Voice Assistant Application Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

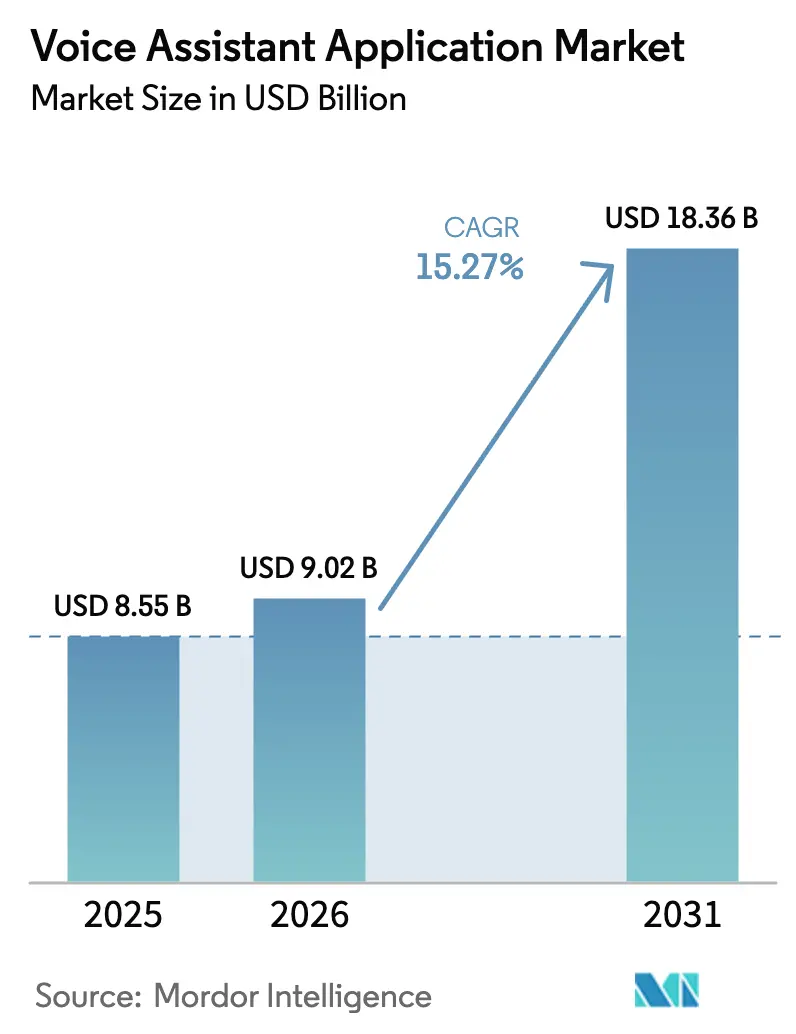

| Market Size (2026) | USD 9.02 Billion |

| Market Size (2031) | USD 18.36 Billion |

| Growth Rate (2026 - 2031) | 15.27% CAGR |

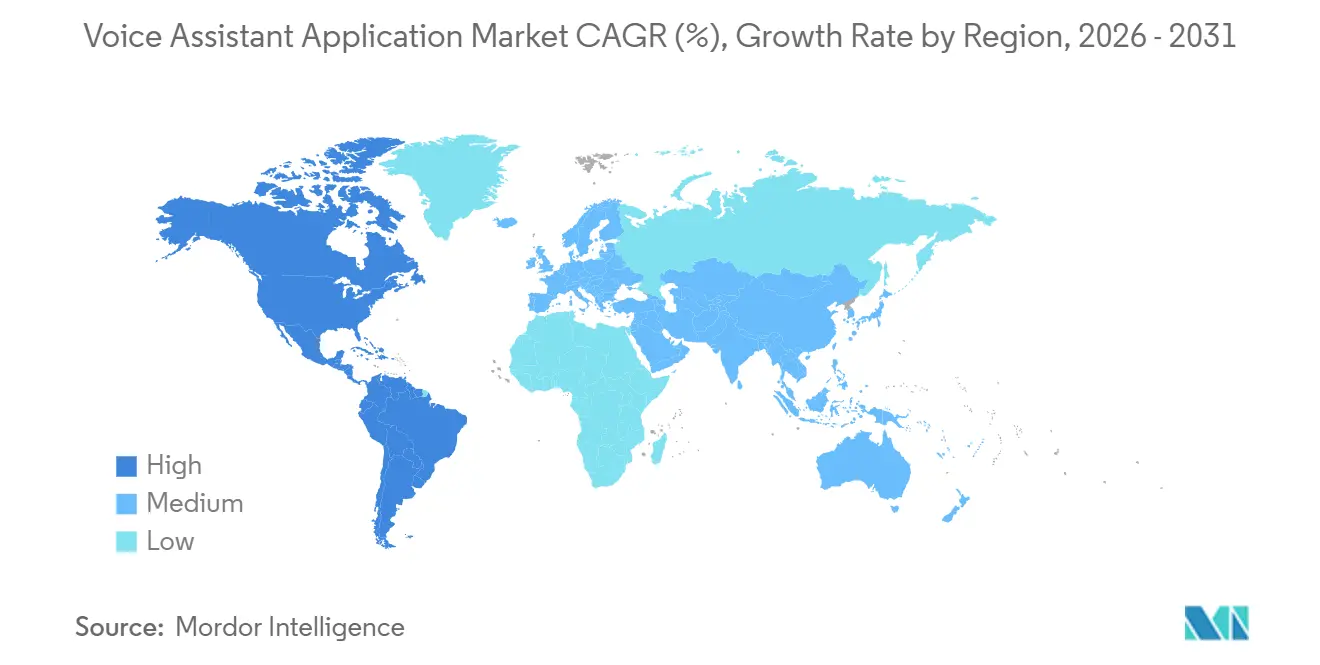

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

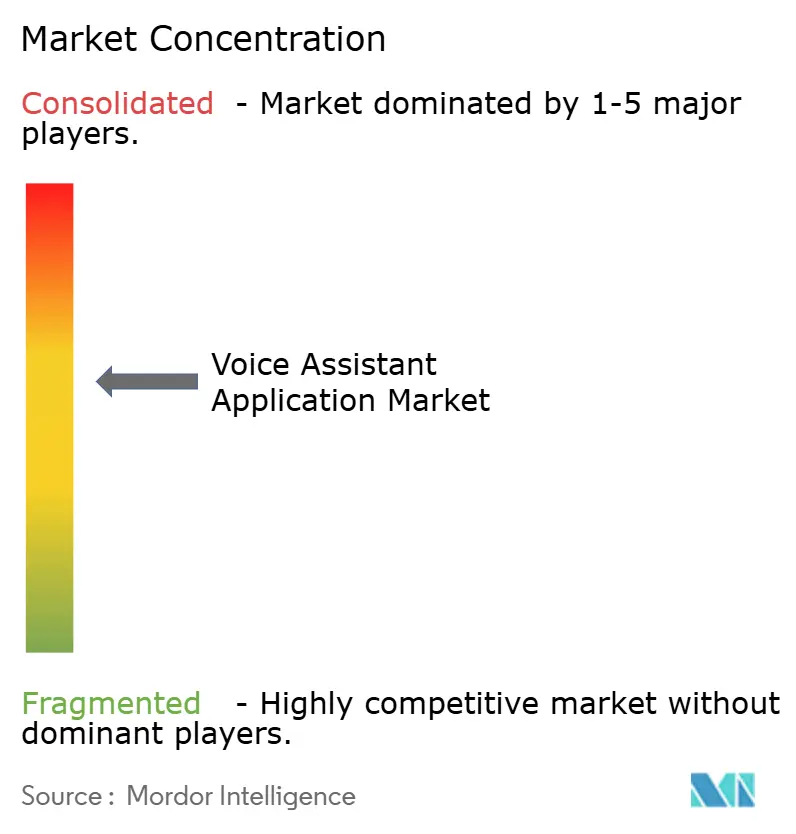

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Voice Assistant Application Market Analysis by Mordor Intelligence

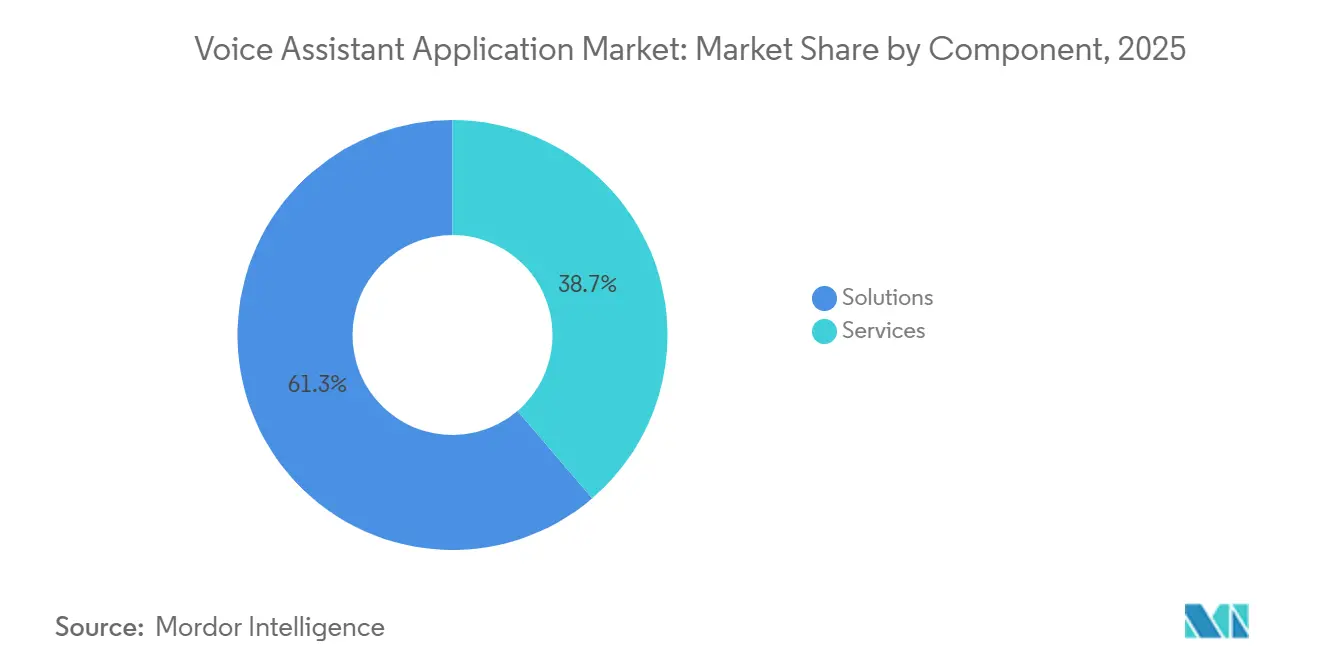

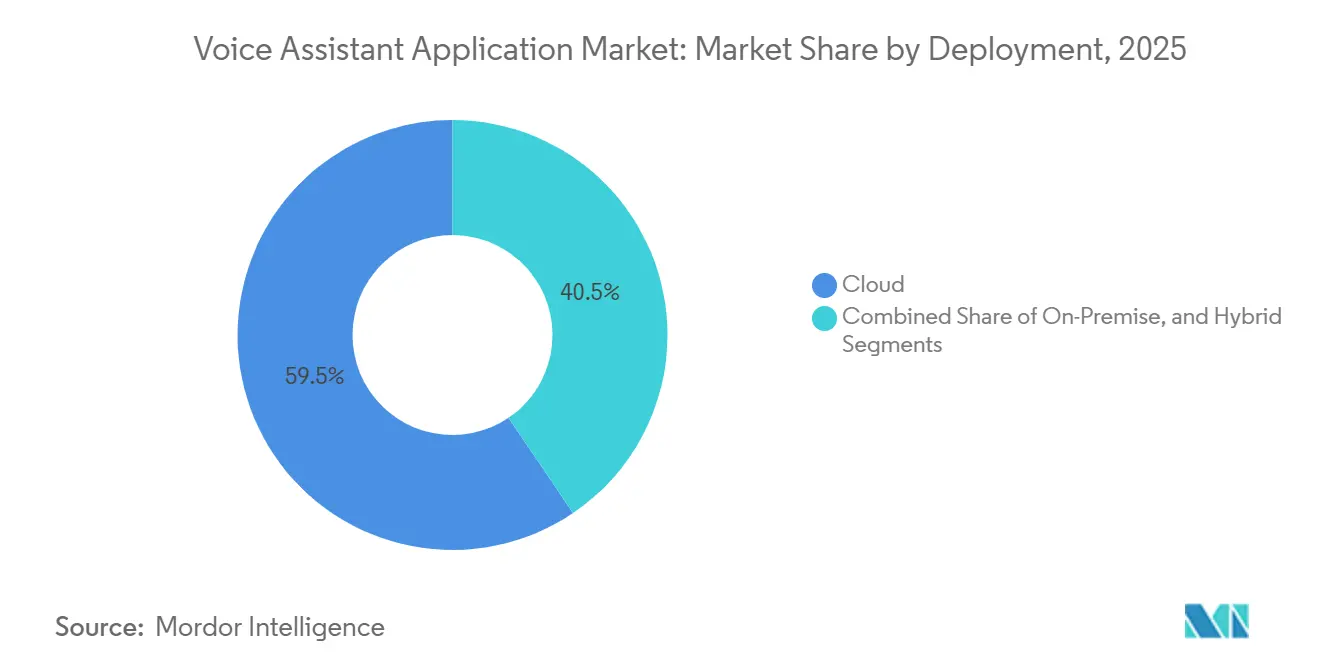

The voice assistant application market size is projected to be at USD 8.55 billion in 2025, reached USD 9.02 billion in 2026 and is projected to climb to USD 18.36 billion by 2031, advancing at a 15.27% CAGR from 2026-2031. This growth trajectory stems from the shift of voice assistants from novelty add-ons to core enterprise utilities as large-language-model dialog engines now handle multi-turn customer interactions with near-human fluency. Within the current landscape, solutions account for 61.27% of the voice assistant application market share, yet services will see faster 17.22% expansion as organizations outsource the integration of Alexa, Google Assistant, and Siri into proprietary workflows. Spending remains anchored in speech recognition at 46.63%, although edge computing is accelerating at 16.88% because automotive and smart-home vendors favor on-device wake-word processing to minimize latency and safeguard privacy. Cloud deployment retains 59.47% share, but hybrid models are widening at 15.75% as healthcare and financial institutions split sensitive and general queries between local chips and hyperscale natural-language engines, while Asia-Pacific outpaces North America on the back of vernacular assistants such as China’s DuerOS and India’s Bhashini.

Key Report Takeaways

- By component, solutions led with 61.27% revenue share in 2025, whereas services are poised to record the fastest 17.22% CAGR through 2031.

- By technology, speech recognition accounted for 46.63% of the voice assistant application market size in 2025, while edge computing is projected to grow at a 16.88% CAGR to 2031.

- By deployment, cloud implementations held 59.47% share in 2025; hybrid architectures are expected to expand at a 15.75% CAGR over the forecast period.

- By enterprise size, large enterprises commanded 61.92% of 2025 revenue, but small and medium enterprises will exhibit a 16.91% CAGR through 2031.

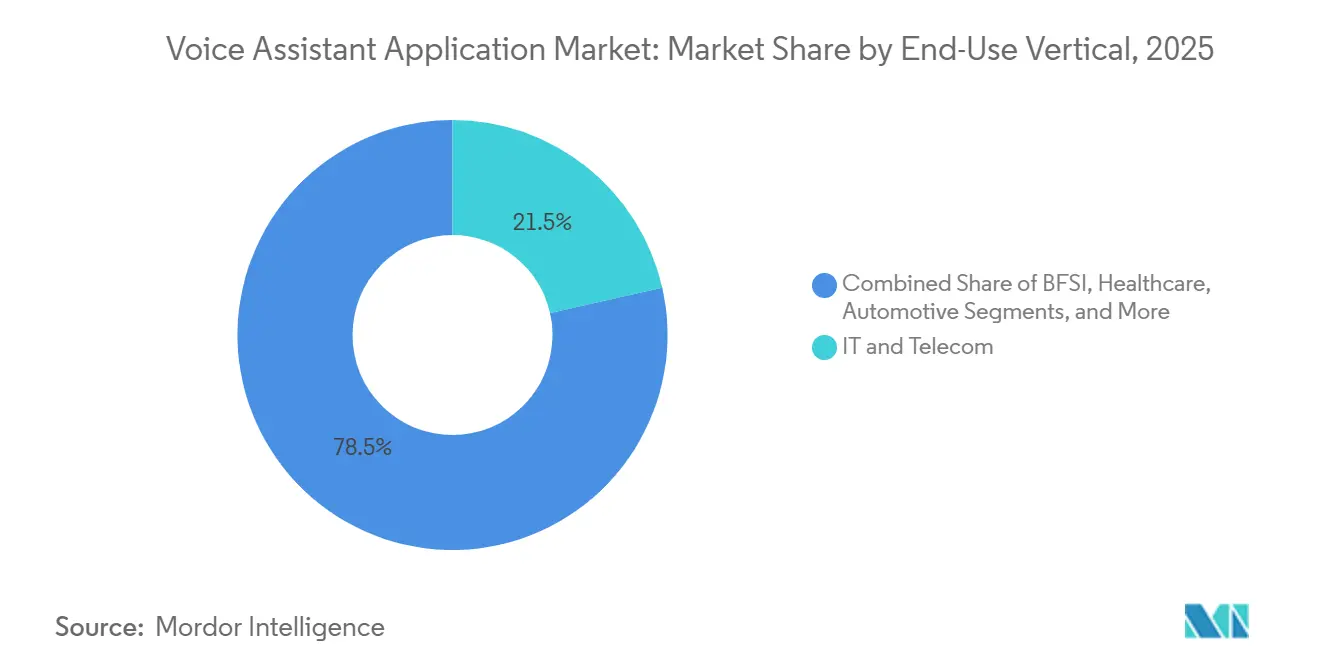

- By end-use vertical, IT and telecom generated the largest 21.48% share in 2025, whereas healthcare is forecast to advance at a 17.06% CAGR to 2031.

- By geography, North America led with 36.65% of 2025 revenue, while Asia-Pacific is set to grow at a 18.02% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Voice Assistant Application Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in smart-speaker and voice-enabled device adoption | +2.8% | Global, with concentration in North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Rapid cost reduction in real-time LLM-powered speech pipelines | +3.2% | Global, particularly benefiting SMEs in Europe and North America | Short term (≤ 2 years) |

| Enterprise push to automate customer-service and IVR workflows | +3.5% | North America and Europe lead, with APAC financial services accelerating | Medium term (2-4 years) |

| Hybrid on-device and cloud architectures unlocking regulated-industry demand | +2.1% | North America and EU healthcare and BFSI sectors, spillover to APAC | Long term (≥ 4 years) |

| Accessibility regulations (WCAG 3.0/ADA) mandating voice UIs | +1.6% | North America federal contractors, EU public sector, gradual APAC adoption | Long term (≥ 4 years) |

| Conversational commerce add-ons boosting average order value | +1.9% | Global retail and e-commerce, strongest in North America and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge In Smart-Speaker And Voice-Enabled Device Adoption

Smart-speaker shipments reached 150 million units in 2024, placing Alexa and Google Nest devices in 40% of U.S. homes and 28% of urban households in the Asia-Pacific region, creating a broad channel for third-party skills.[1]“Voice AI Trends 2025: Enterprise Adoption Survey.” deepgram.com Eighty-four percent of enterprises polled by Deepgram in 2025 planned budget increases for voice assistants, signaling a shift from proofs of concept to production roll-outs. Logistics operators using Alexa for Business reported a 15-20% error reduction in warehouse picking compared to handheld scanners, underscoring the labor-savings potential. Automakers embedded voice assistants as standard equipment, and Tesla logged a 40% year-over-year rise in voice commands during Full Self-Driving mode in 2024, reflecting safety appeal. The expanding installed base supplies usage data that improves model accuracy, establishing a virtuous cycle that reinforces adoption.

Rapid Cost Reduction In Real-Time LLM-Powered Speech Pipelines

Inference costs for large-language-model speech stacks have fallen roughly 60% since 2023 due to speculative decoding and model quantization, keeping intent accuracy above 95% while slashing compute needs. Microsoft Azure trimmed Cortana and Bot Service pricing by 35% for high-volume clients in 2025, a response to price pressure from Voiceflow and Rasa that lowered barriers for small enterprises. Streaming natural-language processing now returns partial intents within 200 milliseconds, eliminating latency that previously eroded customer-service satisfaction. OpenAI’s Whisper v3 Turbo, released December 2025, delivered 15% faster inference across 99 languages while holding word-error rates below 3%, enabling affordable multilingual assistants. Collectively, cheaper, faster pipelines democratize voice deployments beyond large enterprises.

Enterprise Push To Automate Customer-Service And IVR Workflows

Rising labor shortages and wages exceeding USD 50 per hour in North America and Western Europe are reducing the payback period for automated voice assistants handling tier-1 calls. Twilio customers integrating Google Dialogflow into Flex cut average handle time by 28% and saved USD 1.2 million annually for a 200-seat center in 2024. Genesys Cloud CX handled 65% of frontline inquiries without escalation in 2025, up from 42% in 2023, highlighting rapid maturity of conversational IVR. The United States Internal Revenue Service processed 1.3 million calls through a pilot voice assistant in 2024, reducing wait times from 27 minutes to under five minutes. Banks using Boost.ai automated 89% of routine inquiries in 2025, raising satisfaction scores above human benchmarks.

Hybrid On-Device And Cloud Architectures Unlocking Regulated-Industry Demand

Hospitals and banks are adopting split workloads that keep wake-word detection and simple commands local while sending complex intents to the cloud, satisfying data-residency clauses in HIPAA and GDPR. The U.S. Food and Drug Administration’s 2024 draft guidance on software-as-a-medical-device voice assistants requires on-device processing of patient audio, steering vendors toward hybrid models. Nuance’s Dragon Ambient eXperience served more than 550 health systems by 2025, using edge inference to transcribe visits yet uploading only de-identified summaries for model tuning. JPMorgan Chase piloted local voiceprint matching in 2024, cutting fraud losses 34% while meeting cybersecurity rules. Qualcomm’s Snapdragon 8 Gen 3 runs wake-word detection under 2 watts, making always-on assistants viable in wearables and vehicles.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent privacy and data-security concerns | -2.4% | Global, with heightened scrutiny in EU under GDPR and California under CCPA | Medium term (2-4 years) |

| Accuracy gaps across accents, dialects, and noisy settings | -1.8% | Global, particularly affecting non-native English speakers and emerging markets | Short term (≤ 2 years) |

| Integration complexity and specialized talent shortages | -1.3% | North America and Europe SME segments, moderate impact in APAC | Medium term (2-4 years) |

| Rising deep-fake or voice-spoofing threats tightening compliance | -1.1% | Financial services and government sectors globally, concentrated in OECD markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Privacy And Data-Security Concerns

Voice transcripts qualify as biometric data under GDPR Article 9 and the California Consumer Privacy Act (CCPA) rules, requiring firms to obtain explicit consent and minimize retention.[2]GDPR. “Article 9: Processing of Special Categories of Personal Data.” gdpr-info.eu A 2024 PwC poll showed 63% of consumers uneasy with always-on microphones, citing the 2023 Alexa breach that exposed 1.2 million transcripts. Hong Kong police documented the first deep-fake audio job-interview scam in February 2024, driving insurers to exclude voice-spoof losses without liveness checks. Illinois, Texas, and Washington biometric laws carry statutory damages up to USD 5,000 per violation, posing an existential risk for startups without compliance tooling. The U.S. Federal Trade Commission fined a telehealth provider USD 8 million in 2024 for unencrypted recordings, deterring investment in healthcare voice assistants.

Accuracy Gaps Across Accents, Dialects And Noisy Settings

Stanford University found 19% higher word-error rates for non-native versus native English speakers across major assistants in 2024. A Forrester survey the same year reported 38% of enterprises delaying deployments because assistants mishandle accented speech. Google Assistant reached only 78% accuracy on Indian English, far below 94% for General American English, limiting adoption in South Asia. Code-switching utterances such as Spanglish and Hinglish still exceed 40% error rates, undermining customer-service quality in bilingual markets. Background noise above 70 decibels degrades transcription by up to 35%, forcing companies to buy beamforming microphones that raise workstation costs USD 200-500 and slow return on investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge As Skill Development Demands Expertise

Solutions captured 61.27% of the voice assistant application market share in 2025, yet the services segment is forecast to post a 17.22% CAGR through 2031 as enterprises realize that embedding Alexa, Google Assistant, or Siri into business workflows involves continuous intent-mapping, dialogue-flow tuning, and compliance audits. Professional services encompass custom skill creation for regulated tasks, such as clinical documentation or shop-floor inventory checks, which require domain-specific vocabulary not available in generic marketplaces. Integration projects still span nine months on average, with nearly half the schedule spent labeling intents rather than writing code, which drives demand for outside linguists and conversation designers. Managed-services contracts are growing because they bundle uptime service-level agreements and periodic model retraining, freeing digital-transformation teams from the need to hire scarce conversational-AI engineers. IBM reported that 68% of its Watson Assistant customers in 2025 chose a managed model over self-service APIs, indicating a clear preference to outsource ongoing optimization.

The solutions segment is benefiting from no-code design tools that let non-developers draft flows, yet even these platforms require linguistic expertise to craft prompts and handle slot-filling errors. Vertical specialists, notably in healthcare, now preload vocabularies and HIPAA-compliant workflows, shrinking time-to-value for hospitals deploying ambient voice assistants. Small and medium enterprises gravitate toward predictable monthly service fees rather than variable cloud-API bills, a trend reinforced by white-label offerings that package hosting, monitoring, and analytics. Although automation will compress services margins over time, the complexity of multi-language deployments and the rise of code-switching use cases ensure that human-in-the-loop quality checks remain critical to the voice assistant application market size expansion over the forecast horizon.

By Technology: Edge Computing Enables Privacy-Preserving Voice Assistants

Speech recognition commanded 46.63% of 2025 spending, yet edge computing is projected to advance at a 16.88% CAGR to 2031 as privacy-conscious users push wake-word detection and routine commands onto local silicon. The voice assistant application market size for speech recognition remains foundational because every conversational stack starts with audio-to-text conversion, but on-device neural processors now handle basic tasks under 2 W, trimming latency and cloud fees. Qualcomm’s Snapdragon 8 Gen 3 demonstrated reliable wake-word detection in automotive dashboards without cellular connections, while Apple’s iOS 19 moved 78% of common Siri queries on-device, reducing infrastructure costs by roughly 40%. Text-to-speech has gained momentum from generative models that add emotional inflection, although vendors now watermark synthetic audio to deter deepfake abuse.

Natural language processing still primarily runs in the cloud for complex queries because large language model inference strains mobile hardware; however, quantized variants, such as Llama 3.2 1B, are starting to power lightweight intent classification on smartphones. NVIDIA’s Jetson Orin platform showed 30-frame-per-second command recognition in warehouse tests, bringing hands-free quality inspection to industrial clients. Regulatory pressure for data localization in healthcare and finance, combined with the economics of avoiding per-query cloud charges, underpins the strong outlook for edge nodes within the broader voice assistant application market.

By Deployment: Hybrid Architectures Balance Privacy And Capability

Cloud deployment held 59.47% share in 2025 thanks to hyperscaler elasticity and rapid model updates, yet hybrid architectures are set to grow at a 15.75% CAGR because regulated sectors must segregate sensitive audio. Under a hybrid pattern, wake-word detection and simple commands run locally, while knowledge queries route to hyperscale natural-language engines; Alexa and Siri already follow this split workflow. The voice assistant application market share for on-premise installations is shrinking as vendors retire perpetual licenses, but air-gapped defense networks still require fully local stacks. Forty-seven percent year-over-year query growth on Amazon Alexa Voice Service in 2024 highlighted cloud scale,[3]Amazon Web Services. “Alexa Voice Service: 2024 Re:Invent Highlights.” aws.amazon.com yet 54% of healthcare CIOs surveyed by HIMSS favored hybrids to satisfy HIPAA encryption rules.

Hybrid deployments introduce orchestration overhead; however, control-plane suites from Azure Stack and Google Anthos now offer policy-based routing, which simplifies management. Processing high-volume, low-risk smart-home commands on-device cuts cloud API costs by up to 70%, allowing budgets to cover more sophisticated analytics. Manufacturers in bandwidth-constrained sites also value local inference because it prevents production delays when connectivity is disrupted. These cost and compliance advantages ensure hybrids remain the fastest-growing slice of the voice assistant application market size through 2031.

By Enterprise Size: SMEs Adopt White-Label Voice Assistant Platforms

Large enterprises generated 61.92% of 2025 revenue by spreading development costs across multiple use cases, but small and medium enterprises will post a 16.91% CAGR as white-label platforms eliminate up-front engineering barriers. Twilio’s Flex reported that 42% of new seats in 2024 came from SMEs lured by entry pricing near USD 1 per user each month. APIs from RapidAPI and turnkey packages from Weave and Podium embed conversational commerce or appointment scheduling without custom skill coding.

Smaller firms still lack proprietary data to fine-tune intents, so they depend on transfer learning from pre-trained models and on managed-service partners for ongoing optimization. Deloitte found that 67% of SMEs struggled to hire conversational AI talent in 2024, underscoring the staffing gap. Meanwhile, large enterprises retain an advantage in data scale, funneling millions of calls into retraining loops that lift accuracy. Even so, predictable subscription tiers and declining inference costs level the playing field, expanding SME participation in the overall voice assistant application market.

By End-Use Vertical: Healthcare Drives Growth Via Ambient Voice Assistants

IT and telecom led 2025 revenue with a 21.48% voice assistant application market share, using conversational bots for network troubleshooting and subscriber self-service. Healthcare, however, is forecast to deliver the fastest 17.06% CAGR to 2031 as ambient clinical documentation and patient-engagement bots offset physician shortages. Microsoft’s Nuance Dragon Ambient eXperience installed at more than 550 hospitals by 2025 and cut note-taking time 50%, freeing clinicians to see two to three extra patients daily. New reimbursement codes for remote monitoring via voice biomarkers give providers a clear economic rationale to deploy assistants.

Banking, financial services, and insurance rely on voice biometrics that reduce account-takeover losses by up to 40%, while retail and e-commerce experiment with conversational ordering, which boosts average basket values. Automotive OEMs ship assistants that act as proactive concierges, and media platforms report 18% higher consumption per session when users navigate by voice. Education pilots tutoring bots that respect accessibility rules, and factories integrate hands-free quality checks that keep operators’ eyes on the line. With physicians projected to be 86,000 short by 2036, ambient assistants will remain healthcare’s preferred automation lever, anchoring the segment’s leading contribution to future voice assistant application market size gains.

Geography Analysis

North America accounted for 36.65% of the 2025 revenue, giving the region the largest voice assistant application market share. With Amazon Alexa and Google Assistant installed in 40% of households, and Section 508 mandates spurring retrofits across federal contractors, the region's dominance is expected to continue. Venture capital remained plentiful as startups raised USD 2.3 billion in 2024, and anchor customers in financial services and healthcare funded early pilots that are now moving toward full-scale roll-outs. Yet, tier-1 use cases, such as customer service, are approaching saturation, so vendors are pivoting toward niche deployments, including legal transcription, real-estate showings, and field-service diagnostics. Canada mirrors the United States' trends, but growth now hinges on bilingual English-French assistants that comply with the Official Languages Act. Mexico is emerging as a near-shore development hub for North American enterprises seeking Spanish voice skills, leveraging its talent pool of more than 650,000 software engineers.

Europe held an estimated 28% share in 2025 as GDPR data-localization rules favored regional providers and the European Accessibility Act of June 2025 mandated voice-enabled e-commerce by 2028.[4]European Commission. “European Accessibility Act 2025.” europa.eu Germany’s automotive giants Volkswagen, BMW, and Mercedes-Benz embed assistants in connected-vehicle platforms, while the United Kingdom’s National Health Service tested ambient clinical assistants in 150 general-practitioner practices. France and Italy focus on smart-home assistants tuned for local dialects, and Spain’s banks deploy voice biometrics in mobile apps to curb fraud. South America is led by Brazil and Argentina, which use Portuguese and Spanish natural-language processing for government and banking, although currency volatility and patchy broadband keep growth in mid-single digits. Chile and Colombia are trialing Spanish code-switching assistants for customer service, aided by regional telecom investments in low-latency fiber routes.

Asia-Pacific is projected to post a 18.02% CAGR through 2031 and drive the largest incremental voice assistant application market size gain, propelled by China’s Baidu DuerOS, Alibaba Tmall Genie, and iFLYTEK Spark ecosystems, India’s 22-language Bhashini platform, and Southeast Asia’s mobile-first adoption curve. Baidu processed over 1 billion queries in 2024 after adding large-language-model capabilities. India’s open-source Bhashini gives 400 million lower-literacy citizens voice access to digital services, while Grab and Gojek weave ordering assistants into super-apps across Indonesia, Singapore, and Vietnam. Japan’s aging population favors elder-care robots powered by voice, with SoftBank’s Pepper deployed in more than 2,000 nursing homes, and South Korea’s Samsung Bixby plus LG ThinQ dominate appliance control. Middle East and Africa remain small today, yet Saudi Arabia’s USD 500 million Vision 2030 budget for voice-enabled citizen services and United Arab Emirates research grants for Arabic dialect models are accelerating double-digit adoption. South Africa pilots voice biometrics that cut call-center fraud 41%, and Nigeria’s mobile-money operators test assistants for low-literacy users, signaling untapped upside once infrastructure matures.

Regulatory Landscape

Voice assistant applications are increasingly shaped by requirements around AI transparency, biometric privacy, and sector-specific rules that affect where audio is processed and how users are informed about AI-driven interactions. In the European Union, the EU AI Act (Regulation (EU) 2024/1689) focuses on transparency disclosures and risk management for voice agents, with full application beginning on 2 August 2026 and Article 50 centered on transparency disclosures when users interact with AI systems.

In the United States, regulation remains fragmented across privacy and sector enforcement, while federal activity emphasizes security governance and benchmarking. In February 2026, the US Treasury Department issued an AI Risk Management Framework with extensive security controls aimed at banks and vendors, reinforcing compliance requirements for voice biometrics and recorded-call workflows in BFSI. South Korea also moved to a mandatory, risk-based posture when the AI Framework Act entered into force on 22 January 2026, adding an additional compliance layer for global voice assistant platforms operating across Asia.

Value Chain Analysis

The value chain for voice assistant applications spans (i) data capture and annotation (speech corpora, domain lexicons, and dialect datasets), (ii) model development and tooling (ASR, NLU/LLM dialog, and TTS), (iii) infrastructure and deployment (cloud, hybrid orchestration, and edge silicon), (iv) application-layer packaging (skills, enterprise workflows, and vertical templates), and (v) distribution channels through device ecosystems and enterprise platforms. Hyperscalers and OS providers anchor the chain by supplying foundational models, developer runtimes, and marketplaces, while enterprises increasingly procure integration and managed services to operationalize monitoring, retraining, and compliance.

Recent ecosystem moves point to stronger upstream-to-downstream integration and more partner-led hardware scaling. In May 2026, Google introduced the Gemini built in program with reference designs for third-party manufacturers to integrate Gemini voice AI into speakers, cameras, and other devices, expanding OEM distribution for voice capabilities beyond first-party hardware. On the embedded side, Cerence and Vivoka expanded their partnership in March 2026 to deliver multilingual embedded voice AI for industrial markets using Vivoka VDK 6, reinforcing how on-device performance, domain vocabulary, and reliability influence vendor selection. Large-scale deployments such as Omilia powering automated drive-thru ordering across 890+ US Taco Bell locations (July 2026) illustrate downstream rollouts where integrators, POS and workflow partners, and ongoing tuning services become central to maintaining accuracy and throughput across thousands of endpoints.

Competitive Landscape

The market is moderately fragmented, anchored by hyperscalers that bundle assistants into cloud and device ecosystems and flanked by vertical or regional specialists. Amazon, Google, Apple, and Microsoft leverage platform lock-in, while SoundHound, Voiceflow, and iFLYTEK win on automotive latency, enterprise orchestration, and Mandarin coverage, respectively. Generative AI has commoditized baseline accuracy, so vendors now compete on dialect breadth, sub-300-millisecond latency, edge-inference efficiency, and pre-built skills for vertical compliance. Qualcomm’s Snapdragon edge chips and Apple’s neural engine enable sub-2-watt on-device wake-word detection, positioning hardware to differentiate software ecosystems. OpenAI’s voice mode and Anthropic’s Claude voice push conversational depth into near-human territory, challenging traditional intent-classification stacks.

Strategic moves illustrate rising intensity. In October 2025 Microsoft closed its USD 19.7 billion Nuance healthcare deal to fuse Dragon Medical with Azure AI, aiming for end-to-end electronic health record flows. Amazon Web Services followed in September 2025 with Alexa for Healthcare, a HIPAA-compliant service that scored 95% terminology accuracy in blind tests. Samsung partnered with iFLYTEK in June 2025 to swap Bixby for Mandarin and Cantonese assistants on Galaxy phones sold in China, acknowledging that localized tuning beats generic models. Nuance filed a United States Patent and Trademark Office application in 2024 for a replay-attack detector that analyzes micro-resonance patterns, signaling a shift toward biometric liveness as a moat. The FIDO Alliance is drafting cross-vendor voice-biometric standards, but uptake is limited to tier-1 banks pending clarity on liability sharing.

Consolidation is likely around three tiers, hyperscalers offering horizontal platforms with ubiquitous language support, vertical specialists delivering compliance-ready skills for healthcare or automotive, and open-source coalitions such as Rasa and Mozilla Common Voice that commoditize data and models. White-space opportunities remain in code-switching scenarios such as Spanglish and Hinglish, and in high-noise industrial sites where error rates still exceed acceptable thresholds. Vendors that master edge-cloud orchestration while guaranteeing privacy and dialect parity will capture outsized share as enterprises prioritize latency, compliance, and total cost of ownership over raw word-error rate metrics.

Voice Assistant Application Industry Leaders

Google LLC (Alphabet Inc.)

Amazon Web Services, Inc.

Apple Inc.

Baidu Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven productization is creating concrete whitespace in enterprise voice workflows, especially where disclosure, consent, and auditability must be built into the interaction itself. The EU AI Act adds a direct requirement for voice-agent transparency beginning 2 August 2026 under Article 50, which supports demand for tooling that manages spoken disclosure prompts, interaction logs, and synthetic-voice marking across contact centers, healthcare intake, and public-sector service lines. Regulated-industry deployments also keep shifting toward hybrid architectures to keep sensitive audio local while using cloud models for complex intents, aligning with HIPAA and GDPR constraints referenced in the market context.

Real-world evidence also shows demand moving toward hybrid architectures alongside the emergence of advanced conversational models. In July 2026, OpenAI released full-duplex conversational models (GPT-Live-1 and GPT-Live-1 mini), while Apple broadened public testing of a redesigned, AI-powered Siri across multiple Apple form factors via an iOS 27 public beta, reinforcing voice as a core UI layer across devices and apps. These announcements support ongoing need for services that tune dialog flows, handle multilingual and code-switching behavior, and integrate voice agents into CRM, commerce, and field-service systems.

Recent Industry Developments

- July 2026: Omilia powers automated drive-thru ordering across 890+ US Taco Bell locations. Omilia's deployment expands automated ordering capabilities, enabling real-time interactions and higher throughput across fast-food kitchens and front-end workflows.

- January 2026: Apple and Google announced a multiyear agreement for Google to provide Gemini models and cloud technology to power AI features for Apple, including the overhauled Siri voice assistant. The arrangement signals deeper cross-platform reliance on third-party foundation models and requires enterprise governance for dialog intelligence sourced externally.

- February 2024: Hong Kong police documented a deep-fake audio job-interview scam, highlighting voice spoofing and identity-risk scenarios. The incident reinforces the need for liveness detection and stronger authentication in voice-driven workflows, particularly for BFSI and government use cases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers revenue earned from voice assistant applications that enable voice-driven interactions across consumer and enterprise use cases, including related application software and services delivered through common deployment models.

Scope exclusions: This sizing excludes core device hardware revenue (such as smart speakers and microphones) and counts only application layer spend tied to voice assistant use.

Segmentation Overview

- By Component

- Solutions

- Services

- By Technology

- Natural Language Processor (NLP)

- Speech Recognition

- Text-to-Speech Conversion

- Edge Computing

- By Deployment

- On- Premise

- Cloud

- Hybrid

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-Use Vertical

- IT and Telecom

- BFSI

- Healthcare

- Retail and E-commerce

- Automotive

- Media and Entertainment

- Education

- Manufacturing

- Government and Public Sector

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, build the initial demand indicators, and create sanity checks for regional splits. We leaned on public sources that explain how voice assistants are adopted and governed, such as US FCC materials on communications and devices, US NIST publications on AI and cybersecurity, OECD digital economy indicators, ITU ICT statistics, and WIPO patent databases for voice and speech related filings.

On top of these, we reviewed company annual reports, earnings call transcripts, product documentation, developer notes, and reputable press coverage to understand where monetization sits (subscription, usage based pricing, and enterprise licensing). For select steps, paid subscriptions for company financials and intelligence, news and financials, patent databases, and global contracts and tenders were used to speed up cross-checks on pricing signals and commercial activity. The sources listed here are illustrative, and many other public references were consulted to collect data, validate assumptions, and clarify unclear points.

Primary Interviews and Surveys

Primary work focused on validating what is actually purchased for voice assistant applications, and how pricing and deployment mix changes by industry. We spoke with a spread of solution owners, channel partners, systems integrators, and enterprise buyers so gaps from desk research could be filled, and assumptions could be confirmed with real buying patterns across major regions.

To reduce bias, we tested the same set of inputs with different respondent roles, then rechecked areas where responses varied, for example, cloud versus hybrid usage, and how often models are refreshed in production.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 12% | APAC: 45% |

| Mid tier: 51% | Functional/Unit leaders: 39% | EMEA: 31% |

| Smaller Players: 19% | Managers: 49% | Americas: 24% |

Market-Sizing & Forecasting

The sizing starts with a top-down build where digital adoption signals are translated into an addressable pool of voice-enabled use cases by region, and then converted into spend using observed deployment and pricing patterns. We then corroborate totals using selective bottom-up approximations, such as rolling up sampled supplier revenues, checking channel feedback on deal sizes, and validating typical price per deployment against usage intensity.

Key inputs used in the model include voice assistant penetration in customer service and contact center workflows, the share of enterprises using cloud, on-premise, or hybrid setups, average contract duration and renewal patterns, language coverage needs (single language versus multilingual), and the split between software subscriptions and services for integration and tuning. Where bottom-up signals are incomplete for smaller deployments, gaps are handled by applying validated adoption ratios to the wider enterprise base, and then adjusting with region-specific price and usage ranges.

For forecasting, scenario analysis is used so growth can flex with AI investment cycles and enterprise compliance needs, and then the midpoint path is selected after comparing expert expectations on adoption timing. The forecast is also checked against expected changes in unit economics, such as automation rates in support functions and the move toward on-device processing for latency and privacy.

Data Validation & Update Cycle

Outputs are validated through triangulation across multiple checkpoints, including consistency between adoption signals, pricing ranges, and observed commercial activity. When a variance appears, it is traced back to a specific assumption, for example deployment mix or service attach rate, and then rechecked through follow-up discussions and desk revalidation before the model is finalized.

A multi-step review is followed, where an analyst peer reviews calculations, inputs, and logic, and then a final pass is completed before sign-off. Reports are refreshed annually, and interim updates are made when material events occur that can shift demand or pricing. Before delivery, we do a fresh scan so clients receive the most current view available at that time.

Mordor Intelligence's Voice Assistant Application Market Estimate Compared With Other Published Estimates

Published market numbers for voice assistant applications often do not match, and the differences usually come from what is counted as revenue and how closely assumptions are checked with real buyers. The year chosen for the base, the handling of currency conversion, and the inclusion of adjacent categories can also widen the spread.

Device and platform layers are a common source of inflation, because some estimates blend application spend with smart speaker hardware, general speech recognition tools, or broader conversational AI suites. Smart speaker hardware revenue sits outside Mordor Intelligence's scope for this market, and totals are instead tied to application software and related services that are purchased to deploy voice assistant capabilities, which keeps the number aligned to a clearer spending pool.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.02 B (2026) | |

| Industry Report Publisher A | USD 5.16 B (2025) | Uses an earlier base year and a narrower interpretation of monetized voice assistant applications, which can undercount enterprise deployments that are bundled with broader software contracts. |

| Industry Report Publisher B | USD 3.90 B (2024) | Appears to anchor sizing on a smaller adoption pool and aggressive early-stage discounting, which can reduce the implied average spend per deployment in initial years. |

Across the three figures, the spread mainly reflects scope and year alignment, followed by how pricing is normalized across deployment models. When application-only revenue is separated from hardware and broader AI categories, and when adoption and pricing are checked with multiple buyer types, the estimate becomes easier to trace and repeat in future updates.

Key Questions Answered in the Report

How fast is the global voice assistant application market expected to grow through 2031?

Revenue is projected to rise from USD 9.02 billion in 2026 to USD 18.36 billion by 2031, reflecting a 15.27% compound annual growth rate.

What factors are driving enterprise adoption of voice assistants?

Falling inference costs, the push to automate contact centers, and growing smart-speaker penetration are accelerating deployment, while services revenue expands as firms outsource skill development.

Which geography is projected to see the highest growth for voice assistant applications?

Asia-Pacific is forecast to log a 18.02% CAGR through 2031, powered by China’s DuerOS ecosystem, India’s 22-language Bhashini platform, and Southeast Asia’s mobile-first users.

How are hybrid deployments addressing privacy regulations for voice assistants?

Organizations process wake-word detection and simple commands on-device while sending complex queries to the cloud, a split that satisfies HIPAA and GDPR data-residency rules and trims cloud fees up to 70%.

What is the current competitive landscape for voice assistant solutions?

The space is moderately concentrated (score 6) with hyperscalers like Amazon, Google, Apple, and Microsoft holding roughly 60% combined share, while specialists such as SoundHound and iFLYTEK compete on latency, dialect coverage, and vertical skills.

Which end-use vertical is forecast to expand the fastest for voice assistant applications?

Healthcare is set to grow at a 17.06% CAGR as ambient clinical documentation and patient-engagement assistants cut physician paperwork and unlock new reimbursement codes.

Page last updated on: