barriers and shortens deployment cycles. Meanwhile, multilingual recognition breakthroughs are expanding the addressable workforce and opening fresh opportunities across Asia Pacific and Latin America.

Key Report Takeaways

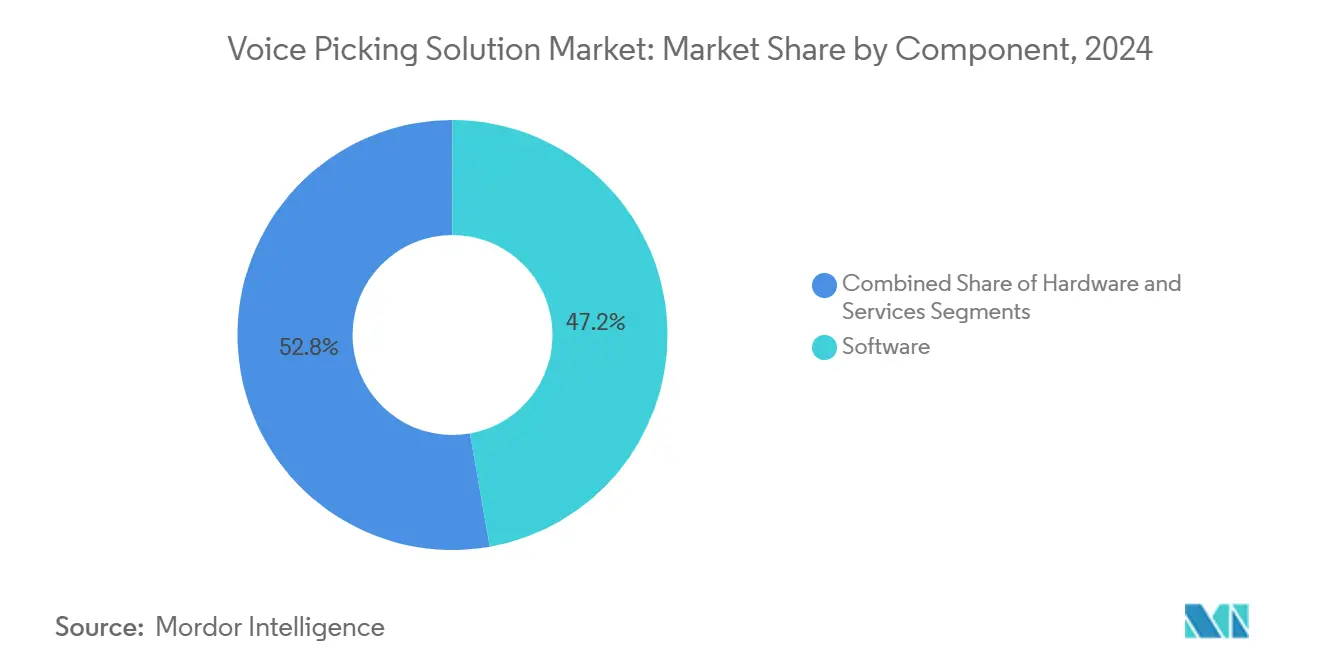

- By component, software captured 47.22% of the voice picking solution market share in 2024, while services are on track to compound at 15.22% CAGR through 2030.

- By deployment mode, on-premises led with 64.44% of the voice picking solution market size in 2024, yet cloud implementations are pacing a 16.42% CAGR to 2030.

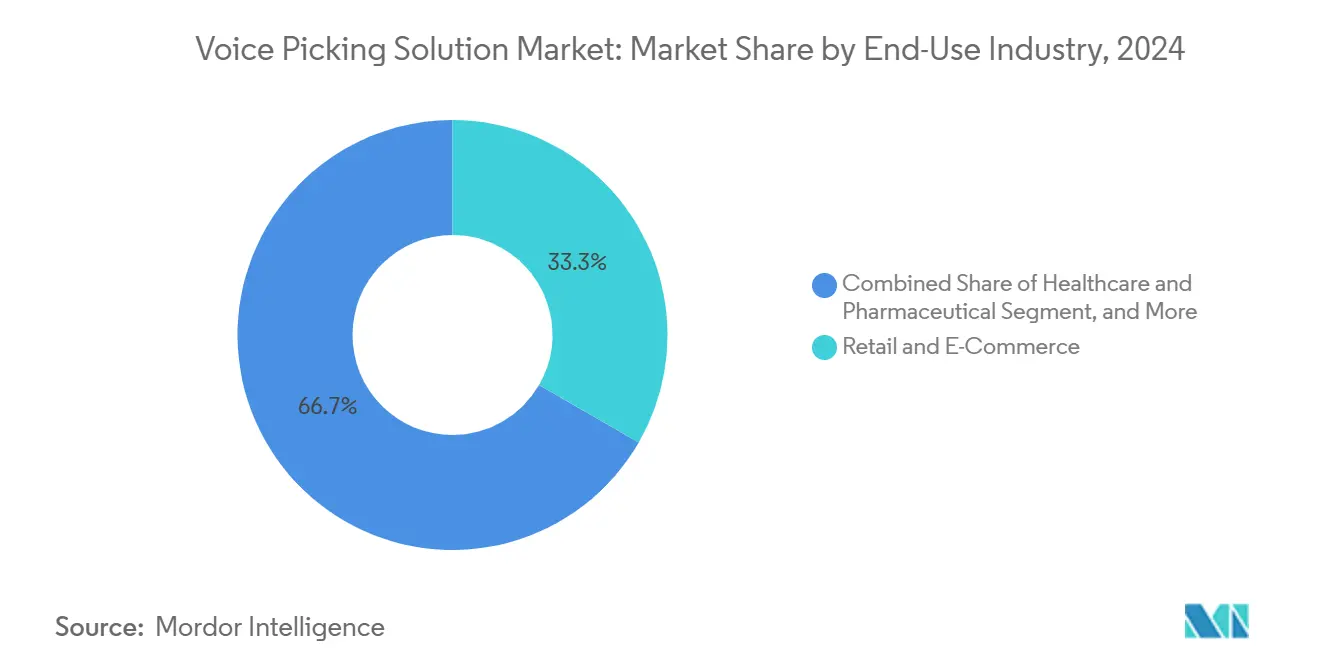

- By end-use industry, retail and e-commerce held 33.33% revenue share in 2024, whereas healthcare and pharmaceutical applications show the fastest 17.78% CAGR through 2030.

- By warehouse size, facilities larger than 250,000 ft² accounted for 57.88% of 2024 demand, but small and medium sites are advancing at a 15.56% CAGR across the forecast 2030.

- By geography, North America dominated with 36.78% revenue share in 2024, while Asia Pacific is expanding at 16.72% CAGR through 2030.

Global Voice Picking Solution Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing E-Commerce Order Volumes | +3.2% | Global, with concentration in North America and APAC | Short term (≤ 2 years) |

| Acute Warehouse Labor Shortage | +2.8% | North America and Europe, spreading to APAC | Medium term (2-4 years) |

| Integration With Autonomous Mobile Robots | +2.4% | North America and EU, early adoption in APAC | Long term (≥ 4 years) |

| Rapid ROI From Hands-Free Workflows | +2.1% | Global | Short term (≤ 2 years) |

| Multilingual Voice Recognition Advances | +1.9% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Cloud-Subscription Pricing Models | +1.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing E-Commerce Order Volumes

Single-piece and small-batch orders now represent a large share of daily picks, making hands-free navigation critical for maintaining throughput without extra labor. High-velocity sites processing 36,000-plus daily orders have raised accuracy from 99% to 99.94% after voice rollout, supporting next-day and same-day commitments that drive customer loyalty. Real-time order streaming removes fixed wave cycles, allowing facilities to absorb last-minute purchases without overtime. These productivity gains directly translate into lower fulfillment costs per line item and strengthen margins in razor-thin retail models.

Acute Warehouse Labor Shortage

With national warehouse vacancy rates below 5% in major logistics hubs, operators report double-digit annual wage inflation and record turnover.[1]Honeywell International, “Never Too Small for Voice,” honeywell.com Voice workflows cut new-hire training from weeks to hours and let multilingual teams ramp quickly, easing peak-season staffing pressure. Facilities that adopted voice have documented three-fold pick-rate improvements and up to 30% lower ergonomic injury claims, extending worker tenure and lowering rehiring cycles. These quantitative gains underpin the technology’s resilience against chronic labor shortfalls.

Rapid ROI From Hands-Free Workflows

Typical payback on a full voice deployment ranges from 6-18 months, far faster than large-scale robotics that may exceed three years. Error-reduction savings compound benefits, since a single mis-pick can cost USD 8-40 in rework or customer returns. One grocery distributor saved USD 4,960 per selector annually while trimming training time by two-thirds, freeing capital to reinvest in further automation layers. The financial profile resonates with both corporate finance teams and warehouse managers under pressure to justify every capital line item.

Multilingual Voice Recognition Advances

Modern neural engines support 40+ input and 60+ output languages, closing historical adoption gaps in linguistically diverse regions. Chinese-dialect models now reach 92.97% character accuracy, proving viable in high-noise cross-dock settings. Built-in live translation lets supervisors give instructions once and have them replayed in multiple languages, raising cross-shift flexibility. As manufacturers and 3PLs expand into Southeast Asia and Latin America, this capability becomes a decisive procurement criterion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Integration Costs | -1.8% | Global, particularly affecting SMEs | Short term (≤ 2 years) |

| Workforce Change-Management Resistance | -1.4% | North America and Europe, traditional industries | Medium term (2-4 years) |

| Accent-Related Recognition Errors | -1.2% | APAC and MEA regions with linguistic diversity | Medium term (2-4 years) |

| Data-Security AND Privacy Concerns | -0.9% | Global, heightened in regulated industries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Integration Costs

Custom interfaces between voice software and legacy warehouse management systems can inflate roll-out budgets and deter smaller operators. Subscription bundles that package hardware, software, and support into monthly fees are softening capital spikes, while no-code screen-scrape tools allow proof-of-concept pilots without touching back-end logic. Yet many SMEs still face cash-flow constraints that delay full production deployment.

Accent-Related Recognition Errors

Even with neural models, thick accents and high ambient noise can drag accuracy below operational thresholds, eroding worker trust.[2]Zetes, “Voice Picking FAQ,” zetes.com Vendors are responding with adaptive acoustic models and noise-cancelling headsets, but acceptance remains uneven, especially in regions where English is a second or third language. Continuous learning modules and accent-specific tuning are improving results, though the perception of reliability remains a hurdle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software-Led Evolution Toward Unified Platforms

The software layer held 47.22% of the voice picking solution market share in 2024, reflecting its role as the command center that links voice prompts, real-time analytics, and robot orchestration. Service revenues are climbing 15.22% CAGR through 2030 as enterprises seek managed hosting and continuous optimization. Hardware revenue grows modestly, aided by lighter headsets and multimode scanners. Integration of artificial intelligence into software frameworks compresses worker travel by up to 50% and fuels dynamic task reprioritization mid-shift. The voice picking solution market size tied to software is set to capture incremental value as warehouse execution systems absorb adjacent modules such as labor management and slotting optimization.

As voice providers morph into platform companies, competitive moats rest on API breadth, AI modeling depth, and the ability to ingest sensor data from robots and smart conveyors. Vendors that secure early software footprints can upsell analytics and subscription add-ons, locking in multi-year recurring revenue. Consequently, hardware suppliers are forging alliances with software specialists to preserve relevance and share in the expanding profit pool.

By Deployment Mode: Cloud Momentum Gains but On-Premises Still Rules

On-premises instances commanded 64.44% of the voice picking solution market size in 2024, anchored by security policies and tight coupling with established WMS databases. Cloud roll-outs, however, are compounding at 16.42% CAGR thanks to elastic scaling, auto-updates, and lower IT overhead. Pay-as-you-go pricing appeals to 3PLs that inherit client demand spikes without long budgeting cycles. Multisite enterprises adopt hybrid models, retaining sensitive data on-premises while connecting to cloud analytics for fleet-wide insights.

As cybersecurity standards mature, barriers that once favored local servers are weakening. Independent SOC2 and ISO 27001 attestations give cloud providers parity with in-house data centers. The voice picking solution market will increasingly view deployment choice as an operational, not philosophical, decision, weighed by bandwidth resilience and corporate cloud policy alignment.

By End-Use Industry: Regulatory Precision Drives Healthcare Uptake

Retail and e-commerce made up 33.33% of 2024 revenue, but healthcare and pharmaceuticals lead growth at 17.78% CAGR, propelled by FDA traceability and Good Manufacturing Practice mandates. Picking accuracy influences patient safety and asset-loss exposure, so hospitals and drug distributors prioritize technologies with audit-grade logs. Cold-chain food distributors also adopt voice because gloves and condensation impede touchscreen devices.

FDA-compliant labeling workflows and two-factor voice confirmations are becoming standard features. Vendors offering out-of-the-box validation packs can shorten go-live windows, a critical factor for time-pressed healthcare IT teams. As similar traceability rules emerge for cosmetics and nutraceuticals, voice providers prepared for regulated environments will gain first-mover advantage.

By Warehouse Size: Democratization Reaches Mid-Tier Facilities

Sites larger than 250,000 ft² represented 57.88% of deployments in 2024, but small and mid-size facilities are accelerating at 15.56% CAGR as cloud subscriptions sidestep capital hurdles. Mid-tier adopters report 20-30% productivity boosts within three months, validating ROI even without six-figure SKU counts. Modular licensing lets operators add picking zones or workflows only when volume dictates.

The voice picking solution market share captured by smaller warehouses is poised to swell as integrators roll out pre-configured starter kits that require no WMS modifications. Integrators also bundle quick-start training materials, enabling weekend cutovers that limit downtime for resource-constrained businesses.

Geography Analysis

North America’s USD-heavy fulfillment networks continue to adopt advanced voice-powered tasking to mitigate labor scarcities in metro hubs like Dallas and Atlanta. Regional operators showcase enterprise roll-outs covering 20-plus distribution centers and 5,000 headsets, setting benchmark productivity baselines that ripple through the supplier ecosystem. Shared-services 3PLs drive template standardization, accelerating cross-client deployments and boosting voice picking solution market penetration.

Asia Pacific’s rapid e-commerce growth, government-supported automation incentives, and native-language AI are tilting capital flows toward voice investment. Chinese logistics majors combine voice with AMR fleets for integrated goods-to-person models, In China, large 3PLs link voice workflows with conveyor systems to address 11.9 million annual parcel deliveries, while India’s Grade-A warehouse build-out is attracting providers offering Hindi and Tamil speech packs. [3]Invest India, “India’s Warehousing Boom,” investindia.gov.inwhile Japanese manufacturers deploy subscription bundles to offset high labor costs during demographic contraction. India’s multimodal logistics parks, each exceeding 500 acres, embed voice workflows from day one to leapfrog legacy RF scanning.

Europe benefits from stringent worker-safety directives that elevate voice as an ergonomic upgrade over handhelds. Diverse language requirements validate the business case for real-time translation, with German facilities routinely onboarding Polish and Romanian seasonal labor without extra trainer headcount. Emerging Latin American sites pilot voice in bonded warehouses near free-trade ports, banking on cross-border order growth to unlock scale-driven payback.

Competitive Landscape

The market is moderately fragmented: the top five suppliers account for roughly 35-40% combined revenue, leaving room for niche specialists. Honeywell, Zebra Technologies, Lucas Systems, Körber, and EPG compete on end-to-end workflow coverage, bundling voice, vision, and robotics under unified dashboards. Zebra’s planned Photoneo acquisition deepens 3D vision capability that complements its existing wearable computer portfolio. Körber integrates voice into its warehouse control software to orchestrate AMRs, conveyors, and put-walls in a single scheduler.

Mid-market challengers differentiate via cloud-native architectures and API openness, courting 3PLs that juggle multiple customer ERPs. Several venture-backed entrants build large language model overlays that translate standard operating procedures into dynamic voice prompts, positioning voice as a gateway to warehouse generative AI. Hardware commoditization spurs headset manufacturers to embed biometrics and noise-cancellation as table stakes rather than upsell options.

Strategic partnerships matter: robot makers align with voice vendors to deliver turnkey picking cells; WMS suppliers embed voice add-ons to blunt best-of-breed encroachment. Consolidation will likely intensify as platform economics favor scale for AI training and global support coverage.

Voice Picking Solution Industry Leaders

-

Honeywell International Inc.

-

Zebra Technologies Corporation

-

Ivanti Software Inc.

-

Lucas Systems Inc.

-

Voxware Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: EPS Japan announced aggressive market expansion targeting 1,000 LYDIA Voice licenses across Japan over three years (2025-2027), focusing on apparel logistics and manufacturing applications with multilingual workforce support through authorized reseller AINIX Inc. The initiative represents significant geographic expansion into Asia Pacific's second-largest economy, leveraging Android-compatible deployment and VoiceWear Air wearable devices for harsh environment applications.

- August 2025: Colruyt Group completed comprehensive voice picking technology modernization across seven food distribution centers supporting over 800 stores, upgrading legacy systems to future-proof hardware and software while maintaining workflows for approximately 8,000 employees with individual headsets. The project integrated new EU-mandated tobacco track and trace requirements using Bluetooth finger scanners, demonstrating regulatory compliance capabilities essential for pharmaceutical and controlled substance applications

- June 2025: EPG revealed that EPG ONE, featuring voice-picking solutions, received the title of “Overall SupplyTech Solution of the Year” from the SupplyTech Breakthrough Awards

- January 2025: Zebra Technologies closes the Photoneo acquisition to fuse 3D vision with voice-directed workflows.

Global Voice Picking Solution Market Report Scope

| Hardware |

| Software |

| Services |

| On-Premises |

| Cloud-Based |

| Retail and E-Commerce |

| Food and Beverage |

| Healthcare and Pharmaceutical |

| Logistics and Transportation |

| Automotive and Manufacturing |

| Small and Medium (<250k sq ft) |

| Large (≥250k sq ft) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Deployment Mode | On-Premises | |

| Cloud-Based | ||

| By End-Use Industry | Retail and E-Commerce | |

| Food and Beverage | ||

| Healthcare and Pharmaceutical | ||

| Logistics and Transportation | ||

| Automotive and Manufacturing | ||

| By Warehouse Size | Small and Medium (<250k sq ft) | |

| Large (≥250k sq ft) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the voice picking solution market?

The voice picking solution market size is USD 6.45 billion in 2025.

How fast is the market expected to grow?

It is projected to register a 14.04% CAGR between 2025 and 2030.

Which region is expanding most rapidly?

Asia Pacific is forecast to grow at 16.72% CAGR through 2030, making it the fastest-growing region.

Which industry vertical shows the quickest adoption pace?

Healthcare and pharmaceuticals are advancing at a 17.78% CAGR due to stringent accuracy and traceability needs.

What deployment model is gaining momentum?

Cloud-based deployments are growing at 16.42% CAGR as enterprises favor subscription pricing and elastic scaling.

How soon can companies expect payback from voice picking?

Typical return-on-investment falls within 6-18 months, driven by 15-50% productivity gains and fewer picking errors.

Page last updated on: