Europe IP Telephony And Unified Communications As-a-service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

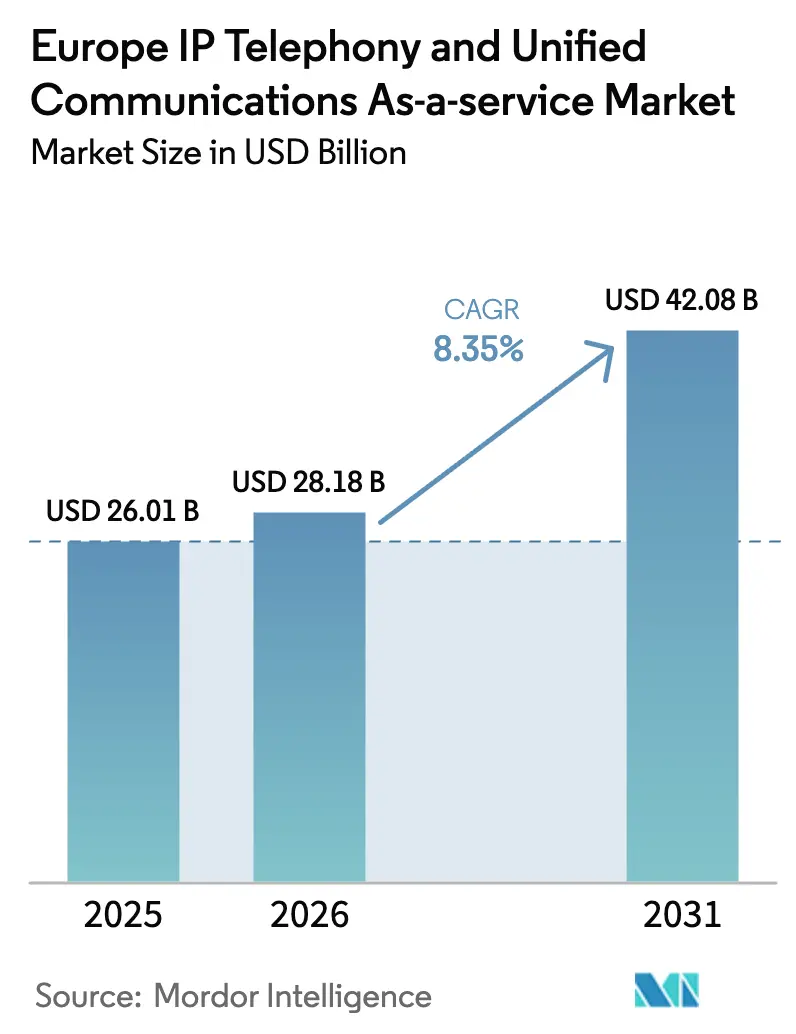

| Base Year Market Size (2025) | USD 26.01 Billion |

| Market Size (2026) | USD 28.18 Billion |

| Market Size (2031) | USD 42.08 Billion |

| Growth Rate (2026 - 2031) | 8.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe IP Telephony And Unified Communications As-a-service Market Analysis by Mordor Intelligence

The Europe IP Telephony and Unified Communications As-A-Service market size in 2026 is estimated at USD 28.18 billion, growing from 2025 value of USD 26.01 billion with 2031 projections showing USD 42.08 billion, growing at 8.35% CAGR over 2026-2031. The growth reflects accelerated digital transformation across enterprises, stronger regulatory alignment under the European Electronic Communications Code, and mandatory shifts from ISDN to all-IP networks. Rapid 5G deployments by major operators are enabling sub-10 millisecond latency for UCaaS workloads, while the EU Data Act encourages multi-vendor portability that weakens supplier lock-in. Hybrid work policies have become permanent for many organizations, driving the need for cloud-native communication suites that unify voice, video, and messaging. Public subsidies that offset subscription costs for SMEs and sector-specific integration requirements in healthcare and manufacturing further widen the addressable base for service providers. Competition remains moderate as global hyperscale vendors face region-specific specialists with deep regulatory expertise, fueling both innovation and pricing pressure.

Key Report Takeaways

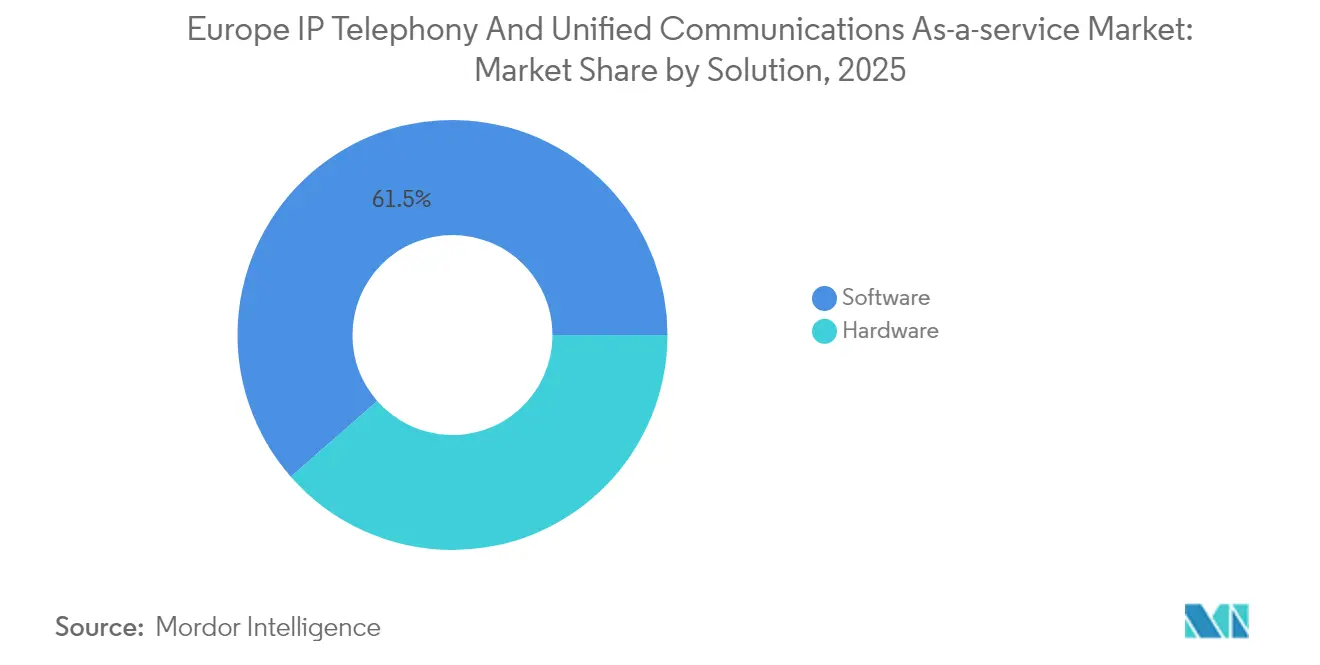

- By solution, software captured 61.45% of revenue in 2025, while hardware trailed due to the shift toward API-driven platforms.

- By type, hosted IP PBX held a 41.92% share in 2025, whereas CPaaS is projected to expand at an 8.58% CAGR through 2031.

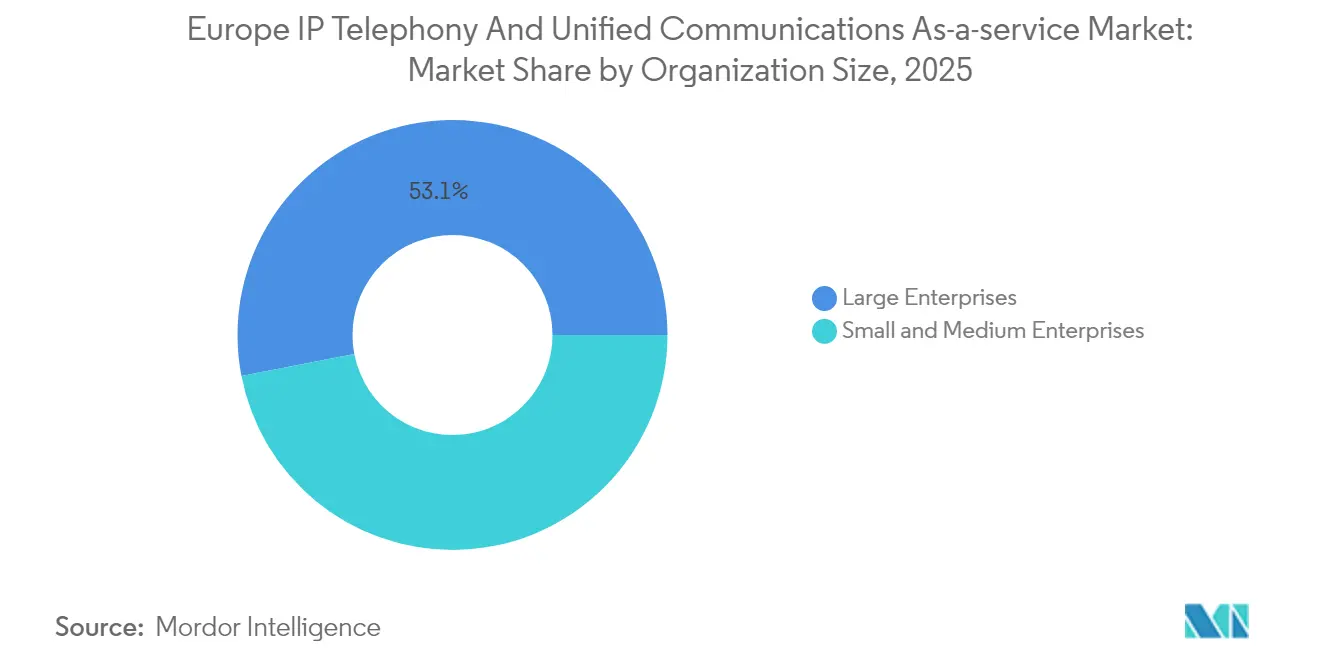

- By organization size, large enterprises contributed 53.05% of 2025 revenue, but SMEs are advancing at a 10.05% CAGR.

- By end user, the IT and telecom segment led with a 30.94% share in 2025; the healthcare segment is forecast to grow at an 8.42% CAGR to 2031.

- By geography, the United Kingdom commanded a 22.05% share in 2025, while Spain is set to record an 8.46% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe IP Telephony And Unified Communications As-a-service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 5G rollouts enabling low latency UCaaS | +1.8% | EU-wide, strongest in Germany, UK, Netherlands | Medium term (2-4 years) |

| Shift toward hybrid work policies across Europe | +2.1% | Pan-European, highest in Nordic and Benelux | Short term (≤ 2 years) |

| Rapid migration from ISDN to all-IP networks | +1.5% | Germany, UK, France, spillover to Eastern Europe | Medium term (2-4 years) |

| Growing SMB demand for OpEx friendly subscriptions | +1.2% | Southern and Eastern Europe | Long term (≥ 4 years) |

| Integration with vertical specific SaaS workflows | +0.9% | Western Europe core | Long term (≥ 4 years) |

| Edge computing adoption for real time voice | +0.9% | Major metropolitan clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G Rollouts Enabling Low-Latency UCaaS

Standalone 5G coverage now blankets most metropolitan areas in Germany and the UK, giving enterprises consistent sub-10 millisecond latency that rivals circuit-switched voice.[1]Deutsche Telekom, “5G Network Expansion 2024,” TELEKOM.COM Operators have placed voice processing functions at the network edge through Network Function Virtualization (NFV), which reduces dependence on centralized data centers and improves call quality in contact center scenarios. These architecture gains support real-time capabilities such as language translation and AI call analytics. The shift differentiates European providers from global hyperscalers in terms of latency-sensitive workloads and accelerates the migration from legacy PBX systems.

Shift Toward Hybrid Work Policies Across Europe

Post-pandemic labor regulations in France and the Netherlands now codify flexible work rights, cementing long-term demand for mobile-first collaboration suites.[2]European Commission, “Flexible Work Directive,” EC.EUROPA.EU Nordic employers report high employee satisfaction when cloud tools replace traditional hardware PBX systems, leading to broader rollouts of presence, messaging, and video functions. A policy emphasis on work-life balance drives the uptake of AI-powered meeting summaries that limit after-hours interactions. Public-sector agencies follow the European Commission’s own digital workplace guidelines, ensuring steady demand from government accounts.

Rapid Migration From ISDN to All-IP Networks

Germany completed its nationwide ISDN shutdown in December 2024, forcing businesses to adopt IP voice or risk service loss.[3]BT Group, “All-IP Migration,” BT.COM All-IP mandates remove technical excuses for retaining on-premises PBX and expand bandwidth for 4K video conferencing. Regulatory obligations for IP-based emergency calling under the Electronic Communications Code further encourage organizations to adopt cloud suites with built-in E911 compliance. SMEs benefit most because they avoid capital outlays associated with ISDN hardware maintenance.

Growing SMB Demand For OpEx-Friendly Subscription Models

SMEs value predictable monthly costs and reduced IT overhead, a preference reflected in a 73% subscription bias captured by the European Investment Bank survey. Spain’s Kit Digital scheme reimburses up to EUR 12,000 (USD 13,560) in UCaaS expenses, lifting penetration among previously price-sensitive firms. Similar incentive programs in Poland and the Czech Republic extend the model to Eastern Europe. Subscription models simplify upgrades and enable SMEs to scale licenses in response to seasonal workload changes, thereby strengthening vendor lock-in while also stabilizing cash flows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented cross-border data sovereignty regulations | -1.4% | EU-wide, strong effect on multinational deployments | Medium term (2-4 years) |

| Heightened cyber attack surface in cloud telephony | -0.8% | Northern Europe and financial clusters | Short term (≤ 2 years) |

| Vendor lock-in concerns hindering contracts | -0.6% | Western Europe enterprise segment | Medium term (2-4 years) |

| Skills gap in SIP and VoIP network management | -0.7% | Eastern Europe rural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Cross-Border Data-Sovereignty Regulations

Despite the GDPR, France, Italy, and Germany maintain parallel localization frameworks that require UCaaS vendors to duplicate infrastructure, thereby increasing compliance costs and complicating pan-European rollouts. Multinational firms must map traffic flows to each jurisdiction and maintain separate disaster recovery zones, limiting economies of scale. The proposed Data Governance Act aims for harmonization, yet enforcement is not expected to be implemented until 2027, leaving uncertainty over future platform architecture.

Heightened Cyber-Attack Surface in Cloud Telephony

ENISA recorded telecommunications as a top ransomware target between July 2023 and June 2024, noting the 3CX supply-chain compromise that infiltrated thousands of European endpoints. The incident revealed systemic risk inherent in concentrated UCaaS software stacks. Swiss cybersecurity authorities logged a surge in voice-based fraud, prompting enterprises to bolster endpoint security. Security fears slow adoption among risk-averse sectors such as finance, despite clear cost benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Software Dominance Accelerates Integration

Software solutions held 61.45% of the Europe IP Telephony and Unified Communications As-A-Service market share in 2025 due to demand for scalable cloud-native platforms that embed into existing workflows. The category is projected to post a 10.03% CAGR to 2031 as enterprises favor API orchestration over hardware refresh cycles. Call control and PBX software benefit directly from IP emergency service mandates, while unified messaging and team collaboration tools ride the wave of established hybrid work practices. Vendors integrate AI-based transcription and sentiment analytics, boosting value without additional hardware.

Hardware remains essential for sectors that need physical endpoints with certified security, including defense and utilities. IP desk phones continue to serve trading floors that require tactile interfaces and a fixed quality of service. VoIP gateways ease transitional scenarios during the ISDN phase-out, although their relevance declines as fiber reaches regional hubs. Video endpoints are pivoting toward software-defined meeting rooms, but continue to prioritize where guaranteed optics matter. Overall, hardware growth lags behind software, yet it acts as a compliance safeguard.

By Type: Hosted IP PBX Leads While CPaaS Emerges

Hosted IP PBX contributed 41.92% of 2025 revenue, reflecting its role as a direct cloud replacement for on-premises legacy systems. The model delivers familiar PBX features with cloud scalability, easing compliance with emergency calling standards. Integrated SIP trunking remains a backbone service but loses market share to comprehensive UCaaS suites that include video and messaging.

Communication Platform as a Service (CPaaS), although smaller, is the fastest-growing type, with an 8.58% CAGR through 2031. Developers utilize CPaaS APIs to integrate voice and video capabilities into customer applications, thereby eliminating the need for standalone interfaces and promoting vertical innovation. Managed IP PBX appeals to enterprises that want operational outsourcing but still retain on-site control for sensitive workflows. Cloud call control offers a middle path by decoupling signaling from hardware, allowing firms to preserve their sunk investments. Together, these types illustrate a migration continuum toward programmable communications that underpin digital transformation.

By Organization Size: SME Momentum Outpaces Enterprise Adoption

Large enterprises owned 53.05% of spend in 2025 through multi-site deployments that integrate contact centers, analytics, and compliance modules. They prioritize advanced encryption, granular role-based access, and direct peering relationships with carriers. Yet SME growth, at a 10.05% CAGR, is overtaking as smaller firms exploit subsidy programs such as Spain’s Kit Digital to offset adoption costs.

SMEs value ease of use, mobile accessibility, and predictable operating expenses. Providers respond with packaged offers that bundle broadband, security, and UCaaS under one invoice. The Europe IP Telephony and Unified Communications as-a-Service market size for SMEs is slated to rise sharply as high fiber coverage lowers latency and supports video-heavy workflows. Incentives in Poland and the Czech Republic replicate Spain’s success, suggesting sustained demand over the forecast window.

By End User: Healthcare Drives Fastest Growth

IT and telecom firms led the adoption at a 30.94% share in 2025, as they require collaboration suites for distributed software teams. Banking and insurance organizations follow closely due to the need for stringent audit trails and the requirement for omnichannel customer engagement.

Healthcare is the fastest-growing vertical, with an 8.42% CAGR to 2031, spurred by the EU Digital Health Strategy mandates that facilitate cross-border teleconsultations. Hospitals integrate UCaaS with electronic health records and IoT medical devices, while compliant cloud architectures address patient data privacy. Manufacturing adopts UCaaS to link shop floor sensors with enterprise resource planning data, supporting Industry 4.0 goals. Retail leverages programmable APIs for click-to-call in mobile apps, creating frictionless omnichannel experiences that raise customer satisfaction scores.

Geography Analysis

The United Kingdom held a 22.05% share in 2025, leveraging early fiber rollouts and mature cloud usage patterns. BT Group completed national IP migration, and Vodafone extended 5G to half the population, enabling edge analytics and AI-driven voice services. Growth expectations remain steady, although Brexit-related compliance divergence adds costs for providers serving EU clients.

Germany is the second-largest market, thanks to the completion of ISDN shutdowns and strong industrial demand. Enterprises favor hybrid topologies that combine on-site gateways with cloud call control to meet data residency requirements. France is growing steadily due to support for its sovereign cloud policy, although stringent localization requirements raise entry barriers for foreign platforms. Spain delivers the fastest CAGR at 8.46% due to the España Digital 2026 roadmap and generous SME subsidies that stimulate cloud adoption. Italy accelerates recovery fund allocations targeting public service digitalization. The Netherlands leverages dense data center clusters for low-latency UCaaS, while Nordic countries exhibit the highest per-capita usage and serve as test beds for AI features. Eastern European states benefit from EU infrastructure funds, moving quickly from low baseline penetration to modern cloud communication suites.

Competitive Landscape

The Europe IP Telephony and Unified Communications as-a-Service market exhibits moderate fragmentation, as global suites compete with local specialists. Microsoft Teams dominates through existing Office 365 tenants, yet faces antitrust scrutiny that could lead to unbundling pricing in the future. Cisco Webex leverages extensive channel partners, while RingCentral builds its European footprint via operator alliances, such as Vodafone’s multi-country launch. Zoom partners with Mitel to offer hybrid packages targeting organizations with significant PBX investments.

Regional players such as NFON, Wildix, and Gamma Communications harness regulatory insight and language localization to win mid-market accounts. Gamma’s 2024 purchase of Placetel extends its reach in Germany and adds Cisco Webex capabilities. Telecom operators bundle UCaaS with connectivity, fostering integrated offers that simplify procurement. CPaaS vendors, such as Twilio and Vonage, enter through developer channels, encouraging custom workflows that bypass traditional monolithic suites. Mergers and strategic alliances are expected to continue as vendors seek to scale, achieve broader geographic reach, and drive AI innovation.

Europe IP Telephony And Unified Communications As-a-service Industry Leaders

Microsoft Corporation

Cisco Systems Inc.

RingCentral Inc.

8x8 Inc.

Vonage Holdings Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The EU Data Act officially took effect, obliging UCaaS vendors to let customers move their data to another provider within 30 days and scrapping all switching fees by Jan 2027. The new rule loosens long-standing vendor lock-in and gives European enterprises far more leverage at the bargaining table.

- August 2025: Vodafone Business fast-tracked its RingCentral partnership, widening the joint UC platform to more than 30 countries. By pairing RingCentral’s AI features with Vodafone’s 5G network, the offer promises operating-cost cuts of up to 30% for companies still running legacy PBX gear.

- June 2025: Microsoft came under sharper EU scrutiny over the way it packages Teams with Office 365. Regulators are weighing a possible unbundling order after rivals complained that the bundled pricing puts stand-alone UCaaS providers such as RingCentral and 8x8 at a disadvantage.

- April 2025: Deutsche Telekom finished rolling out a nationwide 5G Standalone network across Germany’s largest cities. Sub-10 millisecond latency is now achievable for real-time UCaaS workloads, opening the door to edge-enabled contact-center applications that demand ultra-low delay.

Europe IP Telephony And Unified Communications As-a-service Market Report Scope

Any technology that falls under internet-based telecommunications, such as fax and other similar technologies, is referred to as IP telephony. To send data from the phone to the service provider, it uses a variety of open-source protocols. Furthermore, because IP telephone solutions are portable and cost-effective, corporations are increasingly embracing them. Additionally, IP telephony systems are gaining popularity due to their ease of use, advanced technology, and increased productivity.

The Europe IP Telephony and Unified Communications As-A-Service Market Report is Segmented by Solution (Hardware, and Software), Type (Integrated Access - SIP Trunking, Managed IP PBX, Hosted IP PBX, Cloud Call Control, CPaaS), Organization Size (Large Enterprises, and SMEs), End User (Healthcare, Retail, IT and Telecom, Government, Manufacturing, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

| Hardware | IP Desk Phones |

| VoIP Gateways | |

| Video Conferencing Endpoints | |

| Other Hardwares | |

| Software | Call Control and PBX Software |

| Unified Messaging | |

| Team Collaboration Platforms | |

| Contact Center Applications | |

| Other Softwares |

| Integrated Access - SIP Trunking |

| Managed IP PBX |

| Hosted IP PBX |

| Cloud Call Control |

| Communication Platform as a Service (CPaaS) |

| Large Enterprises |

| Small and Medium Enterprises |

| Banking, Financial Services and Insurance |

| Healthcare |

| Retail and E-Commerce |

| Information Technology and Telecom |

| Government and Public Sector |

| Manufacturing and Industrial |

| Education |

| Hospitality |

| Other End Users |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Solution | Hardware | IP Desk Phones |

| VoIP Gateways | ||

| Video Conferencing Endpoints | ||

| Other Hardwares | ||

| Software | Call Control and PBX Software | |

| Unified Messaging | ||

| Team Collaboration Platforms | ||

| Contact Center Applications | ||

| Other Softwares | ||

| By Type | Integrated Access - SIP Trunking | |

| Managed IP PBX | ||

| Hosted IP PBX | ||

| Cloud Call Control | ||

| Communication Platform as a Service (CPaaS) | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End User | Banking, Financial Services and Insurance | |

| Healthcare | ||

| Retail and E-Commerce | ||

| Information Technology and Telecom | ||

| Government and Public Sector | ||

| Manufacturing and Industrial | ||

| Education | ||

| Hospitality | ||

| Other End Users | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe IP Telephony and Unified Communications As-A-Service market in 2026?

It is valued at USD 28.18 billion in 2026 with a projected CAGR of 8.35% to 2031.

Which deployment type holds the largest revenue share?

Hosted IP PBX leads with 41.92% of 2025 revenue.

What segment is expanding the fastest by type?

Communication Platform as a Service is forecast to grow at an 8.58% CAGR through 2031.

Why are SMEs adopting UCaaS more quickly now?

Government subsidies and subscription models lower upfront costs, pushing SME CAGR to 10.05%.

Which country records the highest growth rate to 2031?

Spain shows the fastest expansion at an 8.46% CAGR due to its España Digital 2026 incentives.

What is the key restraint for multinational deployments?

Fragmented data-sovereignty rules require separate hosting footprints, raising complexity and cost.

Page last updated on: