Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Vo5G Market Report is Segmented by Service Deployment (Cloud-Based, On-premises/Edge), Network Architecture (Standalone SA, Non-Standalone With EPS Fallback, and More), Application (Consumer Voice and Video, and More), End-User Industry (IT and Telecommunications, Media and Entertainment, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

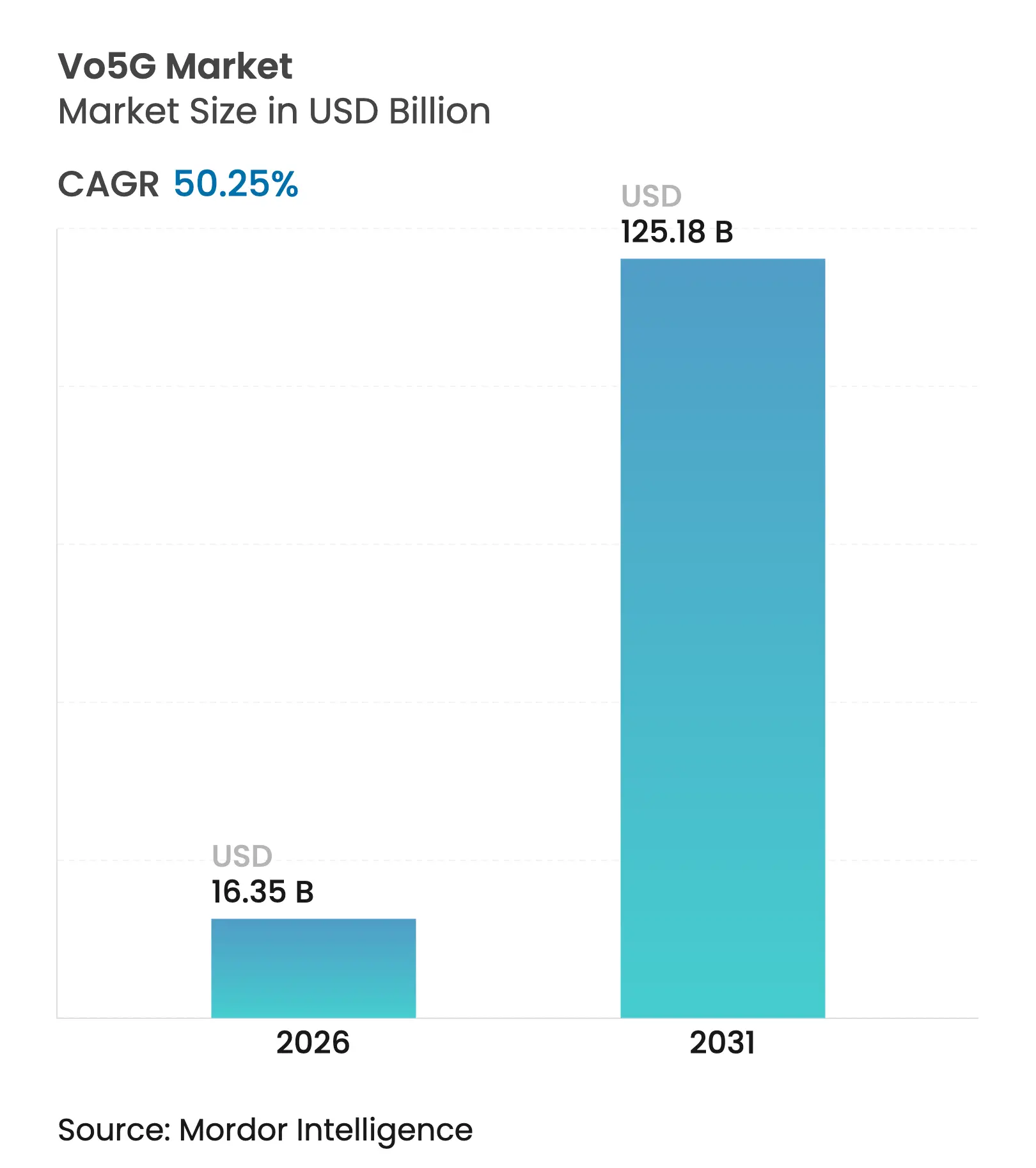

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 16.35 Billion |

| Market Size (2031) | USD 125.18 Billion |

| Growth Rate (2026 - 2031) | 50.25 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Momentum stems from operators monetizing 5G investments through premium Voice-over-New-Radio (VoNR) tiers, hyperscaler edge deployments that cut media-path latency below 20 milliseconds, and device makers standardizing Enhanced Voice Services (EVS) codecs in flagship smartphones. Cloud-native IMS cores further boost profitability by trimming operating costs up to 40% while accelerating service rollout cycles. Asia-Pacific’s first-mover advantage, bolstered by nationwide standalone (SA) rollouts in India and South Korea, cements the region’s dual role as volume leader and innovation testbed. Competitive intensity remains moderate as infrastructure vendors, CPaaS platforms, and mobile operators focus on distinct value-chain layers that collectively expand the addressable Vo5G market.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

5G-SA deployments enabling native VoNR

5G-SA deployments enabling native VoNR

| +18.5% | Global; APAC & North America leading | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+18.5%

|

Geographic Relevance

:

Global; APAC & North America leading

|

Impact Timeline

:

Medium term (2-4 years)

|

5G smartphones with EVS codec support

5G smartphones with EVS codec support

| +12.3% | Global; premium device clusters | Short term (≤ 2 years) | |||

Cloud-native IMS cores lower OPEX

Cloud-native IMS cores lower OPEX

| +15.7% | North America & EU primary, APAC following | Medium term (2-4 years) | |||

“5G New Calling” apps via IMS Data Channel

“5G New Calling” apps via IMS Data Channel

| +8.9% | North America & EU early adoption | Long term (≥ 4 years) | |||

Hyperscaler edge nodes shorten media paths

Hyperscaler edge nodes shorten media paths

| +6.2% | Global; hyperscaler presence determines magnitude | Medium term (2-4 years) | |||

Integrated AI voice analytics in CPaaS

Integrated AI voice analytics in CPaaS

| +5.5% | Global; enterprise hubs | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

5G-SA deployments enabling native VoNR

Standalone 5G deployments remove the fallback bottlenecks that once tethered voice to legacy LTE, allowing carriers to market guaranteed-quality VoNR tiers at premium price points. [1]Corporate Blog, “T-Mobile Nationwide 5G Advanced,” t-mobile.com Operators such as Vodafone Idea in India replaced multi-generation radio stacks with Ericsson 5G radios, consolidating costs while activating advanced voice slicing capabilities that attract enterprise client. The sub-20 millisecond end-to-end latency achieved on SA networks also enables high-demand use cases like remote surgery and industrial safety systems. Competitive differentiation now hinges on how rapidly carriers migrate subscribers onto SA cores. The resulting uplift in average revenue per user underpins the double-digit contribution of this driver to overall Vo5G market growth.

5G smartphones with EVS codec support

A sharp rise in 5G-capable devices featuring the EVS codec removes the device-side quality bottleneck that once muted HD-voice adoption. Flagship handsets from Samsung and Apple ship with automatic VoNR fallback plus battery-optimized EVS profiles, which pave the way for mass-market premium-voice upsells. Fixed wireless access gateways equipped with Qualcomm X65 chipsets extend crystal-clear calls into rural households, expanding the Vo5G market beyond mobile handsets. As more mid-tier smartphones adopt the codec, the addressable subscriber base broadens, pushing operators to bundle enhanced voice in core tariff plans. This device penetration surge directly fuels double-digit CAGR acceleration for the Vo5G market. [2]Product Sheet, “Qualcomm Snapdragon X65 Modem,” qualcomm.com

Cloud-native IMS cores lower OPEX

Cloud-native IMS cores slash hardware footprints and enable DevOps release cadences that shrink feature rollouts from months to weeks. AT&T’s public-cloud deployment with Nokia demonstrates 30–40% OPEX savings, freeing capital for marketing premium calling tiers that further raise average margins. Boost Mobile’s fully cloud-hosted voice core validates commercial readiness even for challenger brands, trimming total cost of ownership and democratizing access to next-generation services. Seamless integration with hyperscaler AI engines allows real-time noise suppression and speaker-ID functions, creating revenue streams that transcend the traditional per-minute model. Collectively, these economics elevate cloud IMS to a top-three growth catalyst for the Vo5G market.

“5G New Calling” apps via IMS Data Channel

IMS Data Channel-powered “5G New Calling” transforms voice from a utility into a multi-media platform. Telefónica’s holographic-calling trials proved that 3D avatars can run natively in standard dialers, delivering experiential upgrades that justify subscription premiums. Nokia’s spatial-audio demo illustrated how immersive soundscapes increase user engagement and call durations, providing carriers with monetizable metrics in advertising and in-call commerce. As SDKs mature and move into the hands of third-party developers, an ecosystem of voice-centric apps—language tutoring, immersive events, virtual retail—emerges. Operators that expose network APIs accelerate this platformization trend, fortifying Moats against over-the-top challengers and driving sustained Vo5G market expansion. [3]Blog Post, “Telefónica Next-Gen Communications,” telefonica.com

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High 5G core and IMS upgrade CAPEX

High 5G core and IMS upgrade CAPEX

| -8.7% | Global; disproportionately affects smaller operators | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-8.7%

|

Geographic Relevance

:

Global; disproportionately affects smaller operators

|

Impact Timeline

:

Short term (≤ 2 years)

|

Fragmented device compatibility across regions

Fragmented device compatibility across regions

| -6.2% | Global; diverse regulatory bands | Medium term (2-4 years) | |||

QoS complexity with encrypted traffic (DoH/QUIC)

QoS complexity with encrypted traffic (DoH/QUIC)

| -4.1% | Global; hampers optimization tooling | Long term (≥ 4 years) | |||

Regulatory uncertainty on 2G/3G sunsets &

emergency-calling compliance

Regulatory uncertainty on 2G/3G sunsets &

emergency-calling compliance

| -5.8% | North America & EU; spillover to APAC | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High 5G core and IMS upgrade CAPEX

The capital intensity of 5G core refreshes weighs heavily on carriers with limited spectrum portfolios and smaller subscriber bases. AT&T elevated 2024 network investment to USD 20.3 billion, 13% higher than the prior year, underscoring the scale of expenditure required to unlock VoNR revenues. Smaller regional operators lack similar balance-sheet flexibility, prompting delays or joint-venture models that ultimately slow overall Vo5G market uptake. Financing constraints also push some providers toward phased rollouts that compromise nationwide service consistency and user experience over the next two years.

Fragmented device compatibility across regions

Device-fragmentation stems from divergent 5G band allocations and national certification mandates that force handset vendors to create localized SKUs. Manufacturers shoulder incremental testing costs and longer release cycles, which translate to steeper device price tags in emerging markets. Operators then grapple with mixed codec and band support across their installed bases, driving up customer-care and network-optimization overheads. Standard-harmonization initiatives remain multi-year projects, leaving carriers exposed to compatibility issues that dampen the near-term Vo5G market CAGR.

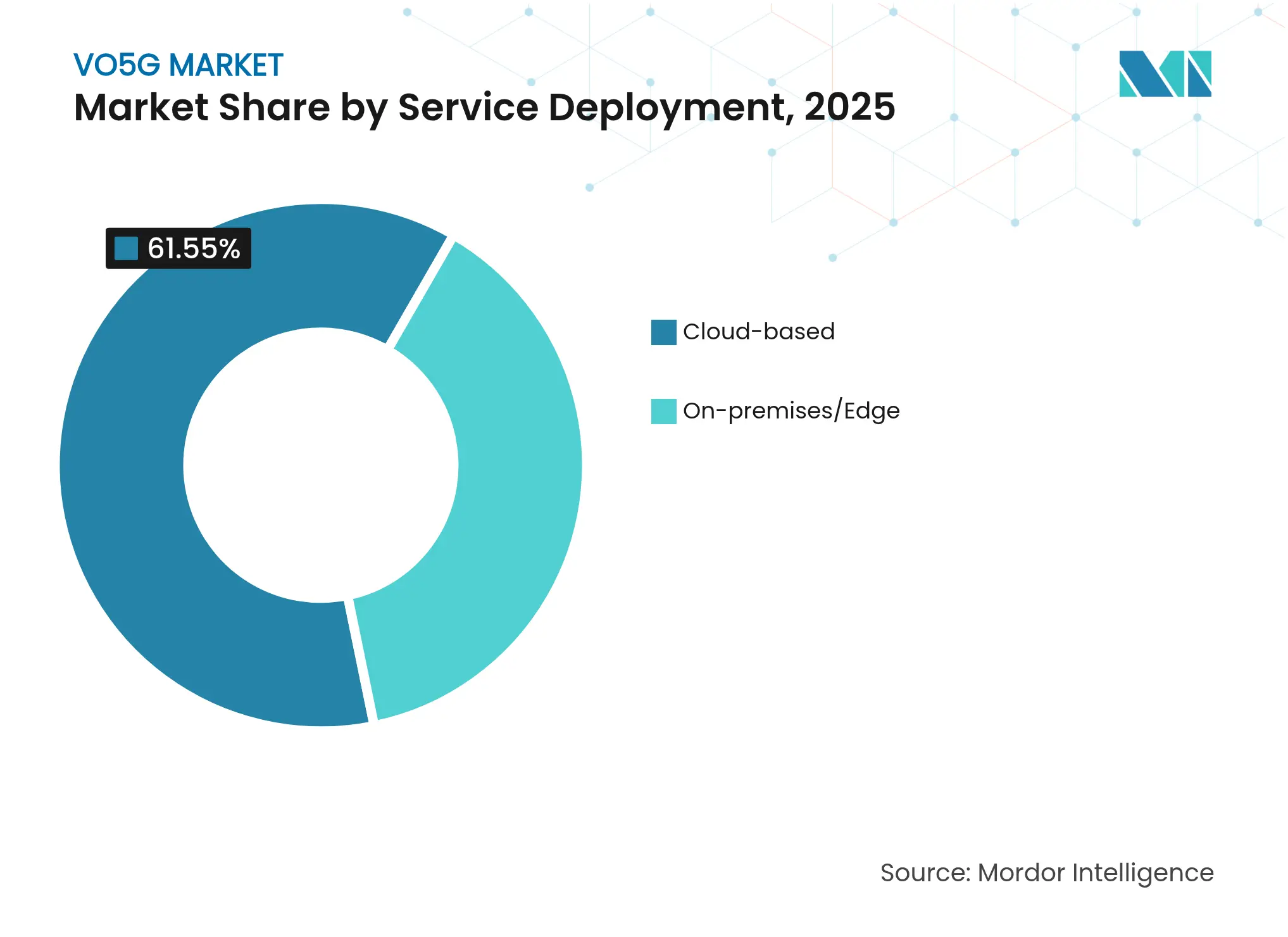

By Service Deployment: Cloud Dominance Accelerates Migration

Cloud implementations accounted for 61.55% of the Vo5G market share in 2025, and the segment is set to widen its lead with a 51.05% CAGR through 2031. The economics of serverless scaling, hot-patch upgrades, and pay-as-you-grow licensing resonate with operators seeking capital-light expansion paths. Cloud IMS also plugs directly into hyperscaler AI toolkits, enabling on-the-fly quality enhancements and sentiment analytics that unlock new revenue pools. Regulatory requirements for data sovereignty foster hybrid topologies in Europe and parts of APAC, but even these networks anchor control-plane functions in public or telco clouds to maximize agility. Service-level automation—zero-touch provisioning, CI/CD pipelines, and closed-loop assurance—shortens customer onboarding cycles, boosting stickiness and driving incremental Vo5G market size gains.

On-premises and edge deployments retain relevance in ultra-low-latency use cases such as mission-critical manufacturing lines and defense communications. Operators therefore deploy micro-edge instances of cloud IMS for proximity-based processing while centralizing non-time-sensitive workloads. This tiered model delivers both efficiency and compliance, yet the management overhead is lower than legacy architectures thanks to container orchestration. As more vendors ship hardened Kubernetes distributions for telecom workloads, small and mid-size carriers gain confidence to leapfrog directly into cloud-first strategies. Consequently, the Vo5G market continues tilting toward elastic infrastructure even as localized gateways proliferate.

Note: Segment shares of all individual segments available upon report purchase

By Network Architecture: Standalone SA Drives Premium Services

Standalone networks represented 54.10% of the Vo5G market size in 2025 and are advancing at a 51.74% CAGR as operators chase QoS differentiation. Fully decoupled from LTE EPC cores, SA setups enable network slicing that promises dedicated voice lanes for enterprises willing to pay for hard SLAs. Early deployments in India and the United States report sub-20 millisecond call-setup times, elevating user-perceived quality and reducing call-drop rates. Operators leverage these metrics in marketing, enabling upsell bundles that lift average revenue even in saturated markets. Non-Standalone modes persist mainly where coverage ambitions outweigh immediate monetization goals, notably across parts of Southeast Asia and Latin America.

RAT fallback configurations, while transitional, still act as safety nets in heterogeneous device environments. However, once penetration of SA-capable chipsets crosses the 60% threshold, carriers accelerate LTE sunset timelines to reclaim spectrum for capacity augmentation. Vendor roadmaps anticipate wider availability of low-band SA radios, which will extend premium voice experiences into rural zones. Collectively, these factors entrench SA architecture as the foundation for high-value voice services, reinforcing its impact on overall Vo5G market growth.

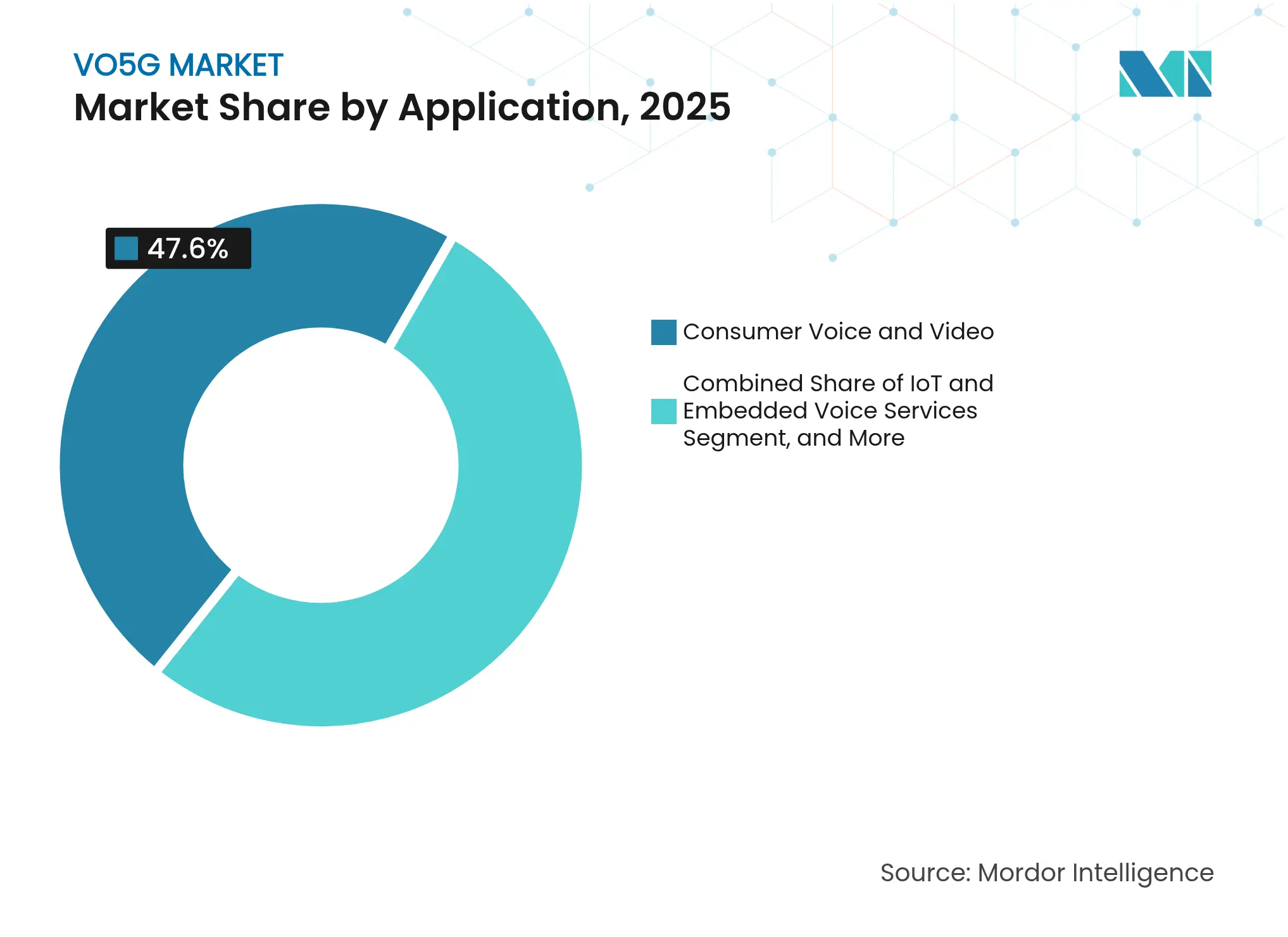

By Application: Enterprise CPaaS Outpaces Consumer Growth

Enterprise CPaaS and interactive calling is projected to register the fastest 52.41% CAGR, while consumer voice and video held 47.60% revenue share in 2025. Businesses are embedding carrier-grade voice APIs into workflows ranging from field-service dispatch to tele-banking, turning calls into data-rich transactions that justify higher ARPUs. Twilio’s AI-powered summarization illustrates how analytics plug-ins enhance productivity and compliance simultaneously, fortifying willingness to pay for premium channels. Public-safety networks, exemplified by FirstNet’s USD 6.3 billion upgrade plan, accelerate adoption of mission-critical Vo5G features, further expanding the Vo5G market size.

Consumer traffic growth remains healthy but shows margin compression as over-the-top providers commoditize basic calling. Operators counter by bundling spatial-audio and in-call translation to restore pricing power. IoT voice, though nascent, gains traction in automotive emergency systems and smart-home devices that need embedded two-way communication. As handset data usage plateaus, diversified application segments keep the Vo5G market on its steep growth trajectory.

Note: Segment shares of all individual segments available upon report purchase

By End-user Industry: Healthcare Leads Digital Transformation

Healthcare is on track to grow at a 51.88% CAGR, driven by latency-sensitive telemedicine, remote surgery, and smart-hospital deployments that demand premium QoS. Real-time voice acts as a clinical tool, linking remote specialists and bedside teams without perceptible lag, thereby enhancing patient outcomes. IT and telecommunications, holding 36.00% of 2025 revenues, continues to invest as operators use their own networks as live test beds for advanced voice services. Manufacturing embraces Vo5G for safety alarms and robotic control loops, where voice remains the intuitive interface for human-machine collaboration.

Financial-services institutions adopt encrypted VoNR channels for trading-floor compliance and secure advisory calls. Retail blends voice with augmented-reality shopping assistants, extending customer engagement beyond text chat. Transportation and logistics integrate voice into vehicle telemetry for incident response, capitalizing on network slices that guarantee always-on availability. These diverse uptake patterns underscore how sector-specific KPIs sustain expansion of the Vo5G market.

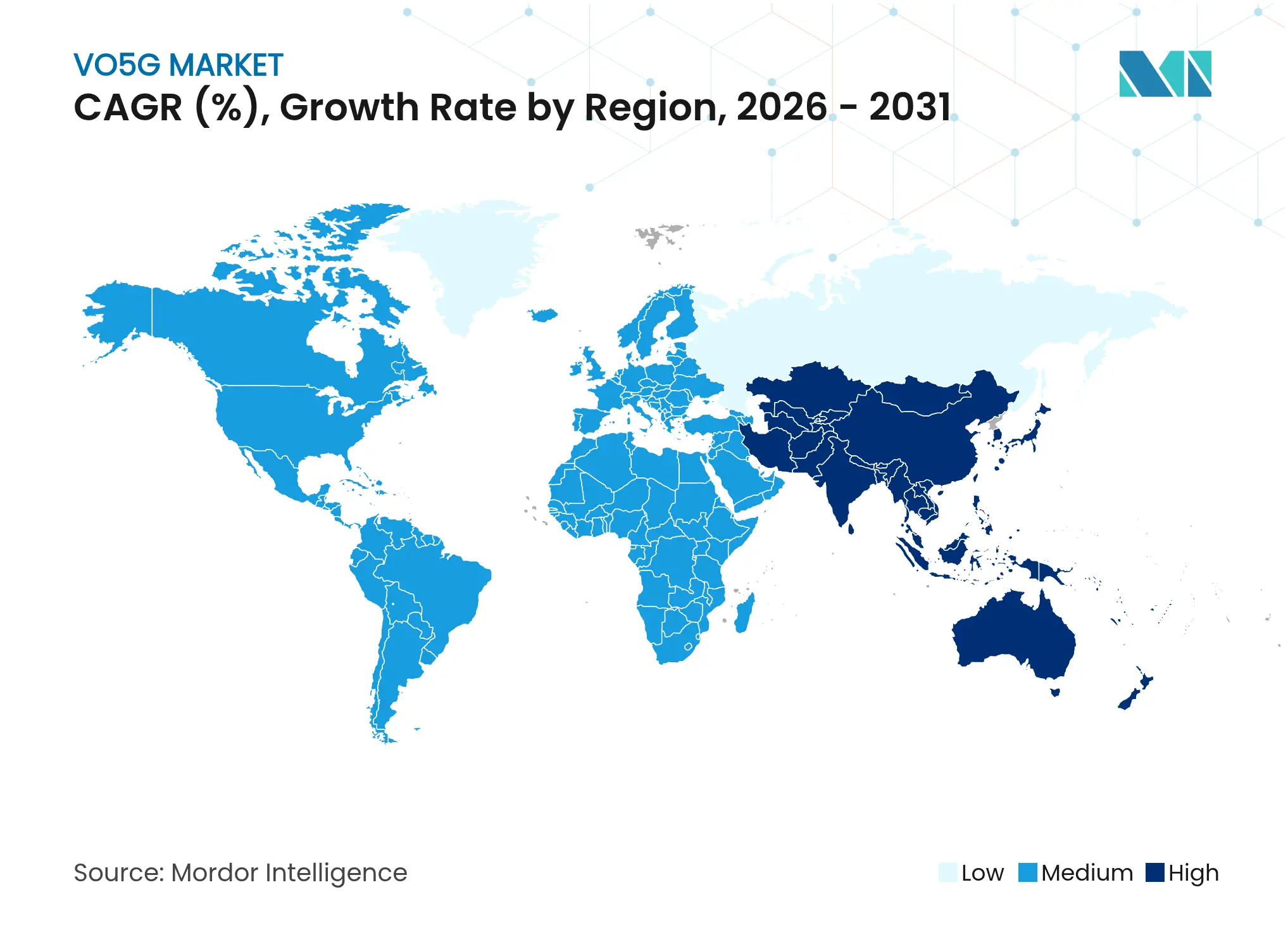

Asia-Pacific commanded 39.10% of global Vo5G market share in 2025 and is forecast to expand at a 52.62% CAGR through 2031. Dense urban populations, competitive spectrum pricing, and government-backed digital initiatives accelerate both consumer and enterprise adoption. India’s full-scale VoNR rollout by Jio proved that emerging markets can bypass intermediate LTE-voice stages, instantly unlocking premium revenue layers. South Korea exploits SA slicing to monetize corporate voice channels in manufacturing and media, setting global pricing benchmarks that other operators replicate. China’s scale draws device and chipset vendors, fostering cost declines that spill over into ASEAN markets and elevate regional Vo5G market size.

North America leverages early network leadership to pursue enterprise ARPU rather than pure subscriber volume. T-Mobile turns nationwide 5G Advanced coverage into a platform for tiered voice experiences aimed at small-to-medium enterprises that value guaranteed quality. AT&T’s cloud-native IMS adoption reduces operational drag, allowing faster commercialization of AI-enhanced call features. Regulatory emphasis on public-safety reliability stimulates specialized voice slices, anchoring further growth in the Vo5G market.

Europe emphasizes harmonized standards and privacy-by-design architectures. Deutsche Telekom co-founded the Global Telco AI Alliance to pool resources on multilingual LLMs fitting GDPR constraints, ensuring compliant rollouts of AI voice services. Cross-border roaming agreements that maintain VoNR continuity enhance user experience for frequent travelers, creating premium-roaming bundles that lift revenue. Progress in smaller markets such as the Nordics demonstrates that even with modest populations, high digital literacy translates into robust per-capita spending on advanced voice.

Market Concentration

The Vo5G market exhibits moderate concentration. Huawei, Ericsson, and Nokia collectively shipped close to 58% of global Vo5G RAN and core units in 2024, leveraging economies of scale in chipset supply chains. Ericsson’s 2025 network-API joint venture with major carriers extends its influence into the platform layer, threatening hyperscaler dominance in service exposure. Nokia pursues a cloud-agnostic strategy, partnering with AT&T and Boost Mobile to validate public-cloud IMS at scale, a move that resonates with cost-sensitive disruptor brands.

Infrastructure incumbents increasingly collaborate with CPaaS leaders. Sinch integrated Ericsson’s network APIs to deliver QoS-aware calling to enterprise CRMs, stitching telecom reliability into SaaS workflows. Twilio maintains a device-agnostic edge by focusing on developer experience, yet now negotiates preferential network slices that improve call initiation speed for critical verticals such as healthcare. These alliances blur historical boundaries, but also raise the competitive bar for smaller voice-application vendors.

Start-ups carve niches via specialized voice-AI or ultra-secure encryption stacks. Hologram-calling pioneer Matsuko partners with Telefónica to co-develop consumer AR experiences embedded directly in stock dialers, circumventing over-the-top friction. Edge-native analytics vendors offer network-resident voice anomaly detection that appeals to public-safety agencies. While M&A activity remains subdued, analysts anticipate targeted acquisitions as incumbents race to integrate differentiated capabilities and solidify their foothold in the expanding Vo5G market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Voice over 5G (Vo5G) enables voice calls to be transmitted over the Internet Protocol (IP). Vo5G necessitates a new radio system to harness its full voice capabilities. Additionally, it can leverage the 4G voice and video communication framework, known as VoLTE, which operates on the IP multimedia subsystem.

The market is defined by the revenue accrued from sales of Vo5G (Voice-over-5G) solutions offered by market vendors to companies across the globe.

Voice-over-5G (Vo5G) Market is segmented by service deployment (cloud-based, on-premises), by end-user industry (IT & telecommunication, retail (digital e-commerce), BFSI, transportation, media and entertainment, other end-user industries), by geography (North America, Europe, Asia Pacific, Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.